Quick Answer

Start with a governed shift from paper checks to ACH plus instant payments, then enforce one sequence: verify payee, route by policy, disburse once, and reconcile with traceable records. For insurers modernize claim disbursements digital payout platform decisions, the practical checkpoint is whether every payout can be tied to approval evidence, provider reference, and ledger output. Keep checks as exceptions, not defaults.

Why insurers are modernizing claim disbursements#

Claims payouts are where an insurer proves the product. If the money arrives late, trust erodes fast, and paper-heavy payment flows add friction. That is not just a service issue. The cited research says the longer it takes for money to reach the insured, the more trust erodes, and payment delays can stretch a claim by days or even weeks.

That pressure matters because the claims experience carries real retention weight. In the cited research, nearly 80% of policyholders said the claims process is the most important factor in deciding whether to stay with their current insurer. Separate cited research also points to up to $34 billion in annual premiums at risk from negative claims experiences. When operators talk about modernizing disbursements, this is the business case underneath the project.

The mistake is treating digital payouts as a nicer check printer. A digital claims payment platform is broader than that. You are deciding how claim disbursements get routed, approved, traced, and reconciled across digital payment methods, with paper as an exception path. That is why this article stays focused on the choices that shape outcomes: payment-method selection, policy gates, audit trail, and reconciliation quality.

If you lead finance, ops, or engineering, the useful question is not whether to go digital. Modern payment methods can speed up payouts, but insurance disbursements still sit inside regulatory requirements and multi-party claim interactions. The better rule is simpler: move faster only where you can explain and control the payout. Before you turn on faster rails, make sure every payment can be traced from claim approval to provider reference to ledger posting and reconciliation export.

That checkpoint matters because the ugliest failures are often operational, not headline events. They show up in unclear statuses, avoidable exceptions, and queues that are hard to explain cleanly to claimants or auditors. Paper checks create their own version of that pain through slower, more manual handling, but digital disbursements need discipline too. Speed without evidence and controls just gives you a faster mess.

So the promise here is practical. Teams can make meaningful modernization progress when they keep scope narrow and operational. Start with the highest-friction claim disbursements, define when different payment methods should be used, put approval and verification gates in front of faster rails, and design reconciliation before launch. The goal is a compliance-gated payout model with fewer surprises, clearer tradeoffs, and less reliance on paper checks.

For a deeper look at reconciliation controls in high-volume payout operations, see Catching Payout Errors Early in High-Volume Platform Operations.

Who This List Is For and How to Judge Options#

This list is for teams that own claims disbursements across product, finance, and engineering. If your goal is mostly a claimant-facing refresh, you will likely miss the harder requirement: fast payouts that are still traceable and explainable when exceptions happen.

| Area | What to confirm | Red flag |

|---|---|---|

| Rail coverage | ACH is the U.S. baseline, plus instant-payment support for time-sensitive cases; in the FedNow context, that means near real-time availability on a 24x7x365 service | A vendor is strong on only one rail, so exceptions fall back to paper or manual handling |

| Orchestration | Workflows verify payees, route ACH vs. instant payments by policy, and keep checks as an exception path | Only send capability or a vague "frictionless payouts" claim, without the exact pre-disbursement verification checkpoint |

| Controls | Role-based approvals, verification gates, and an audit trail before faster rails are enabled | Faster rails are enabled before those controls are shown |

| Failure handling | Idempotency for safe retries plus one concrete trace from request through status updates to ledger posting and reconciliation output | A demo ends at a generic "paid" status or resolves timeouts with "just resend" |

-

Start with rail coverage that matches real claim traffic. For U.S. payouts, ACH is the baseline because it reaches U.S. bank and credit union accounts. Then confirm instant-payment support for time-sensitive cases. In the FedNow context, that means near real-time availability on a 24x7x365 service. If a vendor is strong on only one rail, exceptions often fall back to paper or manual handling.

-

Judge orchestration depth, not just send capability. Look for workflows that verify payees, route ACH vs. instant payments by policy, and keep checks as an exception path. Digital account verification is a key control before faster rails. Ask to see the exact pre-disbursement verification checkpoint, not just a "frictionless payouts" claim.

-

Require controls before speed. KYC/CIP procedures are risk-based and part of AML programs, and KYB focuses on verifying company ownership and legitimacy. Controls will vary by program, but you should still see role-based approvals, verification gates, and an audit trail before faster rails are enabled.

-

Exclude vendors that cannot show end-to-end failure handling. Idempotency should allow safe retries without duplicate payouts. Ask for one concrete trace from request through status updates to ledger posting and reconciliation output. A demo that ends at a generic "paid" status, or resolves timeouts with "just resend," is a red flag.

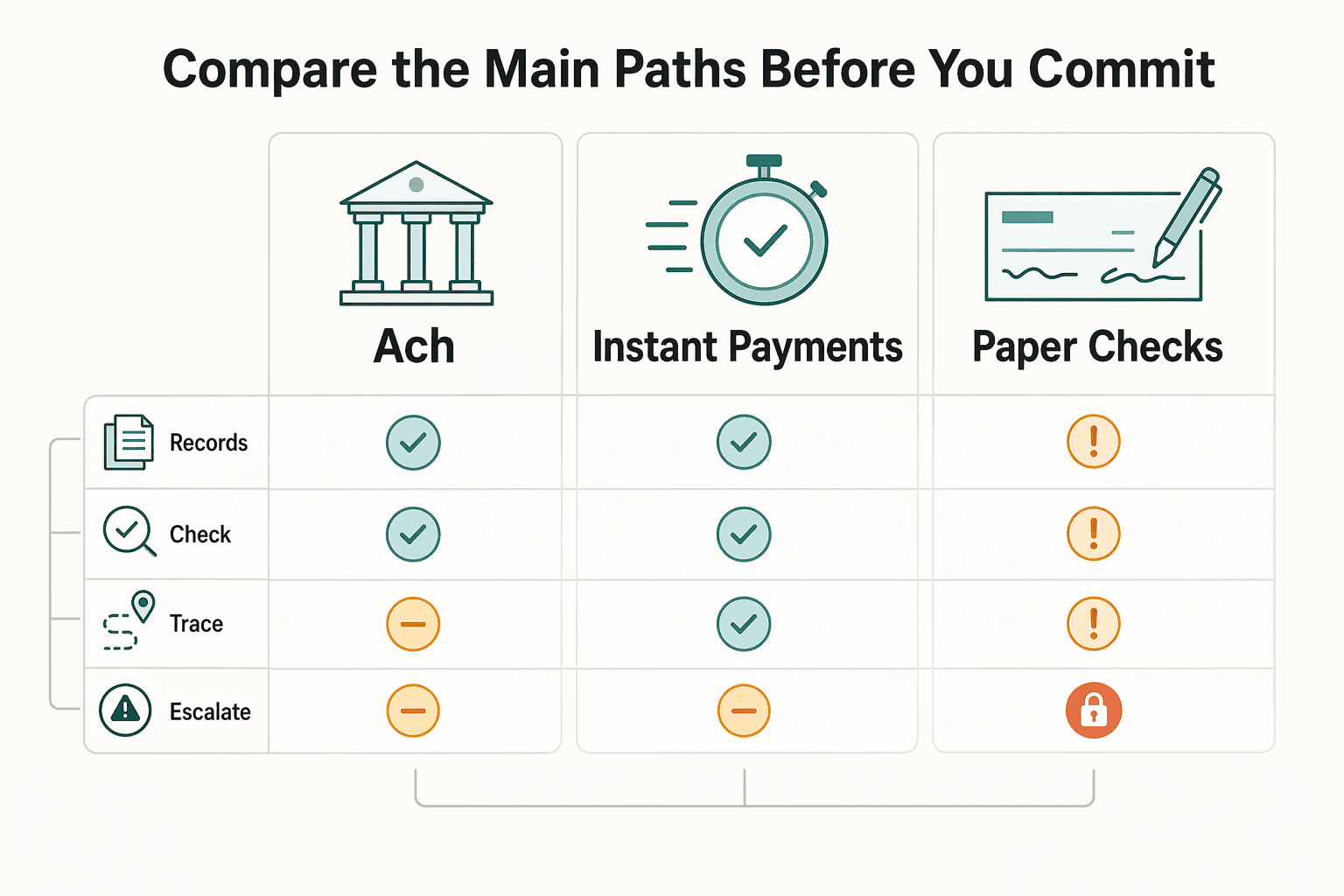

Compare the Main Paths Before You Commit#

Choose your default rail mix based on where failures hurt you most, not on speed claims alone.

| Path | Speed | Common failure modes | Customer friction | Operational effort | Fallback behavior | Plaid-style verification fit | Payout orchestration controls | Tool and model fit |

|---|---|---|---|---|---|---|---|---|

| ACH | Standard ACH follows bank settlement timing; Same Day ACH is designed for same-business-day movement (with payments up to $1 million) | Incorrect account/routing data, ACH returns, missed cutoffs; settlement is not standard on weekends and federal holidays | Moderate | Moderate | Retry by policy, move from Same Day ACH to standard ACH, or route to controlled check exception | Strong for setup: Plaid Auth can request checking/savings/cash-management account and routing details | Rail rules, retry policy, status tracking, reconciliation-ready records | Strong U.S. baseline rail |

| Instant payments | FedNow is built to send, receive, and process payments instantly | Ineligible or unverified accounts, instant rejects, timeout/retry mistakes | Low after payee setup is complete | Higher upfront | Fall back to ACH when instant is unavailable or blocked; keep checks as last resort | High priority, because faster rails make bad account data costlier | Policy gates, real-time error handling, duplicate-send prevention, immutable status trail | Strong when speed and status visibility are priority outcomes |

| Paper checks | Slowest and least predictable due to delivery/deposit timing outside digital bank rails | Address errors, lost/stale checks, reissues, weak status visibility | Highest | Highest ongoing manual burden | Fallback when digital rails fail, are declined, or policy requires paper | Limited relevance for bank-account verification | Exception approvals, stop/reissue flow, audit history | Keep as controlled exception, not primary path |

How to read this table in practice#

If reissues and "where is my money" tickets are your main pain, start by evaluating instant payments with ACH fallback, then confirm your verification checkpoint is enforced before release. If compliance exceptions are your main pain, start with policy gates and review queues before expanding faster-rail usage.

Where Plaid, Orbipay, and Tipalti fit#

Plaid Auth is a verification component for ACH setup, not a full claims disbursement platform. Orbipay EBPP is focused on electronic bill presentment and payment acceptance (bank, credit, debit), so the fit depends on whether inbound payment acceptance is part of your model. Tipalti mass payments is aimed at broad partner/supplier-style coverage across 196 countries and 120 local currencies, which may fit global payee operations better than domestic-only claim programs.

A useful vendor answer is specific: when ACH is used, when instant is used, when checks are used, and what evidence is retained when a payout fails or is rerouted.

Reason 1 Faster Disbursements Protect Retention at the Worst Moment#

If claims settlement feels slow, disbursement speed becomes a retention issue, not a cosmetic one. In claims experience benchmarks, trust and time to settle claim are both core dimensions, so payout timing directly affects how customers judge your process after a loss.

The practical move is to route verified, lower-risk claimants to digital rails first, keep status visibility clear, and retain paper checks as a governed exception path. This is not about promising churn fixes from speed alone. It is about improving one proven pressure point: in the cited research, 31% of claimants were not fully satisfied, and among that group, 60% cited settlement speed issues.

Why faster rails matter operationally#

The operational win is not only faster money movement. It is fewer "where is my payout?" moments because rail behavior and payout status are easier to explain.

FedNow is designed for real-time, always-on payments, while ACH settlement still depends on Federal Reserve settlement-service availability. That difference should drive policy:

- Use instant payments when the claimant is verified, eligible, and immediacy matters.

- Use ACH as the broad default when same-moment delivery is less critical.

- Keep paper checks for policy-required or digitally blocked exceptions.

What good execution looks like#

Strong execution is disciplined, not "instant for everyone." Start by moving low-risk, digitally verified claimants to faster rails, preserve paper as an approved exception path, and keep a usable status trail for both claimants and support teams.

Before release, your payout record should clearly show the verification result, selected rail, timestamp, and provider reference when available. If a vendor cannot show that event trail from verification to rail selection to outcome, exceptions and disputes become harder to resolve.

The tradeoff is upfront design work: faster rails reduce waiting friction, but they require tighter controls, including verification gates, timeout handling, and fallback rules. The standard to hold is simple: faster where verified, explainable everywhere, paper only by policy.

Reason 2 Automation Cuts Manual Ops Load and Support Tickets#

After you speed up verified payouts, the next operational win is reducing repeatable check exceptions. If finance and support are spending time on lost mail, stop-payments, reissues, stale-dated items, and uncashed check follow-up, moving that flow into digital payout orchestration can remove a large share of manual queue work.

Paper checks create a predictable loop: delays or delivery issues trigger status questions, then teams investigate and often rework the payment. Plaid describes this claimant friction directly through mail delays, lost checks, and reissue time, which leaves policyholders asking where the money is. ClaimsPages describes the back-office side of the same problem: tracking, stop-payments, reissues, stale-dated follow-up, escheatment processing, and uncashed-check handling all add administrative layers.

What actually reduces the queue#

The lever is not just "digital payments." It is orchestration with batch execution and webhook visibility so ops can send, track, and reconcile in one workflow. Nium's bulk payout model reflects the capabilities to look for: a single batch request, asynchronous processing, real-time webhooks, and full batch visibility.

Keep the order of operations explicit:

- Verify payee

- Route by rail

- Execute payout

- Reconcile outcome

Do not skip step four. With asynchronous batch payouts, a submitted response is not a final state. Your payout record should carry verification result, selected rail, batch or request ID, provider reference, status updates, and the reconciliation value that posts to your ledger export.

A common failure mode is fast execution without reliable outcome matching. In that setup, status updates arrive later and teams still reconcile by hand, so payment-status questions stay unresolved. Checks also remain a risk-heavy channel: AFP's 2024 survey found 65% of organizations reported check fraud activity.

Track this against your own baseline: reissue count, stop-payment volume, claimant status tickets, and days to reconcile each payout batch. If you need that baseline first, use Payout Support Ticket Cost Calculator: What Delayed Disbursements Really Cost Your Platform.

Reason 3 Compliance and Audit Readiness Improve When Controls Are Built In#

Fast payouts are only durable if you can defend each one later. Keep broad rollout gated until your KYC/KYB/AML requirements, approval policies, and audit trail are in place.

For regulated P&C teams, this becomes critical when disbursements involve identity and tax records. Some payout infrastructures require user verification before you can process payments or pay out funds, so compliance cannot be bolted on after launch. If you cannot show who was verified, who approved the payout, and which tax record supports treatment, keep faster rails limited to lower-risk cases.

Put the tax document path in the product, not in email#

Tax-document collection needs to be part of the payout flow, not a side process. In the US, Form W-9 is used to provide a correct TIN to payers. In broader programs, tooling may need to support W-9 plus W-8BEN, W-8BEN-E, W-8EXP, W-8IMY, W-8ECI, and Form 8233, and support year-end reporting for 1099 and 1042-S.

| Form or report | What the article says | Applies to |

|---|---|---|

| Form W-9 | Used to provide a correct TIN to payers | U.S. |

| W-8 series (W-8BEN, W-8BEN-E, W-8EXP, W-8IMY, W-8ECI) | Tooling may need to support these forms | Broader programs |

| Form 8233 | Tooling may need to support this form | Broader programs |

| Year-end reporting (1099 and 1042-S) | Tooling may need to support year-end reporting | Broader programs |

| Local tax ID and VAT | Collection may also apply | Non-U.S. payees |

For non-U.S. payees, local tax ID and VAT collection may also apply. One market example is collection in 60+ countries, but treat that as provider-specific capability, not a default. For cross-border or mixed-entity claims, confirm which forms are collected, validated, and retained in-flow, and which cases still route to manual review.

The checkpoint that keeps audits sane#

Set one strict rule: every payout event should be explainable from request to provider reference to ledger posting to reconciliation export. At minimum, you should be able to retrieve:

- Payee verification result and approval history

- Provider payout ID or reference

- Internal ledger or settlement posting record

- Downloadable payout reconciliation output

Do not accept a dashboard status of "paid" as complete evidence. Confirm you can retrieve the same payout through dashboard view, API payout detail retrieval, and a payout reconciliation report built for settlement-batch reconciliation.

The tradeoff is straightforward: stricter controls can slow some payouts, especially when W-8/W-9 records are missing or verification evidence fails review. That delay is often cheaper than cleanup later. IRS instructions note that without valid W-8 or W-9 documentation, tax may be assessed at 30% under chapter 3 or 4 or at the 24% backup withholding rate. If the record is incomplete, hold and route to review instead of creating an untraceable exception.

For a practical comparison of payout rails by market, read PIX vs. SEPA vs. ACH vs. SWIFT for Platform Payout Decisions by Market.

Reason 4 Better Engineering Design Prevents Duplicate or Opaque Payout Failures#

If you own payout engineering, treat every retry as unsafe until idempotency and clear state handling prove otherwise. Faster claim disbursements only help when a timeout, webhook retry, or delayed status cannot turn one approved payout into two payouts.

Idempotency is the first control, not an API nicety#

Use idempotency keys on payout create and update calls so a replayed request does not create a second disbursement. Idempotency exists to make retries safe and avoid performing the same operation twice.

If your provider supports keys up to 255 characters and can prune them after at least 24 hours, design your retry window and key storage around that boundary. The practical check is simple: for one payout attempt, you should be able to trace your internal payout ID, the idempotency key, and the provider reference to the same payment record.

When a provider response is unclear, do not open a new payout attempt. Retry with the same idempotency key and correlate the response to the original request.

Model failure states explicitly by rail#

Generic "retry later" logic creates duplicate and opaque failures. Handle each rail with explicit failure paths.

| Failure case | What to expect | What you should do |

|---|---|---|

| ACH return | ACH failures use standardized return codes that indicate why payment failed | Route by return code, not generic retry logic |

| RTP status or reject | RTP uses pacs.002 status messages and reject reason codes | Parse status and reason codes before deciding next action |

| FedNow reject | A receiving institution can return RJCT in pacs.002 | Mark rejected with reason context and route by policy |

| Webhook delay or duplicate delivery | Non-2xx responses can trigger webhook retries | Make webhook handling idempotent so duplicate deliveries do not duplicate posting |

| Provider timeout with unclear response | You may not know whether the request was accepted | Investigate with idempotency key and provider lookup before any resend |

If provider status is delayed, avoid blind manual resend. Route to investigation, keep event history intact, and run reconciliation checks before any further payout action.

Keep three implementation artifacts ready before rollout#

Before rollout, keep these three artifacts ready so failures stay diagnosable:

| Artifact | What it covers | Key detail |

|---|---|---|

| Retry policy matrix | Actions by failure type | Define auto-retry, retry-with-same-key, hold-for-review, or fail |

| Webhook contract tests | Retry and duplicate-delivery behavior | Verify non-2xx retry scenarios and duplicate event deliveries do not create duplicate outcomes |

| Incident run notes | Failure diagnosis record | Record event sequence, provider reference, idempotency key, reconciliation result, and required fix |

When evaluating a platform, ask for a live failure-path demo: create a payout, simulate a timeout, replay with the same idempotency key, then show provider record plus reconciliation output.

Related reading: Platform Economics 101 for Commission Fees, Payout Costs, and Gross Margin.

Reason 5 Modern Rails Expand Optionality for Cross-Border and Future Programs#

If international expansion is on your roadmap, treat modernization as a phased path: start with domestic rails, then add cross-border capability market by market as controls mature.

ACH remains a practical U.S. base, and U.S. instant options like FedNow are also domestic rails, not global ones. FedNow went live on July 20, 2023 and is available to depository institutions in the United States. That separation matters: domestic rail choices and international payout design are different decisions. Cross-border payouts add FX conversion, multi-institution routing, and jurisdiction-specific operating constraints that do not show up in a domestic-only launch.

Expand by jurisdiction, not by slideware#

Before enabling a new market, confirm the operating path in writing:

- Exact jurisdiction and supported payout method

- Expected payout timing and settlement behavior for that market and business profile

- FX path for the currency pair in scope

- Compliance evidence your team must retain for cross-border movement

Avoid assuming domestic approval logic and reconciliation fields will transfer cleanly. Cross-border provider regulation and supervision vary across jurisdictions, and the FSB final report dated 12 December 2024 makes that variation explicit. If a provider says coverage is "generally supported," push for market-level detail.

Treat emerging rails as options#

CBDC is worth monitoring, especially for potential cross-border improvements, but it should not be a day-one dependency for claims disbursement modernization. Evaluate it as an extension path, not the core reason to modernize now.

Related: How Platforms Should Prepare for CBDC Payments: What Digital Currency Means for Contractor Payouts.

Conclusion#

Modernizing claim disbursements is worth doing, but only if you treat it as a controls decision with faster rails attached. For most teams, the right move is a governed shift off paper checks: verify the payee, route by policy to ACH or instant payments, disburse once, and reconcile with an audit trail that still makes sense when something fails.

- Move off checks by policy, not by slogan.

Paper checks should become a managed exception path, not the everyday default, but you do not need to force a full cutover on day one. ACH is a practical base rail because the Nacha Operating Rules are built around explicit participant roles and responsibilities, and Nacha's fraud-monitoring amendments take effect on March 20, 2026 and June 19, 2026. The real differentiator is not "digital" in the abstract. It is whether you have clear rail eligibility rules, named approval owners, and a documented fallback when verification or review does not clear.

- Lock in duplicate prevention before you chase speed.

In the insurance claims payment process, a fast retry that creates a second payout is worse than a slow payout. A practical early checkpoint is simple and unforgiving: send the same idempotent request twice in testing and confirm the platform returns the prior result instead of issuing a second disbursement. Some APIs retain idempotency keys for at least 24 hours, which matters when retries cross shifts, batch windows, or overnight investigations. If your team can manually resend after a timeout without seeing durable event history, that is a red flag, not an ops shortcut.

- Demand records that explain every payout after the fact.

A digital payout platform earns trust when reconciliation is boring, not when the demo is fast. Ask to see webhook delivery state tracking that shows whether events are Delivered, Pending, or Failed, and ask what happens during retry windows that can run for up to 3 days. For instant rails, FedNow's ISO 20022 message format supports richer data and more automated end-to-end processing. That only helps if your side stores the message, processes it durably, and ties it back to the approval record and ledger entry. If a vendor cannot show one complete payout record from approval through payment event to reconciliation output, treat that as a risk that exceptions will become manual investigations at volume.

That is the standard to hold. If a platform cannot show failure handling, control gates, and traceable records, keep it out of high-trust claim disbursements until it can.

Frequently Asked Questions

Why modernize claim disbursements now instead of optimizing paper checks?

Paper checks can add delay and fraud exposure. Plaid notes that payment delays can extend the life of a claim by days or even weeks, and the FBI says suspicious activity reports tied to check fraud nearly doubled from 2021 to 2023 amid mail-theft pressure. If your team is spending time on check exceptions such as stop-payments, address fixes, and "check not received" calls, you are tuning an exception path instead of fixing the main payout channel.

What usually causes payout delays in the insurance claims payment process?

Delays often come from operational handoff issues, such as payee-data errors, manual review queues, rail cutoff timing, and weak status visibility after the payment is sent. A simple checkpoint is whether you can trace every payout from approval decision to provider reference to ledger posting. If you cannot, delays turn into long investigations instead of quick corrections.

When should a team choose ACH versus instant payments for claim payouts?

Choose ACH when immediate funds access is not required and it fits the claim context. Same Day ACH is faster than standard ACH and, per Nacha, settles three times daily with a per-payment limit of $1 million. Choose instant payments when the claimant needs funds right away and your controls can support immediate release, since FedNow states recipients have full access to funds immediately. If you are unsure, start with ACH as the base rail and reserve instant for verified, lower-exception cases.

What controls are required before enabling instant claim disbursements?

At minimum, teams typically need risk-based identity verification and sanctions controls before enabling faster rails, with clear approval rules and auditability before scale-up. The Customer Identification Program requirement in 31 CFR 1020.220 calls for risk-based procedures to verify identity, and OFAC expectations are also risk-based by product, customer, transaction, and geography. The exact allocation depends on your entity model and partners, but the control categories should be settled before you scale faster rails.

How do digital account verification and payout orchestration reduce payout failures?

Digital account verification can help catch wrong or stale bank details before money moves and may reduce avoidable returns and rework. Payout orchestration adds routing logic: send eligible claims to instant, fall back to ACH when needed, or hold for review if checks fail. A red flag is any process that lets staff manually resend after a timeout without confirming provider status first.

What should a realistic first 90-day modernization sequence include?

There is no universal, evidence-backed 90-day sequence, but a practical first phase can include mapping current check exceptions, picking a domestic rail pair such as ACH plus instant, and defining the fields needed for approval, provider tracking, and reconciliation. Then launch with a limited claimant segment, not every line of business at once. In practice, you want idempotent request handling, webhook status capture, review queues, and exception reporting in place before you widen eligibility.

How should teams measure success after launch besides payout speed?

Track reissue volume, return or reject rate, fraud and sanctions exceptions, manual reconciliation effort, and "where is my money" ticket volume. JD Power’s 2026 U.S. Property Claims Satisfaction Study says faster repair and payment cycle times, along with stronger digital capabilities, helped drive improvement, so customer experience should be part of the scorecard. If payouts are faster but exceptions and support contacts rise, the rollout is not actually healthier.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/OfficeOfForeignAssetsControl/01trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fbi.gov/investigate/cyber/alerts/2025/mail-theft-rel...trusted

- federalreserve.gov/paymentsystems/fednow_about.htmtrusted

- federalreserve.gov/paymentsystems/fedach_about.htmtrusted

- imf.org/-/media/Files/Publications/FTN063/2024/Engli...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/instructions/iw8trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Payout Support Ticket Cost Calculator for Delayed Disbursements

Delayed disbursement tickets are not always just a queue problem. In many teams, one customer contact triggers additional internal follow-up, so visible ticket counts can understate total operating effort.

Tipalti Payouts Explained for AP-Centric Supplier Disbursements

**For platform teams, understanding Tipalti payouts is a buying and operating question, not a feature tour.** The useful question is not "does it support global payouts?" Ask whether this AP-centric model fits your controls, your reconciliation needs, and the countries, currencies, and payout methods you actually have to support. That is how you avoid expensive exceptions later.

How Platforms Should Prepare for CBDC Payments in Contractor Payouts

Separate your immediate payout launch from your CBDC readiness work. That is the baseline. Payment stablecoins have firmer policy signals today, while CBDC rollout paths remain market-specific and timing-sensitive.