Quick Answer

Start by designing crypto payouts tax reporting as an operations control, not a year-end patch. In this US-focused framework, digital assets are treated as property, so you should log payout receipt and later disposal as separate events, capture event-time values, and preserve correction links. Collect W-8 or W-9 data before first disbursement as a program control, then verify monthly tie-outs across ledger records, provider data, and export rows. Before scale, define who owns Form 1099-DA decisions and mismatch handling.

How US Tax Reporting Works for Bitcoin and Ethereum Gig-Worker Payouts#

If you plan to pay gig workers in Bitcoin or Ethereum, treat reporting design as part of product design from day one. Faster settlement can help operations, but weak controls can leave you with harder reconciliations and more compliance risk.

This guide is a U.S.-focused operator brief for teams building or scaling payout programs, not personal tax advice. It is written for product, engineering, finance, and compliance owners who need payout flows that are practical to run and defensible at year-end.

At the federal level, the baseline is straightforward. The IRS says income from digital assets is taxable, and digital assets are treated as property, not currency. In practice, reporting turns on operational details like transaction-time valuation and records that let users answer digital-asset return questions on Form 1040, Form 1040-SR, or Form 1040-NR.

The main operating risk is simple: an in-app flow can look clean while your books get messy if you cannot reliably reconstruct the transaction time and fair market value for each payout. When records are incomplete, finance, compliance, and support inherit cleanup that could have been avoided.

The goal is practical: help you choose payout patterns and controls your teams can actually operate and audit. Confirm applicable obligations before rollout for your specific program design and filing context.

The tax baseline your payout product cannot ignore#

For U.S. programs, the baseline is clear. The IRS treats digital assets as property, not currency, and IRS FAQ language points to Notice 2014-21, 2014-16 I.R.B. 938 as an anchor for that treatment. The IRS also uses digital asset as a broad term for value recorded on cryptographically secured distributed-ledger technology, and uses virtual currency in its FAQ terminology.

For payout design, that means a crypto disbursement is not just a cash-like transfer. The IRS says general property tax principles apply, and taxpayers who sell crypto, receive it as payment, or have other digital-asset transactions need to report those transactions accurately. In practice, you should classify, log, and reconcile payout events in records that support accurate reporting.

Return behavior is mandatory, not optional. IRS guidance says filers on Form 1040, 1040-SR, 1040-NR, 1041, 1065, 1120, and 1120-S must answer the digital-asset question "Yes" or "No." That question covers both:

- receiving digital assets, including payment for services or property

- selling, exchanging, or otherwise disposing of digital assets

One scope guard matters. IRS virtual-currency FAQs say they generally apply to transactions completed before Jan. 1, 2025. Use them as baseline guidance, but not as a complete answer for every later edge case.

How payout events map to taxable outcomes#

Treat payout receipt and later disposal as two separate reporting moments. If a worker is paid in cryptocurrency and later sells or converts it, your system should keep separate records for each event, not one blended "crypto activity" record.

The IRS digital-asset question reflects that split. It asks whether a filer received digital assets as payment for property or services, and whether they sold, exchanged, or otherwise disposed of digital assets. That is a useful operating frame, even if it is not a full rule engine.

A practical event map#

| Payout lifecycle event | IRS signal from provided excerpts | Reporting lens to prepare for | Form step to preserve |

|---|---|---|---|

| Worker receives cryptocurrency as payment for services | Receiving digital assets as payment for services is explicitly listed; income from digital assets is taxable | Receipt-side income evidence | Preserve timestamp, asset amount, and fair value at receipt; keep records usable for downstream income-reporting review |

| Worker later sells or converts that asset | Selling, exchanging, or otherwise disposing is separately listed | Separate disposal-side gain/loss analysis, especially where held as a capital asset | Preserve acquisition value/date linkage plus disposal value/date; maintain records for Form 8949 review |

| Worker transfers assets between wallets/accounts | IRS states digital assets can be transferred, but excerpts do not say every transfer is taxable | Tracking/continuity event unless facts show otherwise | Preserve tx hash, source, destination, and ownership linkage to prevent double counting |

| Platform or payee exchanges one digital asset for another | "Exchange" and "otherwise dispose of" are in scope | Disposition candidate that needs fact-specific review | Capture asset out, asset in, timestamp, and values on both sides for Form 8949 review if applicable |

The implementation rule that prevents reconciliation failures#

Do not rely only on the eventual cash-out value. You need the value at receipt and the value at disposal so you can separate compensation-related income tracking from later price movement.

Operationally, every disposal record you prepare for Form 8949 review should trace back to the original payout record, including quantity, timestamp, and fair value at receipt. If that linkage is missing, gain/loss and holding-period analysis become unreliable.

Entity pathways you cannot ignore#

This is not only a Form 1040 workflow. If your marketplace pays trusts, estates, or partnerships, IRS guidance also requires digital-asset question handling for Form 1041 and Form 1065 filers, so you still need the same receive-versus-dispose record split.

Where automation should stop#

Set guardrails before you ship automated tax labels. The virtual-currency FAQs generally apply to transactions completed before Jan. 1, 2025 and, except as otherwise noted, apply to taxpayers holding virtual currency as a capital asset. For DeFi mechanics and NFT-specific gain or income treatment, route to tax counsel review rather than auto-classifying.

Related: How Online Course Marketplaces Handle Instructor Revenue Splits and Tax Reporting.

Choose your payout and conversion model before shipping#

Choose the model based on evidence burden first. If you want lower tax-support burden, tighter conversion windows and clear valuation timestamps usually help. The more user discretion you allow to hold, switch, or convert later, the more basis, timing, and reconciliation questions your team may need to handle.

This is an operations decision, not just a UX decision. Because virtual currency is treated as property, your payout and conversion flow affects how many property-transaction records you need to retain and reconcile. IRS FAQ language on this point is scoped: it generally applies to digital-asset transactions completed before Jan. 1, 2025, and generally to taxpayers who hold virtual currency as a capital asset.

| Model | What it gives you | What it costs you | Evidence to retain |

|---|---|---|---|

| Direct Bitcoin or Ethereum payout | Straightforward payout flow for users who want the asset | Higher downstream support burden when users later sell, exchange, or move assets; price volatility can shift to the user at receipt | Asset, quantity, payout timestamp, value at receipt, wallet destination, transaction hash/provider reference, fees, and correction links |

| Instant conversion to fiat | Tighter value window, lower payout-time volatility exposure, potentially fewer later valuation disputes | More in-stack routing and exception handling when quotes expire, funding fails, or approvals delay settlement | Pre-conversion asset amount, value timestamp, conversion timestamp, fiat proceeds, fees/spread if separately shown, provider reference, and retry/cancellation linkage |

| Delayed conversion with user choice | More user flexibility | Often the highest support and reconciliation burden because timing choices can multiply disposal scenarios | Original payout record plus each later conversion decision, timestamp, value, fees, asset in/out, and ownership continuity across wallets or accounts |

If your team is not ready for a heavier evidence trail, avoid open-ended user-directed holding in the payout flow. A controlled conversion path, whether immediate or within a narrow operational window, usually produces clearer records: one payout event and one conversion event, if applicable, with cleaner value timestamps.

Whichever model you ship, keep data that supports downstream Form 8949 reconciliation and any applicable Form 1099-DA outputs. The 2025 Form 8949 instructions reference a Form 1099-DA pathway and include digital-asset boxes G, H, I for short-term and J, K, L for long-term. Design records for reconciliation, not just a single proceeds field.

Before launch, run a test payout through your ledger and confirm you can reconstruct receipt value, any conversion value, timestamps used, fees applied, and the export row feeding 1099-DA or Form 8949 review for both a happy path and a failed-then-retried path. If that reconstruction requires guesswork, the model is not ready.

If you want a deeper dive, read Crypto Payout Compliance: AML KYC and Tax Reporting for Blockchain Disbursements.

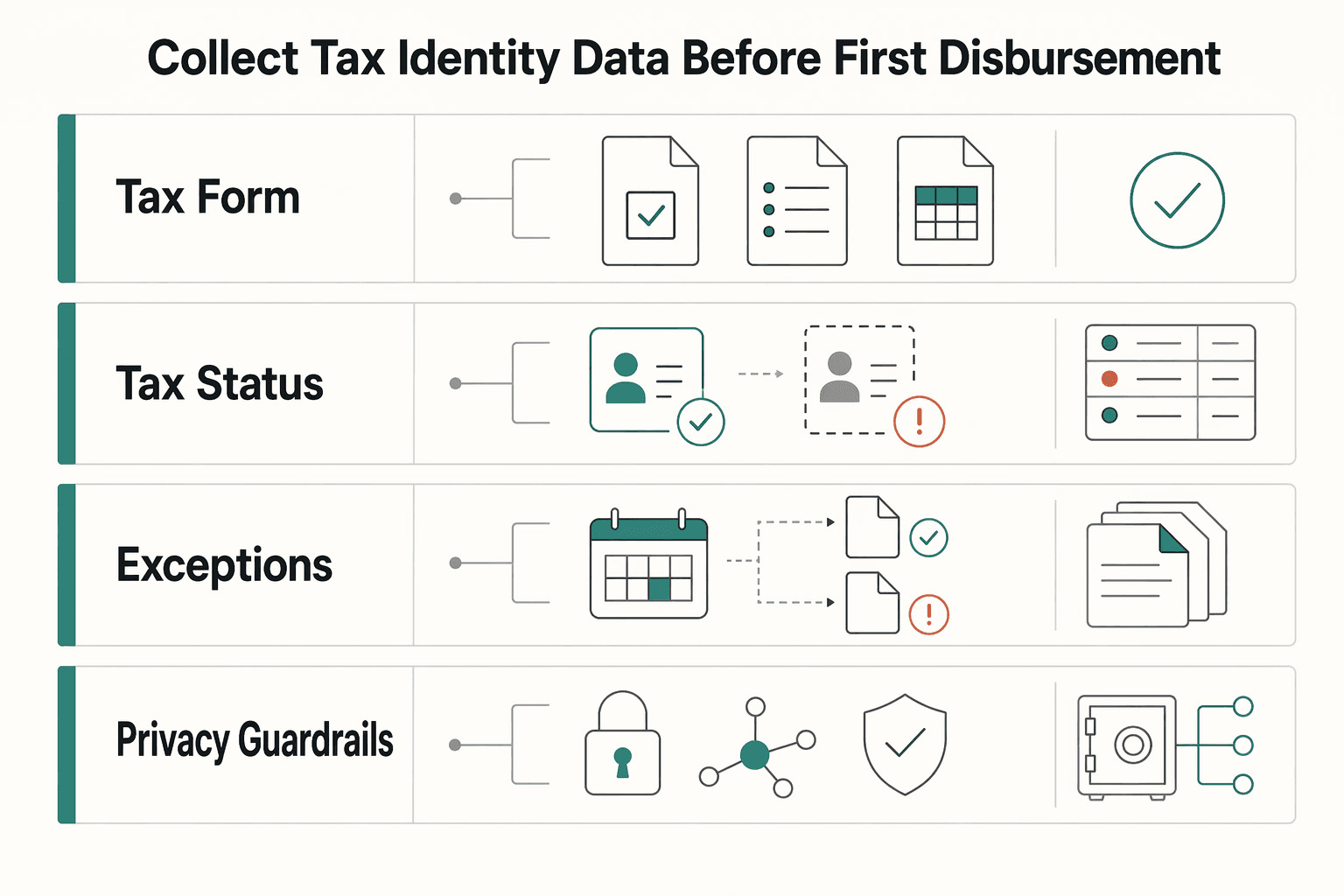

Collect tax identity data before first disbursement#

Make tax profile completion a payout-readiness control, not a year-end cleanup task. Collecting tax identity documentation before enabling disbursements can be a defensible internal policy if your goal is to reduce reconciliation risk after funds move.

| Control | What to do | Keep or track |

|---|---|---|

| Tax-form capture | Treat tax-form capture as part of payout account activation | Form type, capture timestamp, submitted identity details, and correction history |

| Tax status vs KYC or KYB | Track tax-document completeness and KYC or KYB as separate internal controls with separate pass or fail states | Separate pass or fail states; many teams require both states to pass before a payee is payable |

| Escalation rules | Set internal rules for missing, conflicting, or late-changing tax profile data | Document the correction; one approach is to hold the affected payee from a batch until the record is corrected |

| Privacy guardrails | Limit access to tax identity data and default to masked views | Show status and required next action to frontline teams; reserve sensitive-field access for finance and compliance workflows |

The IRS excerpts here do not mandate when forms must be collected. They do establish that taxpayers must answer the digital asset question and report digital-asset-related income, including when digital assets are received as payment. They also place that question on core return forms, creating a concrete filing checkpoint. The broker-reporting material in these excerpts is proposed, not a finalized workflow mandate.

Make tax onboarding a hard payout control#

Treat tax-form capture as part of payout account activation. Frame it as an internal reporting-quality safeguard, not as a legal claim that forms must be collected at a specific moment.

Keep a clear audit trail for each payee: form type, capture timestamp, submitted identity details, and correction history. Preserve updates as history instead of overwriting prior records.

Keep tax status separate from KYC or KYB status#

Track tax-document completeness and KYC or KYB as separate internal controls with separate pass or fail states. They fail for different reasons, and combining them into one "approved" flag can make exceptions harder to diagnose.

Many teams require both states to pass before the payout engine marks a payee as payable. That gives ops a clear reason code when a transfer is held.

Define escalation rules before batch day#

Set internal rules for missing, conflicting, or late-changing tax profile data before you need them. One approach is to hold the affected payee from a batch until the record is corrected and documented. That is an operational choice, not a requirement stated in these excerpts.

Add privacy guardrails to the tax record#

Limit access to tax identity data and default to masked views as internal privacy controls. The provided IRS excerpts do not prescribe specific masking or ops-log exposure rules.

For day-to-day operations, show frontline teams the status and required next action. Reserve sensitive-field access for finance and compliance workflows.

We covered this in detail in FATCA and W-8 Tax Compliance for Platforms: When to Release, Hold, or Withhold Foreign Payouts.

Build an event and ledger schema that survives audit season#

After tax identity gating, ledger design helps protect reporting quality. Record digital-asset activity as discrete events, not just wallet balance movement, so you can reconstruct what happened without guesswork.

The IRS framing distinguishes receiving a digital asset, including as payment, from selling, exchanging, or otherwise disposing of it. Your event types should preserve that distinction. If receipt and disposal are collapsed into one generic transfer record, downstream reporting support gets weaker.

Keep the event record richer than the balance record#

The IRS excerpts do not prescribe a field-by-field schema. As an internal control, keep an event record that answers three questions: what happened, when did it happen, and how do later changes relate to the original entry?

| Record element | Why keep it | What to verify |

|---|---|---|

| Event type | Preserves receipt/payment vs disposal distinctions in the IRS framing | Receipt/payment events are not merged with disposal events |

| Event timestamp | Anchors sequence and timing of activity | Use one consistent event-time source |

| Asset | Identifies what moved | Keep asset movements distinct by event |

| Correction link (when applicable) | Connects reversals or amendments to originals | Corrections reference originals instead of overwriting |

When corrections happen, preserve history. Write a correcting event and link it to the original record instead of replacing the original row.

Make one ledger feed two outputs#

Use one event history as the source for both accounting reconciliation and tax-support exports, even if each output summarizes differently. Separate pipelines with separate logic create avoidable mismatches.

For tax support, focus on traceable evidence: what event occurred, when it occurred, and what asset moved. These IRS excerpts do not provide detailed schedule line-mapping rules.

Retries must be safe to replay#

Idempotency is an implementation control, not an IRS requirement in these excerpts. If payout retries occur, duplicate writes can create false event history.

Design retries so the same business intent replays safely: return the existing event or append status, but do not mint a second payout event unless a new event actually occurred.

Add a monthly checkpoint before close#

A monthly pre-close tie-out is an internal control option instead of discovering issues at year-end. Sample records can be checked across ledger totals, payout-provider data, and tax export rows drawn from the same event set.

Include normal, corrected, and retried cases in the sample where relevant. If mismatches appear, fix the event model or transformation logic at the source, not only in the export output.

Assign form responsibilities for brokers and platforms#

A clean ledger is not enough if filing ownership is unclear. Before you promise user-facing tax statements, decide whether your service is the in-scope broker for a transaction under these rules or whether reporting depends on another broker.

Start with the possession test#

Form 1099-DA is used to report digital asset proceeds from broker transactions, with reporting beginning for transactions on or after January 1, 2025. Basis reporting on certain transactions begins on or after January 1, 2026.

The core scope test is whether your service takes possession of digital assets being sold by customers. IRS examples in scope include custodial trading platforms, certain hosted wallet providers, kiosks, and certain processors of digital asset payments. Current final regulations do not include decentralized or non-custodial brokers that do not take possession, and Treasury and IRS said separate rules are intended for them.

So a "platform" or "integrator" label does not decide filing responsibility on its own. Document your actual custody and transaction flow, then review that fact pattern before you assign filing ownership.

Put names next to each 1099 job#

Assign owners early so product, finance, compliance, and any external broker or filing vendor are not working from assumptions.

| Responsibility | Primary owner to name | What to keep as evidence |

|---|---|---|

| Determine whether Form 1099-DA applies to the transaction flow | Compliance or tax owner, with legal review where needed | Product flow diagram, custody analysis, date-stamped rule memo |

| Generate and deliver 1099 or broker statements | Filing party or external broker named in contract | Filed output version, recipient statement sample, submission receipts |

| Resolve mismatches between ledger, broker files, and statements | Finance ops plus data or engineering | Exception log, record-level diffs, disposition notes |

| Answer IRS or recipient notices | Named tax operations owner | Notice tracker, response drafts, filing history |

| Maintain correction history for 1099 outputs | Finance ops or tax reporting owner | Original file, corrected file, correction reason, approval trail |

Two checks are easy to miss. Taxpayer statements should include the information reported to the IRS on Form 1099-DA, so statement versions and user-facing report versions need control. Also, Form 1099-DA is excluded from the Combined Federal/State Filing Program for tax year 2025, so do not assume a federal path covers state filing needs.

Do not promise self-serve reports before broker-file ingestion works#

If you depend on third-party broker files, build ingestion and reconciliation controls before you offer self-serve tax reports. At minimum, cover file receipt monitoring, schema validation, account matching, duplicate detection, and an exception queue tied back to the payout event.

Use a monthly traceability check: follow one transaction across your ledger, the broker file, and the user-visible statement, including a corrected record. If amounts or counterparties do not reconcile, pause "tax-ready" messaging until the break is resolved.

Also avoid legal overconfidence from web summaries alone. FederalRegister.gov pages are useful, but their own notice says web or XML content is informational and legal research should be verified against official editions.

For a step-by-step walkthrough, see Creator Platform Tax Reporting for 1099 and W-8 Expansion Decisions.

Handle cross-border reporting flags without overpromising#

Keep offshore disclosure screening separate from 1099 ownership. FBAR and Form 8938 are not interchangeable, and Form 8938 does not replace FinCEN Form 114 (FBAR) when FBAR applies.

| Record to keep | Article detail | Why keep it |

|---|---|---|

| Entity or user type | Entity or user type tied to the account | Lets tax teams assess potential Form 8938 and FBAR exposure later |

| Account maintainer | Whether the account is maintained by a foreign financial institution or a U.S. payer | Some accounts are excluded, including certain accounts maintained by a U.S. payer |

| Provider jurisdiction | Account-provider jurisdiction | Supports the account-level pack with owner, provider, jurisdiction, and maximum value history |

| Maximum value | Maximum-value data needed for annual support, including maximum value of all deposit accounts | Needed for annual support and the year-end readiness check |

For operations, screen on scope, not labels. Start Form 8938 support with two checks: whether the filer is a specified individual or specified domestic entity, and whether they hold specified foreign financial assets. Those assets can include financial accounts maintained by a foreign financial institution, with exceptions, and some accounts are excluded, including certain accounts maintained by a U.S. payer. So do not assume every crypto account, wallet, or payout balance is reportable on Form 8938.

Treat this as a risk-screening layer you can evidence, not a filing promise. Keep records that let tax teams assess potential Form 8938 and FBAR exposure later:

- entity or user type tied to the account

- whether the account is maintained by a foreign financial institution or a U.S. payer

- account-provider jurisdiction

- maximum-value data needed for annual support, including Form 8938 fields like maximum value of all deposit accounts

Use a year-end readiness check: can you produce an account-level pack with owner, provider, jurisdiction, and maximum value history without rebuilding from raw logs? If not, your cross-border controls are too thin.

Keep the filing boundary explicit. Form 8938 is attached to the annual return and filed by that return's due date, including extensions. If no income tax return is required for the year, Form 8938 is not required. Thresholds vary by filer type, including $50,000 for certain U.S. taxpayers and $50,000 at year end or $75,000 at any time for certain specified domestic entities. That is why this section stays framed as screening support, not universal filing advice.

Run monthly and year-end controls that catch errors early#

Treat monthly close as filing rehearsal. If wallet activity, payee identity data, and draft form outputs do not reconcile before year-end, correction risk can increase.

Use month-end to surface breaks while they are still cheap#

The IRS excerpts do not prescribe a required monthly checklist, so treat the following as internal controls:

- Tie wallet movements to ledger entries at payout-event level, not only net balances, so retries, reversals, and failed payouts do not get masked.

- Review failed and reversed payouts as a separate queue, and require each record to end in a clear final state linked to the original payout ID.

- Audit valuation timestamps so ledger time, pricing-source time, and exported tax value are internally consistent for sampled payouts.

- Keep unresolved identity exceptions open and visible until cleared.

Build year-end checks around Form 1099-DA logic#

At year-end, use a consistent payer/payee validation snapshot, then test draft outputs against your ledger population and any external files you rely on.

Form 1099-DA is the IRS form for reporting digital asset proceeds from broker transactions, and the instructions split treatment between sales in 2025 and sales on or after January 1, 2026. Reflect that split in your variance checks: for 2025, gross proceeds reporting is mandatory while basis reporting is voluntary; for 2026 and beyond, gross proceeds and basis reporting are mandatory for covered securities, while basis reporting is voluntary for noncovered securities.

If you receive external Form 1099-DA files, compare counts, payee identity fields, and gross proceeds totals before release. Treat mismatches as a pre-release investigation item.

For tax year 2025, include one explicit state-delivery check: Form 1099-DA is excluded from the Combined Federal/State Filing Program for that year.

Track instruction updates and corrections as part of year-end readiness.

Set escalation rules and preserve the handoff trail#

Define and document escalation rules for unresolved mismatches, then communicate scope, owner, and remediation timeline when issues remain open.

Keep handoff artifacts with the close package so release, delay, or correction decisions are traceable. Common internal artifacts include:

- Reconciliation status with open items and release recommendation

- Change logs for code, pricing-source, or export-logic changes that can affect 1099 outputs

- Exception registers for identity gaps, unresolved mismatches, and manual-review holds

The mistakes that trigger expensive cleanup#

A common source of expensive cleanup is treating different tax events as one net crypto line item. IRS guidance treats digital assets as property. The digital-asset question covers both receiving digital assets as payment and later disposal, so keep those paths separate from day one.

- Blending receipt and disposal into one cashflow record.

Track receipt as payment and later sale, exchange, or disposal as separate events. If you collapse them into one export row, year-end reporting can depend on reconstruction work that is harder to validate.

- Starting payouts before tax-profile records are complete.

If W-8 or W-9 data and related payee profile fields are collected late, mismatches against historical payouts can turn into retroactive correction work. Treat payout readiness as a gated state, not an assumption.

- Overstating "tax-ready" output.

IRS FS-2024-12 (April 2024) says filers must answer the digital asset question and report digital-asset income. Product messaging should say exactly what your file includes and what it does not. If your output only covers receipt-side values, state that plainly.

- Overwriting original records during corrections.

Keep the original payout event intact and record corrections as separate events with their own IDs and reasons. Then test traceability from payout to correction to export outputs, including the 2025 Form 8949 digital-asset boxes (G, H, I and J, K, L), where relevant. When that chain breaks, post-filing fixes can be slow.

Related reading: Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know.

A 90-day execution plan by team#

Use the next 90 days as an operating plan to prove control before you expand features. You should be able to show clear ownership of tax outputs, a stable digital-asset event taxonomy, and reconciliation from payout execution back to ledger and export records.

| Window | Focus | Actions |

|---|---|---|

| Days 1 to 30 | Lock scope and naming | Define receipt, transfer, conversion, fee, and disposal-related events; keep receipt events separate from later sale or exchange records; publish a form-responsibility map |

| Days 31 to 60 | Harden intake and ledger controls | Use W-8 or W-9 status as a payout-eligibility gate as an operating control; retain payout ID, event timestamp, asset, value at event time, payee, fees, and immutable links across retries and corrections; test idempotency |

| Days 61 to 90 | Run a parallel close simulation | Use live-like data including failures, reversals, and corrections; confirm records support downstream tax reporting workflows; log unresolved edge cases with owners; use Form 1099-DA timing checkpoints in specs and tests |

| Exit criteria | Exit only when all three are true | No critical reconciliation breaks remain across payout execution, ledger records, and tax exports; exception handling is documented; named owners across finance, ops, engineering, and compliance are signed for tax-season support |

Days 1 to 30#

Lock scope and naming first. Product, finance, and compliance should define receipt, transfer, conversion, fee, and disposal-related events so records stay consistent after funds move.

Keep receipt events separate from later sale or exchange records. IRS guidance treats digital assets as property for tax purposes, and receiving digital assets as payment is reportable, so collapsing these paths creates avoidable year-end reconstruction risk.

In the same window, publish a form-responsibility map. Do not assume Form 1099-DA applies automatically. Assign who determines applicability, who owns 1099 outputs, who manages correction logs, and who handles notices or file mismatches. Use the IRS instructions section "Information Required on the Form 1099-DA" as a data-field checkpoint for internal specs and counterparty expectations.

Days 31 to 60#

Next, harden intake and ledger controls. Use W-8 or W-9 status as a payout-eligibility gate as an operating control.

Strengthen ledger fields and correction linking. At minimum, retain payout ID, event timestamp, asset, value at event time, payee, fees, and immutable links across retries and corrections. Test idempotency so duplicate requests do not create duplicate taxable-event records.

Make reconciliation exports finance-usable, not engineering-only. For each sampled transaction, tie together payout event, provider or wallet reference, ledger record, and tax export record. If you cannot reconcile payout registers to execution, you are operating with uncontrolled payments.

Days 61 to 90#

Before broader rollout, run a parallel close simulation with finance and ops using live-like data, including failures, reversals, and corrections. The goal is to confirm records support downstream tax reporting workflows and to log unresolved edge cases with owners.

Use Form 1099-DA timing checkpoints in your specs and tests. For 2025, instructions state mandatory gross-proceeds reporting and voluntary basis reporting, and they distinguish treatment for sales effected on or after January 1, 2026.

Exit criteria#

Exit only when all three are true:

- no critical reconciliation breaks remain across payout execution, ledger records, and tax exports

- exception handling is documented, including correction approvals and unresolved-edge-case tracking

- named owners across finance, ops, engineering, and compliance are signed for tax-season support

If any one is missing, keep the rollout limited or delay launch. Use this phase to map your checklist to compliance-gated batch flows, retry safety, and reconciliation exports in Gruv Payouts.

Conclusion#

Choose payout and conversion behavior your team can report and reconcile, not what scales fastest in a demo. For U.S. programs, the limiting factor is usually whether finance and engineering can defend each payout event months later.

Start from the tax baseline before product expansion. Digital assets are treated as property for U.S. tax purposes, income from digital assets is taxable, and federal returns include a required digital-asset Yes or No question on forms such as Form 1040, 1040-NR, 1041, and 1065. That means a Bitcoin or Ethereum payout can become a reporting event, not just a payment UX choice.

Execution order matters: define tax handling first, make sure your ledger captures event-level facts, then lock ownership for year-end form decisions and corrections. If you scale before those pieces are stable, mismatches surface later and are much harder to resolve.

Run a controlled pilot before broad rollout. Measure where payout execution, ledger entries, valuation timestamps, and tax exports diverge, and expand only once those joins are reliable.

Keep records complete and traceable for every payout: who was paid, which asset was used, when it happened, what value was used, the execution reference, and how reversals or corrections link to the original event. If a third party may issue Form 1099-DA for covered broker activity, assign clear ownership for intake, variance review, and corrections. Do not treat a missing 1099-DA as "no reporting obligation."

Public summaries also indicate that 2025 transactions filed in 2026 may not include broker-reported cost basis, with broader basis reporting scheduled for transactions on or after January 1, 2026. That is why your own records remain critical.

If you offer multi-wallet flexibility, plan for added reconciliation work. Public summaries point toward more wallet-level recordkeeping pressure. Pilot, measure mismatch rates, fix weak joins, and scale only where the reporting story stays clear from end to end.

Before scaling beyond a pilot, confirm market coverage, policy gates, and operating ownership with the Gruv team.

Frequently Asked Questions

Are crypto payouts taxable and reportable in the US for platform users?

Yes. If a user receives a digital asset as payment, sells it, or has other digital-asset transactions, the IRS says those items must be reported accurately on the tax return. For platform operations, keep the payment-receipt record separate from any later transfer, exchange, or sale record, since those can be different reporting moments.

Does every filer need to answer the digital asset question even if activity seems limited?

Yes. Filers of Forms 1040, 1040-SR, 1040-NR, 1041, 1065, 1120, and 1120S must check either Yes or No to the digital asset question. Low activity does not make this question optional.

Is payout income in Bitcoin or Ethereum always treated as capital gains?

No. The IRS treats digital assets as property, so general property tax principles apply. Do not label all Bitcoin or Ethereum payout activity as capital gains, and keep the initial payout event separate from any later disposal event in your records.

What operational change does Form 1099-DA create for payout platforms?

Form 1099-DA is used to report digital asset proceeds from broker transactions, so the operational change is deciding applicability and ownership, not assuming every payout platform files it. Assign clear owners for applicability decisions, data intake, form output, corrections, and notices. For timing, 2025 instructions describe mandatory gross-proceeds reporting with voluntary basis reporting, and 2026 and beyond expand mandatory basis reporting for covered securities.

What minimum records should a platform retain for crypto payout tax reporting?

These IRS excerpts do not provide a definitive field-by-field minimum ledger schema. As an internal control baseline rather than an IRS-prescribed checklist, keep enough evidence to show who was paid, what asset was involved, when the event happened, what value was used at that time, the execution reference, and how reversals or corrections link to the original event. Validate that payout execution, ledger entries, and tax exports can be tied together end to end.

How should platforms handle unresolved edge cases when IRS excerpts are incomplete?

Do not automate broad rules from partial or older IRS text alone. The virtual-currency FAQ set generally applies to transactions completed before Jan. 1, 2025 and, absent exceptions, only to taxpayers who hold virtual currency as a capital asset. If an edge case falls outside that scope, treat it as an exception and review the 2024 Regulations and other IRS digital asset guidance for transactions on or after January 1, 2025 before finalizing tax output.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Crypto Payout Compliance for Blockchain Disbursements in 2026

Crypto payouts are a compliance decision, not just a payments operations choice. Once digital-asset payouts are in scope, AML oversight, due diligence, tax reporting, and cross-border operations sit inside the same process.

How Online Course Marketplaces Handle Instructor Revenue Splits and Tax Reporting

Most advice on **online course marketplace payouts** skips the part operators actually have to run: who owns the money movement, who owns payout risk, and who owns tax-facing work when exceptions happen. The real decisions usually start with who gets paid, how payouts are routed, and who handles reporting when the simple path breaks.

Tax Residency in Georgia (the country) for a Crypto Trader

Start with residency status, not tax rates. With **georgia tax residency crypto**, the first question is whether you were a Georgian tax resident for the period in question. If that point is unclear, every downstream tax position gets weaker.