Quick Answer

Form 1099-K for freelancers is best handled with a monthly compliance system, not one-time threshold guessing. Classify inflows by channel, reconcile gross receipts to your books, and map forms back to one ledger to prevent double counting. Use forms as checkpoints, report income from records even if no form arrives, and escalate cross-border or state edge cases early.

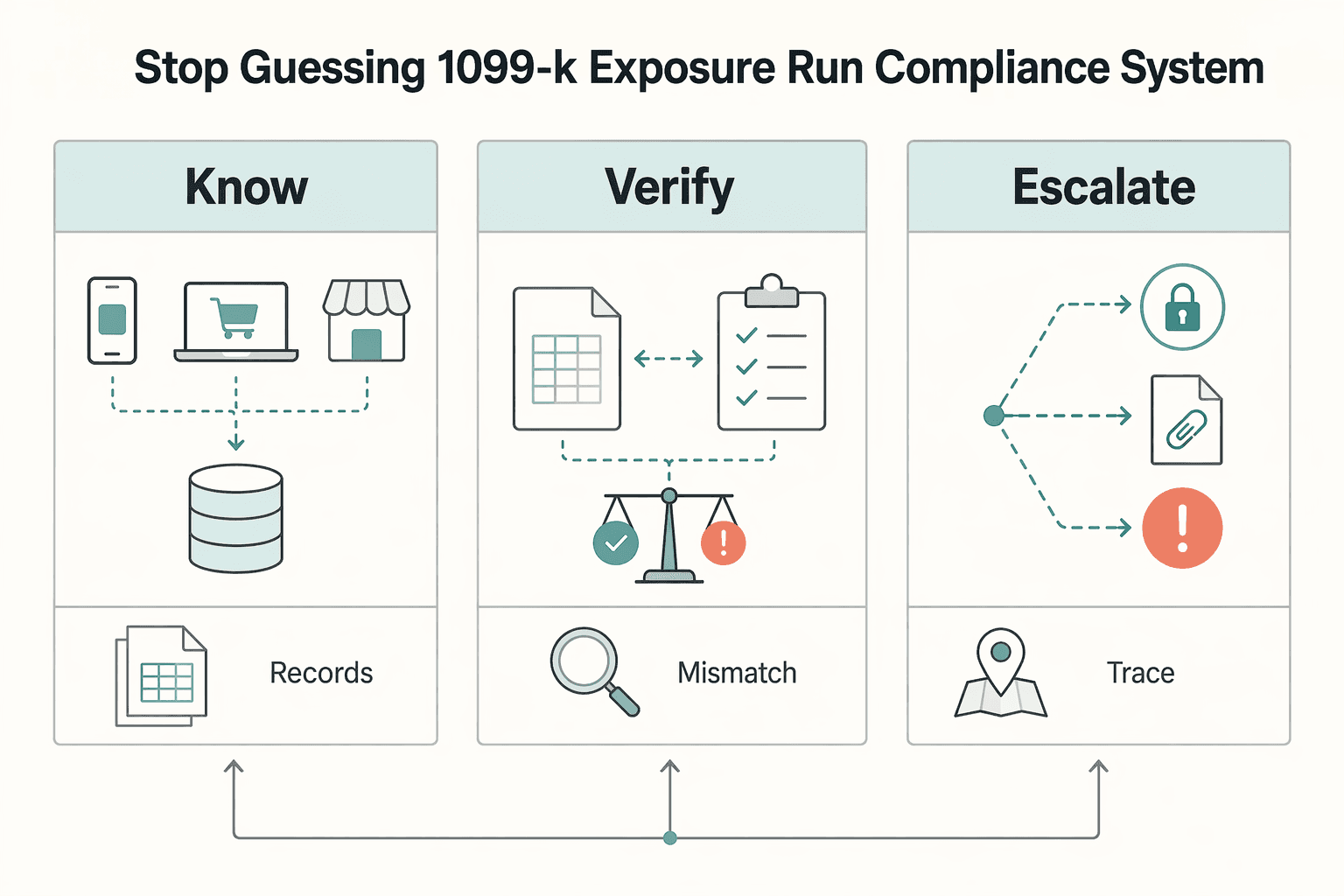

Stop Guessing Your 1099-K Exposure and Run a Compliance System#

Run a monthly Know/Verify/Escalate loop for Form 1099-K instead of guessing thresholds. That routine cuts avoidable tax risk and keeps your reporting process stable when guidance shifts. Payment apps and marketplaces can split your records across platforms, payout types, and reporting rules, which is where the stress starts. If you run a business of one, replace guesswork with a repeatable close process.

Form 1099-K is an IRS information return for payments you receive for goods or services through covered payment channels, including TPSOs such as payment apps and marketplaces. Those organizations send copies to both you and the IRS, and they must send your copy by January 31. IRS pages and instructions have shown different threshold language, so you cannot build your strategy around one static number. You need a system that stays correct even when guidance shifts.

Use this guide as a practical system for Form 1099-K workflows, especially if your payment stack includes mixed channels and work across jurisdictions.

| Framework step | What you do each month | Why it lowers risk |

|---|---|---|

| Know | Export platform summaries and classify inflows by channel and payer type. | You stop relying on memory and create a complete ledger trail. |

| Verify | Reconcile books to platform totals and form expectations, including 1099-K pathways. | You catch mismatches before filing pressure hits. |

| Escalate | Flag edge cases early when facts turn unclear, especially across jurisdictions. | You reserve expert time for high risk issues, not routine cleanup. |

Picture a normal month. One client pays through a payment app, another through an online marketplace, and you move between projects across jurisdictions. If those records stay siloed, your reporting turns into guesswork. If you run Know, Verify, Escalate, you keep control.

This is a practical playbook, not legal advice. Use safe defaults, then escalate when rules or facts get ambiguous. Core default: report income from your records whether or not you receive a form.

Start With Selection Criteria and Who This List Is For#

Choose the payment mix that creates the clearest reporting trail first, then optimize cost and speed.

| Priority | Action | Anchor fact |

|---|---|---|

| Minimize ambiguity first | Prefer channels that give clear statements and stable payer metadata. | Tie each channel to a likely form path and keep monthly exports organized. |

| Add convenience second | Keep extra channels only if you can reconcile them every month without unresolved exceptions. | You want predictable monthly reconciliation and defensible records. |

| Escalate cross-border triggers fast | Move from routine handling to expert review when facts point toward FBAR or broader FinCEN questions. | FBAR obligations can apply when a U.S. person's aggregate foreign account value exceeds $10,000 and reporting runs through FinCEN Form 114. |

Use this section to pressure-test whether your current setup lowers compliance noise or creates it. It is for freelancers and consultants who collect through payment apps, card processors, or marketplaces and want clean IRS workflows. You want predictable monthly reconciliation, defensible records, and clear boundaries between Form 1099-K and Form 1099-NEC logic.

This list is not for people chasing aggressive loopholes or full entity-structure strategy. It also does not replace legal advice for complex cross-border facts. Use it to run safer defaults, then escalate edge cases early.

| Selection criterion | What good looks like in practice | Fact to anchor your decision |

|---|---|---|

| Reporting clarity | You can tie each channel to a likely form path and keep monthly exports organized. | Payment card companies, payment apps, and online marketplaces issue Form 1099-K to the IRS, and recipient copies are expected by January 31. |

| Reconciliation effort | You can close monthly books without guessing what each payout represents. | Direct card processing can produce Form 1099-K regardless of transaction count or amount. |

| Audit defensibility | You keep a form-mapping log that explains why each inflow sits where it does. | Card and TPSO network payments belong on Form 1099-K, not separate Form 1099-NEC or 1099-MISC reporting. |

| Escalation clarity | You define exact triggers for specialist review instead of waiting for filing season stress. | FBAR obligations can apply when a U.S. person's aggregate foreign account value exceeds $10,000 and reporting runs through FinCEN Form 114. |

Use this decision lens as you choose and prune your payment channels:

- Minimize ambiguity first: prefer channels that give clear statements and stable payer metadata.

- Add convenience second: only keep extra channels if you can reconcile them every month without unresolved exceptions.

- Escalate cross-border triggers fast: if facts point toward FBAR or broader FinCEN questions, move from routine handling to expert review.

Hypothetical example: you invoice retainer clients through a card processor, accept occasional backup payments through a payment app, and keep one foreign account while traveling. This framework tells you what stays routine and what moves to escalation before questions pile up.

What Do We Actually Know Right Now About Form 1099-K?#

Form 1099-K is a channel-based IRS information return for payments for goods or services that flow through payment cards and TPSO channels.

Treat Form 1099-K as a reporting signal, not a taxability rule. Start with the stable ground: Form 1099-K reports payments for goods or services that flow through payment cards and TPSO channels, including many payment apps and marketplaces. Your process stays the same either way: reconcile gross receipts to your books, then use forms as checkpoints.

| What we know now | What still moves | Safe operator action |

|---|---|---|

| IRS guidance frames Form 1099-K as a channel-based information return for card and TPSO flows. | Form issuance can vary by platform and reporting context. | Keep a channel map and reconcile monthly by source, not by form count. |

| IRS FAQ language references a federal TPSO filing trigger over $20,000 and more than 200 transactions. | Recent years included $600 transition messaging, a $5,000 phase-in plan, and One Big, Beautiful Bill (OBBB) related updates. | Check current-year IRS updates before filing, every season. |

| Income stays taxable even when no Form 1099-K arrives. | A TPSO may still issue Form 1099-K below the federal threshold. | Report taxable income from records first, then match forms second. |

| IRS fact-sheet content shows recent updates, including October 2025 revisions. | State reporting thresholds may differ from federal thresholds. | Treat federal rules as one input and escalate state mismatches quickly. |

Run this Verify Now checklist before filing so you do not get surprised at the end:

- Confirm the latest IRS Form 1099-K FAQ and instructions for your filing year.

- Reconcile gross receipts across card, TPSO, and other payment channels in your records.

- Log exceptions where form amounts and ledger totals differ.

- Escalate when threshold language or state rules conflict.

Hypothetical: you collect through a card processor and a marketplace, then one platform sends a form and the other does not. You still close the month the same way. Record all income, match each inflow to source evidence, and escalate edge cases early.

Comparison Table Which Payment Path Triggers Which Form?#

Card and TPSO network payments most commonly signal Form 1099-K, while direct client payer reporting most commonly signals Form 1099-NEC.

Map each payment path to its likely form signal, then reconcile to full gross receipts so form volume never drives your tax logic. For freelancers, this is the practical split between card and TPSO reporting and direct payer reporting. Use it as an operating tool, not a filing shortcut.

| Payment path | Typical issuer | Most likely form signal | Primary risk | Control action |

|---|---|---|---|---|

| Direct card processing | Processor or PSE | Form 1099-K | Incomplete channel-level reconciliation | Reconcile processor totals to books monthly. Card flows can trigger 1099-K even at very low amounts. |

| Wallet or app intake through a payment app | App or TPSO | Form 1099-K | Personal and business flow contamination | Keep a business-only profile, export statements monthly, and log exceptions. TPSO channels can issue below the federal threshold. |

| Marketplace intake through an online marketplace | Marketplace or TPSO | Form 1099-K (plus other reporting docs) | Misreading platform adjustments as missing income | Track gross receipts separately from platform fees and adjustments. |

| Direct client payer reporting | Client or business payer | Form 1099-NEC (often when service payments reach at least $600) | Double counting when you also receive 1099-Ks elsewhere | Tie each payer form to ledger entries and channel tags, then reconcile totals once. |

Two rules keep this table honest, and they explain most "why do I have two forms?" confusion:

- Card and third-party network payments belong on Form 1099-K, not Form 1099-NEC.

- One freelancer can receive multiple 1099-Ks across platforms, plus a separate 1099-NEC from direct clients.

That mix is normal, and your process should handle it cleanly.

Hypothetical: you take retainers through a card processor, pick up overflow work paid through a payment app, and one enterprise client pays direct and issues 1099-NEC. You map payer to channel, reconcile monthly, and keep exception notes for any mismatch.

Best Payment Setups for Freelancers Who Want Lower 1099 Risk#

The best payment setup is the one that creates the clearest monthly audit trail and stays easy to reconcile.

| Setup | Best fit | Key difference | Main tradeoff |

|---|---|---|---|

| Direct processor stack with strict bookkeeping discipline | Consulting retainers through a direct card processor and monthly closes. | Direct card acceptance can generate Form 1099-K regardless of payment count. | Cleanup gets messy if you skip exception logs for refunds, fees, and timing differences. |

| App based collections with business only account boundaries | Clients prefer app-based payments. | Payment apps and online marketplaces are TPSOs, and the IRS baseline condition references over $20,000 in more than 200 transactions. | If you mix personal and business transfers, cleanup turns into manual reclassification work. |

| Marketplace heavy model with platform reconciliation controls | Most revenue flows through marketplace platforms. | Some gig platforms can issue both Form 1099-K and Form 1099-NEC, and 1099-K totals can reflect gross customer payments, not net deposits. | If you fail to split gross receipts from platform adjustments, you inflate confusion during filing. |

| Hybrid channel model with formal form mapping policy | You combine enterprise direct clients with app or marketplace demand. | One freelancer can receive multiple 1099-Ks across platforms, and issuers must send recipient copies by January 31. | This model creates the highest reconciliation load, so you must keep a channel map and records long enough to prove reported income and deductions. |

You already mapped which channels trigger which forms. Now choose the operating model that keeps reconciliation clean as volume grows. The right setup depends on control quality, not platform hype.

- Direct processor stack with strict bookkeeping discipline. Choose this if you run consulting retainers through a direct card processor and close books every month. Key differentiator: direct card acceptance can generate Form 1099-K regardless of payment count, so form behavior stays predictable. Tradeoff: cleanup gets messy if you skip exception logs for refunds, fees, and timing differences.

- App based collections with business only account boundaries. Choose this if your clients prefer app-based payments. Key differentiator: payment apps and online marketplaces are TPSOs, and the IRS baseline condition references over $20,000 in more than 200 transactions. Tradeoff: if you mix personal and business transfers, cleanup turns into manual reclassification work, so mark non-business payments correctly when possible.

- Marketplace heavy model with platform reconciliation controls. Choose this if most revenue flows through marketplace platforms. Key differentiator: some gig platforms can issue both Form 1099-K and Form 1099-NEC, and 1099-K totals can reflect gross customer payments, not net deposits. Tradeoff: if you fail to split gross receipts from platform adjustments, you inflate confusion during filing.

- Hybrid channel model with formal form mapping policy. Choose this if you combine enterprise direct clients with app or marketplace demand. Key differentiator: one freelancer can receive multiple 1099-Ks across platforms, and issuers must send recipient copies by January 31. Tradeoff: this model creates the highest reconciliation load, so you must keep a channel map and records long enough to prove reported income and deductions.

Hypothetical: you keep recurring client invoices in Stripe, accept backup payments in a payment app, and pick up occasional marketplace work. Run the hybrid model only if you commit to monthly mapping and exception notes. If you cannot sustain that cadence, simplify first and expand later.

If you want a deeper dive, read The Best Bank Accounts for Freelancers in the UK.

Want a quick next step? Try the W-2 vs 1099 calculator.

How Do You Prevent 1099-K and 1099-NEC Double Counting?#

Prevent double counting by reconciling income to one ledger first, then mapping every form line back to that ledger.

You picked a payment setup. Now put guardrails around overlapping forms so totals do not drift. Run these controls in sequence throughout the year and again at filing time.

| Control | What you do | Key differentiator |

|---|---|---|

| 1. Channel to payer map | Tag each inflow by source (card, TPSO app, marketplace, direct client) and expected form path. | Card and third-party network transactions sit on Form 1099-K, not Form 1099-NEC. |

| 2. Gross first reconciliation | Reconcile gross receipts in your books before you touch form totals. | Form 1099-K reports gross payments only, so use your records to determine reportable amounts. |

| 3. Exception log | Track missing payer IDs, merged payouts, and unclear labels from processors and apps. | A payment on 1099-K is not automatically taxable, and a payment missing from 1099-K is not automatically non-taxable. |

| 4. Escalation trigger | Escalate repeated unresolved mismatches, unclear marketplace adjustments, or issuer-level errors. | Contact the form filer for questions or errors and keep written notes for every follow-up. |

Then apply one hard rule: never add Form 1099-K and Form 1099-NEC totals as separate income buckets. Map each form line back to existing revenue entries, then confirm total taxable income once.

Around January 31, when Form 1099-NEC is due to be filed, verify which client-issued 1099-NEC documents you expected and log missing ones immediately. Fast logging prevents last-minute guesswork.

Hypothetical: you collect retainer payments through Stripe, receive occasional app payments, and invoice one enterprise client directly. Later, you receive two different forms for the same operating period. You avoid duplicate income by reconciling gross receipts first, then using forms only as cross-checks.

Run the 10 Minute Know Verify Escalate Checklist Each Month#

Run a fixed 10 minute Know, Verify, Escalate loop each month to keep Form 1099-K handling accurate and surface higher risk compliance issues early.

Use this loop to catch missed income paths and double counting before they snowball. Apply the same five checks each month across platforms, clients, and foreign accounts. Consistency, not complexity, lowers audit friction.

| Checklist item | What you do in practice | Key differentiator |

|---|---|---|

| Know | Export monthly summaries from payment apps, card processors, and marketplaces. Classify each inflow as TPSO or card platform or direct payer before you lock categories. | One freelancer can receive more than one Form 1099-K across platforms, so channel classification prevents false surprises at year end. |

| Verify | Reconcile books to expected form paths. Map TPSO and card flows to Form 1099-K, and map direct payer income to non-1099-K records before close. Clear every orphan income line before close. | You must report income whether or not a form arrives, so this step protects you from both missing forms and duplicate form logic. |

| Escalate | Trigger advisor review when facts touch foreign account reporting. Check separate thresholds for FBAR and Form 8938, then decide whether one or both filings apply. | FBAR can trigger when aggregate foreign account value exceeds $10,000 at any time, and Form 8938 never replaces FBAR. File FBAR through FinCEN's BSA E-Filing System. |

| State guardrail | If California ties remain, open a state review task during monthly close and confirm residency impact. | California can tax residents on income from all sources, so state exposure can stay live even when your work and travel cross borders. |

| Retention | Store exports, reconciliation notes, and form mapping logs in one audit ready folder by month. Use fixed filenames and owner initials so any reviewer can trace each decision fast. | Keep FBAR records for 5 years from the due date. Put April 15 and the automatic October 15 extension date in your compliance calendar. |

Hypothetical: you collect consulting revenue through card and platform payments, pick up side projects through payment apps, and hold an overseas account while traveling. This checklist tells you what to close today and what to escalate now, before deadlines compress your options.

If state ties look unclear, run a focused review. Start here: Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Build a Reporting System That Survives Rule Changes#

Use one monthly reporting workflow, then date-check IRS threshold guidance before filing, so rule changes do not break your compliance process.

| Step | What to do | Anchor fact |

|---|---|---|

| Lock payment-channel classification first | Tag each payment stream as payment card, TPSO flow, or direct payer when it enters your system. | For payment cards, there is no de minimis reporting threshold for Form 1099-K, including very small amounts. |

| Reconcile gross first, then map forms | Treat Box 1a gross payment amount as a reconciliation input and match form totals to your transaction records before filing. | Where 1099-K reporting applies, avoid duplicating the same transaction on 1099-NEC or 1099-MISC. |

| Verify thresholds using filing-year context | Date-check IRS updates before you finalize assumptions. | Current IRS FAQ language describes the federal TPSO test as more than $20,000 and more than 200 transactions, while older instruction pages may still show $600 language. |

| Keep an audit-ready proof stack | Save monthly exports, reconciliation notes, and exception decisions in one consistent folder structure. | A TPSO may issue Form 1099-K below federal thresholds, and some states may use lower thresholds. |

Build your process around records and reconciliation, not form arrival. Form 1099-K is an information return, and your books remain the system of record. That keeps you steady even when threshold language changes across IRS pages and updates.

- 1) Lock payment-channel classification first. Tag each payment stream as payment card, TPSO flow, or direct payer when it enters your system, not at year-end. Keep that classification consistent month to month. For payment cards, there is no de minimis reporting threshold for Form 1099-K, including very small amounts.

- 2) Reconcile gross first, then map forms to ledger entries. Treat Box 1a gross payment amount as a reconciliation input, not taxable profit. Match form totals to your transaction records and resolve differences before filing. Where 1099-K reporting applies, avoid duplicating the same transaction on 1099-NEC or 1099-MISC.

- 3) Verify thresholds using filing-year context. Date-check IRS updates before you finalize assumptions. Current IRS FAQ language describes the federal TPSO test as more than $20,000 and more than 200 transactions, while older instruction pages may still show $600 language. Use the latest dated IRS update for your filing-year decisions.

- 4) Keep an audit-ready proof stack. Save monthly exports, reconciliation notes, and exception decisions in one consistent folder structure. Keep records long enough to substantiate income and deductions, because the burden of proof is on you. Also plan for exceptions: a TPSO may issue Form 1099-K below federal thresholds, and some states may use lower thresholds.

Use this as your standing monthly close so edge cases are escalated early and decisions stay traceable. For a tighter documentation workflow, use How to Prepare for an IRS Audit.

Frequently Asked Questions

What is Form 1099-K for freelancers using payment apps?

Form 1099-K is an IRS information return that reports payments you received for goods or services through card transactions or a payment settlement entity, including a third party settlement organization (TPSO). Treat it as a reconciliation document, not a profit statement. Your books are the system of record. The form is a checkpoint against that system.

Do I still owe taxes if I don’t receive Form 1099-K?

Yes. You must report taxable income even if no Form 1099-K arrives. Taxability does not depend on form delivery. Close your books from your own records, then use forms to confirm coverage and catch mismatches.

Who sends Form 1099-K to me, the client or the payment platform?

Payment card companies, payment apps, and online marketplaces send Form 1099-K. For card and third party network payments, reporting is handled on Form 1099-K by the payment platform, not your direct client. You should receive your copy by January 31.

What is the difference between Form 1099-K and Form 1099-NEC for freelance income?

Form 1099-K covers card and third party network payments processed by a payment settlement entity. Form 1099-NEC reports nonemployee compensation from a payer. The main operational risk is overlap. You avoid it by mapping each transaction to one ledger entry and using each form only as supporting evidence.

If I take direct card payments, does a threshold still matter?

For payment card transactions, no minimum dollar threshold applies to Form 1099-K reporting. Even $0.01 in reportable payment card volume can trigger a 1099-K. Build your process around monthly reconciliation, not threshold assumptions.

What changed in recent 1099-K reporting rules and what should I verify before filing?

Recent IRS FAQs state that OBBB reinstated the prior TPSO federal threshold framework. The current IRS FAQ update says TPSOs report when gross payments exceed $20,000 and transactions are more than 200 for a payee. Verify the latest IRS release before filing, because rule updates and state rules do not always move together.

How should globally mobile freelancers keep records to stay audit-ready year-round?

Keep one monthly close packet with platform exports, ledger reconciliation, payer mapping notes, and any exception log entries. Save separate support for payment apps and direct payer flows so you can explain each line quickly. By January 31, confirm expected forms arrived and document any missing forms immediately.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Prepare for an IRS Audit

Treat an IRS audit as a records check, not a contest. Your job is to show, item by item, how what you filed ties back to the records behind it.

The Best Bank Accounts for Freelancers in the UK

Confirm with each provider directly, as UK bank product details and eligibility requirements can change. Always verify the current terms on official provider pages before applying.