Quick Answer

Handling payment exceptions at scale requires clear classification, a complete evidence pack, rail-specific routing, ledger-first corrections, and strict manual override approvals. Teams should separate disputes from corrections, keep compliance holds narrow, assign one owner for provider follow-up, and close cases only after provider status, ledger state, and user-facing status reconcile.

Why Payment Exceptions Need a Clear Routing Path#

Handling payment exceptions at volume takes more than a policy statement. You need clear routing, correction controls, and Manual Overrides guardrails so one failed payment does not turn into ledger drift, broken reconciliation, delayed settlements, or an unnecessary customer escalation. If you run payment ops, you need a routing rule your overnight team can follow without rebuilding the case.

This article is for platform finance, payments ops, and product owners making these calls in production across ledgers, reconciliation, settlement breaks, and payout execution. It focuses on the daily decisions that matter under pressure: who owns the case first, what evidence must exist before money state changes, when correction is safer than a dispute path, and when a human override is justified rather than simply convenient.

Before you start#

Use this guide if your team already handles exceptions across one or more payment rails and needs cleaner decisions under pressure. It assumes you already have payment requests, provider references, internal ledger entries, and event history, but your handoffs or escalation paths still create delay. If your handoffs still depend on chat context, you should fix that before you widen automation.

Public guidance from the Office of the Comptroller of the Currency and the Federal Reserve matters, but it serves a different purpose. The OCC Comptroller's Handbook is written for examiner supervision work. The OCC Payment Systems booklet is framed as an overview of payment types, risks, and risk management practices for OCC supervision of national banks and federal savings associations. That is useful control context, but it is not a queue ownership guide for platform teams.

The same limitation applies on the Federal Reserve side. Federal Reserve Financial Services are governed by twelve Operating Circulars, and Operating Circular 5 sets general terms across services. Effective January 5, 2026, Operating Circular 5 was retitled from Electronic Access to General Financial Service Provisions. That tells you where legal and service terms sit, not what your finance ops lead should do when provider status, ledger state, and payout timing conflict in real time.

This article fills that operating gap with practical checkpoints. Classify exceptions, assemble a minimum evidence pack, route by owner and exposure, correct in ledger-first order, and apply Manual Overrides only with the right approvals and audit trail.

One rule runs through everything that follows: if you cannot reproduce payment state from the case record, do not route it, correct it, or override it. That helps avoid a failure mode where teams fix the visible status first, then discover the ledger, provider status, and customer-facing state never converged.

If you want a deeper dive, read Airline Delay Compensation Payments: How Aviation Platforms Disburse Refunds at Scale.

Define what counts as a payment exception and who owns it#

Set your exception taxonomy and ownership map before you set SLAs. If one case can land in two queues, you can get reopen loops, duplicate outreach, and ledger fixes that lag behind customer messaging.

Define the exception classes#

Define exception classes by the operational question, not by who is complaining. You can use labels like data mismatch, settlement variance, provider failure, compliance hold, and customer dispute. This is an internal operating model, not a federally mandated taxonomy.

Use a single intake checkpoint: can a second reviewer tell from the first case note whether the issue is bad data, missing money, rail behavior, a policy gate, or alleged customer harm? If not, the class is too vague.

Split classes by rail and timing risk#

Handling paths change by rail, so split each class by rail and timing risk.

| Rail | What matters for triage |

|---|---|

| Automated Clearing House (ACH) | ACH is a batch network, and Federal Reserve exception guidance uses defined case types with reporting time frames, required fields, and supporting documentation. |

| Fedwire Funds Service | Fedwire is generally used for large-value, time-critical payments, with payment finality once credits post to Federal Reserve master accounts. |

| Real-Time Payments | Federal Reserve material describes participating institutions receiving final and irrevocable settlement for credit transfers, so state mismatches often warrant immediate review. |

| Payment Cards | Under Regulation Z, a billing error notice is written and identifies the type, date, and amount of the alleged error, generally within 60 days of the first statement showing the error. |

Assign default and after-hours owners#

Assign a default owner and, where needed, an after-hours backup. Ownership by class is an internal policy choice, but holds tied to AML or beneficial ownership procedures under 31 CFR 1010.230 should be routed to the compliance function.

Publish the first-triage rule#

Publish one first-triage rule where your queues are actually managed, and label it as an internal operating rule rather than a federal standard.

Before you assign the queue, check the provider reference against the latest ledger journal.

Prepare the minimum evidence pack before you route anything#

Avoid routing incomplete cases. If the next reviewer cannot reconstruct what happened, what state the payment is in, and why it belongs in that queue, the case is likely not ready for manual review. If the packet does not let you explain state in one read, your reviewer will slow down or send it back.

Start with identifiers#

Build the packet around identifiers first, not screenshots or chat excerpts. Depending on your systems, the packet may include payment request ID, provider reference, internal ledger journal IDs, a timestamped event timeline, and current status.

For ACH, this discipline is explicit. Exception handling ties submission to supporting documentation, and intake uses structured fields such as Settlement Date, Processing Date, Trace Number, and Amount. Missing required fields delay resolution, so it is worth applying the same intake-completeness standard across rails. A practical packet can include:

- payment request ID and account or customer identifier

- provider reference or trace number

- internal ledger journal IDs tied to the payment lifecycle (if used)

- timestamped event timeline, including request, provider events, retries, and holds (if available)

- current state across provider and internal records

Add compliance artifacts only when they matter#

Attach compliance artifacts only when compliance is the reason the case is blocked. Include the specific failed check and result, not just a label like "AML" or "KYC."

For identity controls, include relevant CIP verification results. For legal entities, include beneficial ownership information collected at account opening. If suspicious activity review is involved, keep the supporting documentation with the case record.

Add tax or account documents only when they change the outcome#

Add tax or account documents only when they change disposition. Do not default to attaching W-8, W-9, 1099, FBAR, or FEIE material to every packet.

| Document | When it matters | Article note |

|---|---|---|

| W-9 | Supports TIN collection for information returns | Do not attach by default to every packet |

| W-8BEN | Submitted when requested by the withholding agent or payer | Add only when it changes disposition |

| 1099 | Context matters when a transaction is reportable in a trade or business | Not automatic evidence for every exception |

| FBAR (FinCEN Form 114) | Reporting context for foreign accounts | Annual $10,000 aggregate foreign-account threshold; not automatic evidence for a single exception |

Use narrow rules. W-9 supports TIN collection for information returns. W-8BEN is submitted when requested by the withholding agent or payer. 1099 context matters when a transaction is reportable in a trade or business. FBAR is FinCEN Form 114 with an annual $10,000 aggregate foreign-account threshold, so treat it as reporting context, not automatic evidence for a single exception.

Route only reproducible cases#

Use reproducibility as an internal quality check. A second reviewer should be able to reproduce the routing decision from the packet without asking for missing basics.

The fast check is simple: what payment is this, what external transaction does it map to, what happened in time order, and what condition still blocks closure? That matters most when case types come with defined field requirements, reporting time frames, and response checkpoints.

You might also find this useful: Gateway Routing for Platforms: How to Use Multiple Payment Gateways to Maximize Approval Rates.

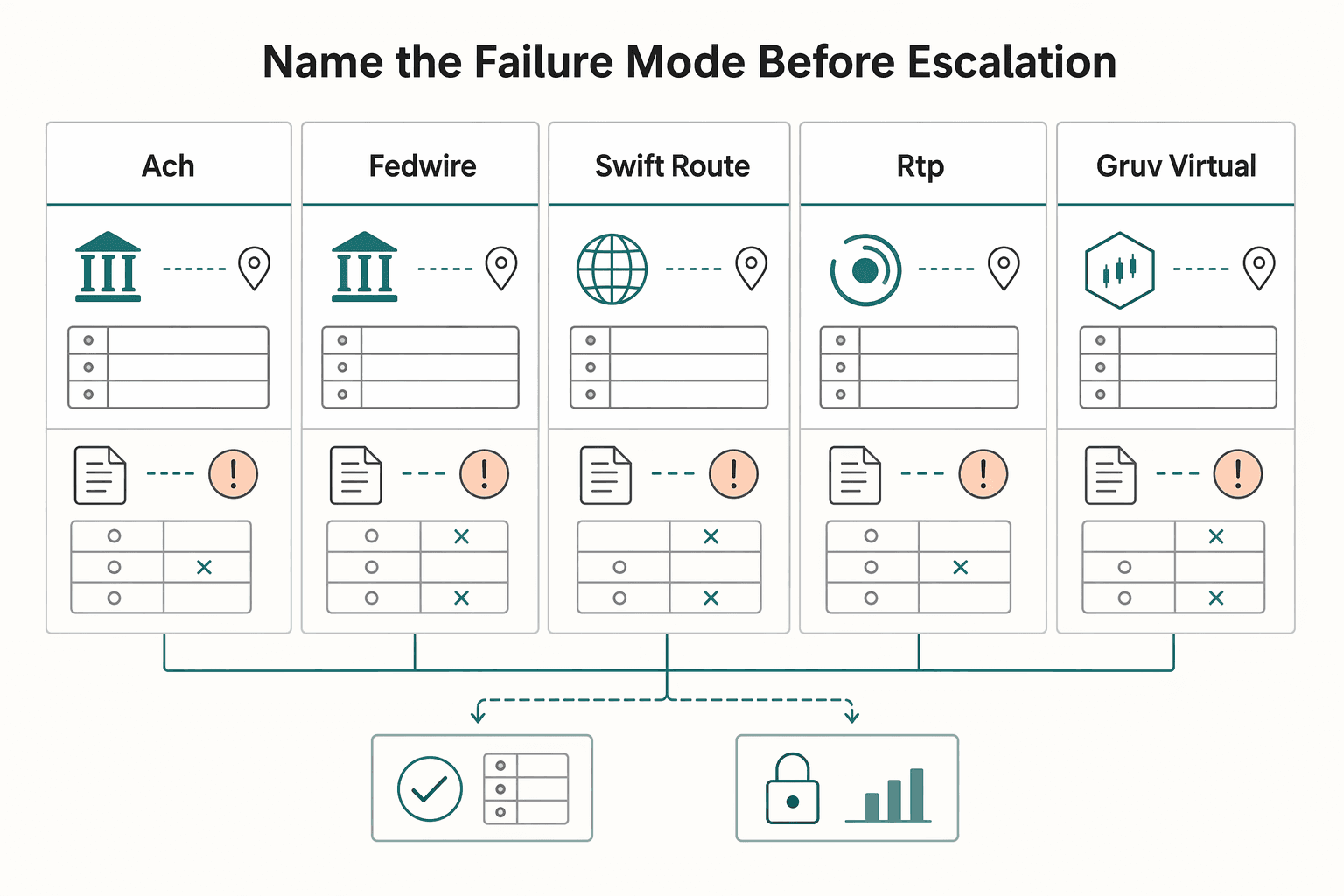

Map rail-specific failure modes before they become disputes#

Once the packet is complete, route by rail and timing boundary first, not by complaint wording. A single "payment missing" report can point to very different failure paths across ACH, Fedwire, SWIFT-route payments, RTP, Gruv Virtual Accounts, and Merchant of Record settlement flows.

Name the failure mode before escalation#

Before you escalate, name the failure mode. If the break is machine-detectable and repeatable, flag it for possible automation after policy and risk review.

| Rail or model | Common breakpoint | First recovery action | Escalate to third party when |

|---|---|---|---|

| ACH | Standard return vs disputed return confusion, or improper reversal on a non-consumer account | Confirm whether the case is a return or disputed return, then validate the return code and timing window. For R17 improper reversal on non-consumer accounts, use the 2-day return timeframe. | Return reason is still unclear, required fields are missing, or the R17 window is at risk without ODFI or processor action. |

| Fedwire | Ledger timing mismatch against wire confirmation | Check whether events are inside the same Fedwire business day (9:00 p.m. ET to 7:00 p.m. ET). If needed, use nonvalue operational messages such as return or report requests. | Order is accepted but internal state is still mismatched, or cutoff risk requires bank or provider action before close. |

| SWIFT-route payments | Aging cross-border item on a variable route | Reconstruct instruction and status by route or corridor, not as one generic international queue. | Item ages beyond corridor baseline, including slower routes that can run beyond two days, and the provider cannot supply route status. |

| RTP | Status divergence between ledger state and network response | Use the RTP Message Status Report (pacs.002) and reject reason codes to classify before any manual balance action. | pacs.002 status or reject output conflicts with your posted state and provider confirmation is required for final disposition. |

| Gruv Virtual Accounts (where enabled) | Unmatched deposit | Open an unmatched-deposit investigation and confirm provider credit or return status before final posting. | Provider details are incomplete or the deposit cannot be matched to an internal payment after investigation. |

| Merchant of Record | Settlement timing difference vs expected availability | Confirm which entity is the MoR, because the MoR carries legal transaction responsibility, including disputes and refunds. Then check whether payout delay is calculated in business days or calendar days for that country or configuration. | Your ledger assumes one settlement calendar while provider logic applies another, or liability is assigned to the wrong entity. |

Two operator checks help reduce avoidable disputes:

- Verify the external transaction identifier before treating the issue as a provider failure.

- Log the exact timing boundary that controls recovery options, such as Fedwire close or ACH return windows.

Escalate through third-party risk controls#

Escalate through third-party risk controls, not ticket volume. The June 6, 2023 interagency guidance frames third-party oversight as a lifecycle: planning, due diligence, contract negotiation, ongoing monitoring, and termination. Your escalation record should be auditable and reproducible.

Capture, at minimum:

- third party, service role, and relationship criticality

- timestamp of first contact and next committed update

- escalation path used and the exact unresolved dependency

If a second reviewer cannot quickly see which rail failed, what recovery was attempted, and why provider action is now required, the case is not ready for escalation.

For a step-by-step walkthrough, see How to Handle Payment Disputes as a Platform Operator.

Build a routing matrix your team can execute under pressure#

After you identify the rail failure, the next decision should be close to automatic. Your matrix should let any responder quickly decide whether a case is a dispute, a correction, or an investigation, who owns it now, and what approvals are required before funds move. We recommend making the owner and next action obvious enough that your responder can act without guessing. We also recommend tagging the required approval before funds move.

Build the matrix around decisions#

Build the matrix around decisions, not queue names. Include exception class, financial exposure band, compliance risk, owner, SLA, and escalation path. Use exposure bands tied to your internal Risk Assessment, not assumed universal dollar cutoffs. The point is consistent internal rules for when tighter controls apply and when scheduled review is acceptable.

| Exception class | Exposure band | Compliance risk | Owner | SLA | Escalation path |

|---|---|---|---|---|---|

| Correction | High | Medium to high if release or reversal is pending | Senior finance ops | Immediate triage, especially near cutoff risk | Finance lead, then bank or processor if external confirmation is required |

| Dispute | Any | Timing-sensitive when consumer-rights clocks apply | Dispute ops with compliance input as needed | Route by the applicable notice and resolution clock | Compliance review, then provider follow-up if needed |

| Investigation | Low to medium | Low unless flagged by internal risk signals | Payments ops or reconciliation | Short internal triage, then reclassify to dispute or correction | Provider or internal product or engineering owner if facts are incomplete |

That first branch matters because it reduces queue bouncing. ACH exception handling has historically relied on bilateral, time-consuming communication, so clear first-pass ownership matters even more as volume grows.

Tie each row to money-movement controls#

Tie each row to internal controls before it can trigger money movement. Ownership alone is not enough. The row should also say whether the owner can execute or only recommend for approval.

For higher-risk wire actions, separate initiator and approver roles. When full segregation is hard, use dual approval as a compensating control for high-exposure cases.

Fedwire often belongs in the strictest lane because it is used for large-value, time-critical payments and is immediate, final, and irrevocable once processed. Near key deadlines, including 6:45 p.m. ET for third-party-benefit transfer initiation, route discrepancies directly to senior finance ops plus an approver, not to a general queue.

Define each branch in plain language#

Define each branch in plain language so cases do not ping-pong between teams.

A dispute is a formal exception lane, not just "customer unhappy." In the ACH context, exceptions include disputes, notifications, questions, and requests for additional information. For payment cards, a written billing error notice should route to a billing-error lane that tracks its own clocks.

A correction means the internal state is known to be wrong and the next step is record correction or a release or return decision. An investigation is a temporary holding lane for missing facts, followed by reclassification.

If a case changes owner twice without changing class, add a branch rule. That is a sign the matrix is missing a decision point.

Set SLAs to the governing clock#

Set SLAs to the governing clock, then batch only where risk permits. Consumer EFT error handling is timing-bound. It allows 10 business days for determination after notice and a 60-day consumer notice window from statement timing. Payment-card billing-error handling follows different clocks, including a 60-day notice window and resolution within two billing cycles, no later than 90 days.

| Case type | Timing in article | Handling cue |

|---|---|---|

| Consumer EFT error handling | 10 business days for determination after notice; 60-day consumer notice window from statement timing | Set SLA to the governing clock |

| Payment-card billing-error handling | 60-day notice window; resolution within two billing cycles, no later than 90 days | Use a billing-error lane that tracks its own clocks |

| High-exposure wire discrepancies | Immediate | Route immediately rather than batching |

| Lower-risk mismatches | Scheduled triage when no statutory clock is at risk | Batch only where risk permits |

Operationally, that means you route time-critical, high-exposure wire discrepancies immediately. Lower-risk mismatches may follow scheduled triage under your policy when no statutory clock is at risk.

Provider escalation does not transfer accountability. Keep an internal owner on the row and log the next committed update time until final resolution.

If you are turning this matrix into runbooks and tooling, use the developer docs to align statuses, retries, and audit-ready operations.

Process corrections in ledger-first order so rework stays low#

Once a case is classified as a correction, work in ledger-first order: freeze the case, confirm source ledger entries, post correction journals, then reconcile downstream balances and statuses. This sequence helps reduce duplicate financial actions and lowers the risk of a case appearing closed before records align.

Freeze the case state#

Freeze the case state before broad status updates. Pause ad hoc retries, lock the active case state, and keep one evidence set attached to the case: request ID, provider reference, ledger journal IDs, and event timeline. This helps prevent conflicting fixes and preserves a clean pre-correction snapshot for review.

Confirm source ledger entries#

Confirm source ledger entries before posting anything new. Treat the ledger as the operational source of truth, and verify that each balance-impacting transaction maps back to an externally reported transaction.

Start from the original journal entries, not wallet projections or UI labels. If you cannot trace the source entry and the supporting external event cleanly, keep the case in investigation.

As a practical check, compare issued and cleared records, including amount, date, and any variance, and keep the case open until unexplained variance is resolved.

Post correction journals without rewriting history#

Post correction journals, but do not rewrite history. Use auditable reversing or offsetting entries so balances stay mathematically consistent and the correction trail remains reviewable.

Apply idempotent replay controls to retry paths so the same correction request does not post twice. Reused keys should return the original result, which supports deterministic recovery after timeouts or transport failures.

Because some providers may prune idempotency keys after 24 hours, keep an internal duplicate guardrail: one correction case ID maps to one intended journal action unless a reviewer explicitly opens a new case.

Reconcile balances and statuses after the journal posts#

Reconcile derived balances and statuses only after the correction journal is posted. Wallet views, settlement dashboards, and user-facing states should follow ledger truth.

Treat closure as a control check. Before closing, confirm provider status, internal ledger status, and user-facing status are consistent. For reconciled bank items, also confirm cleared and corrected issued records align and any variance is documented. Before you close, we recommend checking whether you could defend the record to audit without adding new context.

Sample corrected cases on a recurring cadence#

Run sample audits of corrected cases as an operational checkpoint, not a universal legal requirement. Sample across rails and exposure levels, then trace each case end to end: original request, provider reference, event and log history, source ledger entry, correction journal, reconciliation result, and final decision.

Retain records long enough to support later investigation and operational review. If a reviewer cannot reproduce why a correction was made, your case documentation is not strong enough.

Related reading: How to Set Up an IRS Payment Plan and Keep It Active.

Set strict rules for when Manual Overrides are allowed#

Manual Overrides should be rare, explicit, and reviewable. If people can bypass routing or release logic too easily, exception volume and repeat risk can climb back up.

Define the override gate#

Set a clear internal policy for when an override is allowed, and treat it as a control choice, not a universal legal rule. A practical default is to allow a bypass only when automated handling is not sufficient for the case and the case is fully documented.

Define the case packet before approval: request ID, provider reference, ledger journal IDs, event timeline, current status, and the exact action requested. If a responder cannot explain why automation was bypassed, keep the case in investigation.

Use a reproducibility check here too. A second reviewer should be able to read the case and reach the same decision without missing context.

Separate initiation from approval#

For high-risk actions, use dual control with segregation of duties: one person initiates, a different person approves, and both use separate credentials.

Do not treat informal acknowledgments as approval, and do not allow shared logins. If one person prepares, changes, and releases the same override, the control has failed.

Apply maker-checker discipline to actions like releasing funds, reopening settled cases, changing destination accounts, or force-closing exceptions. More approval layers can be configured in some systems, but two distinct people remain the baseline control pattern.

Protect the audit record#

Keep tamper-resistant audit records that can survive review. Capture who initiated, who approved, what event occurred, when and where it happened, the source event, and the outcome.

Log a reason code for why the override exists so decisions stay searchable at scale. At minimum, store event details, both user identities, timestamps, and the reason code. Protect logs from unauthorized modification or deletion.

Retire repeated overrides#

Manual overrides should stay exceptional, not become normal operations. Review override reasons regularly, and when the same reason keeps recurring, consider moving it into product logic, routing rules, or intake validation.

If a repeated reason code is treated as business as usual, you are preserving a design gap instead of fixing it. Define which actions qualify for bypass and the approval standard for each one so the override path stays controlled.

Handle compliance holds without stalling legitimate payouts#

Compliance holds should be narrow. If you treat operational failures as compliance issues, legitimate payouts can get stuck in the wrong queue and your real compliance work gets harder to see.

Classify holds by cause, not inconvenience#

Split holds into two paths at intake: compliance and operational. Use the compliance path for KYC, KYB, AML, sanctions, and CDD triggers, where CDD means ongoing monitoring for suspicious activity and keeping customer information current, including beneficial-owner information for legal-entity customers.

If the issue is missing payout data, a provider rejection, or a technical or business rail message error, keep it in the operational path unless a compliance trigger is actually present.

This split helps prevent false AML backlogs and keeps blocked and rejected transactions on separate handling paths. A practical control is to require a named trigger source before a case can enter the compliance queue. If no trigger is identified, route it out.

Define release conditions in plain language#

For each compliance hold type, define three things clearly: what clears the hold, who can approve under your internal policy, and what evidence must be retained.

| Hold type | Release condition | Evidence to retain |

|---|---|---|

| KYC or CDD refresh | Required customer information is updated and review is completed | Submitted records, review result, timestamp, case notes |

| Legal-entity verification | Missing beneficial-owner information is collected and checked | Beneficial-owner data source, reviewer identity, decision time |

| OFAC blocked property | Unblocking or transfer is approved under policy and reporting is completed | Block record, release decision, OFAC report when applicable |

For blocked-property cases, keep OFAC timelines explicit: if blocked property is unblocked or transferred, reporting is due within 10 business days, and records are retained for five years after unblocking.

Add VAT or tax gating only where eligibility depends on it#

Use VAT or tax checks only when payout eligibility depends on them, not as blanket gates.

For cross-border EU trade, VIES can be used to check VAT registration status, but it is a search engine rather than a master database. In the UK, domestic reverse charge rules apply only to certain goods and services, so universal VAT holds will overblock.

Handle tax profiles the same way. An incorrect TIN can trigger backup withholding workflows, but that does not mean every payout requires tax review. If tax status changes release eligibility, hold it. If not, keep tax outside the release chain.

Verify release integrity before the payout leaves hold#

Before a held payout is released, require one complete audit trail: original trigger, clearing document or check, reviewer identity, timestamps, and release action in one record.

If payment-card data contexts were involved, preserve access logging so access is traceable. For PAN display, keep masking limits intact, with no more than the first six and last four digits visible.

As an internal control, consider failing release when masked sensitive fields appear manually rewritten in the case record. Route those cases to investigation and correct data at the authoritative source before release.

Related: How to Scale Global Payout Infrastructure: Lessons from Growing 100 to 10000 Payments Per Month.

Track the few metrics that actually prove improvement#

If you only measure speed, you can make the queue look better while controls get worse. Measure speed and quality together, and split both by exception class and rail so rework does not disappear inside averages.

Measure the core five by exception class#

Track queue aging, first-touch time, time-to-resolution, reopen rate, and correction accuracy by class, such as data mismatch, settlement variance, provider failure, compliance hold, and dispute. Treat these as internal operating metrics, and keep classes separate so faster handling is less likely to mask early closure.

For customer-facing cases, pair timeliness with an accuracy check. CFPB complaint oversight focuses on timeliness, accuracy, and completeness, and complaint responses are generally expected within 15 calendar days. That is not a universal payout SLA, but it is a useful quality guardrail.

Use a simple verification loop: sample recently closed cases weekly and confirm ledger state, provider state, and user-facing status still match.

Segment by rail before reading trends#

Segment by rail before you read performance trends, because ACH, wires, and cards behave differently.

| Rail | Metric detail worth tracking | Why it matters |

|---|---|---|

| Automated Clearing House | Return rates by subtype, especially unauthorized, administrative, and overall debit returns | Nacha sets explicit levels at 0.5%, 3.0%, and 15.0%, which makes class-specific error patterns visible |

| Fedwire | First-touch and resolution time for high-value, time-critical cases | Fedwire transfers are immediate, final, and irrevocable once processed, with a 6:45 p.m. ET third-party initiation deadline each business day |

| Payment Cards | Monthly dispute and fraud counts or ratios | Visa monitors dispute and fraud levels monthly through a count-based VAMP ratio |

Keep additional rails separate as well, even when thresholds are internal, so correspondent-banking issues do not get buried inside ACH or card volume.

Read exposure and override signals together#

If you track value at risk in the active queue and the share of cases requiring Manual Overrides, treat both as internal control metrics with internal definitions. They are not regulatory benchmarks, but they can highlight where unresolved work still creates financial or operational exposure.

If reopen rate rises while time-to-resolution falls, treat that pattern as a warning signal to investigate, not proof by itself that quality is worsening. One possible failure mode is closing on a status update before reconciliation proof is complete, so tighten closure checks in the classes and rails where the pattern appears.

Fix the common mistakes that keep exception queues noisy#

Noisy queues usually come from a few preventable choices: vague intake, unowned provider follow-up, routine manual approvals, and weak closure checks. Fix those and you reduce ambiguity without adding unnecessary process.

Split disputes from corrections at intake#

Do not run disputes and internal corrections through one queue with one rule set. Under Regulation E, a notice of error is not the same as a routine balance inquiry, and computational or bookkeeping issues can fall under error handling.

Your intake should force a clear branch, such as customer notice of error, internal correction, or provider-side issue. If a case may qualify as a notice of error, treat it with timing discipline. Consumers generally have up to 60 days after the statement is sent to notify the institution, and institutions generally must determine whether an error occurred within 10 business days of receiving a notice of error.

Assign one owner for provider follow-up#

Provider dependency does not remove your responsibility to manage the case. Every provider-side exception should have one named internal owner and a documented next action.

Keep third-party follow-up visible in the case record, including the provider reference, last contact point, and next expected update. That keeps escalation and ongoing monitoring active instead of leaving the case in a generic waiting state.

Tighten manual approvals with dual control#

Manual overrides should be controlled, not treated as a default path. For sensitive approvals, enforce dual control so one person cannot complete the full process alone.

Capture the override reason and approver trail so repeat patterns are easy to review. When the same reason recurs, treat it as a process or rules-design signal, not just queue noise.

Block closure until reconciliation evidence exists#

Do not close on a status toggle alone. Closure should require reconciliation evidence that is timely, documented, and verifiable.

Set a closure gate that requires a completed comparison across related records, a clear variance explanation, and identification of needed adjustments.

Launch this in 30 days without breaking current operations#

This works best if you roll it out in a controlled way. A 30-day launch gives you enough time to make routing, evidence, and approval rules explicit while keeping live payment handling stable.

| Week | Focus | Grounded actions |

|---|---|---|

| Week 1 | Taxonomy, ownership, evidence packet | Lock the minimum exception taxonomy, name the accountable owner for each class, and use one shared evidence packet template |

| Week 2 | Routing and SLA rules for ACH and wire transfer | Publish rail-specific routing and SLA rules, with ACH timing windows and same-day wire escalation tied to Fedwire operating timing |

| Week 3 | Manual Overrides and closure training | Enforce dual control for high-risk actions, audit logging, and train responders on override justification and mandatory closure evidence |

| Week 4 | Baseline KPIs and choose fixes | Split baseline results by ACH and Fedwire, then prioritize one automation fix and one control fix |

Finalize taxonomy, ownership, and the evidence packet#

In week 1, lock the minimum exception taxonomy, the accountable owner for each class, and one shared evidence packet template across finance ops, payments ops, and compliance. Keep ownership explicit for cases that touch money-movement state versus ledger state.

Treat this as an internal-control design step, not an analyst-only exercise. The OCC framework places responsibility for effective controls with leadership, so ownership and decision authority should be named and clear.

Keep the evidence packet lightweight but reproducible for independent review. Include the core identifiers and timeline details needed to reconstruct the case, plus any compliance gate result that affected release.

Ship routing and SLA rules for ACH and wires#

In week 2, publish rail-specific routing and SLA rules for top exception classes, starting with ACH and wire transfer. ACH and wire need different handling because timing constraints differ, and Fedwire settlement is immediate, final, and irrevocable once processed.

Set ACH rules around class-specific timing windows, including contexts with 2-day and 60-day return timelines for applicable reason-code and account-type scenarios. Set wire escalation to same-day boundaries tied to Fedwire operating timing, including the 9:00 p.m. ET business-day start and 7:00 p.m. ET end, with message cutoffs before close. If Reserve Bank electronic access is in scope, align procedures and evidence handling to Operating Circular No. 5 controls.

Enforce Manual Overrides and train to closure standards#

In week 3, enforce manual overrides with dual control for high-risk actions and audit logging. Capture who initiated, who approved, what changed, why automation was bypassed, and what follow-up check is required.

Train responders on two decisions: when an override is justified and what closure evidence is mandatory. Keep second review independent so the person making the change is not the person validating completion.

Baseline KPIs and pick one automation fix and one control fix#

In week 4, baseline core exception metrics and split results by ACH and Fedwire before making changes. Use the baseline to identify top reopen causes, then prioritize one automation fix and one control fix.

Keep scope tight: fix one repeat issue that is automation-ready and one control weakness driving avoidable reopen loops. If resolution time improves while reopen rate rises, treat that as a control-quality warning and adjust closure standards before scaling further.

Conclusion#

Fewer reopens usually come from tighter controls, not more triage. A clearly documented workflow, explicit routing ownership, and tightly governed exception handling can reduce both risk and rework.

That is also the practical through-line in the control expectations behind this work: documented requests, clear accountability, dual control, segregation of duties, independent review, and prompt reconciliation. You do not need a heavy model. You need a small set of rules that gets enforced every time. If you want a copy-and-paste starting point, use this checklist:

- Define your exception taxonomy and assign a clear owner for each path.

- Require complete case documentation at intake so another reviewer can reproduce the case independently.

- Keep dispute and correction routing separate, including ACH error-on-authorized-payment cases (R11) versus no-authorization claims.

- For any Manual Override path, require initiator and independent approver controls with auditable reason tracking.

- Close cases only after reconciliation evidence and documented internal review are complete.

- Track a small, consistent KPI set and review repeat reopen causes regularly to drive root-cause fixes.

If your control documents still use the old title for Federal Reserve Operating Circular 5, update them. Effective January 5, 2026, it was renamed General Financial Service Provisions. When you are ready to validate this operating model against your own payout and reconciliation workflow, talk to Gruv.

Frequently Asked Questions

What is a payment exception at scale?

A payment exception is any case that still needs action, not just a failed payment. It can include disputes, notifications, questions, and requests for additional information. At scale, the goal is consistent classification and routing so the same issue is not handled differently across multiple queues.

How should payment disputes be routed differently from correction requests?

Route disputes to the team handling formal challenge workflows, and route corrections to the team that can fix payment and ledger records. A card dispute starts when a cardholder challenges a payment with the issuer, while correction work is usually an operational fix to transaction records or status. For consumer EFT error claims, apply Regulation E timing rules, including the 60-day notice window and the baseline 10-business-day determination window after notice.

When is a manual override acceptable, and who must approve it?

A manual override is acceptable when automation cannot safely resolve a time-sensitive case and the record is complete enough for independent review. The decision should be reproducible from the retained case evidence and timeline. High-risk overrides should use dual control with an initiator and an independent approver.

Which metrics best show whether exception handling is improving?

There is no universal KPI set for exception handling. Teams often track first-touch time, time to resolution, queue aging, reopen rate, correction accuracy, value at risk in queue, and override rate. Segment results by payment channel, and treat faster closure with rising reopen rates as a control-quality warning.

How do we apply high-level guidance from the OCC Comptroller's Handbook to daily operations?

Use the OCC Handbook as a control framework, not a queue playbook. In daily operations, that means explicit ownership, approval authority, evidence requirements, and review checks. Accountability for effective internal control stays with the board and senior management.

What details are still unclear in public guidance like Federal Reserve Banks Operating Circular No. 5?

Operating Circular No. 5 gives general terms for access and use of Federal Reserve Financial Services, but it does not define every exception case type or field-level procedure. Federal Reserve guidance says ERS details come from ERS-specific materials, and the Quick Reference Guide should be used with the ERS Guide referenced in OC 5 Appendix D. Use those materials to confirm case types, reporting time frames, action steps, and field requirements.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/02trusted

- ecfr.gov/current/title-12/chapter-X/part-1005/subpart...trusted

- ecfr.gov/current/title-12/chapter-X/part-1026/subpart...trusted

- fdic.gov/risk-management-manual-examination-policies/...trusted

- fdic.gov/news/financial-institution-letters/2023/fil2...trusted

- federalreserve.gov/paymentsystems/fedfunds_about.htmtrusted

- federalreserve.gov/paymentsystems/fedach_about.htmtrusted

- irs.gov/businesses/comparison-of-form-8938-and-fbar-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: