Quick Answer

Handle a German Scheinselbstständigkeit audit by proving how you actually work day to day, not by relying on contract labels. Build a consistent evidence pack across contracts, invoices, delivery records, and communications, confirm the exact scope of any inquiry, and keep replies factual. If the relationship looks employee-like in practice, remediate the working model or plan a transition instead of defending weak facts.

You can handle a German Scheinselbstständigkeit audit without losing control#

Protect your status by proving day-to-day independence, not by leaning on contract labels. In Germany, authorities look at the real working relationship, and private agreements do not override German labor law.

Step 1 Anchor your defense in daily reality#

Treat this as a facts exercise. Scheinselbstständigkeit means someone is labeled a contractor but handled like an employee in practice. Genuine self-employment means you control how and when the work gets done.

Start with a quick self-check: in recent work, who decided the method, schedule, and tools? If that was mostly the client, you likely have a status risk to address.

Step 2 Define scope before you change anything#

This guide focuses on freelancer-side actions in Germany when false self-employment risk appears. If your engagement can be assessed under German labor law, the core question stays the same: does the relationship look like independent business activity or dependent employment? Contract wording alone does not settle that if daily practice points the other way.

Step 3 Accept that there is no magic checklist#

There is no single factor that guarantees an outcome. The assessment is holistic, so no one clause or metric can carry your case on its own.

Use warning signs as signals, not legal thresholds. If one client provides 80% or more of your revenue, or the relationship runs more than a year, treat that as increased risk and review the full fact pattern.

Step 4 Make your records tell one consistent story#

Your position needs to line up across contract terms, delivery behavior, invoices, and communication history. If your paperwork says "independent," but the working pattern shows company tools, an internal email address, and presentation as part of the client's team, the file can read as dependent employment.

Run a practical check on one client now: compare the signed agreement, recent invoices, recent messages, and delivery records. If they show independence and entrepreneurial risk, your defense is stronger. If they show integration and dependence, fix the operating reality first. Reclassification can trigger social security contributions, tax liabilities, fines, employee-rights claims, and retroactive social security exposure for up to four years.

For a related tax angle, see Can Digital Nomads Claim the Home Office Deduction?.

Know what authorities test before they read your contract#

Start with the facts, not the labels. In a German Scheinselbstständigkeit audit, authorities assess whether your setup looks like dependent employment or a genuinely independent contractor relationship under German status rules.

Step 1 Identify the real status test#

Start with daily practice. False self-employment is a contractor label paired with employee-style control, while genuine self-employment means you decide how and when the work is done.

This is an overall relationship test, not a one-factor test. No single clause secures your position, and no single datapoint decides it alone.

Step 2 Recognize who can trigger scrutiny#

In practice, status reviews can be triggered by bodies such as the German Pension Insurance Association, labor courts, and social insurance actors. They focus first on verifiable working facts.

Build your explanation around evidence: who sets your schedule, tools, and working method. If your records show internal email access, company-equipment dependence, or employee-style integration, that weakens your case.

Step 3 Check the red flags authorities notice fast#

Some patterns draw attention quickly because they look employee-like in practice:

- specific instructions on how to perform tasks

- fixed working hours or a fixed daily schedule

- integration into the client team

- use of company equipment or an internal email address

- working exclusively for one client in Germany

Contract wording helps, but conduct usually carries more weight. If your agreement says "independent contractor" while the client controls your hours, tools, and methods, treat that as active risk and fix the operating pattern first.

For a step-by-step walkthrough, see A US Software Developer's Guide to Germany's 'Scheinselbstständigkeit' (False Self-Employment) Laws.

Build your audit evidence pack before anyone asks#

Build one evidence pack now so you can explain the working facts quickly if questions come up later. Treat this as a practical internal record, not an official Germany-issued checklist or a guaranteed audit outcome.

Step 1 Create one client-month file#

Use one repeatable structure for every client and every month so records are easy to export and review. This is an internal filing method, not a mandated format:

| File section | Keep in it |

|---|---|

| 01 Contract | signed agreement, scope, amendments |

| 02 Scope changes | change requests, approvals, revised deliverables |

| 03 Invoices and payment | invoice, payment proof, late-payment follow-up |

| 04 Delivery record | milestone submissions, acceptance messages, key work communications |

| 05 Status and tax notes | cross-border social security/tax records, adviser notes, certificate workflow items |

Checkpoint: for any client-month, a third party should be able to see what was agreed, what changed, what was delivered, and how billing happened.

Step 2 Save business-operation evidence, not just polished documents#

Save the records that show how you actually operated: pricing decisions, method choices, tools you used, and your business expense trail. If relevant, keep light proof of multi-client activity, such as overlapping proposals or invoices. If you had a single-client period, keep context notes rather than leaving a silent gap.

These records help explain operations, but they do not by themselves determine legal status.

Step 3 Keep cross-border social security records in a separate lane#

For U.S.-connected work, keep Certificate of Coverage records together and separate from delivery files. Under totalization agreements, the goal is to prevent dual social security taxation on earnings. The certificate is used as proof that the employee and employer are exempt from foreign social security taxes when coverage is assigned to the United States.

Employers and self-employed individuals can request certificates online. Keep the request trail complete: submission details, confirmation details, evidence that required fields were completed, and the control number for status lookup. Required fields must be complete for submission. Missing information may prevent an accurate and timely decision. Track timing in your index: allow 90 business days before follow-up, and once issued, mailing can take up to two weeks. Keep local copies of what you submitted, since web submission carries interception risk.

Step 4 Add a short client narrative (optional)#

Add a short internal memo for each client that matches the file: services delivered, who set outcomes, who chose the method, tools used, and how the role operated in practice. Keep it factual and link each statement to records in the folder.

If you run contingency analysis for possible tax or social security contribution exposure, store it separately in the tax and status lane and label it clearly as analysis. We covered the broader recordkeeping side in How to Handle a Tax Audit When Your Income is Paid Through Deel or Remote.

Triage the first 72 hours after an inquiry arrives#

Your first move is to stabilize the record, not to argue. Early on, focus on preserving facts and avoiding new behavior that could make the setup look more dependent than it is.

Step 1 Freeze optional changes that increase integration#

Pause non-essential process changes while you verify facts. Keep delivering the agreed work, but avoid new routines that reduce your entrepreneurial freedom or increase integration into the client's organization. Those are common false self-employment risk signals.

Step 2 Confirm the exact request before sending documents#

Confirm what was requested and respond to that scope directly. If the scope is unclear, ask for clarification before sending additional materials.

Step 3 Keep one clear internal response record#

Keep a single internal record of key requests, what you sent, and when. Save the exact versions you sent so someone else can reconstruct the sequence quickly if needed.

Step 4 Keep replies factual and consistent#

Use observable facts: what was agreed, what was delivered, how invoicing worked, and how the work was carried out in practice. Avoid speculative or casual phrasing, and say plainly when a point is still being verified.

Score each client relationship before you respond#

Score first, then respond. You need an internal, evidence-backed view of whether each client relationship still looks independent or already reads like dependent employment.

Step 1 Build an internal risk table for each client#

Use a low, medium, high table as an internal tool, not an official German matrix.

| Risk factor | Low | Medium | High |

|---|---|---|---|

| Instruction control | You choose method and execution | Client sets priorities, you choose delivery approach | Client directs day-to-day tasks like a manager |

| Schedule control | You control your hours and delivery rhythm | Some recurring coordination windows | Client determines your working hours or expects employee-like availability |

| Org integration | Clear external-vendor posture | Frequent collaboration with internal teams | You are embedded in internal routines, for example through company email access |

| Tool ownership | Mostly your own tools/environment | Mixed tools for project reasons | Mostly client tools/environment, which can increase day-to-day control or integration |

| Client concentration | Revenue spread across clients | One dominant client for a period | More than 83.3% of income from one client, especially longer than a year |

Two guardrails still matter. Treat tool ownership as a practical signal, not a standalone legal decider. Treat the 83.3% and one-year markers as practitioner indicators, not universal legal thresholds. Add one evidence note for every rating so the table reflects facts, not assumptions.

Step 2 Escalate risk clusters early#

A cluster of high-risk signals calls for action, not better wording. If multiple high-risk factors sit together, treat dependent-employment risk as material and move into remediation.

If instruction control, schedule control, and org integration are all high, your risk posture has changed. If client concentration is also high, the exposure is more serious. That does not make reclassification automatic, but it can make an independent-contractor position harder to defend.

Also assume enforcement can be substantive, not just procedural. Authorities have increased focus on alleged false self-employment across industries. In the cited period, Finanzkontrolle Schwarzarbeit audited 42,631 employers and initiated 101,423 criminal proceedings plus 48,812 administrative offense proceedings.

Step 3 Adjust for operating form without overrating it#

Operating form can affect legal posture, but it does not override employee-like facts in practice.

The Bundessozialgericht checkpoint from 20 July 2023 (B 12 BA 1/23) is a useful reminder. Social-security obligations are not automatically avoided just because the contract is with a single-member corporation. Score working reality first and the legal wrapper second.

Step 4 Choose defense or transition based on facts#

Make a clear call for each client: defend, remediate, or transition.

If the record supports independent work, respond with evidence and fix medium-risk patterns. If the relationship reads like employee management, prepare a transition path instead of defending a weak independent-contractor position. The goal is a defensible outcome, not better wording around weak facts.

Turn your high-risk scores into clearer scope, control, and autonomy language with the Freelance Contract Generator.

Fix the red flags in day-to-day delivery#

If risk is already visible, change the working pattern now. In Germany, status is judged by practical day-to-day reality, so your delivery model needs to look like independent service work, not employee-style management.

Step 1 Rewrite the engagement around outputs#

Move from task control to defined results. Your scope should state deliverables, target dates, acceptance criteria, and how scope changes are handled. If the client is directing daily tasks, reprioritizing your week, or approving each step like a manager, the relationship is drifting toward employee-like control.

Keep invoices detailed and tied to outputs or clearly defined services before payment. That helps show a contractor relationship in practice.

Step 2 Strip out integration signals#

Operate like an external supplier, not part of the client hierarchy. Where practical, reduce employee-style titles, manager-like approval chains, and team positioning that makes you look like internal staff.

Collaboration is fine, but direction and accountability should stay vendor-to-client, not manager-to-employee. Check your access, role labels, and meeting load against what an outside provider would normally need.

Step 3 Keep control of tools, hours, and method#

Keep control where you reasonably can. Use your own equipment and tools wherever practical, since that is a recognized independence indicator. Client systems can be necessary for delivery, but your default setup should still reflect your own business operations.

Use the same logic for time and method. Coordination windows are normal. Client-controlled working hours and employee-like availability are higher-risk signals. When that pattern appears, renegotiate around deadlines, deliverables, and response expectations.

Step 4 Review for drift on a regular internal cadence#

Status risk can increase through gradual drift. Run a recurring internal review for each client and focus on:

- scope and scope changes

- whether invoices still map to outputs

- tool and access usage

- calendar control and who sets working patterns

- client concentration and whether you still work across multiple clients

If several items drift toward employee-style control, remediate quickly or plan a transition. That is how you manage Scheinselbstständigkeit risk in practice.

This pairs well with our guide on How to Handle Termination of an International Contractor.

Tighten contract terms that support independence in real audits#

Once daily delivery is fixed, make sure the contract tells the same independent-service story. In Germany, contractual form is reviewed alongside operational reality, so mismatched wording can weaken your position in a Scheinselbstständigkeit review.

Step 1 Write termination around the engagement, not employment#

Keep termination language consistent with a service engagement, and make sure day-to-day offboarding practice matches that framing. Contract labels alone are not enough if operational reality points the other way.

Step 2 Set liability and indemnity like a vendor, not staff#

Treat liability and indemnity as part of overall status consistency, not as standalone proof of independence. If the contract describes an external provider but the working model looks like employment, misclassification risk can still remain.

Step 3 Choose governing law and jurisdiction deliberately#

For cross-border deals, choose governing law and jurisdiction intentionally, but do not rely on those clauses alone as a status defense. If the contract and operating facts point toward German false self-employment risk, those facts still matter.

This is especially important if you contract through a one-person company. A Federal Social Court ruling from 20 July 2023 (B 12 BA 1/23) clarified that social-security obligations are not automatically avoided just because the contract uses a single-member corporation.

Step 4 Define dispute mechanics before narratives diverge#

Assume the engagement may be reviewed, and keep contractual and operational records aligned from the start. German authorities have run nationwide misclassification operations, and Finanzkontrolle Schwarzarbeit has reported large audit and proceeding volumes. If Hauptzollamt or prosecutors review the relationship, consistency across documents matters.

Need the full breakdown? Read How to Conduct a Personal Security Audit as a Freelancer.

Decide when to stay freelance and when to move to EOR#

Use a simple checkpoint for internal decision-making. The sources here do not set a Germany-specific legal test for when someone must move to employment or EOR, so treat this as an operating framework and validate with local counsel.

Step 1 Score the reality after remediation#

Re-check whether daily work still matches the freelance model you intend to run, both in practice and in the documents.

If persistent mismatch remains after remediation, treat that as an escalation point for legal/tax review and a possible model change. The core question is whether both sides can clearly explain and document how work is assigned, reviewed, invoiced, and run.

Step 2 Choose the path that matches the facts#

| Path | Choose it when | Verify now | Main tradeoff |

|---|---|---|---|

| Remain freelance | Autonomy is still real in practice | Operational record and contract still align with independent services | Fastest to keep, but requires ongoing discipline to maintain |

| Local employment | The work is being managed like staff and local hiring is practical | Employment transition owner, start date, and contractor offboarding steps | More admin now, fewer handoffs after transition |

| EOR | Employment is needed, but direct local hiring is not practical yet | Legal employer, management split, payroll/tax handling, and transition date | Added vendor cost and another operating handoff |

The tradeoff is short-term speed versus long-term operating certainty.

Step 3 Check cross-border social security separately#

For U.S.-Germany cross-border setups, keep social-security coverage mechanics separate from employment-status classification. The U.S.-Germany Social Security agreement is listed as in force from December 1, 1979. Totalization agreements are meant to assign coverage to one country to avoid dual social-security taxation.

If coverage is assigned to the United States, SSA can issue a Certificate of Coverage as proof of exemption in the other country. Employers or self-employed individuals can request it online. Keep the Control Number and track status as Received, Pending, or Completed. Required fields must be complete to submit, and missing information can prevent an accurate and timely decision. SSA asks requesters to allow 90 business days before follow-up, and issued certificates may take up to two weeks to mail.

A Certificate of Coverage helps on coverage allocation. It does not determine German employment-status classification.

Step 4 Frame the client conversation as risk reduction#

Frame the change as risk reduction, not blame.

- "We tightened contract and delivery controls, but the current management pattern still looks closer to employment than external services."

- "To reduce mismatch risk around status and social-security handling, we should either restore real contractor autonomy or move to employment."

- "If direct local hiring is not practical right now, an EOR can be one transition option."

Leave the conversation with one written decision, one owner, and one transition date. If you want a deeper dive, read Germany Freelance Visa: A Step-by-Step Application Guide.

Align with the client before officials compare both stories#

Before anyone responds externally, make sure you and the client are describing the same relationship. Conflicting explanations raise risk because German authorities assess the full working reality, not contract text alone.

Run one pre-response fact check. Have a short sync with the people who shape or explain the relationship day to day. Confirm the practical facts: what you deliver, who decides how the work is done, whether you control your schedule, how work is organized, and whether you remain free to serve other clients.

If you and the client cannot describe the setup the same way in plain language, pause and fix that first. A simple red flag is one side saying "external service provider" while the other describes the role like internal staff.

Reconcile the records people may read. Review your contract and day-to-day records as one story. You are looking for contradictions between what the contract says and how the work actually runs.

Watch for drift. A contractor arrangement can start independent, then become employee-like over time through deeper integration and tighter control.

Freeze risky language and track every fix. Set one rule with the client: do not use ad hoc wording in email, chat, or tickets that labels you as staff without review.

Keep one shared issue list with owner, deadline, and completion evidence for each fix. If the setup is later reviewed by the German Pension Insurance Association, a labor court, or a social insurance body, consistent facts from both sides are easier to explain than conflicting accounts.

Prepare for reclassification outcomes and recovery options#

Treat this as a multi-track recovery problem, not one broad "audit risk" issue. A status finding, payment exposure, and a client dispute can move in parallel, so your plan should separate them from the start.

Map outcomes by track before you defend facts. Build a one-page matrix for each client relationship with three tracks: status risk, payment risk, and dispute risk. Use payment risk for potential social security contributions and other tax exposure, and dispute risk for conflict with the client.

Do not assume one fix closes all tracks. A contract argument may not resolve payment exposure, and a payment cleanup may not resolve the private dispute.

Check cross-border social security relief separately. If the relationship touches the U.S. and Germany, evaluate social security coordination separately from employment-status classification. The U.S.-Germany Social Security agreement has been in force since December 1, 1979, and totalization rules can assign coverage to one country to prevent dual social security taxation.

When U.S. coverage applies, SSA can issue a U.S. Certificate of Coverage as proof of exemption from foreign social security taxes. Use it for social security coverage documentation only, not as proof of independent-contractor status in a Scheinselbstständigkeit review.

For Germany-specific reclassification penalties and court outcomes, details remain unresolved — confirm them with qualified legal counsel before making commitments.

Keep administrative exposure separate from more serious allegations. Different files can carry different risk levels depending on record quality and consistency.

Set a clear rule: correct design and documentation issues quickly, and involve legal counsel early when facts could be read as intentional. Do not alter old records or create backfilled evidence.

Sequence recovery actions in order. Start with legal review, then set settlement posture, then reset the client arrangement, then add repeat controls.

If independent work is still the real model, align scope, operating boundaries, and day-to-day behavior with that model. If the setup is effectively employee-like, move to a compliant structure instead of defending a weak classification.

Close with controls you can prove: dated correction logs, preserved document history, and periodic checks for drift. Recurrence in the same client relationship can be a warning sign for the next review.

Related reading: How to Prepare for an IRS Audit.

Mistakes that make audits harder than they need to be#

The fastest way to lose control is to defend contract labels when the daily setup looks employee-like. In Germany, status turns on practical autonomy and material reality, not wording alone.

Step 1 Treat status as a behavior test, not a paperwork exercise#

Start with how the work actually runs: who decides how, where, and when the work is done. If the client sets fixed hours, dictates day-to-day execution, or requires company-owned equipment, your facts are pointing away from independent work.

Use a simple checkpoint: review one recent month of calendar entries, chat threads, ticket assignments, and access logs. Those records can show the real control pattern faster than the services agreement.

Step 2 Build one complete, consistent record set#

Do not rely on a polished master contract and invoices alone if scope changes, project emails, acceptance notes, and delivery evidence tell the real story. Organize records by client and period, then cross-check dates, role descriptions, and signatures before you respond.

Missing or inconsistent records can weaken your position.

Step 3 Stop defending facts that clearly point to employment#

If the relationship is managed like employment, either fix the operating model or move to a compliant structure. Pushing weak facts can raise risk beyond an administrative review, including scrutiny tied to social security fraud allegations and Section 266a of the German Criminal Code.

Take escalation signals seriously: a backdated German Pension Insurance assessment, a prosecutor letter, or a customs dawn raid. At that point, stop improvising and get legal counsel.

Step 4 Clean up cross-border contract conflicts early#

Cross-border files can contain mismatched Governing Law and Jurisdiction language across the MSA, SOW, and purchase order. Those clauses do not override material reality in status analysis, but inconsistencies can weaken your overall file when documents and operations point in different directions.

Check that active documents describe the same service model, dispute path, and place of performance. If the work reality is in Germany, align the paperwork before a dispute forces the issue.

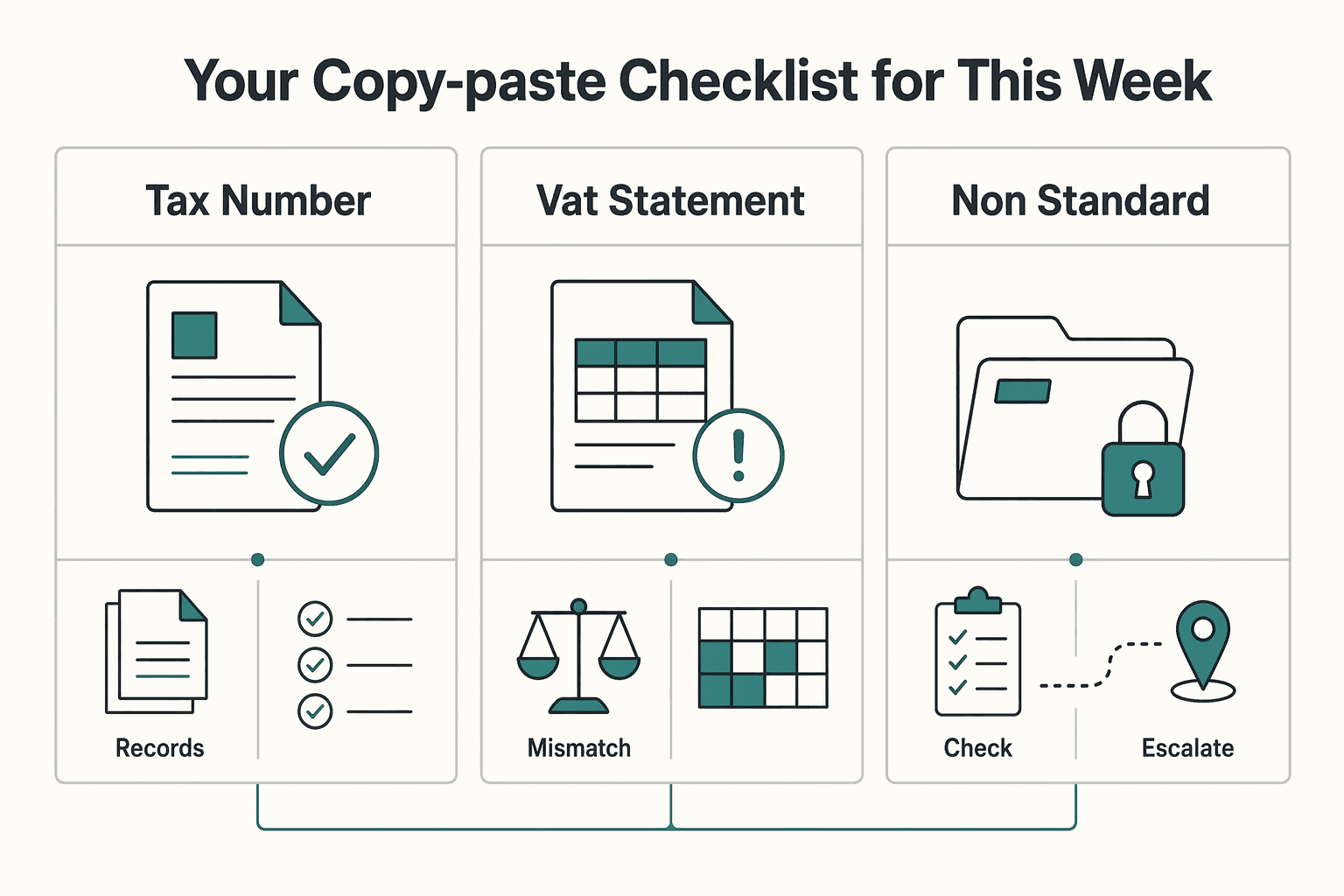

Your copy-paste checklist for this week#

If one client setup already looks employee-like in practice, treat this as a facts-and-records problem first. This week, focus on consistency across your contract, delivery behavior, and invoices, then decide early whether the current setup is still workable.

Step 1. Review every active client with the same risk table you already use, and mark each one low, medium, or high with one plain-language reason. Keep the focus on real working patterns, not labels.

Treat this as practical screening, not a definitive legal test.

Use a simple decision rule: if high-risk signals cluster for one client, escalate that file now instead of waiting for a formal inquiry.

Step 2. Build one evidence pack per client, per month, and make sure the story is consistent across documents.

At minimum, keep these items easy to retrieve:

- Signed contract and any scope changes

- Invoices for the month

- Delivery proof, for example accepted deliverables or milestone sign-off

- Communications that show how work, timing, and commercial terms were handled

- Tax-registration basics used in Germany, including your

Fragebogen zur steuerlichen Erfassungsubmission and yourSteuernummer

Before closing the folder, cross-check one invoice, one contract clause, and one real workweek. If they describe different realities, fix that gap now.

Step 3. Clean up invoice hygiene this week. Weak habits can become expensive if an audit happens years later.

| Checkpoint | What to verify | Red flag |

|---|---|---|

| Tax number on invoice | Use your Steuernummer or, where appropriate, your USt-IDNr. | Putting your Steueridentifikationsnummer (St-IDNr.) on client invoices |

| VAT statement | If you charge VAT, make sure the shown rate matches your treatment | Missing or unclear VAT wording |

| Non-standard VAT treatment | If you are not using the standard 19% VAT, quote the relevant legal paragraph each time | Reusing templates without the legal paragraph |

Keep this distinction clear: the St-IDNr. (11 digits) is personal and does not belong on freelance invoices; the Steuernummer (10 digits) is used for freelancer tax registration and invoicing.

Step 4. Patch contract language where needed, but treat that as alignment work, not a cure by itself. Review scope, deliverables, invoicing terms, and working-practice wording for consistency with how the work is actually done.

If contract language, delivery behavior, and invoicing tell different stories, fix the contradiction directly.

Step 5. If the facts still look weak after cleanup, choose a transition path early instead of defending a setup you cannot document cleanly. Practical paths can include reshaping the engagement, moving to direct employment, or discussing an EOR model where it fits your operating needs.

You might also find this useful: Freiberufler vs. Gewerbetreibender: A Critical Distinction for German Freelancers.

If your checklist shows the relationship is drifting toward managed employment, review a transition path in Merchant of Record for freelancers.

Frequently Asked Questions

What is Scheinselbstständigkeit in an audit context?

In an audit context, Scheinselbstständigkeit is a contractor label paired with an employee-like working reality. The key issue is whether your day-to-day work shows control and subordination instead of independent delivery.

Can a private contract alone prevent reclassification?

No. Authorities look at how the work is actually performed, not just what the contract says. If your calendars, approvals, tools, and delivery records look employee-like, contract wording alone will not prevent reclassification.

Which red flags matter most?

The main red flags are client control over your hours, method, and day-to-day tasks, plus integration into the client organization. On-site work with client materials, use of company tools or email, and relying heavily on one client can all strengthen the employee-like picture.

Who can trigger or run scrutiny?

Scrutiny can come from bodies such as the tax office, labor courts, the pension insurance association, and other social insurance actors. Before replying, confirm who sent the inquiry and respond only to the requested scope with one consistent factual account.

What can happen if I am reclassified?

Reclassification can trigger retroactive contributions that should have been paid, along with tax liabilities, fines, employee-rights claims, and retroactive social security exposure. In severe cases involving deliberate intent to defraud, the material says consequences can include significant fines or prison.

When should I switch to an EOR model?

Consider an EOR when the work is consistently being managed like employment and real contractor autonomy cannot be restored. If the client keeps directing your hours, place of work, and materials over time, reassess early instead of defending a weak freelance setup. Keep cross-border social security analysis separate from employment-status classification.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- ec.europa.eu/newsroom/just/document.cfmtrusted

- ela.europa.eu/sites/default/files/2021-09/Report%20UDW%20i...trusted

- ela.europa.eu/sites/default/files/2021-09/Study%20UDW%20Fa...trusted

- opts.ssa.gov/strusted

- sec.gov/Archives/edgar/data/1603756/0001603756210000...trusted

- ssa.gov/international/CoC_link.htmltrusted

- ssa.gov/international/agreement_descriptions.htmltrusted

- freelancermap.com/blog/false-self-employmentexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Germany Freelance Visa Application Path for Freiberufler and Gewerbe

Choose your track before you collect documents. That first decision determines what your file needs to prove and which label should appear everywhere: `Freiberufler` for liberal-profession services, or `Selbständiger/Gewerbetreibender` for business and trade activity.

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

Freiberufler vs Gewerbetreibender for German Freelancers

**Classify first, then file and invoice from the same description.** The safer path is the one that matches your real services, not the one that looks easier on admin.