Quick Answer

Use HSBC Expat as a storage anchor, not as your only account. The article recommends a three-tier system: keep core funds in HSBC Expat, use a separate movement layer for day-to-day cross-border payments and FX, and maintain a compliance layer for statements, balance tracking, FBAR review, and Form 8938 review. That reduces single-point payment risk and keeps reporting clearer.

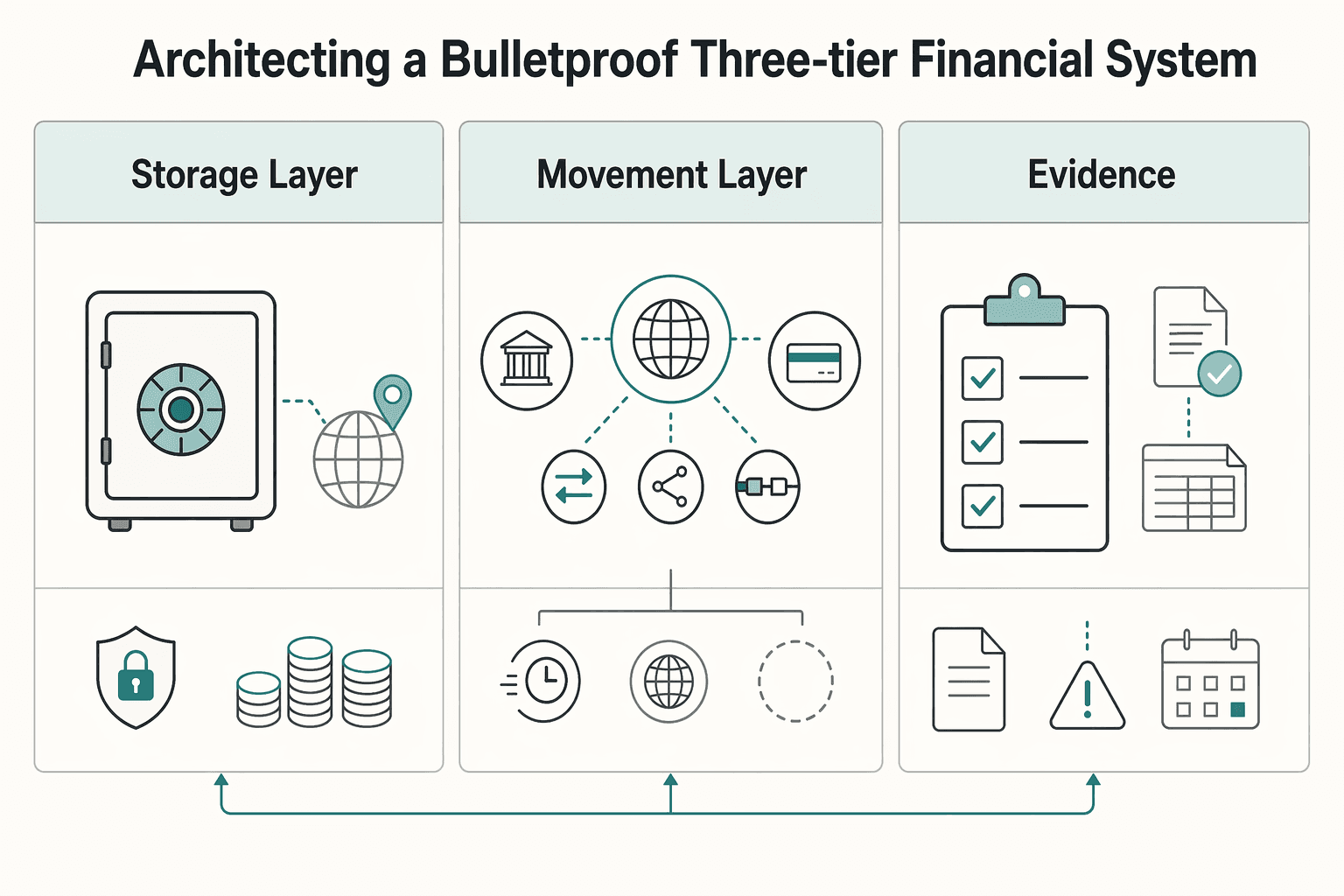

Beyond the Bank: Architecting a Bulletproof Three-Tier Financial System#

One account is rarely enough for international client cash flow, because you are asking one provider to do three different jobs: store capital, move money, and support compliance across accounts. A better approach is to assign each job to the right tool:

| Layer | What it does | Grounded note |

|---|---|---|

| Storage layer (institutional anchor) | Park core funds with stability as the priority | HSBC Expat fits best as the storage anchor |

| Movement layer (multi-currency transactions) | Optimize payout speed, routes, and FX execution | A bank can be strong for storage and still be slower for daily cross-border payouts |

| Compliance layer (visibility and records) | Track balances, statements, and reporting data across providers | FBAR uses the aggregate value across foreign accounts once it exceeds $10,000 at any point in the year |

In that setup, HSBC Expat fits best as the storage anchor. HSBC presents it as a central account that can stay with you when you move, but it does not replace the rest of the stack. The base current account is in GBP, USD, or EUR. Global Money can hold up to 19 currencies and transfer in more than 50, but the payment rails still differ. HSBC says transfers between HSBC accounts can be instant. Non-HSBC transfers can take 1 to 3 days.

That distinction matters because delays, conversion loss, access risk, and messy reporting often come from using the wrong tool for the job. A bank can be strong for storage and still be slower for daily cross-border payouts. A fintech may be useful for movement, but safeguarding is not the same as deposit insurance. The FCA notes customers can face losses or delays if a firm fails. For HSBC Expat specifically, deposits are not covered by UK FSCS. Jersey depositor protection is capped at £50,000 per depositor per Jersey banking group.

Before you choose tools, score each one on four checks:

- Stability: protection model, jurisdiction, and continuity if you relocate

- Transfer speed: your actual payout route, not the headline promise

- FX transparency: rate clarity before you confirm

- Compliance visibility: whether you can maintain complete records across foreign accounts

Do not skip the last check. If you are a U.S. person, FBAR uses the aggregate value across foreign accounts once it exceeds $10,000 at any point in the year. It is not a per-account test.

With that screen in place, the next step is to evaluate each tier by job, tradeoffs, and the point where it stops being the right tool. For the bank-account side of the setup, see A Guide to Opening a Bank Account in Hong Kong as a Foreigner.

Tier 1: The Institutional Anchor#

Use the HSBC Expat multi-currency account as your treasury base, not your day-to-day operating account. Park core funds here and maintain a cross-border banking relationship. If you need faster payouts or tighter FX execution, hand that work to later tiers.

In this model, the institutional anchor is the central offshore base account that holds core funds and connects to local accounts for everyday banking. Think of it as a passive vault: you keep capital there deliberately, then move working funds to other tools. Multi-currency holding means keeping balances in multiple currencies within one digital account structure. FX margin is the conversion spread built into HSBC's quoted exchange rate.

HSBC places Expat squarely in this role. The Expat Bank Account is held in Jersey and offered in GBP, EUR, or USD. After opening that base account, you can add Global Money, a mobile-only account in the HSBC Expat app. Global Money lets you hold 19 currencies and send or spend in over 50 currencies across 200 countries and regions.

What the product looks like in practice#

Check fit before you apply. One published route is to save or invest £75,000 within 3 months of account opening. Another is a salary of at least £120,000 paid into your Expat Bank Account. HSBC says applicants should hear back within 10 days. Verify the current eligibility requirement before you rely on it.

Before you submit, decide which eligibility route you will use and line up the supporting evidence. That can reduce late friction around funding expectations, app setup, or documents.

| Tier 1 strength | Practical use case | Tradeoff you accept |

|---|---|---|

| Jersey-held base account | Park reserves in a cross-border base | Protection follows Jersey DCS terms, including £50,000 per depositor per Jersey banking group |

| Base account in GBP, EUR, or USD | Hold treasury funds in a major invoicing currency | Core account is not itself a 19-currency wallet |

| Global Money with 19 currency balances | Hold funds in multiple currencies before conversion | FX quote includes an HSBC margin |

| Global Money transfer rails | Move funds from the app to other accounts | Non-HSBC app payments are typically 1 to 3 days, not always instant |

| Mobile-only Global Money | Manage balances and transfers in-app | Mobile-only workflow may not fit every approval or record-keeping process |

Where Tier 1 stops#

Tier 1 is for capital storage and basic movement, not the fastest payout routing, the best conversion shopping, or full compliance tracking across all foreign accounts. HSBC notes that non-HSBC app transfers usually take 1 to 3 days, third-party fees may apply, and exchange rates include an FX margin.

It also does not handle compliance for you. If you are a U.S. person, FBAR is triggered when the aggregate value of foreign accounts exceeds $10,000 at any point in the year. It is filed through BSA E-Filing separately from your tax return. Use Tier 1 for capital and relationship stability, then hand payout optimization to Tier 2 and reporting control to Tier 3.

For the workflow side of this, read Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe.

Tier 2: The Agile Fintech Fleet#

Use Tier 2 as your day-to-day execution layer, not your reserve layer. This is where you run invoicing and payouts for potentially faster settlement, tighter FX execution, local payout rails, and multi-currency operating balances.

| Provider | Stated feature | Cited cost or timing |

|---|---|---|

| Wise | Businesses can receive money with local account details at the speed and price of local payments; supports 40 currencies | Uses the mid-market rate for conversion |

| Revolut Business | Offers local and global account details | 0.6% exchange fee above monthly plan allowance |

| HSBC Global Money | Can hold 19 currencies and transfer in over 50 currencies | No HSBC transfer fees; non-HSBC transfers can take 1 to 3 days |

In practice, this means using a multi-currency operating account to receive client payments, convert when needed, and pay out through the best available route. Wise says businesses can receive money with local account details at the speed and price of local payments, supports 40 currencies, and uses the mid-market rate for conversion. Revolut Business also offers local and global account details. That is a different job from Tier 1, which is better suited to holding capital.

What Tier 2 does best#

Tier 2 is the right choice when the payment is operational, frequent, or time-sensitive. If a client can pay your local account details, you can often reduce friction and cross-border payment drag. If you need to pay contractors in their local currency this week, this is usually the right layer.

Cost still depends on the route and the plan. Wise states mid-market conversion in-account. Revolut Business states a 0.6% exchange fee above monthly plan allowance. HSBC Global Money can hold 19 currencies and transfer in over 50 currencies with no HSBC transfer fees. HSBC also states that non-HSBC transfers can take 1 to 3 days.

| Decision factor | Use Tier 2 | Route to Tier 1 |

|---|---|---|

| Transaction purpose | Client invoicing, contractor payouts, recurring vendor payments, card spend | Reserve holding, larger inbound payments, capital you do not need daily |

| Urgency | You need local-speed execution; some routes may be instant, but not all | Timing is less critical, or payment is between HSBC accounts where HSBC says transfers can be instant |

| Cost sensitivity | You want local account details and tighter FX execution | You accept slower movement to keep funds in the institutional base |

| Restriction risk | Payment is routine and well documented | Payment is business-critical or unusually large, where a temporary limitation would disrupt operations |

The real risk is interruption#

The main Tier 2 risk is temporary account restriction during routine or regulatory checks. Wise says it may temporarily restrict accounts while checks are completed. Revolut Business says limitations can affect transfers, card payments, merchant actions, and exchanges, and review can take up to 15 business days.

Treat that as a normal operating risk. FCA guidance also says balances held with non-bank payment providers are not FSCS protected if the provider fails. Protection is instead through safeguarding. That is why Tier 2 should remain your execution layer, not your treasury layer.

Keep a restriction-ready checklist#

If you rely on Tier 2 for live operations, prepare for a review before one happens. Keep these basics ready:

| Checklist item | Primary rule | Direct note |

|---|---|---|

| Documentation readiness | Keep invoices, contracts or statements of work, legal counterparty names, expected amounts, and proof of delivery ready | Ready to upload |

| Account redundancy | Keep at least one backup execution route plus your Tier 1 details | Test both before you need them |

| Cash-buffer rules | Do not park your next essential payroll, tax, or rent cycle in one provider | Sweep excess operating cash back to Tier 1 on a schedule |

Tier 2 only delivers real speed and cost benefits if you can still see the whole picture across all accounts. That is where Tier 3 comes in, including tracking whether aggregate foreign balances could trigger U.S. FBAR filing for U.S. persons at the $10,000 threshold. For account comparisons, see The Best Multi-Currency Accounts for Digital Nomads and Freelancers.

Before you pick your day-to-day transfer rail, run your common payment routes through this payment fee comparison. That way, your Tier 2 choice is based on total cost, not headline claims.

Tier 3: The Compliance Brain#

Use Tier 3 as your oversight layer. Here, you track exposure across accounts and turn compliance into a repeatable process. Your accounts hold funds. This layer holds the evidence, rule checks, and filing steps that keep surprises out of filing season.

Providers can support your accounts, but disclosure obligations still sit with you. If you use HSBC Expat alongside fintech and local foreign accounts, your reporting exposure can span all of them.

Job one is cross-account reporting readiness#

The goal here is simple: keep a live register that lets you confirm filing obligations quickly and defensibly. For many readers, that includes FBAR (FinCEN Form 114) and a separate Form 8938 review, because one does not replace the other.

Inputs you maintain for each foreign account:

- institution, jurisdiction, account number, legal owner

- open/close dates

- currency and balance snapshots

- highest-balance method plus supporting statement

- Form 8938 review flag

- linked evidence folder (monthly statements, year-end exports)

From that register, you produce:

- FBAR candidate list

- Form 8938 review list

- filing calendar

- institution folders with consistently named records

Use this review cadence:

- monthly reconciliation: every active foreign account appears in the register, and every line has supporting records

- pre-filing checkpoint: confirm due dates and extension workflow, then finalize the pack

Keep a visible field in your register for the reporting trigger, and leave its value pending until you confirm the live requirement from the official source.

Job two is residency tracking#

Residency should be treated as a live risk check, not a year-end guess. You need a country-by-country status view with risk flags, because different rule families use different tests and exclusions.

Inputs you maintain:

- entry/exit dates

- passport/itinerary evidence (including transit context where relevant)

- accommodation dates

- work-location notes

- local registration or payroll start dates

From that, you produce:

- country-by-country residency status view

- risk flags tied to specific rule families

- action log for travel or filing decisions

Review it:

- monthly if you travel frequently

- immediately before or after any long stay that could change status

Keep a visible field in your dashboard for residency-rule limits, and leave its value pending until you confirm the live rules for the relevant jurisdiction.

| Rule family | What you must track | Where mistakes usually happen | Action when a risk flag appears |

|---|---|---|---|

| U.S. foreign account reporting | Full foreign-account inventory, legal owner, highest-balance evidence, filing calendar for FinCEN Form 114 and Form 8938 review | Looking at one account in isolation, assuming Form 8938 replaces FBAR, missing account records | Freeze the year's account list, backfill missing records, verify current reporting trigger, and prepare filing materials early |

| U.S. tax residency | Current-year presence, prior-year travel context, excluded-day categories | Counting days with one rule, ignoring exclusions, relying on memory | Rebuild the log from source records, verify current residency limits, and get advice before extending stays |

| UK tax residency | UK tax-year travel log, workdays, home/family ties, automatic-test outcomes and ties analysis | Treating residency as only a day-count issue, tracking the wrong tax-year frame, missing tie factors | Map facts to the SRT structure, review sufficient-ties exposure, and pause discretionary travel until status is clear |

| CRS and cross-border data matching | Declared tax residencies and account-holder details across institutions, plus year-over-year changes | Stale profile data, inconsistent residency declarations across providers | Update records across institutions, reconcile declared residencies, and align filing positions to current account data |

Handled properly, Tier 3 is what makes the rest of the setup reliable. Reconcile accounts monthly, update residency logs as you travel, and enter filing season with an evidence pack that is already organized. For the tooling side, see The Best Accounting Software That Handles Multi-Currency Invoicing.

From Anxious to in Command#

You move from anxiety to control when each tier has a distinct job, a fallback role, and a clear escalation trigger. Stop asking one provider to do everything. Give each part of your setup a narrow, deliberate role.

Tier 1, the Institutional Anchor, is where you keep core cash and continuity. If your anchor is HSBC Expat, treat it as a central holding layer connected to your wider banking setup, not your daily payment rail. That can reduce concentration risk, but it does not remove product limits or compliance duties. HSBC Expat Global Money is mobile-only and can hold 19 currencies. It cannot receive incoming payments from outside HSBC Expat or from other customers, so do not rely on it for third-party collections. Deposits and investments made with non-UK HSBC group members do not benefit from UK FSCS-style protection.

Tier 2, the Agile Fintech Fleet, is for speed, routing flexibility, and lower-friction day-to-day transfers. It is not your long-term vault. This tier can reduce operational delays and payment friction, but some providers are not banks. Wise, for example, says customer funds are kept separate from operating funds and also says it is not a bank.

Tier 3, the Compliance Brain, is your evidence and filing layer, not an account. It can reduce reporting errors by keeping one register across all foreign accounts. FBAR can be triggered when aggregate foreign account value exceeds $10,000 at any point in the year, and Form 8938 review is separate.

| Tier | Primary use | Best for | Watchouts | When to escalate |

|---|---|---|---|---|

| Institutional Anchor | Core cash storage | Reserves and banking continuity | Product features vary by market; some setups are not a daily collections hub | Large balance shift, relocation, or a product limit blocks a needed workflow |

| Agile Fintech Fleet | Transfers and spend | Invoicing flows, FX conversion, routine payouts | Some providers are not banks; feature constraints can interrupt routes | Incoming payment blockage or repeated transfer friction |

| Compliance Brain | Reporting readiness | FBAR workflow, Form 8938 review, residency tracking records | Easy to neglect until filing season | Aggregate balances increase, travel pattern changes, or account footprint changes |

A compact operating checklist helps keep the tiers working together:

- Weekly: place excess cash into Tier 1, run active payment routing through Tier 2, and log failed or delayed transfers.

- Monthly: reconcile every foreign account in your register, save statements, and keep balance records organized.

- Pre-filing: review FBAR timing (April 15, with automatic extension to October 15 if needed), then review Form 8938 separately.

- Trigger-based: update Tier 3 immediately when you change country, open or close accounts, or start carrying larger balances.

Audit your current setup against the three tiers, identify the missing layer, and take the next implementation step that closes that gap. For a step-by-step walkthrough, see Opening a UK Bank Account as a Foreigner Without Guesswork.

As you put the three-tier setup into practice, keep your travel and residency evidence in one place with the tax residency tracker.

Frequently Asked Questions

How does HSBC Expat compare with Wise or Revolut?

They fit different roles. HSBC Expat is the banking anchor for core funds in GBP, USD, or EUR, while Wise and Revolut are positioned as operating tools for transfers, FX, and account details used in day-to-day payments. Confirm the exact route, plan, and market before you move money.

What are the real fees when you exchange currency?

The main cost is usually the FX margin, not just a visible transfer fee. Even if HSBC shows no HSBC transfer fee on a Global Money transfer, you still need to check the quoted rate and any non-HSBC or intermediary costs on your route. Compare the quoted rate with the mid-market rate and estimate total conversion cost before converting.

Is HSBC Expat enough on its own if you are a U.S. person abroad?

No. The account can hold funds, but it does not determine your FBAR position, FEIE eligibility, or state tax residency status. U.S. citizens and resident aliens abroad are still taxed on worldwide income, and claiming FEIE does not remove U.S. return reporting.

Does the account help with FBAR or Form 8938?

No. The account itself is not a compliance tool, and FBAR and Form 8938 review are separate. File FBAR on FinCEN Form 114 when required, and review Form 8938 separately. Keep one combined record across all foreign accounts so you do not miss part of your reporting footprint.

What should you verify before applying?

Verify whether your country is currently eligible and which entry route applies to you. Criteria can change, so confirm the live salary, savings, or investment requirement. HSBC says opening usually takes 7 to 10 days after required documents are received, so do not base critical payment timing on that estimate.

What documents should you prepare for account opening?

Prepare a valid ID and recent proof of address. HSBC's FAQ points to a current passport and proof of address such as a utility bill issued within the last 4 months. Check that names, address details, and document dates are correct before upload.

Can bank statements prove your tax residency?

No. Bank statements are supporting evidence, not a standalone residency determination. Build an evidence file with travel logs, housing records, registrations, and tax documents, then use statements as one supporting piece. Verify current rules with the relevant tax authority because country rules differ.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- ftb.ca.gov/file/personal/residency-status/index.htmltrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/individuals/international-taxpayers/substant...trusted

- oecd.org/en/publications/consolidated-text-of-the-com...trusted

- remittanceprices.worldbank.orgtrusted

- tax.ny.gov/pubs_and_bulls/tg_bulletins/pit/permanent_pl...trusted

- tax.virginia.gov/residency-statustrusted

- expat.hsbc.com/international-banking/multi-currency-accountsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Automating Your Freelance Finances: A Zapier Workflow for Connecting Stripe, QuickBooks, and Wise

Cleaner books and fewer month-end fire drills come from sequence, not software. Run this in the right order: structure, compliance, accounting architecture, then automation.

Opening a Hong Kong Bank Account as a Foreigner With Fewer Delays

Opening a Hong Kong account as a foreigner is possible in some cases, but success usually comes down to eligibility and routing, not form filling. Access, document checks, and whether you can start remotely all depend on the provider you choose.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.