Quick Answer

Pick one operating path first: direct CASP, partner-led CASP, or hybrid, then freeze ownership for approvals, exceptions, and reconciliation before engineering expands scope. Escalate legal review as soon as payout design could map to ART or EMT behavior, and treat MiFID II overlap as a boundary check. Launch only after failure-path testing and dated evidence are in place, including jurisdiction decisions, partner responsibilities, and request-to-ledger trace records.

MiCA crypto payouts for EU platforms in 2026#

Use this guide to separate what needs legal escalation from what your product, finance, and operations teams can decide now. Move quickly where the record is solid, and slow down where it is not.

- Built for platform operators

This guidance is for founders, product leads, finance ops, and engineering owners building contractor, creator, marketplace, or embedded payout flows. The useful unit is the operating choice you make before code, contracts, and user messaging lock you in.

VAT operations offer a practical EU reminder. They do not answer MiCA questions, but they do show how quickly a compliance choice becomes an operating commitment. Under OSS, a business can register in one Member State, the Member State of identification, for covered filings. In some Union-scheme cases, that choice can bind you for the calendar year plus the next two.

- Decision value over legal theater

The goal is to identify your likely exposure path faster, compare operating models clearly, and execute against named checkpoints across legal, product, and operations. If public material does not answer a question cleanly, log the gap instead of filling it with confidence.

In VAT, obligations include record-keeping and filing cadence. OSS returns are quarterly for non-Union and Union schemes and monthly for the import scheme, and a Member State can exclude a participant. Before launch, assign ownership for filing logic, status history, exception records, and the document trail behind each design choice.

- Use this as operating guidance, not a legal conclusion

This guide is operational guidance based on the public VAT materials summarized here. It is not legal advice. These materials do not establish MiCA-specific obligations.

VAT Cross-border Rulings illustrate the right discipline. Taxable persons can seek advance rulings on complex cross-border VAT transactions, but requests must follow national VAT-ruling conditions in the country where they are filed. Apply that same discipline to payout design. If a classification question is unresolved in public materials, set an escalation gate before contracts are signed or wallet flows are shipped, and keep a dated evidence pack of sources, open questions, and owners. Move fast on decisions you can support, and slow down where the public record does not justify certainty.

For a step-by-step walkthrough, see Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know.

Choose your path before you design your payout stack#

Choose the operating model before you design wallets, ledgers, and payout UX. For crypto-specific classification questions, treat scope and obligations as legal unknowns and escalate before build starts. The OSS materials below cover EU VAT process decisions, not MiCA determinations.

- Start with the perimeter question

First decide who sits inside the compliance perimeter: your entity or a partner. Keep it concrete: who contracts with users, who sets and approves payout policies, and who handles exceptions.

- Score each path on the same five criteria

Compare options on OSS registration setup, VAT return cadence and payment operations, record-keeping and audit workload, exit or exclusion scenarios, and dependence on third parties. Use the same checklist each time so the tradeoffs show up early, not after launch.

- Assume early EU operating choices are sticky

In VAT OSS, the Member State of identification choice in the Union scheme can bind the business for the current calendar year plus the next two. Make path decisions with that level of commitment in mind.

- Create a dated evidence pack before vendor and flow decisions

Keep a short memo with the proposed model, open legal questions, owners, and the public materials used. For complex cross-border VAT treatment questions, consider whether a VAT Cross-border Ruling request is appropriate under the national conditions where the request is introduced.

Option 1 run as a MiCA authorized CASP#

Choose this path only if you want the regulated perimeter in-house and will verify MiCA specifics before finalizing the design. The grounding for this section does not establish MiCA authorization criteria, timelines, or supervisory expectations, so treat those as legal checks, not assumptions.

Best for#

Use this route only if you plan to keep payout policy, monitoring, and exception handling internal and are prepared to validate the MiCA implications with counsel. If your immediate goal is speed, demand testing, or limiting legal surface area, defer this route until your perimeter and ownership model are fully defined.

What you gain and what you take on#

Do not assume either the control upside or the compliance load until you validate MiCA authorization outcomes. Keep legal analysis, product design, and audit-trail design aligned from the start.

Use VAT OSS only as a stickiness analogy, not as a MiCA shortcut. For covered cross-border activity, businesses can register in one Member State and submit electronic VAT returns. Returns are quarterly for Union and non-Union schemes and monthly for the import scheme. Online marketplaces and platforms also face record-keeping requirements, and in some Union-scheme cases they can be bound to their Member State choice for the current year plus the next two.

What to verify before you commit#

- Perimeter memo

Define the contracting entity, who sets payout rules, and who handles exceptions.

- Jurisdiction lock-in check

Test how hard it will be to change your setup later before selecting a likely jurisdiction path.

- Records and traceability test

Confirm you can produce clear, end-to-end operational records from request through outcome.

Option 2 partner with an authorized CASP and keep orchestration in-house#

If you need to launch faster without owning the full regulated perimeter on day one, this is often the practical path. You rely on a MiCA-authorized CASP for regulated crypto-asset services while your team keeps core payout orchestration in-house where the partner model allows it.

Best for#

This model fits teams that need production momentum before direct authorization is realistic. A vendor-stated timeline for pursuing your own CASP authorization is about ~3 to 9 months depending on jurisdiction and application quality, so partnering can remove a major schedule dependency.

It can also fit early and mid-stage platforms that want to validate payout demand before building a full in-house compliance function. With the broader rule set around Regulation (EU) 2023/1114 still evolving, partner coverage can buy time while you decide where direct control is strategically necessary.

What you gain#

The main advantage is speed and a lighter internal licensing load. Some licensed providers position EU coverage through passporting under a single regime, which can simplify near-term expansion planning.

Service scope can also map directly to payout execution, including storage and administration, transfers, and exchange of crypto-assets into funds. Some providers also position combined authorization coverage for crypto, EMT, and fiat settlement flows on one regulated platform. Treat that as provider-specific, not universal.

What you give up#

The tradeoff is control in edge cases. Exception handling, sanctions matches, Travel Rule data issues, and off-cycle approvals may follow partner policy, not your preferred operating model.

Commercial dependency matters too. Third-party pricing and related terms can change your unit economics as volume grows, so stress-test assumptions before signing.

What to verify before you sign#

- License and service-scope fit

Confirm the partner's CASP authorization and match licensed services to your actual payout design, for example transfers, custody-related functions, or crypto-to-funds exchange.

- Control-boundary memo

Define ownership for routing, reconciliation, ledger posting, exceptions, customer communications, and incident decisions before go-live.

- Compliance operations evidence

Request concrete proof of KYC/KYB, sanctions screening, and Travel Rule handling, plus usable status outputs or logs for end-to-end traceability.

Concrete use case#

A contractor platform may keep parts of payout routing, reconciliation, and ledger controls internal while a licensed provider executes the regulated crypto service layer. Whether that split works depends on the partner's operating model, license scope, and contract terms. This path works when product value sits in orchestration and finance operations, with explicit acceptance of partner dependency for regulated-perimeter decisions. This pairs well with our guide on USDC Contractor Payouts for Platforms and Stablecoin Rollout Decisions.

Option 3 use a hybrid model with phased control transfer#

Use a hybrid model when you want launch speed now and optional control later. Treat it as an operating choice, not a predefined regulatory handoff lane. This evidence pack is VAT/OSS-focused, not MiCA-specific, so keep transfer points explicit early and avoid improvising them later.

Best for#

This model fits platforms that want partner-led execution in the near term but may internalize selected controls if volume and product differentiation become strategic. If not, keep the partner-first setup and improve commercial and operational terms instead.

Structure and decision rule#

Start with partner-led activity, then move only selected controls in-house when operating evidence shows clear value. If deeper ownership will not improve outcomes, do not force a transfer.

How to run the phased model#

- Partner-led launch

Keep partner scope and your internal ownership boundaries explicit from day one, including exception ownership, customer messaging, and ledger correction decisions.

- Evidence gate before transfer

Transfer only when records and status outputs are strong enough to trace key flows from request to closure without manual guesswork.

- Selective internalization or contract hardening

Internalize only where tighter control materially improves operations. Otherwise, strengthen contract terms, reporting access, and escalation paths.

Adjacent EU obligations that can affect execution#

If your model also touches EU VAT flows, OSS mechanics can shape workload and controls. OSS registration is in one Member State of identification, and participation is optional. Once you opt into a scheme, you must declare all supplies that fall under it through OSS returns.

Filing cadence differs by scheme: quarterly for non-Union and Union schemes, and monthly for import. In some Union-scheme scenarios, Member State choices can bind you for the calendar year plus the next two. OSS also carries record-keeping obligations, and a Member State can exclude a participant from a scheme. For complex cross-border VAT treatment, VAT Cross-border Rulings can provide advance rulings.

Concrete use case#

An embedded-payments platform launches with partner coverage to go live faster, then reviews real operating data before deciding whether to bring specific customer-flow or exception operations in-house. If the evidence is weak or the strategic upside is limited, it keeps the partner model and improves contract and data terms instead. Related reading: Invoice Settlement for Platforms That Match Payouts and Close Disputes.

Compare the three operating models side by side#

Do not force a legal ranking across direct, partner, and hybrid models. Use the comparison below as an operating checklist. Focus on where ownership sits, what evidence you can produce, and what still needs legal confirmation.

The grounded process pattern here comes from OSS VAT operations. It includes optional scheme use, one Member State of identification, quarterly or monthly filing cadence by scheme, ongoing record-keeping and audit duties, potential lock-in for some identification choices, and possible exclusion. Use that pattern to pressure-test execution readiness, not to claim MiCA outcomes.

| Comparison point | Option 1 direct CASP | Option 2 partner with authorized CASP | Option 3 hybrid with phased transfer |

|---|---|---|---|

| Authorization burden | Not established by this OSS/CBR evidence set; confirm legal scope and required approvals with counsel. | Not established by this OSS/CBR evidence set; confirm in contract who owns regulated obligations and evidence access. | Not established by this OSS/CBR evidence set; define legal scope and evidence ownership for each phase before transfer. |

| Time to launch | Confirm with legal counsel; use registration, filing cadence, and record/audit readiness as launch gates. | Confirm with legal counsel; include partner onboarding and evidence-access readiness in those gates. | Confirm with legal counsel; include phase-transfer gates for filing and record ownership. |

| Operating cost profile | Cost outcomes are not established here; map costs to ownership of registration, filing/payment cadence, record-keeping, audits, and exclusion handling. | Cost outcomes are not established here; map partner fees against retained oversight, reconciliation, and evidence duties. | Cost outcomes are not established here; map overlap costs during transfer windows. |

| Control of payout UX | Confirm with legal counsel; treat control boundaries as a legal and operating-design decision. | Confirm with legal counsel; treat control boundaries as a legal and operating-design decision. | Confirm with legal counsel; treat control boundaries as a legal and operating-design decision. |

| Incident response ownership | No model-specific rule is established here; keep a traceable owner map from request to closure. | No model-specific rule is established here; define escalation, messaging, and correction ownership in contract terms. | No model-specific rule is established here; define owner changes at each transfer checkpoint. |

| Expansion flexibility across the EEA | Requires separate legal analysis; confirm model-specific expansion outcomes with counsel. | Requires separate legal analysis and contract review; confirm model-specific expansion outcomes with counsel. | Requires separate legal analysis and phase planning; confirm model-specific expansion outcomes with counsel. |

| Best for | Verify company-stage fit with your legal and operating team. | Verify company-stage fit with your legal and operating team. | Verify company-stage fit with your legal and operating team. |

| Breaks when | Registration scope, filing cadence, record-keeping, or audit evidence is unclear. | Contract terms do not preserve record access, auditability, or exclusion-response duties. | Phase triggers are undefined, so ownership and evidence split across models. |

| Recommendation | Confirm the best-fit model with legal counsel. | Confirm the best-fit model with legal counsel. | Confirm the best-fit model with legal counsel. |

Use one decision rule: choose the model you can evidence today. Before you commit, require a concrete pack covering registration scope, filing cadence, domestic VAT return handling, record and audit access, lock-in or change constraints, and exclusion handling.

Once you pick a model, pressure-test it against real payout routing, status handling, and exception ownership so legal and engineering assumptions stay aligned: Review Gruv Payouts.

Pick the payout asset design with MiCA scope in mind#

Asset design is a gating decision, not a polish step. If your payout token starts to resemble an ART or EMT, pause product lock-in and get legal classification before finalizing UX promises, treasury flows, or partner contracts.

| Area | When relevant | Key differentiator | Before launch |

|---|---|---|---|

| ART-sensitive payout designs | If positioning implies stable value tied to reference features | Users may expect more than "you received crypto." They may expect a defined value profile. | Require written classification review before sprint sign-off, and review all user-facing statements on stability, value, and redemption. |

| EMT-sensitive payout designs | If the token is used like a money-like payout instrument | Users may expect cash-like handling, especially for redemption timing and failed transfers. | Map redemption end to end: request intake, approval owner, ledger postings, and completion or reversal evidence. |

| Other crypto-asset payout designs | If the asset does not resemble ART or EMT behavior | The promise is usually "we pay in this asset," not "we preserve money-like value." | Use auditable payout status history, exception handling, and recurring records that can stand up to supervisory review. |

| MiCA boundary checks against other EU regimes | If design resembles an instrument covered elsewhere | This is a legal-perimeter test, not just asset selection. | Keep a pack with the token description, attached rights, redemption mechanics, target jurisdictions, and the customer-journey screens where those rights are communicated. |

Under MiCA, issuer and CASP obligations can differ significantly, so your asset choice can change both compliance posture and day-to-day operations. Treat the token as more than a transfer rail. It shapes user expectations on value stability, redemption, and who stands behind balances when something fails.

- ART-sensitive payout designs

If positioning implies stable value tied to reference features, ART analysis may be relevant. You do not need to self-classify, but you do need early escalation when marketing, onboarding, or partner materials imply value-reference behavior. Key differentiator: users may expect more than "you received crypto." They may expect a defined value profile. Require written classification review before sprint sign-off, and review all user-facing statements on stability, value, and redemption.

- EMT-sensitive payout designs

If the token is used like a money-like payout instrument, EMT questions can surface quickly. Teams can blur the payout event, stored balance, and redeemable claim, which can create support and finance failures later. Key differentiator: users may expect cash-like handling, especially for redemption timing and failed transfers. Before launch, map redemption end to end: request intake, approval owner, ledger postings, and completion or reversal evidence. Finance should reconcile the payout request, internal ledger posting, onchain transfer result, and partner settlement or exception records.

- Other crypto-asset payout designs

If the asset does not resemble ART or EMT behavior, it may still fall under another MiCA category rather than being out of scope. This is operationally cleaner only if your promise is explicit about volatility, settlement finality, and support boundaries. Key differentiator: the promise is usually "we pay in this asset," not "we preserve money-like value." The control test is execution quality: auditable payout status history, exception handling, and recurring records that can stand up to supervisory review.

- MiCA boundary checks against other EU regimes

Do not evaluate scope through MiCA alone. EU policy material notes that some crypto-assets may already fall under existing EU legislation, and application is not always straightforward. Assets already regulated as securities, deposits, or e-money are described as outside MiCA scope, so boundary checks with regimes such as MiFID II matter. Key differentiator: this is a legal-perimeter test, not just asset selection. If your design resembles an instrument covered elsewhere, escalate before commercial terms are signed. Keep a pack with the token description, attached rights, redemption mechanics, target jurisdictions, and the customer-journey screens where those rights are communicated.

Do not assume all scope questions are settled. ESMA continues to develop standards and guidance. It has also noted that at least one scope point should not be defined in RTS, so treat classification as a launch gate when token design is core to your payout proposition.

Plan non EU entry carefully because reverse solicitation is narrow#

Treat non-EEA entry as a regulated access decision, not a growth experiment. The concrete guidance available covers VAT procedures. Confirm the MiCA-specific legal test for reverse solicitation with legal counsel before launch.

- Route reverse-solicitation questions to counsel

If teams argue that inbound demand is enough, route that to legal review before launch decisions are made. Product or growth should not set that boundary on their own — MiCA-specific thresholds, country triggers, and solicitation tests require legal confirmation.

- Tie EEA onboarding to a live jurisdiction map

Use one shared view of where you onboard users, which entity contracts with them, what partner covers activity, and whether tax registration and reporting are in place. If your country onboarding rules, help-center language, acquisition settings, and partner territory clauses do not match, expansion is already ahead of compliance posture.

- Use OSS decisions as an early non-EU checkpoint

For eligible cross-border B2C VAT activity, OSS allows registration in one Member State of identification to declare and pay VAT due across multiple Member States. Under the non-Union scheme, a business with no EU establishment can choose any Member State of identification. Where multiple fixed establishments exist, that choice can bind for the current calendar year plus the next two and cannot be changed unless the relevant fixed establishment is dissolved or moved.

- Add a stop/go gate before each expansion sprint

Require a short approval pack covering legal sign-off, partner constraints, and tax readiness for each new EEA push. For complex cross-border VAT treatment involving two or more participating Member States, consider a VAT Cross-border Ruling request under the filing country's national VAT ruling conditions. Also assign ownership for OSS return cadence: quarterly for non-Union and Union schemes and monthly for the import scheme.

Operationally, the rule is simple. Where MiCA entry analysis is still a legal question, lock down what you can verify now, especially jurisdiction tracking, partner coverage, and Member State choices that create lasting VAT consequences.

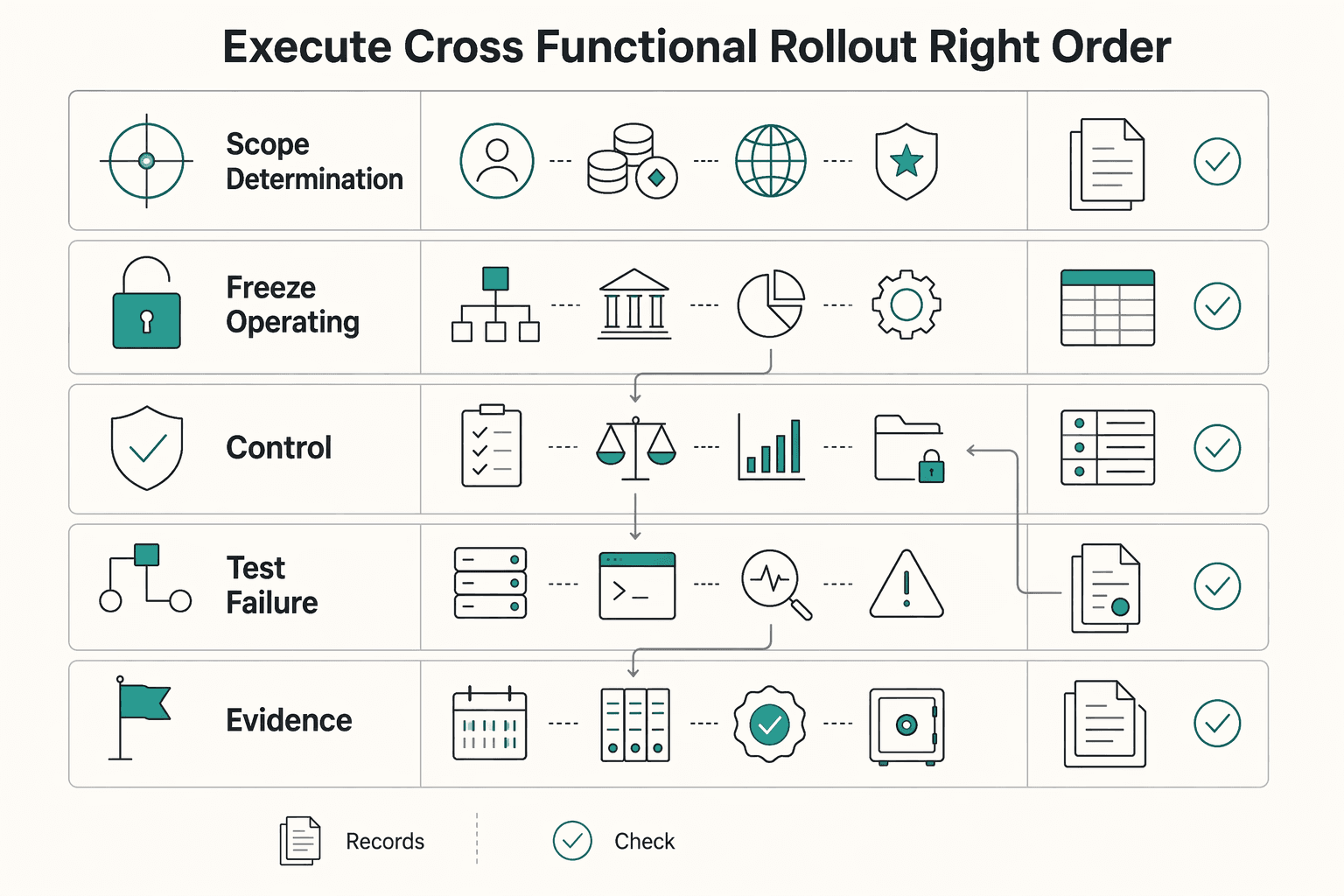

Execute a cross functional rollout in the right order#

Once jurisdiction and partner coverage are locked, rollout order becomes a control decision, not just a delivery plan. Do legal scope first, then operating model, then controls, then integration and testing, then launch approval. That sequence keeps legal, technical, and finance controls aligned before money moves.

- Scope determination comes first

Define which entity serves which users, what crypto-asset is used for payout, and whether your role is CASP-like activity under MiCA. Keep timing explicit in the decision record: stablecoin rules started June 30, 2024, the full service-provider regime became mandatory on December 30, 2024, and transition windows are not uniform across Member States. Sign-off artifact: a short legal memo plus a product scope map covering countries, entity, asset type, and partner dependencies.

- Freeze the operating model before technical work spreads

Choose one route: direct CASP, partner-led, or hybrid. MiCA Title V is the key dependency because it governs CASP authorization, governance, and operational safeguards. The model changes who owns approvals, monitoring, and incident handling. If you use a partner, require concrete authorization or transitional-status evidence. Treat public licence announcements as useful evidence signals, but do not assume another institution's licence automatically covers your activities.

- Design controls before API integration

Define how payouts are approved, created, updated, reconciled, and held or reversed when needed. Engineering checkpoints can include idempotent payout requests, webhook replay safety, status traceability, and auditable mapping from payout request to ledger posting. Operations checkpoints: policy-gated approvals, named exception-queue owners, clear reconciliation ownership, and a written incident path for halt, escalation, and resumption decisions.

- Test failure paths, not just happy paths

Include duplicate submissions, delayed webhooks, out-of-order events, manual holds, failed ledger postings, and reconciliation breaks. Keep evidence for each case and prove replayed events do not create duplicate ledger outcomes. This matters more as activity scales.

- Treat launch as an evidence gate

Go-live should be an evidence review across legal, product, engineering, and finance ops. Authorization status is a core checkpoint because transitional treatment can end before July 1, 2026 if authorization is granted or denied earlier, and supervisory timing still varies by Member State. If reconciliation behavior, approval policies, or incident ownership is unresolved, delay launch. A practical 30-60-90 sequence can keep execution ordered without implying one universal MiCA timeline:

| Period | Primary owners | Deliverables | Evidence artifacts for sign-off |

|---|---|---|---|

| Day 1 to 30 | Legal, product, compliance | Scope memo, country and entity map, operating model decision, partner diligence kickoff | Legal determination note, approved scope map, partner authorization or transitional-status evidence, decision log |

| Day 31 to 60 | Engineering, finance ops, product | Payout lifecycle design, approval policy, ledger mapping, retry and webhook handling, exception process | Sequence diagrams, event-to-ledger mapping samples, approval matrix, reconciliation design, incident escalation doc |

| Day 61 to 90 | Engineering, finance ops, legal, launch manager | End-to-end integration, failure-path testing, dry-run reconciliations, launch checklist and hold criteria | Duplicate and replay test logs, payout-to-ledger trace samples, reconciliation outputs, launch approval record with named sign-offs |

If you need one rollout rule, use this: no launch until you can show who approved each payout, how status changed over time, and how the final ledger entry was produced.

Build the evidence pack before go live not after#

Go-live should depend on records you can produce immediately, not on documentation you plan to finish later. The materials used here do not confirm a MiCA-specific minimum evidence pack. Use a simple standard: if a reviewer asks why a registration, filing, payment, or scheme-status decision was made, the answer should already be in your records.

| Section | What to keep | Grounded details |

|---|---|---|

| Decision spine | Named owners and dates for OSS decision points | Include where you registered (Member State of identification), what filing cadence applies, and how scheme status is maintained. |

| System-of-record proof | Primary records, not last-minute screenshots | Keep registration details, submitted OSS returns, payment records, and record-keeping/audit materials so another operator can reconstruct what was filed and when. |

| External reference log | Official materials relied on, what was checked, and what decision it informed | Prefer official EU pages on the europa.eu domain and avoid relying on unvetted summaries in launch evidence. |

| Jurisdiction and status watchlist | Adjacent EU reporting or tax constraints in the same pack | Keep timing constraints visible, including quarterly or monthly filing cadence and Member State-of-identification lock-in for the current year plus the next two. |

- Decision spine

Keep your OSS decision points together with named owners and dates: where you registered, what filing cadence applies, and how scheme status is maintained. If a key choice has no clear approval history or scope, treat it as not ready for launch.

- System-of-record proof

Build the pack from primary records, not last-minute screenshots. Keep registration details, submitted OSS returns, payment records, and record-keeping or audit materials so another operator can reconstruct what was filed and when.

- External reference log

Track the official materials you rely on and record what was checked, when, and what decision it informed. For verification, prefer official EU pages on the europa.eu domain and avoid relying on unvetted summaries in launch evidence.

- Jurisdiction and status watchlist

If your flow depends on adjacent EU reporting or tax operations, keep those constraints visible in the same pack. OSS is a useful documentation model because it explicitly covers registration, declaration and payment, record keeping and audits, and leaving the scheme. It also shows practical timing constraints, including quarterly or monthly filing cadence and Member State-of-identification lock-in for the current year plus the next two.

Also log publication dates and country-level procedure dependencies for external notices you use. For example, the Commission CBR notice shows 19 APRIL 2024, and CBR requests must follow national VAT-ruling conditions in the participating country.

If you need one hold rule, use this: no go-live until your pack shows registration and scheme choices, filing and payment records, and the official references that supported those decisions.

Watch the failure modes that usually create expensive rework#

Expensive rework usually starts when product, legal, and partner decisions happen out of order. Use your evidence pack as a sequencing control so those gaps show up before launch instead of after it.

| Failure mode | What to confirm now | Grounded cue |

|---|---|---|

| Launching before controls are designed | Confirm you can produce a suspected market abuse case record and map it to a report template and authority contact path. | ESMA specifies arrangements, systems, and procedures for detecting and reporting suspected market abuse, plus coordination procedures between relevant authorities. |

| Assuming harmonized text means identical supervisory practice | Keep a country-risk note in the launch file showing which classification view you relied on and where it may not transfer. | ESMA states there is no commonly adopted application of the MiFID II financial-instrument definition across the EU. |

| Finalizing payout design before classification and partner capability checks | Get a classification memo and partner confirmation on supported assets, unsupported edge cases, and control ownership if the classification view changes. | If legal cannot state the likely category with confidence, freeze product sign-off. |

| Treating open regulatory detail as background noise | Maintain an open-issues log for classification assumptions, cross-border supervisory variance, and technical expectations still evolving through RTS, ITS, and guidelines. | ESMA published its third consultation paper on 25 March 2024, closed consultation on 25 June 2024, and reported 29 responses. |

- Launching before controls are designed

Treat "we will add controls after launch" as a launch blocker, not a scheduling note. Under draft RTS for MiCA Article 92(2), ESMA specifies arrangements, systems, and procedures for detecting and reporting suspected market abuse, plus coordination procedures between relevant authorities. If your payout flow cannot preserve event history, escalation paths, and reportable data fields, you are likely creating later data-model and process rework. Key differentiator: confirm now that you can produce a suspected market abuse case record and map it to a report template and authority contact path.

- Assuming harmonized text means identical supervisory practice

Do not assume one supervisory view travels cleanly across Member States. Regulation (EU) 2023/1114 is EU-wide, but ESMA states there is no commonly adopted application of the MiFID II financial-instrument definition across the EU. That divergence can have practical consequences under MiCA for crypto-assets. Key differentiator: keep a country-risk note in the launch file showing which classification view you relied on and where it may not transfer.

- Finalizing payout design before classification and partner capability checks

Do not lock the payout asset, redemption promise, or settlement flow before classification and partner checks are written down. Get a classification memo covering MiCA scope and whether MiFID II boundary questions are in play, then obtain partner confirmation on supported assets, unsupported edge cases, and control ownership if the classification view changes. Key differentiator: if legal cannot state the likely category with confidence, freeze product sign-off.

- Treating open regulatory detail as background noise

Keep open regulatory detail in active scope because implementation expectations continue to settle through RTS, ITS, and guidelines. ESMA published its third consultation paper on 25 March 2024, closed consultation on 25 June 2024, and reported 29 responses. After translated guideline publication, NCAs have a two-month period to notify ESMA on compliance intent, and guidelines apply three months after translations. Key differentiator: maintain an open-issues log for classification assumptions, cross-border supervisory variance, and technical expectations still evolving through RTS, ITS, and guidelines.

Related: A Guide to the Bank Secrecy Act (BSA) for FinTech Platforms.

Make the decision now and de risk execution#

Decide on one operating model this quarter and document why it fits your plan. Delay is rarely neutral. It hides product risk, pushes legal questions into build sprints, and leaves finance ops cleaning up decisions nobody formally owned.

- Choose one model and write the reason down

Pick the model you will run for the next 12 months, not the one you might want in two years. Document three points: your expected EU growth plan, the compliance capacity you already have, and the payout roadmap you are not willing to slow down. If those do not align, the model may be wrong even if it looks attractive on paper.

Under MiCA, the pressure is operational as much as legal: issuing and trading provisions include transparency, disclosure, authorisation, and supervision of transactions. MiCA entered into force in June 2023. ESMA states Level 2 and Level 3 measures were developed on a 12-to-18-month deadline, with most now in application. Treat "we will clarify later" as a risk signal, not a plan.

- Turn the model into owned checkpoints before you build more product

Once you choose the model, assign explicit checkpoints across legal, product, engineering, and finance ops. Legal should confirm how your payout asset and service shape fit MiCA scope, including potential ART or EMT treatment. Product should lock user-facing promises that depend on that classification. Engineering and finance ops should define control ownership, reconciliation, exception handling, and evidence retention before rollout.

A launch plan is most credible when each function can show an artifact, not just a status update. In practice, that means a decision log, control inventory, payout policy, escalation matrix, and sample audit-trail records. Include a check of ESMA's Interim MiCA Register, including the downloadable crypto-asset service provider file, and the non-compliant entities list. In the cited ESMA excerpt, the register shows Last update: 1 April 2026; if your partner, issuer, or counterparty assumptions fail that check, pause rollout.

- Use partner support where it reduces risk, but verify coverage and accountability

If you need controlled, auditable payout operations with partner flexibility, use Gruv modules where supported and verify coverage before rollout. Be specific: which markets are in scope now, which regulated activities sit with the partner, what evidence you receive for reconciliation and incident review, and who owns user-impacting exceptions.

Do not treat listing status as approval status. ESMA states listed crypto-asset white papers have not been reviewed or approved by a competent authority, and the issuer or offeror remains responsible for the content. Also avoid assuming implementation is uniform in practice across Member States. Secondary reporting still notes divergent national interpretations and open questions on MiCA interaction with existing payments and investment-services rules. If your expansion plan depends on uniform treatment, tighten those assumptions before scaling.

For the broader EU payments framework around these decisions, read PSD3 and PSR: What the Next EU Payment Regulation Means for Platform Operators.

If your team is moving from decision to rollout, align legal, product, and engineering on one implementation checklist with clear evidence outputs: Read Gruv Docs.

Frequently Asked Questions

What does MiCA require from crypto platforms in one sentence?

MiCA obligations should be verified on official EU pages on the europa.eu domain. Implementation guidance typically includes operational details such as record keeping and audits. Confirm the specific requirements that apply to your platform with legal counsel.

Does MiCA apply the same way across all EU countries?

Verify country-level MiCA execution directly with the relevant authority rather than relying on EU-level summaries. A relevant pattern from OSS: you register in one Member State of identification, and that choice can bind you for the current calendar year plus the next two. Treat country execution as something to verify directly.

What are the key milestones teams should anchor to?

Verify MiCA phase-in milestones in official implementation guidance. The kinds of milestones teams should expect include registration, declaration and payment, record keeping and audits, and leaving the scheme. If guidance stays at principles and skips those checkpoints, it may not be implementation-ready.

Can a non-EU platform serve EU users without EU setup?

For MiCA questions on non-EU access or reverse solicitation, confirm with legal counsel. A relevant pattern from VAT: participation can be optional, but once you opt in, scope obligations apply. In OSS, that means declaring all supplies in the chosen scheme through OSS returns, with quarterly returns for Union and non-Union schemes and monthly returns for the import scheme.

Where should operators verify current implementation status?

Use official EU pages first. Official EU website addresses are in the europa.eu domain. For VAT, relevant dated artifacts include the CBR page (19 APRIL 2024) and guides (30 JULY 2021). For MiCA-specific register or ESMA-tracker checks, verify directly with the relevant authority.

What is still unclear from public summaries?

The risky gaps are usually procedural detail: filing steps, record-keeping duties, and what happens if a Member State excludes a taxable person or intermediary from a scheme. The VAT pages make that concrete by covering record keeping and audits and by stating that a taxable person or intermediary can be excluded from an OSS scheme by a Member State. They also note that online marketplaces can have record-keeping duties even when they are not treated as the deemed supplier.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- esma.europa.eu/sites/default/files/2024-12/ESMA75-453128700...trusted

- esma.europa.eu/esmas-activities/digital-finance-and-innovat...trusted

- law.georgetown.edu/international-law-journal/wp-content/uploads...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC12883517trusted

- scholarship.law.vanderbilt.edu/context/vjtl/article/2772/viewcontent/Global...trusted

- sec.gov/files/ctf-written-input-daniel-bruno-corvelo...trusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platform Operators Should Prioritize PSD3 and PSR Controls

Treat [PSD3 and PSR](https://finance.ec.europa.eu/publications/financial-data-access-and-payments-package_en) as a control-prioritization exercise now, not a project to begin only after the final political text lands. For online platforms and Technical Service Providers, separate what you can verify today from what still depends on final European Union wording. Then build only the controls that reduce downside without locking you into the wrong model.

Bank Secrecy Act Fintech Decisions That Prevent Review Delays

Start with one decision: choose the control model you can prove before launch. Know what to put in place before go live, what a bank partner will likely ask for, and which proof points help avoid long review loops.

Choosing Between a New York Money Transmitter License and BitLicense

Licensing scope is the first call, not form filling. If you are evaluating New York BitLicense exposure, decide whether your activity points to a BitLicense, a limited purpose trust company path, or a narrower next step while your model is still constrained.