Quick Answer

Start by proving status, then test activity type. For georgia tax residency crypto, the practical route is to confirm 183 days in a rolling 12-month period (or a valid HNWI basis), then determine whether your facts support personal investing rather than business or company operations. The cited 0% outcome is framed for resident individuals with supportable records, not all traders. Keep day logs, provenance notes, and pre-filing sign-off on interpretation-heavy items such as VAT or mining.

Start Here if You Want Georgia Tax Residency Without Tax-Haven Guesswork#

Start with residency status, not tax rates. With georgia tax residency crypto, the first question is whether you were a Georgian tax resident for the period in question. If that point is unclear, every downstream tax position gets weaker.

Use this conservative baseline: you become a tax resident if you spend 183 days in Georgia within any rolling 12-month period. Once residency is established, Georgia's territorial tax system applies. Foreign-sourced income can be taxed at 0% if structured correctly. That is not the same as saying crypto is always untaxed.

The first gate#

Do not treat immigration status as tax status. The source makes this explicit. Tax residency is not the same as having a visa or residence permit, and the digital nomad visa does not change tax rules.

| Step | What to do | Grounded point |

|---|---|---|

| 183-day test | Confirm the 183-day test first with a rolling 12-month count | You become a tax resident if you spend 183 days in Georgia within any rolling 12-month period |

| Status split | Separate tax and immigration status | Tax residency is not the same as having a visa or residence permit, and the digital nomad visa does not change tax rules |

| Income treatment | Then assess income treatment under Georgia's territorial framework | Foreign-sourced income can be taxed at 0% if structured correctly |

| Edge cases | Escalate early on mixed-country timelines or unclear facts | Get professional advice if you are near the 183-day line or depend on interpretation instead of clean records |

If your timeline spans more than one country, keep the facts aligned. A defensible position comes from consistent records, not from a single label.

Use this decision sequence.

- Confirm the 183-day test first with a rolling 12-month count, not a calendar-year guess.

- Separate tax and immigration status so you do not rely on a visa, permit, or bank setup as proof of tax residency.

- Then assess income treatment under Georgia's territorial framework, including whether income is foreign-sourced and whether your setup is structured correctly.

- Escalate early on edge cases if your timeline is mixed across countries or your facts are not clean.

Planning matters more than late paperwork.

Have your evidence ready before you act. Keep enough support to defend your position later, such as:

- a dated travel log of days in and out of Georgia

- matching entry and exit support for that log

- records that help you explain your timeline if reviewed later

If you would need to rebuild your day count from memory at year-end, your position is already weaker than it should be.

Escalate early when the facts are close. Get professional advice if you are near the 183-day line or depend on interpretation instead of clean records. Early advice can save time, effort, and money. If you want a lower-stress outcome, treat Georgia as rules-based, not rumor-based.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Build the Core Tax Logic Before You Act#

Classify your case before you chase a rate. In Georgia, residency is the first gate, and the cited guidance repeatedly points to the 183-day test. Income source and taxpayer type then determine whether you are applying Personal Income Tax logic or Corporate Income Tax logic.

Georgia is commonly described as a territorial tax system: Georgian-source income is taxed, and foreign-source income is generally not taxed for individuals. For crypto, that means the result turns on classification, not on a blanket assumption that crypto is always tax-free.

Sort the taxpayer before the rate#

| Taxpayer type | What to verify first | Grounded tax point |

|---|---|---|

| Resident individual investor | Is this personal investing, with profits supportable as foreign-source? | The cited guidance says crypto trading profits for Georgian resident individuals are exempt from income tax. |

| Sole operator or individual entrepreneur | Does your activity still fit the treatment you are assuming, or are you relying on a special regime? | Do not assume 1% treatment. The cited guidance says Small Business Status for crypto trading is uncertain, and SBS can be lost above 500,000 GEL annual turnover. |

| Georgian company | Are you now in company tax rules instead of individual rules? | The source describes 15% Corporate Income Tax as payable when profits are distributed, plus 5% withholding on distributed dividends. |

Keep headline rates separate from legal classification. A resident individual investing personal capital is a different tax posture from a company trading through the same exchanges and wallets.

Build proof for the classification you want to defend. Once you know which taxpayer bucket you are in, build the paper trail to match it. Document where the original capital came from and whether proceeds are personal or business funds. Keep that consistent across your records and bank files. In practice, weak documentation can lead to delays or rejection, and mixing personal and business flows is a common failure point.

For a residency walkthrough in another jurisdiction, see A Guide to Tax Residency in the Czech Republic for Nomads.

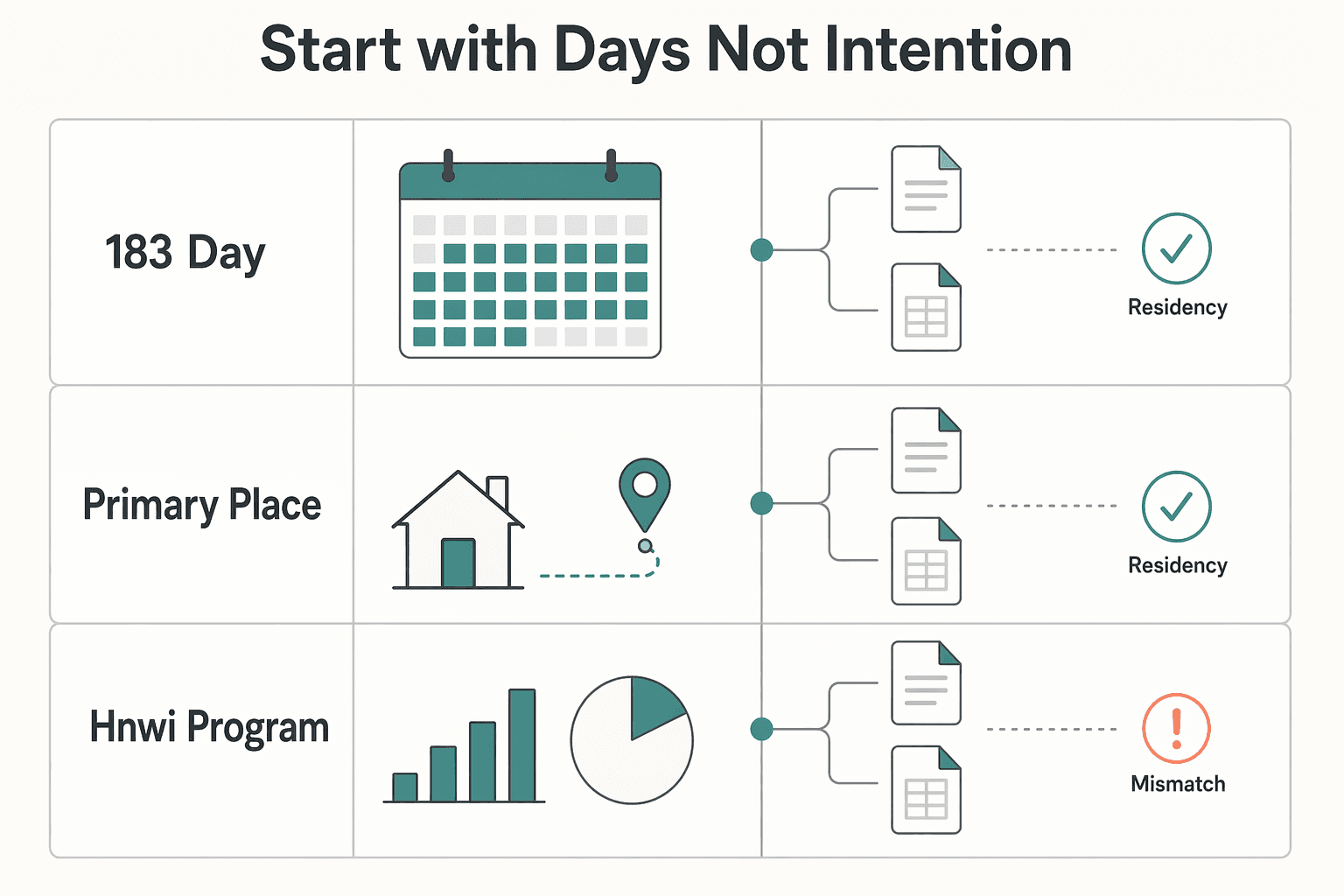

Decide Your Residency Status for This Tax Year First#

Before you model any crypto tax outcome, confirm whether you are a Georgian tax resident for this tax year. The clearest starting point is the 183-Day Rule.

Start with days, not intention#

Build a month-by-month calendar and count the days you are in Georgia (country). The cited guidance describes the test in slightly different ways, including living in Georgia for more than six months and spending at least 183 days within a 12-month period. Use a conservative count.

| Basis | What the cited guidance says | Caution |

|---|---|---|

| 183-Day Rule | The test is described as living in Georgia for more than six months and spending at least 183 days within a 12-month period | Use a conservative count and build a month-by-month calendar |

| Primary place of business / primary economic interests | A person might be considered a tax resident if their primary place of business or primary economic interests are in Georgia | Use this path carefully and keep the facts coherent and consistent with how you actually live and work |

| HNWI program | The High Net-Worth Individual program is an alternative path with specific asset or income requirements | The thresholds are not provided here, so verify eligibility before relying on it |

If you cannot produce a clean timeline without guessing, treat your residency position as uncertain until you can.

Use the alternative basis carefully. The source also says a person might be considered a tax resident if their primary place of business or primary economic interests are in Georgia. That can matter when day count is not your main basis. If you rely on this path, make sure your facts are coherent and consistent with how you actually live and work.

Treat the HNWI path as eligibility first. The High Net-Worth Individual (HNWI) program is an alternative path with specific asset or income requirements. The thresholds are not published here, so verify whether you meet the eligibility requirements before relying on that route.

Do not decide the outcome first and retrofit your residency story later. Residency is the gate. If that gate is unclear, every tax position built on it gets harder to defend.

You might also find this useful: A Guide to Andorra's Low-Tax Residency Program.

Classify Your Crypto Activity Before You Claim Exemption#

Once residency is clear, classification becomes the deciding step. The same Bitcoin or Ethereum gain can read as personal investing in one case and business income in another. Do not claim a favorable outcome based on the asset alone. Match the result to how the income was actually earned, including any foreign-source position.

A practical filter helps here: the more your activity looks commercial, the harder it is to defend a pure investor position. That does not mean every active trader loses favorable treatment. It does mean phrases like "crypto is tax-free" are unsafe unless your facts clearly support an investor profile.

Use behavior, not the coin, as your first filter#

Start with conduct, not with the token involved. Watch for signs your activity is moving out of the personal-investor lane:

- frequent trading activity that may look like ongoing business activity

- non-disposal income streams, such as staking, yield farming, or airdrops

- patterns that may affect SBS eligibility, including high turnover or activity treated as a currency operation

One cited guidance point says crypto is often considered foreign-sourced, not always. If your facts are mixed, document why foreign-source treatment still fits, and where it may not.

Bucket wallet activity before you bucket tax treatment. Do this before filing season. Label each movement so a third party can follow your logic without guessing.

| Bucket | Typical examples | Records to keep | Main tax question |

|---|---|---|---|

| Personal investment disposals | Selling your own BTC/ETH, swapping assets you acquired for yourself | Exchange statements, wallet history, acquisition dates, disposal values, self-transfer notes | Does this still read as personal capital management, and can you support any foreign-source position? |

| Other crypto income streams | Staking rewards, yield farming proceeds, airdrops, or other non-disposal receipts | Wallet receipt history, platform statements, conversion records in GEL or foreign currency | How should this income type be classified before you choose individual, SBS, or company treatment? |

| Operational transfers | Moving assets between your own wallets, exchanges, custodians, or off-ramps | Internal transfer log, source and destination wallet IDs, timestamps, bank statement match | Is this asset movement rather than income? |

If you cannot label each CSV line cleanly, fix that now. Unlabeled flows make personal-activity treatment harder to defend later.

Be conservative when facts are mixed. If you have hybrid activity, do not force one story across all flows. Split and document each track separately: disposals, other income streams, and operational transfers.

For non-disposal income streams, keep records that show how each receipt arose. For investment disposals, keep acquisition and disposal support. For transfers, keep wallet-to-wallet mapping so internal moves are easier to distinguish from receipts or sales.

Apply the same caution to Small Business Status (SBS). One source presents SBS (1% tax on turnover for qualifying businesses) as efficient for many traders, but another says SBS applicability to crypto trading is uncertain. Two explicit risks are losing SBS if crypto trading is classified as a currency operation, and losing SBS if annual turnover exceeds 500,000 GEL.

A common mistake is claiming an investor outcome before separating disposals, other income streams, and internal transfers. Clean classification first, then exemption claims.

This pairs well with our guide on Hungary Tax Residency for Nomads and the White Card.

Compare Individual and Company Paths Before You Incorporate#

Choose a company only when you have a clear operating reason, not because you assume structure alone will improve your outcome. Individual and company treatment may follow different legal analyses, so decide structure only after you map how money and documentation will actually work.

Individual logic and company logic are different lanes#

As an individual, the confirmed checkpoints here are residency basis and documentation. If you use the HNWI route, confirm you meet asset and income thresholds rather than relying strictly on the 183-day rule, then verify you received the tax residency certificate and completed tax registration, including your TIN.

A company does not eliminate documentation work. Even if you have seen summary references to company-tax mechanics and payout treatment, verify them in current Georgian laws, regulations, and rulings before you rely on them.

Model cash movement before you choose structure. Before incorporating, draft a one-page cash map that shows:

- what stays in the entity

- what you need to withdraw personally

- when withdrawals happen

- which payout route you expect to use

Do not rely on headline summaries of a corporate model alone. For company treatment, confirm the legal mechanics in current Georgian laws, regulations, and rulings, and get professional guidance for your specific facts.

Compare decision friction side by side.

| Path | First decision question | What to verify now | Main failure mode |

|---|---|---|---|

| Individual | Do your facts support your residency path (HNWI route or day-count route)? | HNWI asset/income eligibility (if relevant), tax residency certificate, TIN, supporting records | Assuming status is settled before documentation is complete |

| Individual Entrepreneur | Is there a real business case for this form? | Whether IE setup and any Small Business Status assumptions fit your facts | Treating IE/SBS applicability as settled without confirmation |

| Company | Do you have a real operating reason to use an entity now? | Company tax mechanics and payout treatment under current law/rulings | Incorporating for a hoped-for tax result without verified mechanics |

Use a conservative decision rule. If key company mechanics are still unclear, stay individual for now and keep your records clean. If you still plan to incorporate, run a full company analysis before filing, including VAT and business-exposure planning.

Also treat summary guides as directional, not final authority. Even major guides note they can contain errors or omissions and may be dated, for example information stated as current as of February 2025. For restructuring decisions, use primary law and adviser review as the final checkpoint.

For a separate residency concept, see A Guide to the 'Look-Back' Rule for US Tax Residency.

Handle VAT and Mining Edge Cases Without Surprises#

Treat VAT as a separate analysis from your income tax position. In Georgia, VAT directly affects pricing, invoicing, reporting, cash flow, and compliance posture, so classify crypto-related activity before year-end instead of leaving it for filing season.

The standard VAT rate is 18%, but that headline number is not a crypto conclusion by itself. Keep your file activity-specific, and treat crypto-specific VAT conclusions as unresolved until you confirm them with current primary Georgian legal guidance.

Keep VAT analysis separate from your personal tax position#

Do not assume residency and personal income tax analysis answers VAT. Your VAT position depends on what you actually did and how those activities are legally characterized.

Start with evidence. Pull 12 months of invoices, exchange statements, wallet records, contracts, and bank inflows, then classify each line item with working labels such as:

- own-account investing

- service revenue

- operational transfer

If you cannot classify items cleanly, your VAT file is not ready.

Map mining by output, not by label. For Cryptocurrency mining, classify by output and payer, not by the word "mining." At minimum, separate:

- selling mined coins for your own account

- selling hash or computing output

- operating a hosted or managed service for someone else

Attach supporting records for each lane: pool terms, customer agreements if any, payout reports, wallet receipts, and the fiat settlement trail. Georgian VAT outcomes for these mining models require local legal confirmation, so keep treatment marked as pending until you obtain professional sign-off.

Treat VASP and AML as parallel checks. Specific VASP scope tests and AML obligations for crypto activity require local legal review. If your activity goes beyond personal holding and disposal, document your facts and route the question for local legal review rather than assuming treatment.

Keep that memo with your tax records, along with onboarding materials, counterparty lists, service descriptions, and transaction logs.

Validate before year-end. If your facts touch VAT, mining, VASP, or AML questions, run a year-end legal check while records and invoicing can still be corrected. Waiting until filing season increases the chance that a classification gap becomes a compliance issue with the Georgian Revenue Service.

If facts are mixed, take the conservative path: mark classification as unresolved, preserve complete evidence, and get local professional review before finalizing year-end treatment.

Related: Using a Data Processing Agreement (DPA) with Subcontractors.

Pressure-Test Home Country Conflict Risk Early#

If dual-residency risk is plausible, pause major crypto disposals until you have tested both countries' positions side by side. A move can look clean locally and still become costly if another country can support a parallel residency claim.

Reconcile the two systems before you move#

Treat this as a cross-border coordination check, not a single-country filing exercise. Crypto activity is global, and cross-border cooperation is an active focus across jurisdictions, so your position needs to hold up across borders, not just inside one local narrative.

Write down, for each country, the facts that strengthen your residency position and the facts that weaken it. Use primary authority for legal-status checks. Peer-review reports can help frame risk, but they are not binding legal authority. A bill marked "Introduced in House" (12/17/2024) is still a proposal, and contributor opinion pieces are not legal authority.

Build a simple conflict matrix. Use one page and force the facts into a comparison.

| Test area | What to collect | What increases risk |

|---|---|---|

| Residency claim strength | travel timeline, housing access, family ties, work pattern, banking and exchange footprint | both countries can present a credible claim for the same tax year |

| Treaty or tie-break relevance | whether a treaty exists, documents likely needed, where specialist review is required | assuming treaty relief without checking the actual text and process |

| Crypto exposure | planned or completed disposals of Bitcoin, Ethereum, and other holdings | large gains or concentrated sale windows while residency facts are still unclear |

Focus on disposal timing, not labels. Timing is often where cross-border positions are tested. A major disposal during a period when two countries may both argue residency can raise conflict risk. Delaying a disposal until your residency facts are stable is often safer than trying to repair a weak cross-border position after filing.

Before large disposals, make sure your evidence pack is coherent across both countries. That includes movement records, housing records, exchange history, wallet ownership evidence, bank inflows, and a short written position.

Use a practical rule for escalation. If you cannot explain your cross-border position clearly on one page, get advice before the sale. This matters most when ties to your prior country are still strong, the year is split, or the gain is material.

Your move works when your facts, timing, and filing position stay consistent across borders.

Related reading: Tax Residency in Mexico for Nomads Beyond the Temporary Resident Visa.

Build an Audit-Ready Evidence Pack From Day One#

The practical move is to build one clean evidence pack from day one, so every transfer and disposal is traceable without a year-end reconstruction.

Keep one folder and one version of the truth#

Use one master folder for the year under review, with clear subfolders for residency documents you rely on, exchange statements, wallet logs, and fiat account records. Keep related fiat and crypto records together by event, not in separate archives.

Each month, run a quick cross-match. Wallet movement, exchange activity, and fiat settlement should align by date, asset, and amount. If you cannot explain a transaction chain quickly, the pack is not audit-ready yet.

Track provenance before transfers blur the story. Label each transaction by source type: personal wallet, exchange account, or VASP interaction. This reduces the risk that internal transfers are later misread as new inflows.

Where a transaction touched a VASP, store the platform name, account identifier, and export date of the file you saved. One excerpt describes mainland VASP registration as regulated by the National Bank of Georgia, so clear counterparty records are a practical control.

Save your reasoning, not only raw exports. For each material treatment choice, keep a short note in plain language: what happened, how you treated it, and which facts support that treatment. Also record what could weaken your position.

That note protects you against hindsight edits. A short explanation written near the event is more reliable than a reconstruction at filing time.

Add monthly controls and flag business-like drift early. Run a monthly close: reconcile opening and ending balances, label internal transfers clearly, and keep an exceptions list for unmatched items. Resolve breaks while records and memory are still fresh.

Escalate early if activity starts to look frequent, commercial, or operational rather than personal. Once mixed patterns spread across wallets and accounts, your evidence becomes harder to defend.

Know the Red Flags That Require Professional Review#

If any of these red flags apply, do not treat your filing as routine. Get a Georgia tax review before you file.

| Red flag | What to prepare | Grounded issue |

|---|---|---|

| Frequent, business-like trading | A short memo with trading frequency, venues, whether you used only your own capital, and whether any client, signal, or execution service was involved | Confirm the threshold for when trading becomes a business with a tax adviser; do not assume foreign income is always exempt. |

| Moving from individual activity to a company | Bring your draft ownership setup, expected personal withdrawals, and planned distribution timing to an adviser before setup | The cited guidance describes Georgian crypto-trading companies as subject to 15% corporate income tax, with tax timing linked to profit distribution in that guidance, and dividend distributions as triggering an additional 5% withholding tax |

| Mixed income streams or service-like operations | Separate investing from consulting or other crypto-related services | Where operations become service-like, crypto businesses are described as regulated from January 1, 2023, with potential VASP licensing and AML/KYC obligations |

| SBS assumptions in crypto cases | Confirm SBS is active before billing, file monthly declarations on time, and monitor annual turnover | The cited guidance notes the 1% turnover regime for qualifying businesses, says SBS treatment for crypto is uncertain, and says crossing 500,000 GEL annual turnover means loss of SBS |

Your trading no longer looks like occasional investing#

A key red flag is moving from occasional investing into frequent, business-like trading when you cannot clearly defend foreign-source income treatment. The cited guidance warns against assuming foreign income is always exempt and flags activity misclassification as a common mistake.

Professional review matters here. Prepare a short memo with your trading frequency, venues, whether you used only your own capital, and whether any client, signal, or execution service was involved.

Another red flag is moving from individual activity to a company. If you are considering a company structure, review the full tax path before incorporating. The cited guidance describes Georgian crypto-trading companies as subject to 15% corporate income tax, with tax timing linked to profit distribution in that guidance, and dividend distributions as triggering an additional 5% withholding tax.

Model how you will actually use the company, not just headline trading treatment. Bring your draft ownership setup, expected personal withdrawals, and planned distribution timing to an adviser before setup.

Mixed income streams and SBS assumptions also need review. Mixed activity, for example investing plus consulting or other crypto-related services, is a red flag because classification becomes harder to defend. Where operations become service-like, crypto businesses are described as regulated from January 1, 2023, with potential VASP licensing and AML/KYC obligations.

Treat Small Business Status (SBS) conservatively in crypto cases. The cited guidance notes the 1% turnover regime for qualifying businesses, but also says SBS treatment for crypto is uncertain and may be denied based on classification. Confirm SBS is active before billing, file monthly declarations on time, and monitor the 500,000 GEL annual turnover limit because crossing it means loss of SBS.

Use Gruv Records to Reduce Filing Friction#

Use Gruv records to reduce admin friction, not to prove your tax position. For georgia tax residency crypto cases, treat platform data as supporting chronology only, then confirm legal treatment with an adviser using your full evidence set.

If the last section raised red flags, apply a stricter standard here. Platform records can help organize events, but they do not settle legal or filing questions by themselves.

Verify each Gruv record before you rely on it. Confirm you can match it to external evidence you control. For each item, tie date, amount, currency, counterparty, and purpose to bank statements, exchange records, invoices, or wallet history where available.

Use a quick stress test: sample entries from different months and rebuild each flow end to end. If you cannot explain one movement without guesswork, treat that record as incomplete for filing support.

Keep the records you still need outside the platform. Keep the full crypto-to-fiat trail when relevant. Preserve exchange confirmations, wallet references where applicable, bank evidence for the fiat leg, and a short note on business purpose.

One failure mode is keeping only one leg of a multi-step movement. That gap can show up during adviser review when timing, value, or purpose does not reconcile cleanly.

Use the records properly. Treat Gruv outputs as operational support, not as proof that compliance requirements were met or that your filing position is correct. When year-end treatment depends on legal judgment, have your adviser document the conclusion separately and keep that memo with your evidence pack.

Run a Pre-Filing Decision Checklist Before You Submit#

Before you file, lock the legal positions first and mark any interpretation-dependent point for professional sign-off.

Lock the residency basis first#

Confirm your residency basis before anything else. If you are using the 183-Day Rule, test it as a rolling 12-month period and use the 183 days or more threshold. Consecutive days are not required.

Treat this as an evidence check, not a memory check. Also confirm whether you may still have residency exposure in another country, because becoming Georgian resident does not automatically end residency elsewhere.

Recheck who the taxpayer really is. Separate individual residency from corporate exposure. These are different analyses, and passing one does not settle the other.

Review whether your facts indicate only personal activity or possible company-level exposure. Management, contract signing, employees, or operational control in Georgia can create corporate risk even when your personal position looks compliant.

Use a quick pre-filing check:

- classify each income stream as personal activity or company activity

- match each wallet or exchange account to its legal owner and controller

- flag any period where company management or operational control was exercised from Georgia

- if ownership, control, and banking do not align cleanly, pause and get advice before filing

Mark VAT and mining assumptions explicitly. If your position depends on VAT treatment, mining, or crypto-adjacent service classification, label that point as interpretation-dependent and get sign-off before submission.

Run a final evidence pack review. Make sure the file tells one coherent story across the full year. Keep transaction records for the full year, and link wallet history, exchange records, and fiat movements so a reviewer can follow ownership, timing, and purpose end to end.

Final pre-submit test: can a reviewer quickly confirm why you are resident, who earned the income, and why your treatment follows from the facts? If not, do not file on assumption.

Need the full breakdown? Read Tax Residency in Croatia: A Guide for Nomads on the Adriatic.

If your day-count or travel pattern changes often, keep a monthly log so your residency position stays defensible: Use the Tax Residency Tracker.

Conclusion#

Georgia can be favorable for crypto activity, but only when your residency basis, activity classification, and records all line up.

Start with status, then activity, then documentation. The favorable 0% treatment discussed in this article is framed for Georgian tax resident individuals holding crypto as a personal investment, not business or commercial activity. Territorial-tax framing helps only when the underlying facts are solid.

Use a conservative order of operations:

- Confirm your residency route first. Use either the 183-day path or the High Net-Worth Individual path, and keep proof that matches the route you rely on.

- Classify activity honestly. Keep personal investment activity clearly separated from business or company activity.

- Maintain records continuously. Build a clean year file so your position is defensible under review.

- Escalate mixed cases early. If facts are blended or complex, get local professional review before filing.

Also respect the limits in the excerpts. VAT outcomes are activity-specific, including different treatment described for hash sales within Georgia versus abroad. The rules may also change over time, so avoid building a filing position on a fixed assumption.

The durable advantage is a defensible position under current rules, not a headline about low tax.

If you want cleaner evidence trails for cross-border inflows and withdrawals, set up a workflow with traceable receiving records and payout statuses where supported. Explore Virtual Accounts.

Frequently Asked Questions

Is crypto really tax-free in Georgia for everyone?

No. The cited 0% treatment is described for resident individuals in Georgia (country) when crypto is treated as a personal investment, not business activity. The territorial-tax framing helps only if your facts support that resident-individual position.

How do I become a tax resident in Georgia in practice?

The cited routes are the 183-day path and the High Net Worth Individual (HNWI) path. For day count, the cited threshold is 183 days in a calendar year. For HNWI, the key checkpoint is a legal application to the Revenue Service, with supporting documents tied to that route.

Does the individual crypto exemption apply if I trade through a company?

Do not assume it does. The favorable treatment described in this article is tied to resident individuals, while company structures are treated separately, including an LLC model with 15% corporate tax upon profit distribution. If activity is company-run in practice, treat it as a separate tax analysis from your personal position.

Are crypto sales and conversions subject to VAT in Georgia?

This grounding set does not resolve VAT treatment for all crypto sales and conversions. If your filing position depends on VAT treatment, do not rely on assumptions. Get local professional sign-off before filing.

What can disqualify my claim to favorable crypto tax treatment?

Common failure points are straightforward: no valid Georgian tax residency basis, facts that look like business activity instead of personal investing, or company-level trading presented as personal. Dual-residency risk is another issue, because you may still owe tax in your home country. Treaty outcomes can help, but they depend on the specific treaty wording.

What records should I keep to defend residency and crypto tax positions?

Keep documentation that supports the residency route you claim and the basis of your position. If you rely on the HNWI route, keep the Revenue Service application and supporting wealth or income documents together.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- brooklynworks.brooklaw.edu/cgi/viewcontent.cgitrusted

- congress.gov/bill/119th-congress/house-bill/1/all-infotrusted

- congress.gov/bill/118th-congress/house-bill/10445/texttrusted

- cs.cornell.edu/courses/cs1110/2014fa/assignments/assignment...trusted

- cs.princeton.edu/courses/archive/spring18/cos226/assignments/...trusted

- democrats-agriculture.house.gov/uploadedfiles/117-36_-_49769.pdftrusted

- digitalcommons.law.uga.edu/cgi/viewcontent.cgitrusted

- dot.ga.gov/InvestSmart/Freight/GeorgiaFreight/GeorgiaFr...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Using a Data Processing Agreement with Subcontractors

Put your data processing agreement in place before a processor or sub-processor gets access to personal data. If you use a processor, UK GDPR guidance requires a [written contract or other legal act](https://ico.org.uk/for-organisations/uk-gdpr-guidance-and-resources/accountability-and-governance/contracts-and-liabilities-between-controllers-and-processors-multi/when-is-a-contract-needed-and-why-is-it-important). Set that contract boundary before support logins, shared folders, or troubleshooting access turn into live processing.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.