Quick Answer

To pay U.S. subcontractors from Canada, finish onboarding before the first payment, then use a fixed payment and reporting process. Collect the correct tax form, a signed agreement, and a written classification memo, choose currency and payout method in advance, and tie each contract, invoice, and transfer to one reference ID. If services are performed in Canada, assess Regulation 105 separately.

Engaging U.S. talent can be a strong growth move for a Canadian business. The challenge is making the cross-border mechanics feel routine on your side and invisible on theirs. If payments, compliance, and reporting are sloppy, you create financial risk, waste time, and look less credible to the people you want to keep. When they are handled well, your back office starts to work in your favor.

This guide lays out a three-step protocol for paying U.S. subcontractors. The goal is not just to stay compliant. It is to become the kind of client skilled contractors trust: clear on process, easy to work with, and reliable at every step.

Part 1: The Compliance Foundation - Your Shield Against Risk#

As a practical rule, do not send a first payment until your onboarding file is complete: correct tax form, signed agreement, and written classification memo. That packet supports how you classified the worker and how you handled payment and reporting if questions come up later.

Collect intake documents in order#

Open the file as soon as you decide someone will be paid as an independent contractor. For a U.S. person, that starts with Form W-9. Keep the signed W-9 in your records for 4 years. Fix missing or incorrect TIN details before payment, because backup withholding risk can be 24% on reportable nonemployee compensation. Assign an owner and checkpoint for each item:

| Item | Who | When | Storage / review |

|---|---|---|---|

| Signed W-9 | U.S. subcontractor | Before kickoff or first invoice | Vendor tax file with restricted access; finance checks completeness, signature, and date; keep in records for 4 years |

| Service-location declaration | Subcontractor | In onboarding, before contract signature | Stored with the tax file; finance or tax confirms whether services will be rendered in Canada |

| Signed contractor agreement | Both parties | Before work begins | Stored with tax and vendor records; approved by the hiring owner and contract reviewer |

| Year-end reporting flag | Created internally | After onboarding | Stored in AP or vendor tracking; finance reviews for Form 1099-NEC monitoring against the filing-year threshold you verify before filing |

If you collect those items in that order, most avoidable setup problems surface before money moves.

Use the right form for the right payee. A U.S. person gives you a W-9, not a W-8BEN. W-8BEN is for a foreign individual to provide to a withholding agent or payer, not to the IRS. Entities use W-8BEN-E.

| Form | Purpose | Who provides it | Trigger point | Downstream use | Common mistake |

|---|---|---|---|---|---|

| W-9 | Provides correct TIN for IRS information-return reporting | U.S. person contractor or payee | After contractor determination, before first payment | Supports payer records and IRS reporting workflows | Starting work without it, or accepting incomplete TIN data |

| W-8BEN | Certifies foreign individual status for U.S. withholding and reporting contexts | Foreign individual, not U.S. person | When requested by the withholding agent or payer | Supports withholding-agent or payer documentation; generally valid through the last day of the third succeeding calendar year unless circumstances change | Requesting it from a U.S. contractor, or using it for an entity |

If services are rendered in Canada, assess Regulation 105 during onboarding, not after invoices arrive. Withholding can be 15% of gross. Remittance is due by the 15th of the following month, and reporting is on T4A-NR due by the last day of February following the payment year. Without CRA written notification, required withholding remains mandatory.

Lock risk controls into the agreement#

Your agreement should reduce ambiguity, not just label the worker a contractor. Contract wording alone does not determine status, so treat the agreement as one piece of a broader classification record.

Include clauses that map to actual operating risk. Common areas to cover include contractor status, defined scope and deliverables, payment terms including currency, invoicing cadence, fee allocation, IP terms, tax responsibility, and dispute handling. Where legal specifics vary, flag clauses for counsel review, such as governing law or forum and IP assignment wording.

Before approval, run a consistency check across the agreement, onboarding form, and payment setup. They should all tell the same story. If the contract says project-based work but the day-to-day setup looks like ongoing employee-style control, treat that as a classification warning and resolve it before work expands.

Document classification with evidence#

The classification memo is where you turn judgment into something you can defend. Keep it to one page, but make it specific. Use the IRS common-law categories: behavioral control, financial control, and relationship of the parties. There is no fixed score, so record facts and supporting evidence instead of trying to force a points formula. Use an evidence log like this:

- Behavioral control: who sets method, schedule, tools, and work location; attach SOW terms and communications showing control boundaries.

- Financial control: who bears business costs or risk, invoices for work, and serves other clients; attach invoices and other business evidence.

- Relationship factors: whether the engagement is project-based or open-ended, and whether employee-type benefits exist; attach contract term and renewal details.

Close each memo with two lines: Decision and Review trigger. Good review triggers include scope becoming indefinite, growing control over hours or methods, or reduced outside-client activity. Include a reporting reminder line as well: 1099-NEC threshold for this filing year: pending official IRS or tax-advisor verification before filing.

With the file built correctly, you can move into payments without turning compliance into a cleanup project later. Related: What to Do If You've Been Misclassified as an Independent Contractor. Before you send the first payment for a foreign contractor, standardize W-8 tax intake with this W-8 form generator so your records are consistent from day one.

Part 2: The Seamless Payment Workflow - Professionalism in Every Transaction#

If you want fewer avoidable issues when paying cross-border subcontractors, treat payment as a fixed invoice-to-payout process. Contractors invoice first. You then pay through the method and schedule already set in the agreement and vendor file.

Choose your default rail before the first invoice#

Pick your default method up front based on legal context, fee impact, and contractor preference. Then confirm what the provider actually supports before you standardize around it.

| Option | Fee transparency | FX handling | Payout speed reliability | Dispute or hold risk | Accounting export quality |

|---|---|---|---|---|---|

| Business bank wire | Confirm how bank and intermediary fees are disclosed | Confirm who sets FX and what FX details are retained in records | Confirm expected timing and cutoff dependencies | Confirm return/repair workflow for exceptions | Confirm export fields needed for invoice-level reconciliation |

| Modern payout platform | Confirm in-platform fee visibility, pricing, and corridor coverage | Confirm rate/fee display and retained FX fields | Confirm expected timing and recipient setup requirements | Confirm review, return, and exception workflow | Confirm transfer exports include invoice and reference fields |

In practice, do not wait until the first invoice to decide how money will move. That is when fee surprises and payout delays usually show up.

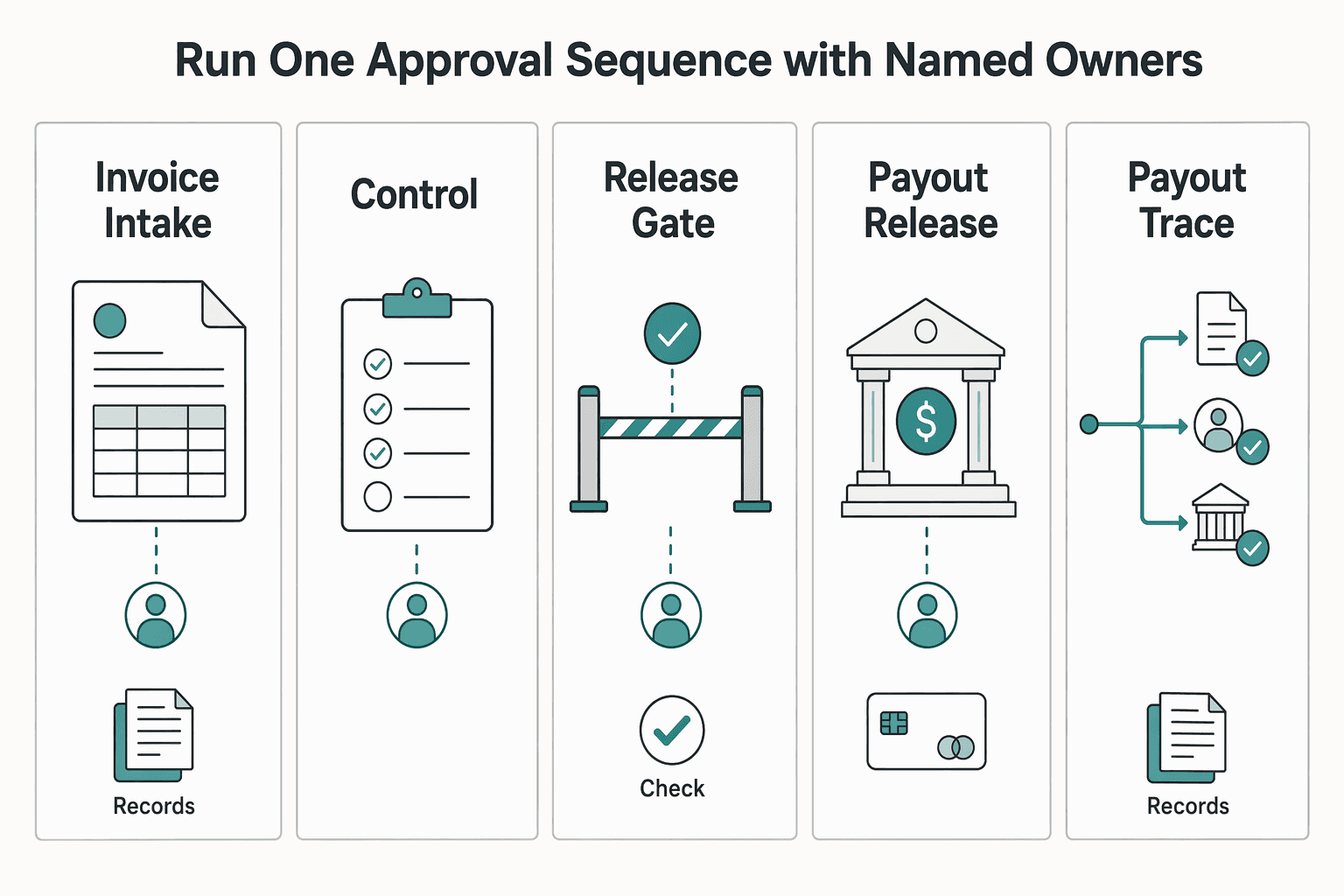

Run one approval sequence with named owners#

A clean payment process separates work acceptance from payout release. That keeps the file auditable and reduces the chance that an invoice gets paid because everyone assumed someone else checked it. Use one sequence every time:

| Step | Owner | Action |

|---|---|---|

| Invoice intake | AP owner | Receive invoices in one AP inbox or portal, not across scattered email threads |

| File validation | AP + finance control | Confirm the invoice matches the contractor file and agreed terms before approval |

| Work approval | Hiring owner or project lead | Confirm deliverables were accepted before money is released |

| Payout release | Finance owner | Pay using the agreed method and schedule, and pay by the due date in that agreed process |

| Reconciliation | Finance or AP | Match invoice, transfer record, and ledger entry on a fixed cadence |

If one person performs more than one role on a small team, keep the steps distinct anyway. The control comes from the sequence and the record, not just the org chart.

Make the audit trail operational with one reference ID#

If your team cannot trace a payment quickly, the process is weaker than it should be. The simplest fix is to require every payout to map to the same three records: contract, invoice, and transfer confirmation.

Use one internal reference ID, such as IC-US-2026-0041, across approval notes, invoice records, and payout instructions so anyone can follow the transaction without reconstructing it from email history.

For rejected or returned payments, keep the original record, log the reason, and reissue under the same base ID with a clear suffix, such as -R1. Do not accept payout-detail changes from invoice free text alone. Route them through your vendor-update control before release.

Set a one-page default policy#

Once the payment path is set, write down the operating defaults. Use a one-page policy that answers the same questions every time:

- Currency: set the default currency in the policy; if conversion applies, record who absorbs conversion cost.

- Payout method: name the approved bank wire or payout platform; exceptions require approval from the role listed in the policy.

- Remittance details: collect via vendor setup, not ad hoc invoice notes.

- Reference standard: every payout includes contractor file link, invoice number, and internal reference ID.

- Reconciliation cadence: choose weekly, twice-monthly, or monthly reconciliation, with exception cleanup before close.

- Provider capability verification: confirm pricing visibility, FX record fields, returned-payment notifications, approval permissions, and export fields.

That is how the process becomes repeatable instead of personality-driven. If you want a deeper dive, read Separating Business and Personal Finances: An Important Step for LLCs.

Part 3: The Audit-Proof Reporting Loop - Closing the Year with Confidence#

Year-end goes more smoothly when the reporting path is decided early, the filing data comes from fixed records, and your evidence file is complete before anyone starts pulling totals. If you leave those steps until close, small setup mistakes turn into filing problems.

Verify the reporting path before you total payments#

Classify first, then total payments.

- If the payee is a U.S. person and the payment is reportable nonemployee compensation for your trade or business, use Form 1099-NEC.

- If the payee is a nonresident alien, report nonemployee compensation on Form 1042-S and not 1099-NEC.

- If payment was made by card or third-party network, those transactions are generally reported on 1099-K, not again on 1099-NEC.

Keep U.S. and Canadian obligations on separate tracks. Your IRS information-return duty is one track. Canadian Regulation 105 is a different track that applies only when you pay a non-resident of Canada for services provided in Canada. In that case, withholding is mandatory unless you have written CRA notification. Withholding is 15% of the gross amount paid. Remittance is due by the 15th of the following month, and reporting goes on T4A-NR by the last day of February following the payment year.

Build each filing from fixed source records#

Do not build year-end filings from memory, inbox searches, or invoice notes. Create one close sheet per contractor and populate it from fixed sources only.

- Furnish the recipient copy.

Use Form W-9 data on file for legal name, address, and TIN. Current recipient-copy furnishing deadline pending official IRS or tax-advisor verification before use. IRS guidance points to January 31 for furnishing the recipient copy, but filing rules can change after instructions are published.

- File with the IRS.

Use the same verified identity data. Then pull the annual paid amount from your payment ledger and confirm it against transfer evidence. Current Form 1099-NEC reporting threshold and IRS filing deadline pending official IRS or tax-advisor verification before use. If you paper file 1099-NEC, include Form 1096. If you have 10 or more information returns in aggregate, file electronically.

- Remove non-NEC transactions before filing.

Exclude card and third-party network transactions from 1099-NEC totals to avoid duplicate reporting.

| Filing input | Required | What it feeds | Source checkpoint |

|---|---|---|---|

| Form W-9 on file | Yes (1099-NEC path) | Legal name, address, TIN | Match W-9 to vendor master record |

| Contractor identity record and agreement | Yes | Payee classification support | Confirm U.S. person vs other status is documented |

| Calendar-year payment totals | Yes | Reportable amount | Reconcile AP ledger to paid transactions, not invoices alone |

| Payment evidence | Yes | Proof of amount paid | Match bank or platform confirmation to each invoice or reference ID |

| Recipient delivery confirmation | Yes | Proof form was furnished | Save mail log, portal receipt, or email delivery record |

| CRA written notification / T4A-NR file | Conditional | Canada withholding file | Keep only when services were provided in Canada |

Lock records into a repeatable close file#

A defensible filing is really a recordkeeping job. The easier it is to trace each payment, the easier year-end becomes. Use one folder structure for every contractor:

| Folder | Included records |

|---|---|

| 01_Onboarding | agreement, W-9, classification notes |

| 02_Invoices | all invoices in date order |

| 03_Payments | bank or platform confirmations |

| 04_Year_End_Reporting | drafts, filed copies, Form 1096 if used, delivery proof |

| 05_Exceptions | returns, corrected forms, issue notes |

Use one naming rule: YYYY-MM-DD_DocType_ContractorName_RefID. Before filing, confirm one number ties across all three sources: invoice register, paid transaction export, and filed form amount. If it does not tie, stop and resolve the mismatch first.

Run an audit-response routine and set retention policy#

The best audit response is a file you can hand over without rebuilding it. Run reconciliations monthly, then run a final close reconciliation in January. Check whether W-9 details still match current name and TIN records, duplicate-reporting risk from card payments, and any services-in-Canada cases that belong in a separate CRA file.

Set retention policy text now, but leave the exact period unresolved until legal or tax review confirms the applicable U.S. and Canadian requirements. Do not hardcode one universal retention period.

For a step-by-step walkthrough, see How to Pay US-Based Contractors from Australia.

From Transactional to Transformational: Becoming a Premier Client#

Once compliance, payment, and reporting are connected, the contractor experience improves too. That is the real advantage. In cross-border work, the complexity usually sits with regulations, providers, and payment relationships across countries. Your process should absorb that complexity instead of pushing it back onto the contractor.

Set a practical operating standard#

The useful distinction is not small versus large client. It is vague versus dependable. A simple test is whether you can answer what was sent, when, in what currency, and under which reference from one folder or screen.

| Daily behavior | Transactional client | Premier client |

|---|---|---|

| Onboarding clarity | Requests details in fragments | Collects agreement, tax forms, and payout details in one intake pass |

| Payment currency choice | Defaults without discussion | States currency options early and confirms the contractor's choice in writing |

| Payout reliability | Pays when convenient | Pays on the agreed schedule and keeps one reference ID per transfer |

| Remittance communication | Sends "paid" with no detail | Shares amount, currency, send date, and transfer reference |

| Year-end follow-through | Rebuilds records at close | Uses verified records and delivers year-end documents when required from the reporting file |

Apply one client experience checklist on every engagement#

A good contractor experience usually comes from consistency, not extras. Use the same operating checklist on every engagement so people know what to expect.

- Acknowledge new contractor intake within your verified internal SLA.

- Name the payment support owner and the escalation path, for example AP first, then finance lead.

- Share payment status at each handoff: approved, scheduled, sent, or exception.

- Keep one evidence pack per contractor: agreement, tax form, invoice, and transfer proof.

- Pilot any new provider with a low-risk payout first, and treat vendor marketing as a lead, not proof.

Run intake, payout, and reporting as one routine#

The process works best when onboarding, payment, and year-end are treated as one connected routine instead of three separate jobs. Run it as one routine:

- Intake: collect signed onboarding documents, store identity records consistently, and record currency preference.

- Payout: pay on the promised cadence, send remittance details, and save transfer confirmations.

- Reporting: close from verified records only and keep delivery proof for year-end documents when applicable.

Track relationship signals without forcing hard numbers: repeat-engagement willingness, priority access to preferred contractors, and fewer payment-status disputes. If those signals are weak, tighten the routine before adding new tools.

You might also find this useful: How to Fill Out Form W-8BEN for a Foreign Freelancer.

If you want to operationalize this process across contractors, review Gruv Payouts for compliance-gated payout flows, status visibility, and audit-ready tracking where supported.

Frequently Asked Questions

What do you collect before first payment?

Before first payment, finish the onboarding file with the correct tax form, signed agreement, and written classification memo. For a U.S. subcontractor, that means collecting a signed Form W-9 and keeping it in your files for four years. If a U.S. person sends Form W-8BEN, pause setup and request a W-9 instead.

What do you file at year-end?

File Form 1099-NEC only if the payments are reportable nonemployee compensation for your trade or business. If the payee is a nonresident alien, use Form 1042-S instead, and exclude card or third-party network payments that are generally reported on 1099-K. Verify the threshold for the specific tax year before hardcoding it, furnish the recipient copy and file by January 31 if required, use Form 1096 for paper filing, and e-file if you have 10 or more information returns in aggregate.

What do you withhold?

Do not assume withholding is always zero. For a U.S. payee, backup withholding can apply at 24% when TIN requirements are not met for reportable nonemployee compensation. For a non-resident performing services in Canada, Regulation 105 can require 15% withholding and may also require a T4A-NR.

What do you pay in, and which rail do you use?

Pay in the currency you and the contractor agree to in writing, and state who covers FX in the contract or invoice. Choose the rail before the first invoice by comparing fee visibility, FX handling, speed, traceability, and reconciliation impact, then confirm what the provider actually supports. If you pay by card or certain third-party networks, document that with the invoice because reporting may shift to Form 1099-K.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

How to Fill Out Form W-8BEN for a Foreign Freelancer

For many global professionals, Form W-8BEN is the first real point of friction in a U.S. client relationship. It often gets treated like routine paperwork. That is the wrong frame. If you run a business of one, this form is an early operating decision that affects cash flow, onboarding speed, and how much confidence a client has in your setup.