Quick Answer

Handle these payments by separating FATF jurisdiction risk from actual sanctions-list obligations. Use FATF status to set review depth, then screen parties and transactions against applicable official lists at onboarding, payout creation, and release. If there is no unresolved listed-party match, apply heightened review rather than automatic rejection. If a possible match remains unresolved, hold and escalate before release.

What changes when you pay high-risk countries#

Do not treat jurisdiction risk and sanctions obligations as the same decision. That is the simplest way to reduce real sanctions risk without choking off legitimate cross-border payouts.

If you own compliance, legal, finance, or risk at a payment platform, this guide gives you a simple operating model. Separate country-level risk signals from transaction-level legal obligations, then route cases through clear escalation points and evidence standards. Done well, you tighten review where risk is real and avoid blanket holds where the facts do not support them.

The distinction matters because the signals come from different sources and mean different things. FATF high-risk jurisdictions reflect strategic AML/CFT/proliferation financing deficiencies at the jurisdiction level. As of 13 February 2026, FATF's "High-Risk Jurisdictions subject to a Call for Action" calls for enhanced due diligence for all countries it identifies as high risk. In some cases, it also calls for stronger measures. By contrast, jurisdictions under increased monitoring still matter for risk, but FATF explicitly says its standards do not envisage blanket de-risking and do not call for enhanced due diligence measures for those jurisdictions as a category.

Sanctions obligations work differently. Sanctions screening is a control to detect, prevent, and manage sanctions risk, and transaction screening focuses on transactions involving targeted individuals or entities. The legal trigger is a listed name and the specific measures attached to that designation, not simply that a payment touches a higher-risk jurisdiction. The UN Security Council Consolidated List reflects that structure by linking obligations to listed individuals and entities and the measures for each listed name.

In practice, if a payout involves a FATF-flagged corridor but no actual list match, use heightened review rather than automatic rejection. If a possible match to a listed person or entity remains unresolved, escalate before release.

Before you start#

Use this guide as an operating model, not legal advice. Regulatory guidance makes that boundary explicit. If you are unsure about obligations in a specific case, obtain independent legal advice. This matters most when obligations are unclear, facts are incomplete, or jurisdictional rules may conflict.

Before relying on any screening outcome, verify two basics:

- Source and recency of lists: The UN Security Council Consolidated List was last updated on 30 March 2026. Search tools can have narrower coverage or stale data. For example, OFSI's legacy search notes it only searches designations made up to 28 January 2026.

- Whether a "no hit" is still supported by due diligence: A search result alone is not a substitute for appropriate due diligence, documented review, and clear escalation logic. Search tools themselves state that using the search function does not remove due diligence obligations.

A common failure mode is collapsing everything into one blunt rule, such as "high-risk country equals prohibited payment." That can create avoidable payout friction and weak case notes when an auditor asks why a payment was stopped or released. The sections that follow are built to prevent that outcome. Triage the jurisdiction signal, screen parties and the transaction, then apply go, hold, escalate, or reject decisions your operators can defend.

Define what high-risk country payments actually mean in operations#

A high-risk country is a risk indicator, not a legal conclusion. In practice, each payment needs two separate answers: does the corridor raise AML/CFT risk under FATF publications, and does the payment involve a listed person or entity under an applicable sanctions regime?

Label the jurisdiction signal precisely#

FATF's High-Risk Jurisdictions subject to a Call for Action means significant strategic AML/CFT deficiencies and calls for enhanced due diligence, and in the most serious cases, counter-measures. That is not the same as jurisdictions under increased monitoring, where countries have committed to remediation and FATF does not call for enhanced due diligence as a category.

Record the exact FATF publication and date in your note, for example 13 February 2026 for Call for Action or 13 June 2025 for Increased Monitoring. Notes like "grey list country" or "blacklisted country" are too vague for an audit-ready decision.

Check for an actual listed-party prohibition#

In UN, EU, and U.S. listed-party regimes, legal exposure is tied to a match to a listed name and the measure attached to that listing, not to FATF jurisdiction risk by itself. The UN Security Council Consolidated List, last updated 30 March 2026, is structured around listed individuals and entities, with measures tied to each listed name. Similar listed-party logic appears in EU and U.S. regimes.

Do not call a case a "sanctions hit" when the issue is only country risk. If there is no unresolved listed-party match, do not describe the payment as prohibited on that basis alone.

Standardize case language for defensible handoffs#

Standardize case language so handoffs stay defensible. At minimum, each review should clearly state:

- Risk indicator: FATF status, corridor concern, or other jurisdiction signal

- Screening result: no hit, possible match, or confirmed match against official sanctions lists

- Decision owner: who can release, hold, or escalate under your internal policy

- Escalation points: when ambiguity moves from operations to compliance or legal

Use one operating rule throughout: FATF status changes the review lane, while a listed-party match changes the legal decision. If either the FATF classification or a list match is unclear, hold release and escalate with the source record, search result, and analyst rationale.

For a step-by-step walkthrough, see How Availability Heuristic Distorts Risk Assessment for Freelancers.

Set ownership and escalation points before you process payouts#

Once you separate FATF jurisdiction risk from an actual list match, assign decision ownership before funds move. We recommend a simple split: payments ops place immediate holds, compliance confirms or clears matches, legal decides when prohibition is still unclear, and finance owns fund movement and reporting duties tied to that movement. Adjust this split to your jurisdictions and business model.

Assign day-to-day screening ownership#

Assign a named day-to-day owner for sanctions screening on cross-border payments. FFIEC guidance recommends designated day-to-day OFAC compliance ownership for banks. You can use that as an operating model even if your platform is not a bank.

Document this in policy, not just practice: who can stop a payout, who can release after review, who can reject, and who reports material issues to senior management. Name a deputy for absences.

Set hold, release, and rejection authority before the first alert#

Let payments ops place immediate holds at onboarding or pre-release when a possible match appears, but do not let ops reject a case unilaterally on weak name data or incomplete identity data.

Compliance should clear false positives or confirm no listed party after documented review. Escalate to legal when a possible sanctioned individual or entity is involved and legal effect is still unresolved. Assign finance explicitly when your team is the holder, transferrer, or releaser of funds, since OFAC assigns primary reporting responsibility to that actor.

Where a U.S. nexus exists, under OFAC rules blocked property has a 10-business-day initial reporting deadline, and rejected transactions are also reportable. Avoid split-accountability failures by naming the reporting owner in advance.

Map escalation to payment stage#

Map escalation to payment stage instead of routing everything into one queue:

- Onboarding: escalate identity gaps, alias concerns, and country-risk cases needing enhanced due diligence before activation.

- Payout release: escalate unresolved list ambiguity, changed party data, or corridor changes discovered at release.

- Post-event review: define who collects the record, who assesses follow-on action, and who decides whether external reporting is required.

Run a short tabletop test with one case per stage. If any stage lacks a named owner, the process is not operational yet.

Create an urgent lane for call-for-action cases#

Create an urgent lane for cases involving High-Risk Jurisdictions subject to a Call for Action when list-screening ambiguity remains unresolved. FATF calls for enhanced due diligence in this category and, in serious cases, counter-measures. It does not, by itself, make all payments legally prohibited.

As of 13 February 2026, this FATF publication listed the Democratic People's Republic of Korea, Iran, and Myanmar. For these cases, bypass normal queue order: ops holds immediately, compliance reviews source records and screening evidence, legal decides block versus reject under the applicable regime, and finance prepares required reporting steps.

Prepare the minimum data and evidence pack before screening starts#

Do not start screening with partial data. In practice, incomplete inputs create alerts that are harder to resolve and decisions that are harder to defend.

Once ownership is clear, enforce intake discipline. You should be able to show what data was screened, which official sanctions lists were checked, what Enhanced Due Diligence (EDD) material was reviewed, and why the payment was cleared, held, escalated, or rejected.

Collect the minimum fields before a case enters screening#

Set a hard intake gate for the fields needed for sanctions checks and later transaction monitoring. If required data is missing, pause the case before screening.

| Input | What to capture | Why it matters |

|---|---|---|

| Party identity data | Full legal name and address, and for higher-value cross-border peer-to-peer payments above USD/EUR 1,000, standardized identity fields such as date of birth where applicable | Richer identity fields support more reliable match review and disposition |

| Payment data | Amount, execution date, and payment instructions | These are core transmittal-order records and tie the decision to a specific transaction |

| Corridor data | Origin country, destination country, recipient institution identity, and recipient identifiers | Geographic location is a stated risk input, including FATF high-risk jurisdictions subject to a Call for Action |

| Case context | Payment purpose and relevant internal case context, for example prior internal cases or transaction monitoring alerts, when available under policy | Practical review input for pattern detection, even if not an explicit cited legal minimum field |

For U.S.-nexus operations, 31 CFR 1010.410 still matters in design: nonbank financial institution transmittal recordkeeping starts at $3,000, and some transfer-related records are triggered above $10,000.

Build one evidence pack that links decisions to checks performed#

Your evidence pack should function as a defensible case file. At minimum, store submitted payment data, screened identifiers, screening date and time, official sanctions lists used, alert output, analyst notes, escalation notes, and final disposition with owner and timestamp.

For U.S.-linked cases, tie checks to OFAC-administered lists, including the SDN List and relevant OFAC consolidated non-SDN data. Where AML/CFT risk drives heightened review, keep EDD artifacts in the same case file as the sanctions decision record.

Avoid the standard documentation failure: "false positive, cleared" with no reasoning. Record which identifiers broke the match and whether escalation was required under policy.

Set retention to a sanctions-ready standard#

Set retention so records remain audit-ready under the rules you may be examined against. OFAC's 2025 final rule extended certain recordkeeping requirements from five years to 10 years, effective March 21, 2025. Current OFAC regulations also require covered transaction records to be available for examination for at least 10 years.

Because some FFIEC material still references five years, do not rely on older references alone. For OFAC-covered activity, set sanctions screening and investigation records to a 10-year standard, then confirm whether separate local AML/CFT rules require longer.

For more on country risk signals and FATF list monitoring, see Handling the FATF Blacklist and Greylist as a Freelancer.

Run jurisdiction triage with FATF signals before transaction-level screening#

Treat jurisdiction triage as a routing control, not a sanctions decision. Its job is to set review depth before transaction-level screening so you can tighten controls where needed without defaulting to blanket blocking.

Build a jurisdiction triage table#

Create a table for every country you pay into or out of. For each jurisdiction, record the current FATF category, whether Call for Action or Increased Monitoring, the source date, reviewer, and a short corridor-risk note relevant to your business.

The ICRG context helps you interpret jurisdiction risk, but it is not a sanctions-list hit on its own. Keep that distinction explicit before party and transaction checks against official designation sources, for example EU official texts and the UK Sanctions List.

A reliable table should let you confirm the exact FATF category and how current it is in seconds. If labels are stale or unclear, triage is not dependable enough for payment decisions.

Assign standard, heightened, and restricted lanes#

Map each corridor to an internal lane that defines review depth, approvals, and expected payout friction.

| Lane | Typical trigger | Documentation depth | Approval level | Payout timing impact |

|---|---|---|---|---|

| Standard | No FATF concern and low internal corridor risk | Baseline records required by policy | Baseline review under policy | Normal path if list checks are clear |

| Heightened | Increased Monitoring context or elevated corridor or case risk without a direct sanctions match | Additional case documentation as required by policy | Escalated compliance review under policy | Possible pause for additional review |

| Restricted | Call for Action context or severe combined risk signals | Enhanced case file and escalation record as required by policy | Senior compliance or legal review under policy | Outcome and timing depend on sanctions-screening results and policy |

If jurisdiction risk rises but there is no direct sanctions hit, route the case to heightened review and documented risk management rather than blanket blocking. That fits the FATF risk-based approach and FATF's position against de-risking whole customer groups.

Keep the two FATF buckets separate in daily operations. FATF does not call for the application of enhanced due diligence measures to jurisdictions under Increased Monitoring. Call for Action can call for enhanced due diligence and, in serious cases, counter-measures.

Write the rule that keeps triage separate from sanctions screening#

Put the rule plainly into policy: triage sets review intensity, while sanctions screening determines whether a payment can proceed, be held, or be rejected.

This prevents a recurring error: treating a high-risk jurisdiction label as an automatic legal prohibition. Where no applicable sanctions-list match exists, handle the case through documented risk management and escalation under your approval matrix.

Document what your policy requires for a defensible heightened-lane decision, and require analyst notes that explain why the jurisdiction signal changed, or did not change, the disposition.

Refresh the table on FATF publication dates and evaluation developments#

Refresh triage on FATF publication cadence, three times a year, and keep a standing checkpoint for mutual evaluation outputs and FSRB developments.

That checkpoint matters because the FATF Global Network began a new evaluation round in 2024, and mutual evaluations cover both effectiveness and technical compliance. Even without an immediate list-category change, new evaluation context can justify lane or escalation updates.

After each FATF update cycle, verify three things: the table is refreshed, lane changes are version-controlled, and reviewers are told what changed. For a related screening walkthrough, see OFAC Sanctions Screening for Global Businesses.

Run party and transaction screening at the right control points#

Once jurisdiction triage sets the lane, make sanctions decisions through event-based screening at control points where risk can change. Use both customer and name screening and transaction screening, and tie each result to the exact data screened.

| Control point | What to screen | Verification before moving on |

|---|---|---|

| Payee onboarding | Payee identity data and known counterparties | Result is linked to the final onboarding record and input snapshot |

| Payout creation | Payer and payee identities plus transaction attributes in the instruction | Screen ran on the actual payout data, including post-onboarding edits |

| Payout release | Current party and transaction data when anything material changed or prior results are stale | Latest successful screen is newer than the last material edit and latest list ingestion |

| Post-release alerts | New list updates, corrected identity data, monitoring or investigation alerts | Decision recorded on whether to review only the new event or run lookback |

Screen names at onboarding#

Run customer and name screening when a payee is created or approved, and re-screen when key identity fields change. Onboarding is the first checkpoint, not a one-time pass.

Your case record should show exactly what fields were screened and when. If you cannot reconstruct the screened inputs, the decision will be difficult to defend later.

Screen the payout at creation#

Run transaction screening when the payout instruction is built, not only at onboarding. Include the identities and transaction attributes that can change risk at payment time.

Use official lists based on your legal exposure and corridors. For UK exposure, UK sanctions designations are now only on the UK Sanctions List (UKSL) from 28 January 2026. If UN measures are in scope, use the UN Security Council Consolidated List.

Re-screen before release and apply a clear disposition rule#

Before release, re-screen if data changed or earlier results are no longer current. Do not release until required checks are complete. Then apply written disposition criteria that define which potential matches require hold and analyst review and which require block and compliance or legal escalation, based on full case evidence.

Approximate-matching tools and confidence sliders can help triage alerts, but they do not set your threshold for you and they do not replace due diligence. Make the final disposition from the full evidence, not from the score alone.

For UK relevant firms, if you know or reasonably suspect a designated person or breach, report to OFSI as soon as practicable. Where required, include the nature and amount or quantity of funds or economic resources held.

Prevent the main failure modes#

Focus controls on three recurring breakdowns: stale results, missing retries, and unlogged overrides.

If a screening call fails or is incomplete, follow your documented retry policy and hold when required checks are still incomplete at decision time. For overrides on suspected matches, log case ID, reviewer, approver, timestamp, list source, rationale, and evidence reviewed. For post-release alerts, decide and document whether the event needs only case review or a historical lookback on related payouts.

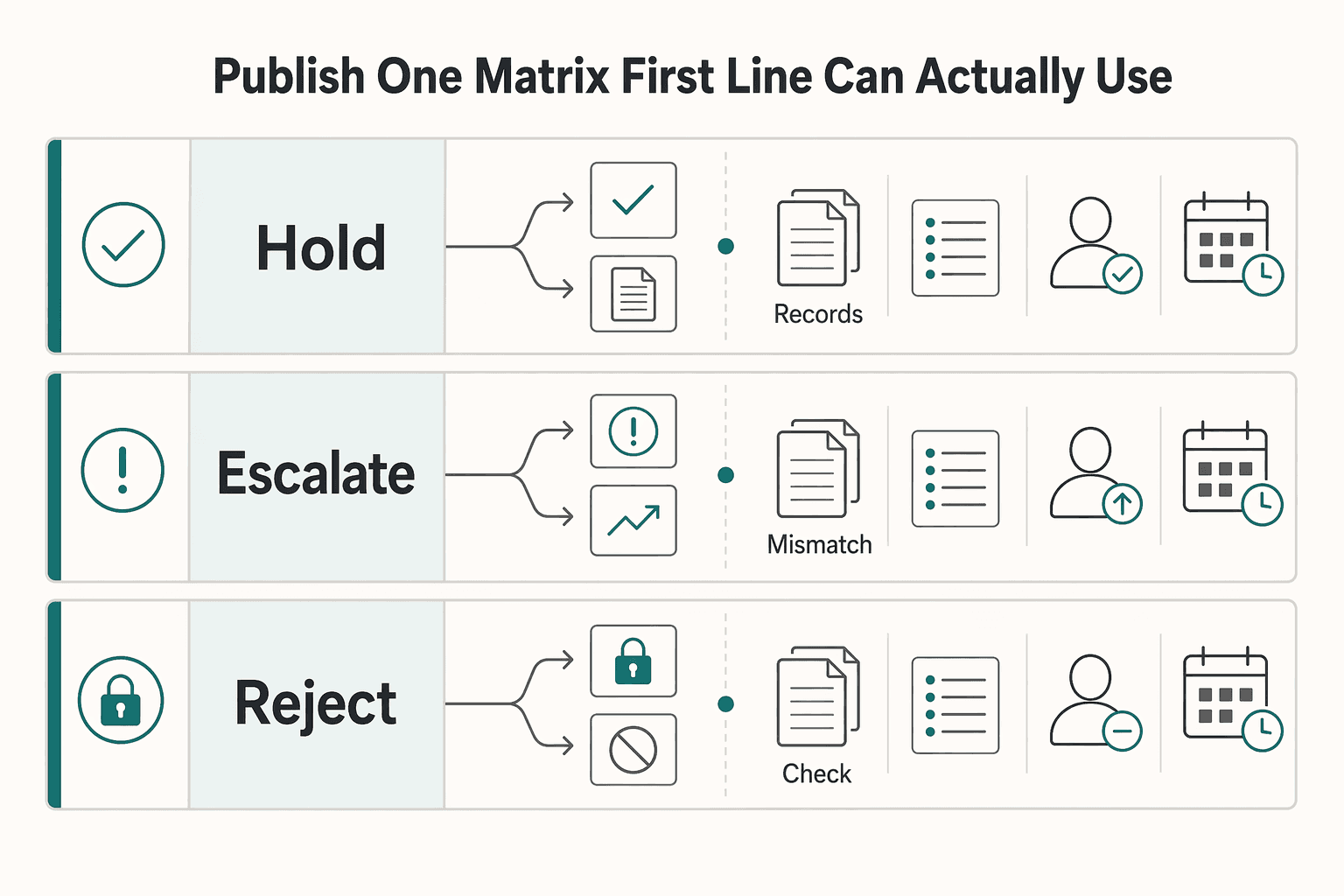

Apply go hold escalate reject rules your team can execute fast#

Use one four-outcome matrix so first-line teams make consistent decisions under time pressure and compliance can defend the record later.

Publish one matrix your first line can actually use#

Make this your internal disposition path for screening outcomes in cross-border payments. FFIEC examination procedures include a defined process to investigate potential matches, escalate potential matches, handle block or reject outcomes, and inform management.

| Action | Use when | Immediate owner | Verify before moving forward |

|---|---|---|---|

| Go | No list hit, no unresolved data gap, jurisdiction risk already triaged | Payments ops | Latest successful screen, input snapshot, and no material edits after screening |

| Hold | Potential match is low confidence or identity data is incomplete | First-line analyst | Hold reason logged, missing data requested, retry or review deadline set |

| Escalate | Facts are mixed, material, or high consequence | Compliance or legal second line | Escalation record and evidence pack attached |

| Reject | Review concludes the transaction cannot proceed | Compliance or legal per policy | Final rationale recorded and required reporting path triggered |

At minimum, each case should show screened inputs, list source, decision maker, and timestamp.

Separate operational differences from legal thresholds#

Contractor payouts and seller payouts can run through the same stack but still produce different review patterns. Your legal threshold should stay consistent, even if the evidence handling differs.

| Flow pattern | Typical review risk | Control emphasis |

|---|---|---|

| Contractor payout | A single payee match can drive the whole case | Strong identity reconciliation and match analysis |

| Seller payout | More moving parts and post-onboarding changes can increase stale-screen risk | Re-screen discipline and change-trigger controls |

Do not turn corridor discomfort into an automatic reject rule. FATF says jurisdictions under increased monitoring are not automatically subject to FATF-called enhanced due diligence, and FATF standards do not support blanket de-risking of customer classes.

Force second-line review for the highest-risk combination#

Require second-line review when both conditions are true: high jurisdiction risk and a possible sanctioned-individuals match.

If a payment touches a FATF High-Risk Jurisdiction subject to a Call for Action, route it to escalated review at minimum. FATF calls for enhanced due diligence for these countries and, in the most serious cases, calls for countermeasures. Keep cases in hold or escalate when key identifiers are missing rather than turning uncertainty into release.

Make unresolved high-risk cases impossible to release casually#

Set a hard internal control rule: no payout release for unresolved high-risk cases without documented compliance sign-off and an escalation record.

This prevents release-by-handoff failures and preserves reporting readiness. If the final path is reject or block, your record should clearly support the outcome. Rejected transactions covered by 31 CFR 501.604 are reportable to OFAC, and initial blocked-property reports under 31 CFR 501.603 are due within 10 business days.

If your team is finalizing the go/hold/escalate/reject matrix, review how Gruv Payouts supports compliance-gated releases, batch visibility, and audit trails.

Add ongoing monitoring for repeat payees and payout batches#

Do not stop screening after onboarding or the first payout. Repeat payees and batch releases need ongoing, risk-based re-screen triggers so you can catch changes after an initially clean result.

Set a risk-based re-screen trigger for recurring payees#

Use two triggers together: a periodic schedule and event-driven review. FATF frames ongoing monitoring as checking whether transactions remain consistent with what you know about the customer, and Wolfsberg positions customer and transaction screening as lifecycle controls, not one-time onboarding checks.

Keep the trigger set simple:

- Re-screen recurring payees on a documented periodic schedule based on risk.

- Re-screen when transaction monitoring raises a meaningful alert or another significant risk event occurs.

- Re-screen before release when material identity data, corridor, or counterparty details changed after the last clean screen.

Before release, the case record can show the latest successful screen timestamp, the screened input snapshot, and whether any relevant data changed after that screen.

Treat payout batches as a separate control surface#

Batch payouts need controls beyond single-payment checks. Wolfsberg highlights transaction volume and distribution channels as risk factors, and cross-border flows can require extra scrutiny, especially where corridors touch High-Risk Jurisdictions subject to a Call for Action or Jurisdictions under increased monitoring.

For batches, review more than name matches:

- corridor mix, including any High-Risk Jurisdictions subject to a Call for Action

- unusual volume, velocity, or concentration by country

- whether one changed payee record affects many payouts at once

If a batch includes a high-risk corridor, avoid relying on sampling alone. Review the affected segment, attach the batch ID and reviewer notes, and document whether enhanced due diligence is required.

Review external risk posture when FATF and lists change#

Set governance triggers to external updates, not just annual review. FATF issues its two public high-risk and monitored-jurisdiction documents three times a year and continually reviews jurisdiction risk, so each new FATF publication should trigger a corridor review, watchlist refresh, and rule check.

Also monitor non-FATF list owners. For example, the UK Sanctions List showed an update on 31 March 2026, which is a practical reminder to recheck affected repeat payees and queued batches before release when external status changes.

Handle false positives and investigations without freezing all payouts#

Do not freeze every payout on a weak name hit. Use a fast review lane for likely false positives, but keep documented reasoning and timed escalation so controls stay risk-based instead of turning into blanket holds.

Route likely false positives into an expedited review lane#

Triage alerts quickly: weak, name-only, or fuzzy-search hits go to expedited review, while plausible matches move straight to full investigation. FATF's risk-based approach supports case-by-case handling, not wholesale restriction, and it does not require a zero-failure standard.

Even in the fast lane, require a human check against the relevant list entry and your internal evidence. Do not clear a case from tool output alone. OFSI notes fuzzy search can catch misspellings and partial words, but relevance can drop, so the analyst should record exactly what matched, what did not, and which screened input snapshot was used.

If objective identifier mismatches make the hit non-credible, clear and document it promptly. If plausibility remains after identifier review, hold and escalate out of the expedited lane.

Capture the decision record so it is defensible#

Every alert needs a defensible case note, including alerts cleared in minutes. Search tools do not remove due diligence obligations, and relying on search results does not limit liability, so the record must show reasoning, not just outcome.

At minimum, capture:

- case ID, alert ID, analyst, and timestamps

- screened party data and the exact input snapshot

- list entry or entries reviewed

- match rationale, including matched and mismatched identifiers

- supporting evidence

- final decision, decision owner, and payout status, whether released, held, escalated, or rejected

A short note is enough if another reviewer can reconstruct why the decision was made.

Set timeout and handoff rules so holds do not become indefinite#

Set internal investigation time limits by lane, and make handoff automatic when the timer expires. If first-line review cannot resolve the case in time, escalate to legal or compliance with a named owner instead of leaving it in queue.

This addresses a known failure mode: OFSI published an enforcement notice where a potential match triggered an alert and profile suspension, but escalation was not reviewed that day. For UK relevant firms, reporting obligations mostly apply, and OFSI says you should contact it as soon as practicable when you hold relevant information.

At handoff, verify three things: who owns the case now, what evidence transferred, and whether payout release remains blocked. Related reading: How to De-Risk a Fixed-Price Project with a Phased Payment Schedule.

Avoid common failure patterns and recover quickly#

Most repeat failures come from four controllable mistakes: confusing FATF risk signals with legal prohibitions, screening with weak identity data, relying on one-time checks, and keeping poor records.

Separate FATF risk signals from legal sanctions obligations#

Treat High-Risk Jurisdictions Subject to a Call for Action as a risk signal, not an automatic payment ban. FATF calls for enhanced due diligence across those jurisdictions, with countermeasures in the most serious cases.

In each case note, record whether the trigger was a FATF jurisdiction flag or a match to a designated person, entity, ship, or ownership or control link on an official sanctions list.

If analysts cannot distinguish those triggers in the record, retraining is overdue. Blanket de-risking is the failure pattern to prevent.

Block payout creation when identity data is incomplete#

Incomplete identity data makes screening less reliable, so set an intake gate before payout creation:

- for individuals: verified identity data, not only a typed name

- for entities: legal entity details plus enough ownership or control information to assess sanctions exposure through unlisted but controlled entities

Do not mark screening complete when required identity fields or supporting documents are missing.

Add recurring checks, not just onboarding checks#

One-time onboarding clearance is not enough for repeat payees. Controls should include ongoing due diligence and transaction scrutiny throughout the relationship, not just at onboarding.

Use a simple control check: each recurring payee should show a latest-screened timestamp and a documented re-screen reason when triggered. Do not rely on stale onboarding results when payee details or risk context change.

Standardize records for AML/CFT audit and recovery#

Weak documentation makes decisions harder to defend. Standardize EDD and escalation notes so analysts consistently capture screened inputs, list entries reviewed, identity evidence, rationale, decision owner, and payout status.

Search tools do not remove due diligence obligations, and enforcement messaging has highlighted screening, escalation, and training weaknesses in breach outcomes. Where UK anti-money laundering and counter-terrorist financing (AML/CFT) recordkeeping rules apply, Regulation 40 sets a five-year baseline for retaining records and supporting evidence needed to reconstruct the decision.

Build the reporting checklist auditors and leadership will ask for#

Turn standardized case notes into management information that supports decisions, escalation, and audit reconstruction. The goal is a reporting pack that shows who decided what, when, on what evidence, and what happened next.

Define a minimum case reporting pack#

Create one case-level record for every escalation, release after review, rejection, and material exception. Regulators do not prescribe one universal template, but your pack should let senior management oversee sanctions risk, support timely escalation, and reconstruct a transaction when requested.

A practical minimum pack can include:

- case ID

- current decision status (hold, release, escalate, or reject)

- named owner and approving function

- evidence references, not only free-text notes

- escalation timestamps (opened, reviewed, handed off, and closed)

Use a simple test: sample any case and confirm a reviewer can trace it from alert to final payout status in one place. If list-screening results, identity evidence, relevant Enhanced Due Diligence (EDD) material, and escalation history are split across tools, the pack is not audit-ready yet.

Add trend metrics that show control performance#

Report outcomes, not just alert volume. Track matches or breaches and related outcomes such as holds, releases after review, rejected payouts, and unresolved exceptions.

Where it helps decision-making, break metrics by corridor and risk lane to separate exposure changes from data-quality issues. Also include the age of open exceptions so unresolved cases do not quietly accumulate and weaken oversight.

Tie reporting to governance actions when FATF risk changes#

When FATF high-risk or monitored-jurisdiction outputs change, reporting should trigger governance review, not just note the update. This is especially relevant for High-Risk Jurisdictions Subject to a Call for Action updates overseen by ICRG, including the 13 February 2026 cycle.

If strategic AML/CFT deficiencies worsen, record the control response taken: policy tuning, approval changes, training updates, monitoring changes, or deeper EDD. FCA guidance indicates financial-crime expectation updates can require changes across policies, monitoring, training, governance, and other controls.

Link sanctions reporting to related controls#

Do not keep sanctions reporting separate from adjacent controls. For high-risk payment cases, include links to the related transaction monitoring and EDD records so reviewers can see why a case was opened and how it was resolved.

In practice, add related TM alert IDs and EDD file references to each reportable case. For deeper process design, use transaction monitoring for high-risk payments and Enhanced Due Diligence (EDD).

Conclusion#

The defensible approach is disciplined sequencing. Use FATF country signals for jurisdiction triage, screen parties and transactions against the sanctions regimes that apply to you, then make and document a clear go, hold, escalate, or reject decision. That keeps controls risk-based and avoids blanket freezes where better review is the real need.

Use this closeout checklist with your team:

- Step 1: Confirm ownership and escalation points.

Assign decision owners across compliance, legal, finance, and payments operations before cases arrive. A reviewer should be able to see who approves, who places holds, who is consulted on potential matches, and who informs management of blocked or rejected transactions.

- Step 2: Verify intake data and the evidence pack before screening.

Do not start from partial identity data. Your file should include the identifiers used for screening, key case context, and decision rationale so a second reviewer can reproduce the outcome.

- Step 3: Apply FATF-based jurisdiction triage and record the risk lane.

Use the FATF statements dated 13 February 2026 as your baseline, then refresh when FATF updates after plenaries. Keep the distinction clear: jurisdictions under increased monitoring are not under a FATF instruction for automatic enhanced due diligence, while high-risk jurisdictions subject to a call for action require enhanced due diligence and, in more serious cases, may require counter-measures.

- Step 4: Run screening at your control points and log each result.

If your framework uses onboarding, payout creation, and payout release checkpoints, record timestamped results at each one. Customer screening and transaction screening are distinct controls, and stale earlier results can leave control gaps.

- Step 5: Use one decision matrix and document every hold, release, escalation, and rejection.

Apply one consistent path from potential match to final action, with timestamps and rationale. Where UK relevant-firm obligations apply, if you know or reasonably suspect a customer is a designated person, report to OFSI as soon as practicable, including the nature and amount or quantity of any funds or economic resources held for that customer.

- Step 6: Re-screen recurring payees, review exceptions, and update controls when risk signals change.

Re-screen when corridor risk shifts, monitoring raises new concern, or FATF country statements change. Tighten where risk increases, but do not treat increased-monitoring status as a blanket stop on legitimate payouts.

When you are ready to pressure-test this framework against your corridors and operating model, talk with Gruv to confirm control and market coverage details.

Frequently Asked Questions

What is sanctions screening for high-risk-country payments, in one practical definition for operators?

For operators, it means screening the parties and the transaction against applicable sanctions lists while treating FATF status as a separate jurisdiction-risk signal. FATF risk changes the review lane, but a listed-party match drives the sanctions decision.

Does FATF high-risk status automatically prohibit a payment, or does it trigger heightened review first?

It generally triggers heightened review first, not an automatic prohibition. FATF calls for enhanced due diligence for high-risk jurisdictions and, in the most serious cases, counter-measures, but that does not by itself make every related payment prohibited across all regimes.

When should a payment to a high-risk jurisdiction be escalated instead of approved or rejected?

Escalate when material uncertainty remains, especially around a possible designated-person link or a possible sanctions offence. If the evidence or rationale is not clear enough to document, do not release the payment. Hold it and escalate to compliance or legal.

What records should we retain to defend a sanctions-screening decision during audit?

Keep a case file that shows what was screened, what matched, what evidence was reviewed, who decided, and when the decision changed. Include screened identifiers, search results, rationale, escalation history, and final status. For OFAC-covered transactions, records must be available for examination for at least 10 years, and blocked-property records must be kept through the block period and for 10 years after unblocking.

How often should we re-screen repeat payees and recurring payout flows?

There is no universal re-screening interval in the cited sources. Use ongoing, risk-based monitoring and re-screen when risk signals change, including material data changes, meaningful monitoring alerts, or FATF public listing updates. At minimum, FATF public updates occur three times a year.

What is the fastest safe way to clear likely false positives without creating compliance blind spots?

Clear likely false positives by checking stronger identifiers and documenting exactly why the hit is not credible. Where your regime requires it, include owned-or-controlled analysis because prohibitions can extend to unlisted entities owned or controlled by designated persons. Do not release a payout based only on a partial name mismatch without a clear evidence trail.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/OfficeOfForeignAssetsControl/01trusted

- bsaaml.ffiec.gov/manual/OfficeOfForeignAssetsControl/01_eptrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-V/part-5...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-V/part-5...trusted

- federalregister.gov/denied-persons-specially-designated-nationalstrusted

- federalregister.gov/documents/2025/03/21/2025-04864/reporting-pr...trusted

- federalreserve.gov/econres/feds/files/2025092pap.pdftrusted

- sanctionslist.ofac.treas.govtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: