Quick Answer

Start with a control-first build: require clear pass states before funds release, split routing into auto-pay, queue-review, and hold lanes, and send payout requests with the same idempotency key on retries. Keep claim approval and payment finality separate, post accounting only after confirmed outcomes, and run daily exception tracking for returns, failures, and duplicates before adding new rails or higher volume.

Insurance claim payout automation that scales with control#

Scale claim payouts as a control program first and a speed program second. The goal is to move policyholder disbursements faster at higher volume without weakening fraud controls, AML discipline, or reconciliation when exceptions happen.

That balance matters because you are managing multiple risks at once. Claims outcomes are judged on fairness, trust, and settlement speed together, not speed alone. In 2026 property-claims results, the average time before final payment was 40.7 days, down 3.4 days year over year. Faster cycles can help, but only if your payout trail stays defensible.

Name the constraints early so execution does not drift toward "approved claim equals paid claim." Insurance fraud remains financially material ($308.6 billion a year cited by NAIC), and for covered products insurers must maintain written AML programs with risk-based internal controls under 31 CFR 1025.210. Rail choice also changes your operating model: FedNow supports near real-time payments and runs continuously, while ACH works within defined processing deadlines and carries explicit fraud-monitoring expectations under Nacha's 2026 phases. If your team can only describe payout initiation, not exception handling, you are not ready to scale.

This guide focuses on four decisions that determine whether automation holds up under volume:

- Choose your payout rail mix based on urgency, data quality, control needs, and exception workload.

- Set automation boundaries before API wiring so higher-risk or incomplete cases stop for review.

- Design integrations for traceability, not just connectivity, with consistent IDs and status mapping across claims, payments, and ledger records.

- Define go-live checkpoints: AML control path for covered products, a documented exception queue, and reconciliation views that tie provider references back to claim IDs.

If you want a deeper dive, read 5 Reasons Insurers Should Modernize Claim Disbursements with Digital Payout Platforms.

What to prepare before you automate the first claim payout#

Before you automate the first payout, lock down ownership and evidence. If you cannot name who approves rule changes, reconciles money movement, and handles failed disbursements, you are not ready to scale.

Step 1 Assign named owners#

Start by naming primary and backup owners across claims management, payments ops, finance ops, and engineering. Launch controls should explicitly cover approvals, verifications, and reconciliations.

Minimum checkpoint for one sample claim:

- owner of claim approval data

- owner of payout release

- owner of ledger posting

- owner of incident response

Shared ownership can become a failure mode. It feels collaborative until a duplicate payout or reconciliation break occurs.

Step 2 Inventory rails and actual volume#

Inventory what you use now, not what you might add later: ACH, real-time bank transfers, debit card push payments, digital wallets, and paper checks.

For each method, capture:

- monthly count

- average claim value

- geography

- claimant type

- usage type (

standard,urgent, orexception-only)

In the U.S., ACH is still a core rail (33.6 billion ACH payments in 2024, including more than 1.2 billion Same Day ACH payments). For real-time rails, separate FedNow from RTP because both run continuously and are distinct networks. Do not assume real-time, wallet, or debit-push options are available in every market or program.

Step 3 Build the launch-day evidence pack#

Before go-live, define the minimum production evidence pack:

- policyholder disbursement status map

- reconciliation reporting format

- audit trail requirements that can reconstruct payout events

Then test it with one claim from approval to payout outcome using timestamps, internal IDs, provider references, and approval records. If finance cannot tie provider events back to claim IDs, pause launch.

Step 4 Mark compliance boundaries by program and market#

Do not use one global checklist. Document where KYC, KYB, AML, and VAT validation are required, optional, or not applicable by program and jurisdiction.

| Check | Applies when | Note |

|---|---|---|

| Insurance AML under 31 CFR 1025.210 | Covered products, not every insurance product | Requires a written AML program with risk-based internal controls; covered-product scope under 31 CFR 1025.100 is program-specific |

| Beneficial-owner verification under 31 CFR 1010.230 | Business claimants, if it applies to your institution | Reported FinCEN relief effective February 13, 2026 may change timing |

| VIES VAT validation | EU flows | Can validate VAT numbers as valid or invalid, but that is not the full VAT determination |

Insurance AML obligations under 31 CFR 1025.210 apply to covered products, not every insurance product, and covered-product scope under 31 CFR 1025.100 is program-specific. For business claimants, confirm whether beneficial-owner verification under 31 CFR 1010.230 applies to your institution and whether reported FinCEN relief effective February 13, 2026 changes timing. For EU flows, VIES can validate VAT numbers as valid or invalid, but that result is not the full VAT determination.

You might also find this useful: How to Scale Global Payout Infrastructure: Lessons from Growing 100 to 10000 Payments Per Month.

Set risk and compliance gates before adding more automation#

Set hard release gates before you add payout speed. No claim should move to payout release until identity, due diligence, fraud signals, and audit evidence all reach a clear pass state you can test and explain.

Step 1 Encode policy into release rules#

Start with machine-enforceable states, not policy text. For U.S. programs, that typically means risk-based identity verification before release, risk-based ongoing due diligence in your AML design, and a sanctions block that stops payment creation or submission until cleared. For business claimants, define a KYB path for legal-entity review and beneficial-owner handling that matches your institution's actual obligations.

| Outcome | Release action |

|---|---|

| Pass | Payout can proceed |

| Fail | Payout is blocked |

| Needs review | Payout cannot auto-release |

| Blocked | Hold and reporting path required |

This matters even more on real-time rails because they can settle with finality and irrevocability. Put KYC, AML, and sanctions checks before payment instruction, not after.

Verification point: test one sample claim and show the exact pass or hold reason, timestamp, source check, and approver or rule version. A generic "verified" flag is not enough evidence.

Step 2 Build a review ladder with named decision owners#

Use a risk-based ladder, not one review lane for every claim. Auto-approve low-risk claims only when required checks are green. Route medium-risk claims to an analyst queue with defined evidence requirements. Escalate high-risk outcomes from risk scoring models to a named compliance or risk owner before any funds release.

Make ownership explicit at each stage. Claims ops should not make silent AML decisions, and compliance should not have to guess who approved an override. If your regulated structure requires internal controls, independent testing, training, and named AML ownership, your escalation ladder should mirror that structure.

Verification point: document who can clear each stage, what evidence is required, and who can override. Red flag: an analyst can clear a hold without a reason code, attached evidence, and a traceable audit entry.

Step 3 Pair AI fraud detection with forced fallback actions#

Treat fraud control as layered by design. Rules alone are weak against newer threats, and models alone are not enough, so combine model-driven signals with explicit fallback actions.

Define action by signal type before launch:

- duplicate-claim signal: hold straight-through payout and require analyst sign-off

- behavior inconsistency: step up verification before release

- anomaly risk on payout integrity: route to manual review and pause rail escalation until resolved

For suspicious activity paths, keep escalation time-bound. In U.S. banking rules, SAR filing can be due within 30 calendar days after initial detection, with no more than 60 calendar days when no suspect is initially identified, and urgent cases may require immediate law-enforcement notification by phone. If your organization is not the SAR filer, map exactly who files and when before launch.

Step 4 Add a compliance checkpoint before expanding payout volume#

Before you add rails, geographies, or claim types, run a control-quality gate. Speed alone is not a release signal. The audit trail must be complete enough to reconstruct both the decision and the money movement.

Require pre-expansion confirmation of four artifacts:

- identity and due-diligence status

- fraud-review outcome

- payout-release approval record

- payout event trace back to claim ID

If a sanctions block occurred, confirm the blocked-property reporting path is defined, since OFAC reporting can require action within 10 business days. If you cannot produce a clean record of why a payout was released, held, or blocked, pause expansion until control evidence is reliable enough for independent testing.

Pick the right payout rail for each claim scenario#

Once release gates are in place, rail choice should follow a simple rule: use real-time bank transfers for urgent claims with verified destination details, and default to ACH when cost sensitivity is higher and timing is flexible.

That rule covers most claims. The edge cases cause the trouble: instant payments with weak account data, wallets treated like bank rails, or paper checks left as an ungoverned fallback that adds fraud and support load.

Step 1 Use urgency and verified beneficiary data to set the default#

Set the default rail with two checks: how quickly funds must arrive and how confident you are in the destination details. If urgency is high and bank credentials are verified, real-time bank transfer is the first choice. In the U.S., FedNow runs continuously, including weekends and Federal Reserve holidays.

If urgency is lower, make ACH the baseline. FedACH is a batched, low-cost rail, and ACH credits can settle same day, next banking day, or in two banking days. Same Day ACH is the middle path when you need faster delivery without moving to an instant rail. It supports payments up to $1 million and settles three times daily.

Verification point: before auto-routing to an instant rail, confirm you can show the exact account details used, when they were last verified, and which claim approval triggered payment.

Step 2 Build a rail matrix with an explicit no-use lane#

Put the decision logic in one place so operations, finance, and support apply it the same way.

| Rail | Use when | Timing and ops profile | Do not use when |

|---|---|---|---|

| ACH transfers | Cost sensitivity matters more than immediate delivery | Batched, low-cost; can settle same day, next banking day, or two banking days | Account and routing details are incomplete or stale; ACH return oversight tracks administrative and account-data errors, including R02, R03, and R04 |

| Real-time bank transfers | Claim urgency is high and bank details are verified | Instant-style delivery; FedNow runs 24/7, and RTP payments are final and cannot be cancelled or automatically recalled | Beneficiary account confidence is weak, reversibility may be needed, or the receiving endpoint is not confirmed on your approved instant rail |

| Debit card push payments | You need fast consumer payout and have an eligible debit-linked destination | Funds can reach eligible debit-linked bank accounts in real time; Visa Direct states U.S. bank-account availability within 1 minute or less starting April 2025 | The claimant cannot provide supported debit credentials, or eligibility is unknown |

| Digital wallets | The claimant already uses the wallet and accepts wallet-specific transfer terms | Speed and fees vary by wallet; for example, Venmo lists standard bank transfers with no fee, while instant transfers carry a 1.75% fee (minimum $0.25, maximum $25) | The claimant expects direct bank settlement with bank-style traceability, or your team cannot support wallet-specific exceptions and cash-out questions |

| Paper checks | No workable digital route is available and mailed payment is still permitted | Can be slower to reconcile; support burden around mailing, receipt, and replacement can be higher | The claim is time-sensitive, address quality is weak, or fraud exposure is a concern; FBI alerts report check fraud is rising with mail theft as a major driver |

The no-use lane matters as much as the use lane. It stops teams from forcing a rail just because it exists.

Step 3 Define fallback logic before the first rail failure#

Define fallback rules in advance so decisions stay consistent under pressure.

- Step down from real-time bank transfer to ACH when urgency drops, the receiving account cannot be confirmed for your approved instant rail, or data is acceptable for ACH but not strong enough for irreversible instant release.

- Route to debit push only when an eligible debit-linked destination is available and the claimant has consented.

- Use a wallet only when the claimant actively prefers it and your support team can explain that wallet's speed and fee tradeoff.

- Move to paper check only when usable digital payout details are still unavailable after outreach and controls allow mailed disbursement.

Plan for finality risk explicitly. Mistaken RTP payments may not be recoverable. RTP payments are final, cannot be automatically recalled, and recovery is not guaranteed, so real-time flows should fail closed on weak beneficiary data.

For ACH, risk often concentrates in exception handling and data quality. Include account-entry source, validation result, and return reason when a credit is returned. If you submit an ACH return request, the RDFI response timeline is defined at 10 banking days.

Step 4 Verify support and reconciliation impact before you expand rail mix#

Rail mix changes support and reconciliation, not just speed. ACH is batched, which often aligns with batched close cycles. Real-time rails can require near-continuous status capture and support coverage outside standard banking hours. Wallets can split customer experience between wallet receipt and bank cash-out. Checks can add ambiguity across issuance, mailing, deposit, and clearing.

Run one live or simulated claim per rail. Confirm you can trace claim ID, beneficiary, payment reference, payout status, and any failure or return event in one record.

If you want to scale disbursements without making support and reconciliation the bottleneck, standardize around one default rail, one urgent rail, and one exception rail. For many teams, that means ACH as default, real-time bank transfer for urgency, and paper check only as a governed last resort.

Draw the line between straight-through payouts and manual review#

After rail selection, set a hard boundary between claims that can move untouched and claims that need a person in the loop. Use three payout lanes: auto-pay for low-risk claims, queue-review for explainable risk hits, and hold for integrity risks that require analyst sign-off before release.

If you want to scale without creating fraud, AML, and support cleanup, make this boundary explicit and traceable.

Step 1 Segment claims into three payout states#

Use three explicit states in the claims system: auto-pay, queue-review, and hold. Assign states with both risk scoring and business rules. Use a risk-based approach: stronger controls for higher risk, simplified handling for lower risk.

- Auto-pay: low-risk claims that cleared release gates, beneficiary verification, and claim approval checks.

- Queue-review: claims with mismatches, alerts, or missing elements that need human judgment.

- Hold: claims with material integrity or compliance concerns that must not be paid until resolved.

Store the exact reason code for lane assignment. Generic labels like "medium risk" are not enough.

Verification point: sample recent claims and confirm each record shows lane, triggering rule or score, and the claim approval event tied to payout eligibility.

Step 2 Apply a hard stop for payment integrity flags#

Use a hard stop when configured payment-integrity controls flag material risk: route the claim out of straight-through payout and require analyst review.

This is a control design choice, not a claim that every insurer must use identical signals. Monitoring cannot catch every illicit case automatically, so a manual queue is a necessary backstop. For flagged claims, requiring investigation before payout is easier to defend than pay-first, investigate-later handling.

| Review state | Trigger condition | Owner | Action | Required evidence to close |

|---|---|---|---|---|

| Auto-pay | Low risk score, no configured integrity flag, release gates passed | Claims ops or automated decision service | Submit payout on approved rail | Claim approval record, beneficiary verification result, release timestamp, rail decision |

| Queue-review | Medium risk score, data mismatch, destination detail change, missing documentary support | Claims analyst | Review facts, confirm or reject payout eligibility, document decision | Analyst notes, updated claimant or beneficiary evidence, rule-hit summary, final approval record |

| Hold | Configured integrity flag (for example duplicate-case or anomaly signal), AML alert, unresolved identity concern | Fraud, compliance, or designated senior analyst | Block payout until investigation closes and sign-off is recorded | Investigation notes, supporting documents retained, disposition reason, approver identity and timestamp |

If a claim is serious enough to stop, closure should require structured evidence, not side-channel approval.

Step 3 Govern overrides so they cannot bypass AML#

Manual review is manageable. Untraceable manual review is not. Every override should create a chronological audit-log record of who changed status, when, what was overridden, and what evidence supported the decision.

For hold-to-payable changes, capture the original hold reason, linked evidence, approver identity, and final release event. Silent edits are not sufficient.

Apply stricter controls to AML-related steps. Overrides can change payout disposition, but they should not erase AML checkpoints. Alert handling and filing decisions need explicit ownership and documentation, and supporting documents must be retained.

Reserve override rights to a small named group, require reason codes, and consider separating who clears held alerts from who releases funds.

Step 4 Publish lane SLAs that match the review path#

Do not force one universal SLA. Define predictable expectations by lane so disbursements stay understandable when claims move out of straight-through processing.

- Auto-pay: fastest path after approval and release gates.

- Queue-review: processed within a documented operating window, with outreach when evidence is missing.

- Hold: handled under fraud or compliance investigation rules with clear escalation ownership.

Keep SLA wording tied to product line and jurisdiction. Standards vary, but claims decisions still need to move within a reasonable time after complete proof-of-loss documentation is submitted. NAIC model text references payment within thirty (30) days after affirmation of liability. Treat that as a jurisdiction-dependent design input, not a blanket promise.

Checkpoint: review one week of queued and held claims and confirm you can state current owner, aging, next action, and missing evidence for each claim.

For a step-by-step walkthrough, see How Staffing Agencies Automate Contractor Disbursements with Batch Payouts via CSV.

Build the integration path from claim approval to payout confirmation#

Treat claim approval and payout confirmation as separate states. Your claims system is the source of payout intent, but a payout is not final until the provider confirms it. Collapsing those states can let retries, timeouts, and late webhooks create duplicate disbursements or a ledger marked paid before funds move.

Step 1 Emit one payout instruction from one approved claim decision#

Start from one approved claim decision event, then create one immutable payout instruction record before any provider API call. Freeze the submission-time amount, currency, rail, beneficiary details, and internal approval reference in that record.

Use this operating sequence: claim decision event, payout instruction creation, provider submission, webhook acknowledgment, then ledger posting on confirmed state. This is a control sequence for auditability, not a claim that every insurer uses the same flow.

Verification point: sample five paid claims and confirm each has a claim decision event ID, one payout instruction ID, one provider submission timestamp, and a later confirmation event before final ledger posting.

Step 2 Send provider requests with idempotency, not blind retries#

Blind retries can create duplicate payouts. For POST calls that support idempotency, assign one idempotency key per payout instruction and reuse that exact key for every retry. Do not issue a new key after a timeout.

Keep the guardrails explicit:

- Stripe accepts idempotency keys up to

255characters. - Stripe may prune keys after

24 hours, so keep your own dedupe record tied to the payout instruction beyond provider retention. - Idempotency compares retry parameters to the original request, so changing amount, rail, or beneficiary data on retry should error instead of replaying.

Also handle recovery after server errors carefully. With Stripe-style behavior, the same key can return the original result, including 500 errors. Before resubmitting, check whether the first attempt already created a payout attempt.

Step 3 Define a canonical identifier map across claims, provider, and ledger#

Use a fixed identifier map for traceability. Do not rely on names, email addresses, or dashboard search as join logic.

| Identifier | System of origin | Why it matters |

|---|---|---|

claim_decision_event_id | Claims management system | Proves why payout became eligible |

payout_instruction_id | Internal payments layer | Primary dedupe and retry anchor |

Provider id or resourceId | Payout provider | Used to fetch full transfer details when webhook payloads are lightweight |

Provider reference or referenceForBeneficiary | Payout provider | Supports support-case tracing and reconciliation |

ledger_entry_id | Finance ledger | Connects external payout state to accounting finality |

If support asks what happened to a claim payment, this map should let you move from claim decision to provider record to ledger entry without guesswork.

Step 4 Consume asynchronous updates and post the ledger only on confirmed outcome#

Treat webhooks as asynchronous status signals, not the full payout record. Because payloads can be lightweight, acknowledge quickly and fetch the full resource afterward. For Dwolla, return a 200-level response within 10 seconds, and note sustained failures can pause delivery after 400 consecutive failures and 24 hours since last success.

Normalize provider labels into internal statuses that fit your ledger (for example, processing, credited or posted, returned, failed, and canceled), while storing raw provider status alongside them. Status vocabularies differ: Adyen documents pending, failed, credited, and returned payout events, while Stripe Global Payouts exposes processing, posted, failed, returned, and canceled views.

If you use Virtual Accounts, add a readiness checkpoint. One documented implementation allows PENDING to transition to FAILED, and funds sent while pending may be returned, so do not treat non-active account states as ready for payout-related flows.

Checkpoint: trace one payout from approved claim to provider resourceId or reference, then webhook receipt, then ledger posting. If system records cannot prove the mapped internal status and raw provider status for outcomes like credited or posted, returned, failed, or canceled, the integration path is not production-ready.

Make reconciliation and audit evidence non-negotiable#

Reconciliation is most defensible when finance can prove each payout from claim authorization through provider execution to ledger record. Treat the ledger as the source of truth, and make reconciliation reports join to provider reference, internal payout transaction ID, and the status events behind the final outcome.

Step 1 Anchor reconciliation to the ledger#

Start from the ledger entry, then join outward to payout_instruction_id, provider id or resourceId, provider reference, and the claim decision that authorized the disbursement. Your provider dashboard is an input, not the book of record.

If you run real-time bank-transfer flows where the rail supports it, include real-time advices, acknowledgements, and debit or credit notifications in reconciliation reporting, even if final accounting posts on your normal schedule.

Verification point: for one business day, trace paid claims three ways: claim to ledger, ledger to provider reference, and provider reference back to raw status events. If a record is recoverable only from dashboard search or inbox threads, it is not close-ready evidence.

Step 2 Produce close-ready artifacts every day#

Do not wait until month-end to surface breaks. Daily artifacts like these help surface breaks early:

- Daily exception report for mismatches, for example provider confirmed but no

ledger_entry_id, ledger posted with no provider reference, or payouts stuck in processing beyond your expected window. - Unresolved return list with each returned or failed payout, linked claim, current owner, next action, and reissue status.

- Payout-to-claim mapping linking claim ID, claim decision event ID, payout instruction, provider ID or reference, ledger entry, amount, currency, and final status.

Build these artifacts as a chronological audit trail that lets teams reconstruct and examine the full sequence of events without manual storytelling.

Step 3 Attach tax and compliance documents only where they apply#

Treat tax documentation as conditional, not universal. When it applies, attach it to the same payout record instead of managing it as a side file.

| Item | Use case | Note |

|---|---|---|

| Form W-9 | Provide the correct TIN to a requester filing an information return | Tie it to the same payout record when it applies |

| Form W-8 BEN | Provided by a foreign beneficial owner to the withholding agent or payer when requested | Tie it to the same payout record when it applies |

| Form 1099-MISC | Covers rents, royalties, prizes, awards, and other fixed determinable income | If you file 10 or more information returns, IRS guidance requires electronic filing, and filers must furnish statements to recipients |

| Form 1099-NEC | May be required for independent-contractor service payments | If you file 10 or more information returns, IRS guidance requires electronic filing, and filers must furnish statements to recipients |

| FBAR | Include only where foreign financial accounts are in scope for your operations | Threshold is aggregate foreign account value above $10,000 at any time during the calendar year; due April 15 with an automatic extension to October 15 |

- Form W-9: used to provide the correct TIN to a requester filing an information return.

- Form W-8 BEN: provided by a foreign beneficial owner to the withholding agent or payer when requested.

- Form 1099 workflows: if enabled, keep form status, TIN status, recipient type, and recipient-statement delivery status connected to payee and payout history.

Use the right 1099 path: Form 1099-MISC covers rents, royalties, prizes, awards, and other fixed determinable income; Form 1099-NEC may be required for independent-contractor service payments. If you file 10 or more information returns, IRS guidance requires electronic filing, and filers must furnish statements to recipients.

Include FBAR controls only where foreign financial accounts are in scope for your operations. The threshold is aggregate foreign account value above $10,000 at any time during the calendar year, due April 15 with an automatic extension to October 15.

Step 4 Gate month-end completion on evidence, not optimism#

Set an internal close control such as: treat a payout batch as complete only after reconciliation reporting passes and the audit trail is reconstructable end to end. This aligns with audit-evidence expectations and books-and-records control requirements.

At month-end, sample closed payouts from the ledger and confirm claim authorization, provider execution reference, final status event, and any return or reissue handling, then require controller or finance-ops signoff. If signoff depends on narrative reconstruction instead of documents and IDs, the batch is not actually ready to close.

Need the full breakdown? Read Automating B2B Rebate Calculations and Disbursements for Platforms.

Before expanding volume, run your control checklist against your build plan: review Gruv docs for payout flows, webhooks, and operational status handling.

Plan failure handling before scale exposes weak spots#

Plan failure handling before launch, or growth can turn routine exceptions into duplicate payments, conflicting customer updates, and reconciliation breaks. Treat exception design as part of the payout system, with one status model shared by claims, support, engineering, and finance.

Step 1 Define failure classes before retries#

Use a small set of failure classes tied to specific actions. Avoid vague buckets that hide whether to retry, reissue, or stop.

| Failure class | What it means | Recovery action | Escalation owner |

|---|---|---|---|

| Rejected payout | Provider or receiving institution declined the transfer | Do not blind-retry. Review reject details, correct data if needed, then issue a new payout instruction when valid | Payments ops |

| Stale beneficiary details | Recipient name, account number, or routing details are outdated or mismatched | Hold payout, collect corrected details, confirm with recipient, then reissue | Support or claims ops |

| Duplicate submission | Same payout request sent more than once, often during retry or replay | Reuse the same idempotency key so retried requests return the same prior result instead of executing twice | Engineering, then payments ops |

| Provider timeout | Payout sent, but no final outcome in expected window | Retry only with idempotent handling; if still unresolved, move to manual investigation instead of sending a new payment | Engineering |

| Webhook mismatch | Duplicate delivery or signature-validation failure caused status drift | Verify signatures, deduplicate repeated events, and reconcile using internal payout ID plus provider reference | Engineering |

Use different customer messages by failure class. A rejection and a timeout are different states and should not produce the same recipient update.

Step 2 Separate retries from returns and reversals#

Do not run ACH and real-time bank-transfer failures through one generic playbook. For ACH improper reversals, keep a defined returns path: R11 has a 60-day return timeframe upon consumer claim, while R17 has a 2-day return timeframe.

| Rail | Mechanism | Note |

|---|---|---|

| ACH improper reversals | Defined returns path | R11 has a 60-day return timeframe upon consumer claim, while R17 has a 2-day return timeframe |

| FedNow | Payment status response (pacs.002) and payment timeout clock | Used to indicate expected settlement or rejection timing |

| RTP | Return-of-funds messages (camt.056 request and camt.029 response) | Used for errant or fraudulent payments |

For real-time payments, handle responses and exceptions explicitly. FedNow requires a payment status response (pacs.002) and uses a payment timeout clock to indicate expected settlement or rejection timing. RTP uses return-of-funds messages (camt.056 request and camt.029 response) for errant or fraudulent payments. Build your process around those mechanisms instead of assuming instant payments can be unilaterally reversed.

Use one internal status ladder across rails, for example: submitted, pending response, rejected, credited, return requested, returned, reissue approved.

Step 3 Create an exception queue with aging and evidence fields#

Create a single exception queue before scale, and track aging from first detection. Each item should include claim ID, payout instruction ID, provider reference, failure class, first-seen timestamp, latest status event, current owner, next action date, and customer-contact state.

Aging rules do not need to be universal, but they must trigger escalation to a named owner when action stalls. If you use the Federal Reserve Exception Resolution Service for ACH or FedNow cases, store the case ID and case history details with the payout record so the 13-month archive is usable during investigation and close.

Roll out in phases with hard go or no-go checkpoints#

Once failure classes and exception handling are in place, rollout discipline becomes the next control. Expand in stages and treat each stage as pass or fail before moving forward. Use these checkpoints as a pattern, then adapt phase boundaries to your operating model.

Step 1 Start narrow to isolate risk#

Start with a narrow cohort, and consider beginning with one payout rail, so issues are easier to trace to claim logic, integration behavior, or rail behavior. The first check is traceability, not volume: each payout should map cleanly across internal IDs, external references, and status history.

Do not treat a short happy-path run as proof of readiness. Early success can still hide retry and status-event handling gaps.

Step 2 Validate in sandbox with evidence, not screenshots#

Treat sandbox as formal readiness testing. Financial-institution change-management guidance expects pre-implementation systems, integration, functional, user-acceptance, and security testing, so a 200 OK response alone is not enough.

Your readiness evidence should include:

- passed systems, integration, functional, user-acceptance, and security tests

- audit-trail records showing what changed and when

- phase-level verification results for the rollout plan

If key evidence is missing, hold the rollout.

Step 3 Use a limited live cohort as a canary#

Move to live traffic only after readiness evidence is complete. Canary rollout means starting with a small share, evaluating results, and only then expanding. A phased pattern can be 25% -> 50% -> 100%, but the important part is the decision gate between phases.

Gate expansion on signals you can verify in real time:

- canary evaluation results support proceeding to the next phase

- audit-trail records are complete enough for investigation and review

- risk indicators remain within your predefined thresholds

Use alarms or equivalent controls to stop rollout when risk signals breach your thresholds.

Step 4 Require production validation and rollback readiness before full handoff#

Run a production-validation phase before full operational handoff. Payment-rail launches have used formal certification and production validation to confirm readiness before broad launch.

Document rollback procedures before expansion: if customer-impacting issues appear, pause or roll back and preserve a complete audit trail of what changed. If control quality drops during scale-up, stop expansion, fix root causes, and resume from the last phase that passed.

Compare vendors by operating fit not marketing claims#

Choose the vendor that can prove the controls you need to run live claims, not the one with the strongest speed language. If integration surfaces, reporting outputs, and payout-status visibility are not demonstrable against your flow, treat that as a material gap.

Step 1 Score verifiable evidence before demos#

Start with what is public and testable. Tranzpay publishes Gateway API documentation and claims core-claims integration plus real-time status updates. Dots shows API-first payout integration, Payout Links, and volume-based pricing language. PayQuicker documents a RESTful API and report retrieval actions. CCC highlights multi-party capabilities, reporting and analytics, and straight-through processing goals. Guidewire Marketplace language also says integration can reduce IT effort, while noting access is through direct CCC engagement. Choice Digital's public evidence is higher-level and centers on scalable disbursements plus bulk payment uploading.

| Vendor | Verifiable public signal | Key unknown to flag |

|---|---|---|

| Tranzpay | Gateway API, claims-system integration claim, real-time status updates claim | Pricing, rollout effort, production benchmarks |

| Dots | API-first integration, Payout Links, volume-based pricing language | Insurance-specific control depth, live benchmarks |

| CCCIS | Multi-party capabilities, reporting and analytics, Guidewire integration signal | Access path, pricing, implementation scope |

| Choice Digital | Scalable disbursements positioning, bulk upload dashboard wording | API depth, reporting detail, production evidence |

| PayQuicker | RESTful API, transaction and user report retrieval, 80+ currencies claim | Pricing path, insurance-workflow fit, failure-state detail |

Step 2 Require proof for the controls you will operate#

Have each vendor walk one claim from approval to payout confirmation using your evidence pack. The proof point is concrete: interface path, API or file, provider reference, status history, exception state, and reconciliation output finance can close. Ask for exported reports, sample status payloads, and at least one failed or returned payout path.

Step 3 Treat unknowns as decision risks#

Current public evidence does not support audited head-to-head benchmarks, standardized pricing comparability across all vendors, or complete webhook, idempotency, and failure-state behavior for every provider. Score those as explicit unknowns with owners and follow-up questions. Otherwise, demo polish can hide control gaps that appear only after go-live.

Step 4 Use one weighted scorecard with joint ownership#

Engineering, payments ops, and finance ops should co-own a single evaluation sheet and agree on the weighting before final selection. If engineering cannot verify interface behavior, or finance cannot verify reconciliation outputs, the vendor is not operationally ready.

Related reading: Automating Market Research Incentive Disbursements for 10,000 Respondents in 24 Hours.

Common mistakes that break claim payout automation and how to recover#

Claim payout automation often breaks at control boundaries, not at the payment rail. The pattern is familiar: speed-first rollout, unclear auto-versus-manual decisions, reconciliation treated as cleanup, and retry logic that can duplicate payouts.

Step 1 Re-sequence for controls before speed#

The fix for speed-first rollout is to gate release on controls first. Use a risk-based sequence: establish ongoing CDD/AML controls and maintain a complete audit trail before expanding faster payout paths, especially where settlement is final and irrevocable.

Set explicit launch blockers. Before funds move, confirm the claim is in the required review state and the activity record is complete and chronological from approval through submission. If either is missing, pause fast-rail expansion.

Step 2 Codify auto-pay versus review rules#

The fix for vague decisions is written routing logic. Define explicit risk-based rules, including duplicate-claim and anomaly triggers, so similar patterns route consistently and support ongoing suspicious-transaction monitoring.

Keep the routing states explicit: auto-pay, analyst review, or hold. Validate with replay tests for duplicate, high-value, and abnormal-timing scenarios, and require a reason when an analyst overrides the route.

Step 3 Make reconciliation reporting a go-live gate#

The fix for reconciliation drift is to treat reporting as a launch requirement. In 24x7x365 operations, unresolved exceptions can compound quickly.

Before scaling volume, require reporting that ties claim ID, internal transaction ID, provider reference, and payout status in one view. At minimum, accounts should be reconciled at least monthly, within 30 days, and finance should be able to isolate unmatched, returned, and duplicate items without raw-log workarounds.

Step 4 Enforce idempotent retries in API integrations#

The fix for brittle retries is idempotent request handling. Require an idempotency key on payout creation so safe retries return the original outcome instead of creating a second disbursement.

Test beyond happy-path sandbox runs. Simulate a provider timeout after acceptance, resend the same request, and confirm no duplicate payout is created.

Related: Airline Delay Compensation Payments: How Aviation Platforms Disburse Refunds at Scale.

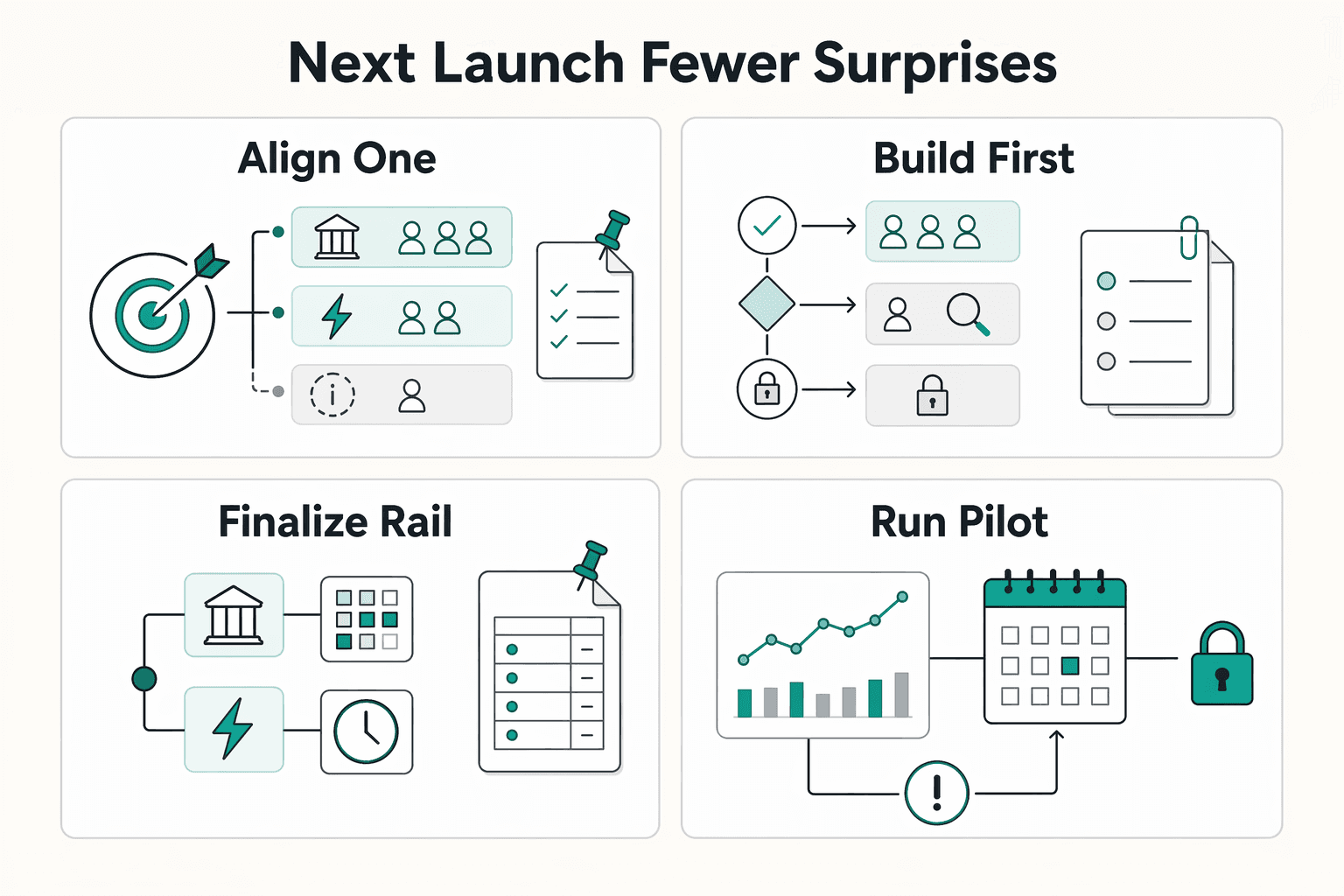

What to do next to launch with fewer surprises#

Start with one written launch decision: your initial rail mix, your automation boundary, and your first control gate. That keeps payout automation fast without making it fragile.

- Align one operating decision this week.

Pick an initial rail mix you can defend operationally. A common pattern is ACH as the batch default, with real-time transfers reserved for urgent claims where account details are verified. Define the boundary clearly: which claims go straight through, which route to review, and which stay blocked until a control clears.

Document the decision on one page and get named approval from claims, finance, ops, engineering, and compliance. If you operate in the U.S. and the product is a covered product under 31 CFR 1025, a written AML program under 31 CFR 1025.210 is required, and senior management approval is required. Keep market rules market-specific, since AML and CFT implementation is not identical across countries.

- Build the first implementation cut in writing.

Write the sequence before you scale volume: claim approval, payout instruction creation, provider submission, status ingestion, and ledger posting. For each step, assign an owner, a verification checkpoint, and a rollback action.

Make retry behavior explicit. If a provider times out after accepting a payout, define whether the next action is retrying with the same idempotency key, waiting for status confirmation, or escalating to manual review. For your chosen provider, verify that reusing the same idempotency key returns the same result, and verify webhook signatures using the raw request body exactly as sent.

- Finalize the rail table and trigger matrix before go-live.

Build the rail table around actual rail behavior. ACH is batch-based, not instant. FedNow is designed for 24x7x365 processing where participating institutions are enabled, and settlement is final. RTP settlement is final and irrevocable and supports transactions up to $10 million per transaction. Your fallback logic should not assume payouts on final-settlement rails can be revoked after release.

Make the trigger matrix explicit. Route duplicates, anomaly flags, stale beneficiary details, and missing claimant verification to manual review. If a reviewer overrides a hold, require a named approver, a reason code, and an audit-trail entry.

- Run a pilot cohort and require proof before expansion.

Start with one claim segment and one rail. Expand only after reconciliation reporting passes without manual repairs. Webhook updates are asynchronous and may be delivered more than once, so the pilot must prove deduplication and clean linking across claim ID, internal transaction ID, provider reference, and ledger entries.

Use this as the minimum launch gate:

- Confirm AML/CFT and audit-trail requirements by market, and document where U.S. covered-product rules under 31 CFR 1025.210 apply. * Finalize the rail decision table for ACH transfers, real-time bank transfers, and fallback paths. * Approve the auto-pay versus manual-review trigger matrix, including duplicate and anomaly holds. * Validate idempotent API integrations, webhook signature checks, duplicate-event handling, and reconciliation flow. * Run a limited live cohort and require clean reconciliation reporting before broader rollout.

If the pilot exposes reconciliation breaks, unclear ownership, or override abuse, pause expansion before increasing volume.

If you want a practical readout on rail fit, compliance gating, and rollout sequence for your program, talk to Gruv.

Frequently Asked Questions

How do insurers automate claim payments at scale without increasing fraud risk?

Do not expand straight-through payouts until your risk gates are written, owned, and testable. For covered products, 31 CFR 1025.210 requires a written anti-money-laundering program with risk-based policies, procedures, and internal controls, plus a designated compliance officer, training, and independent testing. In practice, route low-risk claims to auto-pay and send duplicate, anomalous, or suspicious patterns to review, especially where a covered-product transaction could trigger FinCEN reporting at the $5,000 threshold when other rule conditions are met.

Which payout methods are most automation-ready for policyholder disbursements?

Start with a narrow rail mix instead of launching every method at once. Vendor evidence shows insurance payout automation using ACH plus real-time rails, with some programs also supporting wallets, cards, and checks. A practical rollout is ACH and real-time bank transfers first, then cards, wallets, or checks once your customer data, support process, and reconciliation reporting are stable.

What controls should be in place before moving claims to real-time bank transfers?

Treat real-time transfers as a control decision, not just a speed upgrade. FedNow materials describe instant payments as final, irrevocable, and available 24x7x365, and RTP supports instant U.S. payments with transactions up to $10 million. Before enabling this path, require verified account details, a locked claim approval state, AML checks for the relevant covered product, and a complete audit trail.

What should stay manual versus automated in claims disbursements?

Automate the clean path: approved-claim event, payout instruction creation, provider submission, status ingestion, and ledger posting. Keep manual review for duplicate indicators, anomaly cases, stale beneficiary details, and payouts with unclear facts that may require suspicious-transaction review for a covered product. Any override that bypasses a risk hold should require a named approver and a recorded reason in the audit trail.

How do API integrations reduce payout delays and reconciliation errors?

They can reduce delays when payout creation is retry-safe and status updates are event-driven. Idempotent requests let you retry creation without performing the same operation twice, which is critical when a provider times out after accepting a payment. Webhooks provide event-driven updates, but duplicate deliveries and multi-day retry windows are possible, so deduplicate by event ID and reconcile by claim ID, internal transaction ID, and provider reference.

What are the first checkpoints to confirm a claims payout automation rollout is truly production-ready?

First, confirm you can trace a live payout end to end from claim approval to provider confirmation to ledger entry without raw-log workarounds. Second, test failure handling with duplicate webhook delivery, provider timeout after acceptance, and replay of the same idempotency key. Third, ensure finance reporting cleanly separates paid, failed, returned, and duplicate items, since some ACH return scenarios can surface later, including the 60-day R11 timeframe.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- advocacy.sba.gov/2026/02/18/fincen-issues-exceptive-relief-to...trusted

- csrc.nist.gov/glossary/term/audit_trailtrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalreserve.gov/paymentsystems/fednow_about.htmtrusted

- federalreserve.gov/paymentsystems/fedach_about.htmtrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

5 Reasons Insurers Should Modernize Claim Disbursements with Digital Payout Platforms

Claims payouts are where an insurer proves the product. If the money arrives late, trust erodes fast, and paper-heavy payment flows add friction. That is not just a service issue. The cited research says the longer it takes for money to reach the insured, the more trust erodes, and payment delays can stretch a claim by days or even weeks.

Airline Delay Compensation Payments for Customer Experience and Control

If you are evaluating an `airline compensation payments customer experience delays platform`, split the work into three lanes first: legally owed refunds, discretionary compensation, and outsourced claims recovery. Vendor pages often blur these together, but they lead to different policy choices, ledger treatment, and customer outcomes.

Scaling a Global Payout Platform from 100 to 10000 Monthly Payments

Scaling a global payout platform is rarely just a vendor problem. More often, it is an infrastructure and operating-discipline problem, because cross-border payments still carry persistent issues around cost, speed, access, and transparency. If growth is framed as "one more provider" or "higher API throughput," breakpoints can show up in finance, support, compliance, and reconciliation.