Quick Answer

Start by mapping one live payout flow, logging licensing assumptions, and assigning one owner per unresolved issue. In psd3 psr eu payment regulation platforms planning, implement controls you can evidence now and park interpretation-dependent changes in a counsel queue. Keep proposal texts, impact assessments, provider contracts, and user-facing payment steps in one dated evidence pack so legal and operations review the same facts.

Prioritize PSD3 and PSR controls before final text lands#

Treat PSD3 and PSR as a control-prioritization exercise now, not a project to begin only after the final political text lands. For online platforms and Technical Service Providers, separate what you can verify today from what still depends on final European Union wording. Then build only the controls that reduce downside without locking you into the wrong model.

EU VAT changes provide a useful pattern. From 1 July 2021, VAT rules for cross-border B2C e-commerce changed. Online sellers, including online marketplaces and platforms, can register in one EU Member State for eligible VAT declaration and payment, and in some cases a platform is deemed for VAT purposes to have received and supplied the goods itself. Those VAT facts do not determine the final PSD3 or PSR outcome, but they do show that EU changes can shift platform accountability.

-

Start from roles you can prove. Before debating future payment-regulation exposure, document how live flows are characterized today across onboarding, charge collection, holding periods, and payout instructions. Focus on evidence: who contracts with the user, who sets or discloses fees, who owns transaction records, and whether the platform is already in scope elsewhere as a marketplace or deemed supplier.

-

Prefer low-regret controls over speculative builds. OSS shows that a single registration point does not mean a low operating burden. A taxable person can register in one Member State of identification, but OSS still includes rules on records to be kept, invoices, and bad debt relief, and filing cadence varies by scheme. Returns are quarterly in the Union and non-Union schemes and monthly in the import scheme. The practical takeaway is to strengthen traceability, ownership, and evidence retention now, and defer builds that depend on final PSD3 or PSR wording.

-

Flag lock-in decisions early. Some choices look reversible until operational constraints become clear. Under OSS registration rules, a business can be bound by its Member State of identification choice for the current calendar year plus the two following calendar years. Apply that lesson here. If a design decision could create multi-year rework across legal, finance, and operations, escalate it early and document why.

Before moving through the rest of the list, check whether your team can produce three artifacts on demand: a current map of cross-border money movement and payout flows, existing OSS and VAT registration choices, and a named owner for records and invoices. If those basics are fragmented across legal, finance, and operations, that is already a risk signal. A common failure mode can be not missing a final rule, but letting teams describe the platform differently while the law is still evolving.

This article is intentionally practical. It does not assume final PSD3 or PSR text is settled, and it does not assume every platform will face the same outcome. It focuses on controls to stand up now, decisions to defer, and escalation points to surface before you expand volume, geographies, or reliance on third-party payment providers.

You might also find this useful: Account Reconciliation for Payment Platforms: How to Automate the Match Between Payouts and GL Entries.

How to use this list before legal text is final#

Use this list as a triage tool, not a promise that every control should ship now. For each control, make one call up front: implement now, design and hold, or escalate. That keeps the rest of the article grounded in decisions you can actually take.

- Score every control on three tests

Check three things first: the downside if legal interpretation lands unfavorably for your model, the disruption to live collection and payout flows, and whether you can prove the control with records today. If evidence is weak, treat the control as weak. A practical check is whether you can produce a dated flow map, a named owner, and supporting records without rebuilding the story from chat threads.

- Use this with the right team

This list is for compliance, legal, finance, and risk owners at multi-market EU platforms where money movement, invoicing, and payout operations cross functions. It is not a substitute for Member State legal advice. If a decision depends on local VAT treatment or registration scope, escalate to counsel and confirm applicable national ruling conditions.

- Implement low-effort, high-downside controls now

Prioritize controls that are reversible and evidence-heavy. Ownership records, role mapping, and transaction evidence collection can improve audit readiness even when interpretation changes. Use an OSS-style checkpoint: can you show who registers, who declares or pays, and who keeps records and audit files?

- Design uncertain controls, then defer rollout when legal interpretation is the hinge

If counsel says a decision turns on unresolved interpretation, design the control and hold implementation. Assign a clear owner and escalation path so legal and operations do not drift apart under pressure.

Related: Real-Time Payment Use Cases for Gig Platforms: When Instant Actually Matters.

Control 1 role and scope mapping across the payment chain#

Start here. A facts-first map of one live payment flow gives legal, ops, and finance a shared baseline before anyone makes PSD3 or PSR classification calls.

- Best for: teams that use different labels for the same flow, such as platform, technical layer, or payment actor.

- Pros: surfaces where future PSD3 or PSR interpretation could matter and aligns cross-functional language.

- Cons: requires detailed process mapping and exposes ownership gaps.

- Concrete use case: map one contractor payout flow from onboarding to disbursement, then tag each step to a PSP touchpoint and an internal control owner.

Build the map around actions, not labels#

Map one end-to-end flow first: onboarding, contractual setup, payer charge or invoice, PSP handoff, internal approval, payout instruction, disbursement, exception handling, and record retention. For each step, record:

- legal entity performing the step

- external party involved, including PSPs

- customer-facing or contractor-facing role shown in product copy or contracts

- internal control owner

- evidence available now, for example contracts, PSP agreements, product screens, ledger entries, payout files, and policies

If a step has no evidence attached, treat ownership as unproven.

Use current EU role evidence to pressure-test consistency#

Use VAT and OSS artifacts as consistency checks, not as substitutes for PSD3 or PSR legal analysis.

Under OSS, a taxable person that opts into an OSS scheme registers in one single Member State of identification and submits electronic OSS VAT returns. Filing cadence is quarterly for Union and non-Union schemes and monthly for the import scheme. If different entities appear across product, PSP contracting, and OSS registration, flag that mismatch for legal review.

Also, do not assume "not deemed supplier" means no obligations. Online marketplaces can still have record-keeping duties even when they are not deemed suppliers.

What good looks like in practice#

A strong map is dated, versioned, and scoped to one flow, one entity set, and one geography set. Keep separate maps where cross-border setups differ.

In the contractor payout lane, confirm who onboards the contractor, who approves payability, which PSP disburses funds, who can stop payouts or initiate reversals where applicable, and who stores payout and exception records. If two teams assign different legal entities to the same customer-facing step, pause rollout on that lane and escalate.

If unresolved issues involve complex cross-border VAT treatment, a VAT Cross-border Ruling can be considered. The request must follow national VAT-ruling conditions in the filing country. Where multiple companies are involved, one company should file on behalf of the others.

We covered this in detail in Choosing Small Payment Institution or Authorised PI for UK Payment Platforms.

Control 2 licensing trigger log and exemption position#

This control matters most when the operating model keeps changing but teams still describe it as "just a platform." The goal is not to settle, from ops alone, whether a PI or EMI path is required. It is to turn unresolved licensing assumptions into dated, reviewable decisions and make escalation triggers explicit, especially when the model relies on an exemption position.

What the log should capture#

Keep entries short, but specific enough for counsel to act quickly. Each review entry should include:

- payment flow name, version date, and legal entities involved

- the assumption in use, for example an exemption position or "no current PI/EMI conclusion"

- what changed since last review, such as product copy, contracts, PSP setup, approval rights, or payout handling

- evidence available now, not planned later

- escalation owner, current status, and next review date

If evidence is missing for the current position, treat the assumption as stale and escalate.

Use VAT records as consistency checks, not licensing answers#

VAT OSS and cross-border VAT ruling records can be used as consistency checks, but they do not decide PSD3 or PSR licensing outcomes. Concrete checks you can run include:

| VAT check | Fact in article |

|---|---|

| OSS registration | Registration is in one single Member State of identification |

| Union and non-Union cadence | OSS returns are quarterly |

| Import-scheme cadence | OSS returns are monthly |

| Relevant Union-scheme choice | With multiple fixed establishments, the Member State choice can bind for the calendar year plus two following calendar years |

| Marketplace record keeping | Online marketplaces and platforms can still have record-keeping requirements |

- If you use OSS, registration is in one single Member State of identification.

- OSS return cadence is quarterly for Union and non-Union schemes, and monthly for the import scheme.

- In relevant Union-scheme setups with multiple fixed establishments, the Member State choice can bind for the calendar year plus two following calendar years.

- Online marketplaces and platforms can still have record-keeping requirements.

If the user-facing entity, PSP contracting entity, and OSS entity do not match, treat that as an escalation trigger.

Define escalation triggers before they happen#

Set triggers in advance so legal does not have to reconstruct facts after launch. Typical triggers include:

- a new entity starts contracting with payers, sellers, or contractors

- product copy changes who appears to control onboarding, approval, or payout timing

- PSP onboarding or settlement model changes

- OSS registration, filing ownership, or record-keeping ownership changes

- a cross-border VAT issue is complex enough that a CBR request is considered

For CBR, keep the procedural facts in the log. Requests are filed in the participating EU country where the requester is VAT-registered and must follow that country's national VAT-ruling conditions. Where multiple companies are involved, one company should file on behalf of the others.

The failure mode to watch#

The main failure is not one wrong legal view. It is an old view surviving new facts. If the log says "no change" while onboarding screens, fee flows, or payout approvals changed, the control failed and that lane should be paused until legal review and evidence are updated.

Control 3 fraud liability and SCA operations#

Use this control as an incident gate. If a payment lane shows a control failure or unresolved evidence, pause scale-up in that lane until review is complete and the control design is updated. Keep VAT OSS interpretation and broader payment-law interpretation as escalation items for specialist review, not assumptions embedded inside ops.

The practical challenge is usually alignment, not tooling. VAT record-keeping and invoice evidence often sit in one function, while payment acceptance, payout approvals, and PSP handling sit elsewhere. That split creates inconsistent decisions unless ownership and evidence feed into one review path.

Make the incident gate mandatory#

Set one enforceable if-then rule. If a payment route has a material control break or an incident you cannot reconstruct clearly, require formal review before increasing volume, adding markets, or reusing the same route pattern.

Keep the review short and evidence-led. Capture the flow version, PSP, legal entity, user-visible outcome, control behavior, and evidence available now. If any of that is unclear, treat the control as unproven.

Reuse evidence you already keep#

Start incident reconstruction with the trigger log from Control 2. Then add a compact evidence pack with the transaction record, relevant invoice, and related VAT OSS record-keeping artifacts.

Those artifacts help verify who charged the customer, which entity invoiced, and whether your internal flow narrative matches operational reality. If those facts do not line up, the incident review is incomplete.

| Review element | What to verify | Red flag |

|---|---|---|

| Flow ownership | Same entity across product copy, PSP setup, and invoice trail | User-facing and invoicing entities diverge without explanation |

| Transaction evidence | Record trail is complete enough to reconstruct what happened | Missing or fragmented event history |

| Cross-border consistency | OSS and related tax records align with the operating entity in the flow | PSP, seller, and tax records point to different owners |

Expect product tradeoffs, not just control wins#

Tighter controls can add friction and review workload. Make that tradeoff explicit by assigning a decision owner who can balance loss exposure, conversion impact, and evidentiary quality.

When uncertainty is cross-border and VAT-related, document facts early and escalate that VAT question through the VAT Cross-Border Rulings route where appropriate. Keep the boundary clear: VAT clarification is separate from broader payment-law liability decisions.

Related reading: ERP Sync Architecture for Payment Platforms Using Webhooks, APIs, and Event-Driven Patterns.

Control 4 fee transparency and customer communication discipline#

Treat fee transparency as an operating control, not a copy exercise. If a customer, seller, or contractor cannot reconcile what they saw before payment with what appears after payment, complaint handling can get harder and risk can rise.

- Pre-transaction charge view

Show the charge logic before commitment, especially when platform fees, FX-related charges, or payout deductions can affect the final amount. Keep labels, charging entity, and currency explanation consistent with what finance and support will use later.

- Post-transaction record alignment

Keep receipt, statement line, invoice, and payout record aligned to one version of events. In cross-border EU flows, verify that the invoicing entity matches your VAT treatment, including cases where a marketplace can be treated as a deemed supplier for VAT purposes.

- Complaint evidence pack

For disputed charges, keep a compact pack: pre-transaction screen copy, transaction record, invoice, payout advice if relevant, and the support template used. The goal is to answer quickly what was disclosed, by whom, and where the amount landed.

Use OSS record-keeping as a practical checkpoint. From 1 July 2021, cross-border B2C e-commerce VAT rules changed, including record-keeping requirements for marketplaces and platforms. OSS VAT returns are additional to domestic VAT returns. This VAT evidence supports process discipline, but it does not by itself define PSD3/PSR-specific fee-disclosure wording. That helps when a fee complaint becomes a question of who supplied, who invoiced, and which Member State of identification sits behind the filing setup.

The tradeoff is execution effort. Clearer disclosure usually means updates to product copy, statement descriptors, and support scripts. If a charge type cannot be explained clearly in one pre-payment view and one post-payment artifact, pause rollout in that lane until the communication path is fixed.

Control 5 PSP and vendor governance across banks and non-bank providers#

Once fee records are aligned, apply one internal governance standard to every PSP. If you use multiple providers, including non-bank PSPs, the control objective is comparability and audit readiness, not trying to stretch VAT or OSS sources into final PSD3 or PSR vendor obligations.

Standardize the renewal test#

Use one renewal questionnaire for every bank and non-bank PSP, even when products differ. Keep commercial terms separate from control evidence so pricing does not hide documentation gaps.

Set a clear minimum. Before renewal, require current evidence on SCA handling, fraud controls, and incident-escalation contacts as your internal diligence baseline. Label it that way, because the VAT and OSS sources here do not make those artifacts explicit PSR requirements.

Tie provider review to records you actually need#

Anchor provider review to records you must keep and file. OSS explicitly covers records, invoices, and bad debt relief, and if you use an OSS scheme you must declare all supplies that fall under that scheme through the OSS return.

| Review area | What to verify | Why it matters |

|---|---|---|

| Transaction and settlement records | Can the provider deliver stable exports that match charge amount, payout amount, currency, correction entries, and invoice references? | OSS has defined record-keeping and audit expectations. Missing fields can become filing issues and weaken audit readiness. |

| Filing alignment | Can finance map provider data to your Member State of identification and the correct return cadence, quarterly for Union and non-Union schemes and monthly for the import scheme? | You need one consistent record between payment operations and VAT reporting. |

| Structural changes | Can the provider change merchant-of-record setup, settlement entity, or country routing without formal notice? | In some cases, the Member State of identification choice is binding for the current year plus two following calendar years. |

Do not stop at uptime and fraud tooling. Confirm that provider outputs support the VAT records your cross-border model depends on, including cases where a marketplace is treated as a deemed supplier.

Escalate the right red flags#

Escalate two issues immediately: a provider without a documented correction path for bad data or post-transaction changes, and any provider model change that makes cross-border VAT treatment unclear. In the second case, get specialist advice and consider whether a VAT Cross-border Ruling is appropriate for a complex transaction.

Treat persistent reporting gaps as governance risk, not just operations friction. A taxable person can be excluded from an OSS scheme by a Member State. Since 1 July 2021, the cross-border B2C VAT changes apply across online sellers and marketplaces/platforms.

A practical evidence pack can support renewal decisions: signed questionnaire, sample reports, incident contacts, change-notice terms, and one reconciled example showing how provider data feeds invoice and OSS records. If a vendor cannot support that pack, do not renew on price alone.

Control 6 open banking and data handling boundaries#

Keep this control narrow and defensible while PSD3 or PSR open-banking specifics are still uncertain in your working evidence. Treat these steps as internal control design, not as a claim of finalized PSD3 or PSR requirements. Set boundaries by business purpose, and keep them tight enough that you can explain every field, access decision, and retention choice.

If a feature cannot show why it needs a field, how long it keeps it, and who can access it, do not approve broader collection just because the integration can return more data.

Purpose map before field map#

Start with a short purpose register for each feature that touches open-banking connectivity. For each purpose, define the minimum data needed, approved access, and records needed for finance and tax operations.

Use a simple rule: if a field does not support a customer action, a reconciliation need, or a required record, keep it out of scope. This supports a cleaner audit narrative, including marketplace cases where record-keeping obligations can still apply even when a platform is not a deemed supplier.

Retention tied to filing and audit needs#

Do not apply one blanket retention period to all account-data payloads. Split short-lived operational data from records needed for filings and audits.

OSS materials explicitly cover registration, VAT declaration and payment, record keeping, and audits, and OSS VAT returns are additional to domestic VAT returns. For each retained dataset, require a named owner, deletion trigger, and legal or operational reason to retain it. If none exists, delete or truncate sooner.

Access approvals based on filing impact#

Tighten cross-team access when data can affect regulatory or tax reporting narratives. If data feeds records used for Member State of identification or OSS return preparation, require named approvals instead of broad internal visibility.

Keep operating cadence in view. Union and non-Union OSS returns are quarterly, and import-scheme returns are monthly. In some cases, Member State of identification choices are binding for the current calendar year plus two following calendar years. If a data-model change could alter record interpretation across that period, treat it as a controlled change with a dated decision log and a clear revocation path.

What to implement now and what to defer until text is final#

Use a low-regret split: implement controls now when they are confirmed by current EU VAT OSS/CBR rules, and defer PSD3/PSR-specific items until final legal text is available. Keep current VAT operations in view while you do this. OSS returns are quarterly in the Union and non-Union schemes and monthly in the import scheme. A Union-scheme Member State of identification choice can bind you for the current calendar year plus two following calendar years.

| Control area | Known in the provided material | Dependency on final wording | Implementation effort | Risk if delayed | Escalation owner |

|---|---|---|---|---|---|

| OSS scheme registration and Member State of identification | If you use OSS, you register in one single Member State of identification | Low | Medium | Medium | Tax + Compliance |

| OSS return scope completeness | If you choose an OSS scheme, all supplies under that scheme must be declared through that scheme's OSS return | Low | Medium | High | Tax Operations |

| OSS filing cadence controls | Non-Union/Union returns are quarterly; import-scheme returns are monthly | Low | Low to medium | High | Tax Operations + Finance |

| OSS participation governance | A participant can deregister voluntarily or be excluded by a Member State | Low | Low to medium | Medium | Tax + Compliance |

| OSS record-keeping and audit readiness | OSS guidance includes a dedicated record-keeping and audits checkpoint | Low | Medium | Medium to high | Finance Controls + Compliance |

| CBR request intake and submission | CBR can provide advance VAT treatment for complex cross-border transactions; requests must follow the participating country's national VAT-ruling conditions | Low to medium | Medium | Medium | Tax + Legal |

| CBR multi-company coordination | If multiple companies are involved, one company should submit on behalf of the others | Low | Low | Medium | Tax + Legal |

| PSD3/PSR-specific controls (role mapping, SCA/fraud thresholds, fee wording, PSP evidence formats, CAE/TSP boundaries) | Not confirmed in the provided VAT excerpts | High | Design only until legal text is final | Context-dependent | General Counsel |

Implement now#

Start with OSS and CBR controls that are already supported: registration setup, return-scope checks, cadence controls, participation governance, and record-keeping/audit readiness. If you use an OSS scheme, report all supplies that fall under that scheme through that scheme's OSS return.

For complex cross-border VAT uncertainty, run a CBR track in parallel. Submit under the participating country's national VAT-ruling conditions, and use a single submitting company when multiple companies are involved.

Design then defer#

Defer PSD3/PSR-specific legal interpretations until final PSD3/PSR text is available from dedicated legal sources. For each deferred item, keep a short design memo with the current assumption, the business impact if wrong, and the trigger for reopening.

If you are converting this now-vs-later control table into an operating workflow, use Gruv Docs to align policy gates, payout states, and audit-ready records.

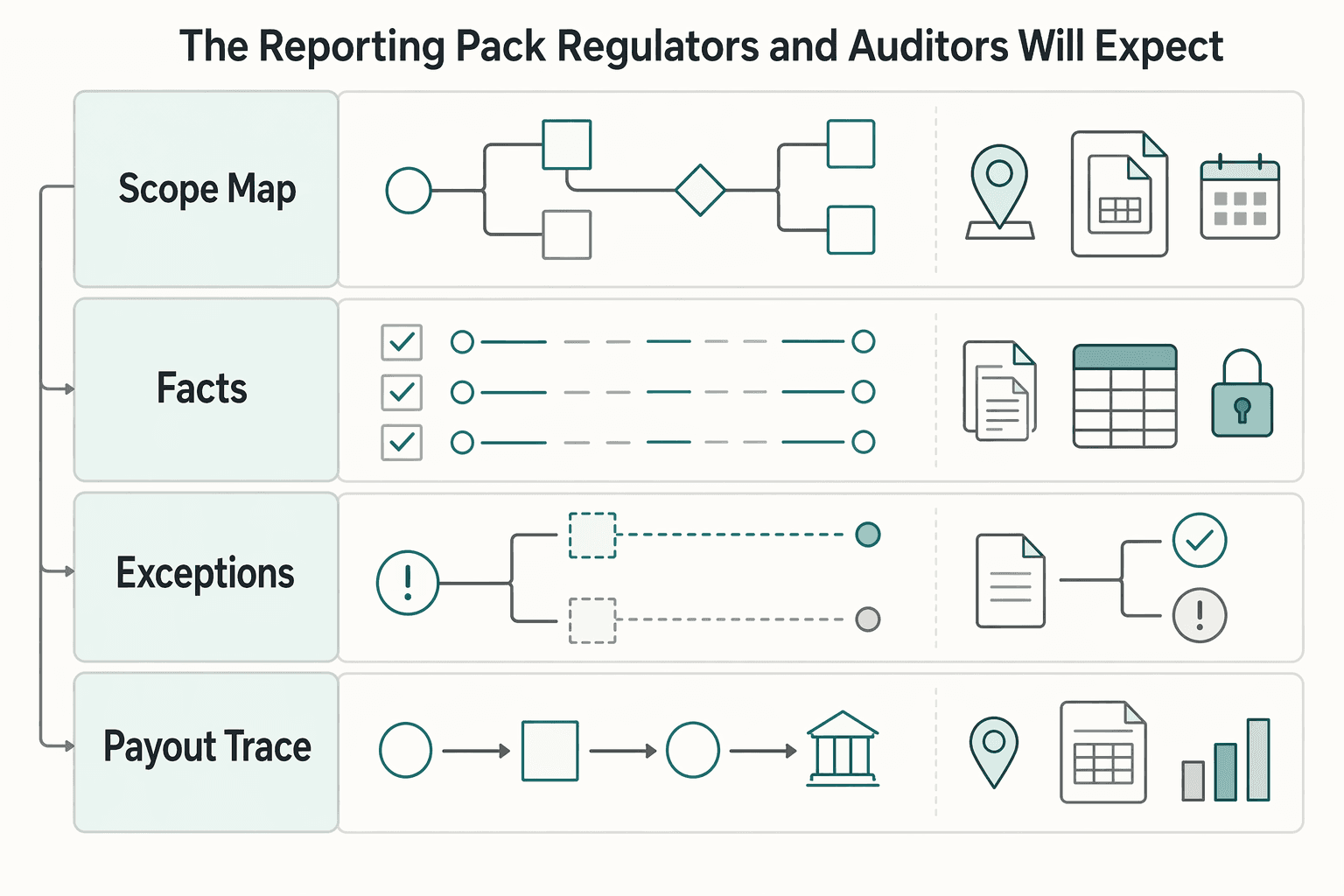

The reporting pack regulators and auditors will expect#

Assume you will need to prove decisions with dated evidence, not just describe controls. For PSD3 or PSR planning, a workable internal baseline is VAT-style record discipline plus a clear separation between what is confirmed and what is still interpretation.

| Pack item | What to keep | Notes |

|---|---|---|

| Scope map and licensing trigger log | One current map of each payment flow, the assumed role in that flow, and trigger points for legal escalation, with every assumption, approval, and change dated | If the model uses OSS, record the Member State of identification because it can bind the current calendar year plus the next two in the cited VAT context |

| Core control artifacts | Scope map, licensing trigger log, governance records, and period-versioned copies; SCA/fraud inventories and fee disclosure artifacts can also be tracked as internal evidence if relevant | Quarterly for Union and non-Union schemes and monthly for import can be used as an operating rhythm, but the article says this is a process choice |

| Verification checkpoints and exceptions register | Control attestation, incident trend review, and an exceptions register with owners and closure dates | If an exception stays open, keep dated remediation evidence or flag the residual risk explicitly |

| End-to-end traceability and exportable evidence | Traceable records and audit-ready exports so one payout can be reconstructed from approval state to final outcome with timestamps and actor traceability | Keep proof for both OSS and domestic VAT returns, and keep transmission evidence when available |

- Scope map and licensing trigger log

Keep one current map of each payment flow, your assumed role in that flow, and the trigger points for legal escalation. Date every assumption, approval, and change so you can show what was known at the time. If your model uses OSS, record the Member State of identification and treat that choice as operationally significant, since it can bind the current calendar year plus the next two in the cited VAT context.

- Core control artifacts tied to payment risk

Keep a minimum internal pack: scope map, licensing trigger log, and governance records used in your PSD3 or PSR readiness process. If relevant to your model, you can also track SCA/fraud control inventories and fee disclosure artifacts as internal evidence, not as requirements established by these VAT/CBR excerpts. Version each artifact by period instead of keeping only the latest copy. For operating rhythm, you can align reviews to known OSS cadences: quarterly for Union and non-Union schemes and monthly for import. Keep clear that this cadence is a process choice, not a confirmed PSD3 or PSR legal timetable.

- Verification checkpoints and exceptions register

Run recurring checkpoints, for example control attestation, incident trend review, and an exceptions register with owners and closure dates, so your team can evidence response quality over time. These checkpoints are not presented here as PSD3 or PSR legal requirements. They are governance controls when legal text is still moving. If an exception stays open, keep dated remediation evidence or flag the residual risk explicitly.

- End-to-end traceability and exportable evidence

For Gruv or similar systems, keep traceable records and audit-ready exports so policy gates, approvals, and payout outcomes can be reconstructed end to end. The standard is reconstruction, not dashboard snapshots: you should be able to follow one payout from approval state to final outcome with timestamps and actor traceability.

Treat two VAT-linked operator details as hard evidence items where relevant. OSS returns are additional and do not replace domestic VAT returns, so keep proof for both filing tracks. Also keep transmission evidence when available, because the OSS process includes cross-Member-State transmission through a secure communications network.

If your position depends on scope or exemption arguments, increase documentation depth rather than reducing it. In the VAT material, record-keeping can still apply even where a marketplace or platform is not treated as a deemed supplier.

90-day execution sequence for legal, risk, finance, and ops#

Use this sequence as a conservative operating plan under uncertainty: lock scope first, verify OSS setup and return operations second, standardize evidence third, and then publish a board-level view. It is not a PSD3, PSR, or PSD2 legal timetable.

| Weeks | Focus | Output / checkpoint |

|---|---|---|

| 1-3 | Lock the role and scope map and freeze the trigger log | For each material payment flow, record assumptions with date, owner, and legal reviewer; if you use OSS, record the selected scheme and Member State of identification; mark unresolved legal interpretation as no expansion pending counsel |

| 4-6 | Test OSS registration, declaration, and payment workflows in evidence | Produce an exceptions register with owner, closure date, and missing evidence; confirm quarterly cadence for non-Union and Union OSS and monthly cadence for the import scheme |

| 7-9 | Standardize VAT evidence collection across internal owners and providers | Request the same core evidence pack each period for records to be kept, invoices, bad debt relief, and declaration/payment operations; include record-keeping artifacts even where the platform is not treated as a deemed supplier |

| 10-12 | Publish the board summary and make deferrals explicit | Separate implemented controls, deferred decisions, and escalation points; anchor the summary to scope map version, OSS registration status, return schedule, declaration and payment evidence, and record-keeping packs |

- Weeks 1-3: lock the role and scope map, then freeze the trigger log

Build one current map for each material payment flow, including onboarding, fund collection, holding logic if any, payout initiation, reversals, fee deductions, and complaint handling. For each step, record assumptions with date, owner, and legal reviewer. Keep confirmed current-state facts separate from forward-looking interpretation so a reviewer can reconstruct decision logic. If you use OSS, record the selected scheme and the Member State of identification in the same decision pack, since that choice can bind the calendar year plus the two following calendar years. If a lane depends on unresolved legal interpretation, mark it immediately as no expansion pending counsel.

- Weeks 4-6: test OSS registration, declaration, and payment workflows in evidence, not policy text

Test whether controls can be evidenced end to end with timestamps, screenshots, decision logs, and named owners across success, failure, and dispute paths. The required output is an exceptions register with owner, closure date, and missing evidence. Confirm the return cadence for your scheme: quarterly for non-Union and Union OSS, and monthly for the import scheme.

- Weeks 7-9: standardize VAT evidence collection across internal owners and providers

Request the same core evidence pack each period so evidence is comparable. Focus on dated documentation for records to be kept, invoices, bad debt relief, and declaration/payment operations. If you operate a marketplace/platform flow, include record-keeping artifacts even where the platform is not treated as a deemed supplier. Do not rely on undated generic materials.

- Weeks 10-12: publish the board summary and make deferrals explicit

Publish a short, precise summary that separates implemented controls, deferred decisions that depend on legal interpretation, and escalation points for external counsel. Treat this as governance discipline, not a stated PSD3 or PSR legal requirement. Anchor the summary to named artifacts: scope map version, OSS registration status, return schedule, declaration and payment evidence, and record-keeping packs. Where VAT design questions materially affect flow decisions, state that directly. For complex cross-border VAT questions, VAT Cross-border Rulings can provide advance rulings under national filing conditions, and a taxable person or intermediary can be excluded from an OSS scheme by a Member State.

If a flow still depends on unresolved legal interpretation, pause expansion in that lane until counsel sign-off.

For a step-by-step walkthrough, see Accounts Payable Days (DPO) for Platforms in the Real Payment Cycle.

What platform operators should do next#

Treat PSD3/PSR readiness as a prioritization queue, not a one-time memo. The legal unknowns are real, but they are not a reason to delay controls that improve evidence quality now. Implement high-certainty controls first, and isolate only the points that truly require legal interpretation.

- Stand up evidence controls now

Build the records you will likely need regardless of final PSD3 or PSR text: dated flow maps, owner assignments, escalation contacts, screenshots of user-facing steps, signed contracts, and version history. This creates a practical evidence baseline for what changed, when it changed, and who approved it. Use adjacent EU compliance operations as an evidence-discipline benchmark, not as a substitute for payments advice. For example, OSS explicitly covers registration, declaration and payment, and record keeping and audits, so keeping those artifacts current and retrievable is a practical readiness signal.

- Use one cross-functional decision register

Keep a single register across legal, risk, finance, and ops, with one row per unresolved point. At minimum, track the issue, current assumption, affected flow, owner, escalation owner, review date, and supporting evidence file. Separate confirmed operating facts from live legal interpretation in that same register. Where VAT treatment affects flow design, record the exact reliance point: OSS scheme used, Member State of identification, deemed-supplier treatment if relevant, and whether a VAT Cross-border Rulings request is in progress. Taxable persons can request CBRs for envisaged complex cross-border transactions, but requests must follow the national VAT-ruling conditions of the filing country.

- Escalate edge cases early and refresh evidence on cadence

Escalate early when a flow may sit near a licensing or exemption boundary. Do not wait until launch. If a lane depends on unresolved interpretation, pause expansion in that lane until specialist counsel signs off. Put a fixed review cadence behind that escalation. Quarterly is a sensible minimum for the main register and aligns with OSS quarterly return cadence in Union and non-Union schemes. If you use the import scheme, monthly review is often more practical because that return is monthly.

Optional schemes can still create hard operating consequences once chosen. Under OSS, opting in means declaring all supplies that fall under the chosen scheme through the OSS return, and a Member State can exclude a taxable person or intermediary from a scheme. In the cited Union-scheme case, the Member State of identification choice can bind the current calendar year plus the two following years. Keep those decisions in the same register as payment-model assumptions, with current evidence attached.

If you want a deeper dive, read PSD2 and PSD3: What Every Platform Operator Must Know About EU Payment Regulation.

If unresolved licensing or exemption questions could block rollout, pressure-test your target flow and market setup with Gruv before you scale.

Frequently Asked Questions

What is the practical difference between PSD3 and PSR for platform operators?

From the excerpts in this section's source pack, the practical PSD3/PSR split is not verified. Treat it as an open legal-interpretation point in your decision log, not a settled operating fact. If a product, treasury, or expansion decision depends on that distinction, hold it until counsel confirms the position in writing.

Do PSD3 and PSR apply only to banks, or can they affect online platform models too?

These excerpts do not establish the full PSD3/PSR perimeter. Do not assume "not a bank" means "not relevant" without a dated legal review. For marketplace, contractor, or creator payout flows, record the assumption, owner, review date, and counsel status so it does not harden into policy by default.

What should we implement now if enforcement timing is still uncertain?

These excerpts do not verify a PSD3/PSR implementation checklist or enforcement timeline. If you take interim steps, label them as internal risk controls rather than confirmed PSD3/PSR requirements, and keep dated flow maps, role assumptions, and decision records.

How should we treat the Commercial Agent Exemption while final text is pending?

From these excerpts, the PSD3/PSR treatment is not verified. Keep any lane that depends on this exemption flagged as a live risk item, and pause expansion in that lane until counsel signs off. Maintain a short memo that separates operational facts from legal interpretation so changes are traceable.

What evidence should we keep to defend our decisions during supervisory review?

These excerpts do not provide a verified PSD3/PSR evidence checklist. For adjacent EU VAT workflows covered here, keep OSS artifacts for registration, declaration and payment, and record keeping and audits, including your Member State of identification. Also retain records of OSS failure-mode risk, including possible exclusion from a scheme by a Member State. Where relevant, note that certain Member State-of-identification choices can bind the current calendar year plus the two following years. If VAT treatment is unclear, document any VAT Cross-border Rulings request and the national VAT ruling conditions used in the filing country.

How does this relate to other EU payment changes such as the EU Instant Payments Regulation?

The provided excerpts do not verify a legal PSD3/PSR relationship to Instant Payments. Treat Instant Payments as a parallel change track with its own owner, timeline, and dependencies, then document operational overlaps clearly. If you need that track next, use EU Instant Payments Regulation: What Platforms Must Support.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

PSD2 to PSD3 for Platform Operators: What to Implement Now, Stage for Later, and Escalate Early

If you run a platform and need decisions now, start with one split. Decide what to implement immediately, what to keep reversible while PSD3 and the Payment Services Regulation (PSR) details are still unsettled, and what to escalate to specialist review before it hardens into product or policy.

What Platforms Must Support Under the EU Instant Payments Regulation

This article is for compliance, legal, finance, and risk owners at platforms and marketplaces operating across EU markets. It is meant to help you decide what to handle internally, what to align with payment providers, and what to escalate for legal review before you make customer-facing payment promises.

When Instant Payout Matters for Gig Platform Payments

Instant payout is a tool, not the goal. The real operating decision is where instant timing creates measurable value, where batch timing is enough, and where both should run side by side.