Quick Answer

Choose a narrow launch lane and prove it end to end before scaling. For performance marketing payouts affiliates compliance, start with one market cluster, one payout model, and one evidence path from affiliate onboarding to approved payout to reconciliation output. Lock ownership for partner vetting, privacy review, and payout approvals, then enforce line-level holds for missing tax information, disputed attribution, or unauthorized discount codes. Expand only after pilot cycles stay auditable and exceptions remain controlled.

Start with the expansion decision you actually need to make#

The first decision is not where you can grow fastest. It is which vertical and country pair you can launch now without creating payout compliance debt. Get that wrong, and early volume can hide messy approvals, weak records, and payout disputes that slow you down later.

Step 1. Choose the launchable slice, not the biggest opportunity#

Start by narrowing the choice to one vertical and a small set of countries you can support operationally on day one. The practical question is whether you can onboard affiliates, approve payouts, and reconcile payments cleanly in that slice before you widen anything.

A good first filter is compliance intensity. Financial services is the clearest example in the source material. Affiliate managers there often spend real time vetting partners and monitoring partner content for risk. If your team cannot review partner claims and referral placements consistently, do not make a highly regulated or claims-heavy vertical your first expansion move. Pick a vertical where the approval burden matches your current team.

Use a simple checkpoint here. Can you explain, in one page, why this market is launchable now? That note should name the vertical, target countries, expected partner type, who owns affiliate onboarding, and who owns payment reconciliation. If ownership is fuzzy at this stage, the launch is not ready.

Step 2. Rank operational constraints before growth signals#

Next, rank candidate markets by the constraints that affect payout compliance first. Privacy pressure matters because affiliate tracking sits directly in the path of data collection and consent expectations. The source material points to GDPR in Europe and CCPA in California as part of the pressure on affiliate programs, alongside platform tracking changes. So your market choice should reflect where your current tracking, consent handling, and recordkeeping are strongest, not where CPMs or conversion rates look most attractive.

Keep privacy and security separate. Privacy is about whether users know data is collected and have permitted its use. Security is about how that data is protected. You need both, but privacy gaps can break attribution decisions, while security gaps can break trust more broadly.

One red flag is enough to stop expansion. If you are still debating how referral links will be tracked or how partner content will be reviewed, do not add more countries yet. Growth signals are easy to find. Evidence is harder.

Step 3. Define success in payout terms you can actually verify#

Your first expansion works only if three things happen together. The first payout is compliant, reconciliation is clean, and your controls are auditable without grinding the team to a halt. Those are better success criteria than clicks, signups, or partner count because they show the program can survive scrutiny.

Make that concrete with a minimum evidence pack for each proposed launch market:

- partner vetting standard and content review owner

- privacy and tracking assumptions that affect attribution

- required onboarding and payout records for affiliates

- payout approval path and reconciliation owner

Verification matters. Before launch, you should be able to trace one sample affiliate from onboarding to approved payout to your reconciliation record without missing documentation. Incomplete documentation can force holds, manual fixes, and disputed payouts. The right rollout sequence is the one your team can prove, not the one with the loudest demand forecast.

If you want a deeper dive, read Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance.

Set scope before you choose any payout model#

Set your operating boundary before choosing payout mechanics. If markets, currencies, and onboarding records are still unsettled, payout model decisions usually create rework in approvals and payout holds later.

Step 1. Lock the launch perimeter. Define the countries for cross-border payouts, the currencies you will pay in, and whether you will pay partners directly or through an affiliate network. Capture budget inputs at the same time: commission payouts, platform or network fees, and program management. If direct vs. network is still unclear, treat model selection as premature.

Step 2. Document required compliance inputs by market. For each market in scope, list the privacy and consumer-protection requirements you need to operate under, plus the identity verification and tax information you plan to collect during onboarding. Keep this tied to payout operations: tracking quality, partner accountability, and attribution records affect whether approvals are defensible.

Step 3. Confirm tax-document readiness before recruitment. Affiliates are generally treated as non-employees, so tax handling should be built into onboarding, not added right before payout. If your program uses US tax forms, decide in advance how IRS W-9 form and IRS W-8 form collection will work, who checks completeness, and when missing or inconsistent forms trigger a hold. Keep launch scope narrow at first: one vertical and a small partner cohort.

Related: Performance Royalties Explained: How PROs Collect and Platforms Distribute Performing Rights Payouts.

Compare payout models by compliance workload and abuse risk#

Choose the payout model your evidence can support today, not the model that looks best in a growth deck. The payable event you define determines what you must identify, assess, monitor, and mitigate across the full partner lifecycle, from onboarding to contract end.

First, standardize model language in your team docs. In one common glossary, PPC is defined as pay-per-call, not pay-per-click, so spell out the payable event explicitly before ops or finance builds controls.

Use this control-first comparison before launch:

| Model label in plan | What must be explicit before launch | Referral-link validation check | Unauthorized discount-code check | Reconciliation check |

|---|---|---|---|---|

| PPC / CPC variant | Exact payable event definition and system of record | Can you trace issued links to approved payout rows? | Can a code change credit after link attribution? | Can ops explain any payout row quickly from raw logs? |

| PPA | Exact action definition and approval state | Is the partner ID preserved from referral to approved action? | Are code rules documented when action credit is assigned? | Can one approved action be tied to one payout rule without manual interpretation? |

| PPI / CPM variant | Exact impression unit and counting source | If links are used, are ownership and redirects auditable? | If codes are present downstream, do they alter credit logic? | Can large-volume counts be reproduced consistently in payout exports? |

| TTAP / two-tier setup | Tier relationship rules and entitlement start/stop conditions | Are referral paths and tier relationships both auditable? | Are code-credit rules consistent across both tiers? | Can tiered entitlements be recalculated without rebuilding history manually? |

Direct rules for rollout:

- If link and attribution validation are weak, do not start with a model that depends on them for payout approval.

- If conversion attribution is already clean and auditable in your stack, prioritize the model that pays on that approved conversion event.

- In early-country launches, keep one model and one tight approval path first; add two-tier scale only after monitoring and reconciliation are stable across markets.

We covered this in detail in FATCA and W-8 Tax Compliance for Platforms: When to Release, Hold, or Withhold Foreign Payouts.

Pick markets using a compliance evidence pack#

Market selection should be a go or no-go evidence decision, not a forecast decision. Do not launch a country until you can show the proof you will rely on for the first payout.

Step 1. Build one country sheet per market#

Use one standardized sheet per market so gaps are visible across countries.

| Country-sheet field | What to capture | Source note |

|---|---|---|

| Payout rails | Payout rails you expect to use | Every material claim should map to a source and a named owner |

| Identity verification requirements | Identity verification requirements you believe apply | Prefer authoritative anchors when available |

| Tax information requirements | Tax information requirements for affiliate onboarding | Treat source quality as part of the evidence |

| Privacy and consumer protection | Privacy regulations and consumer protection laws to review | For U.S.-specific references, a .gov source is an official U.S. government website |

| Evidence tracking | Policy gaps, unanswered questions, source URL, source type, owner, and last verified date | Mark syndicated press releases as promotional |

Treat source quality as part of the evidence, not a footnote. Every material claim should map to a source and a named owner.

Step 2. Set a go or no-go checkpoint around legal exposure#

Make the checkpoint about reviewability. If legal or compliance cannot state the current position on privacy and consumer-protection obligations for a market, keep that market in no-go.

Do not fill evidence gaps with weak substitutes. An OECD Working Paper can help with background framing, but it does not represent official OECD or member-country views. Study aids like Quizlet flashcards are not market-entry authority.

Step 3. Check document readiness before launch approval#

Confirm you can onboard and pay without improvising before launch. Review your affiliate onboarding packet, local terms language, and any IRS W-9 or IRS W-8 collection workflow your program uses.

Run one test affiliate through the flow and confirm you can collect tax information, capture acceptance, and retain records before creating any payout file.

Step 4. Use a traffic-light rule and assign reconciliation ownership#

Launch only on green: evidence complete, acceptable source quality, document readiness confirmed, and a named reconciliation owner. Keep yellow and red markets out of launch sequencing until gaps are closed.

If you want a practical template for that market review, this cross-border compliance checklist is the right next reference.

Build the minimum control stack before first payout#

Do not launch the first payout until you can show, for each line item, why it was earned, approved, and exported. The minimum stack is a practical gate: it should catch fraud risk, partner conduct issues, and payout-record gaps before money moves.

| Control area | What to include | Operational check |

|---|---|---|

| Partner vetting and attribution | Payee profile, accepted terms version, tax-information status, identity-verification status, controlled referral link issuance, and partner-level tracking IDs | Trace activity back to issued links |

| Pre-payout approval logic | Release rules before the first live batch; missing tax information, unresolved identity checks, disputed attribution, and unauthorized discount-code activity trigger explicit holds | Keep holds at the payout-line level with statuses approved, on hold, and released |

| Conduct boundaries and escalation | Prohibited claims, unauthorized code use, required review paths for higher-risk traffic, and assigned escalation ownership across legal, compliance, and ops | Treat abusive conduct risk as a real control requirement |

| Reconciliation dry run | Sample payout trace from request to approval to batch output to ledger/export, plus an evidence pack for each payout decision | No orphaned lines, summary-only totals, or manual overrides without notes |

- Vet partners and lock attribution controls first.

Start with partner vetting before payout mechanics. A payable partner record should include the payee profile, accepted terms version, tax-information status, and identity-verification status. Keep referral link issuance controlled, use partner-level tracking IDs, and make sure you can trace activity back to issued links, because payout logic in performance marketing depends on completed actions and reliable tracking.

- Define pre-payout approval logic with line-level holds.

Set release rules before the first live batch so holds are not ad hoc decisions during operations. Missing tax information, unresolved identity checks, disputed attribution, and unauthorized discount-code activity should trigger explicit holds. Keep holds at the payout-line level and keep status tracking clear (approved, on hold, released) so one bad record does not freeze a full run.

- Set partner-conduct boundaries and escalation ownership.

Write policy boundaries that are easy to enforce: prohibited claims, unauthorized code use, and required review paths for higher-risk traffic. Assign escalation ownership across legal, compliance, and ops before launch. This is especially important in consumer-facing programs where abusive conduct risk must be treated as a real control requirement, not a post-incident cleanup task.

- Prove reconciliation with a dry-run trace before scale.

Run a sample payout trace from request to approval to batch output to ledger/export. The trace should reconcile cleanly with no orphaned lines, summary-only totals, or manual overrides without notes. Keep an evidence pack for each payout decision so disputes can be resolved from records, not reconstructed from memory.

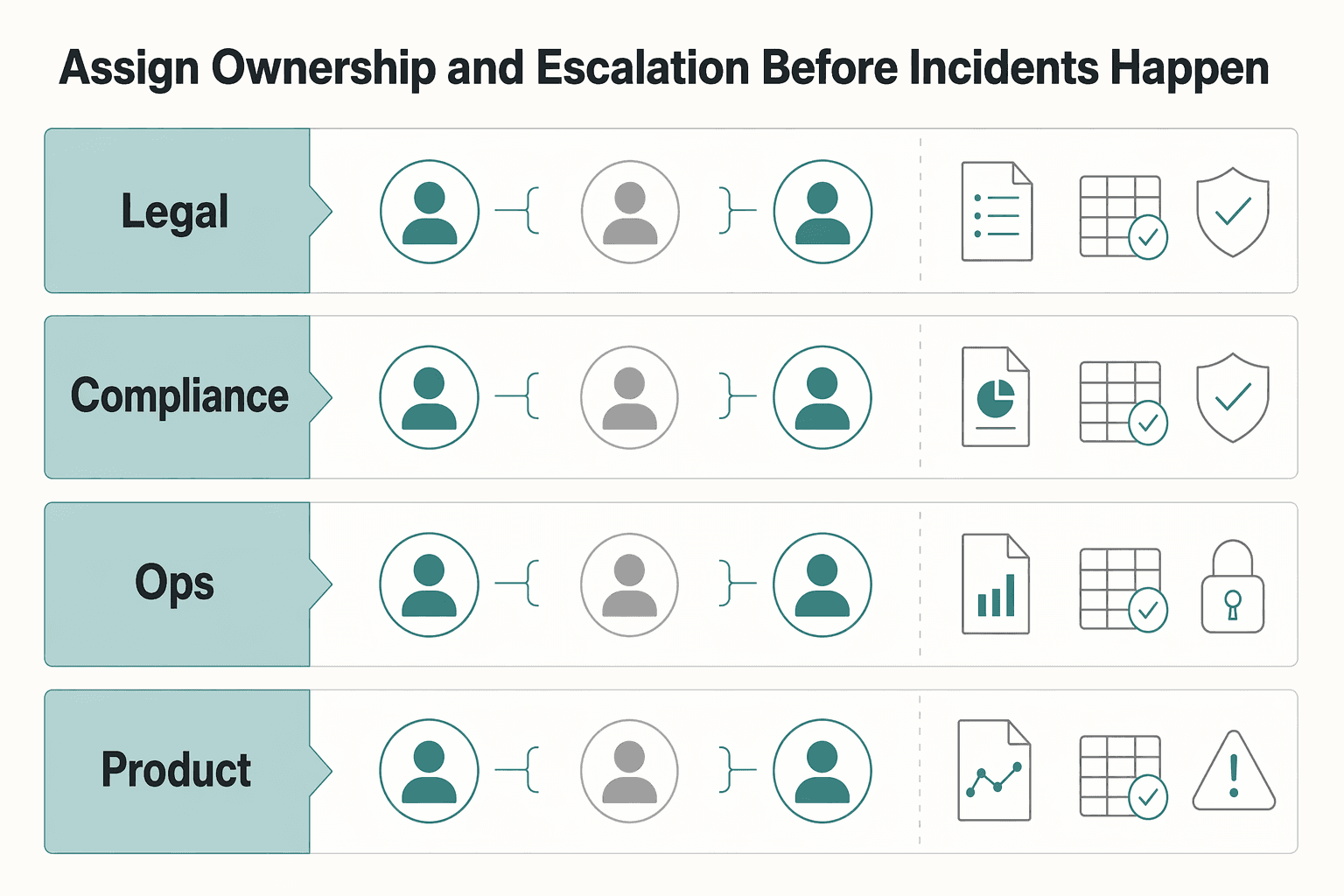

Assign ownership and escalation before incidents happen#

Controls only prevent bad payouts when someone can act as soon as a control trips. Before you scale, assign each incident class one primary owner, one backup, and one evidence standard that can stand up in reconciliation and audit review.

| Function | Primary role | Examples in the article |

|---|---|---|

| Legal | Interprets risk | Consumer protection and deceptive marketing risk |

| Compliance | Defines controls | Control rules, incident classes, and hold or release criteria |

| Ops | Executes payout exceptions | Holds, reruns, and failed global mass payment handling |

| Product | Enforces system gates | Prevents a partner from reaching payable status when required fields such as tax information are missing |

- Map ownership by decision, not by department name. Legal interprets consumer protection and deceptive marketing risk. Compliance defines control rules, incident classes, and hold or release criteria. Ops executes payout exceptions, including holds, reruns, and failed global mass payment handling. Product enforces system gates so a partner cannot reach payable status when required fields, such as tax information, are missing.

The check is simple: for each incident class, name the primary owner, backup owner, and payout-release approver.

- Define incident classes with clear triggers and first actions. Keep the core classes short and explicit: affiliate misconduct, disputed attribution, failed global mass payments, and missing tax information. Each class should have a trigger, an immediate hold rule, and a clear resolution condition.

Route conduct-risk cases to legal and compliance, and route attribution or payout-operation failures to ops and product so teams can verify tracking, approval, and payout records quickly.

- Set explicit escalation paths with internal time targets. High-risk cases in financial services and high-volume markets should escalate in minutes, not days. Document who freezes payouts, who blocks further release, who determines whether a control failed, and who assesses potential consumer protection or regulatory exposure.

Keep these as internal operating targets, not universal legal requirements, and test the path with drills before launch.

- Require an evidence pack for every escalation. Retain the partner record, accepted terms version, identity verification status, tax information status, attribution or referral record tied to the payout, payout batch status, reconciliation export, internal approval notes, and final resolution.

This is what makes decisions defensible. Weak governance increases risk and also hurts performance because teams spend time reconstructing decisions instead of resolving incidents.

For a step-by-step walkthrough, see VAT and SEPA: How European Platforms Combine Tax Compliance with Automated Euro Payouts.

Execute rollout in phases with hard checkpoints#

Roll out in phases, and move forward only when your operating checkpoints are consistently met. In payout compliance work, launch volume is less important than whether back-end operations stay measurable and controllable.

Step 1. Start narrow, then add complexity deliberately. Begin with one market and one payout model for the first live cycle. Expand markets only after that pilot is stable, then add more complex payout configurations. This sequence helps you isolate what changed when issues appear.

Step 2. Gate each phase with objective checks. Treat each phase as a controlled rollout with tracked metrics and variables. Do not advance on volume alone; advance when records are complete, statuses are explainable, and reconciliation is clean.

| Checkpoint | What to verify before moving on | Common red flag |

|---|---|---|

| Onboarding completion | Required partner fields are complete, terms acceptance is captured, and payee setup is usable for payout decisions | Partners are active but cannot be paid because setup is incomplete |

| Identity verification status | Pass/fail/pending trends are reviewed by market and partner cohort | Pending reviews accumulate and require ongoing manual cleanup |

| Required tax-record readiness | Tax documentation required by your process is present and tied to the payee record used for approval | Documents exist but are disconnected from payout approval records |

| Reconciliation completion | Approved payout items, batch status, and reconciliation outputs match without unexplained gaps | Payout lines cannot be traced end to end |

Step 3. Pause expansion when exceptions outpace resolution. If exception queues grow faster than your team resolves them, stop adding markets and tighten controls. That usually signals an operations-capacity issue, not a market-opportunity issue.

Step 4. Define exit criteria before each phase starts. Set clear exit criteria in advance so readiness is explicit. Use those criteria to decide progression, and hold the phase when exception handling is not under control. This keeps teams from mistaking higher volume for operational readiness.

Handle common failures without breaking trust#

When a payout incident shows up, contain it first and communicate quickly. Trust usually breaks when teams keep paying through uncertainty or go silent during review.

Step 1. Freeze only affected payouts and classify the failure. Pause only the related payee records, payout batch items, or corridor, and label the issue consistently: invalid affiliate referral links, unauthorized discount codes, payout delays, or missing tax information. A clear label set keeps ops, compliance, and legal aligned. The FDIC II-14 violation-codes model (chapter last updated December 2024) is a practical reference for this kind of structured classification.

Step 2. Re-verify identity, correct records, rerun reconciliation, then resume. Use the same sequence every time: confirm identity verification status, fix the source record, rerun payment reconciliation, and release only after the trace is clean. Your check is straightforward: affiliate ID, payout approval, payout batch, and reconciliation export should match without orphaned lines. Collected documents that are not linked to the payable entity are a common failure pattern, especially after rushed onboarding.

Step 3. Communicate holds with facts, not suspicion. Tell the affiliate exactly what is paused, what record is missing or under review, and what they need to submit or confirm. Internally, keep one incident owner and one written status trail for cross-border holds so finance, ops, and support stay aligned. Unclear communication and rushed onboarding are known drivers of affiliate-program errors and trust loss.

Step 4. Close with one control update before the next cycle. An incident is not fully closed when funds move; close it when one preventive control is added. That can be tighter referral-link validation, stricter discount-code approvals, a required tax-information field, or a pre-payout identity gate. Nevada Regulation 5 reinforces the operating discipline here: it explicitly lists reports of violations (5.055) and production of records (5.060), even where that rule is not the one governing your program.

You might also find this useful: How to Handle Unclaimed Payouts: Escheatment Rules and Dormant Funds Compliance for Platforms.

Move first with control depth, then with market breadth#

Treat this as a sequencing decision: build control depth first, then add market breadth only after your controls hold up in live payouts.

- Confirm a narrow launch scope before onboarding opens.

Pick one lane you can operate with clear ownership, defined checks, and complete payout readiness. If ownership or required checks are still unclear, treat that lane as no-go for this phase. Verification point: You can name the reconciliation owner and show the current onboarding packet for each launch market.

- Choose the payout model you can verify cleanly, not the one with the loudest growth case.

There is no universal "easy" model. Use the model where attribution, monitoring, and approval reasons are auditable line by line, then evaluate growth with CAC and LTV together before widening scope. Failure mode: Volume looks strong, but approvals become disputed because evidence is weak.

- Lock onboarding and tax-document readiness before earnings accrue.

In this context, affiliates are non-employees, so records should be categorized accurately and aligned with tax reporting compliance. Require complete, traceable records before payout approval so affiliate, payee, and tax-document status stay in sync.

- Implement minimum controls before the first live batch.

Set partner vetting, content monitoring, pre-payout approval logic, payout status tracking, and a response path for unauthorized discount codes. This is where country-level payout readiness becomes an operational gate.

- Run pilot payouts, then expand only after checkpoints pass.

Pilot one market and one model, then trace sample lines from referral/transaction evidence to approval and export or ledger entry. Expand only when exceptions are handled consistently; if holds or document gaps outpace resolution, pause breadth and return to control depth.

Related reading: Gruv Platform Payments for Global B2B Payouts and Compliance.

Frequently Asked Questions

What does affiliate compliance mean in performance marketing payouts?

Affiliate marketing is a performance model where publishers promote a product or service and earn commission on resulting sales. In this context, compliance means using documented processes to show promotions and payouts follow your rules. In practice, that includes vetting affiliates, monitoring their content, and respecting privacy requirements.

Which payout model is easiest to operate compliantly: PPC, PPA, PPI, or TTAP?

There is no credible one-size-fits-all winner in the source material here, so do not force a ranking. Pick the model you can verify cleanly with your current controls, especially attribution, content monitoring, and reconciliation. If the approval reason is fuzzy or often disputed, that model is not the easy one for your team.

What controls are non-negotiable before we send the first affiliate payout?

Based on the source material here, the non-negotiables are clear processes to vet affiliates, monitor their content, and account for privacy requirements. Beyond that baseline, define your approval and payout controls with legal and compliance owners for your specific market.

How do we scale global mass payments without losing compliance visibility?

As volume grows, keep affiliate vetting and content monitoring consistent across markets, and make privacy requirements explicit by market. Use payout review workflows that preserve enough detail for checks and follow-up instead of relying only on high-level summaries.

What documentation should affiliates submit before payout approvals start?

The grounding here does not define a universal required document packet for affiliates. Set documentation requirements with legal and compliance before payouts begin, and align them to each market or vertical.

How should we choose launch countries when cross-border payout constraints differ?

Launch where your monitoring and privacy processes are already operational, and pause markets where ownership or review steps are still unclear. For regulated sectors, remember the SEC marketing compliance FAQs updated Jan. 15, 2026 are staff views with no legal force or effect, and the Commission has neither approved nor disapproved them.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- advocacy.sba.gov/wp-content/uploads/2019/07/How-to-Comply-wit...trusted

- consumerfinance.gov/compliance/supervisory-guidance/policy-state...trusted

- fac.gov/assets/compliance/2025-Compliance-Supplement...trusted

- fdic.gov/consumer-compliance-examination-manual/ii-14...trusted

- federalregister.gov/documents/2024/11/15/2024-25534/negative-opt...trusted

- gaming.nv.gov/siteassets/content/home/features/regulation5...trusted

- law.lis.virginia.gov/vacodefull/title59.1/subtitle/parttrusted

- oecd.org/content/dam/oecd/en/publications/reports/202...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance

Invisible payouts should make life easier for contractors without hiding the controls your team needs. Contractors should get a predictable, low-friction flow, while internal teams can still enforce and document payout decisions when needed. If you run contractor payouts at scale, you need both outcomes at once. We recommend treating every easy payout as a controlled release path your team can replay later.

How PROs Collect Performance Royalties and How Platforms Distribute Payouts

Treat this as an infrastructure decision, not a music-rights explainer. If you cannot connect PRO collection to a payout process you can verify, reconcile, and audit, you are not ready to ship a royalties product, no matter how strong the demand story looks.

Country-by-Country Launch Rules for Platform Payout Compliance

Treat each new payout country as a go or no-go decision. It may be blocked by law, blocked by operations, or cleared only with conditions. This guide helps compliance, legal, finance, and risk teams make that call early, assign ownership, and keep an evidence trail that holds up later.