Quick Answer

Yes, some taxpayers can claim the home office deduction for digital nomads, but only when a dedicated workspace and documentation support the position. Keep this analysis separate from FEIE and lodging classification, then select either the simplified method or the actual-expense method on Form 8829 based on your file quality. If your location timeline, income records, and workspace proof conflict, defer the claim and get targeted professional review before filing.

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

That is the right starting point because the IRS requirements here are strict, and weak support can create problems. Trying to treat travel or lodging costs as home office expenses without clear support is risky. The safer sequence is simpler: confirm your filing posture, classify income and expenses, test the quality of your records, and only then decide whether the deduction belongs on the return.

If you are self-employed and filing while living or working abroad, the deduction may still be available. But the workspace must be a dedicated home office used exclusively for work and as your primary place of business. Labels matter less than whether your classification and documentation support those facts.

Keep other tax concepts separate from the home office analysis from the start. A home office claim has its own requirements and records. It is not validated by a broad expat framing, and it does not automatically turn personal lodging into a business deduction.

A practical way to lower risk is to make two checks before you draft the return. First, choose a method you can actually support with your records: the simplified method, up to $1,500, or the actual-expense method on Form 8829. Both methods reduce Schedule C business profit, which can lower federal income tax and self-employment tax. Second, keep a dated location log with work addresses that matches the rest of your business records. If business use is not clearly supportable, treat the deduction as high risk and get targeted professional advice before you file.

The terms that actually decide your outcome#

Your first decision is classification, not calculation. Keep each concept in its own lane so your return position matches what your records can support.

| Term | What it answers | Decision criterion | Do not confuse with |

|---|---|---|---|

| Worldwide income reporting | What income belongs on the U.S. return | If you are a U.S. citizen or resident alien, report worldwide income even when you live abroad | Travel lifestyle, frequent moves, or FEIE plans |

| Home office deduction | A separate topic from the FEIE/FTC rules in this section | Handle this lane separately; this section does not determine home-office eligibility. For dedicated guidance, see The Complete Guide to the Home Office Deduction | FEIE, foreign housing benefits, or personal lodging |

| Tax home | Whether you have a supportable foreign-country tax-home position for FEIE-related benefits | For FEIE-related benefits, your tax home must be in a foreign country, and your records should support one consistent position | A "nomad" label, a mailing address, or day count alone |

| FEIE | Whether qualifying foreign earned income can be excluded after it is reported | Confirm foreign earned income, a foreign-country tax home, and a qualifying test, such as 330 full days in 12 consecutive months under physical presence | A non-filing rule or blanket exclusion for all income |

| Foreign Tax Credit | Whether foreign taxes paid can offset U.S. tax through credit rules | If filing Form 1116, use a separate form for each income category and check only one category box per form | One combined Form 1116 or a replacement for FEIE analysis |

Tax home is where many files break. Treat it as a defensible facts-and-records position. For FEIE-related benefits, your tax home must be in a foreign country, and your records should tell one consistent story. If they do not, stop and reconcile before claiming. For a deeper breakdown, see What is a 'Tax Home' and Why Does it Matter for US Expats?.

FEIE also stays in its own lane. You still file a U.S. return reporting the income, and physical presence is a strict day-count test: 330 full days in any 12 consecutive months, with a full day equal to 24 consecutive hours. Near misses do not qualify, and days in a foreign country while violating U.S. law do not count.

Keep the final gate simple: "nomad" is not a tax category. If your records conflict, default to no claim until you reconcile them. For the broader cross-border filing framework, use The Ultimate Digital Nomad Tax Survival Guide for 2025. For a step-by-step walkthrough, see this guide.

A 60-second claim or do-not-claim decision#

Use this as a hard screen, not a gut check. Move quickly only when your worker setup, location story, work-location facts, and records all align. Run the gates in order.

The four binary gates#

| Gate | Pass | Fail |

|---|---|---|

| Worker setup | Where you physically worked, how income was reported, and the return positions you plan to take all match one setup | Work location, reporting, and filing positions point in different directions |

| Location pattern | Your documented location pattern supports one coherent story and your arrangement type is clear | You rely on memory or shortcuts instead of records |

| Work-location facts | You can consistently document where work was performed and keep that story aligned with your filing position | Your work-location story is inconsistent or unsupported by your records |

| Evidence quality | Your records are sufficient and consistent enough to support your location and reporting positions | Key records are missing, contradictory, or reconstructed after the fact |

Gate-one reality check#

Be strict at gate one. Remote work can create multiple tax issues, and a useful checkpoint is the state tax trifecta: nexus exposure, payroll withholding, and individual income tax filing requirements. If your facts raise open questions across those buckets, this is not a quick-file claim. Complications are especially likely when an employee works in a jurisdiction where the employer had not previously engaged in business.

Outcome#

| Outcome | Trigger | Action |

|---|---|---|

| Claim | All four gates pass and records tell one consistent story | Claim |

| Defer and repair file | Any gate fails because records are missing, unclear, or misaligned | Defer and repair file |

| Escalate for professional review | Worker setup is disputed, or nexus, withholding, or filing exposure questions remain open | Escalate for professional review |

Pandemic-era temporary exclusions and special tax provisions largely expired, so do not rely on old remote-work assumptions. For broader filing context beyond this quick screen, see The Ultimate Digital Nomad Tax Survival Guide for 2025. Unresolved evidence means do not claim yet.

Your worker type changes the risk profile#

Lock worker classification before you test the deduction. Worker type does not decide eligibility on its own, but it does change the Social Security coverage check and the proof steps when more than one country is involved.

If you cannot document whether income was employee compensation or self-employment income, pause. Similar travel patterns or workspace costs do not fix a classification gap.

| Worker type | Classification cue | Primary filing path | Main error risk | Required evidence |

|---|---|---|---|---|

| W-2 employee | Work performed as an employee under employer payroll | Employee wage-reporting path tied to payroll handling | Assuming payroll handling alone resolves cross-border contribution issues | Payroll records, employer confirmation, and any Certificate of Coverage tied to the work period |

| Self-employed | Business income earned directly from clients or customers | Self-employment reporting path with your own contribution tracking | Skipping Totalization checks when two countries could tax the same earnings for Social Security | Income or payment records and any Certificate of Coverage if applicable |

| Mixed or unclear facts | Contracts, payroll, and tax records describe the same work inconsistently | Not a quick-file case | Blending employee and contractor treatment on one fact pattern | Records that reconcile worker status, payment flow, and corrected documentation before filing |

Use that table as a decision aid, not a formality. If two countries could tax the same earnings for Social Security, verify whether a Totalization agreement applies.

Cross-border coverage is a mandatory validation step#

Once classification is clear, run one non-optional check whenever two countries could both seek Social Security taxes on the same earnings. Totalization agreements assign coverage to one country to prevent dual Social Security taxation, but you still have to confirm that protection applies to your facts. For U.S. purposes, these agreements cover Social Security and Medicare taxes.

The key proof is a Certificate of Coverage. When an agreement assigns U.S. coverage, SSA issues a U.S. certificate, and employers or self-employed individuals can request certificates online. Keep the scope clear: this certificate supports Social Security tax exemption in the other country. It does not determine income tax treatment.

Country rules can also vary by worker type. Under the U.S.-Italy agreement, self-employed U.S. nationals working in both countries are assigned U.S. coverage. In an employee case under that agreement, the certificate step can run through an Italy-side request using form IT/USA 4. For broader filing context, see The Ultimate Digital Nomad Tax Survival Guide for 2025.

Proof file by worker type#

Build the proof file that matches your status before you claim anything:

- Employee: payroll records for the exact work period, employer confirmation, and any applicable Certificate of Coverage.

- Self-employed: records tying self-employment earnings to the work period and any applicable Certificate of Coverage.

- Mixed facts: separate each income stream, reconcile contracts with how you were paid, and fix inconsistencies before filing.

The practical rule is simple: confirm status first, then confirm cross-border Social Security coverage. If classification is wrong, the agreement and certificate steps are easy to misapply.

Tax home is the hinge point for nomads#

Treat tax home as a gate for FEIE-related positions. If it is not defensible on paper, pause and reassess the claim. For globally mobile filers, tax home is an evidence-backed filing position, not a lifestyle label, and mixed location facts can weaken your filing position.

Keep the tests separate#

These are related, but they are not the same test:

- For FEIE, you must have foreign earned income, your tax home must be in a foreign country, and you must meet a qualifying status test.

- One qualifying route is the physical presence test: 330 full days in foreign countries during 12 consecutive months.

- The 330 days do not have to be consecutive.

- A full day is 24 consecutive hours from midnight to midnight.

- The physical presence test is based on time abroad, while tax home also considers the nature and purpose of your stay.

- Passing a day count does not, by itself, prove tax home or resolve separate deduction treatment.

- If you claim FEIE, you still file a U.S. return reporting the income.

Quick coherence check (pass/fail)#

| Check | Pass | Fail |

|---|---|---|

| Base pattern | Your work timeline and income records show where work was carried on during the claim period | Contracts, invoices, calendar records, and client communications point to different centers with no clear anchor |

| Address consistency | Your return, billing or banking correspondence, lease or housing records, and client files broadly tell the same location story | Different countries appear across records with no dated explanation |

| Travel-purpose records | Each trip has dates plus a short purpose note, such as work travel, relocation, or personal | Trips are labeled as business travel after the fact without contemporaneous support |

Records over narrative#

Before you proceed, make sure these four items align: a dated work timeline, income records tied to that timeline, a consistent address trail, and trip-purpose notes. For a deeper definition, see What is a 'Tax Home' and Why Does it Matter for US Expats?.

If facts are mixed, use the conservative default: narrow or defer the claim until your documents support one consistent story. Related: How to Write Off a Home Office as a Renter.

Home office deduction is not FEIE and not a travel write-off#

This is a lane-control step. Keep home office, business travel, FEIE, and FTC separate so one test does not get used to justify another.

A simple rule helps: do not use one bucket to prove a different bucket. FEIE day counts belong in the FEIE lane. Foreign taxes paid belong in the FTC lane. Home office and lodging treatment should be analyzed in their own lane. If you need foreign-tax-home fundamentals, see What is a 'Tax Home' and Why Does it Matter for US Expats?.

Keep the four buckets separate#

| Bucket | What this bucket can do | What it cannot do | Evidence required |

|---|---|---|---|

| Home office deduction | Analyze workspace-related deduction treatment | It does not replace FEIE qualification checks or travel-expense analysis | Workspace records tied to your facts; for fundamentals, see The Complete Guide to the Home Office Deduction |

| Business travel expenses | Review trip-cost treatment in its own lane | It does not create FEIE eligibility | Dated records, purpose notes, and invoices |

| FEIE | Exclude qualifying foreign earned income if FEIE tests are met | It cannot classify deductions or replace expense analysis | Support for foreign earned income, foreign tax home, and qualifying-status records |

| FTC | Credit eligible foreign taxes paid or accrued | It cannot replace FEIE tests or merge all foreign income into one filing bucket | Form 1116 workpapers by income category, one category box per form, with separate country lines or columns where required |

FEIE is narrow, not general-purpose. You must have foreign earned income, a foreign tax home, and a qualifying status test. If you use physical presence, the threshold is 330 full days in 12 consecutive months, and a full day is 24 consecutive hours (midnight to midnight). If you miss 330 full days, you fail that test.

Use this filing order#

| Order | Action | Detail |

|---|---|---|

| 1 | Report income first | Excluded foreign earned income is still reported on your U.S. return to claim FEIE |

| 2 | Run FEIE and FTC checks next | Keep those qualification and credit steps separate from deduction analysis |

| 3 | Then classify deductions and expenses | Evaluate home office, travel, and lodging treatment separately |

| 4 | If using housing exclusion, compute it before final FEIE capacity | FEIE capacity is reduced by any foreign housing exclusion claimed |

For 2026, FEIE is capped at $132,900 per qualifying person. The general housing-expense limitation is 30%, or $39,870 for 2026. Keep those numbers inside the FEIE lane only.

Common misclassification to avoid#

Example: you work from an Airbnb kitchen table for 10 days and keep receipts. Treat that as needs separate classification rather than assuming one treatment from FEIE or FTC facts alone. Keep invoice, date, and purpose records together, and finalize treatment only when the file supports it.

Pre-file consistency check (pass/fail)#

| Lane | Pass | Fail |

|---|---|---|

| Income | Worldwide income is reported and matches your work timeline | Excluded income is omitted, or records do not match claimed periods |

| FEIE | You can support foreign earned income, foreign tax home, and qualifying status, including 330 full days in a 12-month window if using physical presence | Day counts are estimated, full-day tracking is missing, or tax-home support is mixed |

| FTC | One category box per form, with multi-country taxes separated by country line or column where required | Foreign taxes are blended without category or country separation |

| Deductions | Each lodging or workspace item is reviewed in its own deduction lane (home office candidate, travel candidate, personal, or unresolved) | FEIE status is used as the reason an expense must be deductible |

If any lane fails, take the conservative default: narrow or defer the claim until the records support one consistent story. For broader context on how these lanes fit together, see The Ultimate Digital Nomad Tax Survival Guide for 2025.

For a domestic example of method choice and recordkeeping, see Home Office Deduction for Real Estate Agents: Qualify, Choose a Method, and Keep Records.

Airbnb and short-term stays need strict classification#

An Airbnb or short-term stay is a classification decision first, not a deduction decision. If the facts are mixed or weak, default to personal lodging.

| Working bucket | Use only when your file clearly shows | Conservative default |

|---|---|---|

| Personal lodging | The stay mainly functioned as where you lived, and you do not have clear support for another category | Keep it personal |

| Business travel lodging | You can clearly document where you lived, worked, and earned income, plus a business purpose you can defend | Keep personal treatment until verified |

| Home-office candidate | Do not assume a short-term stay qualifies automatically; if you are exploring this angle, start with The Complete Guide to the Home Office Deduction and verify current rules before claiming | Treat as personal when use is mixed or unclear |

| External office rent | Terms and charges are clearly separated from housing, and treatment is verified before filing | Do not merge uncertain charges into lodging |

A common failure mode is the kitchen-table setup. Daily work there, by itself, does not automatically convert lodging into office treatment. Use this sequence for each stay:

- Classify the stay pattern.

- Document where you lived, worked, and earned income.

- Verify any deduction treatment before you claim it, especially when personal and business use overlap.

- If facts stay unclear, keep personal treatment.

If any gate fails, keep personal treatment. That conservative default is cleaner when residency treatment is still unclear and proof of residency can affect your broader position. If that foundation is unclear, review What is a 'Tax Home' and Why Does it Matter for US Expats? before filing.

For each stay, keep a clear record set tied to where you lived, worked, and earned income. If your personal and business use overlap and you cannot explain the split clearly, keep personal treatment until you verify the applicable rules.

State exposure still matters when you are globally mobile#

Going abroad does not switch off state tax rules. For California, run three separate pass-or-fail lanes before you file: residency status, income sourcing, and filing or withholding alignment.

Residency status#

Start here. If your residency period is not defensible with dated records, pause everything else. California treats someone as a resident if they are in the state for other than a temporary or transitory purpose. It also treats someone as a resident if they are domiciled in California and away only temporarily or transitorily. Residency is primarily a question of fact.

Pass only if your file clearly supports when you were resident, part-year resident, or nonresident. Fail if your position is mostly narrative, for example, "I left California," without records showing when status changed. Your documentation has to carry this position.

If your federal posture is still unclear, review What is a 'Tax Home' and Why Does it Matter for US Expats?. If your broader cross-border setup is still unsettled, step back to The Ultimate Digital Nomad Tax Survival Guide for 2025 before locking a state filing position.

Income sourcing#

For services, work location drives sourcing. For nonresidents, and for the nonresident portion of a part-year period, services physically performed in California are California-source income.

Do not default to client address, payer address, or contract labels when the work happened elsewhere. If you allocate compensation, reconcile it to dated records. California scenario guidance uses a workday ratio, CA Workdays / Total Workdays = % Ratio, then % Ratio x Total Income = CA Sourced Income. That method only works if calendar dates, invoices, and contract service periods match.

Stop if they do not match. If your calendar, payment trail, and service-period records do not tell one consistent story, fix that before assigning sourced income or preparing Form 540NR.

Withholding and filing compliance#

Treat compliance as its own lane. Even a solid residency and sourcing analysis can fail if reporting and return positions do not align. Check current filing requirements before you file, then confirm your reporting posture and any withholding treatment match the sourcing position you are actually taking.

Use a minimal pre-filing packet:

- Dated residency timeline, showing resident, part-year, and nonresident periods

- Work calendar with California workdays and total workdays

- Invoices mapped to service periods and work location

- Payment records and year-end forms mapped to the same periods

- Short position memo: fully California, partly California, or not California-source

Form 540NRworkpaper and a note to verify the current filing requirement before filing

If calendar, payment trail, and reporting position do not reconcile, do not file until they do.

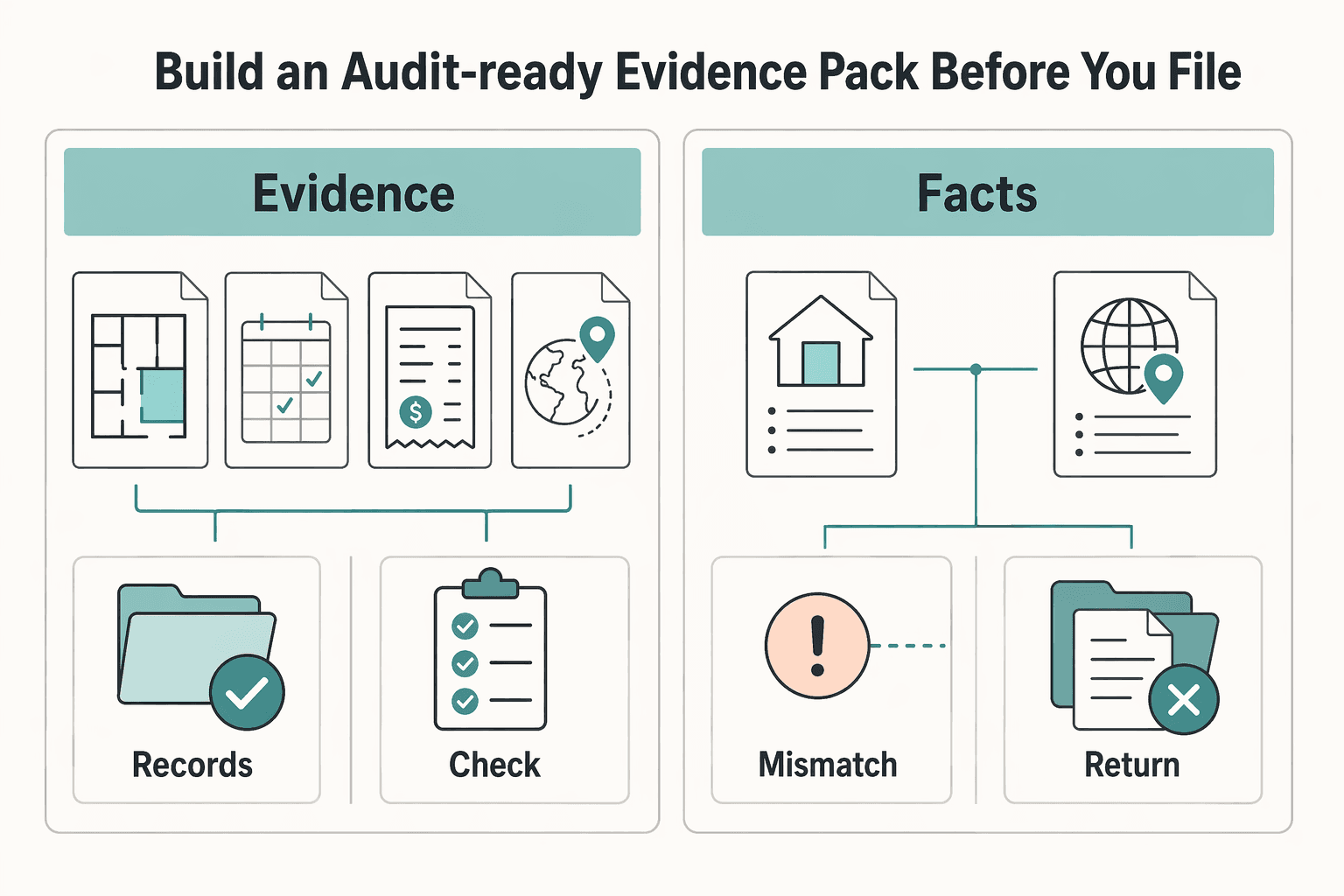

Build an audit-ready evidence pack before you file#

Build the evidence pack first, and draft the return second. That order catches weak classifications early, so unsupported positions do not get baked into a filing you may have to defend later.

Use this sequence for every position you plan to file:

- Define the position in one sentence.

- Map the minimum records that prove that position.

- Mark anything without support as not ready to claim.

Day counting is only one FEIE gate, not the whole test. FEIE eligibility is multi-gate: foreign-earned income, a foreign tax home, and a qualifying-status test. If you need upstream context before locking this position, review What is a 'Tax Home' and Why Does it Matter for US Expats?.

| Filing position | What you are asserting | Minimum evidence to collect | Status if support is missing |

|---|---|---|---|

| FEIE (physical presence route) | You had foreign-earned income, your tax home was in a foreign country, and you met the time test | Dated location log, passport or entry records, flight confirmations, tax-home memo, FEIE workpaper | Not ready to claim |

| Foreign-earned income allocation | Income was earned from personal services performed abroad and tied to the correct tax year | Contracts, invoices, service-period calendar, payment records, workpaper mapping income to year earned, not only year received | Not ready to claim |

| Account-reporting analysis | Separate account-reporting duties may apply and should be reviewed separately from FEIE | Account statements, ownership or signatory records, year-end summaries, and account-change notes | Not ready to file that analysis |

| Final return workpapers | Your forms match the facts you are taking | Draft forms, reconciliation notes, position memo, date, location, and income cross-check | Pause until reconciled |

For the physical presence route, track the rule precisely: 330 full days in any 12 consecutive months, and a full day is 24 consecutive hours beginning and ending at midnight. If records show only travel events, they may be incomplete for day-count support. If the time requirement is missed, this route fails even for common disruptions. If you think an adverse-condition waiver applies, verify the current annual IRS Revenue Procedure before treating the shortfall as waived.

Keep folders by purpose so retrieval is fast:

Location proof: where you were, and on what dates.Income sourcing: what services you performed, where, and when income was earned.Account reporting: account records kept separate from return-drafting files.Form workpapers: draft forms plus notes and schedules explaining each number.

Use a light monthly reconciliation routine:

- Update the location log and reconcile it to travel records.

- File contracts, invoices, and payments by service period.

- Save new account statements and ownership or signatory changes.

- Add a short month-end note with new records, open questions, and mismatches.

If core evidence is missing or conflicts across folders, pause filing and resolve the gaps before submission. When your records tell two different stories, do not file the more convenient one.

For the FEIE side of the file, review Tax Home vs. Abode: A Critical Distinction for the FEIE.

Keep your filing stack clean and non-overlapping#

Once the evidence pack is built, keep the filing stack clean by separating four lanes: the federal return, FBAR (FinCEN Form 114), Form 8938, and Form 8938 Part III. They answer different compliance questions, and no single check replaces the others.

| Filing item | What it checks | Boundary that matters |

|---|---|---|

| US federal income tax return | Whether you must file an annual return, and where related tax items are reported | Form 8938, if required, attaches to this return and is filed by that return's due date, including extensions |

| FBAR (FinCEN Form 114) | Separate foreign-account reporting analysis | Filing Form 8938 does not replace FBAR when FBAR is otherwise required |

| Form 8938 | Whether a specified person with an interest in reportable specified foreign financial assets meets the filing conditions and exceeds the applicable threshold | Apply the current threshold only after checking the latest instructions |

| Form 8938 Part III | Whether tax items tied to reported foreign assets match the correct return form or schedule lines | This is a tax-item alignment check, not a substitute for asset testing |

Start with the return, then run Form 8938 gates#

Use this order every time:

- Determine whether an income tax return is required for the year.

- If no return is required, do not file Form 8938 for that year.

- If a return is required, test specified-person status.

- Then test whether you have an interest in specified foreign financial assets required to be reported.

- Only then apply the correct threshold set, using the latest instructions.

This sequence helps you avoid jumping straight to a threshold number and skipping earlier gates.

Test each account independently for each regime#

Assume scope can differ by form, then prove inclusion separately. A practical rule is that each account gets one FBAR inclusion decision and one Form 8938 inclusion decision, even if the account already appears on one form.

Keep your tracker explicit: return treatment, Form 8938 inclusion, FBAR inclusion, and related tax-item location. One "handled" checkbox is not enough.

Make maximum values reproducible#

Treat maximum value as a reproducibility standard, not a memory standard. For each account, your workpapers should show:

- Source statements used

- Valuation window reviewed

- Currency conversion method used, if not USD

- Rounding approach used

If someone cannot reproduce the reported value from your file, treat the form as not ready to file.

Stop-go checks for complex years#

Before filing, run this triage:

- Foreign assets were acquired or sold during the year: refresh the asset list, value support, and both FBAR and Form 8938 analyses.

- Return line items changed during preparation: reconcile Form 8938 Part III to final form or schedule lines.

- Filer-status facts changed, for example, status or entity facts: re-verify the correct Form 8938 threshold set.

- Prior-year foreign-reporting gaps or unresolved account-classification conflicts exist: consider resolving those before finalizing current-year filing.

If you need upstream context before making the stop-or-go call, first review What is a 'Tax Home' and Why Does it Matter for US Expats?. Then revisit The Ultimate Digital Nomad Tax Survival Guide for 2025.

If you are still planning the move itself, Legal and Financial Pre-Departure Priorities for US Digital Nomads covers the pre-departure checklist.

Red flags that mean stop and get professional review#

Run one final coherence test before filing: can your filing position and residency position both be supported by the same records? If not, stop. Breakdowns often come from inconsistent facts, not one missing document.

Cross-border problems often come from patterns that invite scrutiny, even without bad intent. If your documents change the story, pause filing and rework the position before submission.

Filing-scope confusion#

Stop when you cannot clearly place each fact in the right compliance lane. If your approach depends on overlapping assumptions instead of a clear, consistent record trail, pause and get specialist review.

Stop here too if core records conflict: payroll dates versus immigration dates, missing residency updates, or split payroll. Those are explicit red flags and justify specialist review before filing.

Account-value support gaps#

Stop if key reported amounts cannot be reproduced from your records. If numbers change depending on which record set you use, your position is not stable.

Pause and get targeted help before filing when more than one record set tells a different story.

Inconsistent classifications across work, travel, and residency#

Stop when one fact pattern is classified multiple ways across the file. A common example is the same stay treated as personal time in one place and work time in another.

Also pause when residency and work-location logic do not form one coherent narrative. Rebuild the evidence pack and recheck filing-lane separation before proceeding.

Unresolved prior-period issues#

Stop if your current filing position depends on unresolved inconsistencies from earlier records.

Use a simple test: if you cannot support the position with one coherent, consistent set of facts, pause and escalate before filing.

Final gate#

- Proceed: filing lanes are clear, records support one consistent narrative, and key amounts and classifications are reproducible.

- Revise positions: core facts are mostly consistent, but some items still need reclassification, stronger documentation, or removal.

- Consult specialist: payroll and immigration dates conflict, residency updates are missing, split payroll is unresolved, work/travel classification is inconsistent, or your position depends on unsupported assumptions.

If you land in Consult specialist, do not file first and fix later. A short pause is usually lower risk than defending a position your file cannot support.

Can digital nomads claim the home office deduction?#

Yes, sometimes, especially if you are self-employed and using a dedicated business workspace. Here, that means a deduction tied to a dedicated workspace, not a general remote-work write-off. The key gate is a consistent workspace record. If your records are weak or conflicting, skip the claim and review The Complete Guide to the Home Office Deduction.

Does having a tax home abroad automatically mean I can take the deduction?#

No. A foreign tax home is part of FEIE analysis, but it does not by itself establish home-office eligibility. If your records conflict, keep tax-home and deduction decisions separate and get professional review.

Does FEIE replace the home office deduction?#

No. FEIE is a separate exclusion for qualifying foreign earned income, not a shortcut for workspace treatment. The gate is foreign earned income, a foreign tax home, and a qualifying status test. If any of those are weak, do not use FEIE to support other deductions. Review What is a 'Tax Home' and Why Does it Matter for US Expats?.

Can I use the physical presence test if I move constantly?#

Yes, if you meet the count. The test is time-based: at least 330 full days during any 12 consecutive months, and a full day is 24 consecutive hours from midnight to midnight. The gate is a day-by-day record that reproduces the total. If you are estimating days, counting partial days, or have gaps, default to not claiming the test and escalate when FEIE is central.

If I claim FEIE, do I still file a U.S. return?#

Yes. FEIE may reduce qualifying foreign earned income, but you still file a U.S. return reporting that income. The gate is a complete return with exclusion calculations supported by records. If you treated FEIE as a reason not to file, stop and correct that first.

Is Airbnb or short term rent deductible if I work there every day?#

Not automatically. A blanket rule for Airbnb or short-term rent is not established here, and remote work alone does not settle home-office treatment. The key gate is line-by-line support: invoice, dates, purpose, and consistent treatment. If a stay can be read more than one way, default to a conservative treatment until you can support a narrower position.

How do I know whether my income qualifies as foreign earned income?#

Foreign earned income is compensation for personal services you performed, such as wages, salaries, or professional fees. This term is about income character, not home-office eligibility or rent treatment. The gate is payment records tied to your services and the correct period. If categories or timing are mixed, do not force FEIE treatment without review.

Can I use both FEIE and housing related benefits?#

Yes, sometimes, and order matters. The housing amount is figured first, which reduces income available for FEIE. The gate is a worksheet that applies this order clearly. If your workpapers mix housing, exclusion, and deduction items, pause and get help before filing.

Are there two ways to calculate the home office amount?#

Yes. The two methods here are a simplified method (up to $1,500) and an actual-expense method on Form 8829. The gate is choosing one method and supporting it with records. If expense support or space-allocation records are weak, the safer default is to skip the claim.

Do state tax rules still matter if I spent most of the year abroad?#

Potentially. State exposure is a separate lane. The gate is state-specific residency and sourcing support. If state ties are still active, your address timeline is unclear, or reporting issues remain unresolved, review The Ultimate Digital Nomad Tax Survival Guide and get state-focused professional advice.

For cross-border filings, defensibility is the point. Outcomes generally turn on facts and documentation, not travel identity alone.

Run one conservative pass through your file before you submit. Treat uncertain items as unproven, fix evidence gaps first, and file only positions you can explain clearly from your records. The throughline across this article is simple: confirm tax residency first, classify carefully, document early, and keep each obligation in its own lane so one weak assumption does not contaminate the whole return.

Use this final pre-filing check:

- Re-run your claim or do-not-claim review for each filing position and keep the written rationale in your file.

- Confirm your tax residency status first. That is the starting point for understanding your cross-border obligations.

- If you worked across countries, check for overlap risk where one country may tax by residence and another by where work was performed.

- If you are a U.S. citizen working abroad, confirm your U.S. income-tax obligations before choosing filing positions.

- Run a separate foreign-account reporting check, because additional reporting requirements such as FBAR may still apply.

- Keep home-office analysis separate. Eligibility turns on facts like exclusive work use, not on nomad status alone.

A recurring risk at this stage is overlap confusion: assuming one rule settles another or mixing different tests. Home-office eligibility, income-tax obligations, and foreign-account reporting are related, but they are separate determinations.

If key facts remain mixed after this review, get targeted professional review before submission.

If your residency story is still mixed by the end, use the Tax Residency Tracker to organize travel days before filing.

Frequently Asked Questions

Can digital nomads claim the home office deduction?

Yes, sometimes, especially for self-employed taxpayers using a dedicated business workspace. Here, the home office deduction for digital nomads means a deduction tied to a dedicated workspace, not a general remote-work write-off. The gate is a consistent workspace record. If records are weak or conflicting, skip the claim and review The Complete Guide to the Home Office Deduction.

Does having a tax home abroad automatically mean I can take the deduction?

No. A foreign tax home is part of FEIE analysis, but it does not by itself establish home-office eligibility. If your records conflict, keep tax-home and deduction decisions separate and get professional review.

Does FEIE replace the home office deduction?

No. FEIE is a separate exclusion for qualifying foreign earned income, not a shortcut for workspace treatment. The gate is foreign earned income, a foreign tax home, and a qualifying status test. If any of those are weak, do not use FEIE to support other deductions. Review What is a 'Tax Home' and Why Does it Matter for US Expats?.

Can I use the physical presence test if I move constantly?

Yes, if you meet the count. The test is time-based: at least 330 full days during any 12 consecutive months, and a full day is 24 consecutive hours from midnight to midnight. The gate is a day-by-day record that reproduces the total. If you are estimating days, counting partial days, or have gaps, default to not claiming the test and escalate when FEIE is central.

If I claim FEIE, do I still file a U.S. return?

Yes. FEIE may reduce qualifying foreign earned income, but you still file a U.S. return reporting that income. The gate is a complete return with exclusion calculations supported by records. If you treated FEIE as a reason not to file, stop and correct that first.

Is Airbnb or short term rent deductible if I work there every day?

Not automatically. This guide does not set a blanket rule for Airbnb or short-term rent, and remote work alone does not settle home-office treatment. The gate is line-by-line support, invoice, dates, purpose, and consistent treatment. If a stay can be read more than one way, default to a conservative treatment until you can support a narrower position.

How do I know whether my income qualifies as foreign earned income?

Foreign earned income is compensation for personal services you performed, such as wages, salaries, or professional fees. This term is about income character, not home-office eligibility or rent treatment. The gate is payment records tied to your services and the correct period. If categories or timing are mixed, do not force FEIE treatment without review.

Can I use both FEIE and housing related benefits?

Yes, sometimes, and order matters. The housing amount is figured first, which reduces income available for FEIE. The gate is a worksheet that applies this order clearly. If your workpapers mix housing, exclusion, and deduction items, pause and get help before filing.

Are there two ways to calculate the home office amount?

Yes. The two methods here are a simplified method (up to $1,500) and an actual-expense method on Form 8829. The gate is choosing one method and supporting it with records. If expense support or space-allocation records are weak, the safer default is to skip the claim.

Do state tax rules still matter if I spent most of the year abroad?

Potentially. State exposure is a separate lane and is not covered here. The gate is state-specific residency and sourcing support. If state ties are still active, your address timeline is unclear, or reporting issues remain unresolved, review The Ultimate Digital Nomad Tax Survival Guide and get state-focused professional advice.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- ftb.ca.gov/file/personal/residency-status/part-year-and...trusted

- ftb.ca.gov/file/personal/residency-status/index.htmltrusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- ssa.gov/international/CoC_link.htmltrusted

- ssa.gov/international/agreement_descriptions.htmltrusted

- utah.gov/pmn/files/1180739.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Home Office Deduction Rules for Freelancers With Multiple Homes

For globally mobile freelancers, this deduction is a compliance decision before it becomes a tax-saving tactic. The practical rule is simple: claim it only when your facts clearly pass the IRS tests and your records can support that position from worksheet to filed return. If the facts are mixed, stop before you calculate and get a focused review.

What Is a Tax Home for US Expats and Why It Matters

Set your tax-home classification before you touch FEIE or housing math. That call sets the boundary for everything that follows, because foreign days count only for periods when your work-base position is foreign. A perfect travel calendar cannot rescue a weak classification.

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.