Quick Answer

Platforms should accept and disburse across 50+ currencies by verifying each corridor end to end, not by trusting vendor headline counts. Check the customer charge currency, settlement currency, where FX happens, and the beneficiary payout currency for every payer country, beneficiary country, and rail. Then prove acceptance and disbursement separately with docs, sandbox results, or live tests before launch.

Multi-currency payments for platforms without blind spots#

Treat acceptance, FX, and payouts as separate promises until you verify each target corridor. This guide shows how to plan for platforms that need to accept and disburse across multiple currencies using checkpoints rather than vendor headline claims.

Separate the promises first#

Start with the failure points you can actually hit in production. "Multicurrency payments" tells you a provider can handle money in different currencies, but not how funds settle, where conversion happens, or whether disbursement works in the countries and payout methods you need.

Provider currency counts are useful, but they are not corridor proof. One provider documents acceptance in 50 currencies across 160+ countries and territories. Another documents charging in over 135 currencies. Those numbers show breadth, not confirmed disbursement in the same currencies. For evaluation, break the claim into four checks: customer charge currency, funds received, where FX happens, and beneficiary payout currency.

Use precise terms early. Track:

- Presentment currency: the customer-facing charge currency

- Settlement currency: the currency funds are settled into

- If presentment and settlement differ, conversion occurs

For every launch corridor, confirm the presentment-to-settlement pair explicitly instead of accepting "supports multi-currency."

Put teams on one decision path#

Get Finance, Product, and Engineering on one decision path before demos. Product owns what users see. Finance owns how funds settle and how close works. Engineering owns lifecycle states and fund movement. If those tracks stay separate, checkout can look right while payout and reconciliation break later.

Use one shared flow: accept, settle, convert if needed, disburse, then reconcile. FX is not only a checkout event. It can show up in payments, transfers, payouts, application fees, and other transaction types. Assign clear ownership for where conversion is expected and where it would be a surprise.

A practical checkpoint is traceability. Can you follow one transaction from its original charge currency to the final payout batch without ambiguity?

Test claims by corridor and rail#

Test every capability claim at corridor level and by payment rails. Rails are the infrastructure that moves funds, and wire, card, online, and real-time flows do not behave the same way. Coverage can also vary by country or region and by payout currency, not just by having an integration.

| Field | What to record |

|---|---|

| Countries | payer country and beneficiary country |

| Currency pair | presentment currency and settlement pair |

| Payout setup | payout currency and payout method |

| Rails | collection rail and disbursement rail |

| Status path | expected payment lifecycle status path |

| Reconciliation | payout reconciliation method for matching transactions to settlement batches |

Design reconciliation around payout batches, not net totals. If a provider can show a currency count but cannot show corridor-level proof for both acceptance and disbursement, treat the capability as unverified until proven.

For a finance-systems view of multi-currency AP and reconciliation, see Intacct vs. NetSuite for Payment Platforms: Which ERP Handles Multi-Currency and High-Volume AP Better.

What to prepare before you talk to providers#

The corridor checks above only work if you show up with facts, not a generic request for "multi-currency support." If you skip corridor definitions, failure evidence, and close constraints, you will still have to do that work later, usually under more pressure.

Define launch corridors exactly#

Define your launch set at corridor level: payer country, beneficiary country, local currency, and the currency you expect to receive for each flow. Local currency is the customer-facing checkout currency. The received currency is what your platform gets when conversion happens. Track the expected payout method too, because payment-method support is country-specific, and some coverage tables depend on the funding-currency assumption.

Use one checkpoint: can the provider confirm each corridor exactly as written, not just "we support that region"? If the answer changes once you specify country or funding currency, treat the original claim as incomplete.

Bring last quarter's failures#

Bring last quarter's payment reality, not a polished summary. Show failed payouts, failure reasons, manual exceptions, and where reconciliation breaks. Ask for structured fields instead of anecdotes, including payout failure reason, affected destination account, and manual remediation steps. This matters because a failed payout can disable the external payout account involved, which creates Ops and Finance follow-up work.

If the pain is that close takes too long, state it in operational terms: unmatched payouts, missing status updates, or FX differences that Finance has to clear manually.

Name owners before the first call#

Set explicit owners across Payments Ops, Finance Ops, and Engineering before the first technical call. Align on webhook lifecycle, which events drive user-visible status, and where idempotency keys are required so retries do not create duplicate operations. Webhook endpoints can receive the same event more than once, so duplicate delivery has to be part of normal handling.

Use one written event map from provider callback to internal state change to ledger posting. If no one owns replay and backfill behavior, treat that as a launch risk.

Surface ERP close constraints early#

Bring ERP close constraints in early if Intacct, NetSuite, or Xero timelines are non-negotiable. In Sage Intacct, exchange rate types control how foreign-currency conversions are applied. In NetSuite, currency revaluation is part of month-end close. In Xero, multicurrency is plan-gated, so confirm plan entitlement before designing around it.

| ERP | Constraint |

|---|---|

| Sage Intacct | Exchange rate types control how foreign-currency conversions are applied |

| NetSuite | Currency revaluation is part of month-end close |

| Xero | Multicurrency is plan-gated, so confirm plan entitlement before designing around it |

If Finance cannot absorb custom month-end workarounds, say that in discovery. It is cheaper to reject a provider early than after you have mapped feeds, reports, and reconciliation exports.

Map the full money movement before vendor demos#

A demo only becomes decision-useful when the provider can walk one target corridor from acceptance to bank payout to reconciliation. Map that path first, then have vendors prove where money changes state and currency.

Map the full lifecycle#

Map each user segment and corridor as: accept -> hold or settle -> currency conversion -> disburse -> reconciliation. Build separate maps for each real flow you run, such as seller payouts, contractor payouts, and refunds, because support can differ by stage.

Use exact currencies, not placeholders. Mark local currency, the currency you receive, and any foreign-currency leg between them. If you plan per-currency settlement, confirm that each settlement currency you configure has its own supported bank account.

Mark every FX point#

Mark every point where FX can change the outcome. Separate three things on the map: where conversion executes, where additional FX fees may apply, and where rates are only indicative.

Treat quote values carefully. Some APIs say buy and sell amounts are indicative or that a quote is not a firm offer. Product and Ops should not treat those figures as guaranteed execution values. Where you show converted amounts to users or counterparties, present the FX rate and additional fees clearly.

Split rail flows#

Split card checkout and bank-transfer collection into separate rail flows. Card flows can require less customer action. Bank transfers can require payer action through their bank, which changes timing, messaging, and ops handling.

Include hold and capture where they exist. A payment can be authorized but still require capture, and mapping an authorization state to paid too early creates avoidable errors.

Define internal checkpoints#

Define internal checkpoints for Product and Finance, then map provider statuses into those checkpoints. Labels like submitted, pending, paid, returned, and held are useful internally, but provider terms can differ.

Require an event or report behind each internal state, including payout reconciliation that ties each bank payout to the underlying transaction batch. Keep returned explicit, since returned payouts are different from posted payouts and mean the transfer did not reach the destination.

Evaluate acceptance and disbursement as separate products#

Treat acceptance and disbursement as separate products in your evaluation. If a provider can collect in a corridor but cannot disburse on the rail you need, that is a partial fit, not a platform fit.

Build a two-column provider matrix#

Make each provider prove inbound acceptance and outbound payout separately.

| Provider | Inbound acceptance coverage | Outbound payout coverage | What to treat as unproven |

|---|---|---|---|

| Tipalti | Confirm inbound checkout support directly with the provider | Published payout coverage only: 196 countries and 120 local currencies on one page, and 200+ countries/territories and 120 local currencies on another; 50+ payment methods listed including ACH, local bank transfers, global ACH, card, wire transfer, and PayPal | Any inbound acceptance claim; any single definitive country count |

| Airwallex | Docs separately state collection support in 130+ currencies | Docs separately state local and SWIFT bank payouts to 200+ countries/regions and 90+ currencies | Method-level support for every currency, because docs warn some payment methods may not support all currencies |

| Veem | States it can receive payments in over 100 countries and 80+ currencies | States it can send payments to over 100 countries and 80+ currencies | Corridor-level method and cutoff proof until you validate it |

| J.P. Morgan Wallet | Positioned for receivables via APIs | Positioned for disbursements via APIs; Wallet cites 170+ countries and 120+ currencies, while Treasury Payments cites 120 currencies across 160 countries using 40 methods | Assuming Wallet figures apply to every J.P. Morgan product or API program |

| Medius | Confirm inbound checkout acceptance directly with the provider | Supplier-payment and AP messaging supports outbound payment evaluation only, with multi-currency and multi-country support | Any inbound gateway or checkout claim |

Add corridor proof fields#

For each provider and corridor pair, capture:

- supported local currency

- supported received currency

- payout method or rail, such as local clearing or SWIFT

- cutoff behavior, including timezone and banking-day rule

- evidence type, such as docs, sandbox response, or live test

Use the exact payer country, beneficiary country, local currency, and received currency from your money map. Headline totals are not enough. Airwallex documents 130+ collection currencies, but also says some payment methods do not support all currencies. For timing, record exact execution rules, such as Tipalti's 10:30 a.m. PST (11:30 a.m. PDT) same-day cutoff on banking business days and its value-date framing (T to T+1).

Apply one platform-fit rule#

Use one rule consistently: if acceptance works but reliable disbursement on the required rail does not, mark it partial fit. Do not let headline counts stand in for corridor completion.

Apply the same caution to J.P. Morgan figures across pages and products. Treat Global Payments 2 behaviors like idempotency and granular error codes as confirmation-required for your program, since that release is documented as pilot-only as of November 2024.

Label unknowns plainly#

Mark anything not proven in docs, sandbox, or live evidence as unproven. That includes inbound acceptance for Medius and inbound checkout for Tipalti.

For Veem, send and receive claims are useful, but they still do not prove the corridor unless you confirm currency pair, method, rail, and cutoff. In review, every target corridor should be labeled proven, partial fit, or unknown, with evidence attached.

Build a corridor evidence pack that can survive procurement#

If a reviewer cannot trace a corridor from acceptance proof to disbursement completion, treat that corridor as unproven. Build each record so someone else can verify payer country, beneficiary country, local currency, settlement currency, method, and whether both legs actually worked.

Capture proof artifacts for each corridor#

Create one record per corridor, not per provider. Include acceptance evidence, payout evidence, and the identifiers needed for later status checks. For outbound tests, store the provider payout ID exactly as returned. For example, PayPal status checks rely on payout_batch_id, so screenshots without returned IDs are weak evidence.

Include at least:

- API response screenshots or exported payloads for acceptance and payout creation

- successful payout test IDs or batch IDs

- provider confirmation notes for market or currency limitations

- a provider-specific return-code catalog

A second operator should be able to reproduce the test and determine whether the payout completed, returned, or is still pending.

Prove both directions on the same setup#

Where a provider offers both products, prove inbound acceptance and outbound completion on the same setup where possible. If collection and payout require separate products or programs, document that split explicitly.

For acceptance, use country-level method evidence, not broad global claims. For disbursement, record the exact rail, local currency, and settlement currency tested, because support can vary by country or region. Also capture FX legs when they exist. If presentment currency differs from settlement currency, show where conversion happened in the flow.

Record rollout constraints#

Coverage headlines do not catch the issues that break real rollouts. Failures usually show up in method-specific beneficiary data rules, unsupported payout corridors by region or currency, or market-specific gating. If required beneficiary fields are missing, payout creation can fail even when a corridor looks supported on paper.

Track these red flags:

- cross-border destination limits by country or region

- beneficiary data requirements that vary by method, rail, or country

- account-level limits such as whether local payout is supported

If provider docs require account-manager confirmation for region or currency specifics, keep the item open until you have written confirmation.

Maintain an unknowns register#

Keep a living register for anything not confirmed in docs, sandbox, or live testing. Label each item unknown, confirmed, or blocked, and assign an owner and date.

Include unresolved questions on routing, unsupported settlement-currency combinations, country feature tiers, and missing return-code explanations. A return-code catalog turns a generic "failed payout" into a practical operations and risk decision.

Do not approve commercials while material corridor unknowns are open. If a launch corridor lacks payout completion proof, required-field confirmation, or written market-gating confirmation, escalate before signature.

For a step-by-step walkthrough, see How Platforms Build Multi-Currency Sub-Wallets for Contractors.

Choose hold or convert with explicit FX rules#

Choose a default FX mode per corridor as a working model. Hold balances and convert near disbursement when timing is uncertain, and consider pre-converting when payout timing is reliable and quote controls are tight.

Map where FX starts#

Mark the first point where presentment differs from the currency you receive, because that is where FX starts. It may show up in payments, transfers, payouts, application fees, or other transaction stages, not only at checkout.

For each corridor, keep one row with payer currency, held balance currency, beneficiary local currency, and final received currency. If multi-currency settlement is available, record where it applies rather than assuming it applies across all rails or geographies.

Pick a default mode#

Use this as an operating heuristic, then validate it per provider and corridor:

| Condition | Suggested mode | Control requirement |

|---|---|---|

| Payout timing is volatile | Hold, then convert near disbursement | Re-check rate close to release |

| Payout timing is predictable and margin-sensitive | Pre-convert | Strict quote-expiry and payout-window matching |

When pre-converting, make quote handling provider-specific. Stripe documents extended quote windows of 5 minutes, 1 hour, or 24 hours (maximum lock duration: 1 day). Wise exposes rateExpirationTime, and quotes not used to create a transfer can expire within 30 minutes.

Store quote ID, quoted rate, expiry timestamp, intended payout batch, and expected received amount. If a quote cannot be tied to a specific payout window, treat the economics as unconfirmed.

Set markup governance before launch#

Set markup governance before launch, not after you start seeing margin drift. Define one written policy for who sets markup, where it is disclosed, and how changes are approved. Keep provider spread and platform markup separate in your pricing logic so support, finance, and treasury can reconcile outcomes.

If you show converted amounts to users, present both the FX rate and added fees at transaction time. Adyen's 3% markup reference is an example, not a default benchmark for your corridors.

Add margin-protecting failure handling#

Protect margin with explicit FX failure states and controls:

- If a quote is stale, expired, or past

rateExpirationTime, require re-quote before payout release. - If the refreshed rate breaches your approved spread tolerance, route to review instead of auto-release.

- If a quote is withdrawn or cannot be executed in-window, keep the transaction in a distinct pending-FX state, not paid.

Extended quotes can reduce uncertainty, but they are not binding offers and may be withdrawn. For each FX incident, retain the original quote, expiry time, refreshed quote, executed rate if any, provider response, and expected-versus-actual proceeds.

Related reading: Using an HSBC Expat Multi-Currency Account Without Single-Point Payment Risk.

Design payout routing and exception handling before launch#

Lock payout routing before you launch volume. Define one primary path and one explicit fallback per corridor and payout method, and treat compliance stops as hard stops, not rerouting opportunities.

Specify primary and fallback routes#

Build routing at corridor level, not provider level. Broad claims like support for 50+ currencies or 200+ markets do not prove your exact payer country, beneficiary country, rail, and currency combination.

For each corridor, record:

- Primary route

- Fallback route

- Cases where fallback is prohibited

Make prohibited-fallback cases explicit. If a payout is paused for missing or unverified KYC information, or blocked or rejected by sanctions controls, the action is to stop and clear the restriction, not try another rail.

Add hard-fail checks before money moves:

- Bank account currency matches configured payout currency

- Bank account location aligns with currency-receipt requirements where applicable

If either check fails, a fallback that looks available in product can still fail in operations.

Verification point: for each planned route, retain at least one successful test payout reference, observed statuses, and the tracing reference used by the provider. For SWIFT legs, retain the UETR for status tracing.

Define exception classes and owners#

Do not send everything to a generic "payments issues" queue. Define exception classes with a clear owner and the evidence required to close them.

| Exception class | Typical trigger | Primary owner | Evidence to retain |

|---|---|---|---|

| Returned payout | Failed or returned status; invalid account number, invalid routing number, unable to locate account, account closed | Payments Ops | Provider payout ID, return code, submitted beneficiary details, remediation outcome |

| AML or KYC hold | Payout paused because required information was not provided or verified | Compliance or Risk Ops | Hold reason, verification state, requested documents, release or reject decision |

| Unmatched beneficiary details | Missing or inconsistent originator or beneficiary information; destination setup mismatch | Onboarding Ops with Payments Ops | Submitted fields, validation result, corrected details, resubmission date |

| Delayed provider status | Stuck processing; posted without clear beneficiary receipt; intermediary-bank block | Payments Ops | Last webhook timestamp, provider case reference, UETR if applicable, beneficiary confirmation attempts |

Two points matter operationally:

- In some provider setups, a returned payout can disable scheduled payouts for the account holder, so remediation needs an owner who can restore eligibility.

postedis not the same as beneficiary receipt. Receiving banks can still delay release.

Set a pause rule before you scale#

Set the pause rule before you scale, not after failure rates climb. Use your failure-rate trigger as an internal rule, not an industry benchmark. If corridor failure rate exceeds your approved threshold for your defined number of consecutive review cycles, pause expansion, stop adding new beneficiaries to that route, and re-qualify before scaling again.

Keep re-qualification evidence-based:

- re-test primary and fallback paths

- review return-reason mix, such as invalid details, routing errors, or closed accounts

- recheck beneficiary-data and compliance-gate requirements

Measure timing carefully. In one provider lifecycle, regular-speed payouts may confirm in 1-2 business days and then take another 3 business days to reach the receiving bank. Returned payouts are often visible in 2-3 business days, but may take longer by recipient country.

Add investigation and communication SLAs#

Set SLAs around user impact, not queue activity. Define separate targets for investigation start, provider escalation, and beneficiary communication, and assign platform ownership for outbound updates when payouts are paused or interrupted.

Use status-aware handling:

- Returned payout with clear code: investigate immediately and request corrected details

- Delayed SWIFT status: open provider tracing and use UETR before declaring loss

- Platform-initiated pause: account for in-flight payouts that can remain pending up to 10 days

If you use manual payout controls, make sure exception queues do not hold funds past country-specific limits defined by your provider program (for example: Thailand 10 days, United States 2 years, all other countries 90 days in one policy).

For a more specific look at FX exposure on cross-border flows, see Currency Risk for Platforms Collecting USD and Paying INR.

If you are finalizing fallback rules and ownership, review the payout API and status model to align routing, retries, and exception handling before launch: Explore Gruv Payouts.

Implement webhook lifecycle and idempotent retries#

Treat webhook handling and idempotency as money controls. Your system should absorb duplicate and delayed callbacks, and tolerate out-of-order delivery where providers do not guarantee order, without creating duplicate disbursements or premature ledger posts.

Accept fast and store the raw event#

Use a strict intake pattern: return 2xx quickly, store the payload, then process asynchronously. Retry behavior varies by provider, so this protects you from unnecessary redelivery load and missed events. Stripe automatically resends undelivered events for up to three days, PayPal retries non-2xx deliveries up to 25 times over 3 days, and Adyen can retry for up to 30 days.

| Provider | Retry behavior | Window |

|---|---|---|

| Stripe | Automatically resends undelivered events | up to three days |

| PayPal | Retries non-2xx deliveries | up to 25 times over 3 days |

| Adyen | Can retry failed deliveries | up to 30 days |

Persist enough on first receipt to support reconciliation and incident review. At minimum, store:

- provider name, event ID, event type, receipt timestamp, raw payload, and signature verification result

- provider object ID used for reconciliation, such as payout or transfer ID

- internal processing state, such as

received,validated,applied,ignored_duplicate,failed

Verification point: from storage alone, you should be able to answer did we receive this event? and did we already apply it?.

Enforce idempotency on requests and events#

Protect outbound API retries and inbound webhook processing separately. For payout creation, send a stable idempotency key on retries. Stripe returns the first recorded result for a reused key, including failures, and PayPal warns that omitting PayPal-Request-Id can duplicate execution.

For inbound events, de-duplicate by provider event ID before state changes, notifications, or ledger writes. Stripe explicitly notes the same webhook event can be delivered more than once, so request-level idempotency is not enough.

Use a practical control split:

- one request idempotency key for payout creation retries

- one event-ID de-duplication log for webhook intake

- one ledger-posting guard keyed to the economic transaction, not only the webhook event

Separate display status from finality#

Keep user-facing status and accounting finality separate. Pending funds are not yet withdrawable or spendable, and availability timing can differ from display status. Adyen also documents payout statuses that are not final.

Keep separate fields:

- display status: updates from trusted provider lifecycle events

- accounting finality: updates only when your settlement or availability confirmation rule is met

This prevents Product from showing a payout as complete while Finance still lacks settlement finality.

Build replay and backfill early#

Assume you will need reprocessing. Event ordering is not guaranteed for at least Stripe EventBridge destinations, and Stripe can continue automatic retries even after manual undelivered-event processing. Replays need to call the same idempotent transition path as normal intake.

Define backfill triggers, such as endpoint downtime, signature-validation outage, queue backlog, or provider-status mismatch. Record replay evidence:

- event range requested

- internal replay job ID

- counts received, applied, and ignored as duplicates

- open exceptions

If an older event arrives after a newer one, apply transition rules that prevent stale state regressions unless your state model explicitly treats that event as a reversal.

Add compliance gates and audit evidence into the transaction path#

Compliance controls should sit inside the money path itself. Funds should move only when the right risk checks are complete and the evidence is traceable.

Put checks where risk changes#

Use a risk-based approach, not one uniform rule across all users and corridors. Start with onboarding: identify the customer and verify identity using reliable, independent information. For business onboarding, include beneficial ownership evidence that is adequate, accurate, and up to date on true owners.

Then add secondary checks at risk-changing moments, such as flagged activity or sudden destination-account changes. Keep this policy-based by corridor, rail, and user-risk profile rather than treating it as a universal legal trigger in every jurisdiction.

Verification point: for one held payout, confirm you can see the trigger, evidence reviewed, reviewer, and release timestamp.

Link approvals to the money trail#

Every approval should connect cleanly to the money trail. Your audit trail should support forward and backward tracing, for example: request -> provider reference -> ledger entry -> reconciliation export, and back again. Keep that chain durable so Finance and Risk can resolve exceptions without manual joins.

Store at least:

- internal request ID

- provider reference or payout ID

- ledger entry ID

- reconciliation export row ID

- corridor, local currency, received currency, and risk decision code

A practical check is whether Finance can start from a reconciliation break and trace back to the original approval path without Engineering intervention.

Hold by policy, not blanket blocks#

Use policy-gated holds by corridor and user-risk profile, with explicit escalation rules for higher-risk cases. When suspicious activity or higher-risk scenarios appear, simplified CDD is not appropriate, so your policy should define when a flow moves from straight-through processing to review.

Use observable triggers defined in policy, and record override reasons so you can later prove which rule set governed each payout.

Minimize PII in logs#

Keep logs and events limited to what is necessary, and make sure you can prove compliance later. Prefer masked account details, internal IDs, decision outcomes, timestamps, reviewer IDs, and document reference IDs. Avoid logging full passports, full account numbers, or raw onboarding files.

If card-data environments are in scope, PCI DSS 10.2 requires automated audit trails that can reconstruct key access events, and PCI DSS 3.2 prohibits storing sensitive authentication data after authorization, even if encrypted. Retention is jurisdiction- and scope-specific. As a US example, BSA guidance says most bank records should be retained for at least five years where applicable.

Build reconciliation and close routines before scaling volume#

Lock reconciliation before volume grows, or close turns into a manual chase across provider reports, your ledger, and your ERP. The operating goal is simple: Finance can trace each movement from provider statement to ledger event to ERP posting, including FX differences, without routine Engineering help.

Define the three-way match#

Set the control first: tie out provider output, internal ledger activity, and the ERP entry in Intacct, NetSuite, or Xero each cycle.

Stripe frames payout reconciliation as matching bank-received payouts to settled payment batches, while Adyen supports transaction-level settlement reconciliation. The report shapes differ, but your close process should support both batch-level and transaction-level tracing.

In Xero, reconciliation matches bank statement lines against ledger transactions. In NetSuite, close tasks are sequenced on the Period Close Checklist and should be completed in order. In Intacct, keep posting detail that preserves currency and account context to support revaluation.

Track these references for each reconciled item:

- provider payout or settlement reference

- internal request or ledger ID

- bank statement line or provider statement row ID

- transaction state at posting time

- source, conversion, and payout currencies

- ERP journal or posting reference

Verification point: start from one bank payout and confirm Finance can trace forward and backward without querying raw events.

Reconcile by state and currency leg#

Do not reconcile on net totals alone. Reconcile by transaction state and by each currency leg so you can catch settlement timing gaps and other breaks earlier.

Stripe balance transactions include state, such as pending and available, and availability depends on settlement timing. A clean net match can still hide a break if your ledger treats funds as final before the provider does.

At minimum, separate checks by state transitions and by money legs: collection currency, conversion outcome if any, and payout currency.

Add FX variance checks to close#

Run FX variance checks during close, not only when someone flags margin drift. Compare expected converted amounts in your records to executed amounts posted by the provider, then verify where the variance is recorded in the ERP.

NetSuite can include an Exchange Rate Variance account in some account structures. Intacct's revaluation report supports monthly entries for FX fluctuations. Under IAS 21, qualifying exchange differences are recognized in profit or loss, so gain/loss treatment paths should be clear in your mappings.

Red flag: if Finance cannot separate timing effects, fees, and exchange movement, your account mapping is still too coarse.

Publish a standard exception report#

Use a standard exception report so Finance can clear common breaks without Engineering help. Group by exception type, owner, and next action, not just unmatched lines.

Typical groups can include unmatched payout, state mismatch, failed payout, missing ERP post, and FX variance. Stripe's reconciliation reporting includes failed-payout breakdowns, which is a useful model for payout-side triage.

If provider statements, ledger entries, and ERP postings cannot be joined with shared references in that report, fix identifier design before you scale volume.

For reserve planning in less stable markets, see How to Build a Currency Reserve Strategy for Marketplace Platforms Operating in Volatile Markets.

Common mistakes that delay multi-currency launches#

A common launch delay is treating capability labels as production proof. Once scope is defined, remove these four assumptions before go-live.

Separate acceptance from disbursement proof#

Do not treat "supports multi-currency" as proof that both sides of your corridor work. Presentment coverage, where funds land, and payout-method availability can differ by country and by payer or payee setup.

For each corridor, verify separately:

- presentment currency on the charge side

- where funds settle

- payout method availability on your required rails

Red flag: you have acceptance claims like "135+ currencies," but no corridor-level proof that disbursement works for the same flow.

Harden the webhook lifecycle#

Webhook failures can create avoidable launch-week rework. You need to handle duplicate deliveries, retry windows, and stale snapshot payloads before money starts moving.

Use idempotency keys on create and update operations, and retain them long enough for realistic retries. Webhooks can be redelivered for up to three days, and idempotency keys may be pruned only after at least 24 hours.

Verification point: replay the same event and the same payout-create request, then confirm you get one ledger effect and one disbursement.

Set FX markup by corridor#

A single global FX markup can be too coarse for real corridor economics. Conversion can depend on provider rate sourcing and can include explicit conversion fees, so margin and customer impact can vary by corridor.

If you operate in the EU, Regulation (EU) 2019/518 requires transparency on currency conversion charges for cross-border payments within the Union. At minimum, log rate source, quote timestamp, fee component, and customer-visible disclosure per conversion.

Keep review-ready evidence logs#

Skipping evidence logs can slow risk review and incident response because teams may not be able to quickly prove what happened. Audit logs support anomaly detection and forensic analysis, not just compliance.

For exception paths, store:

- provider event ID

- API request ID

- idempotency key

- internal ledger ID

- presentment and received currencies

- operator action

Verification point: pick one failed or returned payout and confirm you can trace request, provider event, and ledger impact without raw-log archaeology.

Related: Xero Multi-Currency for Payment Platforms: How to Reconcile Foreign Currency Payouts.

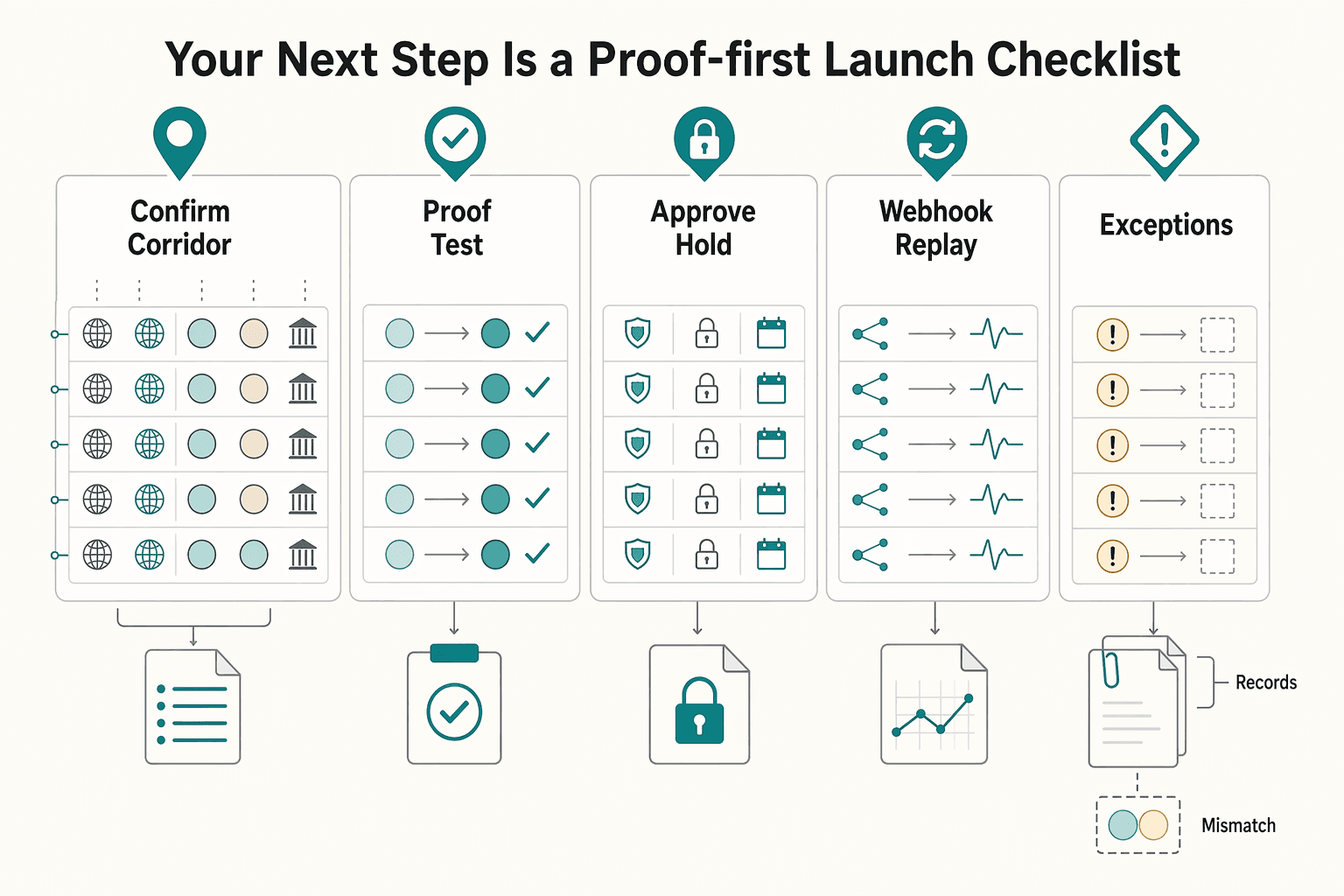

Your next step is a proof-first launch checklist#

Launch only when every corridor has a named owner, a tested local-currency-to-received-currency path, and evidence Finance, Risk, and Engineering can review.

- Confirm the corridor list and lock currency pairs.

For each corridor, document payer country, beneficiary country, presentment or collection currency, required local currency, the currency you expect to receive, and target rail. Presentment and settlement are separate dimensions, and FX applies when they differ. One provider example shows over 100 submission currencies but 18 settlement currencies, so record both values explicitly. Verification point: each corridor row has one exact currency pair and one exact rail.

- Proof-test acceptance and disbursement on the exact rails you plan to run.

Treat inbound acceptance and outbound payout as separate capabilities until both are proven. Headline claims like "50+ currencies" or "200+ markets" are not enough without successful tests for your payer-country and beneficiary-country pair on the intended rail. Save evidence: API responses, test transaction IDs, payout references, return codes, and provider notes. If card acceptance passes but local payout fails, mark the corridor as partial fit, not launch-ready.

- Approve hold-versus-convert rules before exposing volume.

Decide whether funds stay in local currency or convert into a preferred received currency, and assign ownership for quote timing and exchange-rate markup approval. Some providers support locked FX quotes and merchant-controlled markup, but quote-expiry behavior is provider-specific, so include a stale-quote branch. Verification point: each corridor has explicit rules for hold or convert, quote refresh, and fee pass-through.

- Validate webhook lifecycle behavior and make retries duplicate-safe.

Acknowledge webhooks quickly, then process business logic after receipt. Adyen marks delivery as failing if it does not receive acknowledgment within 10 seconds and can retry failed deliveries for up to 30 days. Stripe can resend undelivered events for up to three days and only returns events from the last 30 days for manual recovery. Build replay procedures and idempotency protections for payout creation, status updates, and ledger posting. Stripe notes idempotency keys can be pruned after at least 24 hours. Adyen states keys are valid for a minimum of 7 days. Red flag: if you cannot replay safely without creating a second payout or ledger entry, you are not ready.

- Finalize compliance gates, exception ownership, and escalation paths.

Use a risk-based AML/CFT framework aligned to FATF Recommendations, then define your own gate placement and approvals. Assign who handles held payouts, beneficiary-data mismatches, delayed provider statuses, and beneficiary communication. Verification point: each exception class has a primary owner, backup owner, and escalation route.

- Sign off the Finance close pack before scaling volume.

Finance should reconcile by transaction state and currency leg, not only net cash movement. Confirm ERP mapping for Intacct, NetSuite, or Xero, and test partial failures, cross-currency conversion edge cases, and quoted-versus-executed FX differences. In Xero, cross-currency reconciliation may require a clearing account to convert both sides into base currency. In NetSuite, open balances must be revalued before period close, and exchange-rate variance postings must be understood. In Intacct, multi-currency enablement cannot be turned off later. Verification point: Finance can produce daily controls and reconciliation exception reports without Engineering hand-holding.

When your checklist is complete and you need corridor-level confirmation for your launch plan, request a scoped walkthrough with your ops and engineering constraints: Talk to Gruv.

Frequently Asked Questions

What is the practical difference between accepting in many currencies and disbursing in many currencies?

They are separate capabilities. Acceptance is the presentment currency shown and charged at checkout, while disbursement depends on the currency the destination account can actually receive. That is why a provider can show broad inbound currency support but still have a narrower settlement footprint.

Do multi-currency platforms always settle in local currency?

No. Some setups auto-convert incoming funds into a home-country default currency unless multi-currency settlement is configured. If payout accounts are missing for specific currencies, funds can also move into a primary settlement currency instead of staying local.

How should we evaluate exchange-rate markup against payout reliability and margin?

Evaluate FX as a route decision, not only a rate comparison. A tighter quote matters less if the payout path falls back from local payout to cross-border transfer, where timing and bank-fee exposure can change. Confirm rate sourcing, explicit conversion fees, and any quote lock or refresh behavior before modeling margin by corridor.

What proof should we require before believing a provider can handle 50+ currencies for our use case?

Require corridor-level proof, not headline counts. Validate the exact payer country, beneficiary country, presentment currency, received currency, payout method, and whether the flow is like-for-like settlement or conversion. Also confirm whether the published currency list is card-only, since local payment methods can support fewer currencies.

Can one setup reliably run high-volume real-time operations and cross-border payouts?

Sometimes, but only in the rails, currencies, and countries your corridors actually support. One integration may simplify collection and payout orchestration, but it does not guarantee real-time payout in every market or method. Treat pilot or limited-availability conversion features as higher-change-risk corridors.

What are the first warning signs that a corridor is not production-ready?

The first warning sign is aggregate currency claims without country or region payout-table proof for your corridor. Other signals are no local payout path, forced cross-border fallback, or missing payout-account coverage that reroutes funds into an unplanned primary settlement currency. Card support without local-method confirmation is another common miss.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- bsaaml.ffiec.gov/manual/Appendices/17trusted

- docs.stripe.com/connect/currenciestrusted

- docs.stripe.com/api/idempotent_requeststrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-V/part-5...trusted

- justice.gov/archives/opa/media/1341411/dltrusted

- paypal.com/us/business/make-payments/enterprise-payoutstrusted

- cybersource.com/en/solutions/payment-acceptance.htmlexternal

- fatf-gafi.org/content/dam/fatf-gafi/recommendations/Explan...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: