Quick Answer

Classify contractor obligations by document type and terms before payout: invoice-based trade credit belongs in Accounts Payable, while a written repayment agreement such as a Promissory Note belongs in Notes Payable. Use principal/interest signals, repayment structure, and maturity to route records, then present note amounts as Current Liability or Long-Term Liability based on what is due within 12 months. This keeps ledger posting, reporting, and close checks aligned.

How Platforms Classify Contractor Obligations#

Start with the document, not the payout. In platform operations, contractor obligations are usually easier to classify when you ask one practical question first: are you looking at a routine amount owed for services purchased on credit, or a formal written promise to repay a specified amount? That is the real split behind accounts payable vs notes payable platforms classify contractor obligations, and it matters more than whatever label appears in a product screen. If your team starts from payout status instead, you can misclassify the obligation before review even begins. We recommend making your document check the first approval step.

At a high level, Accounts Payable is money owed to suppliers for goods or services purchased on credit. Notes Payable is different: a written promise by a borrower to repay a lender a specific sum of money. Both appear on the Balance Sheet as liabilities, but they are not interchangeable because the purpose, structure, and time horizon are different. If your intake team treats them as the same thing, finance will usually feel it later in Reconciliation, close review, and audit support.

Bad classification does not stay local. It can weaken liability presentation quality and force cleanup across payout and reporting cycles that should have been avoided at intake. Proper journal-entry treatment for payables and notes supports more reliable financial reporting and audit readiness. So the first checkpoint is not "has this contractor been paid?" but "what is the source obligation document, and what terms does it contain?" If you cannot answer that with clear documentation and a short rationale note, you are already carrying avoidable risk.

A useful early rule is simple: Supplier Invoices and ordinary trade-credit obligations usually point toward Accounts Payable. A Promissory Note, or any obligation that clearly reads like borrowing, should move to Notes Payable review. Keep the verification concrete. Check whether there is a written repayment promise and whether repayment timing extends beyond normal operating payables. Those are small intake checks, but they help prevent larger downstream errors. We recommend treating them as your intake gate before your team routes the item. We would rather hold your queue for one clean check than let your team unwind the mapping later.

Timing matters for presentation too. The SEC balance-sheet basics are straightforward here: Current liabilities are obligations due within the next 12 months, while long-term liabilities are due more than a year in the future. That is especially important for Notes Payable, because maturity can make the same category short term or long term. If your team supports multiple entities or jurisdictions, do not skip controller review. Debt-classification rules differ across accounting frameworks, including IFRS and US GAAP, so platform logic that feels obvious operationally may still need accounting confirmation before you lock posting and reporting behavior.

At-a-glance comparison for contractor obligations#

Default from the source document: contractor Supplier Invoices usually map to Accounts Payable, while a formal Promissory Note or other written borrowing agreement maps to Notes Payable review.

| Criteria | Accounts Payable | Notes Payable | Platform implication |

|---|---|---|---|

| Source document | Supplier invoice matched to purchasing or receiving support | Written promissory agreement to repay cash | Capture the source document ID at intake. Invoice-backed items usually follow AP review; note-backed items should get finance/controller validation before posting. |

| Payment terms | Trade-credit terms, such as due in 30 days | Stated repayment terms with a maturity date | Classify from the document terms, not payout speed. |

| Debt terms | Not defined by a formal debt instrument in the source document | Written debt terms include principal, a stated rate, repayment terms, and maturity | If stated rate plus repayment structure appears, treat as note-like until validated. |

| Liability horizon | Usually handled as an operating payable | Can be Current Liability or Long-Term Liability based on due date | Check due date at posting and reporting: due within 12 months is current; later is long-term. |

| Link to operating cycle | Tied to normal operating purchases and settlement activity | Current classification still references one year (or the operating cycle, if longer) | Include operating-cycle logic in current/non-current checks where relevant. |

| Posting and reporting landing | Recorded in AP from invoice evidence | Recorded as notes payable from the written debt instrument | Keep ledger class aligned to obligation type; do not mix invoice obligations and note obligations because both are unpaid. |

The split is obligation structure, not contractor identity. The same contractor may have invoice-based service charges (AP) and a separate formal borrowing arrangement (notes), and they should not be treated as interchangeable.

Use a short intake checkpoint: confirm whether the file is invoice support or a written repayment promise, then check for note signals (stated principal, stated rate, maturity date). If those signals are present, pause invoice routing and request accounting validation before your team releases or schedules the item.

Ownership should be explicit. The key control is a clear handoff: one owner for document intake and one accounting owner for note classification sign-off. We recommend naming both owners in the same workflow so your reviewer can see who made the call and your team can see who owns the override.

Fast Invoice Processing can still hide classification risk when document controls are weak. If intake captures only amount and due date, a note can be routed like a routine payable, so require a brief rationale note with the mapped account class.

Your minimum evidence pack should include source document, document ID, due date or maturity date, whether a rate is stated, and mapped account class. If those fields are missing, your team does not have review-ready support even when payout execution is clean.

For a step-by-step walkthrough, see Accounts Payable Outsourcing for Platforms When and How to Hand Off Your Payables to a Third Party.

Classification rules at intake before money moves#

Classify from the source document before approval or payout scheduling: Supplier Invoice points to preliminary Accounts Payable, while a Promissory Note or other written repayment agreement points to preliminary Notes Payable.

This sequence keeps routing tied to obligation type instead of payment urgency. Accounts Payable covers amounts owed to suppliers for goods or services received on credit, typically without a formal written promise to pay. Notes Payable covers a written promise to repay, and the note generally states Principal, due date, and Interest.

Use a document-first intake sequence#

- Collect the source obligation document before any approval decision.

- Identify it as a Supplier Invoice or Promissory Note.

- Assign a preliminary class in the accounting record, then route to the matching approval path.

| Intake check | Points to Accounts Payable | Points to Notes Payable | Why it matters |

|---|---|---|---|

| Source document | Supplier Invoice | Promissory Note or written repayment agreement | The document is the strongest classification signal. |

| Principal stated | Usually no | Yes | Stated principal is a note signal. |

| Interest stated | Usually no | Yes | Explicit interest indicates debt terms. |

| Repayment structure | Ordinary trade-credit terms | Defined repayment terms with maturity | A note carries structured repayment obligations. |

| Timing context | Often short supplier windows (for example, 30, 45, or 60 days) | Can also be short-term | Timing alone does not determine AP vs notes. |

Set one bright-line rule#

As an internal control, treat obligations with formal borrowing terms and explicit interest as Notes Payable for finance review under your policy. If a promissory note is involved, use notes treatment instead of AP.

A common failure is classifying by payment urgency instead of document terms. If the document shows principal, interest, and a defined repayment structure, stop invoice-style routing and correct the class before funds move.

For auditability, keep an internal evidence record that matches the document and classification decision (for example: source document ID, owner, rationale note, and mapped account class). Check that record against the uploaded document before final approval.

Related: Manufacturing Accounts Payable Automation: How Industrial Platforms Pay Subcontractors and Suppliers.

How to post and report without mixing liabilities#

Keep posting lanes separate after intake classification: unpaid contractor invoices belong in Accounts Payable, and financing obligations belong in Notes Payable.

For Accounts Payable, post from the invoice lifecycle. At invoice acceptance and approval, record the contractor-services entry as a debit to the relevant expense and a credit to Accounts Payable. At settlement, record a debit to Accounts Payable and a credit to cash. As a control, each open AP item should trace to a Supplier Invoice and its payout status.

For Notes Payable, post from the signed note, not invoice handling. Track Principal, due date, and stated rate as note terms in a separate liability record. On the Balance Sheet, classify amounts due within one year or less as Current Liability, and amounts due after one year as Long-Term Liability.

| Posting and reporting point | Accounts Payable | Notes Payable |

|---|---|---|

| Source record | Supplier Invoice | Written note with principal, due date, and a stated rate |

| Initial posting logic | Debit expense, credit Accounts Payable | Separate note liability record with note terms tracked distinctly |

| Cash settlement logic | Debit Accounts Payable, credit Cash | Reduce note balance under note terms, not through AP |

| Reporting location | AP aging and unpaid invoice views | Debt schedule and Balance Sheet split between Current Liability and Long-Term Liability |

| Main operator check | Invoice and payout status agree | Due dates, principal balance, and note terms agree |

Use a two-queue reconciliation checkpoint. AP aging is designed to find overdue supplier invoices, typically in 30-day buckets such as 0-30, 31-60, 61-90, and older than 90 days, but it does not prove financing items are absent. If an AP-aged item has a stated rate or repayment schedule, treat it as a classification exception; likewise, routine contractor invoices should not sit in debt schedules.

A practical reporting split is:

- Finance: open AP, notes due within one year or less, notes due after one year, and reclassification exceptions.

- Ops: approved-but-unpaid invoices and note obligations on repayment schedules.

- Product: exception telemetry for note-like terms routed into AP, note documents entering invoice lanes, and invoice records appearing in debt reporting.

If you need one rule, use this: report unpaid contractor invoices in AP, report financing obligations in notes, and do not blend them into one unpaid-obligations view. If your team mixes them, the liability view gets harder to defend at close.

Month-end validation checks teams can run in minutes#

Run month-end as an exception pass: detect AP-vs-notes misclassification, confirm current/non-current note presentation, and pause close sign-off until differences are investigated and corrected.

| Check | What to compare | What signals a problem | What to do next |

|---|---|---|---|

| Rate exception scan | Obligations with a stated rate tagged as Accounts Payable | Financing-like terms routed through AP lanes | Pull the source document and route to note review if needed |

| Notes maturity split | Each Notes Payable item versus its repayment terms | Current and long-term portions are not separated correctly | Recalculate and update Current Liability and Long-Term Liability presentation |

| Open invoice reconciliation | Open Supplier Invoices, unpaid AP totals, and settlement records | Amounts or counts do not match across aging, unpaid AP, and disbursement status | Investigate and correct before close finalization |

| Controller checkpoint | A sample of 10 high-value items versus source document type and ledger class | Invoice records posted as notes, or note documents posted through invoice lanes | Document the exception, reclassify if needed, and trace whether intake or posting caused it |

Use each report for its job. The accounts payable aging report helps review unpaid invoices by current and past-due buckets, but it does not complete AP-to-GL reconciliation on its own. For tie-out, use a payables-to-general-ledger reconciliation report (or equivalent) built to reconcile payables transaction data to GL balances.

Also validate Balance Sheet presentation directly. Current and non-current liabilities should be presented separately, so notes should be checked against repayment terms, including what is due within 12 months.

We covered this in detail in Designing an End-to-End Accounts Payable Workflow for Platforms.

Edge cases that cause misclassification#

Misclassification usually starts when a contractor obligation stops looking like trade credit and starts looking like financing. Use this rule: once the obligation has a formal repayment structure with explicit Principal and a stated rate, reclassify from Accounts Payable to Notes Payable.

Accounts Payable is typically trade credit with no formal written promise to pay. Notes Payable is tied to written terms such as a repayment date structure, a specific amount owed, and interest terms, so counterparty type alone is not a valid classification signal.

| Edge case | What keeps it out of note treatment | What triggers reclassification | What to preserve for Reconciliation |

|---|---|---|---|

| Contractor advance | Label alone does not decide classification | A written repayment agreement with financing-like terms, including dated repayment structure and stated rate | Original contractor record, source document ID, approval trail, and the new agreement |

| Deferred payment agreement | A delay or extended Payment Terms by itself | Terms now match promissory-note characteristics: repayment date structure, specific amount owed, and stated rate | Original Supplier Invoice reference, revised terms, and effective date of change |

| Renegotiated overdue obligation | Unpaid amount still under ordinary trade-credit terms | Supplier replaces overdue payable with a new agreement that adds stated rate terms | Original invoice number, note date, original amount moved, and conversion reason |

The highest-risk drift is renegotiating an overdue invoice without reclassifying it. Accounting examples show overdue AP can be converted into a short-term note with interest, and when that happens the original amount moves from AP to notes. If due within the operating period (typically less than a year), it may still be short term, but AP and notes are still separate liability presentations.

For transition handling, keep the original Supplier Invoice link and create a new note liability record instead of overwriting history. Move the original owed amount out of AP into notes (for example, the conversion example uses $12,000) so the audit trail stays intact across intake, posting, and close.

If you close the invoice and open a note without a shared reference key, Reconciliation becomes fragile and duplicate liability risk increases. When terms become financing-like, document the trigger date, signed agreement, affected invoice IDs, and whether maturity is less than a year or beyond. If you skip that shared key, your team can end up reconciling the same obligation twice.

Failure modes in payout and settlement operations#

When classification is wrong, payout and settlement can look complete while financial reporting is wrong. The contractor gets paid, but the liability can remain in the wrong class, which forces retroactive Current Liability cleanup after close.

What breaks first#

The first break is usually a record-classification mismatch, not a failed payment. Settlement can show complete while the obligation is still posted as Accounts Payable when it should be treated as Notes Payable.

| Release check field | What to verify | If incomplete |

|---|---|---|

| Source document | Check it before payout for obligations that no longer look like standard trade credit | Hold release and resolve classification before close |

| Maturity | Check it because current versus non-current presentation can be misstated even when cash movement looks normal | Hold release and resolve classification before close |

| Classification fields | Check them because settlement can show complete while the obligation is still posted in the wrong class | Hold release and resolve classification before close |

Maturity then becomes the pressure point. Under IAS 1, a liability is non-current only when settlement can be deferred for at least 12 months after the reporting period. If teams track payout status but not the governing repayment terms, current versus non-current presentation can be misstated even when cash movement looks normal.

Use a release check before payout for obligations that no longer look like standard trade credit: verify source document, maturity, and classification fields. If those are incomplete, hold release and resolve classification before close.

Where the operational breaks show up#

Not every exception starts with classification, but wrong classification makes exceptions harder to trace and clear.

| Failure mode | First symptom | Typical cause | Control that matters most |

|---|---|---|---|

| Duplicate entries during retries | Two releases or postings tied to one obligation | Retry logic without a stable idempotency key across operations | Reuse one unique key for the same operation so retries return one effect |

| Mismatched payout statuses | Settlement shows paid out, liability stays open or clears in the wrong account | Payout and accounting statuses are not matched reliably | Reconcile payout status to posting status with shared reference IDs and daily exception review |

| Orphaned records between Settlement Workflow and ledger postings | Settlement record exists without a matching ledger post, or the reverse | No durable link between settlement event and ledger entry, or one side failed silently | Require a posting reference that follows the obligation from intake through release |

Payment APIs are often retried by design, so idempotency has to cover both payout actions and ledger posting effects. Reconciliation is record matching; when one system says settled and another says still open, finance inherits manual exception work. A transaction-level settlement details report gives a direct checkpoint for what was settled and paid out versus what was posted.

Controls and escalation#

Keep the control set simple and strict:

| Control | Apply to | Rule |

|---|---|---|

| Idempotent posting keys | Payout actions and ledger postings | Retries do not create a second liability movement |

| Approval gates before release | Debt-like obligations | Require document ID, classification rationale, and maturity fields |

| Exception queues | Obligations that no longer fit ordinary trade-credit handling | Route them to an exception queue |

For key lifecycle, keep a concrete minimum retry-safe window. Stripe guidance notes idempotency keys can be removed after at least 24 hours.

Escalate when close quality is at risk: unresolved classification conflicts at close, repeated mis-tagging by the source team, or recurring Reconciliation breaks. At that point, fix intake and release controls, not just the latest entry. Related reading: How Platforms Stop Business Email Compromise in Accounts Payable.

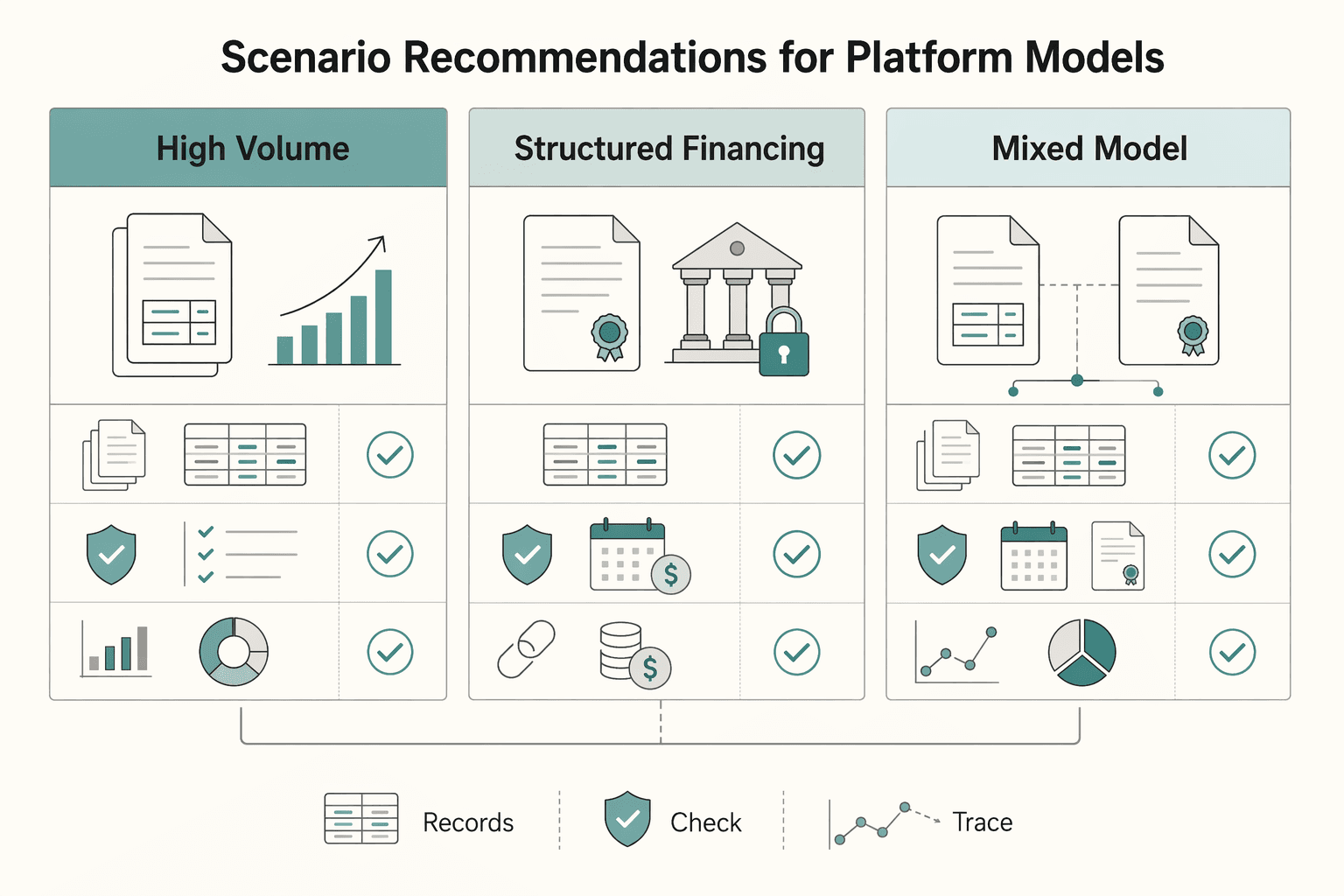

Scenario recommendations for platform models#

Default by obligation type: route routine contractor-credit invoices to Accounts Payable, route formal financing agreements to Notes Payable, and use dual lanes when both exist.

| Platform scenario | Default route | Verify before release | Red flag |

|---|---|---|---|

| High-volume contractor invoice processing with standard payment terms | Accounts Payable | Invoice is present, service or purchase is matched, approval is complete, and the item follows receive, code, match, approve, schedule, pay, and record | Any explicit repayment schedule or interest/rate term |

| Structured financing with a formal contract or promissory note | Notes Payable | Written terms show repayment timing and interest rate, and your system tracks Principal and Interest separately | Team pushes it through the normal invoice queue |

| Mixed model with operating invoices and financing obligations | Dual-lane AP + notes | Intake captures document type first, then routes invoices to AP and debt instruments to notes-specific approval and reporting | One aging queue or one approval path handles both |

For high-volume invoice operations, AP is usually the right default because it records supplier purchases on credit and typically does not include interest. Keep intake strict: if the document is not a standard supplier invoice, or terms include principal-and-interest repayment, stop auto-clear and reroute.

For contractor financing, start in notes from day one. Keep the promissory note, repayment date, and interest rate attached to the record, separate Principal and Interest, and review presentation against the 12 months cutoff. If an overdue AP balance is converted into a note, move it out of AP aging at the same time so operations and finance stay aligned.

For related workflows, see AP aging operations and Accounts Payable vs. Accounts Receivable for Platforms and the Two-Sided Ledger.

Conclusion#

The deciding rule is simple: classify contractor obligations from the document that created or replaced the liability, not from how old the balance is or what happened in payout. If the record is a supplier invoice for goods or services bought on credit, it belongs in Accounts Payable. If that obligation has been replaced by a written promise to repay, such as a signed promissory note with repayment terms, it belongs in Notes Payable and should be reviewed as debt, not routine trade credit. We recommend making that distinction explicit in your approval path so your team is not guessing from aging buckets.

| Sign-off check | What to confirm | Grounded rule |

|---|---|---|

| Document type | The document that created or replaced the liability | Classify from the document, not from how old the balance is or what happened in payout |

| Account class | Accounts Payable or Notes Payable matches the obligation | Supplier invoice goes to Accounts Payable; written promise to repay goes to Notes Payable |

| Presentation split | Any current versus long-term split for note balances | Use the 12-month deferment test |

| Edge-case handling | Renegotiated invoices, deferred payment arrangements, and other borderline items | Do not let them drift between AP and notes without a documented trigger |

That document-first discipline helps keep your Balance Sheet believable. Clear distinctions between AP and notes improve liability classification, and the difference matters even more once you have to present current versus longer-dated amounts. For note balances, the check that matters most is the IAS 1 criterion: do you have the right to defer settlement for at least 12 months after the reporting period? If yes, the non-current portion may stay out of Current Liability. If not, treating it as long-term can create reporting cleanup later. If your team cannot answer that deferment test quickly, the classification is not ready for sign-off.

The payoff is less drama at close. Accurate entries for AP and notes support financial reporting quality, and month-end control still comes down to basic evidence. Was the item recorded in the correct period, reconciled to the general ledger, and supported with documentation before financials were finalized? A useful checkpoint is to make sure no financing obligation is still sitting in AP aging and no ordinary contractor invoice is stranded in a debt schedule. When either happens, Reconciliation slows down because teams are arguing with labels instead of matching records. We would rather see your team stop that mismatch early than explain it to reviewers at month-end.

A common failure mode is a control gap. Teams let payout status, aging, or manual tagging override the underlying document, then discover late in the close that the account class does not match the obligation. If you let payout status override the document, your team will spend close week unwinding a classification error that should have been blocked at intake. You can reduce that risk by requiring the source document, owner, and rationale note on intake, and by making month-end validation non-optional for items with note-style terms or repayment structures.

Your next step is practical. Put the intake checklist into the approval path, then run the month-end validation checks before sign-off: confirm document type, confirm account class, and confirm any current versus long-term split using the 12-month deferment test. After that, review edge-case handling with finance and product owners so renegotiated invoices, deferred payment arrangements, and other borderline items do not drift between AP and notes without a documented trigger. We recommend keeping that review in the same approval path your team already uses so borderline cases do not get handled off to the side. We would rather see your approver stop one ambiguous item than let your team relabel it after payout.

Frequently Asked Questions

Are contractor invoices usually Accounts Payable or Notes Payable?

Usually Accounts Payable. If a contractor sends a standard supplier invoice for goods or services already received, and the obligation sits in normal short term trade credit terms, AP is the starting point. In practice, many of these items fall into the typical 30 to 90 days payable window rather than a formal borrowing arrangement.

When does a contractor obligation move from Accounts Payable to Notes Payable?

It moves when the unpaid balance is replaced with a formal written borrowing obligation, typically a promissory note. A common trigger is when the creditor asks for a note for the remaining balance instead of leaving it as an overdue invoice. Do not reclassify only because an invoice is late. You need the new written agreement, not just aging.

Why does a stated rate usually indicate Notes Payable treatment?

A stated rate is a strong signal that you are no longer looking at ordinary trade payables. Notes payable are written promises to repay borrowing, and that kind of pricing is a standard feature of the obligation over time. That does not mean every item with an extra charge is automatically a note in every jurisdiction, but if you see a stated rate plus a repayment structure, send it to finance review instead of leaving it in AP.

How should teams present Current Liability and Long-Term Liability for Notes Payable?

For note obligations, presentation turns on whether the entity has the right to defer settlement for at least 12 months after the reporting period under IAS 1. The portion due within the next 12 months belongs in Current Liability. The remainder can stay in Long-Term Liability only if that deferment right exists. In practice, focus on the note’s contractual repayment terms when making this classification call.

What document evidence should be required before classification is finalized?

For AP, require the contractor or supplier invoice and proof that the obligation relates to goods or services received. For notes, require the signed promissory note or equivalent written agreement showing repayment timing and any stated rate. In both cases, keep the document attached to the accounting record with the classification rationale to reduce close and reconciliation issues.

What is the fastest way to catch misclassified contractor obligations before month-end close?

Reconcile AP activity to the general ledger before financials are finalized, and make sure each balance is supported by documentation. As a quick exception pass, pull open AP items and review anything backed by a promissory note, a repayment schedule, or a stated rate, because those are the records most likely to be sitting in the wrong bucket. If you want one simple rule, flag “AP balance with note-style documents attached” for review before close sign-off.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 7 external sources outside the trusted-domain allowlist.

- sec.gov/files/balancesheet-building-blocks.pdftrusted

- accountingcoach.com/blog/notes-payable-accounts-payableexternal

- accountingcoach.com/blog/what-is-accounts-payableexternal

- accountingtools.com/articles/the-accounts-payable-aging-report.htmlexternal

- allianz-trade.com/en_US/insights/accounts-payable-vs-notes-pay...external

- biz.libretexts.org/Bookshelves/Accounting/Financial_Accounting_...external

- cflowapps.com/notes-payable-vs-accounts-payableexternal

- corporatefinanceinstitute.com/resources/accounting/notes-payableexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Staffing Platforms Automate Healthcare AP for Clinical Contractors

A key distinction matters: the material reviewed here focuses on healthcare AP workflows, not contractor-payout orchestration. If your expansion bet depends on reliable contractor payments, generic healthcare AP language is useful context, but it is not enough on its own.

Manufacturing Accounts Payable Automation for Industrial Platforms Paying Subcontractors

Industrial finance teams do not need another feature checklist. They need a clear way to decide what belongs inside AP automation, what belongs in payout infrastructure, and what needs to stay tied to ERP and production controls so payables do not create downstream delays.

Accounts Payable Aging Report for Platforms: How to Track Overdue Contractor Payments

Build this to drive action, not just generate another finance report. For platform teams, an AP aging report is most useful when each overdue line shows what is owed, when it was due, and whether the issue is a payable aging problem, a process delay, or payment-system risk.