Quick Answer

Use a net-INR-first workflow: set expected bank credit before issuing the invoice, record fee and conversion assumptions with a timestamp, and capture the purpose code used for the inward remittance path. After settlement, match transaction ID, conversion record, and bank credit in sequence, then log any variance (fee mismatch, FX movement, delay, return, or chargeback). Keep one invoice packet with invoice PDF, receipt proof, conversion note, and bank entry for filing and disputes.

Start with net INR, not headline USD#

For freelancers in India, the number that protects cash flow is the net INR credited to your bank, not the USD amount on the invoice. Start from that outcome and work backward through every payment decision.

| Phase | What to do |

|---|---|

| Before invoicing | Record expected net INR, payment terms, and conversion assumption |

| After receipt | Match provider transaction details to final INR credit and flag meaningful variance |

| For filing | Keep invoice copy, receipt proof, conversion record, and bank credit evidence ready for tax review |

Gross invoice value and final bank credit will not always match exactly. Platform charges and conversion choices can change what lands, so estimate net INR before invoicing and reconcile after settlement.

Set your payment rail and compliance inputs before the first invoice. In India, inbound cross-border receipts use a purpose code, also called an inward remittance code. A wrong code can trigger bank queries, delays, or rejection.

Speed and margin often pull in different directions. International gateways are often presented as faster or cheaper, but treat that as a hypothesis and verify it with your own ledger. If two options look close, pick clearer conversion disclosure and fewer surprise deductions.

Treat expected net INR as a pre-invoice gate. If the assumption is fuzzy, pause and write down fee, conversion, and payout assumptions first. That two-minute discipline avoids back-and-forth later when the client has paid but settlement lands light.

Use the same loop on every client payment:

- Before invoicing, record expected net INR, payment terms, and conversion assumption.

- After receipt, match provider transaction details to final INR credit and flag meaningful variance.

- For filing, keep invoice copy, receipt proof, conversion record, and bank credit evidence ready for tax review.

Clean records reduce filing stress and make payment disputes easier to resolve. Tax treatment is case-specific, so this article focuses on practical habits you can repeat each cycle.

Start with one number that matters net INR per invoice#

Before every invoice, write down one number: expected net INR. Gross USD can look healthy while deductions cut what actually reaches your bank account.

Keep definitions fixed so your tracking stays useful. Use one formula template across rails:

- Gross invoice: USD amount paid by the client.

- Net INR: bank-credit amount after platform deductions, conversion effects, and applicable INR-side charges.

| Rail | One-line formula template | First check before sending invoice |

|---|---|---|

| PayPal | Expected Net INR = (Gross USD - platform deductions in USD) x expected conversion rate - INR-side deductions | Confirm transaction context (market relationship) and the date on your latest fee-page snapshot |

| Payoneer | Expected Net INR = (Gross USD - platform deductions in USD) x expected conversion rate - INR-side deductions | Confirm your latest fee snapshot and payout route for this rail |

| Stripe | Expected Net INR = (Gross USD - platform deductions in USD) x expected conversion rate - INR-side deductions | Confirm your latest fee snapshot and payout route for this rail |

| Razorpay | Expected Net INR = (Gross USD - platform deductions in USD) x expected conversion rate - INR-side deductions | Confirm your latest fee snapshot and payout route for this rail |

PayPal needs extra care here. PayPal defines domestic and international by market relationship, and some regional pages frame domestic context differently. Do not assume one page applies across markets.

Avoid stale assumptions. The US consumer fees page shows Last Updated: February 19, 2026. The US merchant fees page shows Last Updated: February 9, 2026. There is a separate Policy Updates page for upcoming changes. Keep a dated fee snapshot in your records before invoicing.

Before you send the invoice, record one more field: assumption timestamp. If settlement happens later, you can still explain why your expected net INR looked reasonable at invoice time. This keeps pricing reviews grounded in what you knew then, not what changed later.

If options look similar on headline cost alone, use your own reconciliation history and documented exception-fee exposure to decide. On PayPal, fee navigation includes separate dispute and chargeback categories, so factor those into your assumptions.

After receipt, run one close-out check: compare expected net INR with the posted bank credit. Then log any meaningful variance with a reason code. If the same pattern repeats on one route, pause new invoices on that route until the cause is clear.

Map every deduction between client payment and your bank credit#

Make each invoice auditable by mapping every deduction from client payment to final bank credit. If a deduction does not fit a defined layer, mark it unresolved and keep reconciliation open.

Use the same four layers each time: transaction charge, currency conversion impact, tax on service fees, and incidentals such as dispute or chargeback costs.

| Deduction layer | What to record | Where it usually appears | Reconciliation note |

|---|---|---|---|

| Transaction charge | Fee type and amount in source currency | Provider transaction or fee detail | Match invoice ID to transaction ID first |

| Currency conversion impact | Conversion rate used and converted amount | Conversion section or payout detail | Compare expected versus applied conversion and log variance |

| Tax on service fees | If present, tax line tied to platform service fee | Fee breakdown export when tax is itemized | Keep attached to the fee line, not invoice value |

| Incidentals | Dispute or chargeback-related cost | Dispute or adjustment entries | Tag separately so one-offs do not distort normal pricing |

Use PayPal as a reference map because its fee pages expose the main deduction categories clearly. Currency conversion appears on consumer pages, and dispute and chargeback sections appear on merchant pages. Keep market context explicit, because fees are also organized by relevant market or region.

To avoid version mix-ups, store the exact market page and last-updated date with each invoice evidence pack. US consumer and US merchant pages already show different update dates, and regional pages can be older, so mixed snapshots can create false variance.

Then mirror the same deduction map for Payoneer, Stripe, and Razorpay, and only fill what each provider statement actually shows. For Stripe, record the base transaction pricing and separate rows for additional international card, manual entry, and currency conversion charges. Even without setup, monthly, or hidden fees, per-transaction additions still change net receipt.

Do not collapse unresolved deductions into a generic adjustment bucket just to close the week. Leave them open, assign an owner, and add a next action. That keeps your variance log useful when a client asks why a later quote changed.

Before month close, run one checkpoint: trace each invoice to final bank credit, and confirm every deduction row has a source line and reason code. If unexplained gaps repeat on one rail, pause new invoices there until the map explains the variance.

Compare payment rails by what lands in India not by headline fee#

Compare rails by net INR from the same invoice scenario, not by advertised fee headlines. Use one identical test case across rails: same gross USD amount, client country, invoice date window, payout bank in India, and reconciliation method.

| Rail | Net-INR comparison setup | What to check in exports | Evidence confidence today |

|---|---|---|---|

| PayPal | Model transaction fee, conversion impact, and potential dispute or chargeback cost paths under the same test case | Fee line items, conversion details, and whether the transaction was treated as domestic or international on the relevant market page | Higher detail in current evidence pack |

| Payoneer | Use the same test case and fill deduction rows from the provider current schedule | Whether each deduction line maps cleanly to final INR credit | Limited detail here, verify current schedule |

| Stripe | Start with 2.9% + 30¢, then add applicable extras: 0.5% for manual entry, 1.5% for international cards, 1% for currency conversion | Which add-ons actually triggered, and whether account setup reflects country-specific rates | Moderate detail in current evidence pack |

| Razorpay | Use the same test case and fill deduction rows from the provider current schedule | Whether conversion and adjustment lines map to final INR credit | Limited detail here, verify current schedule |

For the PayPal row, transaction classification is a key variable. In the PayPal market pages reflected here, domestic versus international status is defined by market relationship. Grouped markets can affect international rate calculations, so verify the exact market page and date used for each comparison.

For Stripe, do not stop at the base card rate. Extra percentages can materially change realized net INR when manual entry, international cards, or currency conversion apply, and rates can vary by country setup.

When you compare results, keep two verdicts instead of one: realized net INR and reconciliation clarity. A rail can look acceptable on price but still create repeated uncertainty if exports do not cleanly map to bank credit.

If two rails look close, prefer the one with clearer fee-line visibility, clearer dispute/chargeback fee visibility where applicable, and fewer unexplained export adjustments. Keep conclusions for other providers provisional until each current schedule is verified.

Set client terms that absorb fee leakage before it hits cashflow#

Protect margin in the contract, not at month-end reconciliation. Set terms from your target take-home so quoted pricing still works after deductions.

| Checklist item | Details |

|---|---|

| Accepted payment method | Backup method |

| Payer legal name | Matches the contracting entity |

| Invoice currency | Confirmed in writing |

| Payment timeline | Due date and late trigger |

| Proof-of-service artifact list | For each milestone |

| Fallback payout route | If the primary rail fails |

Start each proposal with your target net INR, then back-calculate the quote. For marketplace work, treat deductions as variable, not fixed. A reported 0-20% Upwork commission range shows why flat markup assumptions can fail.

Client mix should shape your terms. Platform comparisons describe broad reach for Upwork and Fiverr, and USD-centered billing on major American platforms. Avoid one-size-fits-all assumptions; choose terms by service type, client location, and account setup.

Payment outcomes in quality disputes depend on contract terms, applicable jurisdiction, and case facts. Keep language explicit on acceptance criteria, payment timeline, and dispute evidence requirements. Contracts often separate acceptance from payment, so vague acceptance wording can delay final payment and, in some contracts, allow payment to be withheld until defects are fixed.

| Term block | What to include | Red flag to avoid |

|---|---|---|

| Payment timeline | Due date, milestone dates, and late-payment trigger | Payment after client satisfaction with no dates |

| Acceptance criteria | Objective deliverables, revision limits, and approval window | Open-ended revisions with no completion point |

| Dispute evidence | Required artifacts and where they are submitted | No documented proof standard for scope completion |

Add one practical check before signature: read each term block and ask whether a third party could verify completion from the contract alone. If the answer is no, tighten the wording before kickoff. This prevents avoidable dispute arguments later.

Before you sign, pre-decide accepted rails and invoice currency for cross-border clients, and document one primary rail plus one fallback route.

Use this pre-signing checklist:

- Accepted payment method and backup method

- Payer legal name that matches the contracting entity

- Invoice currency confirmed in writing

- Payment timeline with due date and late trigger

- Proof-of-service artifact list for each milestone

- Fallback payout route if the primary rail fails

After the first invoice on a new client, run one checkpoint: compare signed terms, platform transaction details, and final bank credit in one file. If they do not match, pause new milestones until terms are corrected in writing.

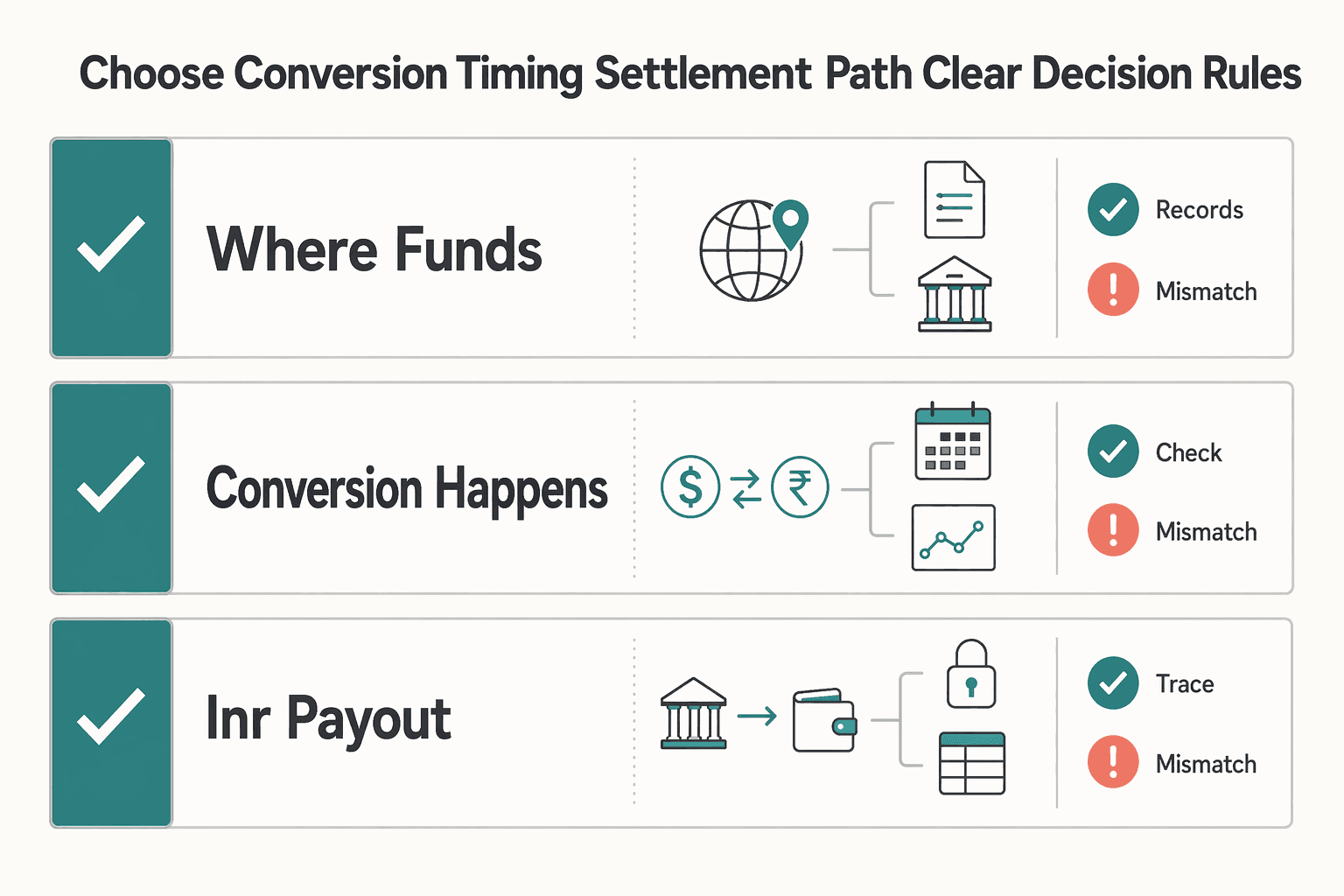

Choose conversion timing and settlement path with clear decision rules#

Split three decisions early if you want more predictable cashflow: where funds are received, when conversion happens, and when INR payout is triggered. If you treat them as one choice, variance gets harder to control. The same discipline applies to account structure, and separating business and personal finances makes reconciliation easier when client payments and household spending would otherwise blur together.

Decide your policy path before payment arrives. For India-focused cross-border work, purpose-code selection is often a key classification step in provider flows. Document the path requested and keep that note with the invoice evidence.

| Decision | What to decide up front | Verification checkpoint | Common failure mode |

|---|---|---|---|

| Where funds are received | Which receiving route collects client payment first | Transaction ID, original currency amount, and receipt timestamp captured the same day | Payment arrives, but intake evidence is incomplete |

| When conversion happens | Convert at receipt, at withdrawal, or in a planned review window | Conversion confirmation details logged with expected INR outcome | Waiting for a better rate and missing a usable conversion window |

| When INR payout is triggered | Automatic payout or manual payout based on cash needs | Trigger time, bank credit date, and actual versus expected INR | Withdrawal delay creates avoidable cashflow gaps |

Set priority rules explicitly. If predictability matters most, choose rails with clear conversion disclosure at confirmation and track variance per invoice. If margin timing matters most, monitor conversion timing and execute within a predefined window.

A simple scenario contrast helps. If a project has near-term expenses, favor earlier conversion and payout for cleaner predictability. If near-term expenses are covered, you can use a planned review window, but only with a pre-decided cut-off so decisions do not drift.

Keep one invoice-level evidence pack so checks stay fast:

- Client invoice and agreed currency

- Provider transaction export with ID and receipt timestamp

- Conversion confirmation record

- INR bank credit amount and credit date

- Purpose-code note used for that payment path

Where supported, test whether a more centralized setup improves traceability versus fragmented wallets and manual transfers. Judge it on practical controls: one status trail from collection to conversion to payout, clear matching rules, mismatch alerts, and real-time reporting that helps reconciliation. If you want a simple operational starting point, try the free invoice generator.

Prevent holds returns and chargebacks before they happen#

Returns and chargebacks are often easier to prevent before invoicing than to fix after payout issues start. The practical move is tighter intake checks and a complete evidence file for each milestone.

For India-based businesses and freelancers using PayPal for international payments, a chargeback is not the same as a refund. Refunds are merchant-approved, while chargebacks can start without merchant approval and then move through dispute resolution. That distinction is why scope records and approval trails are operational requirements, not optional admin.

| Control area | What to set before invoicing | Verification checkpoint | Red flag |

|---|---|---|---|

| Scope documentation | Define deliverables, revision boundaries, and payment terms in writing | Contract and invoice terms match the agreed scope | Scope or terms conflict across documents |

| Approval trail | Define how each stage, revision, and final deliverable is approved | Approval is saved for each milestone | Acceptance happens verbally with no written record |

| Dispute readiness | Prepare a case-file structure in advance | Transaction details and evidence folders are linked to the invoice | Dispute response starts with missing records |

| Reconciliation workflow | Set a routine for data collection, matching, error resolution, and final verification | Transactions are matched and mismatches are resolved before the next invoice cycle | Unresolved mismatches carry forward |

Weak documentation is a common failure mode in disputes and delayed payouts. Keep three records per milestone: agreed scope, delivery proof, and client approval confirmation. If one is missing, pause your next invoice until the file is complete.

Before you send a high-value invoice, run a short pre-dispute check: can you produce scope, delivery proof, and dated acceptance in under a few minutes? If not, fix the evidence pack first.

When a dispute opens, keep your response order strict:

- Lock the final approved scope version.

- Gather dated delivery proof.

- Export the communication log showing revisions and approvals.

- Add the provider case reference and submit one complete response packet.

After submission, reconcile promptly rather than waiting for month-end. Collect transaction data, match records, resolve mismatches, and confirm final status before sending the next high-value invoice.

Build tax-ready records from day one#

Tax prep breaks down when records are scattered. Build one complete packet per invoice from day one so review is file-based, not memory-based. Use four fixed folders per invoice with consistent naming across clients and months.

| Folder | Minimum files to keep | Why it matters |

|---|---|---|

| Invoice | Final invoice PDF, client entity name, invoice currency | Anchors original commercial terms |

| Receipt | Gateway transaction confirmation and transaction ID | Shows payment capture |

| Conversion record | Conversion confirmation, rate note, fee note at conversion time | Explains differences between gross and settled value |

| Bank credit | Bank statement line showing credit date and amount in your settlement currency | Confirms cash arrival |

For PayPal entries, log the exact market or region fees page used, the date checked, and the page's last-updated date. Keep a dated snapshot in the packet because applicability can change through the Policy Updates page. Also note conversion assumptions, including that exchange-rate effects and card-issuer or bank fees may still affect final credit.

For filing prep, add internal routing tags to each packet based on your jurisdiction and return workflow. Treat these tags as review labels, not automatic tax conclusions. India-specific filing requirements are not established by the sources above, so verify them separately with a qualified tax professional. Use a fixed file naming pattern. Keep invoice ID first, then date, then document type so each packet sorts cleanly and scans quickly during filing prep.

Run a monthly tie-out before filing cycles:

- Export transaction data for the same date range from each payment provider.

- Match each row to invoice ID, gross currency amount, and receipt timestamp.

- Match each row to conversion evidence and final bank credit.

- Mark unresolved items as open exceptions and clear them before the next filing batch.

Compliance obligations vary by country and program, so confirm interpretation with a qualified tax professional before filing, revising returns, or applying edge-case treatment.

Run a weekly reconciliation checklist across gateways and banks#

A fixed weekly close keeps month-end clean. Run this checklist so each invoice can be traced from provider record to final bank credit without guesswork.

| Provider | Weekly check | Note |

|---|---|---|

| PayPal | Use the correct market page before classifying a transaction as domestic or international | Save the exact page used, its last-updated marker, and a downloadable PDF, and note if policy updates changed rates or timing |

| Stripe | Separate pricing assumptions from reconciliation errors | Public standard pricing says no setup, monthly, or hidden fees, while listed charges can still apply, including 2.9% + 30¢ plus possible 1.5%, 1%, or 0.5% add-ons |

| Other gateways | Reconcile with that week's transaction exports and active account terms | Do not reuse one provider's fee logic across all providers |

| Step | Weekly action | Evidence to save | Common miss |

|---|---|---|---|

| 1 | Match each invoice to provider transaction ID in PayPal, Stripe, and other gateways you use | Export row with transaction ID, gross amount, currency, and timestamp | Invoice exists but no provider ID, or multiple IDs without explanation |

| 2 | Map each provider transaction to the final bank credit line | Bank statement line with credit date, amount, and reference | Provider status shows completed but no matching bank credit |

| 3 | Flag every variance by cause: fee mismatch, FX variance, delay, return, or chargeback | Variance log with cause label, owner, and resolution status | A variance is accepted without a root-cause note |

| 4 | Archive full evidence pack and update net-receipt dashboard by client and rail | Folder path plus dashboard row for invoice, net receipt, and open exceptions | Files are saved, but dashboard is not updated |

The provider-specific checks above matter because classification mistakes can look like reconciliation errors. For PayPal, save the exact market page, last-updated marker, and PDF used for domestic or international classification. For Stripe, tag any 1.5%, 1%, or 0.5% add-ons before you treat a difference as a reconciliation error. For gateways not covered above, reconcile against that week's exports and active account terms rather than borrowing another provider's fee logic.

Set one fixed weekly reconciliation day and keep a short cut-off time. A predictable cadence reduces carryover items and keeps exception ownership clear.

Close the week by storing invoice, provider export, conversion note, bank credit proof, variance log, and dispute notes in one place. Update the dashboard immediately while details are still fresh.

Decide when to keep patchwork tools and when to centralize operations#

Patchwork is fine as long as weekly close stays clean. Move to centralized operations once end-to-end traceability starts slipping.

Keep patchwork when volume is low, disputes are rare, and one owner can still map each invoice from provider transaction to final bank credit without spillover. Shift when you need one audit trail across collection, conversion, and payout, with clear status history, exception ownership, and export-ready records.

PayPal is a useful pressure test. Fee documentation separates chargeback, dispute, currency conversion, and withdrawal, and fee pages are tied to market or region. It also classifies domestic versus international by whether sender and receiver are in the same or different markets. When those classifications and fee snapshots are scattered, misclassification risk can rise.

| Decision signal | Keep patchwork | Centralize now |

|---|---|---|

| Weekly close | Invoices reconcile in-week | Repeated spillover or unresolved exceptions |

| Forecast reliability | Payout timing and net amounts are usually predictable | Forecasts break because pending states are unclear |

| Fee-change control | Team uses one current fee snapshot and policy-update check | Different snapshots are used across reviewers |

| Evidence readiness | Exports and bank proof are quick to retrieve | Evidence packs are slow or incomplete |

Baseline control is simple: require a date-stamped fee reference when classifying transaction type, and store the exact weekly export with policy-update context. If weekly reconciliation repeatedly fails or forecasting breaks because statuses are not traceable end-to-end, prioritize centralization.

If you need modular controls for invoicing, FX, and payouts in one place, review Gruv docs and confirm India market and program coverage before migrating.

When planning migration, run a short parallel period. Keep current rails active for live invoices while testing whether centralized records improve matching speed, exception closure, and forecast confidence. Move fully only after those checks improve in your own ledger.

Conclusion#

Reliable payout execution beats one-time gateway picking. The practical goal is to predict net INR before invoicing, explain every variance after payout, and keep records ready for review.

In India, cross-border receipts can involve multiple entities, and margin loss can come from stacked deductions rather than one obvious fee line. One reported freelancer example described roughly 2% exchange-rate loss on a direct transfer path plus an additional 0.18% GST-related conversion cost. Use that as a warning signal, not a universal benchmark.

Delay risk belongs in the same control loop as fee leakage. Qualitative reporting includes examples where clients promise payment next week and then stop responding, which can break cash forecasting even when pricing assumptions looked reasonable.

For the next month, keep execution strict:

- Use one invoice assumption template for every deal: gross amount, expected deductions, and expected net INR.

- Reconcile each receipt to final bank credit on a fixed weekly day, then tag each variance by likely cause.

- Store one evidence pack per invoice: invoice copy, payout statement row, conversion note, and bank proof.

- Escalate repeated unresolved variances or repeated unexplained delays instead of normalizing them.

Add one monthly review after the fourth weekly close. Identify recurring variance causes by rail, adjust quoting assumptions, and update client terms where leakage keeps repeating. Small monthly corrections are easier than large quarter-end resets.

Confidence should track your own data quality. For operating decisions, your own ledger, reconciliations, and variance history are still the strongest evidence for what to change next.

Frequently Asked Questions

How do Indian freelancers calculate true net receipt after platform fees, FX spread, and GST-related fee impact?

Calculate expected net INR line by line: gross invoice minus platform transaction fees, any currency-conversion charges, and any taxes shown on provider fee lines. Then match the expected amount to the final bank credit and log any variance before sending the next invoice. Treat this as a repeatable invoice-close step, not a one-time estimate. The calculation only helps if each deduction line can be traced to provider records and then to the final bank credit.

Is **PayPal** effectively closer to headline transaction pricing or materially higher after full deduction layers?

Treat headline pricing as a starting point, not the final cost. PayPal uses market-specific fee pages and classifies transactions as domestic or international by market, and its US business fees page includes separate dispute-fee and chargeback-fee sections. Record the exact market page and last-updated date used for each classification check. If realized cost swings between similar invoices, check classification first, then review any additional fee lines shown on that same market page.

What should I compare first between **PayPal**, **Payoneer**, **Stripe**, and **Razorpay** if my goal is stable **INR** cashflow?

Use one identical invoice scenario across all rails, then rank by net INR received and how clearly deductions map to final bank credit. For Stripe, start with 2.9% + 30¢ for domestic cards and add only applicable extras: 0.5% for manual entry, 1.5% for international cards, and 1% for currency conversion. For PayPal in this comparison, confirm domestic versus international classification on the correct market page before finalizing assumptions. Keep decisions provisional until each provider schedule is checked for the same date window. Comparing mixed-date assumptions can make one rail look better on paper than it is.

How should I set project pricing so fee leakage does not erode margins on cross-border invoices?

Price from target net INR backward, not from headline percentages forward. Build both an expected-cost case and a higher-cost case before sharing terms, then lock payment method, invoice currency, and fallback payout route at kickoff. Reprice when variance logs repeatedly show a thin buffer. Use milestone-level acceptance language so payment release depends on objective completion, not open-ended satisfaction wording. Clear acceptance terms protect both cash timing and dispute response quality.

What records should I keep for **GSTR-1**, **GSTR-3B**, **ITR-4**, and **Section 44ADA** discussions with my CA?

Keep one evidence pack per invoice with invoice copy, gateway export row, conversion record, and final INR bank credit proof. Add a short variance note whenever expected and actual net differ, and maintain monthly tie-outs from provider totals to bank credits. Tag records by reporting period and keep final tax treatment decisions with your CA. If a packet is incomplete, mark it as open and fix it before the filing cycle gets crowded. In practice, unresolved packet gaps create more delay than difficult calculations.

What are the earliest warning signs of hold, return, or **chargeback** risk, and what evidence should I gather upfront?

Possible warning signs include unexplained status stalls, unexpected reversals after apparent completion, and early disputes. Build an evidence-first file immediately with signed scope, delivery proof, dated approvals, and a communication log tied to transaction ID. Keep case references in the same invoice folder so rebuttals are fast when disputes open. Do not wait for a formal case to start documenting. Early organization is what shortens response time if a hold or chargeback appears after delivery.

Watch

Indian Freelancers: Stop Chasing the Cheapest Payout

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- govinfo.gov/content/pkg/CFR-2019-title20-vol1/html/CFR-2...trusted

- icsi.edu/media/webmodules/Final_Book_Tax_Laws_&_Pract...trusted

- irs.gov/pub/irs-access/p2104_accessible.pdftrusted

- nyc.gov/assets/dcas/downloads/pdf/cityrecord/stated-...trusted

- livemint.com/money/personal-finance/indian-freelancers-gl...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.