Quick Answer

International contractors can secure client-funded support without weakening contractor status if they structure it as documented business compensation, not employee-style benefits. Build a formal business setup, use clear contracts and invoice labels, keep business records and banking separate, and verify local classification and tax treatment before accepting stipends, reimbursements, retirement funding, wellness support, or direct plan enrollment.

As an independent professional, your most valuable asset is not your client list. It is your autonomy. That independence is fragile, and it is protected by deliberate business structure, not by hope. Build that structure to protect your autonomy, signal professionalism, and help you operate as a resilient Business-of-One.

This guide shows how to build that protection, from the legal and financial basics to a model you can sustain as the business grows.

The Foundation: Building Your Corporate Shield#

Before you negotiate any stipend or other benefits for international contractors, get your business structure in place. Clear separation between you and the work helps protect your autonomy and gives clients a cleaner business-to-business setup.

Step 1. Formalize the business#

Set up a formal business entity if you have not already. A practical check: can you present business registration details, invoicing details, and signing authority through the business rather than through your personal identity?

If you already work across borders, an Agent of Record can help with early-stage compliance, foreign payments, and global operations. As your volume grows and you need more control, move into your own full entity.

Step 2. Choose coverage by fit, not by label#

Insurance specifics vary by country, provider, and policy, so avoid one-size-fits-all assumptions. Use verifiable criteria for any option you consider: where it applies, what it excludes, and how claims are handled. Request the policy summary, exclusions, and claims path before you buy.

A common miss is buying coverage that sounds global but does not match your actual work pattern.

Step 3. Tighten contract terms around independence#

Your MSA should reflect independent contractor status, but the real protection is also in how the relationship runs. Keep boundaries clear around who sets deliverables and who controls day-to-day execution, and treat jurisdiction-specific legal details as local review items before you sign.

Review indemnity, IP, and confidentiality terms in plain language before signing. The goal is clear, project-aligned boundaries, not open-ended responsibility.

Step 4. Separate your banking#

Use a dedicated business account for invoices and client payments where practical. This keeps your records cleaner and easier to manage. A simple test helps here: could you hand an accountant a clean business ledger tomorrow without first separating personal spending?

Step 5. Execute this week#

Do not leave the setup half finished. You can lock in the basics this week:

| Task | Action | Key item |

|---|---|---|

| Business entity | Register or confirm your business entity details. | Entity details |

| Coverage | Collect policy summaries, exclusions, and claim steps. | Policy summaries, exclusions, and claim steps |

| MSA | Update your MSA so independence and responsibility boundaries are clear. | MSA |

| Business-only account | Open or switch to a business-only account for client money flows where practical. | Business-only account |

| Core records | Store your core records together. | Registration, policy documents, MSA template, and bank confirmation |

With that foundation in place, the next question is whether client-funded support helps you or starts to blur the contractor relationship. Related: How to Manage and Pay a Global Team of Contractors Compliantly.

The Critical Question: Do "Benefits" Put Your Contractor Status at Risk?#

They can in some fact patterns, especially when the arrangement starts to look more like employment than a business-to-business services relationship. In cross-border work, treat benefit requests as a compliance signal to review, not an automatic yes or no.

Classification rules vary by country, state, and engagement facts. Use a jurisdiction-specific review note, and verify current local criteria from official guidance, legal counsel, or HR source records before use. If you cannot clearly explain why the structure still supports independent-contractor status, pause and verify before agreeing.

Step 1. Check the classification lens before you ask#

Start with the jurisdictions tied to the engagement and verify current criteria before naming a structure. The question is simple: does the relationship still look like independent business services in both the documents and day-to-day operation?

In global contractor management, this is risk control, not paperwork for its own sake. Weak compliance can expose businesses to legal, financial, and reputational harm. The goal is to keep the terms clean and reviewable from the start.

Step 2. Ask for a documented structure, not assumptions#

When possible, ask for support as a clearly documented contract term rather than an informal benefit arrangement. That helps keep the contractor relationship reviewable as a business-services engagement.

| Request type | Classification signal | Admin burden | Documentation strength |

|---|---|---|---|

| Enrollment in client benefit plans | Fact-dependent; requires jurisdiction-specific review before agreeing | Varies by jurisdiction and plan setup | Depends on contract and operating records |

| Fixed stipend | Fact-dependent; verify local criteria before use | Varies | Depends on clear contract language and invoicing records |

| Reimbursement | Fact-dependent; verify local handling requirements | Varies | Depends on business-purpose records and consistent processing |

| Rate uplift | Fact-dependent; verify local criteria and contract framing | Varies | Depends on consistent service terms and invoicing |

If you need practical wording for proposals or SOWs, use language like this: "My pricing includes the operating costs required to deliver reliably, including insurance and business overhead."

If the client wants a separate line item: "We can discuss a contractor operations stipend in the SOW, subject to local classification review."

Step 3. Document the support like a business term#

Any separate support line item only helps if you handle it like business compensation. The paperwork, billing, and records all need to line up.

- Define the amount, frequency, and purpose in the contract.

- Invoice it as a business line item through your normal contractor billing flow.

- Verify tax treatment with qualified local advice before finalizing treatment.

- Keep records together: agreement, invoices, payment confirmations, and related business documents.

Step 4. Choose the cleanest structure for your facts#

There is no universal best structure across jurisdictions. Choose the option your local review can support, then keep contract terms and day-to-day administration aligned.

If a client proposes direct enrollment in employee benefits, stop there and ask for a classification review first. It is easier to resolve these questions before implementation than after the structure is already in use.

Once you know how to structure support without weakening your position, the next question is which costs are worth asking a client to help fund.

If you want a deeper dive, read What to Do If You've Been Misclassified as an Independent Contractor.

The Growth Engine: Funding Your R&D Budget#

Use development spend only when it clearly improves client delivery, and define that improvement before you ask for funding.

If you are a US-taxed business, do not assume every learning cost qualifies as research spending. Treatment under I.R.C. §§41, 174, and 174A is fact-specific, so verify current treatment before you classify costs as R&E.

Step 1. Define the bottleneck before you ask for money#

A vague learning request can sound like personal development. A request tied to a delivery bottleneck is easier to frame as an operating need. Start with the constraint, then explain the expected gain in quality or speed and how you will test the result after implementation.

Use a simple before-and-after statement:

- Current bottleneck: where work slows down or errors repeat.

- Expected gain: what you expect to improve in quality, speed, or consistency.

- Validation check: which delivery metrics you will compare over the next work cycles.

If you cannot show how you will validate the outcome, the request may sound like personal development instead of business support.

Step 2. Choose the spend type that matches the client outcome#

Pick the development category that maps directly to the work you already deliver.

| Development spend | Business use case | Expected payoff type | Risk if skipped |

|---|---|---|---|

| Formal training | Close a known gap in method, platform, or process | Potentially better execution quality; fewer avoidable errors | The same delivery problems may keep recurring |

| Certifications | Support client trust where current credentials influence selection | Potentially stronger credibility in evaluation or procurement discussions | You may lose work that requires current proof of competence |

| Peer groups | Get fast input on edge cases and decisions | Potentially faster problem resolution; better decision quality | You may spend too long troubleshooting alone |

| Conferences | Track changes in tools, standards, and buyer expectations | Earlier adaptation to shifts that affect delivery | Your approach may become outdated before you adjust |

| Tooling | Remove repeated manual work in active engagements | Potentially faster cycle time; more consistent output | Repetitive work may keep draining margin and time |

Your network matters most when you can apply it directly to live client work. That can mean faster debugging, better decisions on unusual requests, and steadier delivery when issues show up mid-project.

Step 3. Write the stipend terms like an operating clause#

Keep these terms narrow and commercial so the arrangement stays business-to-business. The more specific the category and records, the easier the spend is to justify and administer.

- Scope the category: training, certification maintenance, peer membership, conference access, or production-support tooling.

- Define eligible spend: what is included and what is excluded.

- Set documentation rules: required records, approval path for exceptions, and storage location.

- Tie spend to delivery: add a short note linking each expense to a client-facing improvement or risk reduction.

- Bill cleanly: if the client wants visibility, invoice through your normal contractor flow as a separate line item.

Step 4. Verify tax treatment and review the result#

Verify tax treatment before year-end, not after filing. As of July 4, 2025, domestic R&E expenditures may be immediately deducted under §174A. Foreign R&E expenditures under §174 must be capitalized and amortized over a 15-year period for taxable years beginning on or after January 1, 2022. Remaining unamortized domestic R&E costs may be deducted entirely in 2025 or over 2025 and 2026.

A common failure mode is labeling spend as "R&D" first and testing support later. Keep your contract file and business-purpose records organized. Then ask a qualified advisor whether your facts support treatment under §41, §174, or §174A for your entity and tax status.

Development spend matters, but it is only one part of keeping the business durable. You also need a plan for retirement, time off, and controlled personal support costs.

You might also find this useful: How to Handle Tax on Inheritance from a Foreign Person.

The Sustainability Protocol: Capitalizing Your Future#

Protect your delivery capacity the same way you protect margin: fund retirement, fund time off, and control wellness spend deliberately.

Start with one operating sheet for the next 12 months: trailing revenue, realistic billable capacity, and current retirement-plan status. You will use that sheet to set funding targets and verify execution each quarter.

Step 1. Choose the retirement setup that fits your cash flow and admin load#

Pick SEP when you want employer-only contributions with year-to-year flexibility. Pick a one-participant 401(k) when you want employee-and-employer contribution mechanics and can handle additional compliance steps as assets grow.

| Decision factor | SEP | One-participant 401(k) |

|---|---|---|

| Eligibility | A self-employed person or business of any size can establish it | Business owner with no employees, or owner plus spouse |

| Contribution flexibility | Employer-only contributions; current contribution cap pending official or benefits-advisor verification. | Employee and employer contributions; current contribution cap and catch-up treatment pending official IRS or benefits-advisor verification. |

| Admin burden | Can be established as late as the tax return due date, including extensions | File Form 5500-EZ when plan assets reach the $250,000 threshold |

| Usually the better fit | Variable cash flow and late-year contribution decisions | You want employee-and-employer contribution mechanics and can manage the reporting threshold |

Execution check: confirm plan documents are complete, contributions are posted to the intended tax year, and bookkeeping matches transfers.

Step 2. Fund paid time off through pricing, not hope#

PTO is not a perk in an independent business. It is a pricing and capacity decision. Federal baseline: the FLSA does not require paid vacation, sick leave, or holiday pay for time not worked. For you, PTO is a self-funded operating cost.

Use this workflow:

- Set target recovery time for the next 12 months, meaning real time off, not assumed downtime.

- Convert that into billable-capacity assumptions for the year.

- Recalculate pricing so income goals and overhead are covered inside that reduced capacity.

- Check quarterly: planned time off, booked work, and reserve balance should stay aligned.

If time off is scheduled but reserves are not funded, PTO is not actually capitalized.

Step 3. Treat wellness spend as a controlled business term#

Wellness support gets risky when it is vague. Keep it narrow, documented, and clearly commercial rather than open-ended or employee-like.

| Area | Requirement | Example / note |

|---|---|---|

| Covered spend categories | Define covered spend categories in your contract and internal policy, with preapproval rules and caps. | Contract and internal policy |

| Source records | Require source records and store them in your normal business recordkeeping system. | Invoices, receipts, and paid bills |

| Invoicing treatment | Keep invoicing treatment explicit. | Include it in base pricing or as a separate contractor invoice line item |

| Tax reporting treatment | Keep tax reporting treatment in normal contractor lanes where applicable. | Form 1099-NEC or Form 1042-S |

| Employee-style benefits | Do not let clients administer wellness amounts as employee-style benefits. | Do not assume wellness amounts are tax-free |

This helps keep the relationship in a business-to-business frame and aligns documentation with worker-classification factors: behavioral control, financial control, and relationship of the parties.

Quarterly sustainability checklist#

- Retirement: plan choice still fits your structure; contributions and books reconcile; current-year limits verified.

- PTO: pricing still reflects real billable capacity; reserve funding matches planned time off.

- Wellness: spend stays inside documented categories; records are complete and retrievable.

- Classification posture: contracts and invoices still present these as contractor compensation terms, not employee benefits.

After you set the model internally, the next job is getting it into the deal without weakening your contractor position.

For a step-by-step walkthrough, see How Independent Contractors Should Use Deel for International Payments, Records, and Compliance.

The Art of Negotiation: A 3-Step Framework to Secure Your Safety Net#

Treat this as a business-pricing conversation, not a personal exception request. Your goal is to set terms that protect continuity, reduce avoidable risk, and keep delivery quality stable inside a clear B2B relationship.

If you frame these asks as personal needs, clients hear optional spend. If you frame them as operating costs of a resilient Business-of-One, they can see the business case.

| Personal request framing | Business-case framing |

|---|---|

| "I need help with health insurance." | "My pricing includes continuity costs so I can stay fully operational during the engagement." |

| "Can you cover a stipend?" | "I can include a defined service-related allowance with clear documentation, not an employee perk." |

| "I need more money for liability coverage." | "Professional liability and E&O coverage reduce disruption and help me support the work responsibly." |

Step 1. Build your internal baseline#

Come into the call with numbers you can defend. Build one internal sheet with the business expense buckets you need to operate reliably over the next 12 months. Include international health coverage, Errors & Omissions insurance, and other documented service-continuity costs tied to your delivery. For each bucket, verify current category details against source records, contract terms, policy documents, or a qualified advisor before use.

Set a private operating floor, not a client-facing memo. Reconcile each line item to real records: policy invoices, reserve assumptions, and the separate business bank account you use to avoid co-mingling. If you cannot support a line with a bill, policy document, or reserve logic, tighten it before you negotiate.

Step 2. Translate each ask into a client outcome#

Map each ask to a client outcome: continuity, risk reduction, or delivery quality. Keep the language short and operational.

- Avoid this: "I need a higher rate because my insurance is expensive."

Say this instead: "My rate reflects the operating costs required for consistent delivery, including health and professional liability coverage."

- Avoid this: "Can you give me paid time off?"

Say this instead: "I price planned non-billable recovery time into service capacity so delivery stays predictable."

- Avoid this: "I want benefits."

Say this instead: "If you want continuity and fewer disruptions, the engagement needs to be priced to support the protections behind the work."

If a client offers employee-style benefits instead of discussing rate or stipend structure, pause and reset. Bring the conversation back to service pricing, defined contractor compensation terms, and clear documentation.

Step 3. Keep the paperwork telling one story#

Your proposal, contract, and invoice should tell one story: this is a business-to-business services relationship. Use commercial labels, not HR-style benefit labels. For example, use a professional services fee plus clearly defined service-related line items.

| Document | What it should show |

|---|---|

| Proposal | This is a business-to-business services relationship. |

| MSA | Explicitly confirm independent-contractor status and include Right to Control language: the client sets deliverables, and you control method, details, and means of performance. |

| Invoice | Use commercial labels, not HR-style benefit labels; use a professional services fee plus clearly defined service-related line items. |

| Payment trail | Do not let it conflict with contract terms and invoice wording. |

Keep your MSA and invoices aligned. Your MSA should explicitly confirm independent-contractor status and include Right to Control language: the client sets deliverables, and you control method, details, and means of performance. If your contract terms, invoice wording, and payment trail conflict, the file is harder to defend, and even baseless claims can still create major defense costs.

Execution checklist:

- Pre-call prep: update baseline sheet; gather policy and cost records; confirm MSA language for independent-contractor status and Right to Control.

- Call agenda: confirm scope; explain continuity and risk-reduction logic; present rate or stipend structure; reject employee-style benefit language.

- Post-call follow-up: send revised proposal or rate sheet, needed MSA redlines, and sample invoice line items that match the agreed B2B structure.

We covered this in detail in The Best Payroll Services for Small Agencies with US Contractors.

Before your next client renewal, run your baseline through the freelance rate calculator so your rate and stipend asks are grounded in actual operating costs.

Conclusion: You Are Not a Freelancer; You Are a Corporation#

Treat contractor support as a business cost, not an employee perk. Your status is strongest when the relationship stays contract-led and invoice-led, with the client buying outcomes while you control how the work gets done.

Health insurance can be framed as continuity planning. Paid time off can be framed as capacity planning. Stipends can be framed as service-reliability funding for tools, connectivity, and skills that support consistent execution.

In practice, price these items into your rate model. Write them into contract terms as contractor compensation, and reflect them in invoice structure and labels as business expenses. Keep the arrangement clearly client-vendor under a written contract, with you responsible for your own taxes, insurance, and operating costs.

Protect that boundary on every renewal. If a funding offer starts to look employee-style, pause and redline before you accept, then run local legal and tax review before final terms. Misclassification can lead to penalties, unpaid taxes, or lawsuits.

For your next renewal or proposal, use this checklist:

- Price insurance, time off, and operating stipends into your annual rate.

- Define funding terms in the contract as contractor compensation, not employee benefits.

- Use invoice labels that read as business charges tied to service delivery.

- Review any employee-style benefit language with local legal and tax advisors before signing.

This pairs well with our guide on A Guide to Using Wise for Payroll for International Contractors.

When you are ready to put this into a repeatable payment workflow, review Gruv Payouts for compliance-gated disbursements with status tracking and audit trail support.

Frequently Asked Questions

How do you get health insurance as an international contractor?

Get coverage you control. Recover the cost through your service fee or a defined contractor allowance so the relationship stays business-to-business. Before finalizing terms, make sure the arrangement is documented in your contract and invoices and run a local law check.

Are you eligible for retirement plans?

You may be, because independent contractors are typically self-employed. The right plan and any contribution limits depend on your tax profile and local rules, so confirm details with a qualified tax adviser. Keep records that support contributions and do not guess on limits or timing for cross-border income.

How do benefits affect your tax status as an international contractor?

The main risk is accepting arrangements that make you function like an employee while your contract and invoices say contractor. Keep a strong contractor agreement, clear invoice labels, payment records, and Form W-8BEN if you are a non-U.S. citizen working with a U.S. client. Because classification rules vary by country, run a local law check before accepting employee-style treatment.

How do you negotiate a remote work stipend?

Quantify the real operating cost, tie it to continuity, risk reduction, or delivery quality, and write it into your proposal and invoice as contractor compensation. Confirm currency, transfer method, and who absorbs fees before you finalize terms. Keep the wording commercial, not HR-style, such as Technology & Infrastructure Allowance.

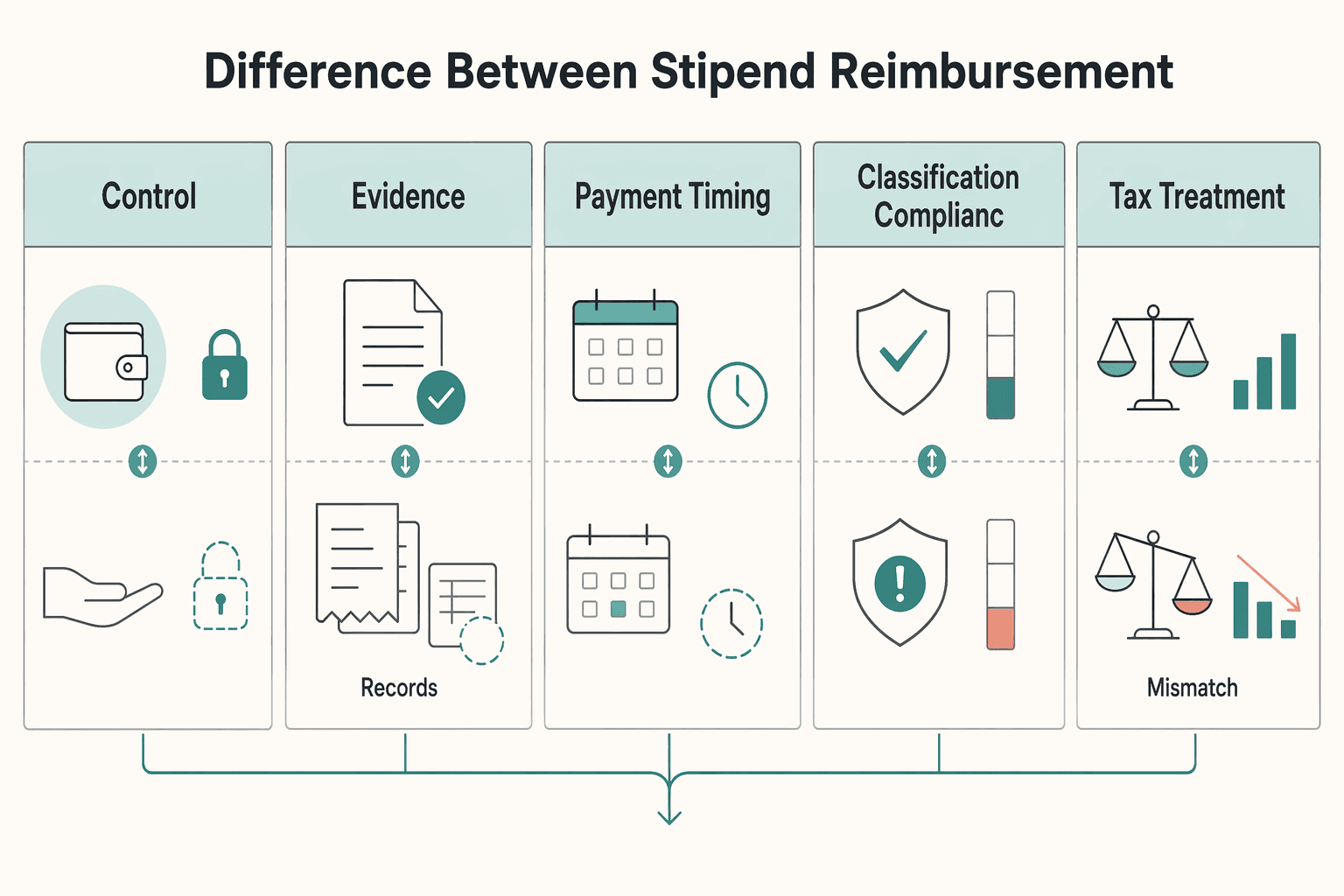

What is the difference between a stipend and a reimbursement?

A stipend gives you a defined amount for an agreed purpose, while a reimbursement repays a specific approved expense. Reimbursements often require receipt submission and client approval, while stipends can be lighter administratively if documented clearly. In either case, confirm jurisdiction-specific tax treatment before finalizing terms.

Should you ever accept being added to a client’s group health plan?

Use caution if the offer looks like employee enrollment, payroll-style deductions, or HR access as staff. Those features can increase misclassification risk in some jurisdictions. A safer option is to keep your own policy and handle support through your rate or a defined services-related allowance, then put that decision in writing and run a local law check before finalizing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/crs-product/R48307trusted

- dol.gov/general/topic/workhours/vacation_leavetrusted

- fema.gov/sites/default/files/2020-03/stafford-act_201...trusted

- irs.gov/retirement-plans/one-participant-401k-planstrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- occ.gov/news-issuances/news-releases/2023/nr-ia-2023...trusted

- ok.gov/dcs/solicit/app/viewAttachment.phptrusted

- pmc.ncbi.nlm.nih.gov/articles/PMC8919475trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

How to Pay International Contractors With Fewer Delays and Disputes

Paying international contractors reliably starts with compliance setup before the first invoice. Missed registration or filing steps turn routine payouts into delays and penalties.

Tax on Foreign Inheritance for U.S. Persons

Start by separating three decisions before you touch any forms: whether a foreign transfer is treated as a gift or bequest that is excluded from gross income, whether `Form 3520` reporting may apply, and when the facts are uncertain enough to require a qualified tax professional. The goal is documented judgment, not guesswork.