Quick Answer

Separate the decision into recognition software and payout execution, then buy only after operating proof is on the table. Ask for a country-by-method matrix, a reconciliation export with payout IDs and provider references, and clear cost drivers beyond per-reward pricing. Runa and Tremendous both show broad option coverage publicly, but those disclosures do not confirm your exact market-method path. Pick the vendor your finance team can model, your product team can instrument, and your support team can run when failures occur.

What changes when recognition payouts scale#

Treat recognition software and payout delivery as two separate buying decisions. If your team will own disbursement outcomes, start with finance and operations, not the reward catalog. That matters even more for global programs, where cross-border execution, multi-currency budgets, and payout-choice expectations can turn a simple recognition launch into a margin and support problem.

The market already shows the split. Tremendous positions itself as a "reward and payout platform" that can send gift cards, prepaid cards, monetary options, and donations, and it advertises recipient reach in over 200 countries. Runa markets broader payout infrastructure. Runa Send claims 5,000+ payout options across 190 countries. Runa Payout Link says recipients can choose how to redeem and cites reach across 30+ countries, 20 currencies, and 16+ languages. Those are useful signals, but they are still marketing disclosures, not proof that a given country, method, or settlement path will work for your exact program.

That is why this article looks at these options through a finance and operations lens, not a feature-list lens. A vendor can look strong because it has a large reward count, familiar brands, or polished recognition workflows. None of that tells you enough about payout method depth, FX exposure, reconciliation effort, or what happens when a recipient needs a locally relevant option instead of a gift card. Before you get attached to any platform demo, ask for three concrete things:

- A country-by-method support matrix, not just "global" coverage language. You want to see where gift cards, wallet-style options, prepaid cards, bank or debit transfers, and recipient-choice flows are actually supported.

- A sample audit and reconciliation pack. At minimum, that means payout IDs, provider references, status changes, and an export finance can tie back to program events.

- Commercial detail beyond per-reward pricing. If your economics depend on cross-border delivery, you need to understand what drives cost when recipients choose different methods or when only part of an issued balance is used.

A common failure mode is buying for recognition UX first, then discovering later that broad catalogs do not always equal reliable disbursement coverage, or that finance cannot model gross-to-net payout cost by market. Support load can rise when recipients cannot redeem through a preferred method, and the cleanup often lands with product, HR, and finance together.

The goal here is simple: help you decide which option fits your monetization model, operating capacity, and cross-border payout reality. We will compare recognition vendors and payout infrastructure on the things that actually determine whether the program scales cleanly: coverage depth, unit economics clarity, integration ownership, reconciliation controls, and failure handling.

Who this list is for and how we will judge options#

This list is for teams that own payout outcomes after a reward is issued, not just recognition UX. It is built for founders, product leaders, and finance operators choosing between recognition-led tools like Kudos and payout-led infrastructure like Runa for HR, which is positioned around real-time payouts for HR platforms.

| Criterion | What it covers |

|---|---|

| Payout coverage depth | Whether the vendor can show country-by-method support for the payout types you need. |

| Unit economics clarity | Whether finance can model cost drivers before launch instead of learning them in production. |

| Integration effort | What product and engineering must build, test, and maintain. |

| Reconciliation controls | Whether program events can be tied to payout records with usable exports and references. |

| Failure handling | What support and resolution look like when payout events do not go as expected. |

Those five criteria run through every option in this list.

Gartner is useful as category framing, not proof of payout fit. The Employee Recognition and Reward Systems market is broad (shown as "Products 1 - 20 of 33"), so labels alone do not establish payout accountability.

That split matters in practice. Bonusly is positioned around peer recognition with points redemption, and Achievers emphasizes engagement, retention, and performance outcomes. If your goal is mainly culture and engagement, those tools may fit. If you own disbursement outcomes, validate payout evidence early with concrete operating proof.

Related: How to Create an Employee Recognition Program.

Best employee recognition payout options by operating need#

If payout accountability is the deciding factor, separate vendors by operating fit: choose payout-led infrastructure first, then test recognition suites for disbursement proof before procurement.

| Option | Best for | Publicly disclosed endpoint types | Global coverage disclosure | Integration ownership clue | Reconciliation evidence on cited pages | Commercial model clarity on cited pages |

|---|---|---|---|---|---|---|

| Runa | Embedded global payout choice | Gift cards, bank transfers, and open-balance choice via Runa Payout Link across currencies, brands, and payout types | 5,000+ payout options across 190 countries | "One integration and contract" | Not shown in cited pages | Limited in cited excerpts |

| Tremendous | Fast incentive catalog rollout | Gift cards, prepaid cards, monetary options, and donations | Worldwide positioning, but no country-by-method matrix in cited pages | Reward and payout scope is clear; detailed ownership model is not | Not shown in cited pages | Limited in cited excerpts |

| Kudos plus payout partner | Recognition-first stack with partner-led rewards | Depends on partner; not established on the cited Kudos page | Not established on cited page | Kudos-side HRIS integration is clear; payout responsibilities must be mapped separately | Not shown in cited pages | Depends on partner structure |

| Recognition-suite cohort | Engagement-first shortlist building | Varies; WorkTango cites 10M+ options, but rail types are not established across the cohort in cited sources | Uneven from cited sources | Requires vendor-specific diligence | Not shown in cited pages | Uneven from cited sources |

- Runa is the strongest fit when you need embedded payout choice at global scale. Public pages are specific: one integration and contract, 5,000+ payout options across 190 countries, plus Runa Payout Link for open-balance recipient choice across currencies, brands, and payout types.

Use a hard gate before selection: request country-by-method coverage for your launch markets and a sample payout-status export. The open issues in the cited material are cost and implementation detail.

- Tremendous is the practical fit when launch speed and broad choice matter most. Its scope is clearly positioned as rewards and payouts, including gift cards, prepaid cards, monetary options, and donations, with 2,000+ options and 24K+ businesses cited publicly.

That supports fast rollout use cases. For deeper payout operations, confirm architecture, controls, and reconciliation outputs directly because those details are limited on the cited pages.

- Kudos plus a payout partner fits teams that prioritize recognition UX first. The cited proof is on HR system connectivity: Kudos states it integrates easily with HRIS platforms.

Treat payout as a separate diligence track. Before you sign, define ownership for payout IDs, exception handling, and ledger-ready exports if finance close requirements are in scope.

- The recognition-suite cohort is best used for engagement-first shortlist creation, not automatic payout selection. Category breadth is real (for example, Gartner market coverage and G2 category listings), and WorkTango's 10M+ options claim signals reward marketplace scale.

Still, the cited sources do not establish equivalent disbursement rails, reconciliation depth, or commercial mechanics across the cohort, so move vendors forward only after payout-specific proof.

Payout coverage details that matter more than reward count#

Reward count is a weak selection filter. Coverage is about which payout methods work in each market, with clear caveats when a method is unavailable.

- Start with endpoint types, then assess scale.

Compare method classes before logos or headline counts. Runa publicly lists gift cards, prepaid cards, and direct-to-card payments in 190+ countries, and Runa Payout Link supports balances that can be split across currencies, brands, and payout types. Tremendous also states multiple endpoint classes, including gift cards, prepaid cards, monetary options, and donations. None of that replaces a country-by-method confirmation for your launch scope.

- Treat catalog brands as appeal signals, not disbursement proof.

Brands such as Edenred, Sodexo, Pluxee, and Perkbox can help with recipient appeal, but they do not prove payout reliability. Reward Gateway's recipient messaging focuses on where rewards can be spent or redeemed, and Pluxee messaging emphasizes merchant-network usage. That is useful for catalog evaluation, not settlement behavior, exception handling, or reconciliation quality.

- Require country-by-method matrices before rollout.

Ask vendors for dated support tables by method class and country, with explicit "where supported" notes. For Tremendous, include redemption-region behavior (options shown by recipient country) and restricted-country caveats tied to banking regulations. This avoids launching on broad claims like "more than 200 countries" or "2,000+ options" and then discovering method gaps at redemption.

| Vendor or layer | Launch markets | Blocked markets | Fallback methods | User communication rules |

|---|---|---|---|---|

| Runa | Only countries where gift card, prepaid, or direct-to-card support is vendor-confirmed | Not established publicly by country in the cited pages | Use Runa Payout Link where supported to preserve recipient choice across payout types | Do not promise the same method everywhere |

| Tremendous | Only countries where the needed option class is confirmed at redemption | Require the restricted-country list because some sends are prohibited by banking regulations | Expect country-dependent option sets and define an alternate method before launch | Tell recipients options may vary by country and are shown at redemption |

| Catalog-brand layer only | Treat as non-launch proof until the payout provider confirms send capability | Unknown until the underlying provider shares support tables | Use another verified method or exclude the market | Say where rewards can be redeemed, not that payout is available in all markets |

Related reading: Accounts Receivable Automation for Platforms to Collect from Enterprise Buyers at Scale.

Unit economics and pricing tradeoffs before you sign#

Price the exact payout paths you plan to use, not a headline per-reward fee. If finance cannot model gross-to-net payout cost by segment, pause selection even if a vendor scores well in recognition-market evaluations.

- Funding flow can be the first hidden fee.

Per-reward pricing is only one layer. Tremendous publicly says "No minimums or subscriptions," but it also says credit cards may incur a 3% processing fee, so unit economics can change before disbursement starts. Keep funding method and payout method separate in your model, and ask for a sample invoice or fee exhibit that breaks out card funding, payout charges, and other transaction lines.

- Payout method mix usually drives more cost than the platform headline.

Public pricing can vary sharply by method: gift cards, prepaid cards, or donations are listed as free, while Venmo, PayPal, Cash App, and bank transfers may incur a 4-6% fee. Model your likely future mix by country, payout type, and funding method before approval, especially if you may add more cash-like options over time.

- Cross-border and FX costs can stack across the flow.

Stripe documents that FX can occur in payments, transfers, payouts, application fees, and other transaction types. Stripe Global Payouts also publishes a cross-border layer of 0.25-1.25% plus 0.50% conversion for USD/EUR/GBP, with no cross-border fee for intra-Eurozone transfers. If cross-border disbursement is part of your margin model, prefer vendors that expose these drivers clearly up front.

- Operational overhead belongs in total cost, even when not shown as a fee line.

Support and reconciliation work affect margin. Tremendous explicitly references a "Dedicated recipient support team" and "Financial reporting reconciliation," so treat those as evaluation items, not back-office assumptions. Request a current pricing sheet or contract exhibit, a sample reconciliation export, and an exceptions list for failed or delayed rewards.

| Cost factor | Public signal you can use now | What to model before signature |

|---|---|---|

| Fixed fees | Tremendous says "No minimums or subscriptions." Public pages for other vendors may not disclose minimum commits. | Separate platform access cost from transaction cost. Mark non-public contract terms as unknown until paper review. |

| Variable fees | One platform says gift cards, prepaid cards, and donations are free, while some monetary methods may incur 4-6%. Stripe Connect publishes one path at 0.25% + 25¢ per payout sent. | Build segment models by payout type, currency, and average reward value. |

| FX treatment | Stripe says FX can occur in payments, transfers, payouts, and fees. Global Payouts shows 0.25-1.25% cross-border plus 0.50% conversion for some pairs. | Map each currency handoff from funding to recipient receipt. Do not assume a single conversion event. |

| Contract lock-ins | Public pricing may show no subscription, but often does not confirm minimum commits, term length, or termination rights. | Require contract review before final selection. Treat unknown lock-ins as commercial risk. |

| Operational overhead assumptions | Some vendors explicitly mention recipient support and financial reporting reconciliation. | Estimate support touch rate, finance review time, and exception-handling cost per 1,000 payouts. |

The practical tradeoff is recognition-first procurement versus payout-first design. Recognition-first can launch faster, but payout-first usually gives you better long-run margin control because country, currency, funding, and support assumptions are priced before scale.

Integration ownership and implementation order for product and finance#

Assign ownership before vendor selection, or integration risk will spill across teams. Define who owns payout initiation, status truth, exception triage, and month-end reconciliation before any API work starts.

- Set owners by payout moment, not department label.

Product should own when a reward becomes payable and what users see at each status. Engineering should own request handling, retry safety, webhook consumption, and status mapping. Finance should own exception rules and close-period reconciliation. A short ownership map for initiation, async status updates, failed or delayed payouts, and reconciliation is usually enough to expose gaps early.

- Require proof of retry safety and webhook reliability.

Do not accept "we support webhooks" as proof. For initiation, require idempotent request behavior: Stripe supports idempotency for safe retries, and Tremendous requires a unique idempotency key for each topup so it is performed only once. For events, require an operational status surface and attempt-level diagnostics. Stripe shows Delivered, Pending, and Failed deliveries, including prior HTTP status codes and future retry timing. Retry behavior also differs by environment: Stripe retries live deliveries for up to 3 days, but sandbox retries three times over a few hours. Tremendous also retries failed webhook deliveries up to 17 times with exponential backoff and expects an HTTP 200 response.

- Sequence rollout in stages, then expand to recognition tools.

Start with sandbox testing, then a limited pilot, then production guardrails, then broader rollout into tools like Kudos or Awardco. Tremendous documents a fully featured Sandbox and an explicit switch to production credentials when ready to go live, and Stripe test keys are intended for testing without affecting live data. In sandbox and pilot, test failure paths, simulate webhook events, and confirm your endpoint returns success codes consistently. Expand only after your team can trace each initiated payout to final status without manual stitching across messages and spreadsheets.

For a step-by-step walkthrough, see Automating B2B Rebate Calculations and Disbursements for Platforms.

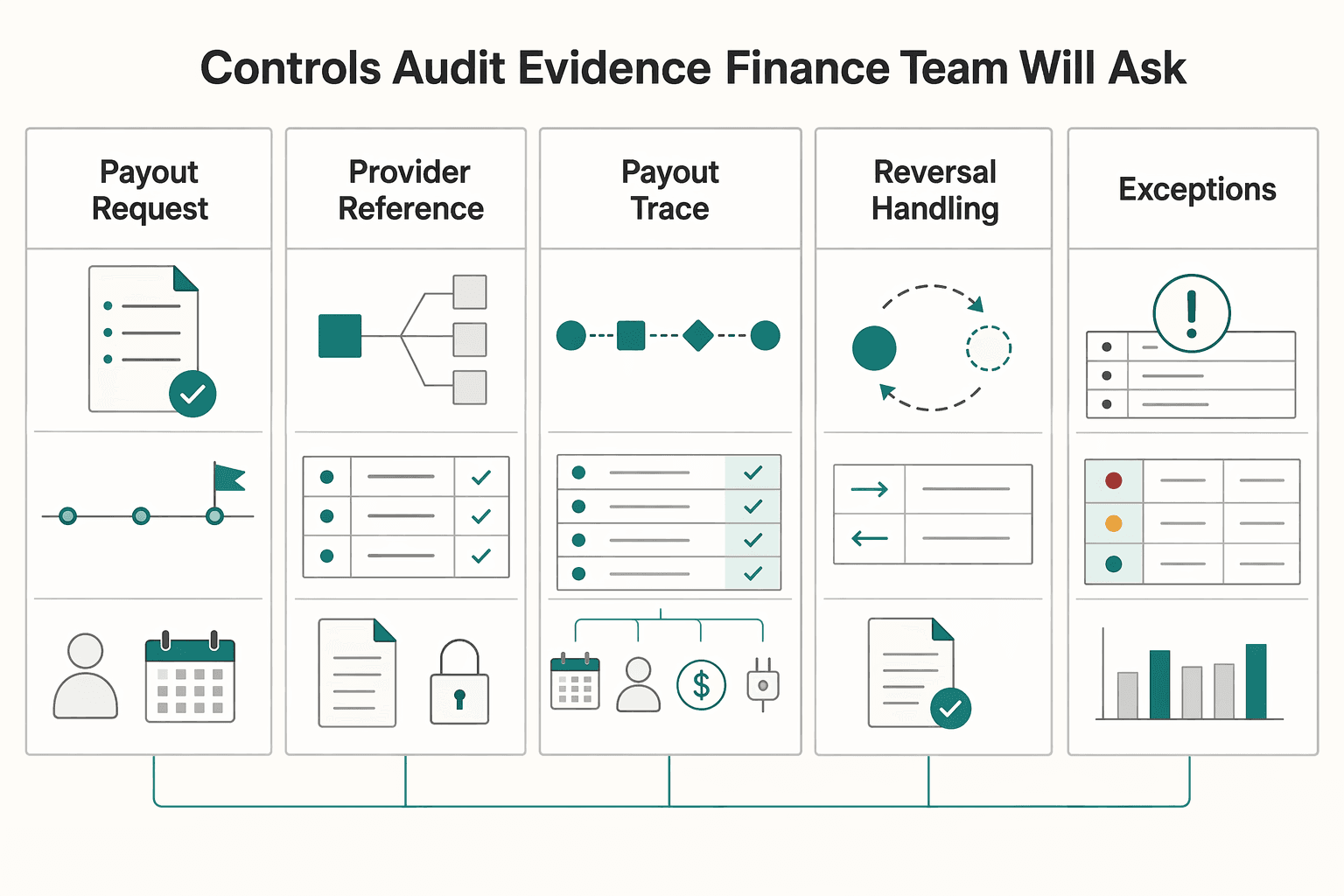

Controls and audit evidence your finance team will ask for#

Finance will ask for evidence, not interface polish. Your setup is only launch-ready when each recognition event is traceable, approvable, payable, reversible when needed, and reportable without spreadsheet stitching.

| Artifact | Why it matters |

|---|---|

| Payout request trail | Lets the team trace one reward from request to payout. |

| Provider reference mapping | Helps verify each handoff has an external reference. |

| Ledger-ready exports | Supports reporting without spreadsheet stitching. |

| Reversal handling | Shows whether a reward can be reversible when needed. |

| Exception logs | Provides evidence for investigating payout issues. |

- Ask for an audit evidence pack, not just a dashboard.

Request five artifacts up front: payout request trail, provider reference mapping, ledger-ready exports, reversal handling, and exception logs. If the vendor affects controls tied to your financial reporting, ask whether they have SOC 1 coverage or a clear plan to obtain it. A quick test is to trace one reward from request to payout and verify each handoff has a timestamp, actor, amount, and external reference.

- Prove approval controls before high-value rewards go live.

Do not assume a recognition suite has the approval behavior you need. Confirm who can approve, whether approval responsibility is explicitly assignable, what happens when an approver is unavailable, and whether edits after approval trigger re-approval. Treat it as a control gap if a requester can bypass approval or if the trail does not preserve the original amount and approver.

- Reconcile by payout method and partner, not by catalog size.

Method breadth increases control complexity, so finance needs method-level evidence instead of a single "rewards sent" total. If your catalog includes partners such as Edenred or Pluxee, confirm how each payout appears in exports and whether cards, wallets, and prepaid rails follow the same reconciliation path or separate ones. Also verify that reports include refunds, deposits, and order payments, since those are core reconciliation inputs.

- Set a hard go-live gate tied to close readiness.

Do not launch until finance can tie a program event to the disbursement event and close the reporting loop without manual patchwork. In practice, test webhook event notifications over HTTPS, match those events to payout reconciliation batches or CSV exports, and then to ledger posting. Include at least one exception case, for example a reversal or failed payout, in pilot validation.

If control design is part of your rollout, see Internal Controls for AP Platforms to Prevent Fraudulent Disbursements.

Failure handling and support model before scale#

If you cannot classify, measure, and route payout failures, keep the program in pilot.

| Failure test | Grounded example | What to verify |

|---|---|---|

| Expired links | Runa RE004 (expired link) | Verify the user message, internal status, retry behavior, and whether finance can match the same external reference in exports. |

| Endpoint eligibility failures | Push-to-card eligibility limits (Visa or Mastercard debit card only) | Verify the user message, internal status, retry behavior, and whether finance can match the same external reference in exports. |

| Delayed provider recovery | Runa RE006 with a documented 24-48 hour recovery window | Verify the user message, internal status, retry behavior, and whether finance can match the same external reference in exports. |

| Duplicate retries | Test duplicate retries with real sample rewards | Verify the user message, internal status, retry behavior, and whether finance can match the same external reference in exports. |

- Run four failure tests before launch.

Test expired links, endpoint eligibility failures, delayed provider recovery, and duplicate retries with real sample rewards. Runa gives concrete cases: RE004 (expired link), RE006 (temporary issue with a documented 24-48 hour recovery window), and push-to-card eligibility limits (Visa or Mastercard debit card only). For each test, verify the user message, internal status, retry behavior, and whether finance can match the same external reference in exports.

- Compare support posture by post-complaint actions, not marketing claims.

Use Runa docs to map known error handling and when to switch to an alternate payout mechanism. In Guusto, manual actions are explicit: edit/resend/cancel are only available before claim, and cancellation is only available within one year of send; when cancellation is available, funds return to the sending account. Bucketlist-style support layers should show both self-serve help and direct support contact so your team has a fast path when a reward is missing or delayed.

- Set escalation by failure class and make triage measurable.

Define one owner path per class: duplicate-request risk -> idempotent retry protection; temporary provider delay -> timed manual review; unclaimed-recipient issue -> user reissue path; non-recoverable aged exceptions -> finance write-off decision. Escalation should vary by incident type, severity, duration, and scope, and failed-payout triage should be tracked as a quantitative reliability metric (SLI). If dashboards cannot show open failures by class, age, and owner, do not expand globally.

Conclusion#

-

Choose economics over catalog theater. A headline like Tremendous offering 2000+ payout methods is real, and it matters, but it should not decide the deal on its own. Catalog breadth tells you how many options exist, not what each option does to your margin once processing costs, settlement timing, and fees show up in production. If finance cannot model gross-to-net cost by method and country before signature, you are still buying a story, not an operating answer.

-

Treat failure handling as a launch blocker, not a later cleanup item. Coverage claims can sound strong across many countries and currencies, yet the practical question is what happens when a payout cannot complete. Payouts have real failure states, and some can be held for review rather than paid out externally, so you need the vendor to show status definitions, freeze or review logic, and who owns communication when something stalls. A common risk is approving a provider because the happy path looks polished, then finding gaps in failure operations once the first batch breaks.

-

Make audit evidence part of vendor selection, not contract fine print. The winning choice is the one that gives finance a way to match payouts back to the transactions they relate to, with security and compliance evidence included in the selection process. Your RFP should force detailed, comparable answers, not broad claims. Ask for sample reconciliation outputs, the fields used to tie payout records to underlying transactions, and the exact evidence pack your team will rely on at month end.

That last point is often where weak options get exposed. A provider may have broad reward choice, but if it cannot give you payout-to-transaction mapping and exports that support close, the operational burden shifts back to your team. You can end up stitching together dashboards, invoices, and exception emails by hand. That is exactly the kind of invisible cost that makes a program look cheaper than it is.

So use this list to narrow the market, then force proof where it matters most: economics, controls, and operating reliability. Ask direct questions, require artifacts, and verify them with a pilot or live sample data set whenever possible. If pricing is still vague, or coverage is still described at a marketing level instead of method by market, treat that as risk now. It will not become simpler after launch.

Frequently Asked Questions

What is the difference between an employee recognition platform and a reward disbursement infrastructure provider?

A recognition platform fits Gartner’s "Employee Recognition and Reward Systems" category: software built to acknowledge and reward employee behavior against company goals. A payout infrastructure provider is API-led and built to send rewards, incentives, and payouts programmatically across markets. If you need recognition-program features and employee-facing UX, start with the former. If you own payout delivery and reconciliation visibility, the payout layer matters more.

When should an HR platform embed payout rails instead of offering gift-card-only rewards?

Embed rails when gift cards stop matching your use case: cross-border programs, configurable recipient choice, or a need to support more than one payout option. Provider docs show a practical distinction here because some let recipients choose across configured payout options rather than forcing a single reward type. A good checkpoint is whether you can get and verify a country-by-method support matrix before launch. One risk is selling "global choice" without verifying where a wallet, prepaid card, or ACH option is actually available.

Which payout methods are most practical for global employee recognition programs?

The most practical mix usually includes ACH transfers, gift cards, prepaid cards, and wallet transfers. Breadth can be real, but you should verify it at the method level: Tremendous documents 2000+ payout methods, while Runa discloses coverage across cards and wallets in 160+ countries plus access to 5,000+ gift and prepaid card endpoints through one integration. Pick a mix with a fallback path, not just a big catalog.

What usually drives total cost in employee recognition disbursements at scale?

Total cost should include transaction-level payout costs, not just the visible reward fee. Finance should ask for reporting that shows costs at the transaction level, similar to a settlement details report, so you can see what each disbursement actually cost. If your team cannot model transaction-level payout cost by segment, pause selection even if the pitch looks strong on the surface.

How should finance teams reconcile recognition payouts across multiple providers?

Reconciliation should tie payout batches back to underlying transactions using downloadable reports and API-accessible payout details. In practice, teams should use provider reports to track and reconcile payout transactions across accounts and providers. The red flag is a provider that gives you only summary invoices or dashboard totals, because that makes it harder to close the books or investigate disputes.

What should be in an RFP for employee recognition payout infrastructure in 2026?

Include both functional and non-functional requirements: payout methods, configurable recipient choice, reconciliation outputs, plus security and compliance evidence. You should also ask how the provider safeguards sensitive data and how quickly it responds to incidents, because those are baseline payments questions, not nice-to-haves. For this category, add exact requests for method-by-market coverage, downloadable and API-based reconciliation data, and security/compliance documentation before you score finalists.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- docs.stripe.com/workbench/event-destinationstrusted

- docs.stripe.com/global-payouts/pricingtrusted

- achievers.com/blog/employee-reward-platforms-enterprise-hrexternal

- developers.tremendous.com/docs/introductionexternal

- developers.tremendous.com/docs/webhooks-1external

- gartner.com/reviews/market/employee-recognition-and-rewa...external

- gartner.com/reviews/product/bonuslyexternal

- help.tremendous.com/hc/en-us/articles/41472312913043-Redemption-...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

5 Reasons Insurers Should Modernize Claim Disbursements with Digital Payout Platforms

Claims payouts are where an insurer proves the product. If the money arrives late, trust erodes fast, and paper-heavy payment flows add friction. That is not just a service issue. The cited research says the longer it takes for money to reach the insured, the more trust erodes, and payment delays can stretch a claim by days or even weeks.

How to Create an Employee Recognition Program for Distributed Teams

If your recognition program was built around office habits, it can miss people and create fairness problems. The problem usually is not intent. It is design. Recognition stops working when people do not experience it as fair, visible, and accessible.

Tipalti Payouts Explained for AP-Centric Supplier Disbursements

**For platform teams, understanding Tipalti payouts is a buying and operating question, not a feature tour.** The useful question is not "does it support global payouts?" Ask whether this AP-centric model fits your controls, your reconciliation needs, and the countries, currencies, and payout methods you actually have to support. That is how you avoid expensive exceptions later.