Quick Answer

Build a risk-based operating model that pauses money movement when identity and payment risk align. Define owner-controlled `stop`, `review`, and `resume` states, require stronger verification for payout-detail changes, and block release when verification or AML status is unresolved. In the first 24 hours, preserve webhook, admin-log, and ledger evidence before systems overwrite key events. Resume payouts only after documented re-verification and dual approval so decisions are traceable.

Where identity theft shows up in freelance payouts#

This guide is for platform teams that own contractor, seller, or creator payouts. If you work in Compliance, Legal, Finance, Payments Ops, or Risk, your goal is a practical identity-theft prevention program: one that protects financial accounts, creates clear stop-and-review points, and leaves audit-ready records.

This is not a personal-security checklist for individual freelancers. The focus is operational: stopping social-engineering attempts before they become unauthorized fund movement in your payout flow. For many in-scope U.S. businesses and organizations, it is also a program requirement, because the FTC Red Flags Rule requires many organizations to maintain a written Identity Theft Prevention Program designed to detect warning signs.

Start with the attack chain, not the payout itself. A common pattern is phishing or other social engineering, then email or account compromise, then unauthorized fund movement. NIST defines phishing as social engineering through authentic-looking but bogus emails, and U.S. enforcement alerts describe both Business Email Compromise and impersonation-led account takeover as active paths into fraudulent transfers.

That framing matters because identity risk can turn into payment risk at handoff points. It happens when requests are trusted without enough verification or payout details are changed without enough proof. If those moments sit across different teams with no shared controls, gaps can appear before money moves.

Before you start#

Start with one question: can you reconstruct a suspected identity event from your own records? You should be able to show who changed account or payout details, who approved or overrode the action, and which timestamped records prove the sequence.

Keep the rest of this guide anchored to a risk-based approach. FATF describes that approach as the cornerstone of AML/CFT and also notes that countries cannot all take identical measures, so control depth varies by jurisdiction and program design. Do not assume one universal KYC or AML rule, document set, or escalation threshold. In at least some U.S. covered-institution contexts, AML duties include identifying and verifying beneficial owners of legal-entity customers.

Assume payout constraints also vary by market and provider setup. For example, Stripe states payout availability depends on industry and country, and initial payout timing can be 7-14 days after the first successful payment. The exact setup is not universal, but the operational point is consistent: place key controls before funds can move, not after. For a separate freelancer-facing topic, see A Guide to Disability Insurance for Freelancers.

Map the identity theft chain before choosing controls#

Map the fraud chain before you choose controls. If you cannot show where a case started, when it became an account-security event, and when funds could move, you will mix business disputes with identity incidents and triage the wrong risk.

Break incidents into evidence-backed stages#

Break each suspected incident into evidence-backed stages. A practical default chain is impersonation or other social engineering, credential theft through phishing or a fake login flow, account takeover, then payout-instruction abuse.

In freelance environments, early signals are often weak unless you define them tightly. On Freelancer.com, one documented warning sign is a request to move contact off platform to WhatsApp, Skype, email, or similar channels. Treat that as an early red flag, not proof on its own.

For each stage you mark, attach at least one timestamped artifact. If a stage has no evidence, do not assume it happened.

Separate identity events from business disputes#

Separate identity and security events from generic business risk before triage. Late delivery, quality disputes, or payment disagreements can be serious, but they are not automatically identity theft.

Use a clear trigger for identity handling: suspicious patterns or specific activities, such as deceptive messages seeking credentials or financial identifiers, unexpected account access, or payment-instruction change requests. Then route ownership accordingly. Dispute teams handle business conflict, while identity and security owners can freeze risky actions, verify account control, and preserve evidence.

A practical rule is to label each case as business dispute, identity/security event, or both, with a short rationale.

Mark where identity risk becomes financial loss#

Mark the point where the chain becomes financial loss. A common moment is when payment instructions are changed and funds are sent based on that update.

The BEC pattern is a useful parallel. Losses occur when a fake updated payment instruction is trusted and funds are sent. Map your own flow to those decision points, then put stop-and-review controls around them.

Your verification check is simple. Can you reconstruct each money-movement event end to end, including who requested it, what access or profile events came first, who approved it, and which red flags were present?

Assign owners and escalation paths before rollout#

Assign ownership before rollout so risky payouts are paused by rule, not by debate. Treat this as an operating control inside your incident response process: clear lead, clear backups, and clear handoff records.

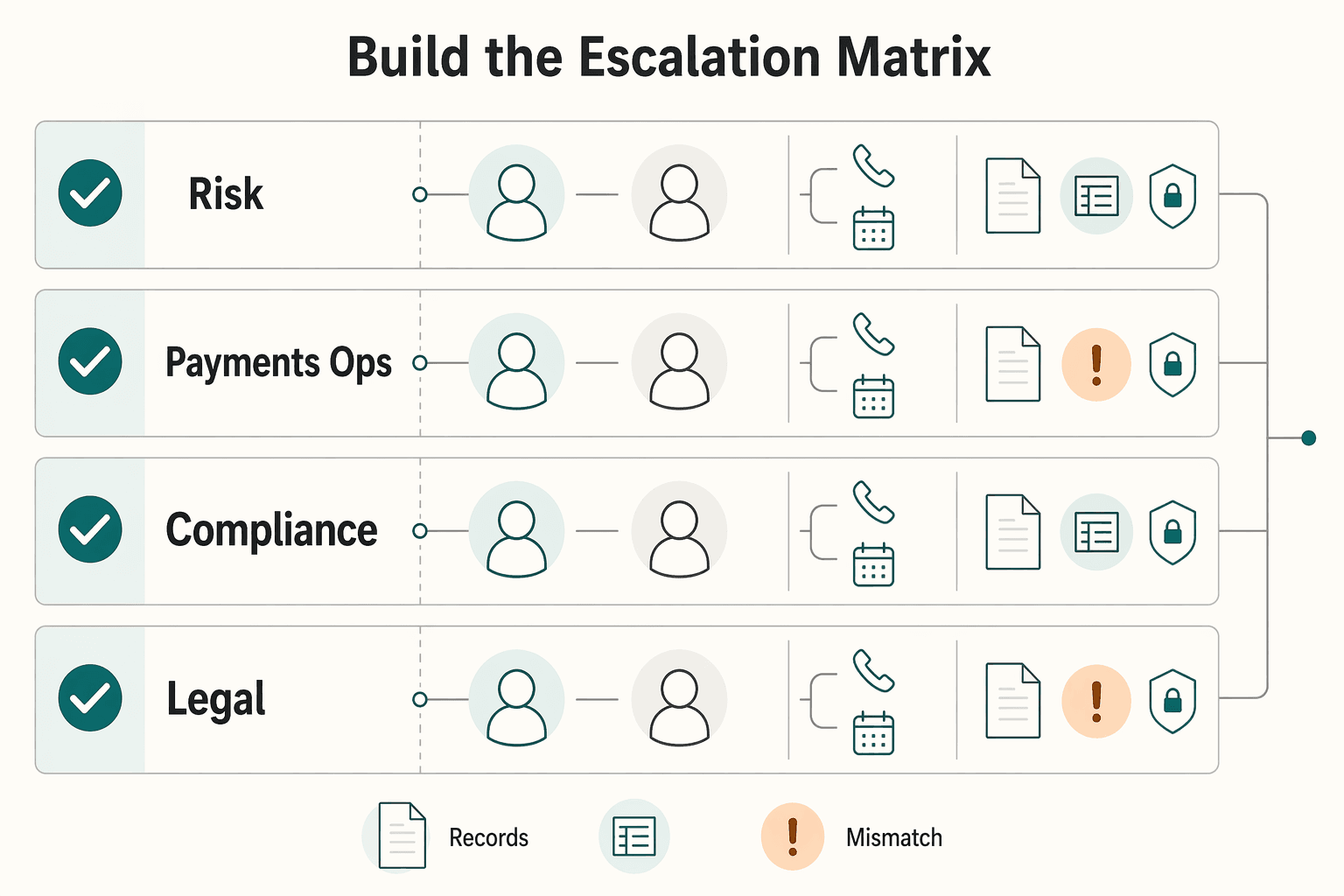

Build the Escalation matrix#

Build an Escalation matrix in your Incident Response Plan, or as an attached control document, with named owners and backups. Keep one incident lead accountable for coordination, and map decision ownership across functions such as Risk Ops, Payments Ops, Compliance, and Legal.

| Function | Primary owner | Authority | Typical trigger |

|---|---|---|---|

| Risk Ops | Incident lead or fraud lead | Open incident, place immediate hold, escalate for review | Identity red flags or suspicious account activity |

| Payments Ops | Payout operations lead | Hold or release payout batches after internal approval | Payout instruction changes or withdrawal events near release |

| Compliance | Compliance owner | Confirm required internal compliance handling and escalation | Identity-risk event with potential payout impact |

| Legal | Legal owner | Advise on legal risk and record-preservation handling | Confirmed takeover indicators or disputed identity |

As a check, each row should name a real person, a backup, and an after-hours contact path.

Set a manual-approval rule for overlapping risk#

Set one explicit policy rule for high-risk overlap: if identity signals and payout-risk signals appear together, route release decisions through manual approval before releasing payout batches. Keep this as an internal control decision, not an ad hoc shift judgment.

Define both signal sets in your playbook so teams execute the rule consistently. Identity signals should track suspicious patterns or activities tied to possible identity theft, and payout-risk signals should map to your own payout flow. Also apply separation of duties at release. The same person should not both investigate and approve fund release in the same case.

Define stop, review, and resume#

Define three internal case states and who can authorize each transition: stop, review, and resume. These are internal operating labels, so keep the definitions short and unambiguous.

stop: Risk Ops or the incident lead pauses risky payout activity when identity red flags are active.review: the case is in manual assessment; release stays blocked until designated approvers act.resume: payout activity restarts only after the designated approver confirms risk is resolved or accepted.

As a check, any on-shift analyst should be able to state, quickly and consistently, who can move a case between states.

Require an Audit trail for every handoff#

Require an Audit trail for every escalation handoff and approval. At minimum, record what event occurred, when it occurred, the outcome, and the identities linked to the event.

For operating quality, include a short internal reason in each handoff entry, even if that rationale field is your policy choice. A practical handoff record includes case ID, previous state, new state, approver, timestamp, linked evidence, and a short reason. If service providers are in the path, include their actions in the same trail.

For a step-by-step walkthrough, see Form T2125 for Canadian Freelancers: How to File With Clear Records.

Prepare prerequisites and system inputs#

Before you add new rules, make sure your baseline checks, evidence surfaces, and sensitive-data controls can support real payout decisions.

Verify baseline checks by market and entity type#

Start by confirming which checks are actually running, not just available on paper. That includes identity checks for individuals and businesses, AML controls, and VAT validation where tax treatment depends on it. In covered-bank contexts, a written Customer Identification Program is part of AML compliance, and legal-entity onboarding may require beneficial-owner identification and verification.

Keep this jurisdiction-specific. EU VAT validation through VIES queries national VAT databases, while UK VAT numbers are checked through HMRC's separate service. Do not treat VIES as valid for GB numbers. That path ceased on 01/01/2021.

Checkpoint: for each check, name the owner, the trigger point, such as onboarding or profile change, and the retained pass or fail evidence.

Inventory evidence surfaces before trusting alerts#

Assume your visibility is incomplete until you prove otherwise. List every source you need to reconstruct incidents: Webhooks, platform admin logs (if available), API request logs, and Ledger journal or subledger entries tied to source documents.

| Source | Retention or timing | Limit noted |

|---|---|---|

| Webhooks | Fast trigger feed | Endpoints may receive duplicate deliveries; some providers retry undelivered events for up to three days |

| Stripe events | Retrievable for 30 days | Compare provider event creation time with webhook delivery time and internal write time before deciding what happened first |

| AWS CloudTrail event history | 90 days of management events only | Does not include data events, Insights events, or network activity |

| Ledger journal / subledger | Tied to source documents | Use with provider events, admin actions, and account history for sequence reconstruction |

Check both coverage and retention against the limits above. A common failure mode is depending on an alert sequence you cannot replay because data aged out or was never captured.

Check how identity data is exposed internally#

Verify identity-data handling before rollout. Sensitive records should be encrypted, operational views should follow your masking approach, and access should follow least privilege so each role has only the minimum needed access.

Run one live check on a recent account-change case:

- Who can view full values

- Who sees masked values

- Whether those access events are logged

Document current proof limits#

Write a short gap note now. State what your team can prove, what it cannot prove, and which missing records would block a defensible stop, review, or resume decision.

If you cannot tie a profile edit, a webhook event, and the related ledger movement to the same case record, state that explicitly before you add controls.

Put preventive gates in front of money movement#

Put your strongest controls at the last decision point before funds leave. If identity status is unclear, payout should not proceed.

Require step-up verification for payout-changing actions#

Treat beneficiary edits, payout destination changes, and first-time withdrawal requests as potentially high-risk in your program. If an action can redirect funds, require reauthentication plus a second factor before accepting the change.

Keep this auditable in one trail. Record which factor was used, when it was completed, and which account field changed so a later payout decision can be tied to that same account and timeline.

Checkpoint: test one recent beneficiary-change case end to end and confirm the edit event, step-up event, and payout decision are connected in the same review record.

Block payout approval when KYC or AML status is unresolved#

Run KYC and AML-related gates before payout approval, not after funds move. Adyen and Stripe both describe verification as a prerequisite to enabling payouts, and Stripe notes payouts can be paused when required information is missing or unverified.

Use a simple implementation rule: check live verification status before an account enters a payout batch. If status is pending, missing required information, or otherwise unverified, route to review or hold automatically.

Where covered-bank onboarding applies, align with Customer Identification Program requirements under 31 CFR § 1020.220, including minimum identifying information before account opening and risk-based identity verification procedures.

Checkpoint: show approvers the current KYC or KYB state, source, last verification timestamp, and open AML flags in the payout decision view.

Reduce direct exposure of payment details where supported#

Reduce direct exposure of real payment details wherever your provider supports it. A virtual card number is a separate number tied to an account that can be used online without exposing the physical card number.

This is not universal across rails or providers, so apply it where available and keep fallback paths tight. Prefer provider-hosted setup, masked displays, and narrowly scoped edit permissions. If direct details must be handled, keep values masked by default and require step-up verification before saving any edit.

If you need a deeper look at tradeoffs, see Virtual Account Numbers for Freelancers: How to Protect Your Bank Details.

Add friction by risk level with explicit review triggers#

More friction is not better unless it lands at the right moment. Use a risk-based control model: stronger measures for higher-risk situations and simpler handling for lower-risk cases. FATF and FTC guidance both support this approach.

In practice, apply stricter checks to higher-risk situations, such as new entities, recently changed payout details, or suspicious patterns, and lighter checks to stable repeat behavior. Define review triggers in advance so response is consistent under pressure.

Use explicit triggers such as:

- payout destination changed and a withdrawal request follows before trust is re-established

- verification requirements reopened by your provider

- identity-risk signals and payout-risk signals appearing on the same account

| Control option | Control objective | Implementation effort | User friction | Failure mode if bypassed |

|---|---|---|---|---|

| Step-up verification on payout-changing actions | Help prove the actor still controls the account when funds can be redirected | Medium | Medium | Account takeover turns a profile edit into payout diversion |

| Pre-payout KYC and AML gate | Stop payouts when required identity data is missing or unresolved | Medium to high | Low to medium | Funds leave while verification gaps or AML concerns remain open |

| Controlled payout setup with virtual card numbers where supported | Reduce exposure of real payment details in online and admin flows | Medium | Low | Raw payment details spread across tools, tickets, or unauthorized views |

| Risk-based review triggers | Apply enhanced checks only where risk justifies them | Low to medium | Variable | Too much friction everywhere, or too little when fraud risk spikes |

As you define step-up checks and release approvals, align your control points with the operational states in Payouts.

Build early detection triggers that are operationally useful#

Your detection layer should answer one question quickly: does this look like possible account takeover with live payment risk, or an anomaly that still needs review? If you do not separate those paths, investigators get noise while risky payouts still move toward Payout batches.

Combine identity and transaction context before alerting#

Single signals are often weak on their own. A stronger trigger is a combination such as a recent profile change, behavior outside the account's normal pattern, and payout-related activity close behind it.

Use a risk-based mix of velocity, anomalies, account characteristics, transaction context, and account history. Build baselines of normal activity so atypical behavior is easier to flag early.

Use Webhooks for speed, then verify against internal records#

Use Webhooks as a fast trigger feed, then confirm what happened in your internal records, admin logs, and account history before escalating.

Focus on sequence integrity against your own policy. Did account changes, required checks, review decisions, and payout approval occur in the expected order? Treat unexpected order as an investigation signal, not standalone proof of account takeover.

Define internal confidence tiers that map to action#

Investigators move faster when alert tiers map cleanly to action. Use clear internal tiers:

| Tier | When it applies | Response |

|---|---|---|

| Low confidence | Unusual identity or account activity without clear payment risk | Queue investigation and continue monitoring for linked events |

| Medium confidence | Mixed indicators that need analyst review before the next payout cycle | Send for analyst review before the next payout cycle |

| High confidence | Aligned indicators with imminent money movement | Handle as a high-priority alert; route to the payout hold path when money movement is pending |

Make each tier auditable by attaching the evidence used for the decision, including event IDs, timestamps, changed fields, and related account actions.

Connect alert tiers to payout decisions#

Alerts should not stop at detection. Tie each tier to a predefined response in your own program. For example, when alerts fire without clear payment risk, queue investigation and continue monitoring for linked events. When alerts fire with pending money movement, route the case to the payout hold path defined in your controls.

Keep payment-delay handling jurisdiction-specific. For UK context, FCA guidance describes that PSPs can delay payments by up to 4 business days to investigate where there are reasonable grounds to suspect fraud or dishonesty. The reimbursement regime referenced there came into force on 7 October 2024. Use that as a model for policy design where relevant, not as a global default.

Run a first-24-hour incident sequence#

In the first 24 hours, prioritize containment, evidence integrity, and safe recovery execution. Treat this as an operational sequence, not a wait-for-certainty exercise. Act fast to limit additional loss, then tighten proof and coordination.

| Window | Primary objective | Required output |

|---|---|---|

| Hour 0-2 | Contain exposure and preserve volatile evidence | Active holds on at-risk payouts and a controlled evidence set |

| Hour 2-8 | Verify actor identity and reconstruct event order | Defensible timeline and impact classification |

| Hour 8-24 | Run cross-functional escalation and timed communications | Timestamped decision log, owners, and next actions |

Contain exposure and preserve volatile evidence#

In Hour 0 to 2, pause only the payouts that could still move money, rather than freezing every payout flow. Temporarily lock the highest-risk account actions, for example payout destination edits, credential resets, and admin override paths, where your controls allow. The goal is to reduce blast radius without freezing the whole platform.

Preserve evidence before systems or responders overwrite it. Snapshot relevant provider event and Webhooks records, auth logs, admin logs, session data, and Ledger journal entries, then maintain chain-of-custody details: who collected what, when, from where, and under which case ID.

Two quick checks can help: confirm the hold is visible in the same queue or state machine that releases funds, and confirm preserved records have stable timestamps and event IDs. If systems use different timezones, normalize immediately.

Verify identity and reconstruct the event order#

In Hour 2 to 8, answer two questions: who is operating the account now, and what happened in what order?

For identity, use an out-of-band verification path that does not trust the active session. If your KYC flow supports re-verification, use it against the established identity record. Government-ID re-verification is used by at least one major marketplace, and manual review can take three to five business days on some platforms.

For sequence reconstruction, combine provider events and Webhooks with your Ledger journal, admin actions, and account history. Do not treat webhook delivery order alone as authoritative. Some providers retry undelivered events for up to three days. Compare provider event creation time, webhook delivery time, and internal write time before deciding what happened first.

Classify impact before moving on: suspicious access only, payout changes pending, or potential funds released. That triage sets communication urgency and ownership.

Activate the Escalation matrix and start timed communications#

By Hour 8 to 24, run this as a cross-functional incident, not a security-only thread. Your Escalation matrix should assign owners across operations, compliance, legal, and communications, with one incident lead controlling handoffs.

Produce a short decision record: what happened, what was paused, what evidence is preserved, who must be contacted, and what remains unproven. Timestamp each handoff and each decision, including deferrals, to avoid parallel, conflicting outreach.

If your entity is in scope for NIS2, map first-day timing accordingly: early warning within 24 hours of awareness of a significant incident, then incident notification within 72 hours. Apply this where relevant, not as a global default.

Enforce idempotent retries in every recovery action#

Retry safety is a core recovery control. If a hold, reversal, or notification call times out or returns an unclear result, retry with idempotency so the same operation cannot create duplicate side effects.

At the API layer, reuse the same idempotency key for retries of the same operation, for example case ID + action type + object ID, until you receive a definitive outcome. Verify results in both places: the external API response and your internal Ledger journal or case log.

Watch for a failure mode: different services generating new keys for the same action. That is how duplicate holds, duplicate notices, and duplicate reversal attempts slip into an already active incident.

Capture evidence that stands up in audit and investigations#

Your evidence pack should let an independent reviewer verify what happened, what it affected, and what you did, using source records instead of team memory.

Start one controlled incident record#

Run one shared Incident reporting checklist for the case so timeline and actions stay in one place. Include what happened, who was involved, a timeline, and actions taken, then keep updating facts as the incident develops.

Use a consistent line format for timeline entries: timestamp, actor or process, source system, and evidence reference. Keep time references consistent across entries.

Tie each claim to system evidence#

Only make a case claim when you can point to the underlying record. Use your Audit trail, webhook event records, and chain of custody records to support each conclusion.

If a reviewer cannot reproduce key conclusions from the references alone, the pack is not ready. Use screenshots as supporting context when needed, but anchor final claims to original records and event references.

Prepare outside-facing summaries with data minimization#

Keep two outputs: a full internal investigation pack and a purpose-limited external summary for partners or regulators. In the external version, include only the personal data needed for the reporting purpose.

Where reporting applies, summaries may need categories and approximate counts of affected people and records, likely consequences, and mitigation measures. Your breach record should also document facts, effects, and remedial action so supervisory review is possible, and timelines should support any applicable 72-hour notification window where feasible.

Track evidence-pack completeness in a table#

Use a compact tracker so ownership and review gaps are visible.

| Artifact name | Owner | Source system | Retention period | Review status |

|---|---|---|---|---|

| Incident reporting checklist | Incident lead | Incident log / case system | Per retention policy | In review |

| Audit trail export | Risk Ops / Security | Admin and account logs | Per retention policy | Verified |

| Webhook event record set | Payments Ops | Provider webhook store | Per retention policy | Verified |

| Breach notification summary | Compliance / Risk | Incident log / case system | Per retention policy | Pending |

| Chain of custody record | Security / Forensics | Evidence register | Per retention policy | Verified |

If an artifact is missing an owner, retention instruction, or review status, treat it as an open control gap.

This pairs well with our guide on A Guide to Form 1099-K for Freelancers Using Payment Apps.

Set payout hold and release rules teams can execute quickly#

Do not release payouts on judgment alone. Base hold and release decisions on two observable factors: identity-risk severity and current evidence quality.

Define hold criteria by risk severity and evidence quality#

Treat a credible identity-theft Red Flag tied to money movement as a hold until review is complete. If key evidence is missing or weak, keep funds held and escalate rather than releasing on partial confidence.

Use a simple reviewer test: from the case file alone, can someone confirm what changed, who requested the payout, and what evidence links that requester to the legitimate account holder? If not, keep the hold in place.

Require dual approval after beneficiary or credential events#

For cases involving beneficiary details or account credentials, use two recorded approvals before release when your controls call for heightened review. One approver confirms the investigation outcome and evidence quality. A separate approver, not the payout initiator, confirms release readiness.

This should be a targeted control for identity-sensitive payout events, not a blanket rule for every payout in every market. Record both approvers, timestamps, and release rationale in the audit trail.

Re-run deterministic release checks before funds move#

Release only after the same checks pass every time:

- Identity re-verification passed. Re-run KYC or equivalent verification required by your program. Where available, step-up checks at withdrawal, such as video verification, can be used for higher-risk cases.

- Required remediation steps are complete. Confirm any credential or access-control actions required by your policy are complete.

- AML-related review is resolved per policy. If the case is still under active AML-related review in your workflow, keep the hold in place and escalate instead of releasing.

Use current source records at decision time, not stale screenshots or unverified notes.

Hold and escalate when evidence is incomplete#

If evidence is incomplete, keep the payout hold and escalate per your escalation matrix. Operational actions such as disabling payouts, suspending accounts, or enforcing stricter KYC checks can be used while risk is unresolved.

If evidence is complete and release checks pass, release with a short written rationale explaining why hold conditions no longer apply. If the user cannot pass required KYC re-verification, do not use informal workarounds. Apply the account-limitation or suspension path defined by policy.

Related reading: FDIC Pass-Through Insurance for Platform Wallets: How to Protect Your Contractor Funds.

Connect identity controls to tax and compliance records#

Closing an identity incident should include tax-record integrity, not just account-access recovery. Add a second verification step before any W-8, W-9, or 1099-related change so a suspicious edit does not create downstream reporting errors.

| Item | Threshold or rule | Article note |

|---|---|---|

| Form W-9 | TIN must match the name on the form | Unresolved name or TIN mismatches can lead to downstream errors and possible 24% backup withholding |

| W-8BEN | A change in circumstances requires a new form | The account holder must notify the payer or withholding side within 30 days |

| Form 1099-NEC | Before the next 1099 cycle, compare the recovered account's current tax profile with prior payouts and prior tax forms | Do not let identity-recovery edits silently change assumptions for reportable payments |

| FBAR | Applies to U.S. persons when aggregate foreign financial accounts exceed $10,000 at any point in the year | Escalate foreign-account disputes early and do not finalize tax records on assumptions |

| FEIE | One pathway includes 330 full days in 12 consecutive months | Eligibility also depends on foreign earned income and a foreign tax home |

Freeze tax-profile edits while identity risk is open#

If the incident includes credential resets, payout-destination changes, or disputed contact details, require manual review for tax-profile edits until the case is resolved. Use one reviewer test: can you link the requested tax change to verified account ownership from current records, not screenshots or copied ticket claims?

Prioritize Form W-9 and W-8BEN checks. A W-9 provides the TIN, and the TIN must match the name on the form to avoid backup withholding. Unresolved name or TIN mismatches can lead to downstream errors and possible 24% backup withholding.

Re-verify tax changes tied to suspicious identity activity#

Require fresh review for post-incident edits to legal name, entity type, TIN, country of tax residence, or treaty-related W-8BEN fields. For W-8BEN, a change in circumstances requires a new form, and the account holder must notify the payer or withholding side within 30 days.

Retain relevant records for the change, including prior and new submissions, reviewer notes, timestamps, and approval evidence. This supports internal defensibility and is consistent with IRS guidance to keep records supporting reported tax items until limitation periods expire, generally 3 years.

Reconcile tax outputs before the next reporting cycle#

Before the next 1099 cycle, compare the recovered account's current tax profile with prior payouts and prior tax forms. If you report nonemployee compensation on Form 1099-NEC, do not let identity-recovery edits silently change assumptions for reportable payments. Validate current-year filing logic and document any correction path.

Escalate cross-border and residency disputes early#

Escalate early when the incident touches country, foreign-account details, or tax residency. [FBAR](https://www.irs.gov/businesses/small-businesses-self-employed/report-of-foreign-bank-and-financial-accounts-fbar) applies to U.S. persons when aggregate foreign financial accounts exceed $10,000 at any point in the year, and FEIE eligibility depends on facts such as foreign earned income, a foreign tax home, and, under one pathway, 330 full days in 12 consecutive months.

If a user reports takeover-related changes to residency or foreign-account information, do not finalize tax records on assumptions. Keep the tax-profile dispute open, preserve the evidence pack, and route for specialist tax review with legal review as needed.

Avoid common implementation mistakes and recover fast#

Once access is restored, recover by tightening only what reduces risk fastest, not by adding friction everywhere. The mistakes below are common because teams either spread controls too broadly or depend too heavily on a single signal, tool, or log.

- Mistake: overbuilding controls across all workflows.

Recovery: Concentrate your strictest checks on the highest-impact steps in your process instead of applying the same burden to low-risk steps.

- Mistake: logging too little or too much sensitive data.

Recovery: Keep evidence complete but controlled. Retain what you need to reconstruct decisions, then enforce data minimization and least-privilege access so sensitive case material stays need-to-know only.

- Mistake: treating every alert as equal.

Recovery: Prioritize incidents by scope, likely impact, and time-criticality. Escalate faster when signals conflict across multiple log types, such as host, network, and authentication logs.

- Mistake: relying on one tool alone, including

Bitdefender Digital Identity Protection.

Recovery: Use monitoring tools as one input in a broader response process. Layered, diversified controls are more resilient than any single product.

Take the next 30 days from policy to proof#

Over the next 30 days, focus on proving three things: your policy changes payout decisions, your evidence is reconstructable, and your team can execute under pressure.

- Week 1: Lock ownership and publish the escalation matrix.

Assign named owners across Risk Ops, Compliance, Legal, and Payments Ops for hold, review, and release decisions, including external contacts when a provider is part of containment. Validate it on one recent payout-detail change: who approves a hold, who communicates with the provider, and who signs off on release.

- Week 2: Confirm market-specific gating before money moves.

Review KYC, internal legal-entity verification, AML, and payout gating by market, product, and customer type, and keep it risk-based. Do not label coverage as "global complete" if controls vary by country. For covered U.S. financial contexts serving legal entities, confirm whether beneficial ownership identification and verification applies to your flow.

- Week 3: Turn event visibility into usable detection.

Enable and test the signals you will investigate: Webhooks and Audit trail exports. Your checkpoint is whether you can reconstruct a clear sequence from access or profile changes to payout setup and release decisions.

- Week 4: Run one live tabletop and remediate gaps.

Run one simulation for an identity-theft scenario tied to payout risk, then update information sharing, response protocols, and recovery procedures based on what breaks. Include Idempotent retries for retryable write actions so repeated attempts do not create duplicate side effects during containment.

Copy/paste checklist

- Finalize the Escalation matrix with named owners, backups, and hold or release approval authority.

- Confirm KYC, internal legal-entity verification, AML, and payout gating rules by market.

- Enable and test Webhooks and Audit trail exports.

- Publish the Incident reporting checklist with evidence ownership.

- Define payout hold or release approvals and Idempotent retries behavior.

- Run one simulation of an identity-theft scenario plus payout risk and document corrective actions.

If one item slips, do not skip the simulation. Untested policy can fail at handoffs, not in policy text.

When you move from policy to rollout, use the implementation references in Docs to validate webhooks, retries, and audit-trail handling.

Frequently Asked Questions

What are the most common identity theft paths for freelancers in payout platforms?

A common path is phishing, spoofing, and impersonation that can lead to credential theft. FTC guidance notes scam messages are designed to steal passwords and account details, and stolen credentials can open access to email, bank, or other accounts. In the FBI’s 2024 reporting, phishing or spoofing was one of the top complaint categories, so treat account takeover plus payout-detail changes as a primary risk path.

What minimum controls should exist before any payout is released?

There is no universal checklist for every platform and jurisdiction, so use a risk-based baseline. A practical baseline is MFA for account access, a documented identity-theft prevention framework (including a written program where Red Flags obligations apply), and an auditable approval gate for payout destination setup or changes before release. If you cannot reconstruct who changed payout details, when, and who approved release, your control floor is still too low.

When should a platform pause payouts after identity-risk signals?

Pause payouts when identity-risk signals and money-movement risk appear together, not for every isolated alert. For example, a credential or access event followed by payout-detail changes can trigger containment review. Where transfers are hard to reverse after release, stop pending transfers while review is in progress.

How do we detect freelancer impersonation early without overwhelming operations?

Use combined signals and tiered escalation instead of treating each alert as equally urgent. Give higher priority to linked anomalies across profile changes, authentication events, and payout actions, and keep lower-risk, no-money-movement events in queue. If your logs do not show a clear event sequence, treat that gap itself as an escalation trigger.

What should an incident evidence pack include for compliance and audit review?

Include a clear timeline, affected accounts, actions taken, controls triggered, approvals, and final disposition, with the underlying log artifacts for each decision. Preserve the records needed for investigation and retention so the event history is reconstructable during review. If your entity has U.S. SAR obligations, structure evidence so filing can support the 30-calendar-day window after initial detection, and no later than 60 calendar days when identifying a suspect.

How do we balance tighter controls with onboarding and payout friction?

Apply friction at higher-risk money moments, not across every workflow. FTC Red Flags guidance supports a streamlined program where risk is low, with stricter controls where identity and payout risk are higher. If low-risk repeat payouts get heavy review while payout-detail changes clear too easily, your calibration is backwards.

Which metrics show the program is reducing identity risk instead of just creating more alerts?

Track outcomes first: faster detection, faster containment, and lower loss exposure from identity-linked payout incidents. Then track signal quality and operational load, such as how many alerts become confirmed cases and how often handling creates duplicate actions. Alert volume alone is not success; better containment and reduced impact are.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumer.ftc.gov/articles/how-recognize-avoid-phishing-scamstrusted

- eba.europa.eu/regulation-and-policy/anti-money-laundering-...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ftc.gov/business-guidance/resources/fighting-identit...trusted

- ftc.gov/business-guidance/privacy-security/red-flags...trusted

- ic3.gov/PSA/2024/PSA240911trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

When Virtual Account Numbers Protect Freelancer Bank Details

If your goal is to protect freelancer payout bank details, focus on the receiving bank detail, not card-masking tools. In practice, the question is whether to give payers a purpose-built receiving detail, often a virtual bank account number, instead of exposing the underlying account behind your payout setup.

How to Protect Trade Secrets When an Employee Leaves

If you want to protect trade secrets when someone leaves, start with a blunt rule. Information is protected only if it is nonpublic, valuable because it stays secret, and something you actually kept under control. General skill, public information, and experience honestly gained doing the work are often portable, subject to any confidentiality duties.

Disability Insurance for Freelancers Who Need Reliable Cashflow

When your work stops, revenue can drop fast. The real job is not finding the cheapest quote. It is building an income-continuity plan that still works when billable hours disappear.