Quick Answer

Pay therapists and counselors in a HIPAA-compliant way by defining your compliance boundary before choosing tools, separating HIPAA from PCI, requiring BAAs for vendors that handle PHI, and making billing and payout activity auditable. Map data flow across intake, billing, support, portals, and payouts, assign control ownership, enforce role-based access and MFA, and verify logs, exports, and exception handling before launch.

What compliant therapist payouts actually require#

Treat this vertical as a control-design decision before a product decision. If your team cannot map how sensitive data moves through intake, billing, support, and payouts, pause roadmap and go-to-market spend until that scope is clear.

- Define the problem as operations, not checkout UI.

This guide is for founders and operators evaluating entry or expansion, not a solo practice choosing a billing tool. In demos, charging a card looks easy. In production, risk usually sits in data visibility, data copied across tools, and whether you can trace the path from invoice to payment confirmation to payout, especially once recurring payments and chargebacks enter the flow. In this category, platforms may handle personally identifiable information like names and contact details alongside health-linked context, so scope and control design come first.

- Separate compliance layers before vendor selection.

HIPAA and PCI obligations are related, but they are not interchangeable. One processor may reduce card-data exposure, and another system may handle part of the record, but that does not solve end-to-end risk. Put procurement behind a clear data-and-control map: who handles which data, and which controls apply across the full payment flow.

- Require auditability before scale.

The key launch question is not only whether therapist and counselor payments can be processed. It is whether your team can prove what happened when something fails. Treat audit logging and monitoring as core controls. Before you scale, confirm that payment activity and login events are recorded, access is limited by role, and status history can be reconstructed for billing changes, retries, disputes, and payout questions.

- Use market caution as an entry filter.

Compliance interpretation is context-dependent, and location can change what handling is required. Treat expansion assumptions as per-market hypotheses, not reusable truths, especially in marketplace models where provider-level pricing can complicate payment flows. The standard for the rest of this guide is practical: make payment flows operationally auditable before you commit heavily to buildout or sales.

Set the compliance boundary before picking tools#

Pick tools only after you can clearly map what data your product touches and where it moves. If that boundary is not clearly documented, pause vendor selection until scope is clear.

Map the full data flow#

Map every intake, billing, and support step where your platform may see data: forms, client messaging, invoices, payment pages, support tickets, exports, and admin views. For each touchpoint, label whether it may include PHI or payment-related data.

Use one verification rule: every box needs an owner, a data label, and a direction of travel. If a support system can view client notes or billing context, include it in scope.

Separate HIPAA from PCI questions#

Separate HIPAA questions from PCI questions before evaluating tools. Using a payment processor does not replace HIPAA risk analysis for systems that store or transmit PHI.

Treat payment pages, billing records, intake workflows, and support tooling as separate boundary decisions. Your documented risk analysis should cover every system that stores or transmits PHI, not only the system that charges the card.

Make BAAs a procurement gate#

Set BAA requirements as a procurement gate, and execute BAAs with every vendor that handles PHI, including EHR, telehealth, and billing vendors. Ask each vendor directly whether it handles PHI and whether it will sign a BAA for that scope. If the answer is unclear, do not move forward.

Add baseline controls and review cadence#

Add baseline controls to the same boundary map: unique user IDs, strong passwords, MFA, encryption, audit logs, and clear ownership for incident response and internal breach-reporting timelines. Recheck this boundary at least annually and again when major product or vendor changes occur.

If you want a deeper dive, read Payments for Healthcare Staffing Platforms: Compliance and Speed Requirements.

Gather prerequisites and evidence before vendor calls#

Before vendor demos, lock your own evidence packet and scoring criteria so you can test fit instead of reacting to sales narratives.

Send an evidence packet before the first call#

Build a short packet and send it before the first call. Include target markets, therapist payout corridors, expected payment methods, and whether EHR or telehealth integrations are in scope. If your product is a therapy app or other third-party platform used to deliver treatment services, state that directly so diligence stays in the right context.

| Packet item | What to state |

|---|---|

| Target markets | List your target markets |

| Therapist payout corridors | List your therapist payout corridors |

| Expected payment methods | List expected payment methods |

| EHR or telehealth integrations | State whether they are in scope |

| Therapy app or other third-party platform used to deliver treatment services | State that directly so diligence stays in the right context |

| Online tracking technologies | State whether you use or plan to use them in billing, intake, or portal flows |

Also state whether you use or plan to use online tracking technologies in billing, intake, or portal flows. HHS OCR says HIPAA obligations apply to regulated entities under the Privacy, Security, and Breach Notification Rules when using online tracking technologies. Part of that guidance was vacated by a federal court on June 20, 2024, and HHS says it is still evaluating next steps. Treat this as a legal-risk checkpoint, not a reason to skip review.

Use one verification test: if the vendor cannot restate your actual use case, including integration scope and payout geography, their answers are not specific enough yet.

Build a control checklist before the first demo#

Create a control checklist before the first demo, including the controls your team considers critical for your environment.

Ask where each control is enforced, who can bypass it, and what evidence can be exported. For audit logs, ask for a sample export or live view that shows traceability in a format your compliance and finance teams can review.

Set non-negotiable operating artifacts before a second meeting#

Define non-negotiable operating artifacts before any second meeting: BAA expectations, incident-response contacts, audit export format, and reconciliation ownership. Treat these as internal procurement gates, not universal legal thresholds.

Pressure-test ownership early. Who handles incidents, who owns reconciliation, and what is provided when you investigate a disputed charge or access event? If answers vary across sales, support, and security, plan for slower incident handling later.

Use ACA guidance as a question framework, not as final sign-off. It is explicitly non-prescriptive, not exhaustive, and should be supplemented with health care legal counsel.

Apply go or no-go criteria consistently#

Set go or no-go criteria before demos and apply them consistently. If answers on BAA terms, subprocessors, or audit-log coverage are still unclear for your use case, pause advancement until the gaps are resolved.

The practical failure mode in this vertical is approving product fit while deferring evidence gaps to "later." If first-round diligence answers are incomplete, treat that as a decision signal. For a related example, see Healthcare and Telehealth Platform Payments: HIPAA-Compliant Provider Payouts.

Choose your stack architecture for year one#

Choose the architecture you can run and defend in year one, not the one that looks best in a demo. If you are launching in one market with limited engineering and a narrow billing model, an all-in-one stack can be a practical path to test first. If you already expect multi-market expansion, custom payout rules, or frequent billing changes, a modular split between EHR and a payment processor may give you more control.

Architecture is an early delivery decision, not a late implementation detail. Make this cross-functional across architecture, regulatory, and security owners, and carry the same evidence packet and go or no-go gates from the previous section into this decision before build momentum makes changes harder.

Match the architecture to your year-one operating shape#

Start from your year-one operating shape, then map it to one of two patterns.

An all-in-one option can keep more of the clinical and billing experience in one product, sometimes including scheduling, notes, Client Portal functions, and payment collection. The main tradeoff is often framed as speed now versus flexibility later, but that framing needs to be validated against your real workflows.

A modular architecture separates responsibilities: EHR in one component, with payment collection, payouts, reconciliation, or billing logic handled through a separate processor and your integration layer. This can add upfront design effort, but it may reduce constraints when payout corridors, portal behavior, or operating ownership change across markets.

Use this decision rule:

- If you need a fast single-market launch with limited engineering capacity, test an all-in-one path first against your required flow.

- If multi-market expansion or payout control is already in scope, test a modular path early and compare evidence.

Checkpoint: make the team walk one full flow end to end, from intake to Client Portal charge, billing change, refund or dispute handling, payout, and audit export. If the flow only works when the vendor does it their way, that is an all-in-one compromise whether you planned it or not.

Compare post-launch friction, not just setup effort#

| Decision area | All-in-one EHR plus billing | Modular EHR plus separate Payment Processor | What to verify before signing |

|---|---|---|---|

| Launch speed | Can be faster if fewer integrations are introduced at once | Can be slower if more boundaries must be connected and tested | Implementation plan, named owners, and what is included versus owned by your team |

| Control depth | Can be constrained when billing and portal behavior follow vendor defaults | Can increase when payment and payout logic is shaped in your integration layer | Whether billing rules, payout logic, and support views can change without vendor intervention |

| Lock-in risk | May increase when clinical, billing, and portal records are tightly coupled | May decrease if exports and identifiers are usable across systems | Sample export, termination process, and ID mapping across systems |

| BAA complexity | Fewer counterparties may reduce handoffs | More counterparties can increase diligence and coordination | BAA template availability, subprocessor clarity, and incident ownership at each boundary |

| Data portability | Can be easier to buy and harder to unwind | Separation can help portability, but only if exports are usable | Export format, timing, and retrieval of historical billing and portal records |

| Support burden for Client Portal and billing changes | Vendor may absorb more first-line behavior, with less control for you | Your team may coordinate more across vendors and internal tools | Who owns resolution when one issue spans portal UX, payment state, and ledger accuracy |

The key question is who owns the authoritative billing event and the evidence trail behind it. If finance, compliance, and support must stitch together three systems to explain one charge adjustment, that is already a year-one operating cost.

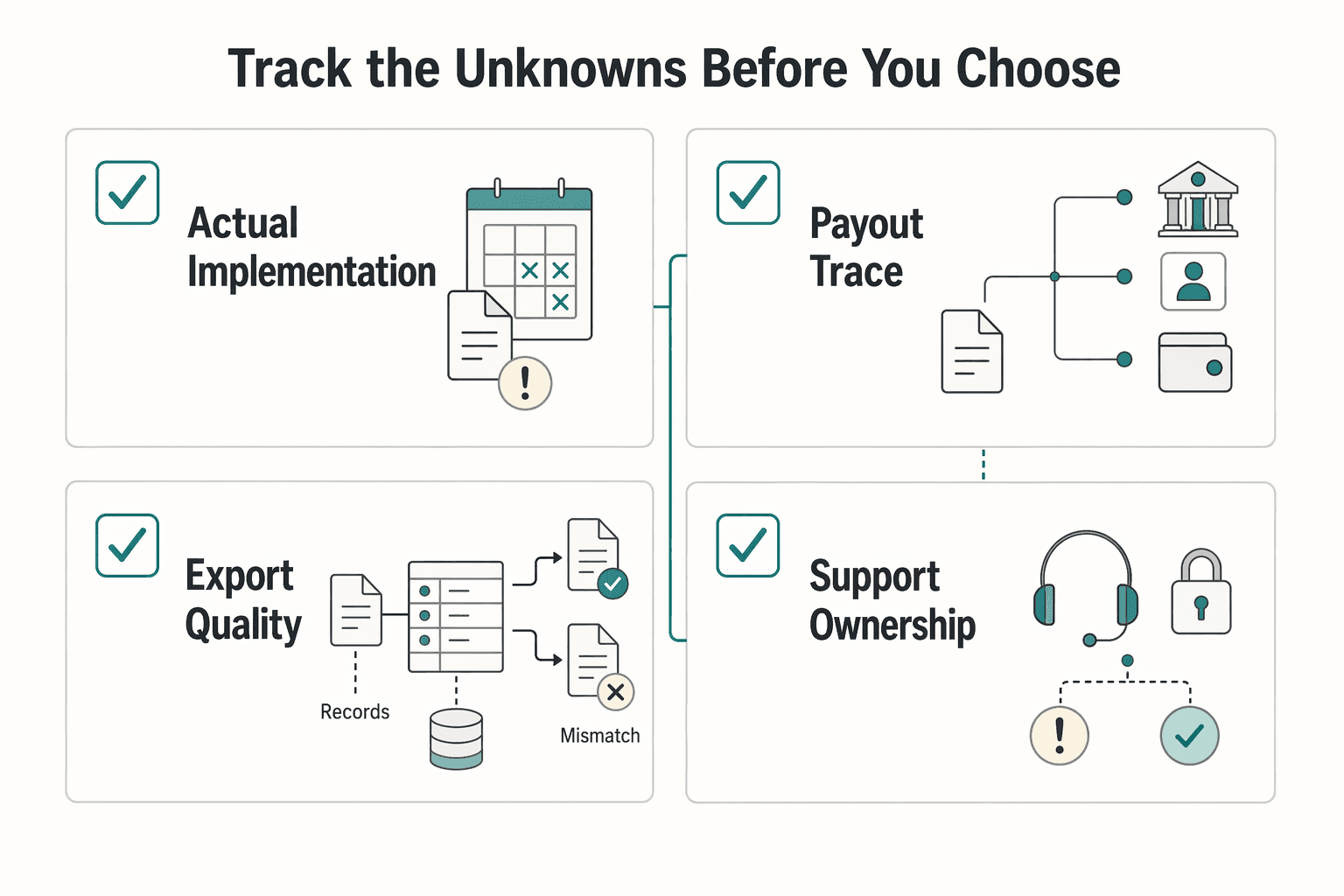

Track the unknowns before you choose#

Document unknowns before choosing, especially costs vendors do not quantify.

Healthcare app delivery has meaningful execution risk. One healthcare-founder guide reports 67% go over budget, 4-8x longer than planned, and 40% never reach users. These are not architecture-specific forecasts, but they are still a useful warning that "simple to launch" and "simple to run" are different outcomes.

For this decision, track at least these unknowns:

- Actual implementation effort for your specific Client Portal and billing flow

- Post-launch change cost for refunds, autopay rules, payout timing, and ledger mapping

- Export quality for migration needs and historical investigations

- Support ownership when one billing issue crosses EHR, payments, and internal admin tools

Compliance risk is also part of architecture risk. Healthcare breach volume remains high, with 725 major breaches reported in 2024, affecting 500 or more people. That does not prove one stack shape is safer by default, but it does justify strict evidence checks on where billing-related data is stored, viewed, and exported.

Use a scenario test, not another deck: update a payment method in the Client Portal, post a charge, correct it, and export the full audit trail. Ask for the BAA template, sample export files, and the support path for that exact case. If the evidence is missing, treat claimed simplicity as unproven. For year one, conservative beats ambitious. Choose the architecture your actual team can explain, evidence, and support.

Assign control ownership across legal and security layers#

Assign control ownership before go-live, or you will lose time in incidents deciding who acts. If legal, security, and payments ops would still debate ownership during a login issue, disputed payment review, or possible data exposure, ownership is not operational yet.

Build one responsibility matrix across parties#

Create one responsibility matrix that covers your platform, the payment processor, the EHR/telehealth vendor, and internal ops in one view. Keep HIPAA obligations and BAA commitments as distinct lines so the team does not collapse everything into a vague "the vendor is compliant" answer.

| Party | Ownership questions to assign | Evidence to collect | Red flag |

|---|---|---|---|

| Your platform | Which screens touch ePHI or billing state? Who approves access changes? | Data-flow diagram, access matrix, screenshots of admin and support views | Support staff can see more than their role requires |

| Payment Processor | What contractual scope applies? What security documentation, log access, and export options are available? | Executed terms, BAA if applicable, security documentation, sample exports | Team assumes the processor covers every payment-facing risk in your product |

| EHR/telehealth vendor | Who enforces access controls on clinical and billing views? What audit logs are available? | BAA template, access-control docs, sample log export | Logs omit user IDs, timestamps, or key admin actions |

| Internal ops | Who provisions users, reviews access, investigates issues, and contacts vendors? | Named owners, escalation contacts, regular review record | First response depends on ad hoc Slack debate |

The target outcome is simple: each control has one operator, one approver on your side, and one evidence artifact you can retrieve quickly.

Define RBAC and MFA ownership at each boundary#

Define who enforces RBAC and MFA at each system boundary, including admin and support surfaces. The checkpoint is concrete: permissions are assigned by role, and login controls include password policy plus multi-factor authentication.

Do not stop at therapist-facing or client-facing views. Verify admin consoles, support tools, finance views, and internal pages that can search users or inspect payment history.

Use audit logs as your main proof point#

Use audit logs as your strongest proof point because they are testable after launch. At minimum, confirm logs capture actions like logins, views, edits, and deletions with timestamps and user IDs.

Also require each party to state retention behavior clearly: what is retained, what can be exported, who can access it, and what happens after termination. If those answers are unclear, incident reconstruction will be unclear.

Rehearse the escalation path before launch#

Set one escalation path for control failures and rehearse it before launch. Name one incident owner on your side, plus one contact each for legal, security, payments ops, the processor, and the EHR/telehealth vendor.

Define plain-language triggers to activate that path immediately, such as suspected unauthorized access, missing audit logs, or support access outside approved roles. Review the matrix on a regular cadence, for example monthly, so ownership stays current as products and roles change. For a deeper implementation walkthrough, see Building a Virtual Assistant Platform Around Payments Compliance and Payout Design.

Design the therapist payment collection path#

Define one collection sequence and make each state change observable. In this workflow, unclear handoffs between invoice, Client Portal, AutoPay, processor response, and your internal ledger can create failures even when card charging itself works.

Map the collection sequence before launch#

Map the sequence in product terms before launch. Decide what event creates an invoice, what the client sees in the Client Portal, when AutoPay can charge a card on file, what counts as payment confirmation, and when the ledger posts.

Keep checkpoints explicit so ops can identify the source of truth at each stage: invoice, processor transaction, or ledger entry. If that answer changes across teams or code paths, reconciliation and support issues can follow.

Do not collapse "payment confirmed" and "ledger posted" into one status. If processor callbacks can arrive after the client action in your stack, acknowledge the attempt in the UI while reserving final ledger state for the signal you trust.

Decide which billing artifacts your product owns#

Decide early which billing artifacts your product owns versus passes through from an EHR or billing partner. If insurer-facing artifacts such as superbills or CMS-1500 forms are in scope, make an explicit call on whether you create, import, export, attach, or link to an external integration.

The operational checkpoint is alignment across support, finance, and product on where each artifact originates and where the final version lives. If answers differ by team, the flow is not ready.

Keep insurer-facing workflows separate from client card collection. HHS materials include health care payment and remittance advice in transaction scope and describe standards for eight electronic transactions. That supports keeping insurance paperwork and patient-pay collection as distinct paths instead of one vague "billing" flow.

Set failure rules before enabling AutoPay#

Set failure rules before enabling AutoPay. Recurring billing is a known risk area, and recurring-payment tracking plus chargeback handling can increase operational burden.

Cover these cases in plain language, where applicable:

- Expired card or failed card-on-file charge

- Partial payment against an open invoice

- Duplicate attempts from retries or repeated callbacks

- Delayed processor callback after your app already showed a pending or failed result

Consider idempotent internal records so late or noisy callbacks do not create duplicate outcomes. If a client retries after a timeout, define one rule for whether to create a new attempt, reuse the first, or route to manual review.

Prove the flow in release checks#

Add release checks that prove the flow still works as designed. In each release, test one normal payment, one AutoPay charge on a card on file, and at least one failed attempt.

Verify three outcomes every time:

- Transaction state remains accurate from invoice to ledger posting

- Audit logs capture the operational actions your team relies on, based on your internal policy

- Support tooling masks unnecessary PII in line with your internal role/access policy

If these checks fail, stop launch and fix the flow before rollout. For a full breakdown, read AgriTech Platform Payments: How to Pay Farmers and Agricultural Workers in Emerging Markets.

Design payout operations that survive scale and failures#

Treat therapist payouts as a separate lifecycle with its own evidence package. Define when a therapist becomes payable, what can block release, and what closes the case, or retries and exceptions become hard to control at scale.

Map the payout lifecycle end to end#

Map the payout lifecycle end to end, and make each state change observable. Start with gates and ownership, then choose rails.

A practical lifecycle can include: payable created, eligibility checked, policy gate passed or failed, payout initiated, external response received, payout completed or returned, exception resolved, and closure evidence stored. Keep these states distinct in your ledger and support tooling. Do not merge "initiated" with "completed," and do not treat "returned" as final if reissue or manual review is still open.

Keep this lifecycle inside the same privacy and compliance control boundary you already defined, especially for payout support notes and exported records. HICP 2023 gives two useful checkpoints here: data-flow mapping for tracing payout-data movement, and IAM lifecycle procedures, including provisioning, transfers, and deprovisioning, for clear control ownership.

Use one launch check: ask product, finance, and support where the source of truth lives at each stage for one payout. If answers differ, the design is not ready.

Define policy gates before payout initiation#

Define policy gates before payout initiation. Keep gates short, explicit, and ordered so operators can apply them consistently.

Typical gate questions are: is the payee account eligible, are required checks complete, is the payable approved, is the payout within release policy, and is there any manual hold. If frequent exceptions are needed to explain decisions, tighten the policy.

Restrict gate actions by role, require MFA, and log each decision in audit logs. At minimum, record actor type, timestamp, internal payout reference, related provider reference, previous state, new state, and reason code. Hold and release actions need the same trace quality as payout initiation.

Make retries explicit before automating them#

Make retry behavior explicit before you automate it. Define an internal rule for how a payable maps to payout instructions, and only allow reissue through an explicit authorization path.

Use a stable internal instruction key tied to the payable, not to click timing or event arrival. When late or replayed events arrive, resolve them against the existing instruction and route unresolved events to exception review instead of creating a new payout.

Do not assume webhook ordering guarantees. Define your expected retry behavior and test it directly before scale.

Choose payout design by reconciliation burden#

Choose payout design options by reconciliation burden and support capacity, not speed alone. Treat these as design hypotheses to validate in your own stack.

You still need to validate settlement time, failure rates, and support-load differences by rail or release mode in your own environment.

| Design choice | Where it can fit | Reconciliation shape | Support impact to expect |

|---|---|---|---|

| Direct bank rails | Primary payout path when payout surface is relatively narrow | Can be simpler if one internal reference is preserved through reissue or return | Bank-detail errors and returns may become a visible queue |

| Alternate rails | Coverage gaps or payee constraints on the primary path | Often adds branching from rail-specific states and evidence | May require more support training on status differences |

| Batch release | Controlled release windows with finance review | Group review can be easier, but exceptions can bunch near cutoff | Ticket volume may spike around cutoff and held batches |

| Real-time release | Faster release expectations after approval | Requires continuous state monitoring and reconciliation | Exceptions can surface throughout the day |

Run a pilot, then decide based on exception volume, reconciliation effort, and support readiness.

Write playbooks for held, returned, and unmatched cases#

Write playbooks for held, returned, and unmatched transactions before adding corridors or automating more volume. You may not need external SLA benchmarks to start. You do need an owner, an internal target, and required evidence fields.

| Case | Owner and target | Required fields |

|---|---|---|

| Held payout | Owner, target review window | Hold reason, actor, timestamp, linked payable ID, release or cancel decision |

| Returned payout | Owner, target for payee contact and reissue decision | Return time, external reference, internal payout ID, payee account version, resolution note |

| Unmatched transaction | Owner, target for investigation and closure | Unmatched amount, event source, import or callback ID, investigation actor, final disposition |

Close no exception without closure evidence. ONC's implementation point applies here: getting health IT to work efficiently and effectively in practice is still challenging, so design for investigation and reporting rather than ideal conditions. Related reading: Gaming Platform Payments: How to Pay Game Developers Studios and Tournament Players at Scale.

If you are pressure-testing retries, returns, and payout status visibility, review how Gruv Payouts structures operational controls before finalizing your year-one design.

Build audit-ready records finance and compliance can both use#

Audit-ready records should let finance reconcile movement and let compliance verify accountability, while keeping PHI and ePHI exposure to the minimum necessary.

Build one minimum audit package for every payment and payout#

Use one required record bundle for every payment event, including payouts, returns, and manual adjustments. Keep it compact and consistent, with fields that support reconciliation and investigation such as payment references, timestamps, user IDs, event types, and linked audit logs.

Make linked audit logs non-optional. Summary fields alone are not enough for investigations. Logs should preserve timestamps, user IDs, and event types, and support tracing actions such as view, edit, export, and e-signature where those actions exist.

Have finance and compliance independently reconstruct completed and returned payouts from the same record set. If either team needs side-channel context to explain the timeline, your package is not complete yet.

Minimize PHI and ePHI in payment events#

Apply minimum necessary access to the payment record itself, not only to user permissions. Keep payment operations centered on references, IDs, timestamps, and other reconciliation fields, and avoid pulling clinical context into payment logs, queues, or support artifacts unless clearly required.

Use role-based permissions so people only see what they need to do their jobs. If a workflow can touch substance use disorder records, design with added caution because 42 CFR Part 2 may impose stricter consent requirements than standard HIPAA.

Set monthly control reviews and keep evidence#

Treat a monthly review cycle as an internal operating control, not a HIPAA-mandated cadence. On that schedule, review sampled transactions, confirm payment-related role access is still least-privilege, and capture any material workflow changes that affect recordkeeping.

For sampled transactions, confirm the package is complete and audit logs explain manual actions. For access review, confirm role changes and departures are reflected in permissions. Keep evidence of each review, and include retention schedules, archived record handling, and defensible deletion so controls cover older records too.

Translate technical evidence into board-level risk statements#

Executives need risk statements, not raw logs. Convert the month's evidence into short judgments on access risk, record integrity, and third-party change impact, with the key driver for each judgment and the required follow-up action.

If leadership cannot understand exposure and trend without reading audit logs directly, the control summary is still too technical.

Plan market rollout by country and program constraints#

Roll out by corridor and care model you can verify, not by the broadest feature set your stack appears to support.

Map each market to verified dependencies and documents#

Create one launch card for each market and program pair: jurisdiction, care model, payout corridor, in-scope products, and the exact documents behind your legal or program assumptions. Also mark where PHI, ePHI, and PII are handled so privacy boundaries are explicit.

Use official artifacts for launch decisions. If you rely on a CMS item shown on FederalRegister.gov, verify it against the linked official PDF on govinfo.gov before treating it as launch policy. FederalRegister.gov states its display is a prototype, and the 2027 CMS Notice of Benefit and Payment Parameters entry dated 02/11/2026 is labeled a Proposed Rule.

If a rollout depends on program timing, treat those dates as planning checkpoints. For example, the IBH NOFO includes an A4.4 IBH Payment Strategy section. It also publishes dates including optional LOI due April 1, 2026, application due June 3, 2026, anticipated award notice September 15, 2026, and an anticipated period of performance from January 1, 2027 to December 31, 2033.

Constrain launch claims when assumptions are still unknown#

If legal status, payout operability, or program timing is uncertain in a market, mark that assumption as unknown, launch only validated corridors, and state explicit exclusions in commercial and support language.

Do not treat "coming soon" or "should work" as in scope. If an assumption depends on a proposed rule, an untested payout route, or a pending program award, keep it out of scope until you have documentary support and production evidence.

Use a per-market launch gate before go-live#

Keep the gate short and enforceable. At minimum, require sign-off on:

| Gate area | Minimum sign-off |

|---|---|

| Legal and privacy assumptions | PHI/ePHI handling is mapped, and unresolved market- or program-specific requirements are explicitly marked unknown |

| Payout operability | One end-to-end payout path and one exception path are completed and reconcilable |

| Support readiness | Queue ownership, macros, and masked views are ready for live cases |

| Incident escalation paths | Internal owners and external contacts are named for relevant payment, EHR, and telehealth dependencies |

Finance, compliance, and support should each be able to explain the same test case from the same evidence pack.

Re-run go or no-go after the first production cycle#

Use first-cycle production data to decide whether to expand, hold, or narrow claims by corridor and care model.

Prioritize concentration signals over totals. If one market drives a disproportionate share of exceptions or support confusion, pause expansion there until the underlying dependency or handoff issue is resolved.

Avoid common failure patterns and recover quickly#

A common failure pattern here is loose boundaries, not intent. Focus on four controls: PHI and ePHI classification, vendor evidence, automation gates, and ops-tool data exposure.

Keep HIPAA work separate from card-data work#

Treat HIPAA and card-data compliance as distinct tracks, then map where PHI and ePHI enter, move, and are stored. HIPAA obligations cover privacy, security, and breach-notification requirements for organizations handling patient data. Your control record should show each tool, the data it handles, and whether BAA obligations apply in your architecture.

Run one real case across legal, security, and support. If teams classify the same record differently, your boundary is still too loose.

Demand implementation proof, not vendor copy#

Vendor compliance pages are not enough for diligence on their own. Request implementation evidence and contract language that matches your use case, including patient-data storage workflows, access controls, and what is committed in writing.

Apply the same standard to legal interpretation. If your flow touches HIPAA access rights under 45 CFR § 164.524, confirm your reading against HHS guidance that remains effective only where consistent with the Ciox court order.

Prove exceptions before enabling automation#

Enable automation only after a controlled cohort shows clean exception handling. Keep manual overrides active, assign reconciliation ownership, and verify audit logs across a clean case, a failed case, and a retry before broader rollout.

For clinical or billing-related outputs, verify that incorrect generated summaries are caught before they are reused in treatment or insurance-billing disclosures.

If support cannot explain who changed status, when it changed, and why a retry occurred, hold expansion.

Remove excess PII from ops tools#

Reduce PHI/PII in support tooling to the minimum needed to complete the task. Enforce role-based access on remaining fields and require compliance sign-off on masked views before broad access.

Test a real support workflow with a non-privileged user. If the work can be completed without full patient detail, keep the mask. If not, redesign the view instead of widening access.

Conclusion and copy-paste launch checklist#

If you cannot prove control ownership, evidence quality, and recoverability, you are not ready to scale this vertical. That is the launch threshold, not a polished demo or a vendor claim.

Prove ownership before launch#

Treat unclear ownership as a stop signal. Keep one current document that shows where PHI, ePHI, and PII enter your flow, which vendors touch that data, and who owns each internal HIPAA and PCI workstream.

For each relevant vendor, keep the contract position you rely on, the reviewed BAA position where applicable, and named internal owners across legal, security, and payments operations. This is not administrative overhead. Business associates are directly liable for HIPAA Security Rule and Breach Notification Rule violations.

Verify access controls with evidence, not screenshots#

Do not mark controls complete from marketing pages. Confirm with test evidence that users are limited to minimum-necessary access and that each user has a unique ID for identity tracking.

Run role-based checks, for example support, finance, and admin, and confirm each role only sees what it should. Validate timeout behavior in practice. The grounding examples include a 10-minute inactivity lock, and 2 to 3 minutes in high-traffic environments. Where security choices reduce usability, document the tradeoff and approval.

Test the billing path and label unknowns clearly#

Feature presence is not deployment proof. Run end-to-end tests for your actual billing path and retain evidence of expected behavior and failure handling.

For checklist items without exact pass criteria here, keep them open until your team defines written acceptance criteria and test records. That includes AutoPay behavior, Superbill handling, CMS-1500 handling, payout retry idempotency, tokenization requirements, audit-log export requirements, and market-specific gates. If CMS-related Federal Register material is used in review, verify it against an official Federal Register edition.

Confirm recoverability and availability#

Plan for more than payment declines. Non-compliant telehealth handling is associated with data-breach and legal-penalty risk, and availability failures can affect both treatment and billing.

If cloud EHR is in your flow, recovery planning should show how treatment and billing remain available during outages. Use this copy-paste prelaunch checklist:

text [ ] Compliance boundary documented for PHI/ePHI/PII [ ] HIPAA and PCI responsibilities mapped internally and ownership validated [ ] BAA position documented for each relevant vendor where applicable [ ] Minimum-necessary access and unique user IDs verified with test evidence [ ] Timeout behavior validated in practice (example checkpoints: 10 minutes; 2 to 3 minutes in high-traffic areas) [ ] Out-of-pack items (AutoPay, Superbill, CMS-1500, payout retry idempotency, tokenization, audit-log export format, market/corridor gates) remain open until internal criteria and test records exist [ ] If cloud EHR is in scope, recovery plan demonstrates treatment and billing availability during outages

If any line has no clear owner, evidence, or recovery path, pause expansion until it does.

For a step-by-step walkthrough, see How to Launch a Legal Compliance Platform for Freelancers and Handle Their Payments. Before rollout, validate corridor and compliance coverage with your real launch constraints by talking with Gruv.

Frequently Asked Questions

Is Stripe alone enough for HIPAA compliant therapist and counselor payments?

No. A payment processor can reduce card-data exposure, but it does not define your HIPAA boundary for PHI handling, vendor responsibilities, or access controls. Before launch, confirm where PHI is stored or transmitted and what audit-log and contract evidence you can produce.

What is the practical difference between HIPAA requirements and PCI compliance in a mental health payment stack?

They cover different scopes. HIPAA focuses on protected health information and related privacy, security, and breach-notification duties, while payment-card controls focus on payment data. Keep them as separate design and review tracks.

When does a Business Associate Agreement (BAA) apply to a Payment Processor or EHR integration?

Use a data-first rule. Execute BAAs with every vendor that handles PHI, including EHR, telehealth, and billing vendors. For a payment processor, scope depends on your actual implementation and the data it receives.

Which controls are table stakes for launch: MFA, RBAC, Tokenization, Data Encryption, and Audit Logs?

Baseline safeguards include unique user IDs, strong passwords, MFA, encryption, and audit logs. If you use role-based access, confirm users only see what they need. In card flows, tokenization matters because it replaces sensitive payment data with generated codes stored outside the main system.

How should we choose between an all-in-one EHR stack and modular payments infrastructure?

There is no single best architecture. Choose the option that gives you clear PHI boundaries, workable vendor accountability, and auditable evidence in your real workflow. If an all-in-one or modular setup cannot show those basics, treat that as a launch blocker.

What should founders verify before expanding therapist payouts to a new country or market program?

Do not assume the current setup carries over unchanged. Re-check PHI handling boundaries, vendor scope, BAA coverage, and payout operability for the new rollout path. If those are still unclear, limit rollout scope until controls and evidence are in place.

What documentation should we require to prove audit readiness before go-live?

At minimum, require HIPAA policies and procedures, training records, a risk analysis, and a risk management plan. Include signed BAAs for PHI-handling vendors and audit-log evidence your team can review in practice. Update the package at least annually or when major changes occur.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- 405d.hhs.gov/Documents/tech-vol2-508.pdftrusted

- aspe.hhs.gov/reports/health-insurance-reform-standards-el...trusted

- cms.gov/files/document/oasis-e2-draft-508-11-14-25.pdftrusted

- cms.gov/files/document/r2021q100-hets-270271-compani...trusted

- digitalcommons.law.ou.edu/context/fac_articles/article/1648/viewconten...trusted

- federalregister.gov/documents/2026/02/11/2026-02769/patient-prot...trusted

- federalregister.gov/documents/2008/11/19/E8-26213/medicare-progr...trusted

- files.simpler.grants.gov/opportunities/45ca8b99-6524-47ec-9e7e-572fa9...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: