Quick Answer

Define point meaning and posting rules first. For a contractor rewards wallet build, lock what counts as Qualifying Purchases, require evidence on Invoice Submission and Code Submission, and trace one sample claim from intake to redemption before expanding. Then pick coalition or branded structure using your Build vs Buy Model, and keep Online Marketplace, invoice credit, and payout-linked redemption as separate flows with clear status checkpoints.

Why Use Your Platform Wallet for Contractor Rewards#

A contractor rewards program with a wallet is a money movement design problem, not just a marketing feature. The moment reward points can become stored balances inside a platform wallet, your team is no longer only shaping engagement. You are deciding how value is recorded, reconciled, and, where supported, moved on top of bank and payments infrastructure.

That shift matters because loyalty programs are long-term incentive tools, not one-off promotions. They can be measurable when rewards are tied to specific behaviors, but many still underperform because of low retention and redemption, time delays, and cost pressure. In a wallet-backed model, those pressures turn into day-to-day operational questions, not just program metrics.

What to decide before anyone writes a spec#

Before anyone writes a spec, answer three questions. They expose scope gaps early:

| Decision | What to clarify | Why it matters |

|---|---|---|

| What points become | Front-end score, non-cash perk, or value that converts into stored balance | If conversion is even a future possibility, treat it as a wallet design from day one |

| Source of truth | Centralized transaction data rather than screens, catalogs, and statements | It is the record you reconcile against and use to explain each balance change |

| Ownership line | Product owns experience choices; finance and ops handle reconciliation, delays, and redemption disputes | If those teams are not in scope early, the build will drift |

- Decide what points become. Are points just a front-end score, a non-cash perk, or value that converts into stored balance? If conversion is even a future possibility, treat it as a wallet design from day one.

- Name the source of truth. Screens, catalogs, and statements are views. They are not the record you reconcile against. You need centralized transaction data that can explain each balance change.

- Set the ownership line. Product owns experience choices, but finance and ops will handle reconciliation, delays, and redemption disputes. If those teams are not in scope early, the build will drift.

A simple starting checkpoint is to pick one qualifying purchase or claim and trace it from source event to earn decision to balance update. If you cannot follow that path cleanly, pause. That break is usually where reconciliation and ownership gaps show up first.

Why this is really about balance governance#

Treat this as balance governance, not just rewards design. Some teams bring payments capabilities in house because they want tighter control of the experience, lower third-party costs, or features like balance-based spending and instant payouts. The same logic applies here. Once rewards live in the wallet, you need explicit rules for when value is earned, when it becomes redeemable, and how exceptions are handled.

What this guide will help you narrow#

Use the rest of this guide to narrow scope before you scale. We are not going to stay at the level of "rewards improve loyalty." The useful questions are narrower: what your first release includes, what transaction evidence you need before build starts, how earn and redemption flows should work, and how to respond when balances or redemptions do not match expectations.

If you can explain every balance change in plain English and match it back to the underlying transaction trail, you are ready to build a loyalty model that can grow without losing control.

Set the system boundary before writing any product spec#

Set the boundary before writing specs so every team is building the same program, not different interpretations of it. Write one shared definition across product, finance, and operations before design mocks or vendor demos drive scope.

What should reward points mean in version one?#

Define reward points in plain language for v1, and keep that definition consistent everywhere. If the team has not finalized what points represent, avoid product copy that implies broader redemption, portability, or wallet behavior than you can support now.

Use a quick alignment test: give product, ops, and finance the same scenario and ask, "What did the contractor earn, and what can they do with it today?" If answers differ, the boundary is still unclear.

Where does the system boundary usually break?#

Separate experience surfaces from system records. Enrollment pages, tier messaging, and offer copy explain the program, but they should not substitute for the internal records you use to decide eligibility, status, and corrections.

Keep a short artifact list that explicitly splits customer-facing pages from internal state records. That keeps support handling, product messaging, and implementation decisions aligned.

Why freeze first-release scope in writing?#

Freeze v1 scope in writing, then hold the line. List qualifying earn events, redemption types, expiration policy, and any manual-override paths; if it is not in that note, it is out for v1.

Choose tooling after scope is locked. Build choices can span a low-code to pro-code continuum, but that flexibility should not expand first-release scope by default.

For wallet design details, read What is a Multi-Currency Wallet for a Platform? How to Build Sub-Wallets for Each Contractor.

Prepare the minimum evidence pack before build starts#

Do not start build until inputs, assumptions, and proof points live in one working pack. If key decisions are still scattered across Slack threads or vendor decks, your MVP is not ready. The minimum version should still reduce risk and help the team learn through real-world validation.

| Pack component | Include | Check before build |

|---|---|---|

| Written inputs | Program terms, definition of Qualifying Purchases, redemption catalog logic, and finance assumptions for breakage and deferred liability | Label finance assumptions as policy, current estimate, or validate after launch; only hardcode policy items |

| Ownership matrix | Product, engineering, finance, and ops for Treasury Workflows, exception handling, and customer support escalation | If key rows say team or TBD, ownership is still unresolved |

| Build-ready artifacts | Event dictionary, state transition diagram, and reconciliation outputs tied to Auditable Purchasing Data | Posted value should trace back to auditable purchase evidence |

| Release-stage checkpoints | Test data source, posting validation, redemption settlement validation, and what complete enough means for the Audit Trail | Use the same sample transactions from design review through staging |

Gather the written inputs that define version one. Collect the program terms, your definition of Qualifying Purchases, the redemption catalog logic, and finance assumptions for breakage and deferred liability. The goal is not perfect coverage of every future edge case. It is explicit, versioned assumptions so product copy, ledger logic, and support guidance all reference the same source.

Handle finance assumptions as forward-looking. Label each one as policy, current estimate, or validate after launch, and only hardcode policy items.

Assign owners before tickets are written. Set an ownership matrix across product, engineering, finance, and ops for Treasury Workflows, exception handling, and customer support escalation. Keep it simple, but specific enough to answer who decides, who approves, and who executes.

If key rows still say team or TBD, ownership is unresolved and implementation risk stays high.

Turn the pack into build-ready artifacts. Before implementation, require an event dictionary, a state transition diagram, and reconciliation outputs tied to Auditable Purchasing Data. In practice, this gives engineering, finance, and ops a shared reference for what happened, why it happened, and how to trace value movement back to purchase evidence.

If posted value cannot be traced to auditable purchase evidence, fix that before release.

Define verification checkpoints for each release stage. Choose validation checks before QA. For each stage, define:

- the test data source

- how posting validation is confirmed

- how redemption settlement validation is confirmed

- what

complete enoughmeans for the Audit Trail

Use the same sample transactions from design review through staging so drift is visible. Only move forward when the team can trace one sample purchase from source data to posted reward to redemption outcome, with each balance change explained in the audit record.

Choose your program model with explicit tradeoffs#

Choose the model based on ownership and dependency risk, not demo polish. Your decision should be explicit on economics, operational risk, and who controls changes after money starts moving.

Which model fits your operating reality?#

Compare a Coalition Rewards Program and a Branded Contractor Loyalty Program directly, then treat the result as a testable decision, not a slogan. The key question is who controls rules, data, and change rights when exceptions, reversals, and support escalations happen.

Set one non-negotiable checkpoint before you commit: name a single accountable owner for the program's financial engine and financial narrative. If that owner is unclear, pause the decision. Without clear ownership, you are likely to inherit liability and operations risk without real control.

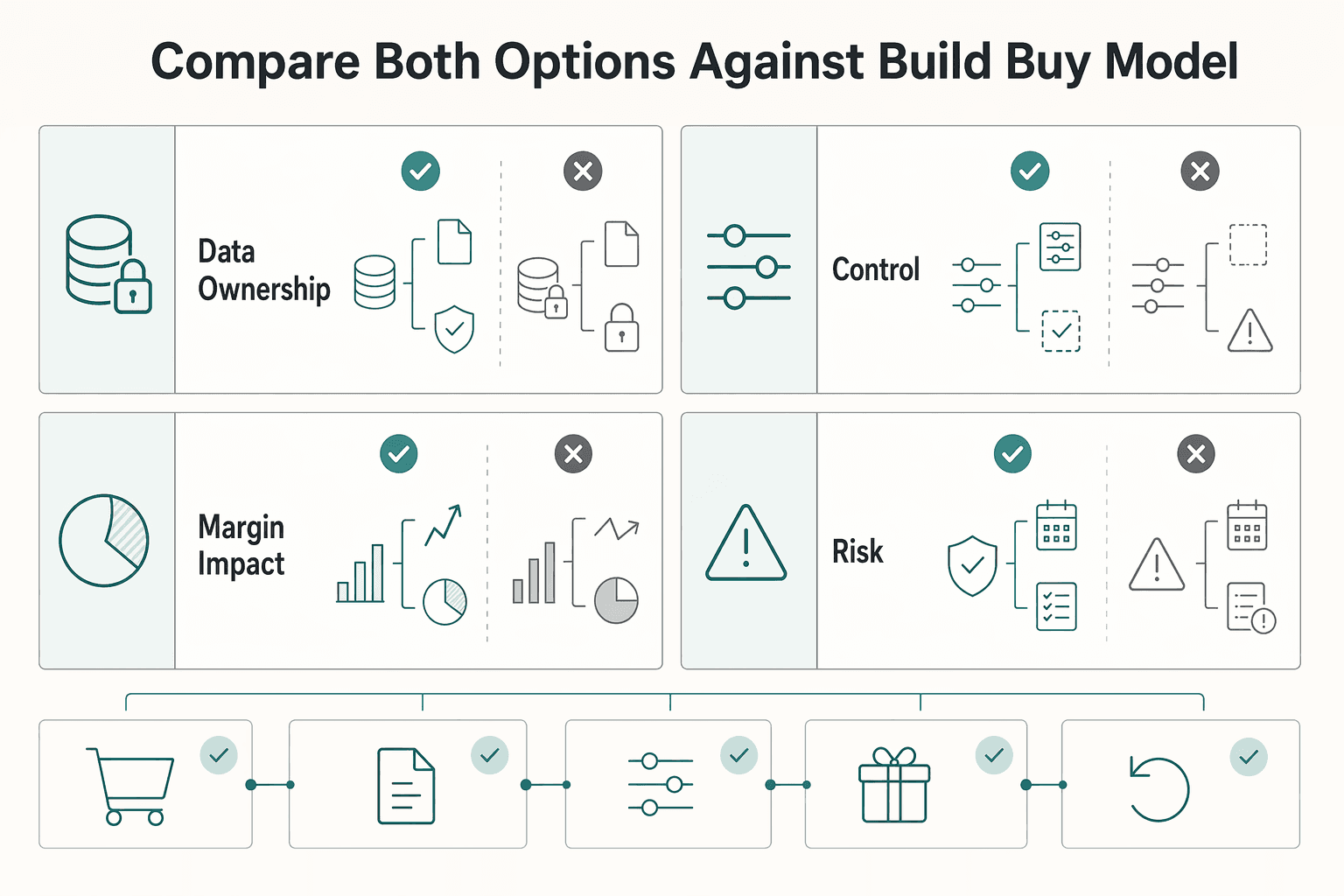

Compare both options against your Build vs Buy Model#

Write the evaluation against your internal Build vs Buy Model so each tradeoff is decision-ready and auditable.

| Decision area | Coalition Rewards Program checks | Branded Contractor Loyalty Program checks | Evidence to collect now |

|---|---|---|---|

| Data ownership | What contractor, purchase, balance, and redemption data is available at event level? | What posts to your own systems vs partner-managed systems? | Event-level export sample, schema, data terms |

| Roadmap control | Which changes depend on external queues, contracts, or release timing? | Which changes your team can ship directly vs through dependencies? | Change process, SLA, approval path |

| Margin impact | Which costs scale with claims, redemptions, and servicing volume? | Which costs shift to internal engineering, finance, and ops? | Fee schedule, staffing plan, finance assumptions |

| Migration risk after year one | How portable are identities, balances, and historical events? | How portable are posting rules, IDs, and reconciliation outputs? | Termination terms, export spec, history sample |

Do not rely on summary dashboards alone. Validate at least one full transaction story end to end: qualifying purchase, posting, adjustment, redemption, and reversal, with traceable IDs and timestamps at each step.

For fund protection and wallet structure, read FDIC Pass-Through Insurance for Platform Wallets: How to Protect Your Contractor Funds.

Design the data and posting model that powers the wallet#

Build the model around one standard: every balance-impacting action must be traceable so you can maintain accountability for transactions.

Before you finalize wallet logic, define what counts as an accepted submission event and what does not. A practical control model is the same one used in secure submission flows such as INFORMS: treat a submission as valid only after it is fully entered, uploaded, acknowledged (Confirm), and recorded in the system.

Apply that control consistently across your claim inputs:

- Accept claims only through approved digital channels.

- Treat late or incomplete submissions as not accepted by the system.

- Do not let hardcopy, email, fax, or ad hoc attachments bypass the defined intake path.

- If an exception is necessary, route it through a documented manual path so the decision is still auditable.

Design wallet operations and support views for complete traceability from intake through posting and settlement states, so your team can explain what was submitted, what was accepted, and what changed.

If your wallet roadmap also includes faster access to earnings, read Earned Wage Access Architecture: How to Build EWA Into Your Gig Platform.

Build redemption and payout paths without hidden liability drift#

Once your posting history is stable, keep redemption paths separate so status and recovery logic stay clear. Model Online Marketplace, direct invoice credit, and payout-linked wallet redemption as distinct flows, even if the user sees one redeem action.

Which redemption destinations need separate paths?#

Define path-specific checkpoints before launch:

| Redemption path | What to decide up front | Posting checkpoint to define |

|---|---|---|

| Online Marketplace | When value is considered committed vs still available | Post redemption only after the order/reservation event you trust |

| Direct invoice credit | Which invoice-side event makes credit final | Start as pending, then finalize only after your confirmation event |

| Payout-eligible wallet balance | Which states make a request payable | Keep non-payable until required states are complete |

Direct invoice credit is where timing mistakes are most common. In one documented flow, a customer sees a Pay with Crypto option and can send stablecoins from a compatible wallet. Payments typically confirm within a few minutes, and after on-chain confirmation, funds settle into the account within seconds. A small fee applies when crypto is on- or off-ramped and can be passed to the customer or absorbed. If you connect redemption to invoice settlement, treat request time and settled-funds time as separate states.

Verification checkpoint: for one sample redemption in each path, point to the exact event that changes status from "requested" to "posted."

When should payout-linked redemption stop before money movement?#

If you support payout-linked redemption, define explicit eligibility gates before a request can become payable. Typical controls include identity status, policy checks, and manual review when needed. Keep this fail-closed: missing, stale, or failed required status should stop progression.

One market taxonomy explicitly treats Client Onboarding & Identity Verification as a distinct business need, which is a useful signal to keep identity checks as a first-class gate in your flow.

When do cash-moving requests need treasury approval?#

If redemption triggers real cash movement, define treasury controls as internal policy. Common patterns include approval steps, separation of duties, and higher scrutiny for larger payouts. Record enough evidence to trace request, approval, and release without editing history.

How should failure recovery work before launch?#

Document failure handling before go-live, with reversal order and auditability defined in advance:

| Failure case | Defined recovery step |

|---|---|

| Failed redemption | Keep the original posting, mark failure state, then add reversal/release postings |

| Stale balance view | Reject the second action with a clear duplicate or insufficient-balance outcome |

| Partial settlement | Keep unsettled value pending and post settled value separately |

| Reversal sequencing | Reverse in order and preserve the Audit Trail across request, approval, settlement attempt, failure, and correction |

For a step-by-step walkthrough, see How to Build a Trust and Safety Program for Your Contractor Marketplace.

Run operational controls that catch abuse early#

Put abuse control inside posting control from day one, because once value can become invoice credit or payout, weak review becomes a balance integrity risk.

What suspicious earn activity should be stopped before posting?#

Stop suspicious earn activity before it reaches the wallet. Put pre-posting checks on suspicious Qualifying Purchases, repeated Invoice Submission, and synthetic claim patterns across related accounts, and hold claims when repeated evidence or highly similar cross-account patterns appear instead of auto-posting through the Rules Engine.

Use a small, fixed abuse-reason taxonomy rather than free-text labels. You can align internal categories to documented risk buckets: the 2026 National Money Laundering Risk Assessment has dedicated sections for fraud, cybercrime, and digital assets, and the 06/23/2025 NIBRS manual updates add Identity-Related Fraud Offenses. That structure helps you separate duplicate-claim behavior, identity-linked concerns, and potential account-linking abuse.

Verification checkpoint: for one blocked or held claim in each category, confirm you can show the claim event, rule hit, hold status, and final reviewer disposition without editing history.

How should exceptions move through manual review?#

Run a defined exception queue, not a generic "fraud review" bucket. Each held claim should have an owner, a team-defined SLA, a disposition code, and a small outcome set the Rules Engine can apply consistently: approve and post, reject and close, request more evidence, or escalate.

Require a consistent evidence pack. For questionable Invoice Submission, include the source document, related prior claim IDs, account-relationship notes when relevant, and the reviewer's reason code; for higher-risk cases, add second review, especially when patterns suggest identity misuse or insider involvement. The 2026 NMLRA's Complicit Insiders topic is a useful reminder that not all abusive patterns are external.

Do not let reviewers "fix" balances outside the queue. Decision changes should create a new recorded outcome, not overwrite the original hold.

Which leading indicators should you review every week?#

Review four signals weekly: claim rejection reasons, delayed validation backlog, redemption dispute rate, and unresolved balance mismatches. The goal is not a perfect dashboard; it is early movement detection so you can tighten controls before cleanup work expands.

If one rejection reason dominates, tighten upstream rules or clarify contractor guidance. If delayed validations grow, add review capacity before held claims become support debt. If mismatches persist week to week, pause new rule changes until each mismatch can be traced from source event to posting outcome.

Related: How Platforms Use Pooled Wallets vs. Individual Wallets for Contractors.

Launch in phases with hard go live gates#

Do not expand this program until you can prove the first cohort works end to end and you know the stop rules.

-

Start narrow and keep redemption simple. Launch with a constrained cohort and one low-complexity redemption path before broadening into

Disbursements/ Payouts. Validate the full trail from earn event to posting, redemption outcome, settlement status, and support history in source records. -

Use explicit go/no-go gates with owners. Keep gates on posting accuracy, reconciliation pass rate, support ticket severity, and payout exception stability, and require evidence that does not depend on ad hoc explanations. If support is staffed in windows like Monday - Friday 7a - 11p, do not widen access right before unstaffed periods.

-

Predefine rollback behavior for each critical flow. Set one rollback rule each for earn accrual, redemption, and settlement, such as disabling new accrual, pausing redemption, or routing settlement to manual handling. Treat Roll Back Pending Record Changes as the operating principle: decide in advance what reverses on failure and what is held for review.

-

Publish the post-launch review checklist before adding scope. Keep it operational: economics drift, fraud signals, unresolved reconciliation items, support themes, and integration debt from temporary fixes. Include contractor-facing pause messaging and clear routing between merchant support and technical support.

Related reading: How to Launch a Referral Program for Your Gig Platform with Built-In Commission Tracking.

Conclusion#

The goal is not speed. It is shipping a contractor rewards program that your finance and support teams can explain line by line without falling back to spreadsheets, chat threads, or manual guesswork.

Build for proof, not just launch#

If you want this program to last, treat every reward as an operational record before you treat it as a growth feature. The emphasis on a rules engine and real-time reporting across distributors, dealers, reps, and end-users points to the same conclusion: the core asset is visibility and operational discipline, not the catalog screen. Your first verification checkpoint is simple: can someone trace one reward outcome from claim source, to validation result, to earn posting, to redemption outcome in one auditable path?

If the answer is no, you are not ready to widen redemption or push volume. A common failure mode is a good-looking launch that still depends on manual tracking and spreadsheet repair behind the scenes. That is where hidden costs start to compound.

Keep the rules deterministic and the boundaries tight#

The operator habit that matters most is defining what the program does and what it does not do before engineering starts filling gaps with exceptions. Rules-based promotions only work when the same qualifying event produces the same outcome on replay. That means your evidence pack should include the event dictionary, validation logic, posting states, and exception reasons, not just program terms and UX mocks.

Warnings about common loyalty strategy missteps are useful here because most failures are not dramatic. They often show up as vague ownership, overly broad promises, and reporting that cannot answer basic finance questions. A practical red flag is any proposal that celebrates fast setup but stays vague on reconciliation and channel-level buying data.

Scale only when balances are boring#

You are ready to scale when a stored balance stops being a debate. In plumbing-focused contexts, contractor influence over product choice can be significant. One source puts that influence at 60 to 80 percent of product selection, which helps explain why some brands treat loyalty as a revenue engine rather than a giveaway. But strategic value only becomes durable when balances are governed well enough to support growth without constant exceptions.

So end with one hard rule for this build: if you cannot explain every balance change from claim to redemption with an immutable record, pause expansion. Tight verification gates, channel data visibility, and deterministic posting are what keep a promising rewards idea from turning into an expensive support and finance problem. When those pieces are in place, scaling becomes a choice rather than a risk.

Frequently Asked Questions

What is a contractor rewards program platform wallet in practical terms?

It is the wallet layer where approved reward activity becomes a balance you can show, redeem, and reconcile. In some setups, that wallet sits alongside online checking, team debit cards, and expense management. In a sponsor bank model, the product company may not be the bank at all: Buildertrend states it is a technology company, not a bank, and that Piermont Bank holds the funds.

What are the minimum components needed to launch one safely?

At minimum, you need a customer-facing experience, an internal admin view, and a wallet flow to pay out and manage rewards. In referral stacks, this can include a customer app, sales app, admin dashboard, and wallet. For account protection, use verified contact info, multi-factor authentication, and session timeout. If cash movement is in scope, define the sponsor-bank custody boundary clearly.

How should teams choose between a coalition model and a branded model?

Choose a partner-currency or coalition-style approach if you want rewards without issuing your own points at launch. Choose a branded model if you want to run your own points currency and program controls. Do not assume a points program means you must create your own currency, because issuing your own points is not the only valid model.

How do invoice and code claims become wallet balances step by step?

Exact claim logic depends on the platform and program rules. A practical flow is to capture the claim event, validate it against qualifying rules, then post the earn event and expose the updated balance for redemption. Prioritize traceability from source event to posted balance.

What does build scope include beyond frontend and reward catalog design?

The scope usually extends beyond frontend and catalog design into admin operations and payout management. In referral stacks, vendors often bundle more than the consumer app, including a sales app, an admin dashboard, and a wallet to pay out and manage rewards.

What unknowns should we validate in vendor proposals before signing?

Ask exactly when billing starts, what onboarding includes, and what "live" means. One vendor, GTR, says billing begins at contract signing and the start of onboarding, not app go-live. It also says app-store access may happen within 3 business days while full implementation averages about 2 weeks, and that successful referral programs need at least 6 months to scale. Early access and production readiness are not always the same milestone.

When should reward balances be redeemable to payouts versus marketplace-only redemption?

Keep redemption limited to non-cash options until posting accuracy, reconciliation, and support handling are consistently stable. Move to payout redemption only after your operating controls are reliable end to end. If unresolved balance mismatches remain, do not add payout redemption yet.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- edps.europa.eu/data-protection/our-work/publications/techdi...trusted

- file.lacounty.gov/SDSInter/bos/supdocs/213493.pdftrusted

- govinfo.gov/content/pkg/FR-2017-03-01/xml/FR-2017-03-01.xmltrusted

- home.treasury.gov/system/files/246/2026-NMLRA.pdftrusted

- loudoun.gov/DocumentCenter/View/217408/RFQ-683930-PDFtrusted

- miamidade.gov/Apps/ISD/StratProc/ProcurementNAS/pdf_Files/...trusted

- michigan.gov/-/media/Project/Websites/dtmb/Procurement/Co...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC8762990trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Build Multi-Currency Sub-Wallets for Contractors

**Short answer:** treat sub-wallets as an operating choice, not just a balance view in your product. The core decision is not about UI. It is about where money lives, what a balance actually represents, and what your team will need to reconcile later.

How Platforms Use Pooled Wallets vs. Individual Wallets for Contractors

Choose pooled wallets when your platform needs centralized control over funds and operations. Choose individual wallets when users must control private keys and accept the recovery boundary that comes with that choice.

The Best Tools for Tracking Your Credit Card Points and Miles

**Pick a stack based on your failure mode (choosing the wrong card vs losing visibility), then run a simple recurring check so you can keep rewards visible without turning them into admin work.** If you're a business of one, rewards only matter if the system runs without stealing focus from client work.