Quick Answer

Build payment method coverage by country as a country-plus-method decision map, then approve launch only after obligations, risk controls, compliance evidence, and auditability are all verified. Use provider coverage pages and preference content for initial screening, but treat them as provisional until you capture dated artifacts, explicit scope, and exception-path details. If sources conflict or route-level outcomes cannot be traced cleanly, keep that market in pilot.

How to assess payment method coverage before launch#

A country is launch-ready only when the country-method path is operationally verifiable, not just listed as supported. For finance ops, payments ops, and product owners, that means timing assumptions you can test, status you can track, and reconciliation checks you can review at close.

- Decide at the country-method level.

Make the decision on country + payment method pairs, not on country names alone. The payment method changes the risk and timing profile, and Trade.gov frames international transactions as having five primary payment methods that must balance risk reduction with buyer needs. A support list or logo grid is not enough for a go or no-go decision.

- Map availability and execution together.

Availability is only the first layer. Add operational checks for status visibility, tracking checkpoints, and reconciliation evidence. In cross-border flows, tracking is an explicit step ("Track the payment"), so weak or misaligned status trails are a pre-launch risk, not a cleanup task for later.

- Prefer decision-grade sources over browse-grade sources.

ECB payment statistics are useful because they are compiled at EU and euro area level and by individual EU country, and include transaction number and value by payment instrument plus payments processed by main payment and settlement systems. That still does not prove method-level readiness for ACH, SWIFT, or SPEI in a given country. What it does give you is the evidence standard: country-level comparison, instrument-level visibility, and operational context for trend-based decisions. Some market-preference pages also require login for full data access, so treat those as incomplete until fully verified.

This map answers a harder question than "is this country supported?": can your team execute payments, track exceptions, and close cleanly? That is the difference between broad coverage on paper and real launch readiness. Related reading: Global Payment Processing Infrastructure Choices for Platforms.

Who this list is for and how to pick coverage signals#

This list is for teams that own payout and reconciliation decisions and need coverage data they can defend before launch and during failures. If you only need consumer preference signals, this is probably more operational detail than you need.

- Operator-owned coverage

Use this list when you need to answer more than "is this country supported?" You need evidence about the last mile to the beneficiary, especially in cross-border flows where persistent pain points include high costs, low speed, limited access, and insufficient transparency. Key differentiator: prioritize execution evidence, status visibility, and reconciliation impact over trend commentary.

- Signals with product and operational detail

Favor sources that show institution coverage, product coverage, and a health or downtime view so you can validate a country-method path, not just browse a support page. Plaid's institutions coverage and status dashboard are good examples of this kind of operations signal. Key differentiator: if you cannot verify both access scope and operational health, treat the source as incomplete. If rail detail and method detail are split across sources, use them for screening, not approval.

- Signals tied to real access gates

Separate sandbox visibility from production readiness. Plaid explicitly distinguishes broad Sandbox access from narrower default Production access, requires a support workflow to expand Production countries, and notes that product-overlap filtering can change returned institution counts. Key differentiator: if a source cannot be tied to your actual operating gates and production-access workflow, keep it directional only. Apply the same caution to wallet participation lists: Apple Pay states that some cards from participating banks might not be supported.

If you want a deeper dive, read How to Expand Your Subscription Platform to Europe: Payment Methods Tax and Compliance.

Comparison table to score every source before you trust it#

Treat every source as provisional until it shows clear scope, a recent-enough update, and operational detail beyond logos or country counts. If it cannot show how a country-method pair behaves when something goes wrong, do not use it for launch approval.

| Source type | Best for | Coverage depth | Update confidence | Operational fields | Known blind spots |

|---|---|---|---|---|---|

| Provider coverage or fee pages (for method pages such as PayPal market pages) | First-pass screening and market definitions | Medium when market and transaction type are explicit, low when only country lists appear | High only with visible dates. PayPal consumer fees: February 19, 2026. PayPal business fees: February 9, 2026 | Domestic vs International definitions, exception categories like Chargeback Fees, downloadable PDF artifacts | May be market-scoped (for example, PayPal consumer-fees excerpt shows United States (US)). Grouped international markets can hide country-level differences |

| Preference content (method preference lists or trend summaries) | Directional demand signals, not launch approval | Low for operational approval | Unclear unless date and geography are explicit | Usually insufficient unless it includes explicit constraints or exception handling | Often mixes preference with readiness. Logos or country counts alone are screening input, not approval evidence |

| Region stats or commissioned research (such as the ECB study) | Regional context and settlement-feature framing | Medium for context, low for production truth | Medium to low when older. Commissioned September 2021, published March 2022 | Can include settlement-feature context and review aids like Annex: Country fiches 94 | Not direct country-rail production status evidence |

What to score before using a source in a go decision#

Score the basics that change operational meaning before you rely on a source:

- Scope: Confirm the exact market, region, and transaction boundary. PayPal's Domestic and International definitions show why this matters.

- Freshness: Capture the visible last-updated date and save the source artifact, including Download printable PDF when available.

- Operational depth: Check whether the source shows transaction boundaries and exception paths, for example disputes or chargebacks, not just availability.

If a source fails these checks, keep it directional only.

Red flags that force verification#

Stop the approval path until you verify these directly:

- Grouped geographies: PayPal business fees notes that certain markets are grouped for international rate calculation, which can hide country-level differences.

- Older research used as launch proof: The ECB report is useful context, but its 2021/2022 timing lowers confidence for 2026 launch decisions.

Decision rule#

If two independent sources disagree on a country-method pair, mark it verification required before launch. Minimum evidence pack: saved artifact, last-updated date, exact scope, and at least one operational field, for example a transaction-type definition or exception category.

Best source for rail availability by country#

For rail availability, provider rail and coverage pages are the right place to start, but not the right place to stop. Use them to narrow the field, then require a second validation before you call anything production-ready.

| Source type | What it gives you | Main limit |

|---|---|---|

| Provider coverage pages | Shortlist country-method pairs before engineering work begins | "Countries supported" language rarely confirms access conditions, onboarding gates, or failure handling |

| SWIFT and cross-border explainer pages | Cross-border context; SWIFT is a global messaging network with reach across over 200 countries | Use for context, not launch approval; SWIFT can involve higher cost and slower settlement through correspondent banking |

| Alternative-rail roundups | Spot categories such as domestic banking networks, card networks, fintech platforms, or stablecoin systems | Roundup size is directional, not exhaustive; one 2026 source frames 4 alternatives and another frames 8 |

- Provider coverage pages

Use these to decide quickly whether a country-method pair belongs on your shortlist at all. They help you cut non-starters before engineering work begins. The limit is straightforward: "countries supported" language rarely confirms access conditions, onboarding gates, or failure handling. If you are checking a specific country and recipient-bank setup, a high-level page still does not prove the rail path is usable for your entity or transaction setup.

- SWIFT and cross-border explainer pages

Use these for context, not launch approval. They clarify that SWIFT is a global messaging network with reach across over 200 countries, and they align on cross-border scope, where payer and payee are in different countries. They do not confirm operational fit. The same source set also flags the tradeoff: SWIFT can involve higher cost and slower settlement through correspondent banking, so "SWIFT supported" should mean "possible, verify further," not "ready."

- Alternative-rail roundups

Use these to spot categories your first screen may miss, for example domestic banking networks, card networks, fintech platforms, or stablecoin systems. Do not treat roundup size as truth. One 2026 source frames 4 alternatives and another frames 8, so list length is directional, not exhaustive.

Practical rule: use provider pages to pre-filter, then require a second layer of validation before launch. For each country-method pair, save the artifact, capture the visible date, lock the scope as domestic or international, and record at least one operational field when available. If access conditions, compliance constraints, or failure behavior are unclear, mark it verification required. A country can be "supported" on paper and still be unready for production.

Best source for local payment preference context#

Preference sources are useful, but only for the question they actually answer. They help you rank checkout methods. They do not prove launch readiness.

| Source type | Grounded signal | Launch-approval limit |

|---|---|---|

| Provider payment method directories | Adyen lets you select country and filter by payment method type; catalog spans Visa, Mastercard, and Cash App Pay | Use to document country selected, method-type filter used, and visible date; it does not prove payout, settlement, or reconciliation readiness |

| Regional market explainers | PhotonPay describes the U.S. as card-dominant, says PayPal, Venmo, and Cash App are growing, and reports China mobile-payment adoption above 98% | Vendor-authored context; excerpt shows 2024-11-05 and still does not confirm settlement, payout, or reconciliation readiness |

| Generic gateway and "top methods" roundups | GoCardless notes recommendations differ by business goals and requirements; excerpt shows a Jan 2026 recency marker | If country nuance, method filters, or collection-versus-payout separation are missing, keep it directional only; if inaccessible, log a verification gap |

- Provider payment method directories

Adyen's payment methods page is a strong starting point because it gives you a concrete workflow: select country, then filter by payment method type. That makes it easier to compare cards, wallets, and other local methods in the same workflow, and the catalog spans options like Visa, Mastercard, and Cash App Pay. It also states that local payment methods processed through a local connection are more likely to be approved by issuers, which supports prioritizing local collection methods in your shortlist. When you use this source, document the country selected, the method-type filter used, and the visible date.

- Regional market explainers

Use these for behavior context when directories are too high-level. In the PhotonPay article, the U.S. is described as card-dominant while wallets like PayPal, Venmo, and Cash App are growing. It reports mobile-payment adoption in China above 98%. That helps you prioritize checkout design, but it still does not confirm settlement, payout, or reconciliation readiness. Before you rely on a regional explainer, record timestamp and scope. This excerpt shows 2024-11-05 and should be treated as vendor-authored context.

- Generic gateway and "top methods" roundups

Treat these as directional only. GoCardless explicitly notes that recommendations differ by business goals and requirements, which is a useful guardrail against one-size-fits-all rankings, and the excerpt shows a Jan 2026 recency marker. If a roundup lacks country-level nuance, method filters, or collection-versus-payout separation, do not let it drive prioritization. If a candidate source is inaccessible, for example Access Denied, log a verification gap instead of inferring missing facts.

Practical use case: rank checkout methods from preference evidence, then validate operations country by country. If a source points to wallet-heavy behavior, prioritize that checkout path, but approve launch only after separate checks for payout path, settlement behavior, and reconciliation handling.

For the reconciliation side, see Account Reconciliation for Payment Platforms: How to Automate the Match Between Payouts and GL Entries.

Best source for settlement expectations and payout timing#

Timing labels are useful for planning, but they become operational only when you pin them to a route, an event, and an owner. Use payout-operations sources to set expectations, then turn each timing claim into an internal SLA row before launch.

- Payout operations trend content

This is a useful starting point for timing expectations. For example, the December 9, 2025 PayQuicker article says payees expect immediate or same-day access and notes expanding real-time payment networks. Do not treat that as a commitment. The same source warns that fragmented provider stacks make global coverage harder to scale, so broad timing language can create false confidence during growth.

- Cross-border platform explainers with operator metrics

Use these to keep payout-speed discussions tied to operating performance. A 2026-dated explainer frames an optimized stack around fast settlement, predictable FX, clean reconciliation data, and scalable compliance, and points to measurable signals like FX spread, failure rates, chargebacks, beneficiary experience, and reconciliation time. This helps you avoid calling a route "fast" when reconciliation time is still high.

- Your internal SLA table built from external timing claims

This is where expectation language becomes usable policy. For each timing statement, create one row with payout method or rail category, exact claim text, visible date, stated scope, customer-facing promise, and exception owner. Before go-live, require a corridor audit for cost spikes, failure clusters, and compliance gaps. If a source gives speed labels without method-level constraints or exception-path detail, keep that row provisional until you validate real payout behavior.

Related: How to Expand Your Subscription Platform to APAC: Payment Methods Currency and Regulatory Market.

Best source for compliance and documentation readiness#

A country is not launch-ready until your compliance evidence is as explicit as your timing SLA. For this decision, prioritize sources that show how onboarding, screening, document capture, and audit records actually support the rail you plan to launch.

- Internal treasury and card policy documents

These are the strongest base because they define the controls you must prove, not just the methods you can enable. A compliance-ready process covers accepting, depositing, recording, safeguarding, and reconciling cash assets. If card acceptance is in scope, confirm PCI DSS obligations are named and owned. If ACH is in scope in the U.S., account for its typical one to two days completion window and verify controls from payment initiation through reconciliation. For each country-method pair, confirm where KYC/AML and sanctions-screening results are stored, who handles exceptions, and what record ties the payment event to a reconciled ledger entry.

- Real-time payment compliance guidance from cross-border operators

This matters because speed exposes weak controls quickly. Real-time domestic schemes are live in more than 70 countries, and the practical standard is clear: compliance has to run alongside payment execution, not only after settlement. If a provider says a country is supported but cannot show how screening, privacy, and documentation checks run during execution, treat that claim as incomplete. Otherwise, exceptions tend to surface later as FX spreads, intermediary deductions, and failed-payment rework.

- Field-level tax and reporting instructions for document design

Use these as design checkpoints, not universal launch rules. They help you define what your onboarding and reporting flow may need to capture where relevant. For example, Form 1099-INT instructions include Box 6 (Foreign Tax Paid), Box 7 (Foreign Country or U.S. Territory), and a FATCA filing requirement checkbox. The excerpts here do not establish W-8, W-9, Form 1099, or VAT obligations by country, so treat those as separate validation checks before launch. Require an evidence pack per country before approval: compliance gate checklist, required document list for that flow, and named escalation owner.

For a step-by-step walkthrough, start here. Accounting Cycle for Payment Platforms: How to Structure Month-End and Quarter-End Close.

Best source for production truth after launch#

After launch, the production truth that matters is the one you can trace in your own systems. Read it at country-plus-rail-plus-method level, not as one blended global result.

- Start with a traceable event chain.

Build your review from the payment path itself, then confirm you can follow each path from initiation to final recorded outcome in your own systems. For each live country-method pair, keep the transaction or message flow visible, including push versus pull behavior, and keep the participant settlement model attached to that route. This gives you a concrete operating artifact when behavior looks inconsistent across paths.

- Segment before you trust trends.

Do not pool unlike instruments or rails into one headline result. Keep route-level slices for the instruments and rails you actually run, then compare like with like. External behavior data is a useful guardrail here: the ECB has tracked payment attitudes since 2016, and behavior still varies by context in the 2024 round. Use that as a reminder that one aggregate performance story can hide route-level risk.

- Track assistance burden, not only end-state completion.

A route can look fine at the final state while still creating operational drag through support demand. Include assistance signals in your weekly review, not just completion labels. The ECB's 2024 survey notes that almost one in ten respondents needed help with digital payments, which is a practical warning to watch support burden alongside payment outcomes.

- Run a weekly country confidence table with explicit pass or fail logic.

Keep the table compact, reviewable, and method-level. The goal is consistency: define internal pass or fail rules once, then apply them every week by country and method.

| Signal | Segment by | Weekly verification focus | Common misread |

|---|---|---|---|

| Completion outcome | Country + rail + method + flow type | Outcome labels are consistent and traceable for each route | Blended totals hide weak paths |

| Assistance burden | Country + rail + method | Support needs are visible by route, not just in aggregate | "Eventually completed" is treated as healthy |

| Flow and settlement mapping | Country + rail + method + flow type | Push/pull transaction-message flow and participant settlement model stay mapped per route | One generic process map is assumed to fit all routes |

If one country only looks healthy after methods are pooled, keep it in verification status until each route can stand on its own evidence.

This pairs well with our guide on Cash Flow Forecasting for Payment Platforms for Payout Go/No-Go Decisions.

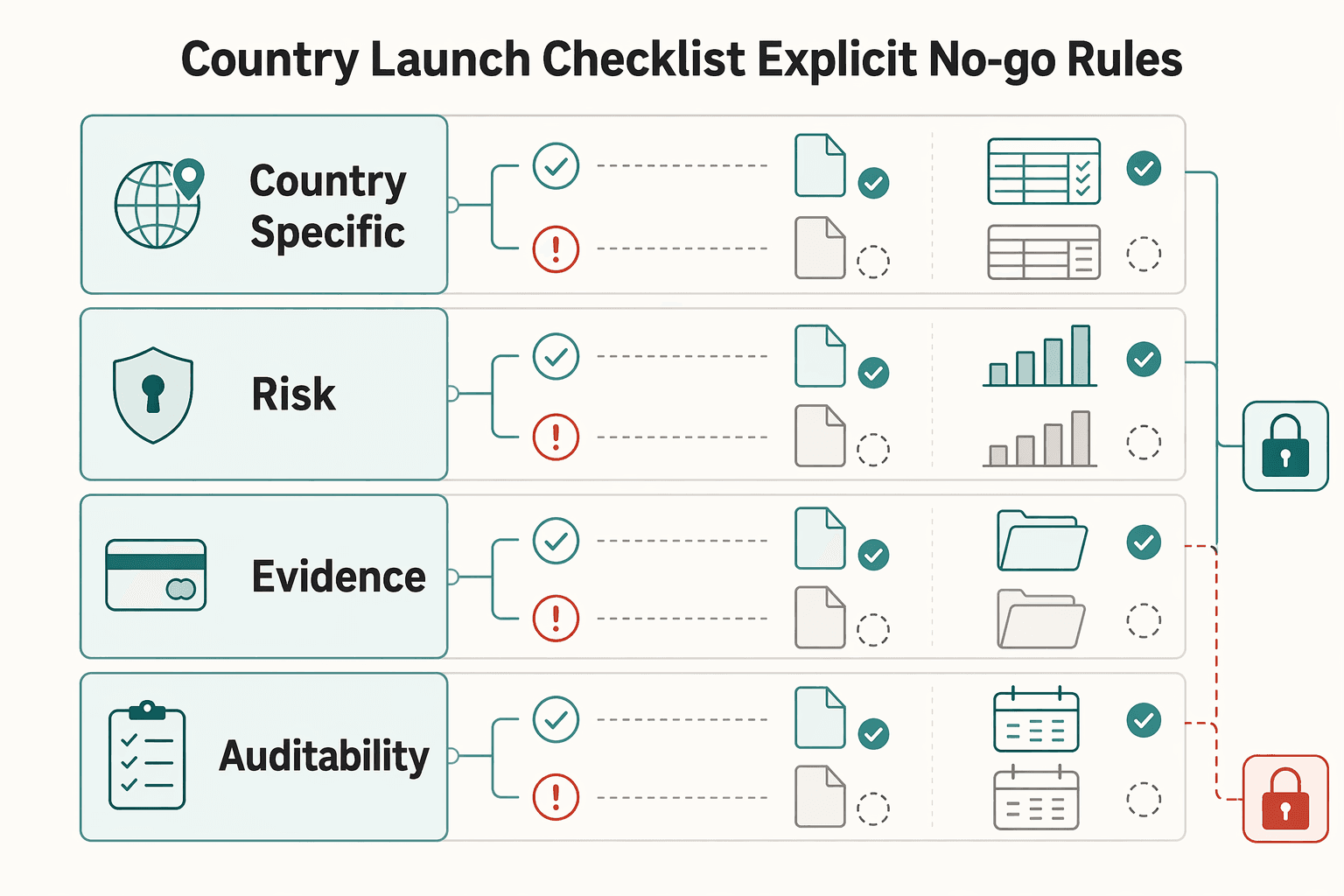

Country launch checklist with explicit go and no-go rules#

Keep a country at no-go until you can verify four gates with evidence in your own systems. Regulatory and compliance requirements differ by country and region, so each gate must be validated country by country. If any gate is missing, do not approve full launch.

| Gate | Required evidence | Keep no-go when |

|---|---|---|

| Country-specific obligations | Assigned obligations for that jurisdiction are documented and reviewed | Obligations are unclear or incomplete |

| Risk controls | How exceptions surface and who owns escalation are documented; include a Transfer Impact Assessment (TIA) when cross-border data transfer risk applies | Exception handling, ownership, or required TIA is missing |

| Compliance and document readiness | Country-specific compliance checks plus audit artifacts: complete system inventory, updated data flow maps, risk assessments, and compliance records; IRS Publication 515 (2026) includes Forms 1042 and 1042-S obligations and Form 1099 reporting with backup withholding | Compliance checks or audit artifacts are missing |

| Auditability | Required obligations, risk controls, and records are current and retrievable | Key evidence cannot be produced on demand |

- Confirm country-specific obligations, not just demand.

Approve only when assigned obligations for that jurisdiction are documented and reviewed. If those obligations are unclear or incomplete, keep no-go.

- Define risk controls before calling the country live.

Set and document how exceptions surface and who owns escalation. When cross-border data transfer risk applies, include a Transfer Impact Assessment (TIA).

- Treat compliance and document readiness as a hard gate.

Compliance checks must be country-specific, and you need audit artifacts: a complete system inventory, updated data flow maps, risk assessments, and compliance records. For U.S. reporting, IRS Publication 515 (2026) includes Forms 1042 and 1042-S obligations and Form 1099 reporting with backup withholding.

- Run an auditability check as the final gate.

Before launch, confirm required obligations, risk controls, and records are current and retrievable. Source availability is part of verification risk, so keep no-go if key evidence cannot be produced on demand.

If coverage looks commercially strong but these four gates do not clear with evidence, launch as a pilot or hold the country back. Full launch is for countries that can withstand both live traffic and audit review.

Turn this checklist into an execution runbook by mapping each go/no-go gate to owners, retries, and exception handling in Payouts.

Failure patterns competitors skip but operators face#

The main post-checklist risk is false confidence. A country can look ready while hidden gaps still break operations. In practice, the misses usually come from three mismatches. If any one is unresolved, keep the country in pilot.

1. Method mismatch#

Collection coverage is not end-to-end coverage. You might collect on Visa or Mastercard while outcomes still vary by processor and market, especially with manual country-level routing. Routing decisions affect more than cost. They also affect approval outcomes and compliance requirements, and bank risk behavior and acquirer performance can differ by market.

Use a method-to-payout map with real statuses, not just "supported." Require visible success, pending, retry, and failed states by country and processor. Then match those outcomes through 3-way reconciliation across internal records, PSPs, and banks. Treat fragmented visibility as a red flag.

2. Timing mismatch#

A country can appear healthy at launch while exception handling is still opaque. That can create cash-forecasting and support pressure when pending items age without clear ownership.

Define an internal expectation per route for normal completion, exception aging, and escalation owner. Then validate real aging behavior from PSP and bank data, not provider marketing pages. If your team cannot explain why items remain pending, the route is not operationally reliable.

3. Documentation mismatch#

Operational rollout often moves faster than compliance and reporting readiness. That creates avoidable risk because routing logic can include compliance requirements, and documentation obligations are not interchangeable across flows.

Maintain an evidence pack per country: KYC/AML checklist, data-flow map, risk assessment, escalation owner, and the tax/reporting records your process is designed to produce. Also keep scope clear: IRS instructions dated 01/2024 for Forms 1099-INT and 1099-OID are specific to interest reporting and should not be treated as blanket proof that all Form 1099 handling is ready.

Conclusion#

The better launch decision is usually a smaller country list with stronger proof. Prioritize only the country-method pairs your team can defend with dated evidence, repeatable checks, and clear exception ownership.

- Use a decision map, not a country count.

A long support matrix is not enough for approval. Each country-method row should show a named source, a validation date, and an owner for exceptions. If any of that is missing, treat the row as unproven.

- Separate demand signals from execution proof.

Preference data can help rank likely user demand, while coverage data shows what a provider or market source says is available. Use both, but do not treat either as final approval by itself. The World Bank snapshot from the sixth iteration of GPSS can help with screening and is structured across domains like legal and regulatory framework and payment-system sections, but the report also says it does not guarantee the accuracy of the data included in this work.

- Apply official-source gates when legal meaning affects launch.

If a launch decision depends on legal or regulatory interpretation, do not rely on an unofficial rendering alone. On the FederalRegister.gov page dated 01/16/2025 (90 FR 5360), the site states the page is an unofficial informational resource, the posted documents are XML renditions, and legal research should be verified against an official edition. It also links to the official PDF on govinfo.gov.

Use that as your final rule. Move forward only when your map shows validated method coverage, documented settlement behavior assumptions, compliance checkpoints, and reconciliation readiness in a way another operator can retrace. If it cannot, keep the country in pilot or mark it no-go until validated. Before expanding to new countries, validate market-specific coverage, policy gates, and rollout constraints with the Gruv team via Contact.

Frequently Asked Questions

What does payment method coverage by country actually include in practice?

It includes the real end-to-end flow, not just a method logo list. In practice, that means checkpoints such as registration, email verification, entering Billing, and initiating payment. A method is only meaningfully "covered" when you can see where it works, where it is excluded, and what happens next.

What is the difference between payment preference data and provider coverage data?

Preference data helps you prioritize what users are likely to choose at checkout. Provider coverage data indicates what a provider says it can support in a specific market or product context. Use them for different decisions: preference for demand ranking, coverage for execution readiness, and not as proof of each other. For demand analysis, conversion-rate data is useful.

Does “countries supported” mean every method is equally available and reliable?

No. Availability can vary even within one provider by product line. One documented case shows card payments accepted for some life policies but not yet for health and annuity policies, and the same payer may not be able to use one method across all policies. Treat "supported country" as a starting signal, not an operational guarantee.

How should operators interpret instant, same day, and T+1 for planning and SLAs?

Treat those labels as directional until the underlying event is explicit. In EU PSD context, payment materials note funds are usually credited to the receiver's account within the next day, which is a different event from "posted immediately" in a UI or internal ledger. If the timestamp definition is unclear, do not lock it into an SLA.

What should be validated when source data is incomplete or paywalled?

Validate recency, scope, and jurisdiction first, then treat unclear claims as directional only. In this topic area, update cadence matters because some compliance FAQs are regularly updated, with visible examples like December 2025 and 20 March 2026. Regulatory differences can create legal uncertainty, so if you cannot confirm what changed, when it changed, and what flow it covers, keep the claim out of launch-critical decisions.

What is the minimum evidence needed before a country moves from pilot to full launch?

There is no universal minimum in the grounded sources, so avoid one-size-fits-all launch gates. Use your own risk standard, but require evidence you can reproduce: a working end-to-end path, clear product-scope exclusions, and timing definitions tied to specific events. If those checks are not repeatable, keep the country in pilot.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cech.uc.edu/about/headlines/cech-chats-podcast.htmltrusted

- documents1.worldbank.org/curated/en/099011624132054588/pdf/P1787031cc...trusted

- ecb.europa.eu/stats/payment_statistics/html/index.en.htmltrusted

- fastpayments.worldbank.org/sites/default/files/2021-11/Fast%20Payment%2...trusted

- federalregister.gov/documents/2025/01/16/2025-00592/securing-the...trusted

- federalreserve.gov/mediacenter/files/financial-inclusion-panel-...trusted

- irs.gov/instructions/i1099inttrusted

- irs.gov/publications/p515trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Payment Method Conversion Rates by Country for Checkout Completion

Adding payment methods can lift checkout completion when the method matches how buyers prefer to pay in that country and still fits your fee and operating model. The real decision is not whether to add more methods, but which method to add in which country, and on what economics.

How to Expand Your Subscription Platform to Europe for Payment and VAT Readiness

Treat a European launch as an operations sequencing decision first. Lock VAT, payments, and compliance ownership before you scale localization or acquisition.

How to Expand Your Subscription Platform to APAC: Payment Methods Currency and Regulatory Landscape

Asia-Pacific (APAC) expansion requires country-by-country launches, not one regional motion. This guide helps you decide with payment, currency, and regulatory evidence so you do not mistake a strong regional headline for real launch readiness in your subscription platform.