Quick Answer

Choose an MLRO model where SAR judgments cannot be bypassed by commercial pressure and where one accountable owner can evidence each case decision. For cross-border payment operations, the article’s practical default is an independent line to General Counsel or Chief Risk Officer, supported by a standard evidence file and explicit escalation timing. If you are in UK scope, verify SMF17 accountability and MLR 2017 appointment records before scaling.

Why Clear MLRO Authority Matters#

A payment platform should treat the Money Laundering Reporting Officer as a control function, not a title added to an already overloaded role. At minimum, the role rests on two established duties: reporting suspicions of money laundering and ensuring compliance with money laundering regulations.

- Start with the real mandate

Weak role design often starts with a vague job description that blurs investigation, policy, and escalation. In UK guidance, the role includes a legal obligation to report suspected money laundering to the National Crime Agency. It is also framed as responsible for AML/CTF compliance oversight. The practical point is accountability: suspicion reporting and program oversight should sit with named individuals, not a generic compliance queue.

One governance checkpoint is clear: natural persons are appointed as MLRO, DMLRO, and AMLCO. In that setup, the operating lesson is accountability. If ownership for suspicious-activity decisions, deputy cover, and compliance controls is unclear, the structure is fragile.

- Design for pressure, not org-chart neatness

This role has existed in UK financial services for around 30 years, and it still sits under real pressure. Research points to pressure from internal and external stakeholders, and that is exactly where weak design shows up. Your reporting line needs to hold when a case is inconvenient or commercially sensitive.

A common failure mode is giving someone the title without the authority. If suspicious-activity decisions can be delayed or steered outside the role, the control is weak before any formal review begins. Define decision rights early. State what must reach the MLRO, who may challenge an assessment, and what evidence is required before a case is closed, monitored, or escalated for filing.

- Use this guide to make defensible choices

This article is for compliance, legal, finance, and risk owners who need an MLRO setup that works under pressure without becoming process theater. It uses a practical list-and-comparison approach to evaluate reporting lines, independence, qualification expectations, and escalation design. The standard is simple: choose what you can defend later, not what looks tidy in a diagram.

The focus stays operational. You will get role-model options, clearer suspicious-activity escalation logic, and a practical evidence checklist for judgment calls. If your current model depends on unwritten exceptions or informal side channels, treat that as a control gap now.

- Expect boundaries, not false certainty

Some design principles transfer across firms, but legal mechanics may not. Filing mechanics, liability, and appointment expectations can vary by market, so this guide separates portable operating practice from decisions that need local legal confirmation.

By the end, you should be able to choose a workable model, set escalation rules people can follow, and define the evidence needed to defend a suspicious-activity decision when tested. For related reading, see How Platforms Keep Contractor Payment Details Accurate and Compliant.

Who this list is for and how to pick the right model#

If AML pressure is already part of daily operations, move toward a more independent design early. This section is for payment-platform teams where KYC, case review, and escalation decisions are live controls, not just documentation.

This is not jurisdiction-specific legal advice. You still need local counsel for local AML-law interpretation. The focus here is operating design, evidence quality, and escalation authority.

- Regulatory exposure

Start with the activity that creates senior accountability. A grounded example is the UK: in-scope firms under the Money Laundering Regulations must appoint someone to own financial crime prevention, and SMF17 makes one named individual personally accountable for AML and financial crime controls. Use that as a governance benchmark, not as proof that one jurisdiction's setup automatically fits another.

- Payment and review complexity

Choose based on case complexity first. If alerts often require due diligence review or PEP assessment, tighten case ownership and review depth. A practical control is the four-step PEP validation flow: name matching, geography, profiling, and confirming whether the person is the PEP or an intermediary. Weak name matches and single-country geography checks are known failure points and need additional research.

- Independence and challenge authority

If you need a credible challenge function, define independence and decision rights explicitly. Some firms split MLRO and MLCO duties, but senior-management accountability still needs to be clear. If case complexity is rising, consider a more independent reporting line and require a documented evidence pack before you close, monitor, or escalate a case. For a step-by-step walkthrough, see FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders.

The five MLRO role designs payment platforms actually use#

Start with the design that gives the function enough seniority and authority to challenge frontline or senior management decisions and maintain a clear suspicion-reporting path. These are practical operating patterns for planning, not a universal legal taxonomy or proven industry standard, so test each one against your jurisdictions and risk profile.

| Design | Use when | Main caution |

|---|---|---|

| Embedded AML compliance officer inside Ops | Operational context and speed matter most | Weaker independence when commercial priorities and AML judgments sit in the same line |

| Nominated Officer plus lean compliance pod | Improve ownership and triage with one named person and a small team | Concentration risk; coverage and handoff quality matter as much as org-chart clarity |

| Independent MLRO reporting to Chief Risk or General Counsel | Need a stronger challenge function and cleaner escalation authority in practice | Final reasoning should be documented when management takes a different view |

| Group MLRO with regional deputies | Improve consistency across markets while preserving local ownership of reporting decisions | Responsibilities may vary by country or industry; UK context should not be assumed to transfer directly |

| Board-access MLRO with formal committee cadence | Escalations can materially affect risk posture or business decisions and need defensible governance records | Heavier governance overhead and potential delay if overused |

- Embedded AML compliance officer inside Ops

This pattern can work when operational context and speed matter most. The benefit can be proximity to transactions. The risk is weaker independence when commercial priorities and AML judgments sit in the same line. Use this only if case outcomes are reasoned and documented, with credible independent review.

- Nominated Officer plus lean compliance pod

This design can improve ownership and triage by giving one named person decision accountability and a small team to prepare cases. It fits the combined-role framing where the MLRO has 2 core responsibility areas: reporting suspicions and helping ensure compliance with Money Laundering Regulations. Its main weakness is concentration risk, so coverage and handoff quality matter as much as org-chart clarity.

- Independent MLRO reporting to Chief Risk or General Counsel

Use this when you need a stronger challenge function and cleaner escalation authority in practice, not just on paper. The test is straightforward: can the role push back on business decisions, and is the final reasoning documented when management takes a different view? If risk appetite, controls, or assessments change, those changes should be reasoned and documented.

- Group MLRO with regional deputies

This model can improve consistency across markets while preserving local ownership of reporting decisions. Treat jurisdictional alignment carefully. Responsibilities may look similar in principle but still vary by country or industry. For example, UK context can include SMF17 and a legal duty to report suspicions to the NCA, which should not be assumed to transfer directly to other markets.

- Board-access MLRO with formal committee cadence

Use this when escalations can materially affect risk posture or business decisions and you need defensible governance records. The benefit can be formal escalation and documented decision-making. The cost can be heavier governance overhead and potential delay if overused. A practical discipline is to benchmark role execution against a 20-responsibility checklist so board access supports, rather than replaces, day-to-day AML ownership. For adjacent platform reporting context, see 1099 Contractor Payment Guide for Platforms: Rules Thresholds and Filing Deadlines.

Compare reporting line options before you commit#

For cross-border platforms, compare COO, General Counsel, Chief Risk Officer, and board-committee models side by side. Treat any choice as jurisdiction-specific, not universal, because reporting lines and legal duties vary by jurisdiction and firm type. Some frameworks also require named officers, for example an MLRO and, where appropriate, an MLCO, or a nominated officer/AMLCO structure.

| Reporting line | Independence | Decision speed | Regulator confidence | Policy exceptions owner | High-risk client continuance approval | Remediation sign-off |

|---|---|---|---|---|---|---|

| COO | Requires explicit safeguards so commercial management cannot dilute independent challenge | May be faster, but test speed against challenge quality | Depends on whether rationale and escalation records are complete | Assign and document a named owner | Assign and document approval thresholds and escalation triggers | Document who assessed the issue, who approved the fix, and why |

| General Counsel | Can support independent challenge when legal governance is clear | Depends on delegation and escalation design | Depends on clear legal rationale and records | Document ownership in legal governance records | Use documented challenge and escalation criteria | Keep decision rationale and accountability records regulator-ready |

| Chief Risk Officer | Can support independent challenge when AML sits inside formal risk governance | Depends on delegation and escalation design | Depends on explicit risk decisions and rationale | Document ownership in risk governance records | Align criteria to risk appetite and escalation rules | Link sign-off to residual-risk assessment and escalation records |

| Board committee | Strong for oversight and escalation authority; day-to-day ownership must be delegated clearly | Depends on committee cadence and delegation | Depends on clear escalation scope and records | Reserve for material exceptions with explicit delegation below committee level | Reserve for escalated or material decisions | Use for oversight of material remediation, with execution ownership below committee level |

Decision checkpoint: if commercial leadership can overrule suspicion judgments without documented independent challenge and escalation, treat that reporting line as a governance weakness for a Second Line of Defense model.

COO reporting can improve speed, but it needs explicit safeguards to preserve independence. General Counsel reporting can work when legal governance is clear and legal rationale is central. CRO reporting can be effective when AML decisions need to sit inside formal risk governance. Board committee reporting is usually strongest as escalation and oversight rather than the day-to-day home for case decisions.

The final test is simple: you should be able to trace one case from alert to suspicion decision to remediation owner without split accountability or undocumented handoffs, and role records should include the named officer and appointment details. For related context, see DAC7 Compliance for Platforms: Reporting Rules Deadlines and Implementation. If you are turning your reporting-line decision into enforceable escalation rules, map the handoffs and status events in one place before rollout: Read the docs.

Responsibilities every MLRO must own from day one#

From day one, the role should have explicit ownership of five areas, even when Ops, Risk, Legal, or AML compliance staff support execution.

- Policy ownership

The MLRO should own the core AML/CFT policy framework, including how customer due diligence and ongoing monitoring are applied in practice. A key control is a clear escalation boundary: what the first line can close, and what must be escalated. If that boundary depends on shift-by-shift judgment instead of documented rules, accountability is already weakening.

- Case governance and decision logging

Internal suspicious activity reports should land with the MLRO, or the formal equivalent such as a nominated officer, and decisions should be recorded in a structured log. For each case, keep the rationale for filing, monitoring, or closure in a reviewable record, not scattered across email or tool comments. If the outcome cannot be reconstructed later, case governance is not reliable.

- Monitoring oversight that proves control effectiveness

This is not just ownership of tools or dashboards. It includes regular review of whether AML/CFT controls are actually working. Transaction monitoring, customer due diligence activity, and related checks should produce outputs that are reviewable and defensible. Alert volume alone is not evidence of effective oversight.

- Team accountability for escalation

Escalation judgment should not sit only with specialist compliance staff. The MLRO should set clear role-based expectations so Ops, Risk, and Finance know what to escalate, what records to preserve, and what they should not close independently. If only one team understands the escalation path, execution becomes fragile.

- Regulator and authority interface

The function should be the operational link to regulators and law enforcement for reportable activity. In the UK context, this can include SMF17 responsibilities for an FCA-approved MLRO. Across multiple markets, keep one accountable owner for external communication, validate market-specific obligations locally, and avoid diffused committee accountability.

Escalation rules when an alert becomes a SAR decision#

Treat escalation as a documented control, not a loose judgment call. When suspicion remains after analyst triage, the case should move to MLRO review through a defined internal sequence with one accountable owner and a record you can reconstruct later.

| Control point | Rule | Detail |

|---|---|---|

| Order of operations | Alert intake, analyst triage, MLRO review, legal checkpoint where needed, SAR decision, filing handoff, control update | Internal suspicious activity routes to the MLRO; SAR filing is a separate external step |

| Escalation trigger | If material uncertainty remains after review and behavior does not match the KYC/KYB profile, escalate to the MLRO | Keep the trigger explicit in policy and track exceptions |

| Evidence pack | Transaction narrative, current KYC/KYB snapshot, available prior SAR context, analyst rationale, note on jurisdiction-specific obligations | Treat this as an internal decision standard, not a universal statutory checklist |

| Legal involvement | Keep Legal as a checkpoint, not the decision owner | Legal input can help with wording, communications, privilege, and cross-border exposure, but the suspicion assessment remains with the MLRO |

| Commercial pressure | Commercial approvers should not close the case before review is complete | Feed the outcome back into monitoring and training |

- Set one internal order of operations

Use a clear internal flow, such as: alert intake, analyst triage, MLRO review, legal checkpoint where needed, SAR decision, filing handoff, then control update. This is an internal governance rule, not a universal legal script, but it prevents ownership gaps across teams. Internal suspicious activity should route to the MLRO for evaluation. SAR filing is a separate external step because it is a formal notification to the relevant FIU, in the UK, the NCA.

- Use an if-then trigger for escalation to MLRO

Analysts need a trigger they can apply consistently: if material uncertainty remains after review and behavior does not match the KYC/KYB profile, escalate to the MLRO under your documented internal timing standard. Keep the trigger explicit in policy and track exceptions. If discretionary payout controls are relevant, state clearly whether a hold is available under local policy and law rather than assuming the same option exists in every market.

- Require a standard evidence pack before MLRO sign-off

The decision should be based on a complete case file, not fragmented notes. A practical internal pack can include a transaction narrative, current KYC/KYB snapshot, available prior SAR context, analyst rationale, and a note on applicable jurisdiction-specific obligations. Treat this as your internal decision standard, not a universal statutory checklist.

- Keep Legal as a checkpoint, not the decision owner

Legal input can be critical for wording, communications, privilege, and cross-border exposure, but the suspicion assessment should remain with the MLRO. In UK SMF17 structures, that ownership is tied to personal accountability for AML controls under the MLR 2017 framework, as amended. Difficult cases should not disappear into committee process.

- Block commercial bypass of the MLRO queue

A common failure mode is urgency: payout, account, or revenue pressure pushing a case out of sequence. For potential SAR events, commercial approvers should not be able to close the case before review is complete. After the decision, feed the outcome back into monitoring and training so the same pattern is less likely to repeat.

Qualifications that are mandatory versus nice to have#

What matters first is management-level AML/CFT accountability in practice. Titles and tools are secondary.

Mandatory baseline

- Role design that is consistent with applicable governance expectations. The EBA guidelines, applying from 1 December 2022, expect an AML/CFT compliance officer at management level and one management body member in the end responsible for AML/CFT implementation.

- For institutions that are part of a group, a group AML/CFT compliance officer is expected.

- These expectations are a baseline and complement broader governance and suitability guidance; they do not replace it.

Mandatory operating competence

- Ability to run AML/CFT governance through decisions, escalation, and remediation follow-through.

- Ability to assess whether a case file is decision-ready and communicate decisions clearly to senior management and board audiences.

- Clear handling of incomplete CDD as a control-failure checkpoint that requires action.

Nice to have by growth stage

- Prior exposure to role frameworks such as AMLRO.

- Multi-jurisdiction and group-level policy experience, especially where a group AML/CFT compliance officer is expected.

- Hands-on RegTech implementation depth to improve execution at scale.

Decision rule

- If a candidate is strong in legal or policy interpretation but has limited live-case ownership, treat operational-readiness requirements as role-specific and confirm them before scaling higher-risk operations. For adjacent systems context, see ERP Sync Architecture for Payment Platforms Using Webhooks, APIs, and Event-Driven Patterns.

Jurisdiction boundaries you should state explicitly#

State jurisdiction boundaries up front. Keep AML role principles portable, but confirm filing mechanics, appointment steps, and liability under POCA, BSA, the USA PATRIOT Act, or PCMLTFA locally.

- United Kingdom and SMF17

If an entity is in UK scope, say so directly. In the UK framing used here, SMF17 is the Senior Management Function designation for the MLRO, tied to FCA approval, with reference to the Money Laundering Regulations 2017, as amended.

The key point is named accountability: one individual is identified as owning AML and financial crime controls. Verify this through records, not verbal assurances, including appointment documentation, approval status where applicable, and written risk assessment findings with rationale and controls.

- United States logic is not a UK transplant

For US entities, keep this article at principle level unless local counsel confirms legal mechanics. Portable role principles may carry over, but exact reporting routes and liability analysis under the BSA or USA PATRIOT Act should be treated as jurisdiction-specific.

Treat copied governance language as a warning sign, especially when UK role labels are reused without jurisdiction-specific legal review.

- European Union implementation still needs local reading

Do not present "EU AML" as a single operational rulebook. Group-level principles may align, but implementation can differ by country and by firm.

Keep EU-wide governance separate from member-state execution, and require local risk assessments with documented rationale rather than relying only on a group policy and sign-off.

- Mark unsupported country claims as unknown

If evidence is incomplete, say that plainly, especially for country-level statutory qualification thresholds.

Also treat overreliance on personal knowledge in transaction monitoring as a control weakness. Decisions should be supported by documented assessment rationale and controls.

Build the reporting pack your board and regulators expect#

Build this pack for traceability first. You should be able to link each alert to a reporting outcome and then to a named remediation owner. Aim for the same record to appear in case files, committee papers, and minutes.

Once you set jurisdiction scope, show how AML and KYC issues roll into the wider compliance program rather than reporting case volume alone. Under FINTRAC guidance, all reporting entities must establish and implement a compliance program, and that program is the basis for reporting, record keeping, client identification, and related know-your-client requirements. Use a consistent cadence that fits your governance calendar.

- Use fixed sections each cycle. Keep the same structure each time, for example alert funnel, SAR outcomes, open investigations, repeat typologies, overdue actions, and AML/KYC control exceptions, so trend breaks are easy to spot.

- Track quality, not just throughput. Include evidence-pack completeness, decision reversals after escalation or QA, and unresolved escalations against your internal timelines so "closed" cases are still defensible.

- Tie risk to the business. Break findings out by payout flows, product surfaces, and higher-impact corridors so leadership can connect control gaps to operational and revenue decisions.

- Maintain one auditable decision trail. Map material outcomes to remediation action, owner, due date, and status so board records, regulator responses, and internal audit outputs reconcile cleanly.

Two governance checks should be visible in this report. First, whether challenge is functioning. The role needs enough authority and seniority to challenge frontline and senior-management decisions, and overruling can still happen in practice. If management changes risk assessment, risk appetite, or controls to support a different view, record the rationale and those control changes.

Second, the pack should support periodic program testing, not just routine reporting. FINTRAC guidance includes a two-year effectiveness review and plan requirement. Your reporting should make recurring exceptions, evidence-quality gaps, and overdue remediation easy to lift into that review. For UK-specific obligations, read HMRC Reporting Rules for Platforms for UK Marketplace Operators.

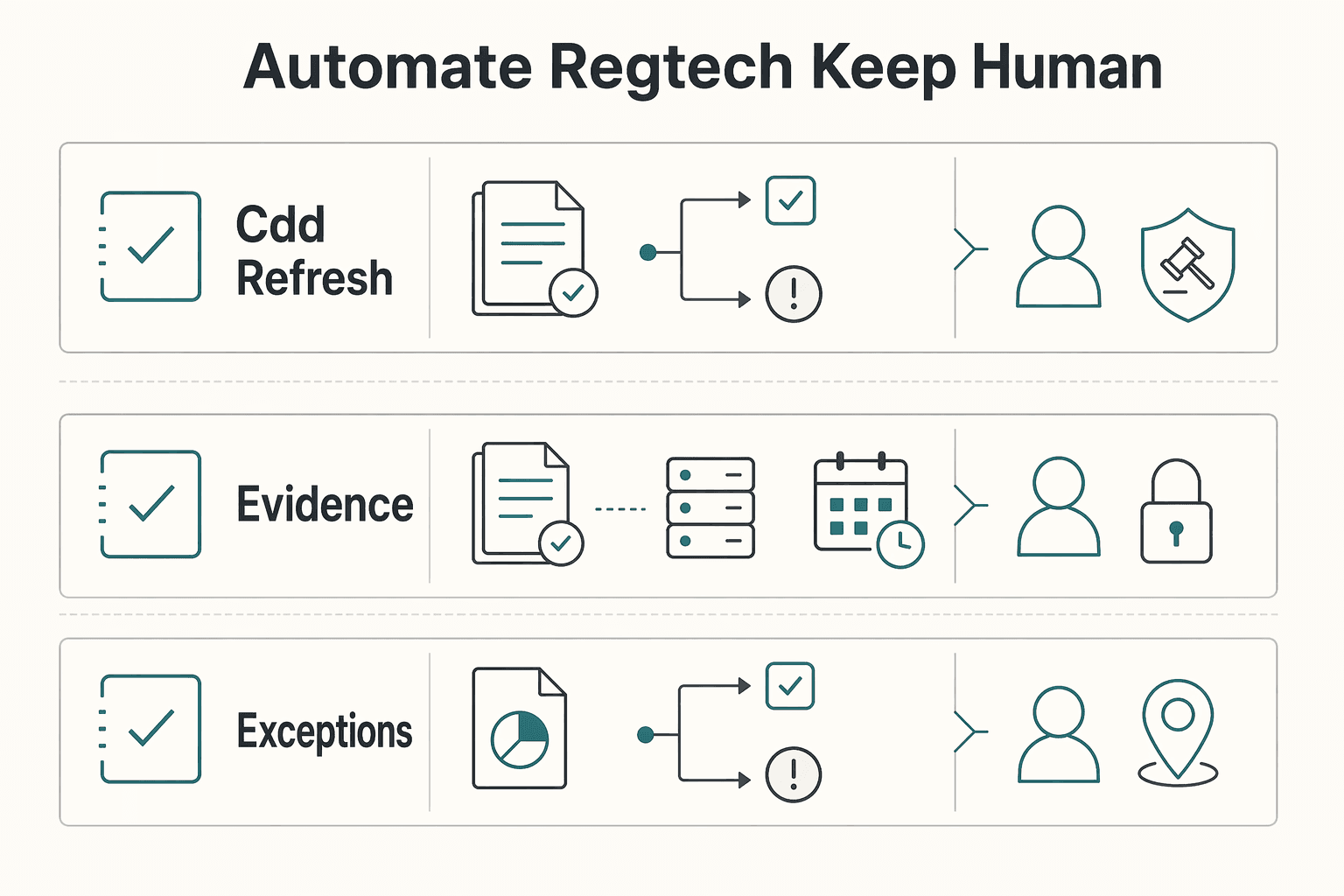

What to automate with RegTech and what to keep human#

Automate repeatable detection and evidence hygiene. Keep accountable people on decisions that create legal and governance risk.

| Workflow area | Primary handling | Boundary |

|---|---|---|

| CDD refresh triggers and case routing | Automate repetitive intake and route alerts from transaction monitoring; queue cases by risk | Automation should surface and sort, not conclude; each routed case should carry the source and date of the AML/CFT data used |

| Evidence assembly and periodic control attestations | Automate evidence-pack assembly and attestation collection | This supports analysis, not replaces it; tooling should support retention decisions instead of defaulting to "keep everything forever" |

| SAR decisions, policy exceptions, and enforcement-sensitive calls | Keep human | Decision rationale and escalation judgment should stay with accountable people, not software |

| Adjacent documentation and reporting workflows | Use workflows to improve document completeness, data consistency, and auditability in case files | Document completeness is not AML judgment; keep AML decisions and profiling safeguards in the human decision path |

- CDD refresh triggers and case routing. Automate repetitive intake: adapt data collection to risk, route alerts from transaction monitoring, and queue cases by risk. This is where rules and ML-based flagging help with consistent ordering, while the MLRO prioritizes what needs attention first.

Key differentiator: automation should surface and sort, not conclude. Each routed case should carry the source and date of the AML/CFT data used to generate the alert.

- Evidence assembly and periodic control attestations. Automate evidence-pack assembly and attestation collection so review records are consistent and complete. The objective is stronger documentation quality, including provenance metadata and data-accuracy controls.

Key differentiator: this supports analysis. It does not replace it. Tooling should also support retention decisions instead of defaulting to "keep everything forever," since AML/CFT guidance highlights retention limits in at least one FIU context beyond 5 years.

- SAR decisions, policy exceptions, and enforcement-sensitive calls. Keep these human. The MLRO is a senior compliance lead and regulatory contact, so decision rationale and escalation judgment should stay with accountable people, not software.

Key differentiator: challenge is essential, but financial-crime risk ownership still sits with the business, not the second line alone.

- Adjacent documentation and reporting workflows. If you already run adjacent document-heavy workflows, use those feeds to improve document completeness, data consistency, and auditability in case files.

Key differentiator: document completeness is not AML judgment. Use these workflows to support data quality and CDD evidence, while keeping AML decisions and profiling safeguards in the human decision path.

If you need one operating rule, use this: automate what you can verify through metadata, timestamps, and repeatable checks. Keep humans on calls that require judgment, challenge, and defensible reasoning. If you want a deeper dive, read What Is RegTech? How Compliance Technology Helps Payment Platforms Automate Regulatory Reporting.

The seven implementation mistakes that create regulatory surprises#

Regulatory surprises usually come from governance design gaps, not a single missed alert. Pressure-test authority, ongoing monitoring, and evidence discipline in day-to-day operations before a regulator or partner does it for you.

-

MLRO title, no real authority. This role is long-established in UK financial services, so a title without practical decision weight is hard to defend. If final SAR or customer-continuance decisions are routed through commercial leaders, independent challenge can weaken before review starts. Business management owns financial-crime risk, but sole accountability should not be pushed onto the MLRO.

-

KYC marked complete, AML assumed complete. KYC at onboarding is only a starting control, not the full AML program. Strong practice pairs customer due diligence with ongoing monitoring of transactions and customer behavior so risk is reassessed after money starts moving. Check that new accounts actually flow into transaction monitoring and payment screening, rather than remaining in a static "KYC passed" state.

-

SAR handling without written escalation rules. A SAR process is only strong when escalation steps are documented and followed. If analysts cannot point to written escalation criteria, a named reviewer, and minimum evidence standards, decisions drift into chat threads and memory. Require a dated escalation trail and clear rationale for filing, monitoring, or closing.

-

One policy copied across the United Kingdom, European Union, and United States. AML programs are not one-size-fits-all, and reused global text can miss local obligations. In the UK context alone, payment and money-transfer requirements can intersect with the Money Laundering, Terrorist Financing and Transfer of Funds Regulations 2017 and the Payment Services Regulations 2017. If you reuse group policy language, require local legal validation and local procedures before launch.

-

Too much faith in RegTech, too little in review quality. Screening controls can flag, block, or escalate payments, but they do not remove implementation risk, even at mature firms. Control quality still depends on trained reviewers, documented challenge, and complete case files. Preserve source data, reviewer identity, and disposition rationale for every alert, because non-compliance can lead to fines, law-enforcement action, and reputational damage.

-

Jurisdiction labels treated as interchangeable. Group-level principles may align, but reporting mechanics and accountability expectations can differ by country and by firm. Reusing UK role labels or governance text in US or EU entities without local legal review creates false comfort. Say what is confirmed locally, and mark unsupported country claims as unknown until records or counsel close the gap.

-

Board packs that show volume but not accountability. Case counts are not enough if leadership cannot trace an alert to a decision, rationale, and remediation owner. A pack that cannot reconcile to case files, committee papers, and minutes is harder to defend when challenged. Keep one auditable decision trail that links alerts, SAR outcomes, overdue actions, and remediation status.

Conclusion#

The strongest setup is the one you can defend under pressure, not the one with the most tools or the largest team. For a payment platform, that means clear authority, defensible escalation decisions, and reporting lines that still hold when a case affects revenue, partners, or launch timing.

- Choose authority before scale

Start with role design before software. The MLRO is a senior AML role, and the control weakens fast if that person cannot challenge frontline or senior management decisions. In larger organizations, independence from business operations and from the receipt, transfer, or payment of monies is a practical safeguard. A simple checkpoint is whether the role can connect directly to senior decision-makers and, when needed, the board or a board subcommittee.

- Lock in escalation governance and document decision changes

Hard failures are often about decision accountability, not alert volume. Your records should let someone reconstruct who decided, what was reviewed, and why the outcome was escalation, monitoring, or closure. The recurring control gap is undocumented override. If management takes a different view, the change in risk assessment, appetite, controls, or reporting judgment should be reasoned and documented.

- Treat board reporting as proof, not presentation

Regular board-facing reporting with summary statistics and conclusions is a real governance checkpoint. The practical test is whether those summaries trace back to case records and named owners. Before adding more tooling, publish a board-ready pack that shows escalation outcomes, control concerns, and remediation status. Benchmarking against a responsibilities checklist, such as the referenced 20-key-responsibility list, is a useful coverage check, not a universal legal template.

If you operate across jurisdictions, avoid copy-pasting one entity's AML structure into another. Core principles travel, but local structuring may not. The Cayman example in the source guidance is a reminder that some frameworks require designated roles such as MLRO, DMLRO, and AMLCO.

Use one final test: can your team explain any AML decision from first alert to board visibility with clear artifacts, ownership, and jurisdiction-aware reasoning, on demand? If not, fix authority, documentation, and reporting discipline before buying more tools. Once your MLRO model and board pack are defined, validate market-specific rollout assumptions with Gruv before implementation: Talk to Gruv.

Frequently Asked Questions

What does an MLRO do at a payment platform day to day?

The day-to-day role centers on internal suspicious activity reporting and decision accountability. The function receives and evaluates internal SARs, reviews customer and business information, and supports escalation decisions that are reasoned and documented when views differ. For that to work in practice, the MLRO needs access to client files and business information.

Who should an MLRO report to in a platform organization?

There is no universally correct reporting line in the source guidance. The practical test is whether the role has enough seniority and authority to challenge frontline or senior-management decisions and escalate concerns when needed. In the UK context, MLR 2017 and SM&CR matter because SMF17 places personal AML accountability on one named individual.

Can management overrule an MLRO on SAR decisions?

The safer governance position is that reporting decisions should not be overruled. A grounded source also indicates that if management takes a different view, the change should be reasoned and documented. A key governance risk is an undocumented override.

What qualifications are required for an MLRO versus preferred?

The grounded sources do not set universal mandatory certifications, fixed years of experience, or one statutory qualification rule across all jurisdictions. The baseline is practical: senior AML oversight capability, authority to challenge management, and the ability to assess internal SARs using full customer and business information. Role labels vary by context, including "nominated officer" in some countries and SMF17 in the UK regime.

How is the MLRO role different in fintech and payout platforms compared with traditional firms?

The source guidance here does not establish a definitive fintech-versus-traditional duty split. What remains consistent is that the MLRO is a senior AML role with real accountability, challenge authority, and access to underlying files and business information. Those fundamentals are the clearest supported expectations regardless of firm type.

What should be included in an MLRO reporting checklist for board review?

There is no fixed board-pack template in the grounded excerpts. A practical checklist can focus on who owns controls, how internal SARs were handled, and whether decision changes were documented with reasons. One source references a checklist of 20 key responsibilities, which can be used as a coverage cross-check rather than treated as a universal legal template.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- eba.europa.eu/sites/default/files/document_library/Publica...trusted

- ec.europa.eu/justice/article-29/documentation/opinion-rec...trusted

- sec.gov/Archives/edgar/data/2025416/0000950123240096...trusted

- amlcertification.com/blog/aml-roles-explainedexternal

- amlwatcher.com/knowledgebase/who-is-a-money-laundering-repo...external

- bakermckenzie.com/-/media/files/insight/publications/2018/07/a...external

- compliancealert.org/view-blog/55external

- complyadvantage.com/insights/payment-screening-process-best-prac...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

What Is RegTech? How Compliance Technology Helps Payment Platforms Automate Regulatory Reporting

RegTech can automate regulatory reporting for payment platforms, but it should not replace legal judgment. The hard part is often not finding the rules. It is keeping up with changes across jurisdictions and producing a defensible record from onboarding through payout.

Choosing 1099 Filing Ownership for Platform Contractor Payments

At platform scale, 1099 risk is usually an ownership and evidence problem before it is a threshold problem. If you run payouts across multiple programs, entities, or payment rails, the question is not just whether a payment triggers a form. It is who owns the filing, what records support that decision, and how exceptions get handled when the facts are messy.

Choosing DAC7 Compliance Platforms Without Overbuilding

Start with operating reality, not feature grids. This section is for compliance, legal, finance, and risk owners who need a defensible decision, not a generic explainer. The goal is practical: make a faster scope call, choose an approach that fits your entity and data setup, and get through reporting with fewer surprises.