Quick Answer

Yes - classify your activity before sending invoices. In freiberufler vs gewerbetreibender cases, the Finanzamt decides unclear classifications, so your first filing should use precise service wording in the Fragebogen zur steuerlichen Erfassung. After submission through Elster or your local tax office, invoice with the issued Steuernummer and keep wording consistent across contracts and billing. If your work includes trade elements, complete Gewerbeanmeldung at the Gewerbeamt and separate mixed activity records before recurring invoice runs.

Start Here: Why This Choice Drives Your Tax Risk in Germany#

Classify first, then file and invoice from the same description. The safer path is the one that matches your real services, not the one that looks easier on admin.

| Step | Action | Keep or confirm |

|---|---|---|

| 1 | Write a short activity description based on real deliverables, not a preferred title. | Reuse that wording in your invoice template. |

| 2 | Submit the Fragebogen zur steuerlichen Erfassung through Elster or your local tax office. | Keep proof of submission. |

| 3 | Track when your Steuernummer is issued. | Use it consistently on invoices. |

| 4 | Keep a dated copy of the initial filing package. | Later changes stay traceable. |

When client work starts quickly, the pressure to invoice is real, but Germany still expects the early registration steps to happen in order. Start with a written activity description, then the Fragebogen zur steuerlichen Erfassung, then your invoice setup once the Steuernummer arrives. Some activities are treated as trade (Gewerbe), so early assumptions can create avoidable rework. Before billing starts to snowball, use this sequence:

- Write a short activity description based on real deliverables, not a preferred title.

- Submit the registration questionnaire through Elster or your local tax office, and keep proof of submission.

- Track when your

Steuernummeris issued and use it consistently on invoices. - Keep a dated copy of the initial filing package so later changes stay traceable.

A quick practical test helps in week one. If you cannot explain your dominant service line in one sentence and reuse that exact wording in your invoice template, pause your billing setup briefly. That pause is usually easier than rewriting contracts, invoices, and registration notes after the first payments arrive.

If you are employed and self-employed at the same time, treat communication as part of setup, not cleanup. Relevant guidance includes informing your employer and registering the activity with the tax office. Missing that step can create friction later once reporting catches up. Escalate early if any of these apply:

- Your services are split between liberal-profession work and trade-like work, and the dominant activity is unclear.

- Filing language, website positioning, and invoice descriptions do not describe the same service.

- You are starting side self-employment while employed and have not handled employer communication clearly.

Use the next side-by-side comparison to lock the classification before your next invoice batch gets larger and harder to fix.

Freiberufler vs Gewerbetreibender at a Glance#

Once your initial setup is clear, run this comparison before billing scales. The choice is about accurate classification, not preference, and unclear cases are decided by the tax office.

| Criteria | Freiberufler | Gewerbetreibender |

|---|---|---|

| Legal basis | Anchored in Section 18 EStG and the Katalogberufe; in ambiguous cases, tax-office interpretation controls the outcome. | Trade or commercial activity outside the catalogue-profession logic; in ambiguous cases, tax-office interpretation controls the outcome. |

| Registration path | Register directly with the tax office via the registration questionnaire, with no Gewerbeamt step in this path. | Register through Gewerbeanmeldung at the Gewerbeamt. |

| Tax types | Not treated as trade for Gewerbesteuer in this category. | Trade registration brings Gewerbesteuer exposure. |

Industrie- und Handelskammer (IHK) | This article does not establish obligations for this category; confirm them based on your filed activity. | This article does not establish obligations for this category; confirm them based on your filed activity after trade registration. |

| Admin duties | No trade-office registration step, but filing and invoice language must match real services. | More registration and admin steps from trade setup. |

| Bookkeeping method | Einnahmenüberschussrechnung (EÜR) is available as a simplified income-minus-expenses method, regardless of turnover. | Do not assume identical bookkeeping treatment automatically; confirm requirements after classification. |

| Reclassification risk | Classification is detail-sensitive: small wording details can change the result, and misclassification can lead to back taxes, penalties, and extra paperwork. | Misclassification can lead to back taxes, penalties, and extra paperwork. |

Use the table as a decision filter. If one row clearly points you toward trade treatment, build around that route first and budget for the added admin from day one. If the rows point to freelance treatment, keep your wording tight and rerun this comparison when your offers change.

The real tradeoff is speed now versus stability later. A rushed filing may get invoices out faster, but detail-sensitive classification often leads to expensive cleanup. One comparison source estimates a potential profit impact tied to trade-tax treatment at roughly 7 to 17 percent depending on municipality, so treat that figure as directional. Before your next invoice batch, run one verification pass:

- Keep a dated copy of your submitted registration questionnaire or

Gewerbeanmeldungreceipt. - Use one consistent activity description across filings, contracts, and invoice line items.

- Check for drift between your filed activity description and delivered services before billing.

- Recheck classification when your service mix changes materially, especially if work shifts toward commercial execution.

What the Tax Office Actually Classifies#

The Finanzamt looks at what you actually do, not what you call yourself. You cannot pick a status for convenience, and a job title alone does not decide the outcome. Use this decision stack before filing:

| Review point | What matters | Evidence or outcome |

|---|---|---|

Section 18 EStG | Legal anchor for freelance treatment. | Start with it before filing. |

Katalogberufe fit | Whether your core activity fits the logic of Katalogberufe. | Check your core activity against that logic. |

| Borderline cases | Facts are ambiguous. | The tax office makes the final call case by case. |

| Activity description | What you actually deliver. | Reviewed with qualifications, portfolio material, and contracts. |

| Mixed activity | Whether activities become intertwined. | Authorities can treat the full activity as Gewerbe, including retroactively. |

- Start with

Einkommensteuergesetz (EStG), especiallySection 18 EStG, as the legal anchor for freelance treatment. - Check whether your core activity fits the logic of

Katalogberufe. - Treat borderline cases as case-by-case review, because the tax office makes the final call when facts are ambiguous.

A simple self-check helps before you file: what do you actually deliver, and what evidence do you have today that supports that description? If either answer is vague, stop and tighten it before filing.

At registration, the activity description is reviewed with evidence such as qualifications, portfolio material, and contracts. That makes the registration questionnaire an important risk point. If the filed language and real delivery drift apart, reclassification risk rises.

One common failure mode is mixed activity that becomes intertwined. In that situation, authorities can treat the full activity as Gewerbe, including retroactively. Before you submit the registration questionnaire, run this checkpoint:

- Write one clear primary activity statement and keep it narrow enough to defend.

- Test that statement against your first contract scopes and invoice line items.

- Keep matching evidence together, including qualification proof, short portfolio samples, and signed contracts.

- If you cannot explain your dominant activity in two clear sentences, redraft before filing.

If your case is borderline, plan for case-by-case review from day one. Use conservative wording that matches current delivery, avoid inflated titles, and update your filing posture when your service mix changes materially. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Describe Your Services So the Filing Matches Reality#

Describe services as you actually deliver them, then keep that wording consistent everywhere. The tax office reviews your activity description with evidence such as qualifications, portfolio, and contracts, so vague language creates avoidable risk. Use this order before submitting the registration questionnaire:

- List your real deliverables.

- Map each deliverable to professional freelance-type work or commercial execution.

- If you have more than one service line, define one primary activity and one secondary activity before filing as

FreiberuflerorGewerbe. - Draft one precise activity description for the office and align supporting documents to it.

Use wording that is specific, narrow, and defensible. The examples below show the difference in practice.

| Profile | Weak wording | Stronger wording for filing |

|---|---|---|

| Consultant | Business consultant for digital growth | Provides advisory services with defined consulting deliverables documented in contracts and invoices. |

| Creator | Content creator and media services | Creates original written and visual content based on client briefs, with defined deliverables in contracts and invoice line items. |

| Mixed services | Freelance consultant and agency support | Primary activity advisory deliverables. Secondary activity execution services listed separately in contracts and billing. |

Before you press submit, put three documents side by side: your filing draft, one active contract, and one draft invoice. If you cannot describe the service with the same nouns in all three places, edit before filing. Classification disputes often start with small wording drift at this step.

This separation is operational, not cosmetic. Split freelance and trade setups are generally recognized only when they are cleanly separated in practice and bookkeeping. If the lines become intertwined, the tax office may treat the whole activity as trade, including retroactively. Use this verification checkpoint:

- The same core activity wording appears in your registration questionnaire and invoices.

Freiberuflerand trade lines are separated in banking, invoices, records, and books when both exist.- If a trade line requires

Gewerbeanmeldung, file at theGewerbeamtbefore, or at the latest immediately after, the first invoice for that line.

A clear red flag is invoicing trade-like work while describing only freelance activity in your filings. Guidance notes possible fines for missing required trade registration, plus retroactive tax cleanup.

Write filing text as if you may need to defend it with documents later. If an invoice line cannot be mapped to your filed activity description, revise before submitting. Related: The Best Analytics Tools for Your Freelance Website.

Registration Sequence Without Missed Steps#

Do not improvise the order. A safer sequence is to confirm your classification (Freiberufler or Gewerbetreibender), begin tax-office registration, and align invoicing only after you have written confirmation.

| Item | What to confirm |

|---|---|

Steuernummer | Received and added to your invoice setup. |

| Tax-office registration | Status confirmed in writing. |

| Business registration or memberships | Any required business registration or memberships confirmed. |

| Insurance and invoicing | Insurance and invoice setup aligned with your registered activity. |

| Service wording | Wording on invoices and website still matches what you filed. |

Common missteps happen when execution gets ahead of registration. Keep your activity description consistent from registration through invoicing, and avoid changing labels midstream. A practical sequence is:

- Define your activity description and classify it as

FreiberuflerorGewerbetreibender. - Start tax-office registration.

- Complete business or trade registration if your activity requires it.

- Confirm your registration documents and

Steuernummerbefore scaling recurring invoicing.

Use this as an operational checklist, and verify local requirements because processes can change. If confirmation letters lag, note any temporary invoicing-hold decisions and keep wording consistent across your records.

Use this checkpoint list before your first recurring invoice cycle:

Steuernummerreceived and added to your invoice setup.- Tax-office registration status confirmed in writing.

- Any required business registration or memberships confirmed.

- Insurance and invoice setup aligned with your registered activity.

- Service wording on invoices and website still matches what you filed.

The Cost and Admin Differences That Matter in Year One#

In year one, both paths still face Einkommensteuer and may have VAT duties. The key difference is that only trade (Gewerbe) status can trigger Gewerbesteuer, and trade status usually brings more admin.

Treat this as part of pricing design, not just tax compliance. If your margins are tight, even moderate trade-tax exposure can change what you need to charge to keep the same net income. Running both scenarios before you publish pricing helps you avoid mid-year price corrections that are hard to explain to clients.

| Decision area | Freiberufler | Gewerbetreibender |

|---|---|---|

| Core cash-flow pressure | No Gewerbesteuer in this category; one comparison source estimates the profit impact of that gap at roughly 7 to 17 percent depending on municipality. | Gewerbesteuer exposure can apply once annual profit is above 24,500 EUR. |

| Taxes both still handle | Einkommensteuer on profit, plus VAT handling where applicable. | Einkommensteuer on profit, plus VAT handling where applicable. |

| Chamber and admin burden | One source notes no compulsory Industrie- und Handelskammer (IHK) membership for this category. | Trade status can bring added chamber and filing obligations. |

| Bookkeeping path | Einnahmenüberschussrechnung (EÜR) is available as a simplified income-minus-expenses method. | Simpler bookkeeping may work early, but one comparison source says a switch to double-entry is required once cited thresholds are crossed: 800,000 EUR revenue or 80,000 EUR profit. |

| Who decides classification | In unclear cases, the tax office decides. | In unclear cases, the tax office decides. |

Use those figures for planning, not as permanent constants. Local handling can vary, so verify thresholds and forms when you file.

Admin differences compound over time. EÜR can keep reporting lighter, but complete income and expense records still matter. On the trade path, plan for more correspondence and tighter bookkeeping as revenue grows. Use this checkpoint before locking first-year pricing and monthly draw:

- Confirm your current service mix still supports your classification.

- Model two scenarios: no trade tax versus trade-tax exposure above the cited

24,500 EURprofit threshold. - Track revenue and profit monthly against the cited

800,000 EURand80,000 EURbookkeeping thresholds. - Keep registration letters, invoice templates, and tax settings aligned.

Separate personal spending assumptions from business-obligation planning in your notes. That small habit makes it easier to absorb added admin cost or bookkeeping changes without distorting your monthly draw decisions.

If your work clearly fits Katalogberufe and stays there, the freelance path is usually leaner. If your model is mixed or trade-leaning, budget like a trade business from day one and treat any lighter outcome as upside.

Mixed Activities Without Guesswork#

For mixed work, the core rule is simple: split treatment works only when freelance and trade activities are clearly separated in day-to-day operations and bookkeeping.

| Evaluation point | Cleanly separated lines | Intertwined lines |

|---|---|---|

| How the tax office can classify | Split treatment can be accepted when your activity description and evidence show two distinct lines. | The whole activity may be treated as Gewerbe, including retroactively. |

| Registration consequence | Classification may allow a split setup, with Finanzamt handling for the freelance line and Gewerbeamt registration where required for the trade line. | Classification can lead to handling both Finanzamt and Gewerbeamt requirements. |

| Operations expected | Separation is visible in banking, invoices, and records. | Blended banking, invoices, and records can weaken a split position. |

Practical separation means each line can stand on its own during review. Invoices, contract language, and bank records should point to the same line consistently. If that trail breaks, split treatment becomes harder to support.

Treat this as an evidence question, not a label question. Assess classification risk early and align your setup before filings drift out of sync. Use this allocation checklist before your next filing or invoice cycle:

- Service categories: assign each offer to either the freelance line or the trade line based on how the work is actually delivered.

- Contract language: keep scope wording specific to that line and avoid language that blends both lines into one package.

- Invoice logic: mirror the same split in line items and descriptions so records stay consistent over time.

- Supporting documents: retain qualifications, portfolio evidence, and contracts that support your declared activity description.

- Operations check: confirm banking, invoicing, and records all reflect the same separation.

If separation is not real in day-to-day execution, a split position is hard to defend. In that case, the tax office may treat the full activity as trade.

Red Flags That Lead to Reclassification Problems#

Reclassification risk goes up when your documents and day-to-day execution stop matching.

| Red flag | Why it raises risk |

|---|---|

| Contract scope or activity descriptions no longer match current delivery | Creates room for the relationship to be interpreted as employment-like. |

| Invoices that look like wages instead of project delivery | Weakens contractor-independence signals, especially without detailed line items. |

| Heavy dependence on one client | Can make a contractor relationship look closer to employment. |

| Day-to-day working patterns that resemble employment | Increases worker-misclassification risk. |

| Registration and invoicing no longer aligned | Signals compliance gaps and raises risk. |

One mismatch is a warning. Repeated mismatches across contracts, invoices, and registration records are a stronger trigger for immediate cleanup. Fixing that pattern early is usually the difference between a contained correction and a broader compliance problem.

In Germany, fake self-employment is treated as a serious compliance risk. Employment-like relationships, wage-like payment patterns, and single-client dependence are known warning patterns. Misclassifying workers as contractors can lead to severe penalties and tax liabilities.

If your work model changed materially, recheck classification before expanding clients or services in Germany. Use a regular internal consistency check with tax office requirements in mind:

- Match contract scope to the work you are delivering now.

- Confirm invoice detail supports contractor-style delivery, not payroll-style payments.

- Review client concentration and payment rhythm for employment-like patterns.

- Verify registration status and invoice language still point to the same classification setup.

- If mismatches repeat, treat that as a decision trigger and correct course early.

Evidence Pack to Keep Before the First Audit Request#

Build one evidence file now so your registration and tax trail is easy to verify before any audit request arrives.

| Evidence item | What to keep |

|---|---|

| Registration and tax setup | Gewerbeanmeldung confirmation from the Gewerbeamt, plus follow-up messages from the Finanzamt. |

| Tax form filing | A copy of the tax form and any confirmation letters/messages you received. |

| In-person submission proof (if used) | If you handed in the form personally to accelerate proceedings, keep proof of when and how you filed it. |

Keep this file in one place and name documents with the date first so the timeline is obvious at a glance. A simple year-month plus document type pattern is enough. The goal is quick retrieval when you need to explain what was filed and when.

For the Gewerbetreibender path, keep the official trail especially tight. Gewerbeanmeldung is done at the Gewerbeamt, and the tax office contacts you automatically after trade registration. Save those messages with clear dates and subjects. If you submitted the tax form in person to accelerate processing, keep proof of how and when you filed it.

Decision Checklist Before You Submit Your Next Invoice#

Before you send an invoice, confirm three basics: your current work still matches the category you operate under (Freiberufler or Gewerbetreibender), your registration with the local tax office is in place for your current setup, and your invoice setup matches your tax handling.

| Checkpoint | Invoice can go out | Pause and fix first | What to verify |

|---|---|---|---|

| Dominant activity | Your current revenue-driving work still aligns with the category you operate under (Freiberufler or Gewerbetreibender). | Your service mix changed and you are no longer confident the current category fits what you sell. | Current contracts, service descriptions, and invoice lines describe the same core activity. |

| Registration state | Your registration with the local tax office is complete for your current setup. | Your registration trail is incomplete or outdated for how you now operate. | Registration questionnaire status and related records for your current model. |

| Tax and invoicing setup | Your invoice template and tax handling are aligned. | Template, tax handling, or documentation conflict with each other. | Invoice fields, tax handling, and supporting records match current operations. |

| Uncertainty trigger | No open classification uncertainty remains. | Any item relies on guesswork or assumptions. | A short decision note on what changed, who reviewed it, and whether professional review is needed. |

Treat this checklist as your go/no-go gate for invoicing. If one row is unresolved, pause the cycle and log the reason in a short note. That habit prevents silent drift and creates a clean decision trail you can reference later.

If offers or your delivery model changed, treat that as a recheck point before the next billing cycle. When in doubt, pause invoicing and get professional review before scaling client volume.

When to Bring in a Tax Advisor#

Bring in a tax advisor as soon as classification uncertainty can affect registration or filing decisions. In these cases, small details can change the outcome, and Gewerbetreibender status can add obligations. Escalate early when classification confidence drops.

Do not wait until the situation becomes hard to untangle. Advisor input is most useful while your setup is still easy to adjust.

| Situation | Keep handling internally | Bring in a tax advisor now |

|---|---|---|

| Service profile | One clear activity line with stable delivery and matching documents. | Mixed activities or a recent shift in how you deliver work. |

| Category fit | You can clearly explain why your current work fits Freiberufler or Gewerbetreibender. | The classification is unclear, borderline, or disputed. |

| Obligation exposure | No signs that obligations changed. | Possible Gewerbe obligations, including Gewerbesteuer and possible IHK membership impact. |

| Decision confidence | Contracts, invoices, and filings tell one consistent story. | You are relying on conflicting non-official guidance. |

Go to the first call with a compact file so the advisor can test classification against what you actually do:

- Current activity description draft with primary and secondary revenue lines.

- Registration questionnaire and follow-up notes.

- Two to three recent sample invoices.

- A current contract set for your main client types.

- Prior tax-office letters.

Send the pack in advance if possible and keep your open questions as a short list. That keeps the call focused on decision points rather than document discovery.

Ask for a written rationale you can keep in your compliance file. Request plain-language reasoning and which facts would change the conclusion. Advisor input reduces ambiguity, but it does not guarantee a specific classification outcome.

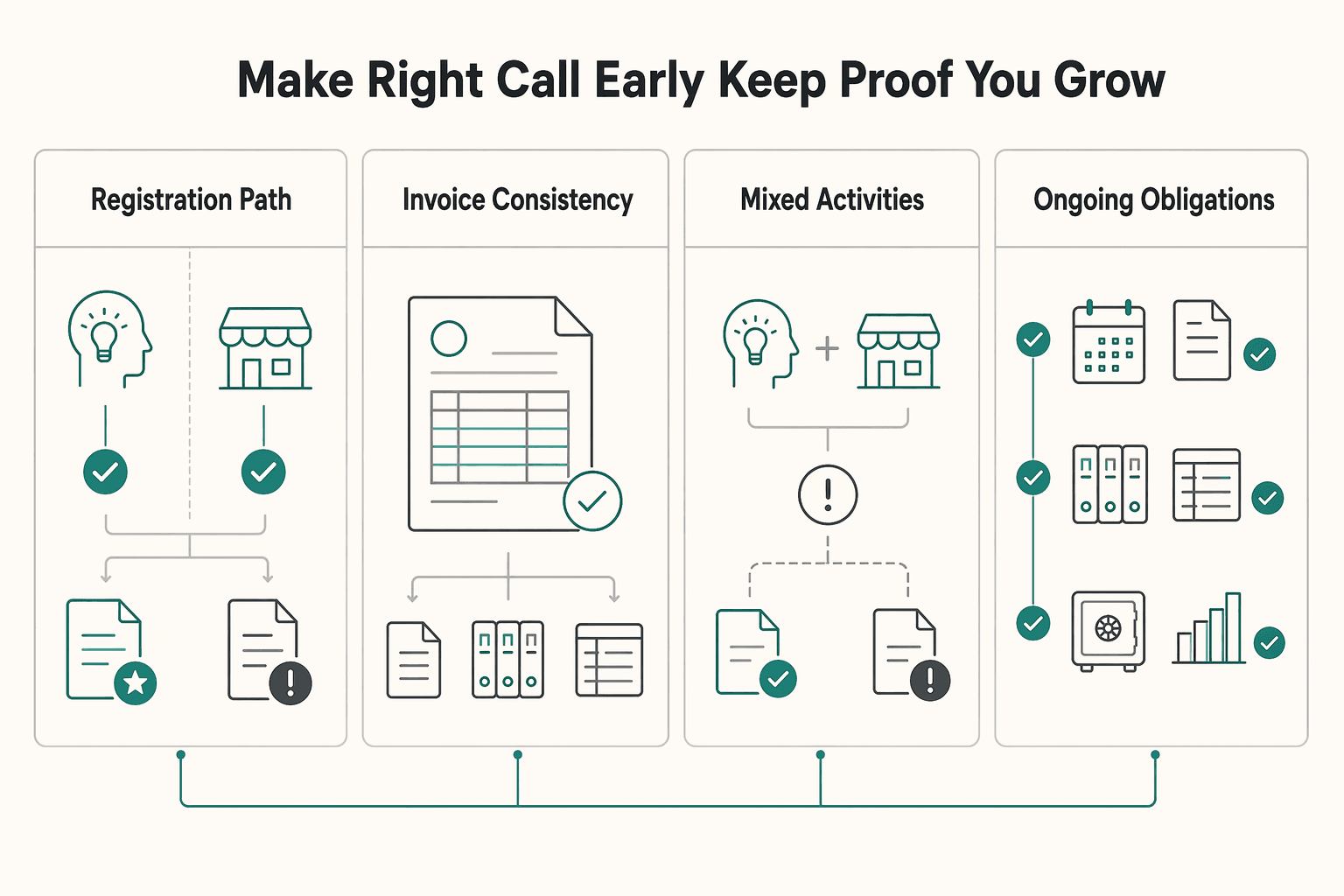

Make the Right Call Early and Keep Proof as You Grow#

Make the classification call early and keep filings, invoices, and records aligned from day one. Fixing a weak setup later usually means more admin and more tax uncertainty.

Freiberufler status is tied to personal intellectual services, while commercial activity is treated as Gewerbe. Classification is based on your activity description and evidence, not the label you prefer.

| Decision point | Early, aligned setup | Delayed cleanup |

|---|---|---|

| Registration path | Use the matching route from day one: Fragebogen zur steuerlichen Erfassung for freelance activity, or Gewerbeanmeldung at the Gewerbeamt for trade activity, then secure your Steuernummer before invoicing. | You may need to correct registration after invoicing has already started. |

| Invoice consistency | Service wording, invoice lines, and registration story stay consistent. | Mismatched wording across forms and invoices can trigger follow-up questions. |

| Mixed activities | Keep freelance and trade lines strictly separated in banking, invoices, and records. | If intertwined, authorities can treat the whole activity as trade, including retroactively. |

| Ongoing obligations | You can prepare for possible chamber notices and keep tax handling predictable. | New obligations can surface later, after volume has increased. |

Use this short action list now:

- Finalize one precise activity description and reuse it across contracts, filings, and invoice line items.

- Complete the correct registration sequence before scaling billing.

- Confirm your

Steuernummerbefore regular invoicing. - Maintain an evidence pack with dated filings, tax-office letters, sample invoices, and your current service description.

Keep this process light: one current activity description, one current invoice template, one current evidence folder, and one short decision note whenever something changes. Those four items help keep growth from outrunning compliance.

If activity is treated as trade, Gewerbesteuer for sole proprietors and partnerships is tied to annual profit above 24,500 EUR. The §35 EStG credit can reduce overlap with income tax, but not always fully, and bookkeeping may shift to double-entry after 800,000 EUR revenue or 80,000 EUR profit.

If your setup is mixed or unclear, get advisor confirmation now and base that review on documents, not assumptions. The practical pattern is simple: decide early, document the logic, and keep proof current as your business evolves. If you need help with the next step, Talk to Gruv.

Frequently Asked Questions

Can I choose `Freiberufler` status myself if it reduces admin work?

No. Status is decided by the tax office based on the nature of your services, not your preferred label. If your work is classified as trade activity, that classification controls.

What happens if `Finanzamt` disagrees with my filing classification?

The office classification governs your obligations. If activity is classified as Gewerbe, the trade registration route and related duties apply. Align filings and records to that classification so documentation stays consistent.

Do `Freiberufler` ever deal with `Gewerbesteuer` issues?

Gewerbesteuer is tied to trade activity, not pure freelance activity. For sole proprietors and partnerships, the cited threshold is annual profit above 24,500 EUR. In practice, both classification and profit level matter.

When is `Gewerbeanmeldung` at the `Gewerbeamt` required?

It is required when activity is classified as Gewerbe. For Freiberufler, the key registration step is the tax-office questionnaire, with no Gewerbeamt trip. For trade classification, registration starts with Gewerbeanmeldung at the Gewerbeamt.

Can one person be both `Freiberufler` and `Gewerbetreibender` through mixed activities?

Yes. Mixed activities can be split so one part is freelance and another part is trade. Keep both lines clearly separated in practice and bookkeeping.

Does using `Kleinunternehmerregelung` change whether I am `Freiberufler` or `Gewerbe`?

No. Kleinunternehmerregelung is based on turnover, not on whether activity is freelance or trade. Classification and VAT treatment are separate questions.

What documents should I keep to defend my classification later?

Keep records that show what services you actually provide, since service nature drives classification. Keep your submitted Fragebogen zur steuerlichen Erfassung and related filing records aligned with the classification applied by the tax office. For broader context, see A Deep Dive into Germany's Tax System for Freelancers.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- home-affairs.ec.europa.eu/system/files/2021-01/germany_start_ups_2020_...trusted

- oecd.org/germanytrusted

- blog.holvi.com/expat-guide-to-freelancing-freiberufler-vs-g...external

- blog.xolo.io/steps-to-start-working-as-a-freelancer-in-ge...external

- qonto.com/en/blog/freelancers/accounting/freelancer-vs...external

- taxfoundation.org/location/germanyexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Germany Freelance Tax Decisions for Globally Mobile Consultants

Set your German tax position first, then register and file. If you are a globally mobile consultant, a lower-risk approach is a clear decision order, not a tax shortcut.

The Best Analytics Tools for Your Freelance Website

Start with one sequence and keep it boring. Decide the business question. Choose one primary reporting source. Verify tracking against the origin. Then review it on the same day each week. That order matters more than which tool wins your shortlist.