Quick Answer

Use milestone escrow when your marketplace needs payment capture and payout to happen at different times and both sides need proof before funds move. It works best for phased, higher-risk transactions with clearly defined deliverables, approvers, evidence requirements, and release amounts. If milestones, review standards, or exception handling are vague, direct payout is usually simpler and less fragile.

When to Use Milestone-Based Escrow#

Use milestone escrow when your marketplace cannot treat payment capture and payout as the same event. If buyers need proof of work before release, and sellers need proof of funds before they begin, staged release through an escrow account is a workable middle ground. It also adds approval, evidence, and reconciliation work that your team has to run well.

This guide is for product, engineering, finance, and payments ops teams that need to evaluate the tradeoff in operational terms. The question is not whether staged release sounds safer. It is whether you can define milestones clearly, verify them consistently, and handle exceptions without turning a straightforward payout flow into a slower, more fragile one.

Step 1. Start with the real decision#

Milestone escrow means a neutral third party holds funds and releases them in stages as milestones are met. That can reduce risk and disputes because release timing is tied to milestone completion, not assumed trust. It is most useful when money should not move instantly just because a payment was captured.

Start with one checkpoint. Can both parties define milestones and payment schedules in a contract before funds are deposited? If milestone language is vague, release decisions will be vague too. A usable milestone should name the deliverable, review standard, approver, and release amount.

Step 2. Treat verification as an operating job, not a feature#

Verification is where this model succeeds or breaks down. The paying party deposits funds into escrow, work is delivered, and release follows review against agreed standards and requirements. That review step carries most of the operating load.

Keep an evidence record for every release decision: milestone reference, submitted deliverable, reviewer, review time, and acceptance or rejection notes. Without that record, dispute handling turns into guesswork.

A real-time dashboard helps only if it makes progress, payment schedule, and completion status visible to both sides. Your internal team needs that same visibility to resolve stalled releases before they turn into support escalations.

Step 3. Plan for delays and reconciliation before you build#

A practical failure mode is ordinary friction, not a dramatic edge case. Revision requests delay approval, approval delays release, and routine review lag becomes a support problem if you have not defined dispute windows and exception handling up front.

Plan for settlement complexity early as well. When one payment is split across sellers, partners, and platform fees, escrow becomes a reconciliation problem as much as a release problem.

That is the thread for the rest of this guide. First decide whether milestone release fits the transaction. Then define the funding model, the approval record, the controls, and the exception path that make it operable.

Decide if milestone escrow is the right model for this marketplace#

Use milestone escrow when release timing is a risk-control decision, not just a payout preference. If a transaction type needs clear proof before funds move, test a Milestone Transaction. If not, direct payout may be simpler.

Step 1. Score risk signals before vendor discussions#

Use this matrix as triage, not a hard rule. If several of these signals cluster, review a milestone model on purpose instead of defaulting to immediate payout.

| Risk signal | Why milestones may fit | What to confirm first |

|---|---|---|

| Multiple deliverables in one transaction | Milestones are designed as phased conditions tied to phased amounts | Can you define each release condition and amount up front? |

| Need proof before each release | Milestones can release funds phase by phase against agreed conditions | Who approves release, and what evidence do they review? |

| Funding-method constraints are likely | Escrow.com milestone flows generally ask for full pre-funding, and split funding is limited | Can buyers meet the funding method and timing constraints for typical order sizes? |

| Unclear control of funds and authority | Practitioner commentary warns that incorrect money-flow structuring can create operational problems | Is authority over funds timing and release explicitly defined? |

Step 2. Confirm the trust gap is about timing and proof#

This model helps when the buyer needs proof of work before release and the provider needs proof that funds are committed. It only works if each milestone is a defined condition tied to a defined amount.

Use a practical checkpoint here: can your team describe each phase with a clear acceptance condition and amount? Escrow.com describes milestones as phases with a defined parameter and corresponding dollar amount. If the work cannot be structured that way, milestone escrow is likely to add friction without solving the real issue.

Step 3. Rule out cases where escrow adds more friction than protection#

Do not force escrow into flows where milestone conditions, approvers, and exception handling are still vague. In those cases, the process can add friction without fixing the core operational gap.

Before you introduce escrow, name the approver, the evidence they will review, and the exception path when they disagree. If those are still unclear, the gap is not product-only. It is operational.

Step 4. Price the operational burden with real funding and fee mechanics#

Trust messaging is the easy part. You still own milestone definitions, approvals, evidence review, release decisions, and exceptions. Escrow.com shows the type of constraints to map early:

| Funding or fee point | Article detail |

|---|---|

| Buyer funding | Buyer is generally asked to fund the full transaction amount upfront. |

| Milestone funding timing | Milestone funding is available only after transaction creation and payment-method selection. |

| Funding methods by amount | Under $5,000, PayPal, credit, or debit card may be available; above $5,000, wire transfer only. |

| Split funding | Split funding is limited to cases where the buyer pays by wire transfer. |

| Incomplete funding | If total funds including fees are not received in full, funding can be delayed and may incur additional handling fees. |

| Fee allocation | Fee allocation can be buyer, seller, or 50/50. |

| Seller disbursement fees | Seller disbursement fees shown are $10 domestic wire, $20 international wire, and $0 for ACH disbursement. |

Final gate before rollout: be explicit about who controls funds, when release is authorized, and what evidence supports that authority. Commentary in RBI-context discussions warns that incorrect money-flow structuring can create serious operational fallout.

Pick the right funding and release model before you build#

Lock your funding and release model before you start API or UX work. In most cases, full pre-fund is the cleanest baseline when release timing is the control point. Staged funding should be an exception path you enable only when buyers can actually support its extra steps.

Step 1. Choose full pre-fund or staged funding on purpose#

Full pre-fund is the simpler starting point. In Escrow.com's milestone flow, the buyer is asked to fund the full transaction amount upfront. Milestone funding happens only after the transaction is created and a payment method is selected.

Staged funding needs tighter conditions. For milestone funding, split payment is accepted only when the buyer pays by wire transfer, and support involvement is required. If your buyers mostly expect self-serve PayPal or card flows, staged funding can create friction quickly.

Use one representative milestone transaction as a checkpoint. Confirm whether the buyer can fund the full amount upfront. If not, confirm that your staged path can actually operate with wire transfer plus support handling.

Step 2. Define rails by path, not by brand name#

Do not treat wire, PayPal, and ACH as interchangeable. Document each rail by funding limits and disbursement implications so product, ops, and finance are working from the same assumptions.

| Rail or path | What the sources support | What you should document |

|---|---|---|

| wire transfer | Required for milestone funding above $5,000; also required if the buyer wants split funding | Which buyer cohorts can fund by wire and whether staged funding is support-assisted |

| PayPal | Available for milestone funding under $5,000; PayPal defines domestic vs international by whether sender and receiver are in the same market | Your amount cap, market assumptions, and fallback when amount is above $5,000 |

| ACH | Supported as a seller disbursement path with $0 disbursement fee | Whether ACH is disbursement-only in your first release model |

Step 3. Set fee ownership before the first release#

Fee ownership needs to be fixed before the first live transaction. Buyer-paid, seller-paid, and 50/50 can affect milestone releases and downstream accounting differently.

Escrow.com supports each option. If the seller pays a share in a milestone setup, that portion can be deducted from the initial disbursement. Your release view should therefore show both the gross milestone value and the expected net payout.

Also model one failure path now: if full funds, including fees, are not received, funding can be delayed and additional handling fees may apply. Do not mark a milestone release-ready until fee collection, not just principal, is validated.

Step 4. Check ledger and release logic together before rollout#

Treat this as an internal control step. For one test transaction, reconcile funded principal, collected fees, and seller-disbursable balance after each state change. If provider status and your ledger do not match, fix that before rollout. Related: How to Pay US-Based Freelancers from the UK.

Gather the policy, people, and system inputs before step one#

Before you open build tickets, lock ownership, gating decisions, and system boundaries that can stop or reverse fund movement. A major execution risk is fragmented accountability, where no single owner can approve, block, or resolve a release path end to end.

Step 1. Assign named owners#

Create a lean role map with one accountable owner per decision surface, for example product, finance, disputes, and engineering. Keep it lean. If a review step exists, it should justify itself. A simple sanity check works well: one test workflow should move from request to completion without handoff ambiguity.

Step 2. List due-diligence and compliance gates by stage#

Document the due-diligence and compliance checks that can pause progress at each stage. Do not leave those decisions scattered across provider docs or legal threads. Teams need one visible stage-by-stage outcome: proceed, hold, or escalate.

For one representative workflow, confirm the exact status that blocks progression and the exact status that allows work to continue after approval.

Step 3. Freeze architecture boundaries#

Boundary decisions belong up front. Decide early which payment paths, integrations, and exception flows are in phase one. If scope is still uncertain, narrow phase one and document exclusions explicitly instead of half-building multiple paths.

Step 4. Define one shared traceability artifact#

Maintain one shared artifact for the lifecycle from request and approval through final accounting and export. It does not need to be complex. A simple table or diagram is enough if every team uses the same version.

The test is simple. Finance, ops, and engineering should all be able to point to the same record and explain why funds moved, who approved the action, and what should appear in export output. For a step-by-step walkthrough, see Material Procurement for Platforms: How Marketplaces Manage Raw Material Purchases and Supplier Payments.

Define milestones that can actually be verified#

A milestone is only useful if a reviewer can make a clear pass or fail decision from the record on one milestone transaction. If the evidence is unclear, keep funds locked and tighten the milestone before you scale the pattern.

Step 1. Write acceptance criteria as evidence tests#

Write milestones as evidence tests, not vague status labels. Define each one as a phase with a clear parameter and assigned amount. Tie it to a concrete deliverable such as a prototype, initial designs, or a key functionality implementation.

Then make the release test explicit: what must be submitted, and what standard must it meet for client approval? Client review against agreed standards is the checkpoint before funds should move.

Step 2. Keep one consistent submission record linked to the escrow account#

Use one repeatable record format for every submission tied to the related escrow account, so approvals are based on evidence rather than memory. Keep the submitted deliverable and review outcome together in that record. If revisions are needed, defer approval and release until adjustments are made. That keeps payment decisions aligned with completed, accepted work.

Step 3. Define release outcomes before you go live#

Set decision rules your team will apply every time:

- Evidence is incomplete or unclear: keep funds locked and request revisions.

- Evidence meets agreed standards: approve release.

- Evidence is mixed or contested: move to a documented exception path instead of ad hoc negotiation.

This keeps release decisions predictable.

Step 4. Confirm funding readiness before review and release#

Acceptance alone is not enough. Before final release decisions, confirm that the milestone is actually funded. Provider rules can affect this step. For example, Escrow.com requires transaction setup and payment-method selection before milestone funding. It also notes that incomplete full funding can delay fund application, add handling fees, or result in funds being refused.

A complete acceptance record matters, but funds can only move if the milestone amount is properly in place.

Build the escrow state machine and ledger postings#

Once milestone evidence is defined, make money movement rules explicit and auditable. Treat the escrow state machine and ledger as core product controls so each movement can be explained from system records.

The sources here do not validate one required escrow state sequence or ledger implementation, so treat the steps below as design choices for your own system.

Step 1. Model explicit states#

Use named states and allowed transitions instead of scattered flags. Keep one canonical status per milestone and one clear transition map that fits your model.

Keep payout eligibility explicit, and separate evidence review from release execution where useful. Store actor, triggering event, and evidence reference for each transition so the system can answer why a state changed.

Step 2. Separate held and contested balances#

Keep held and contested amounts clearly separated in both state and ledger definitions. Use consistent account naming in your own model, and reconcile from ledger records rather than status notes or app logs.

Step 3. Keep release/refund commands idempotent#

Design release and refund handling so one business instruction maps to one recorded outcome, even with retries or replays. Idempotency keys and single-commit patterns are options, but the sources here do not establish one required approach.

Step 4. Handle concurrency conflicts explicitly#

Define how concurrent actions are resolved in your implementation. Optimistic version checks or pessimistic locks are options; whichever approach you choose, fail conflicts clearly and retry against the latest milestone state.

Step 5. Post journals as source of truth#

One design option is to treat ledger journals as the accounting source of truth, then derive payout and wallet views from those records. Choose the ordering that best supports reconciliation and traceability in your system.

In a multi-vendor marketplace, sellers often control inventory, pricing, and fulfillment, while the operator typically focuses on platform technology, user experience, and commission model. That is one reason to keep the state machine and ledger explicit: existing rails are often good enough in practice, and no single rail fits every payment context.

We covered this in detail in How to Build a Milestone-Based Payment System for a Project Marketplace.

Implement release, refund, and partial reversal rules#

Release, refund, and partial reversal should behave like one settlement policy, not three separate one-offs. If you treat them separately, the hard cases expose gaps between policy, ledger, and payout behavior.

Step 1. Define fee timing for release/refund outcomes#

Define how fee impact is recognized when release or refund outcomes occur, and apply that rule consistently. Your ledger should reflect the final operational outcome of the path that actually occurred.

Before launch, map each supported path across capture, split, payout, and possible reversal. For each one, confirm finance can explain from system records what fee was recognized and how it differs from the original funding view.

Step 2. Define partial reversal rules before launch#

Partial outcomes need predefined rules, not case-by-case handling. If your policy supports hold, split, and refund actions, encode partial release and reversal behavior directly in those rules.

You do not need a universal formula, but you do need one documented method applied consistently on your platform. Record principal and fee effects in the same auditable chain so accepted and reversed portions reconcile to the customer outcome.

Step 3. Set trigger ownership and override boundaries#

Assign release, refund, and override authority explicitly by party and event. Map responsibilities to recognized transaction parties, such as seller, buyer, and broker, and then layer internal roles on top with clear permissions.

Define who can trigger release, who can trigger refund, and when admin override is allowed. Add a terms-version checkpoint in your policy review so permissions are tied to the governing terms in force when the transaction is processed.

Step 4. Restrict manual edits to incident protocol only#

Default to standard release/refund system paths, and treat back-office edits as incident-only exceptions. If exceptions are necessary, route them through an incident protocol with a full audit trace so they remain linked to the original transaction chain. That keeps balances, approvals, and journal outcomes aligned instead of drifting into manual side fixes that are hard to reconcile later.

Set dispute and exception operations before launch#

Disputes and exceptions should pause automated fund movement until a human resolves the case in your defined workflow. If evidence is challenged or payout execution fails, the transaction should leave normal automation and enter controlled review.

Because marketplace "escrow" can mean delayed split payouts or legally segregated wallets, align this workflow to the model you actually run.

Step 1. Freeze disputed items at the first credible signal#

Treat a dispute as a state change, not a side comment. Freeze the impacted amount so release and payout automation does not continue on that item until manual resolution approval is recorded.

This matters because escrow flows are multi-party and trigger-based. Without a clear freeze control, exception handling can spill into manual work, which raises error risk and slows operations. Before launch, confirm you have review queues, audit trails, and alerts in place for every disputed case.

Verification point: open a dispute on a test milestone that is approved for release but not yet paid. Confirm automated release and payout actions are blocked and the case appears in a visible manual review queue with a full event trail.

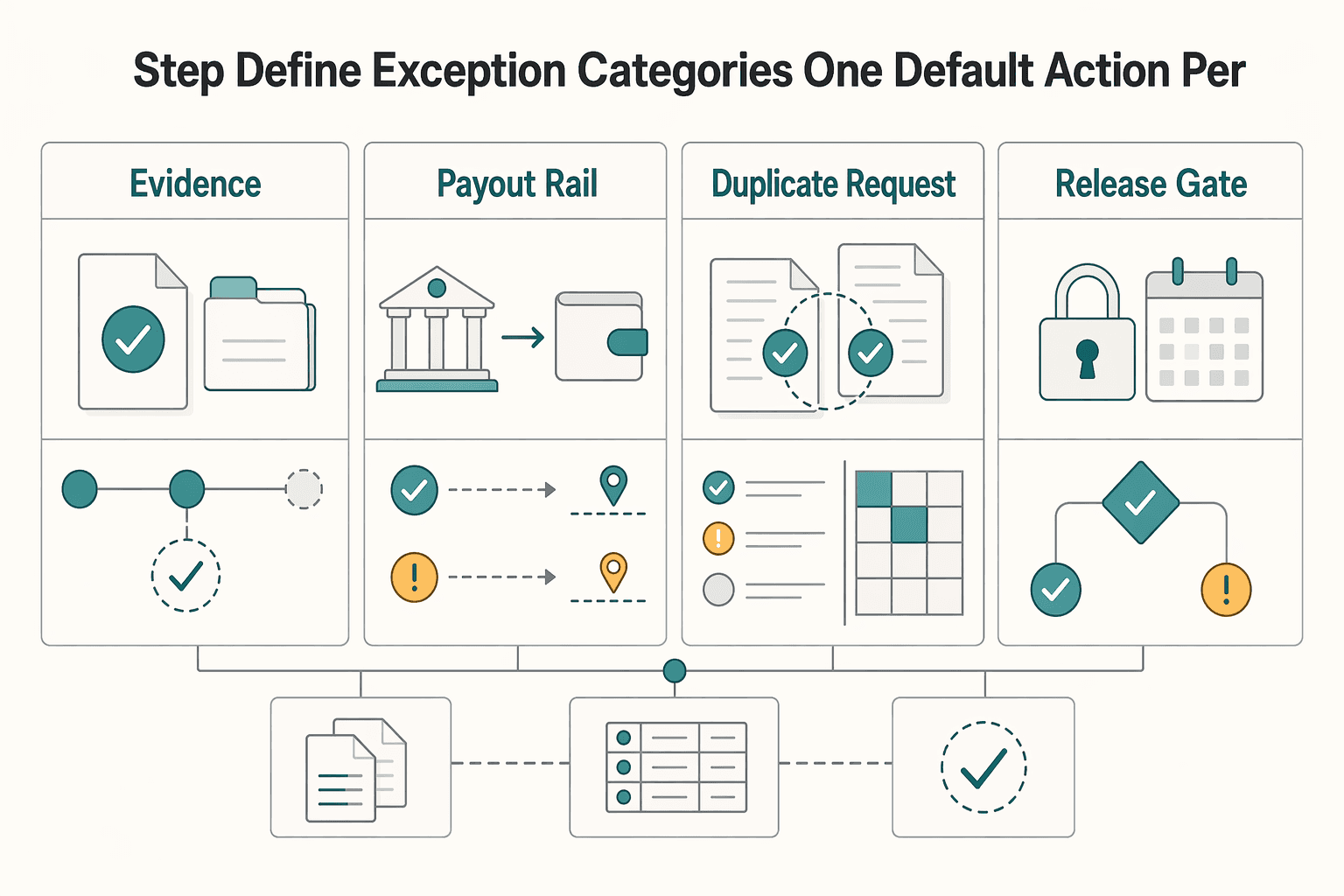

Step 2. Define exception categories with one default action per category#

Do not launch with a single generic "payment exception" bucket. Name categories so ops and finance can triage consistently and apply the right next action.

| Exception category | When it applies | Default action |

|---|---|---|

| Unmatched evidence | Submitted proof does not clearly meet the acceptance rule. | Route to manual review and require a new reviewer decision or platform attestation before funds move. |

| Payout rail failure | Payout execution fails. | Move the case to exception review and require ops confirmation before any further payout action. |

| Duplicate request attempt | The same release, refund, or dispute action is submitted again. | Block duplicate progression and investigate when prior state is unclear. |

| Stale approval | An approval is no longer current for the transaction state. | Require re-approval before release or payout continues. |

For every exception, keep a complete evidence packet and event trail, including the approval or attestation tied to the last state change. If that record is incomplete, the case is not ready for resolution.

Step 3. Set escalation rules before launch#

Set your escalation matrix before launch so intervention is predictable. Define who is alerted when a case remains open, when higher approval authority is required, and when finance joins the path.

Use clear risk signals, such as case age and funds at risk, so lower-risk exceptions stay in standard review while older or higher-risk cases escalate earlier. Where release conditions depend on off-chain events, define how verification is handled, for example platform attestation, oracle services, or cryptographic proofs, before funds move.

Verification point: run one lower-risk and one higher-risk exception test. Confirm alerts, approvals, and queue history behave as designed, and confirm exceptions cannot be resolved through informal back-office work outside recorded review and audit trails. This pairs well with our guide on Accounts Receivable Cycle for Marketplaces: How to Track Buyer Payments Through to Seller Disbursement.

Wire compliance and tax gates into payout timing#

Keep release and payout as separate states. A milestone can be accepted and marked payable while payout still waits for a current readiness check under your internal policy.

Step 1. Separate release approval from payout readiness#

Treat payout readiness as an execution-time internal check, not a one-time onboarding result. If compliance status changes after release approval, you can pause payout and route the case to review, but that routing is a program-policy choice, not a rule established by FEIE/FBAR guidance.

Step 2. Apply VAT checks only where your program supports them#

Use VAT validation as a pre-payout checkpoint only in markets and programs where your own controls support it. Record a clear outcome state, such as passed, failed, unavailable, or not applicable, so operations can act without assuming coverage that does not exist.

Step 3. Record tax form status as auditable readiness evidence#

Capture tax documentation workflow status for W-8, W-9, and Form 1099 handling as structured, masked, auditable records. Keep status, timestamps, and provenance in the payout record so the decision can be reviewed later, and treat these records as operational evidence rather than source-defined payout-release gates.

Step 4. Keep FEIE and FBAR in reporting support, not payout logic#

Do not use FEIE or FBAR status as direct milestone release or payout decision logic. FEIE applies only to qualifying individuals with foreign earned income, and excluded income is still reported on a U.S. return; FEIE is claimed on Form 2555 or 2555-EZ.

If you provide tax-adjacent exports, keep them focused on reporting support. For FEIE context, the physical presence test uses 330 full days in 12 consecutive months, and a full day is 24 consecutive hours; missing the day count can fail qualification even with common disruptions. For FBAR, keep due-date and extension-support artifacts where enabled, rather than turning FBAR into a payout gate.

Run go-live verification and failure drills#

Before launch, run failure-condition checks, not just clean-path demos. This is where you prove the model is operable.

Step 1. Test the transitions you actually expose#

Use the states and actions in your live product, then test each allowed transition end to end. Keep auditable evidence for each test so a reviewer can trace the request and the recorded outcome.

Step 2. Drill retries and conflicting actions intentionally#

Run replay and collision scenarios on purpose, including duplicate requests and near-simultaneous conflicting actions. Define expected outcomes before each drill and confirm the system reaches one consistent final result.

Step 3. Pressure-test async handling, and raise the bar for onchain logic#

Include asynchronous event handling in repeatable drills.

If your flow uses blockchain or smart contracts, include controls aligned to the known risk profile. Use rigorous secure development lifecycle work to reduce vulnerabilities, including reentrancy and oracle exploit classes. Also check throughput, privacy, and key-management tradeoffs explicitly.

Step 4. Verify guidance freshness before control sign-off#

Do not rely only on bookmarked SEC CFI references from earlier reviews. The SEC consolidated CFI page states it is currently out of date due to technical issues and directs readers to the main CFI page for current links. Record the page checked and the date marker used, since the SEC notes that each CFI's bracketed date is its latest publication or revision date.

Use concrete markers in your sign-off evidence when relevant. For example, the consolidated page shows July 1, 2025, while a subsection is marked UPDATED 03/19/26.

Step 5. Run an evidence-based launch decision#

Before launch, hold one evidence review where owners can trace sample scenarios from request through final recorded outcome without guesswork. If that trace is not clear, fix controls first, then rerun the drill. Related reading: How to Use Performance-Based Pricing for Your Freelance Services. Before go-live, align your retry and status runbooks with your implementation team using Gruv Docs.

Common mistakes and how to recover fast#

When something breaks, recover in this order: stop new money movement, isolate the failed control, then repair records before reopening payouts. That sequence matters because this is not plug-and-play. The release path combines compliance handling, including Travel Rule requirements across jurisdictions, with multi-party flow architecture, so rushed patches can create additional failures.

Step 1. Pause unclear release definitions at intake#

If your team cannot clearly explain what should trigger release, pause new deals that use that pattern. Keep the exact acceptance and evidence mechanics in your internal runbook, since those details are implementation-specific.

Step 2. Put compliance checks back before payout dispatch#

If compliance handling is being bypassed, stop payout dispatch and restore required checks before resuming. This is a core implementation checkpoint, not an optional extra.

Delays already put pressure on seller cash flow, and traditional settlement can stretch to 7 to 14 days. Reopening payouts before controls are stable can increase operational risk.

Step 3. Stop inconsistent outcomes during retries and replays#

If retries or replayed events can produce conflicting payout outcomes, keep payouts closed until behavior is consistent. The exact duplicate-prevention and repair mechanics depend on your system design.

Step 4. Reconcile records and reporting before full reopen#

Before full reopen, verify that payout records and operational reporting reflect the same current state. Exact dispute-handling and reporting mechanics are system-specific and should follow your internal controls.

Conclude with a clear next step#

Your launch bar is proof, not feature completion. You should be able to explain why funds moved, who approved them, and what record supports that decision.

Step 1#

Start with one constrained cohort and treat it as due diligence, not a broad rollout. Keep scope tight enough that exceptions are reviewed directly and resolved from records, not reconstructed later. If approval evidence is incomplete or decision trails break, pause expansion.

Step 2#

Keep one governed launch artifact as the source of truth for what policy controls were active at go-live. At minimum, track document-control fields such as version, change number, and effective date; that control style is explicitly shown in AFARS metadata (Change Number 2025-0711, Effective Date 07/11/2025). Record negative findings as launch gates, not footnotes, and address them before widening eligibility.

Step 3#

Expand only after repeated cycles are stable across your review process and reconciliation records. Use your own thresholds, but require consistent performance over time rather than one clean period. If routine cases still need manual rescue or evidence gaps remain, keep the cohort small.

Use this final gate checklist:

- Due diligence activities completed for the cohort

- Launch artifact includes version, change number, and effective date

- Adverse findings logged and addressed before expansion

- Approval and decision trails are complete and auditable

- Cohort review passed before widening eligibility

If market coverage or rail assumptions affect your rollout, confirm scope and support directly before expanding. If you want to validate rollout constraints for your flow, talk to Gruv.

Frequently Asked Questions

What is milestone-based escrow in a marketplace?

Milestone-based escrow releases funds in stages as each defined milestone is approved or otherwise triggered. The transaction is split into phases with clear parameters and linked amounts. Keep enough audit-trail detail so disputes can be reviewed from the record.

When should we use milestone release instead of immediate payout?

Use milestone release when delivery is delayed, phased, or more likely to be disputed, especially in higher-value, service-heavy transactions. It is most useful when both sides need stronger trust controls before money moves. For lower-friction transactions with lower dispute risk, immediate payout is usually simpler to operate.

How do we prevent double release or orphaned funds?

Treat this as a core systems control. Protect release and refund paths with atomic database transactions and concurrency safeguards such as optimistic concurrency control or pessimistic locking. When conflicting actions hit the same held balance, one action should complete and the other should fail with a clear conflict outcome.

Who should approve milestone releases?

Set clear approval roles in policy, and use multi-party approval workflows when risk or complexity is higher. There is no universal minimum approver set in the article. Match the approver chain to the transaction risk and your control model.

How should partial refunds work?

Handle partial refunds as explicit, traceable ledger events rather than ad hoc adjustments. Use one documented reversal method consistently, and record principal and fee effects in the same audit trail. That keeps each adjustment reviewable and reconcilable.

What must be verified before go-live?

Verify that concurrent or retried release and refund actions cannot create double release or orphaned funds. Verify that disputed amounts move to a dedicated disputed funds account so automated payout flows cannot touch them before manual resolution. Verify that your audit trail captures granular transaction details suitable for later dispute or examiner review.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/afars/chapter-5-definitionstrusted

- calosba.ca.gov/for-small-businesses-and-non-profits/permits...trusted

- files.consumerfinance.gov/f/documents/cfpb_final-rule_general-use-digi...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- media.defense.gov/2025/Nov/10/2003819439/-1/-1/1/TRANSFORMING-...trusted

- public-inspection.federalregister.gov/2026-05350.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: