What crypto payout compliance looks like for platforms#

Crypto payout compliance is a product and operations decision, not a post-launch checklist. It affects payout speed, exception handling, audit readiness, and your exposure when regulators or banking partners ask how your controls work in practice.

If you are building contractor, creator, vendor, or marketplace payouts in crypto, you are choosing more than a payment rail. You are deciding who verifies users, who screens for sanctions risk, who monitors activity, who handles Travel Rule data where applicable, and who can prove those checks ran before funds moved.

Treat AML and KYC as operating controls, not paperwork. Ongoing compliance work includes transaction monitoring, customer verification, and suspicious activity reporting. A common failure mode is not recognizing where your crypto exposure starts and ends.

Use this article to choose an operating model your team can actually run, then put defensible checkpoints in place. Start with three questions:

- Who owns the controls?

Define ownership for verification, sanctions screening, monitoring, and payout approval so held payouts always have a clear decision owner.

- What proof exists at release time?

Tie verification status, screening results, approval records, and event history to payout state so evidence is available when needed.

- Where does jurisdiction change the requirement?

Licensing and registration needs vary by business activity and, in the U.S., by state, so a model that works in one market may need different controls in another.

Jurisdiction differences are not edge cases. For example, crypto payroll is discussed in Georgia, while cryptocurrency is not legal tender there, so local treatment can diverge from your rollout pattern in other markets.

This article stays explicit about certainty: clear requirements where grounded, and uncertainty where rules are still proposed. A rulemaking entry dated 03/02/2026 is a proposed rule open for comment, not finalized law on its own, so counsel should confirm classification, licensing, and reporting treatment before you scale.

Who this list is for and how to choose#

Use this list when you still need to decide who owns your compliance controls and how you will prove those controls worked before funds move. It is a decision tool for operating model design, not legal advice for a specific country filing.

- Use it early, while architecture is still flexible

Apply it when you are choosing between in-house, vendor-led, or hybrid ownership for AML/KYC and related control operations.

- Do not treat it as a jurisdiction filing answer

Use it to narrow build-versus-buy decisions before counsel review. It does not determine market-specific registration, filing, or approval outcomes.

- Choose by evidence you can actually produce

Prioritize the model that can consistently show what was checked, when, and by whom. In U.S.-relevant workflows, that includes handling FinCEN-linked checkpoints such as FBAR trigger logic, including the $10,000 threshold context, maximum account value method, exchange-rate source documentation when Treasury rates are unavailable, and explicit use of the FBAR "amount unknown" field, item 15a, where applicable.

- Prefer models you can run repeatedly under change

FinCEN notices emphasize risk when BSA obligations are not met, so pick an operating model your team can execute and document reliably as rules, corridors, and risk patterns evolve.

Best for teams that build compliance in-house#

Choose this model only if your team can run controls end to end and consistently prove what happened from your own records. It fits platforms that can own AML/CFT, KYC/KYB, sanctions decisions, and daily review operations, not just implementation.

Why teams choose it#

The main advantage is control. You decide which payout states require review, how jurisdiction-specific logic maps to internal entities, and which audit records must exist before funds move. That matters when payouts pass through multiple checks across treasury, operations, and reviewer signoff.

In-house ownership is usually a fit for enterprise marketplaces with custom approval paths, strict internal controls, and dedicated review capacity for higher-risk counterparties. If you need different rules by corridor, asset, or customer type, this model gives you more flexibility than a preset vendor flow.

The operator upside most teams underrate#

What teams often miss is not just flexibility. It is direct evidence mapping to the systems your team already trusts.

For U.S.-linked reporting, FBAR, FinCEN Report 114, is a practical example. This does not mean FBAR applies to every crypto payout flow. It means your stack can capture what filing and review require when legal analysis says FBAR is relevant:

- filing is electronic through the BSA E-Filing System, so credentials must be set up before submission

- the general due date is April 15, with an automatic extension to October 15

- maximum account value is recorded in U.S. dollars and rounded up to the next whole dollar, so $15,265.25 becomes $15,266

- each account is valued separately

- if Treasury exchange rates are unavailable, another verifiable rate may be used, and the source should be documented

- where allowed, item 15a can be used to mark amount unknown

These are the details that usually break audit narratives when ownership, timing, and source records are unclear.

Where the burden lands#

The tradeoff is implementation and operating load: slower launch, heavier on-call pressure, and more manual escalations as edge cases pile up. The biggest risk is execution drift, where the policy looks sound but production evidence is incomplete.

If your team cannot reliably handle daily escalations and release holds, full in-house ownership is usually premature. FinCEN has also warned in a CVC kiosk context that illicit risk increases when BSA obligations are not met. The practical lesson is simple: custom logic without reliable execution can increase exposure.

If you build in-house, set a hard release rule early: no payout leaves ready state without the rule version used, control outcome, approver identity, person or service account, and the ledger event that ties approval to release.

Best for teams using a compliance vendor with internal payout orchestration#

This is usually the right middle path when you want faster execution without giving up payout control. You keep routing logic, ledger ownership, and final approval policy in your product, while a vendor supports parts of the compliance and delivery stack.

In practice, orchestration options split between pure connectivity layers, which are routing-focused, and bundled models, which add infrastructure and services. Neither is inherently better. Choose based on your bottleneck: payout control, compliance stack ownership, or corridor expansion.

Why teams pick this model#

Use this setup when you want internal control over payout states and business rules but do not want to build every screening capability from scratch. You can still route by region, risk profile, payment method, or provider performance while offloading selected compliance workloads.

This model is especially useful when launch timelines are tight. Teams often ask how to enter a new market without turning it into a four-month integration project. A vendor can reduce build burden, but only if the integration exposes real operational control instead of acting as a thin connector.

A common pattern is to keep wallet selection, payout approval, and ledger posting in-house while outsourcing identity and sanctions checks. The vendor informs the decision. Your platform still decides whether a payout leaves ready state.

What to verify before you commit#

Before you sign, test three things. First, confirm the integration exposes routing, failover, and data access, not just pass-through connectivity. Second, confirm reporting, reconciliation, and fee transparency work for finance and operations, not only engineers. Third, define what is actually covered for your corridors and counterparties, including where handoffs occur.

Before release, store the vendor decision reference, your internal rule version, the approval actor, and the ledger event linking the compliance outcome to payout release. If you cannot reconstruct that chain, you have not kept true orchestration control.

Where this model breaks#

The main failure mode is assuming the vendor owns more than it does. Coverage gaps often appear late and force rebuilds under launch pressure.

Integration design is another common risk. Retry and idempotency handling can create conflicting states if your side is not robust, even when vendor decisions are clear.

Data quality is the last pressure point. Screening quality depends on the identity and entity data you send. Keep manual hold authority in your product and escalate ambiguous outcomes instead of auto-releasing.

Best for teams partnering with a regulated VASP or payout provider#

Use this model when speed to market and compliance coverage matter most, and you do not want to staff a large internal compliance function first. A regulated Virtual Asset Service Provider (VASP) or payout provider can give you a faster path by combining execution with controls in a licensed, reporting-heavy environment.

The key difference from a vendor-plus-orchestration model is ownership at the execution layer. Instead of only screening data, the provider often runs key control points tied to AML/CFT, sanctions, and monitoring for supported markets and payout types.

Why this model works#

A strong provider can bundle controls that are expensive to build internally: licensing for supported activity, KYC, ongoing transaction surveillance, and scheduled reporting to regulators. For lean teams, that creates a clearer operating posture on who monitors risk, who can stop payouts, and who handles reporting at execution.

This is especially useful for cross-border expansion. Country rules are inconsistent and keep changing, so outsourcing more of the licensed control stack can reduce launch friction. FATF Recommendation 15 is a useful anchor for why many countries regulate VASPs, but it does not make country requirements uniform.

What you need to verify before signing#

Do not treat "regulated" as blanket coverage. Confirm the exact legal entity in your flow, its license or registration scope, and its supported jurisdiction, asset, and payout-type boundaries.

Get a written control map before launch. At minimum, document ownership for KYC, sanctions screening, transaction surveillance, payout holds, and Travel Rule handling where supported. If ownership is unclear in pre-sales, incident response will be slower when payouts are blocked.

Request this document pack up front:

- Current license or registration references for in-scope entities

- Supported country, asset, and payout-type coverage

- Sample decision exports for blocked or escalated payouts

- Reporting and escalation contacts, including regulator follow-up ownership

Where this model breaks#

The main tradeoff is reduced policy flexibility. If your product depends on custom release logic by corridor, wallet type, user segment, or asset, provider-led execution can limit exception paths and control customization.

Vendor concentration is the second risk. If one partner owns execution, surveillance, and most evidence trails, coverage changes can hit operations immediately. Treasury's March 2026 report also frames digital-asset illicit-finance risk as including money laundering and sanctions evasion, which can increase provider-side control pressure over time.

Best-fit example#

A startup marketplace entering several new payout corridors can be a strong fit. The provider handles core AML/CFT controls, transaction monitoring, and some Travel Rule obligations where available, while your team focuses on onboarding, payout initiation, and exception handling.

Choose this model only if you keep internal hold authority and can retrieve evidence for every release, hold, and rejection. If that chain is not reconstructable, the speed benefit weakens quickly under real payout compliance pressure.

Best for teams running a hybrid model by corridor and payout type#

Use a hybrid model when payout risk is mixed across corridors and payout types. Keep stable, repetitive flows on a standard path, and route higher-uncertainty flows through stricter controls.

Why this model works#

This model lets you optimize cost and control by segment instead of forcing one control depth across every payout. The tradeoff is governance complexity. If ownership is unclear, policy drift shows up quickly across markets.

Practical decision rule#

If a corridor has elevated sanctions exposure, weaker counterparty certainty, or Travel Rule uncertainty, use the stricter route. If a corridor is stable, high-volume, and you can show control performance, internal optimization is usually more practical.

How to keep segmentation operational#

Start with a focused pilot scope, not your full payout estate. Before launch, define supported transaction types and expected volumes, then assign clear owners across compliance, payments, treasury, risk, and engineering.

Track performance by segment, not in one blended bucket:

- settlement efficiency and costs

- operational reliability

- customer adoption

| Segment example | Control posture |

|---|---|

| High-volume USDC contractor payouts in a stable corridor | Standard KYC flow and clear release rules |

| Bitcoin payouts in a higher-uncertainty corridor | Stricter vendor controls and tighter exception handling |

| Treasury-like liquidity movements | Separate policy with stronger counterparty review and tighter approvals |

Where teams get burned#

The common failure modes are policy drift and infrastructure dependency. If routing, network, and vendor decisions are made in isolation, you can lose flexibility later. And if settlement moves faster than legacy fraud controls, higher-risk routes may need to move back under stricter vendor control until gaps are closed.

Compare the four operating models side by side#

The practical comparison is straightforward: pick the model that gives you a named owner at every control point, especially at payout release. If ownership is unclear for KYC/KYB, screening, Travel Rule handling, or release approval, expect weaker evidence quality and more exceptions.

| Model | Launch speed | Control depth | Internal headcount | Audit evidence quality | Practical sanctions control reach for 31 C.F.R. §560.314-relevant cases* | KYC/KYB owner | SDN/geolocation screening owner | Travel Rule owner | Payout release signoff | Where unknown on tax/reporting |

|---|---|---|---|---|---|---|---|---|---|---|

| In-house controls | Slowest | Highest | Highest | Strongest when logs, case notes, and payout IDs stay linked | Highest practical reach because rules and exceptions stay in your stack | Internal compliance or ops | Internal tools and reviewers | Internal team or direct integrations | Internal compliance, finance, or ops | You still own IRS and local reporting analysis; non-U.S. duties need local confirmation |

| Vendor checks with internal payout orchestration | Faster | Medium to high | Medium | Good if vendor outcomes are written back to your payout record | Medium to high, depending on integration and exception handling | Vendor for onboarding checks, internal team for policy | Vendor screening, internal team for escalations | Vendor or integration layer | Internal team keeps final release control | Tax ownership usually stays with your finance or tax team; local equivalents remain jurisdiction-specific |

| Regulated VASP or payout provider | Fastest | Medium | Lowest | Moderate to good, based on provider exports and case access | Medium, with less custom policy reach but clearer outsourced execution | Provider | Provider | Provider where supported | Typically shared operationally: you approve business intent, provider executes within its controls | Do not assume provider owns your IRS or local filings; non-U.S. reporting still needs counsel review |

| Hybrid by corridor and payout type | Variable | High where strict routing is used | Medium to high | High only if segment tags and ownership stay consistent | High in stricter segments, uneven if routing or policy drifts | Split by segment | Split by segment | Split by segment | Split by segment owner | Highest risk of fragmented tax/reporting ownership unless one finance lead maps all segments |

*This column reflects practical control reach, not legal sufficiency under 31 C.F.R. §560.314.

How to read this comparison#

Treat the sanctions and Travel Rule columns as evidence questions, not feature checkboxes. For any model, test one payout and confirm you can retrieve in one place: KYC/KYB status, screening result, Travel Rule case status, if applicable, approver name, and payout ID.

Apply the same discipline to tax ownership. IRS guidance states digital assets are treated as property for U.S. tax purposes, and income from digital assets is taxable. A concrete checkpoint from FS-2024-12, April 2024, is whether the digital-asset yes or no question is addressed where relevant on Forms 1040, 1040-SR, 1040-NR, 1041, 1065, 1120, and 1120-S. Provider-led execution does not automatically transfer that analysis away from your team.

Payout type and asset tradeoffs#

| Payout type or asset | Practical tradeoff to decide early | Where unknown |

|---|---|---|

| Employee payouts | Do not default to contractor workflow; assign tax ownership before launch | Jurisdiction-specific filing duties and timing |

| Contractor payouts | Usually a cleaner starting lane if classification is already settled; define who can block release | Local reporting requirements by country |

| Vendor payouts | KYB and counterparty documentation usually matter more; release ownership must be explicit | Non-U.S. reporting and documentation expectations |

| Bitcoin | Often needs stricter exception handling if your standard lane was tuned for narrower asset patterns | Travel Rule applicability details and sanctions-control design specifics |

| USDC | Often easier to standardize operationally, including intermediary-led setups | Asset choice does not remove tax/reporting analysis; local obligations still vary |

Decide by payout type and asset before you design controls#

Set tax-reporting decision gates first, then design payout controls by lane. Use payout type and asset to assign ownership, but do not treat classification alone as the legal trigger for Form 8938 or FBAR decisions.

| Reporting item | Who may need it | Trigger to design for | Filing mechanic to capture |

|---|---|---|---|

| Form 8938 for specified individuals living in the U.S. | U.S. citizens, resident aliens, and certain non-resident aliens | More than $50,000 on the last day of the tax year or more than $75,000 at any time during the year (unmarried or married filing separately); more than $100,000 or $150,000 (joint filers) | Attach to the annual return and file by that return’s due date, including extensions |

| Form 8938 for specified individuals living outside the U.S. | Same filer class, if living abroad | More than $200,000 or $300,000 (unmarried or married filing separately); more than $400,000 or $600,000 (joint filers) | Record the applicable calendar year or tax year on the form decision |

| Form 8938 for specified domestic entities | Certain domestic corporations, partnerships, and trusts | More than $50,000 on the last day of the tax year or more than $75,000 at any time during the tax year | Applies for tax years beginning after December 31, 2015 |

| FBAR (FinCEN Form 114) | Filers under separate FBAR rules | Aggregate account value exceeds $10,000 at any time during the calendar year | Filed with FinCEN, not with the IRS |

Once those reporting gates are clear, separate the lanes before you build release logic:

- Employee lane

Keep payroll logic separate from contractor and vendor logic before launch. If this lane is in scope, assign owner-level accountability for withholding and year-end reporting design before first payout.

- Contractor lane

Define your own onboarding and payout-time refresh policy for KYC/KYB and sanctions checks. The IRS, Form 8938, and FBAR materials do not set that timing for you.

- Vendor lane

Use a distinct vendor path for entity documentation, approvals, and release evidence. Avoid a shared profile model that blurs whether the counterparty was reviewed as a person or a business.

- Foreign-asset reporting overlay

Map FATCA-related workflow checks to concrete form decisions and thresholds. Form 8938 is threshold-based and is not required when no income tax return is required for that year. Filing Form 8938 also does not replace FBAR, and FBAR is filed with FinCEN, not the IRS. Store the decision record for each case: which form was considered, which threshold test was applied, and which calendar year or tax year was reviewed.

Sequence controls from onboarding to payout release#

Once your payout lanes are defined, use a fixed control sequence from onboarding through release. Identity collection, sanctions screening, risk review, approval, and post-payout monitoring should be built into product states, not treated as a one-time checklist.

This order helps prevent the operational failures that show up most often: slow onboarding, missing data, inconsistent approvals, and cross-border payout friction. If controls are not tied to state transitions, teams end up releasing payouts on incomplete files and reconstructing decisions after the fact.

- Collect KYC/KYB first.

Gather enough verified identity data to classify the counterparty correctly and run downstream controls with complete inputs. Keep person and business paths distinct so later checks and approvals are based on the right record type.

- Run sanctions checks before deeper risk review.

Screen as soon as identity data is sufficient for a meaningful result, and hold unresolved matches before normal risk scoring. Keep sanctions checks as lifecycle controls, including a pre-release re-screen and additional review triggers when profile signals materially change.

- Use AML/CFT + SoW review to set disposition.

After identity and sanctions checks, assess relationship and payout risk as ordinary, elevated, or blocked for review. For higher-risk profiles, SoW review can include on-chain tracing, document verification, and risk scoring. For crypto counterparties, due diligence should cover jurisdictional risk, licensing gaps, AML/KYC program quality, and asset risk.

- Gate approval, then enforce idempotent release.

Make approval the policy gate that authorizes execution, and require evidence of who approved, what was checked, and which rules fired before leaving ready. Build duplicate-safe release behavior so retries update state instead of creating a second transfer.

- Monitor after release and preserve traceability.

Post-payout monitoring helps surface exposure that onboarding did not fully reveal, which matters because a major risk is not knowing you are exposed. Blockchain records are time-stamped and immutable, but they only prove movement, so your internal trail should still connect each transfer to identity status, sanctions outcome, risk rationale, and approval history.

Handle failure modes before they become incidents#

Treat unresolved identity, sanctions, or counterparty data as a release blocker, not an ops inconvenience. In practice, recurring failure points are weak customer due diligence, weak transaction monitoring, and weak sanctions screening. Your payout path should force human resolution before funds move.

- Stale KYC or KYB files

Do not treat KYC completed or KYB completed as enough at release time. Use the last verified date, what changed, and whether the payout instruction still matches the approved profile. If the profile changed materially, route back to review before it leaves ready, and keep the evidence pack: old value, new value, review note, final disposition.

- Mismatched legal names

Handle punctuation differences, transliteration issues, and true legal-entity mismatches as different cases. If the mismatch is not document-resolved, keep the payout blocked and require supporting documentation, then log which source record controlled the decision.

- Ambiguous sanctions matches

If sanctions confidence is unclear, hold the payout and escalate to manual review. Do not auto-release partial or near matches against the SDN List as an expedient policy choice. Preserve the screening snapshot, match details, analyst decision, and approval trail so the release decision is defensible.

- Counterparty data conflicts, including VASP/Travel Rule handoff gaps

If counterparty data is incomplete or conflicts with your record, do not patch it with free-text overrides. Resolve the missing or conflicting payload with the counterparty or reroute through a path that can support compliant exchange, and pre-assign escalation ownership across compliance, product, and engineering.

This is not theoretical. A reported incident on December 30, 2025 described unauthorized activity tied to governance permissions and estimated losses of approximately $3.9 million. The operational lesson is straightforward: transaction-level monitoring can miss misuse of administrative control, so document risk assessments, integrate crypto oversight into AML operations, and make overrides fully traceable before they become incident evidence.

Build the minimum audit evidence pack from day one#

If you do only one thing well, make it this: for each payout, keep one evidence bundle that clearly explains why it was released, held, or rejected at the time funds were approved to move.

- Create a payout-level decision bundle

For every payout, retain one linked record with release-time KYC/KYB status, sanctions result, risk score rationale, approval actor, and payout event trail. Preserve point-in-time snapshots instead of overwriting them after later re-screening. An auditor should be able to open one payout ID and immediately see what checks passed, who approved, and what changed after onboarding.

- Record the reason, not just pass/fail

Keep the decision basis: reason code, rule or analyst note, and any manual override with approver identity. For AML/CFT controls, outcome flags without rationale are weak evidence. If you map controls to FATF Recommendations, use that mapping as structure while local legal obligations still govern execution. The OFAC Tornado Cash action on August 8, 2022 is a concrete reminder that enforcement can focus on control failures, with Treasury citing more than $7 billion laundered since 2019.

- Store tax classification context with the payout file

Keep classification context with the payout record so payroll, contractor, and vendor treatment is auditable. For payroll-connected flows, retain the classification basis and generated IRS artifacts such as Form W-2 where applicable. For non-payroll flows, retain the decision record supporting different treatment. This aligns with IRS positions that digital-asset income is taxable, digital assets are treated as property, and digital-asset transactions must be accurately reported.

- Retain audit metadata while limiting PII exposure

Protect sensitive fields with masked or encrypted access and role-based retrieval, and keep regulator-facing metadata easy to retrieve: payout ID, recipient entity, outcome, timestamps, reviewer identity, linked document references, and evidence location. For U.S. tax-connected flows, include whether the relevant digital-asset return artifact exists, including the required yes or no digital-asset checkbox on applicable federal returns. Avoid copying raw documents into tickets or support notes. It increases exposure without improving evidence quality.

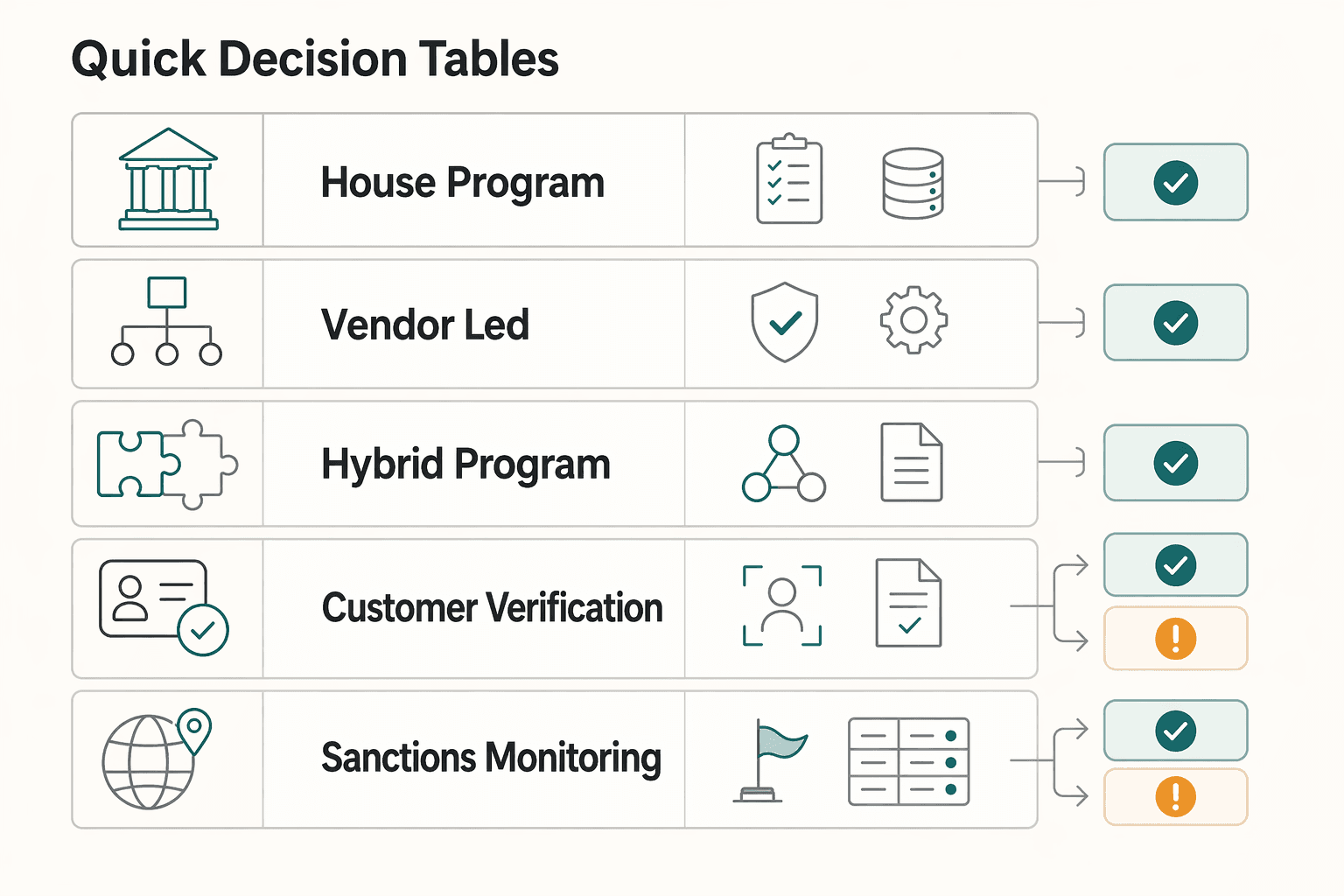

Quick decision tables#

| Operating model | Who owns the controls | What you must prove before release |

|---|---|---|

| In-house program | Your team owns verification, screening, monitoring, and release approval. | Policy version, reviewer identity, and release evidence all sit in your own systems. |

| Vendor-led program | A compliance provider runs a meaningful share of the checks. | You can still retrieve the vendor result, timing, and escalation path before funds move. |

| Hybrid program | You split ownership by corridor, asset, or payout type. | The handoff between provider evidence and internal approval is explicit and testable. |

| Control area | Minimum checkpoint | Escalate when |

|---|---|---|

| Customer verification | Identity and business checks are complete for the route you are releasing. | The customer type, jurisdiction, or ownership structure does not fit the current rule set. |

| Sanctions and monitoring | Screening result, monitoring state, and decision owner are stored with the payout event. | A hit, false-positive review, or missing screening result blocks release. |

| Travel Rule handling | The team knows when counterparty data must travel with the transaction. | Wallet type, provider boundary, or jurisdiction creates uncertainty about data-sharing duty. |

| Evidence artifact | Why it matters | Owner |

|---|---|---|

| Approval log | Shows who released the payout and under which rule version. | Operations or treasury lead |

| Wallet and route record | Confirms which asset, corridor, and provider path were actually used. | Payments product or engineering owner |

| Exception ledger | Keeps rejected, delayed, or reversed payouts visible for audit and remediation. | Risk or compliance operations |

Related Gruv reads#

For related Gruv guidance, compare How to implement pay-fiat-receive-crypto, MiCA crypto payout decisions, Stablecoin payouts for platforms, What AML means for platform operators, and What KYC means for payment platforms before you lock ownership for screening, monitoring, and release approval.

Primary source checkpoints#

Use live primary sources when you finalize controls: the IRS digital assets guidance, the FinCEN notice on convertible virtual currency kiosks and scam payments, and the SEC crypto-asset activity FAQ.

Conclusion#

The right payout compliance model is the one your team can run consistently under normal volume, escalation, and audit, with clear ownership and payout-level evidence.

- Choose one operating model per corridor and payout type

Do not assume one model fits every market or program. Control design depends on your business model and regulatory obligations, so define ownership per corridor: who handles KYC/KYB, who runs sanctions screening, who approves release, and who handles blocked payouts.

- Prove the release checkpoint before scaling volume

Cost advantages do not replace execution controls. Even where stablecoin economics look strong, for example $200 U.S.-to-Colombia for less than one cent versus average remittance fees around 6.6%, validate the release gate first: confirm identity status, sanctions screening, and transaction monitoring before payout, and store that point-in-time result with the payout record.

Sanctions controls should be lifecycle controls, not onboarding-only checks. U.S. sanctions rules apply to digital-asset activity, and late 2022 enforcement focus highlighted ongoing screening against the SDN database. If your program involves U.S. persons under 31 C.F.R. §560.314, include in-process geolocational checks, such as IP and physical address indicators, in release decisions.

- State coverage and unresolved requirements before go-live

A common failure is not knowing where crypto exposure starts or stops. In the launch plan, explicitly list covered markets, assets, and payout types, and flag what still needs legal confirmation, especially for Travel Rule applicability, tax treatment, and partner-dependent coverage.

Keep one payout-level evidence bundle with screening outcome, decision rationale, approver, timestamps, and event trail, plus documented limits, for example unsupported corridors or manual-review paths. If sanctions, tax, or Travel Rule handling is unclear, hold scope and resolve the gap before launch.

Frequently Asked Questions

What is crypto payout compliance for a platform, in practical terms?

In practice, it means you can show why a payout was released, held, or rejected at the moment the decision was made. The operational risk is higher in crypto because transactions are generally irreversible and often larger, so errors are harder to unwind.

Do AML and KYC checks happen only at onboarding, or also before payout release?

KYC starts at onboarding because its core purpose is to verify identity before account opening. It should not be your last control point. Before release, confirm eligibility again and retain a point-in-time status tied to the payout decision.

What sanctions checks are expected during payout execution?

Treat sanctions-screening timing, match thresholds, and escalation rules as specifics to confirm with counsel and your providers. At minimum, require a documented pre-release screening result linked to the payout record.

When do Travel Rule obligations apply in a crypto payout flow?

Confirm Travel Rule applicability, triggers, thresholds, and required data fields with your legal team and payout partners before launch. If those requirements are unclear, expect payout friction during execution.

How do tax obligations differ between employee and contractor crypto payouts?

Do not assume employee and contractor crypto payouts are treated the same. The IRS states virtual currency is treated as property for U.S. federal income tax purposes, and those FAQs generally apply to digital-asset transactions completed before Jan. 1, 2025, unless otherwise stated. Use that as baseline context, then design classification, withholding, and reporting with role-specific tax guidance.

What records should we retain to be audit-ready for regulators and banking partners?

Keep one payout-level evidence bundle that captures identity status, screening outcome, decision rationale, approver, timestamps, and event trail. For tax-connected flows, retain the classification basis and the reporting artifacts generated for that flow. If partners ask about messaging readiness, the ISO 20022 Compliance Checklist is useful implementation evidence, but it is not a certification because ISO 20022 has no official certification authority.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/resources/FinCENFBARHelp.pdftrusted

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- federalregister.gov/documents/2026/03/02/2026-04089/implementing...trusted

- federalregister.gov/documents/2026/04/01/2026-06271/whistleblowe...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/news/news-releases/fincen-issues-notice-use-...trusted

- home.treasury.gov/system/files/246/GENIUS-Act-Illicit-Finance-...trusted

- home.treasury.gov/news/press-releases/jy0916trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: