Quick Answer

Pick Net-30 only when your team can track invoice intake, acceptance, and settlement timestamps end to end. Move to Net-15 for cash-sensitive supplier groups, and use Net-60 only when the extra DPO materially helps and your exception lanes are already owned. For 2/10 Net 30, measure settlement date rather than release date, because day-10 misses erase the discount. If approval queues or reconciliation lag are unstable, keep the base term simpler and tighten operations first.

Start With Cash Flow and Execution Reality#

Choose payment terms based on what your platform can execute reliably, not on the longest term you can negotiate. Moving to longer terms such as Net-30 or Net-60 can improve buyer working capital by keeping cash in the business longer, but it also makes suppliers wait longer to get paid and can strain the relationship. If you cannot execute the term you negotiate, your supplier relationship absorbs the gap. We see the damage when teams negotiate the longer window before they can prove invoice timing and approval discipline.

| Context | Timing rule | Qualifier |

|---|---|---|

| EU commercial transactions | Contractual payment periods are generally capped at 60 calendar days | Unless explicitly agreed and fair |

| EU public-authority payment timing | Payment within 30 days | Stricter than general commercial timing |

| UK public-procurement context | From 1 October 2025, an average of 45 days or fewer | Prompt-payment requirements tighten |

Net terms are deferred payment timelines in a trade-credit agreement. Net-30, Net-60, and Net-90 are day-count windows to pay the full invoice amount. On the buyer side, the core metric is Days Payable Outstanding, or DPO, the average time it takes to pay accounts payable. On the supplier side, pressure shows up as Days Sales Outstanding, or DSO, the average time it takes to turn credit sales into cash.

That is why there is no universal answer across common net terms. Higher DPO can help near-term cash management, but it can also increase supplier-side risk and lead to tighter credit or more friction.

This guide gives you practical checkpoints to choose the term structure that fits your operating reality. Use them to decide what your team can promise now and what it should hold back until AP, finance, and payout controls are ready:

- your cash position and working-capital pressure

- your execution capability across AP, approvals, and reconciliation

- your supplier mix and sensitivity to delayed cash receipt

Scope: this is an operational comparison for platform teams, not legal advice. Net-30 is common, but terms are usually tailored to operating and cash-flow needs, and regional rules can narrow your options. In EU commercial transactions, contractual payment periods are generally capped at 60 calendar days unless explicitly agreed and fair. EU public-authority payment timing is stricter, with payment within 30 days. In the UK public-procurement context, prompt-payment requirements tighten from 1 October 2025 to an average of 45 days or fewer.

The core question for the rest of this article is simple: which term can your platform execute consistently without creating avoidable risk for suppliers or for your own operations? Related reading: How Platform Teams Get Freelancers Paid Faster Beyond Net-30.

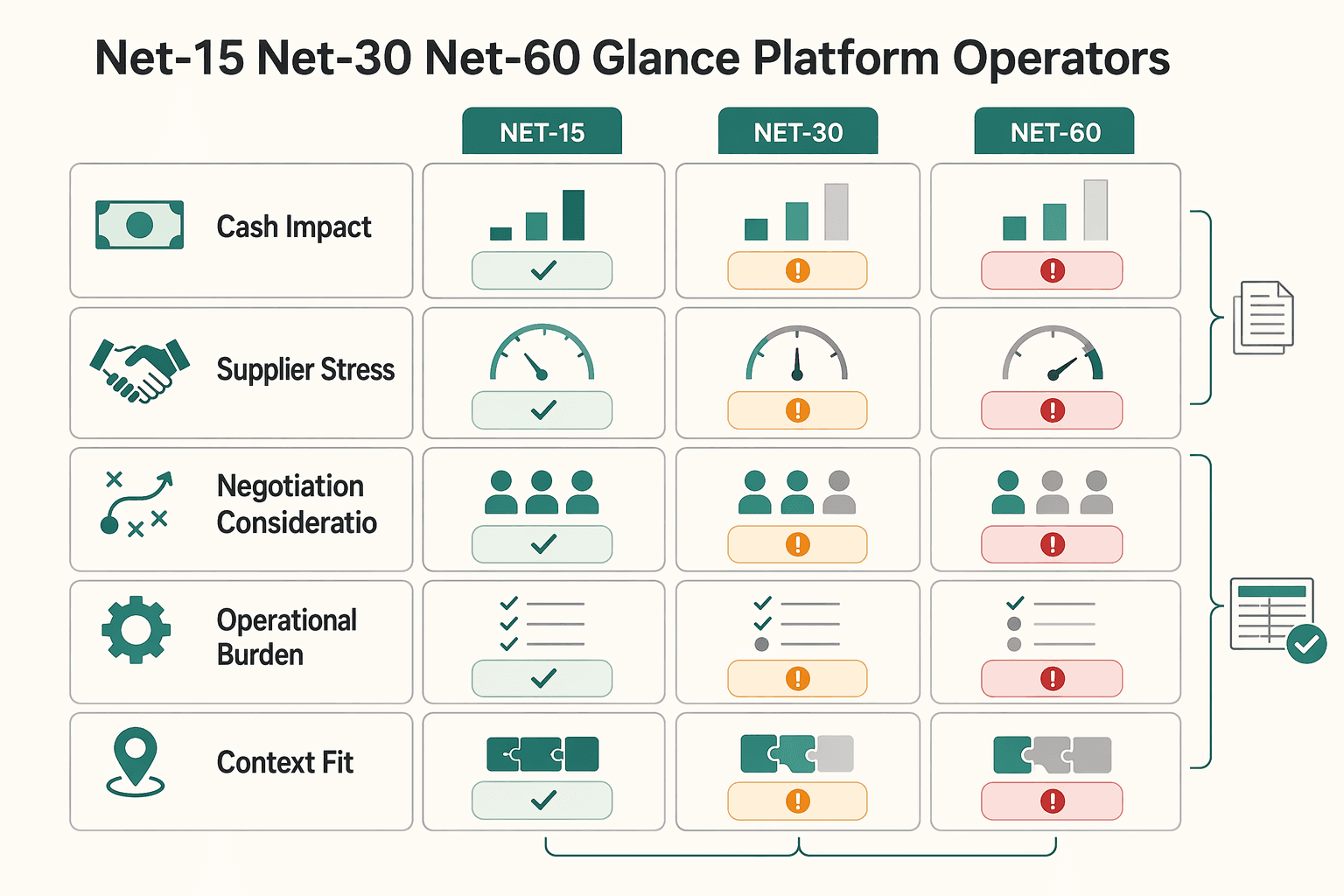

Net-15 Net-30 Net-60 at a glance for platform operators#

Start with execution reality. Set terms suppliers can support and your AP process can execute consistently, then adjust for working-capital goals. We recommend starting from the shortest term your process can hit cleanly, then extending only when your evidence trail stays intact. In practice, we would not extend terms until your invoice and approval timestamps stay stable across the full flow.

| Comparison point | Net-15 | Net-30 | Net-60 |

|---|---|---|---|

| Cash impact (DPO/DSO) | Shorter payment windows generally mean less DPO extension for the buyer and less DSO extension for the supplier. | Midpoint cash-timing impact between shorter and longer terms. | Higher DPO extension for the buyer; moving from Net-30 to Net-60 lets buyers hold cash longer while supplier receivables are delayed and DSO extends. |

| Supplier stress | Usually lower stress because cash arrives sooner. | Can be workable when approvals and payment scheduling are predictable. | Can increase supplier cash-flow strain unless suppliers can absorb longer collection cycles. |

| Negotiation considerations | Often aligns better when suppliers prioritize faster cash conversion. | Often used as a midpoint, but terms still depend on liquidity needs and negotiating power. | May require stronger buyer leverage and supplier capacity for longer collection cycles. |

| Operational burden in Accounts Payable (AP) | Short windows leave little room for slow intake, approval, or scheduling. | Works best when invoice-to-approval cycle time is measured and controlled. | Execution discipline still matters; longer terms do not remove supplier wait-time pressure. |

| Context fit (not a universal rule) | More viable when supplier liquidity needs are a priority. | Commonly used as a baseline trade-credit term. | More viable when industry norms and negotiating power support longer trade-credit cycles. |

Fallback option: 2/10 Net 30 (Early Payment Discount) | Often less relevant when a short base term is already in place. | Keep a 30-day base term, offer 2% discount if paid within 10 days, otherwise full amount due in 30 days. | Can help balance working-capital needs if suppliers resist longer base terms and AP can reliably execute the 10-day discount window. |

Treat this table as a decision aid, not a rulebook. Industry norms, liquidity needs, and negotiating power still shape what is realistic.

One operating rule before you use discount structures: if AP and reconciliation are inconsistent, early-pay discounts are hard to capture reliably.

Start with the cash math before you negotiate#

Start with the numbers, not the ask. Push for longer terms only if they create meaningful near-term working-capital relief and your AP process can execute them reliably.

Working capital is current assets minus current liabilities. In payment terms, the tradeoff is straightforward: longer terms extend buyer float through higher DPO and delay supplier cash conversion through higher DSO. If moving from Net-30 to Net-60 does not materially improve your near-term cash position, it may not justify added supplier relationship pressure.

Same invoice, different cash outcome#

Assume one approved invoice is received and accepted on Day 0, and only the term changes.

| Same approved invoice | Net-15 | Net-30 | Net-60 |

|---|---|---|---|

| Buyer pays by | Day 15 | Day 30 | Day 60 |

| Buyer cash stays on hand for | 15 days | 30 days | 60 days |

| Buyer-side DPO effect | Shorter payable window | Middle ground | Longest payable window |

| Supplier receives cash by | Day 15 | Day 30 | Day 60 |

| Supplier-side DSO effect | Shorter collection cycle | Moderate collection cycle | Longest collection cycle |

| Relationship pressure | Can be lower | Often manageable if predictable | Can be higher if supplier is cash-sensitive |

In plain terms, moving from Net-30 to Net-60 doubles the buyer hold period on the same invoice while pushing the opposite timing effect onto the supplier. Net-60 can improve your liquidity in the near term, but it can also increase supplier cash strain.

The second-order effect operators feel later#

This cost often shows up after the contract is signed as higher coordination load and more pressure in supplier relationship management. You may reduce near-term cash pressure while increasing the service burden on finance and ops.

That does not make longer terms wrong. It means you should count that burden in the decision and plan for clearer status visibility and stronger AP execution controls.

Check execution before you promise the window#

If your process cannot reliably move invoices through AP, negotiated terms are not an execution plan. Check these stages before you commit:

- invoice receipt

- invoice matching

- approval routing

- payment origination

- reconciliation and reporting

Make sure you can see timestamps and clear owners across each stage. If you cannot, do not assume you can consistently meet negotiated windows or capture early-payment discounts. Final rule for this section: do the cash math first, then validate execution readiness.

Pick your baseline term by payout model and supplier mix#

Set your baseline by supplier cash profile and execution reality, not buyer preference alone. Contractor-heavy cohorts often need a shorter starting point. Mixed marketplaces may use Net-30 as an initial middle ground. Net-60 is more defensible when counterparties can absorb longer cycles and exception handling is explicit. If your supplier base depends on predictable cash, treat that as a control input, not a side note in procurement. We would rather start with a clean shorter term than ask your suppliers to finance your process gaps.

| Supplier mix | Baseline starting point | Why it usually fits | When longer terms get risky |

|---|---|---|---|

| Contractor-heavy network | Shorter terms (often Net-15 or Net-30, depending on payout reliability) | Payment timing is often critical for smaller, cash-sensitive suppliers | In settings with weekly payroll obligations (for example DBRA-covered work), defaulting to Net-60 can push financing risk downstream |

| Mixed marketplace | Net-30 as a starting middle ground, then adjust by supplier profile | Balances buyer float with supplier cash realities across varied cohorts | A single term can fail when many suppliers are cash-sensitive or geographically concentrated |

| Enterprise vendors | Net-60 only as a negotiated baseline with clear exceptions | Some counterparties can support longer terms under formal controls | PO controls and administrative friction can make actual payment timing much later than the stated term |

The contractor-heavy case is often where overreach shows up first. In DBRA-covered federal construction work, contractors and subcontractors must pay covered workers weekly and submit weekly certified payroll records, so Net-60 can shift real financing pressure onto the supplier side.

That is also where late-payment risk spreads. Delays can cascade through supply chains, especially when smaller suppliers depend on incoming cash to meet their own obligations.

Use four checks to decide whether your baseline is defensible:

- Concentration risk: If spend is concentrated in a few suppliers or geographies, longer terms can increase operational exposure.

- Supplier cash sensitivity: If timely customer payments are critical to supplier cash flow, aggressive terms raise execution risk.

- Process friction: Complex approval flows, administrative errors, or strict PO controls can turn a nominal Net-60 into a much longer real cycle.

- Legal guardrails and consent: In EU B2B contexts, terms above 60 days need explicit, fair agreement; unilateral 120-day terms have been held unlawful.

For enterprise counterparties, Net-60 can work when exceptions are explicit and enforced. Without that, controls like approvals and PO requirements can turn a documented term into delayed cash in practice.

Negotiate the full payment terms clause not just the day count#

Day count is only part of enforceability. If your payment terms clause does not define trigger events, acceptance, defect handling, and payment method, a stated Net-30 or Net-60 can still slip in practice.

| Clause element | What to define in the Trade Credit Agreement | Why it matters | Red flag |

|---|---|---|---|

| Start date trigger | State whether due date runs from proper-invoice receipt, acceptance, or the later of the two | Payment timing is often tied to invoice quality and acceptance, not the label alone | "Net-30 from invoice date" with no rule for missing fields, missing PO, or unaccepted work |

| Acceptance criteria | Name who accepts, what evidence counts, and what milestone closes review | Undefined acceptance lets approvals drift and extends real payment time | "Payable after review" with no owner, no acceptance event, and no deadline |

| Dispute window | Define how defects are returned, what stops the clock, and what restarts it | Without a documented path, disputes become open-ended | Rejections happen in scattered email/chat with no receipt timestamp |

| Approved payment method | Specify ACH, wire, or other approved method, plus setup prerequisites | Method and setup affect whether payment can be made on time | Contract says Net-30, but bank setup is incomplete or AP defaults to a slower method |

Fix the trigger before you argue about Net-60#

Use a clear trigger model first, then negotiate the day count. A practical structure is "later of proper-invoice receipt or acceptance." This mirrors a U.S. federal approach that anchors due date to the 30th day after proper invoice receipt or the 30th day after acceptance, whichever is later.

If acceptance is ambiguous, do not extend invoice payment terms yet. Agree on an acceptance-by-default timeline first. In the EU framework, acceptance or verification generally should not exceed 30 calendar days unless expressly agreed and not grossly unfair. Pairing long payment terms with open-ended acceptance creates predictable delay risk.

A quick operational check: make sure your ERP and AP flow capture invoice received, accepted or rejected, and returned-for-correction timestamps. If you cannot prove those events, enforcement and auditability both weaken.

Trade term length for something concrete#

Do not concede longer terms unilaterally. If the counterparty asks for Net-45 or Net-60, trade for measurable value: tighter scope and acceptance criteria, volume or forecast commitments, or defined discount or early-pay rights.

| Concession | How it is framed | Example from the text |

|---|---|---|

| tighter scope and acceptance criteria | Measurable value to trade for longer terms | Fixed acceptance milestones |

| volume or forecast commitments | Measurable value to trade for longer terms | Quarterly volume commitments |

| defined discount or early-pay rights | Measurable value to trade for longer terms | Named right to request earlier payment on approved invoices |

| preferred supplier status | Weak concession | Vague |

Weak concessions are easy to absorb. "Preferred supplier status" is vague. Fixed acceptance milestones, quarterly volume commitments, or a named right to request earlier payment on approved invoices are specific and testable.

Handoff to Accounts Payable (AP)#

Execution risk starts after signature, so the handoff needs explicit ownership. A practical internal handoff pack can include:

- signed clause set

- exception matrix for disputed invoices, missing fields, and unaccepted work

- named approval owner in AP

Also define what a proper invoice must include. U.S. federal prompt-payment rules use a 7-day return expectation for improper invoices. Even where that exact window does not govern, it is a useful internal discipline for fast defect notice.

Stretch term length only after trigger, acceptance, defect path, and payment method are documented and owned. If AP cannot execute from the handoff pack without interpretation, keep terms shorter until it can.

Related: Net Payment Terms for Platforms: How to Offer Net 30 60 90 and When to Use Each.

Use early payment discounts only when execution is reliable#

Use an early payment discount only if your AP process can consistently move from proper-invoice receipt to approval to settled payment inside the discount window. If that execution is not reliable, keep terms simple with base Net-30. We recommend proving the 10-day path with real invoices before you market the discount as standard. If your pilot misses the window, we treat that as a control failure before we call it a pricing strategy.

2/10, n/30 creates value only when the 10-day window is operationally real: 2% off if paid within 10 days, otherwise the full amount is due in 30 days. That depends on controls you can prove, not just contract wording.

| Evaluation point | Discount creates value when | It becomes noise when | Verification checkpoint |

|---|---|---|---|

| Invoice start point | Invoice date and proper-invoice receipt are captured at intake and tied to timing triggers | Dates are late-entered or disputed | Confirm invoice date and actual receipt date are captured at time of receipt |

| Approval path | Acceptance or approval owners are clear and queue aging is visible | Invoices stall in inboxes with no bottleneck visibility | Check aging by approver and whether receiving documentation reaches payment operations by the 5th working day after acceptance or approval |

| Payment execution | Payment settles by the discount date | Team tracks release date, but settlement lands after day 10 | Track settlement date, not initiation date |

| Reconciliation | Settlement confirmation is prompt and timing can be verified | Confirmation lags and on-time discount use cannot be verified | Measure lag from release to settlement confirmation |

| Exception handling | Improper invoices are returned quickly with timestamped records | Defects drift and deadline disputes follow | Check return timeliness, for example, a 7-day discipline |

Do not treat payment release as payment completion. For EFT, timing is based on settlement date, so a day-10 release that settles on day 11 misses the window. Taking the discount after the deadline creates penalty exposure, not savings.

Also confirm front-end reliability: payment is tied to a proper invoice and satisfactory performance, so weak intake or slow approval forwarding breaks discount timing before settlement. A practical control check is whether approval and receiving documentation reaches payment operations by the 5th working day after acceptance or approval.

If these controls are weak, remove discount complexity and keep base Net-30 in the payment terms clause until intake timestamps, approval visibility, and settlement controls are dependable.

For a step-by-step walkthrough, see Indian Freelancer Payment Analysis That Protects Net INR.

Build exception rules before rollout#

To keep invoice payment terms enforceable in production, define exception lanes before the first invoice goes live. Each exception type needs a named owner, a documented trigger, and a response SLA, or agreed Net-15, Net-30, and Net-60 terms will drift into ad hoc escalation.

| Exception type | Trigger to enter lane | Decision owner | What must be recorded | Timing rule that matters most |

|---|---|---|---|---|

| Disputed or improper invoice | Missing required fields, pricing mismatch, acceptance dispute, unsupported charge | AP or designated invoice review office | Exact defect reason and return notice | Under 5 CFR 1315.4, return improper invoices no later than 7 days after receipt |

| Failed onboarding or identity review | You cannot form a reasonable belief about customer identity, or entity ownership is unclear | Compliance owner for KYC / AML review | Identity check result, document deficiency, escalation outcome | Set an internal SLA and prevent silent aging while review is unresolved |

| Missing tax documentation | Required taxpayer information is incomplete, invalid, or treaty support is absent | Tax ops or finance owner | Missing-document notice, withholding decision, status timestamp | Resolve before release logic, because backup withholding can be 24 percent and some U.S.-source payments to nonresident aliens may be withheld at 30% unless treaty support applies |

A high-risk lane is compliance gating. CIP requires risk-based identity verification and explicitly covers cases where you cannot form a reasonable belief that you know the customer's true identity. For legal entities, your controls should also capture beneficial-owner verification, meaning the natural person who in the end owns or controls the customer.

Use the invoice dispute lane as your operating template: a designated review office, defect-specific rejection reasons, and the 7-day return discipline. The quality check is whether the return message lists every payment-blocking defect, not just "invoice rejected."

Silent aging is the common failure mode. Require a case record for every exception with intake timestamp, owner, reason code, requested documents, and final disposition so terms stay enforceable instead of aspirational.

Before you lock Net terms, pressure-test exception SLAs and approval states against your real payout and compliance flow in the Gruv docs.

Sequence implementation across product finance and engineering#

Run this in a fixed order: contract signoff, AP configuration, payout routing, then reporting and reconciliation. If you build payout timing before finance locks the payment terms clause and AP state model, terms that look clear in contract can fail at validation, approval, or release. If you reverse that order, you make engineering carry policy ambiguity that finance should have resolved first. We recommend making finance own the clause logic before engineering automates release timing.

| Implementation stage | What to lock | Minimum data/control | Failure if skipped |

|---|---|---|---|

| Contract signoff | Final payment terms clause, clock-start trigger, dispute handling, payment method, jurisdiction-specific default or cap handling | Signed clause, approved term-code mapping, exception owner | AP and engineering implement timing assumptions that do not match the contract |

| ERP/AP configuration | How terms are represented and scheduled in AP | Term code, Terms Date, validation rules, hold rules, approval routing | Recalculated due dates, blocked invoices, or incomplete approval paths |

| Payout routing rules | Eligibility event and disbursement path | Retry-safe eligibility logic, destination mapping, duplicate protection | Duplicate, late, or blocked disbursements under retries or out-of-order events |

| Reporting and controls | How execution is proven against the negotiated term | Approval history, settlement records, reconciliation logs, exception outcomes | No defensible proof that promised timing was met |

Start with contract definitions, not payout code#

Payment timing becomes operational only when contract language is converted into AP-ready fields. For example, AP scheduling depends on Terms, Terms Date, and invoice amount, and a Net-30 due date is calculated 30 days after Terms Date. Decide the clock-start trigger at signoff, then pass one approved definition to AP and engineering.

Jurisdiction handling also belongs here. UCC 2-310 sets a default timing rule unless parties agree otherwise, and the EU framework references a 60 calendar day contractual cap unless expressly agreed. Set this at signoff, not during implementation.

Configure AP around explicit state transitions#

After signoff, map terms to invoice objects and state transitions. At minimum, store the term code on the invoice, set Terms Date, and define approval and hold states that gate payment.

Validation and approval need to be first-class controls. Invoices must validate before payment or accounting, validation can place holds, and approval actions should create explicit status transitions. Your checkpoint is simple: can you name the exact AP state where payment scheduling becomes eligible, and can you show when it changed?

If terms can be edited after ingestion, treat that as controlled risk. Updating terms can recalculate scheduled payment, so actor-and-timestamp audit history should be captured.

Make payout execution retry-safe and reconciliation-driven#

Engineering should implement payout release only after AP states are stable. Idempotent requests are required to prevent duplicate side effects during retries, but they are not enough on their own.

Your payout layer should combine:

- idempotent payment-creation writes

- webhook handlers that tolerate duplicate deliveries and retries, including multi-day retry windows

- reconciliation to source-of-truth settlement records, not event-order assumptions

Event delivery can duplicate and arrive out of sequence. Reconciliation is what confirms money movement, not just event processing.

Define the evidence pack before launch#

Before rollout, require an evidence pack per invoice or payout case:

- approval history

- field-change audit logs, with user and timestamp

- settlement records

- exception outcomes

Then test one cohort end to end:

- Confirm term code and

Terms Dateproduce the expected due date. - Confirm invoices move through validation and approval without unresolved hold dead ends.

- Confirm final settlement reconciles to AP and bank or payment-ledger records.

Broken handoffs between these stages can cause failures even when the day-count setting is correct.

Handle cross-border constraints before they break payment terms#

Cross-border prerequisites should gate payout promises, not just onboarding checklists. Do not promise accelerated terms until tax and identity artifacts are complete enough for payout eligibility. Net-15 in contract does not guarantee release timing if W-8BEN, W-9, VAT validation, or KYC is still pending.

| Prerequisite | What it gates | What breaks if incomplete | Contract or policy rule |

|---|---|---|---|

Form W-9 | U.S. taxpayer identification for information-return reporting | Missing or incorrect TIN can trigger backup withholding at 24% on certain payments | Do not offer accelerated payout until TIN collection and validation status are complete |

Form W-8BEN | Foreign-status withholding or reporting documentation when requested by payer or withholding agent | Insufficient documentation can trigger 30% chapter 3 withholding on amounts subject to that regime | Treat foreign tax forms as payout prerequisites, not post-payment cleanup |

Value-Added Tax (VAT) check via VIES | Validation of EU cross-border VAT registration status | Unverified status can lead to wrong VAT assumptions and downstream rework | Validate before applying VAT treatment assumptions; do not treat VIES alone as final tax treatment |

KYC / identity verification / CIP data | Account onboarding and ability to enable charges or payouts | Invoice approved, payout still blocked because account is not eligible | If identity artifacts are incomplete, keep payout release blocked even if AP timing continues |

The operating rule is straightforward: if tax or identity documentation is incomplete, do not commit to faster terms that imply payout can bypass KYC or required identity controls. Verification requirements vary by country and capability, so contract timing should be policy-gated where local verification or tax setup is still pending.

Keep invoice due logic separate from payout eligibility. You can calculate due date from Terms Date in AP while contract and policy reserve disbursement until onboarding, tax, and identity controls are satisfied.

What to verify before offering shorter terms#

- tax form status by payee type:

W-9for U.S. payees,W-8BENwhen requested for foreign payees - identity status tied to payout capability, not just account creation

- VAT validation path for EU counterparties, including jurisdiction-specific exceptions

- withholding and reporting flags on the vendor record before invoice approval is treated as payment-ready

VIES is a search engine, not a database, and jurisdiction paths differ. For example, UK (GB) VAT number validation ceased in the EU VIES VoW service on 01/01/2021, so one uniform EU VAT-check assumption can fail operationally.

Finance checkpoint before year-end pain#

Before promoting faster terms, confirm invoice timing aligns with withholding and reporting obligations. If Form 1099-NEC is required, the payer must furnish the recipient copy by January 31, so vendor master data, TIN status, withholding flags, and payment history must reconcile in time.

Keep cross-border commitments conservative until one live cohort has a complete evidence pack: tax-form status, KYC status, VAT validation result where relevant, withholding flags, approval history, and final settlement records. If those controls are incomplete, keep standard terms and make release timing explicitly conditional on compliance completion.

For a deeper dive, see Net-30 Payment Terms for Platforms: How to Set Vendor Payment Terms Without Killing Contractor Cash Flow.

Red flags that make your negotiated terms fail in practice#

Many failures happen after signature, when execution does not match what you negotiated. If your payment terms clause leaves acceptance vague, depends on manual AP, or lacks a dispute path, Net-30 or Net-60 can fail operationally before the contract timeline says it should.

| Red flag | Grounded detail |

|---|---|

| Vague acceptance criteria | Nonconformance questions can stall payment and trigger rework or dispute handling |

| Manual AP | Top-performing teams can receive an invoice and schedule payment in about 2.8 days, while slower teams take a week or longer |

| Mismatch risk | Pushing Net-60 while loading terms with risk allocation without a balancing trade can backfire commercially |

| Frequent reconciliation breaks | They can threaten payment accuracy or close timing |

Vague acceptance criteria can be an early failure signal. If an invoice can be submitted but acceptance is not clearly defined, nonconformance questions can stall payment and trigger rework or dispute handling. Before rollout, make sure your trade credit agreement or clause set defines the acceptance standard, the event that starts the invoice payment terms clock, and who can formally raise nonconformance or a dispute.

Manual AP is the next red flag because terms are only as strong as receipt-to-approval-to-scheduling execution. Top-performing teams can receive an invoice and schedule payment in about 2.8 days, while slower teams take a week or longer. If your process is still in the slower range, treat tighter windows and structures like 2/10 Net 30 as execution risk until routing, timestamps, and reconciliation are reliable.

Mismatch risk also breaks terms in practice. If you push Net-60 while loading terms with risk allocation without a balancing trade, terms can backfire commercially. If you need longer terms, pair them with clear tradeoffs such as scope clarity, volume commitment, or discount options.

Use a go or no-go check before launch, and pause to reset terms if these exceed your operating tolerance:

- exception volume rises after contract handoff

- dispute lag has no clear owner or keeps invoices open

- reconciliation breaks are frequent enough to threaten payment accuracy or close timing

If those signals are unstable, fix execution first and renegotiate second.

Conclusion#

The right term is the one your platform can execute consistently without putting avoidable cash pressure on suppliers or weakening control. A longer window helps only if your process can start the clock correctly and release payment as agreed. If you have to choose between a slightly longer float and a cleaner execution path, we would pick the path your team can prove every month.

Decision order matters more than day-count debates. Set the baseline term from your liquidity goals and supplier realities, then define the clause mechanics: what qualifies as a proper invoice and what performance conditions must be met before payment. After that, confirm finance, product, and engineering can run those rules in production.

Execution discipline is the difference between negotiated value and realized value. Signed terms do not enforce themselves. If you cannot evidence proper invoice receipt, contract-performance checks, and settlement timing, you are assuming performance instead of proving it.

Use a small pilot before broad rollout. Validate the full flow end to end, and if you offer 2/10 Net 30, confirm you can reliably pay inside the 10-day discount window. Otherwise keep the base term simpler. Where relevant in the EU, remember the contract payment period is generally capped at 60 calendar days unless a longer period is expressly agreed and not grossly unfair.

Run a pilot supplier cohort through this sequence, measure outcomes, then tune your net-term policy before scaling. This pairs well with our guide on Net Revenue Retention (NRR) vs. Gross Revenue Retention (GRR) for Platform CFO Decisions.

If your policy looks solid on paper but fails in execution, align it to traceable disbursement states with Gruv Payouts.

Frequently Asked Questions

Which term should most platforms demand by default, `Net-15`, `Net-30`, or `Net-60`?

There is no universal default across platforms. Net-30 is often the cleanest starting point when your process can execute against clear triggers, and a major U.S. procurement standard uses 30-day logic tied to operational events. If your acceptance trigger is still unclear or execution is inconsistent, a shorter term is often safer than forcing longer terms.

When does `Net-60` improve cash position enough to justify supplier friction?

Net-60 is defensible when the DPO lift is meaningful and supplier behavior stays stable. If you are already near the upper end of your operating range, extending further can add relationship strain without much incremental cash benefit. If suppliers tighten credit or reduce flexibility, the trade is usually not worth it.

How should `2/10 Net 30` change the decision between `Net-15` and `Net-30`?

Treat 2/10 Net 30 as an execution choice, not just a pricing concession. It only pays off when you can consistently capture the 2% discount within 10 days; otherwise the full amount is still due within 30 days. If your invoice-to-approval flow is unreliable, keep the base term simpler.

What should be negotiated besides the payment window in a `Payment Terms Clause`?

Negotiate the trigger mechanics, not only the day count. Define what qualifies as a proper invoice, what counts as acceptance, and how disputes affect clock treatment. That structure matters because due-date logic can depend on invoice receipt, acceptance, and dispute status.

How do `DPO` and supplier `DSO` affect long-term supplier reliability?

Higher buyer DPO extends how long suppliers wait for payment, which can make cash conversion harder on the supplier side. That can weaken trust and reduce credit flexibility over time. Watch for early signs such as tighter terms or reduced flexibility.

What compliance blockers can delay payment even when invoices are approved?

Invoice approval is not always the final gate. Missing or incorrect tax data can trigger backup withholding at 24 percent, foreign payees may need Form W-8BEN when requested, beneficial-owner verification requirements can delay payment setup or release, and sanctions controls can require transaction rejection. Confirm these controls are cleared before committing to payout timing.

How often should teams review and re-negotiate terms after rollout?

There is no single mandatory review cadence. Reopen terms when performance drifts, supplier behavior changes, or your benchmark position no longer matches policy. Compare DPO with dispute lag, exceptions, and missed discount windows, then decide whether the current term still fits.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/32.905trusted

- acquisition.gov/far/52.232-25trusted

- dol.gov/agencies/whd/fact-sheets/66-dbratrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- eur-lex.europa.eu/EN/legal-content/summary/combating-late-paym...trusted

- irs.gov/businesses/small-businesses-self-employed/ba...trusted

- irs.gov/forms-pubs/about-form-w-8-bentrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Net-30 Payment Terms for Platforms: How to Set Vendor Payment Terms Without Killing Contractor Cash Flow

---

Net Payment Terms for Platforms: How to Offer Net 30 60 90 and When to Use Each

Choose **Net 30, Net 60, or Net 90** based on what your payment process can meet consistently, not on generic B2B norms. The right term is one your team can execute reliably while protecting cash flow.

Why Your International Wire Arrives Late and Costs More

When a client says they paid but your money arrives late, lands short, or is hard to trace, that is a cash-flow risk, not a minor inconvenience. If the amount and timing are uncertain, planning your next moves gets harder.