Quick Answer

Build the process around one intake form, fixed evidence rules, and a triage-to-closeout path before cases scale. Tie each ruling to Ledger journal and ERP records, separate reviewer and approver authority with RBAC, and require written reasons when proof is insufficient. Keep negotiation time-boxed, escalate contract-meaning conflicts to legal review, and keep final determinations and settlement actions under human approval even when AI support is used.

What a fair payment dispute process needs#

A dispute process that stays fair under volume has to be designed up front, not improvised when urgent cases hit. This guide is for platform finance, ops, and product owners building or adapting an internal contractor payment dispute process that is fair, usable, and auditable.

Fairness does not happen by default. Process design can privilege some perspectives over others, and vague rules can push reviewers toward inconsistent judgment. A workable process uses a consistent timeline, asks for consistent minimum evidence by issue type, and records why any exception was made.

The focus here is operational execution, not abstract policy. Decide who reviews, who approves, what evidence is enough to decide, when negotiation continues, and when escalation starts. In practice, that means grounding each decision in documented records and explicitly logged changes.

One early checkpoint matters: confirm that the underlying records and timeline agree before you rule. If records conflict or key changes were not documented, resolve that gap first. Rushing to approve or deny can create a second dispute.

Plan for repeat exceptions, not just one-off cases. A scalable process handles recurring cases across teams without rewriting the rules each time.

Ambiguity is a common trigger: unclear rights, obligations, milestones, or payment terms, plus informal undocumented changes. A practical control is to set a clear timeline at intake and document changes carefully. Negotiation-first handling can reduce escalation, but final determinations and settlement actions should still be human-validated, including when AI-supported tools are used.

By the end, you should have a design that separates evidence review from opinion, clarifies decision rights, and leaves a defensible case file months later.

Related reading: How to Handle Payment Exceptions at Scale: Routing Disputes Corrections and Manual Overrides.

Define fair process rules before you open intake#

Set fairness as policy before intake opens. Equivalent dispute types should follow the same evidence standard, the same review steps, and the same appeal path, with any exception documented.

- Write fairness as a repeatable rule

Treat your dispute channel as a formal grievance mechanism with clear criteria and outcomes. For each dispute type, define the intake and review steps and what qualifies as a valid first response. A practical check is simple: two reviewers using the same case packet should reach the same next step without unwritten guidance.

- Separate authority by risk and complexity

Keep intake, review, approval, and escalation responsibilities distinct where risk and complexity justify it. You can calibrate separation by case risk instead of forcing one model across all disputes. That keeps independence and speed in balance while making ownership explicit.

- Anchor decisions to source records

Your determination should be traceable to the internal records used in the review. If the note explains the conclusion but not the record trail, you have an opinion log, not an audit-ready case file.

- Define "insufficient evidence" before the first dispute arrives

Do not leave this to reviewer instinct. State what is required by dispute type, and require reviewers to name what is missing in writing when evidence is insufficient. Avoid vague requests like "send more proof," which create uneven treatment and unclear follow-up.

If legal or regulatory text informs your policy language, verify it against an official legal edition. Do not rely on prototype Federal Register text alone.

We covered this in detail in Internal Payment Audit Trail for Platform Compliance.

Set prerequisites and owners before launch#

Once the rules are set, launch discipline matters just as much. Before launch, lock key controls in writing: ownership, risk gates, and case-state synchronization. Use a checklist artifact for go-live so each handoff and stop condition is explicit and testable.

| Step | What to define | Why it matters |

|---|---|---|

| Assign owners by decision point | Name one accountable owner for each major decision and handoff; define who can change status and who approves movement between key states | Makes each handoff explicit and testable |

| Define risk gates and outcomes | Document which policy gates can pause actions, who can clear each gate, and clear outcomes for gated cases | Calibrates controls to the level of risk and complexity |

| Set one system of record and sync rules | Choose where status is authoritative, then define when it syncs with related operational systems | Prevents status drift across stages |

| Prewrite contractor-facing notices | Prepare core notice templates before intake opens and validate them against governing contracts and legal authorities | Keeps notice language ready before launch |

- Assign owners by decision point

Name one accountable owner for each major decision and handoff in the process. Define who can change status and who approves movement between key states.

- Define risk gates and outcomes

Document which policy gates can pause actions and who can clear each gate. Define clear outcomes for gated cases, and calibrate controls to the level of risk and complexity rather than forcing one path for every case.

- Set one system of record and sync rules

Choose where status is authoritative, then define when it syncs with related operational systems. Treat lifecycle coverage as a launch requirement so status does not drift across stages.

- Prewrite contractor-facing notices

Prepare core notice templates before intake opens. When notice language draws on manuals or policy references, validate it against your governing contracts and legal authorities, because reference manuals can be informational rather than controlling.

Classify dispute types into one intake path#

One intake path is usually enough. Use a single guided intake with structured choices, then branch behind the form. This keeps case selection sound, consistent, and transparent instead of letting similar disputes come in through inconsistent channels.

Build one guided intake form#

Treat intake as a step-based web flow that steers the submitter toward the right case type. Start with structured categories and a short context field instead of relying on free text alone.

Keep the form single and do the routing underneath it. Multiple entry forms and ad hoc channels can make case-selection decisions less consistent and less transparent.

Split major case families early#

Define major case families early, and test the workflow in one clearly scoped case type before broader rollout. Consider placing one required classification question near the top of the form, and keep the original selection visible if triage reclassifies the case later. This supports a more transparent selection process and makes intake quality easier to improve.

Add governance checks before rollout#

Before publishing the intake path, confirm that it aligns with the rules and requirements already governing your dispute process. If intake changes how cases are classified or escalated, run legal analysis before launch, not after live cases appear.

Capture core context for escalation#

At intake, capture the core case context needed for later review and escalation. You are not deciding legal effect at this stage. You are preserving the record so later review does not stall on missing context.

For the full breakdown, read How to Build a Payment Reconciliation Dashboard for Your Subscription Platform.

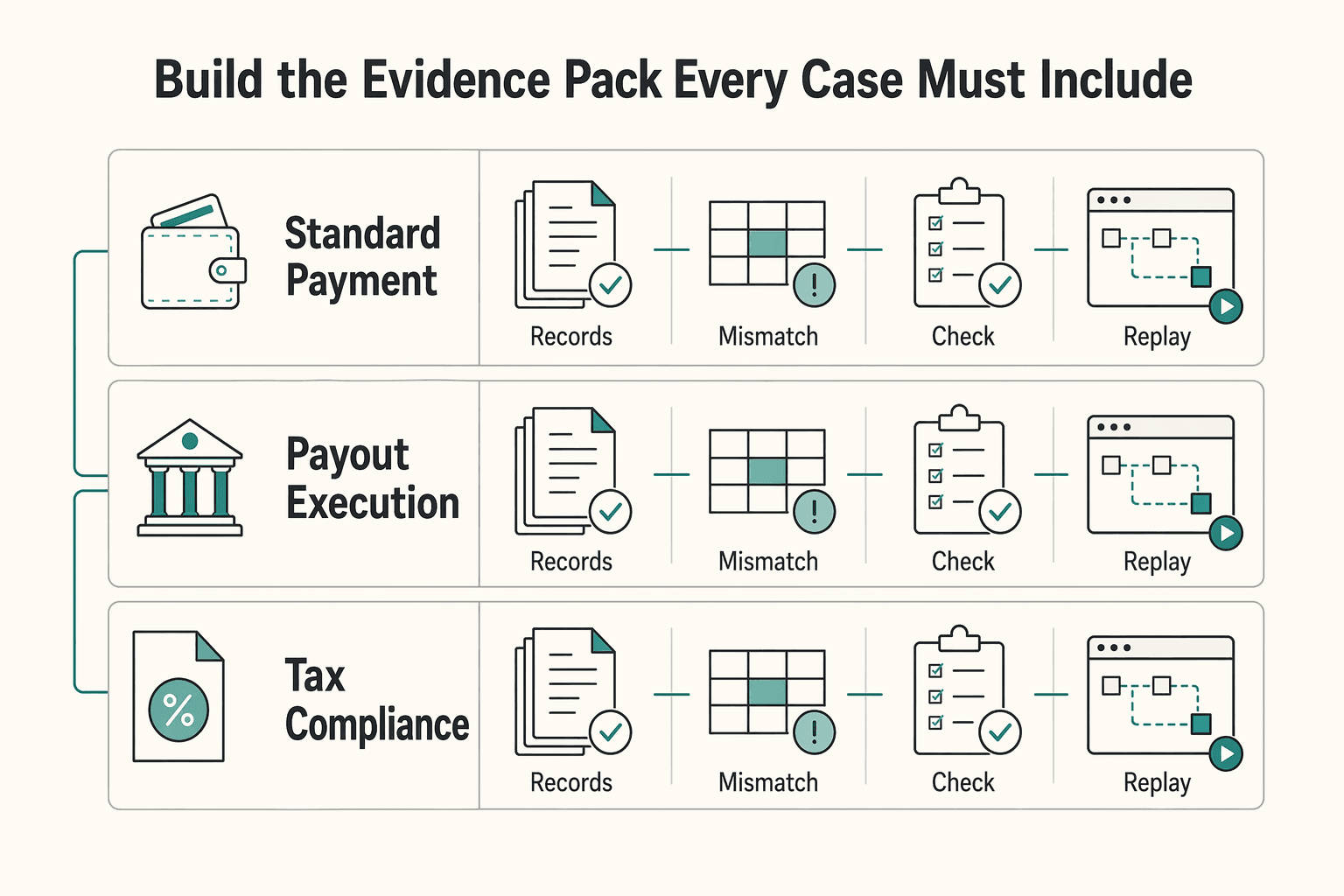

Build the evidence pack every case must include#

Review quality rises or falls on the case packet. Make the evidence pack explicit before review starts, and keep it consistent enough that a second reviewer can reconstruct the case without chasing side-channel context. Use dispute-type-specific fields as internal policy controls, not as claims about universal legal requirements.

A practical anchor from IRS file discipline is IRM 8.6.1, which includes Copies of Written Communications in the case file. The same operational principle applies here: if a decision depends on a message, approval, or notice, keep that written record in the case file.

| Dispute lane | Internal packet (policy-defined examples) | Review checkpoint | Common failure mode |

|---|---|---|---|

| Standard payment dispute | Example internal records: payment object ID, linked Ledger journal entry, ERP invoice reference, written communication copies, settlement timestamp | Can another reviewer trace invoice to settlement without extra context? | Screenshots are present, but system IDs or journal links are missing |

| Payout execution dispute | Example internal records: provider reference, webhook history, idempotency log tied to the Idempotency key, Payout batches context, communication copies | Can you reconstruct request, provider response, webhook sequence, and final posting state? | A provider status is shown, but replay or duplicate risk cannot be proven |

| Tax or compliance hold dispute | Example internal records: current tax profile, relevant forms when your policy requires them, and control outcome records | Is this missing documentation, execution failure, or a control state? | Tax or compliance holds are handled as payout rail failures |

Define the minimum file by dispute type#

Publish a short evidence matrix with intake rules so reviewers know what must be present before a decision. Put internal identifiers and record links ahead of narrative.

Stress-test the standard by handing a case to someone who did not triage it. If they cannot identify the disputed amount, authoritative record, and key written communication from the packet alone, the file is not ready.

Add sequence evidence for payout cases#

For payout execution disputes, include artifacts that let you prove sequence and final state, not just point-in-time status. This is an internal reliability choice so your team can test retries, duplicates, and posting outcomes.

The core question is operational: what did the platform send, what did the provider acknowledge, what did webhooks report, and did any replay or batch process change the result?

Keep tax-hold review tied to current documentation#

When a case involves a tax-related hold, classify it with current documentation, not payment data alone. If your process depends on tax profile or forms, keep those records in the packet before deciding release or reversal.

This prevents routing mistakes between documentation gaps, reporting mismatches, and true execution defects. For related reporting context, keep IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments in the reviewer toolkit.

Separate control outcomes from payment outcomes#

If controls flagged the case, record the control outcome clearly in the file and show how your policy treats that state. Review quality drops when teams cannot distinguish one control state from another.

Also formalize missing-record retrieval as its own task. IRM 8.6.1 includes a specific file-preparation checkpoint, Preparing and Completing the STARS Request, and that discipline translates well to dispute operations. For high-impact decisions, preserve the approval artifact in the file, consistent with formal approval-process patterns such as Written Supervisory Penalty Approval Process. If FederalRegister.gov text is used in legal reasoning, treat it as research until it is verified against an official edition.

Run the internal sequence from triage to closeout#

Use a grounded sequence: define scope and objectives, assign responsibilities and authority, complete internal case research, communicate clearly, and use reporting and appeals checkpoints. That keeps resolution consistent without assuming platform-specific payout rules.

Validate intake and define the case scope#

Start by classifying the case and stating the objective so the handling path is clear. Similar issues can look alike at intake, so the initial scope should be explicit.

A practical cue from IRM 13.1.24 is the separation of Responsibilities and Authority: make it obvious who is responsible for case development and who has authority for case actions. Your checkpoint is simple: a reviewer can immediately see case scope, responsibilities, and authority.

Research internal systems before concluding#

Do not finalize conclusions until internal case research is complete. IRM 13.1.24.3 explicitly calls out advocacy through case research on internal systems, and that discipline fits here.

If internal records are unclear or conflicting, keep the case in research and resolve those gaps first. Move forward when the internal record supports a coherent explanation.

Document conclusions and communicate clearly#

When research is sufficient, document the case conclusion and the basis for it. If evidence is missing, request the exact item needed and explain why it matters.

IRM 13.1.24.3.2 highlights enhanced communication and rapport. Operationally, that means making the next step, missing information, and likely impact clear.

Route case actions through the authority path#

After the conclusion is documented, route follow-on case actions through the defined authority path for the case. Keep the case record aligned with what was decided and what was carried out.

Where a collection issue proceeds to appeal, keep the path label explicit, including Collection Appeals Program (CAP) under 13.1.24.5.2.

Close out with reporting checkpoints and appeals labels#

Closeout should leave a complete, reviewable case record with the outcome, basis, and path taken. IRM 13.1.24.1.4 on Program Reports is a useful reminder that reporting belongs in the process design, not after it.

For collection-related escalation, preserve the applicable appeals label in the final record.

Use a clear escalation ladder when internal resolution fails#

Escalation works best when it follows checkpoints instead of instinct. One practical checkpoint is whether the dispute is still about missing facts or has shifted to contested contract meaning.

| Step | Use when | File needs |

|---|---|---|

| Negotiation | Unresolved facts or fixable misunderstandings are still driving the case, or a quick settlement is still realistic | The disputed amount, record references, and the exact unanswered questions |

| Legal review | Operations cannot resolve the case through record matching and policy application alone, or the dispute turns on contract meaning | Exact clause text, the internal written decision, disputed payment records, and the communication trail |

| Arbitration gate | Contract language and legal review support arbitration | Clause text, legal review outcome, final internal decision, amount in dispute, and settlement-hold status |

| AI support | Evidence summarization, pattern checks, and draft support | Records and contract text behind the result, with human approval for final determinations, notices, and settlement actions |

Start with negotiation when the record is incomplete or a quick settlement is still realistic#

Use Negotiation when unresolved facts or fixable misunderstandings are still driving the case. Keep the goal explicit: close the evidence gap or test whether both sides can accept a written settlement position based on reconciled records.

Keep this step bounded. The case packet should clearly show the disputed amount, record references, and the exact unanswered questions. If the same facts repeat and the disagreement becomes "what does the contract require," move to legal review.

Escalate to legal review when the dispute turns on contract meaning#

Escalate to legal when operations cannot resolve the case through record matching and policy application alone. A common trigger is disputed interpretation of the Dispute resolution clause.

Attach exact clause text, the internal written decision, disputed payment records, and the communication trail showing why internal resolution failed. If the contract references Binding arbitration, capture that language verbatim and flag it for review.

Confirm whether arbitration is actually in scope before you invoke it#

Treat arbitration as conditional, not automatic, and use it only when contract language and legal review support it. Document an arbitration gate before formal escalation. At minimum, confirm the file includes clause text, legal review outcome, final internal decision, amount in dispute, and settlement-hold status.

Do not escalate on the assumption that ADR will always be the lighter path. Process formality can vary by case, including situations where ADR becomes more formal. Treat formal-versus-informal labels as shorthand, not guarantees.

Use AI support as assistive analysis only#

Use AI tools for assistive tasks such as evidence summarization, pattern checks, and draft support. Keep final determinations, notices, and settlement actions under human approval controls.

Do not allow model output alone to trigger closeout, payout release, reversal, or notice sending. If the tool cannot show the records and contract text behind its result, treat it as a review input, not a decision.

Automate the controls that remove repeat disputes#

Automate case-quality controls first, and keep final dispute decisions under accountable human review. That approach can reduce repeat work without shifting final accountability away from people.

-

Tie each control to a written procedure. Start with what the agreement package explicitly names: Appendix I - Verification and Dispute Resolution Procedures, Appendix H - Performance Scoring Detailed Methodology, and Appendix J - Improvement Plan Template. Map each proposed automation to one of those documents before implementation, especially when it affects intake, verification, approval, or closeout. If a control is not defined in those materials, treat it as a new internal policy change that needs explicit approval, ownership, and rollout.

-

Automate completeness gates before outcome decisions. Use automation to flag incomplete files before they move forward. The excerpt does not define exact mandatory fields, handoff rules, or override roles, so document those controls as internal policy before enforcing them.

-

Make settlement actions safe to retry. If your dispute process includes money movement, design retries to avoid duplicate financial effects. The excerpt does not confirm specific idempotency or replay controls, so validate duplicate-submission handling before broad rollout.

-

Route repeat patterns into improvement work. Route recurring issues into human review and formal improvement planning rather than automatic closure. Use the performance-scoring and improvement-plan appendices as the documented path for follow-through.

Related: Payment Disputes and Chargebacks: A Step-by-Step Resolution Guide for Freelancers.

Handle cross-border tax and compliance edges inside the same process#

Keep cross-border tax and compliance checks inside the dispute workflow, but route them through a separate compliance branch instead of payout troubleshooting. The goal is to keep valid payouts moving without masking reporting issues as payment failures.

| Issue | Routing | Key note |

|---|---|---|

| Tax-document checks | Confirm document status and ownership in the case file, then route unclear or conflicting records to tax or compliance review | Treat W-8, W-9, Form 1042-S, Form 1099, and VAT rule logic as policy-owned checks |

| Possible Form 8938 scenario | Route cases with possible foreign-asset reporting implications to compliance with structured account facts in the packet | Form 8938 is not required if no income tax return is required for the year, even if asset values exceed threshold levels |

| Form 8938 and FBAR | Treat them as separate obligations in routing and review notes | Filing Form 8938 does not remove separate FinCEN Form 114 (FBAR) filing requirements |

| Compliance holds vs payout failures | Use distinct reason codes and evidence trails, and keep uncertain VAT-related amount disputes in tax or compliance review | Do not misreport reporting issues as payment-rail defects |

- Keep tax-document checks operational, not interpretive.

Confirm document status and ownership in the case file, then route unclear or conflicting records to tax or compliance review. This section does not define W-8 or W-9, Form 1042-S, Form 1099, or VAT rule logic, so treat those as policy-owned checks rather than reviewer judgment calls.

- Escalate plausible

Form 8938scenarios with complete facts.

Form 8938 applies when specified foreign financial assets exceed the filer's applicable threshold, and thresholds are context-dependent. IRS materials note higher thresholds for joint filers and taxpayers residing abroad, and instructions for certain specified domestic entities reference $50,000 at year-end or $75,000 at any time during the year. If no income tax return is required for the year, Form 8938 is not required even if asset values exceed threshold levels. Route cases with possible foreign-asset reporting implications to compliance with structured account facts in the packet.

- Do not merge

Form 8938andFBARhandling.

Treat them as separate obligations in routing and review notes. Filing Form 8938 does not remove separate FinCEN Form 114 (FBAR) filing requirements.

- Separate compliance holds from payout execution failures in case states.

Use distinct reason codes and evidence trails so reporting issues are not misreported as payment-rail defects. For VAT-related amount disputes, keep the case in tax or compliance review when treatment is uncertain rather than labeling it as an execution failure.

For a step-by-step walkthrough, see How to Handle Payment Disputes as a Platform Operator.

Measure process quality with decision checkpoints#

If you cannot see drift at each gate, you may only discover it after backlog and exceptions pile up. Track quality at each checkpoint, not just at closeout, so timeliness and consistency stay visible from intake through final acceptance.

- Set one metric for each stage. Use one decision checkpoint per gate: was the case ready to move forward, or did the process create delay or error?

| Stage | Metric | What to verify |

|---|---|---|

| Intake | Intake completeness | Required evidence is attached and the reason code matches the dispute type |

| Verification | Verification pass rate | Records reconcile cleanly enough to decide without data repair |

| Decision | Decision latency against internal target | The clock starts at triage and stops when a written decision is issued |

| Settlement | Settlement correction rate | Posted reversals, offsets, or releases did not require follow-up fixes |

| Closeout | Reopen rate | The case stayed closed because notice, posting, and evidence were complete |

Do not infer progress from timestamps alone. Require a visible completion mark at each gate, because correction is not complete until it is verified.

-

Report source-of-truth consistency first. Track the share of cases with matched

Ledger journalandERPdata at first review. This can be a practical health check: low match rates may indicate reviewers are repairing records instead of deciding the case. Define "matched" once and keep it stable. At minimum, the case should show that the ledger event,ERPinvoice reference, and settlement status point to the same payment object. -

Watch fairness controls, not just speed. Speed alone can hide inconsistent treatment. Track decision variance by dispute type, escalation rate by reviewer group, and override frequency under

RBACto spot uneven handling of similar cases. For each override, capture the original decision, approver, reason, and added or reinterpreted evidence. Use outliers to review policy interpretation, training, or evidence standards. -

Publish one monthly exception review. Publish a monthly exception review across

Payout batches,Chargebacks, and compliance-gated holds. Focus it on fix priorities: recurring mismatches, repeated settlement corrections, reopened cases, and concentrated decision patterns. Build this from the same case system used for decisions. Fragmented spreadsheets and email threads weaken coordination and auditability. -

Compare trends to your own baseline. Be explicit about evidence limits. External benchmarks on dispute-team organization and operating patterns are often thin, so internal trend lines are usually more defensible. Read month-over-month changes with context. Annotate policy or intake-definition changes so metric movement reflects process reality, not classification drift.

If your team is defining SLA, variance, and reopen metrics, use this as a build reference for status surfaces, webhooks, and reconciliation workflows in one place. Explore the Gruv docs.

Common failure modes and how to recover fast#

Fast recovery starts with accurate classification. When you know whether the issue is reporting, controls, or approval, the correction path is usually clearer.

-

Identify the failure type and document it in case history. When a case starts accumulating multiple fixes, label what failed: reporting data, case controls, or decision approval. Use case history as the running log so the next reviewer can follow the file without reconstructing it.

-

Treat tax-document mismatches as reporting corrections first. If a payee statement appears incorrect, contact the payor first, preferably before it is sent to the IRS. For affected payments, confirm whether the reporting path is

Form 1099-NECorForm 1042-Sbefore moving forward. Payments of$600 or morein a trade or business can trigger annual reporting,Forms W-2 and 1099-NECare generally due byJanuary 31, andForm 1042-Sis shown dueMar 15. -

Complete the correction workflow end to end. If you issue a correction, mark it as corrected or use the designated correction form, file it with the appropriate agency, and provide the corrected copy to the payee. If the only change is correcting the SSN on a

Form W-2, the excerpt indicatesForm 1040-Xis not required. For a deeper 1042-S process, see IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments. -

Use control checkpoints, not status labels. Require checkpoint artifacts in the record, including case-history updates and freeze-code tracking where applicable. This helps reviewers confirm whether the case is moving, paused, or waiting on a specific control checkpoint.

-

Require written supervisory approval for exception paths. Before finalizing exception paths that can affect reporting outcomes, require written supervisory approval in the case record. This keeps the file clear on what was decided, by whom, and on what documented basis.

Copy and use this implementation checklist#

Use this as a controlled policy artifact, not a team note. It should block closeout until both Roles and Responsibilities and Program Controls are satisfied.

- We documented Roles and Responsibilities for key workflow steps, including review, approval, exception routing, and closeout.

- We documented Program Controls required before a case can be closed.

- We require a written supervisory approval checkpoint before final disposition.

- We maintain an explicit exception path for Cases Needing Further Action instead of forcing an approve or deny outcome.

- We require each closed case to show assigned owner, approver, and the policy or contract clause used for the decision, when applicable.

- We treat contract clauses as controlled artifacts and record the clause used when a dispute depends on contract language, aligned with FAR Part 52 procedures for identifying and modifying clauses.

- We track dispute-process deficiencies and review them on a recurring cadence.

When you are ready to operationalize this process across compliance-gated payout flows and payout batches where enabled, map your requirements to a concrete rollout plan with Gruv. Talk with the team.

Frequently Asked Questions

What makes an internal contractor payment dispute process fair in practice?

A process is fair in practice when similar disputes follow the same evidence standard, the same review path, and a clearly documented rationale. The real test is consistency: equivalent cases should not be approved or denied on different levels of proof. Keep the decision record explicit so any reviewer can see why the outcome was reached.

Which parts should we automate first if we need visible impact in the next quarter?

Start with intake and control steps before automating judgment. Prioritize completeness checks, required case fields, and workflow tracking so decisions are based on complete records. Then add recommendation support, with human oversight, once your inputs are reliable.

Should negotiation always come before escalation to binding arbitration?

No. Negotiation can help when facts are still incomplete or a fast agreement is realistic, but it is not mandatory in every contract or jurisdiction. Escalation order should follow the dispute clause and legal review of the specific contract language.

Can AI tools replace human reviewers for dispute decisions?

AI should support decisions, not make final determinations on its own. The grounded use case is recommendation support that suggests fair, explainable paths, with human oversight on the outcome. If a tool cannot clearly show the reasoning behind its recommendation, treat that as a control risk.

What evidence should be mandatory before approving or denying a dispute?

Set a minimum evidence pack in your internal policy and apply it consistently across similar cases. The decision should be explainable from the documented record, not from reviewer memory or informal context. If core records conflict, pause the decision and resolve the mismatch first.

How do we keep cross-border tax and compliance checks from stalling valid payouts?

Separate tax or compliance review from payment-execution review at intake so every hold is not treated as the same problem. Require a documented reason whenever a case is paused for compliance checks. When a hold depends on a federal notice, verify against an official Federal Register edition or the linked govinfo PDF instead of relying only on the FederalRegister.gov prototype or XML view, which is not an official legal edition.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far-overhaul/far-part-deviation-guide/far-ov...trusted

- acus.gov/sites/default/files/documents/Final%20Report...trusted

- cms.gov/nosurprises/help-resolve-payment-disputes/pa...trusted

- content.leg.colorado.gov/sites/default/files/documents/audits/2251p_a...trusted

- courts.ca.gov/system/filestrusted

- dgs.ca.gov/-/media/Divisions/OLS/Resources/SCM-VI---04-...trusted

- federalregister.gov/documents/2023/11/03/2023-23716/federal-inde...trusted

- flcourts.gov/content/download/725954/file/Online%20Disput...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments

If you own compliance, legal, finance, or risk for a platform paying foreign contractors, sellers, or creators, you may need to make **Form 1042-S** operational. That means clear decisions, reliable checks, and escalation points your team can apply and defend.

Non-Resident Withholding on Contractor Payments: Platform Guide to the 30% Rule and Treaty Reductions

Start with the default. If a payment is in scope for NRA withholding and you cannot support reduced treatment, withhold 30% and escalate unresolved cases before release.

Resolving Payment Disputes and Chargebacks for Freelancer Platforms

This guide is for platform teams managing freelancer revenue risk. The operating rule is simple: by the time a payment dispute or chargeback starts, ownership, first-day actions, and decision criteria should already be defined.