Quick Answer

Platforms use zero-knowledge proofs to verify specific payment-related claims without receiving the underlying personal data. The workable approach is to keep KYC and AML reviews authoritative, tie each proof to one yes-or-no decision, restrict payloads and logs to proof-linked metadata, and define fallback, audit, and rollback paths so lower disclosure does not create new operational risk.

Why ZKPs matter for payment verification right now#

ZKPs matter for payment verification because they let you verify a claim while disclosing less raw user data. That is the promise. The catch is that the privacy gain depends on how you implement the full path from onboarding to authorization to payout. If those flows still collect, copy, and move sensitive records, stronger checks may improve control while leaving the same exposure in place.

Start with the core operational tension#

You need verification to build trust, and every extra data point you collect can become a liability. The practical value of a ZKP is simple: a prover submits a proof, and the checking system validates that proof instead of rerunning the underlying computation or receiving the raw data.

That is why this matters to payment systems now, not just to cryptography theory from the 1980s. It gives you a concrete way to confirm required conditions without transmitting the full underlying record every time.

Set expectations before you commit integration effort#

The goal is not to assume a zero-knowledge design automatically makes a flow private or compliant. The goal is to reduce raw-data disclosure without creating avoidable integration risk.

That distinction matters because privacy outcomes depend on implementation. Some descriptions frame ZKPs as a trustless verification layer. Real financial-compliance designs can still rely on a trusted off-chain KYC provider before proof checking. One January 2025 framework, for example, combines trusted credential validation with a single Sepolia smart contract that verifies submitted proofs.

So evaluate the whole path, not just the proof primitive. Ask who validates credentials, who checks proofs, what gets logged, and where raw identity data can still re-enter the system.

Define success before architecture debates start#

Define success before the architecture debate starts so the work stays tied to outcomes, not novelty.

- Lower the sensitive-data surface area across onboarding, authorization, and payout checks.

- Avoid unnecessary friction or repeated checks in the user flow.

- Define clear controls for cases where proofs fail or require exceptions.

- Keep audit-ready evidence of what was checked, what passed or failed, and how the decision was made.

Use one design test throughout. After verification, can your system make the payment decision from proof results and decision metadata alone? Or does it still need to pull raw personal records back into routine APIs or logs? If it still needs the raw data, you may be adding cryptography on top of the same exposure pattern.

If you want a deeper dive, read Invoice Verification for Platforms: How to Validate Contractor Bills Before Releasing Payment.

What to prepare before you design anything#

Do not start with proof design. Start by mapping your current verification path end to end. A ZKP is most useful when it clearly removes an existing raw-data exposure you can already point to.

Map the current verification path first#

Inventory every verification moment in your current flow, and record what each step does. For each step, capture the trigger, data received, decision output, downstream consumer, and where evidence is stored.

Use one real case as a trace test. If you cannot show where sensitive inputs land or which service reads the result, your baseline is not ready.

Separate current controls from proof use cases#

Document the protections you already run, and keep them separate from ZKPs. Those controls may protect parts of your system, while a proof is about validating a claim without revealing the underlying data.

Mark overlap and gaps. If a proposed proof only duplicates protection you already have elsewhere, it is usually a weak first use case. Also check copied credentials and stored secrets, since centralized stores can still become a large honeypot.

Draft a narrow pilot brief#

If you run a pilot, keep the brief focused on the in-scope verification moment, the claim to prove, and the data that should not be disclosed. Define a fallback path if proof verification fails.

Do not import payment-specific ownership, rollout, and go/no-go mechanics from outside examples unless you have direct evidence they fit your own environment. For a related operating example, see How to Build a Payment Reconciliation Dashboard for Your Subscription Platform.

Define the claims you will prove and the data you will not reveal#

Scope comes before cryptography. If a claim is vague, the proof can either leak too much or fail to replace the raw-data check you were trying to remove.

A Prover should assert one narrow statement, and a Verifier should accept or reject it without receiving anything beyond whether that statement is true.

Write each claim as a binary statement#

Turn policy language into a testable yes-or-no statement. Keep one claim tied to one decision, such as an eligibility-style check, without attaching the underlying records.

Bundling multiple decisions into one proof can make exceptions harder to handle and may increase the odds that someone asks for raw documents later. A good checkpoint is this: can the receiving system return yes or no and a decision code, with no extra fields?

For each claim, define:

- the exact statement being proved

- who is the Prover

- who checks the proof

- what decision the system may take from the result

- what fallback path runs if verification fails

If you cannot express it as one testable statement, narrow the claim.

Choose the interaction mode with explicit assumptions#

For distributed payment verification, noninteractive proofs can reduce coordination because one prover message can be enough for acceptance.

| Interaction mode | Message pattern | Grounded note |

|---|---|---|

| Noninteractive proofs | one prover message can be enough for acceptance | can reduce coordination |

| Interactive proofs | require the prover and verifier to exchange protocol messages | fit controlled cases where both parties are online and message exchange is acceptable |

| Fiat-Shamir heuristic | transforming certain interactive proofs | treat that as a reviewed design choice |

Interactive proofs require the prover and verifier to exchange protocol messages, so they fit controlled cases where both parties are online and message exchange is acceptable.

Keep one assumption explicit. Noninteractive form is not assumption-free in every setting. A common path is transforming certain interactive proofs with the Fiat-Shamir heuristic, so treat that as a reviewed design choice.

Attach a do-not-disclose list to every claim#

A claim is not complete until it has a do-not-disclose list. That is what turns privacy intent into enforceable boundaries in APIs, events, and logs.

For example, if the claim is "eligible for payout release," the receiving system should get the proof result and only the minimum metadata needed to act. Raw source documents and other prohibited attributes should stay out of payloads and logs.

One failure mode is defining the proof but not the payload boundaries, then leaking prohibited fields through structured logs or exception traces. Include log and event review in design signoff.

Add an acceptance test for every claim#

Before rollout, require one acceptance test per claim:

| Acceptance check | Requirement |

|---|---|

| True claim | verifies successfully |

| False claim | is rejected |

| Prohibited attributes | do not appear in API responses, events, or logs |

| Proof generation time | track concrete implementation behavior |

| Gas consumption | track concrete implementation behavior |

| Transaction costs | track concrete implementation behavior |

Check outputs, emitted events, and logs, not just cryptographic validity. Track concrete implementation behavior too, such as proof generation time, gas consumption, and transaction costs. The claim should verify when true, fail when false, and stay bounded in what it reveals.

If a claim fails any of these checks, narrow it before deciding where it belongs in the lifecycle.

Place ZKP checks at the right points in the payment lifecycle#

Put ZKP verification where it reduces repeated raw-data sharing, not where it creates a parallel compliance path. Keep KYC and AML gates authoritative, then use proofs for narrow yes-or-no checks that downstream systems need to trust.

Map each proof to one lifecycle decision#

Attach each proof to one decision point only. The public material on noninteractive ZKP compliance audits shows an overall process, but it does not prescribe exact placement across onboarding, payment authorization, wallet movement, and payout release.

Use a proof when the downstream service needs an accept-or-reject result, not the underlying record. If a stage still needs document review, suspicious-activity escalation, or exception handling, keep the raw-data path there.

Keep KYC and AML as hard boundaries#

Treat proof checking as a privacy-preserving control inside your existing governance flow. Do not let teams choose between a "raw KYC/AML path" and a "proof KYC/AML path" for the same policy gate.

A practical pattern is to complete the authoritative review once, then validate a narrow approved-status claim later without resharing the full evidence set across services.

Keep end-to-end traceability explicit#

Traceability has to survive the privacy improvement. Operators should be able to reconstruct what happened without reopening sensitive records. A practical audit trail can include a request identifier, proof or policy version, proof result, decision code, and resulting state.

Keep privacy checks and operational-risk checks separate in review. One checkpoint tests whether sensitive fields stay out of payloads and logs. Another tests whether decisions remain reliable under retries, failures, and degraded dependencies.

At any lifecycle decision point, use raw data when full document review, analyst judgment, or exception handling is required. Use a ZKP when a downstream service only needs a bounded yes-or-no attestation from an already completed control. In either case, keep an audit trail with the request ID, policy or proof version, proof result, decision code, and resulting state.

Define failure paths before launch#

Define failure behavior for each checkpoint before rollout: proof failure, timeout, stale dependency, and manual review trigger. Each path should return a deterministic outcome and route to a clear owner.

Make retries idempotent so duplicate verification attempts cannot create duplicate financial state transitions. Test replay and timeout scenarios explicitly to confirm that only one authorization or payout state change is ever applied. If you need the full breakdown, read How to Build a Payment Compliance Training Program for Your Platform Operations Team.

Choose a proof system for first production scope#

For first production, pick the proof family you can defend in security, compliance, and operations review with concrete evidence, not the one that looks most advanced.

Compare proof families against real production constraints#

Keep the decision anchored to four criteria: proof size, verification speed, trust assumptions, and implementation complexity. The goal is a reliable allow-or-deny checkpoint with traceable evidence, not an abstract cryptography win.

Current material still flags practical constraints such as limited circuit expressiveness, high proving cost, and deployment complexity. It also highlights tradeoffs across efficiency, scalability, and security. The privacy gain is real, but it is not free.

Use a compact evidence pack for each option:

- one sample claim and circuit scope

- one measured proving path and one measured checking path in your environment

- one security note listing trust assumptions

- one operator note for failure handling and fallback

Ship only when the design produces a proof-linked decision output that downstream services, reconciliation, and audit teams can trace to the policy outcome.

Evaluate setup-dependent proof options as one candidate path#

If the first use case is latency-sensitive or sits inside an existing authorization or payout gate, evaluate setup-dependent options directly in your environment before deciding.

If a candidate requires setup artifacts, document those assumptions explicitly and record who accepts that risk. Keep the review operational: note where setup-dependent artifacts enter the stack, how they are stored and versioned, and how rotation or replacement is handled.

If proving cost or deployment complexity threatens batch windows, payout cutoffs, or response-time targets, reduce circuit scope or defer.

Evaluate setup-transparent alternatives when reviewer confidence is the priority#

If reviewers care most about setup transparency, include alternatives that match that preference in first-scope evaluation. Keep the discussion tied to deployment reality. Can your scope absorb the integration and operational complexity without delaying rollout or reducing visibility?

Test at a concrete checkpoint. If the proof supports an eligibility yes or no for payout release, confirm that the checking service returns a clear decision artifact that reconciliation and audit teams can use directly. If finance or compliance cannot use that artifact, defer.

Record heuristic assumptions and assign signoff#

Current evidence does not identify where specific heuristics appear in a payment stack. If your implementation uses assumptions such as Fiat-Shamir, list where they appear and who signs off.

At minimum, security review should capture:

- which proof path uses that assumption

- which library or implementation introduces it

- which owner approved the assumption

- which evidence is retained with the release decision

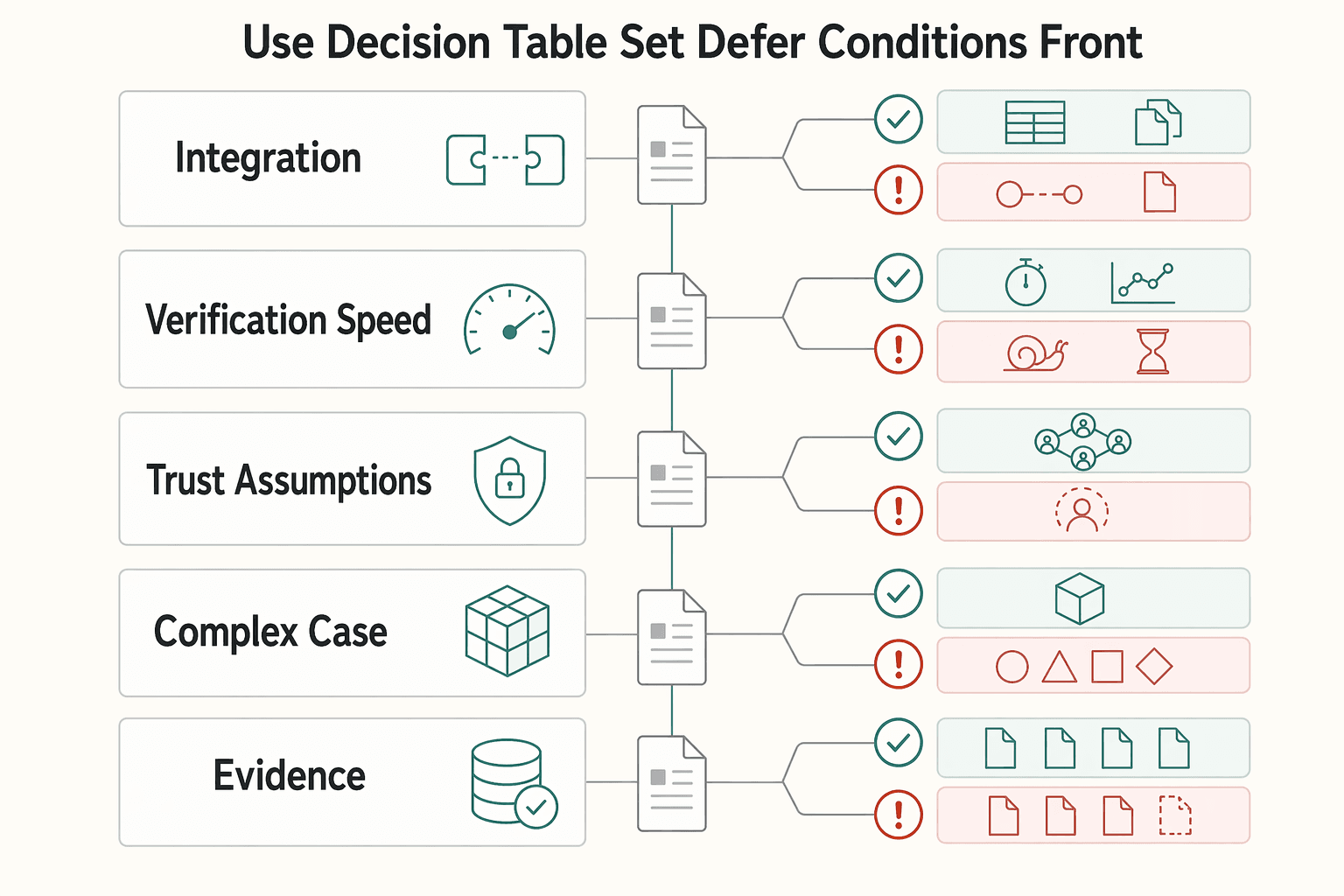

Use a decision table and set defer conditions up front#

| Criterion | Owner | Evidence required | Defer when |

|---|---|---|---|

| Proof size fit for target integration path | Engineering lead | Measured proof artifact from pilot claim, proof-result payload example, downstream compatibility check | Proof packaging breaks API or event limits or creates handling risk |

| Verification speed fit for decision point | Payments engineering | Timed validation test in staging, request-to-decision log, fallback behavior note | Verification path risks response-time targets or payout cutoffs |

| Trust assumptions are reviewable | Security lead | Written assumptions memo, setup artifact inventory (if applicable), approval record | Security cannot explain or accept setup or heuristic assumptions |

| Implementation complexity is supportable | Platform ops and engineering | Deployment note, rollback path, on-call failure modes, versioning plan | Proving cost, circuit scope, or deployment burden exceeds team capacity |

| Audit evidence is sufficient | Compliance and finance ops | Proof-linked decision output, reconciliation sample, audit trail mapping | Outcome is not traceable without reopening raw sensitive records |

If any row is red, defer. For a first production scope, a smaller, explainable proof is usually safer than a broader design that adds operational uncertainty.

For adjacent operating detail, see How to Build a Finance Tech Stack for a Payment Platform: Accounts Payable, Billing, Treasury, and Reporting.

Build compliance evidence without expanding your PII footprint#

The right target is straightforward: treat the proof output as the compliance artifact, and treat raw identity data as an exception path. If the proof check limits disclosure but your logs, alerts, or support tickets still copy identity documents or personal attributes, you may keep much of the same privacy risk while adding complexity.

Map each proof output to a compliance check reviewers already use#

Anchor evidence to checks reviewers already recognize, such as identity verification, beneficial-ownership checks, and ongoing transaction monitoring. Then make sure each proof produces a clear decision artifact that a non-cryptography reviewer can read.

For each claim, keep a compact evidence pack: claim name, proof result, request ID, policy version, and where any underlying governed record lives outside the application path. A practical test is whether compliance or finance can explain an allow or deny decision from that pack alone. A useful pattern is threshold proofing, such as proving a user is over 18 without exposing the full birthdate.

Remove raw personal data from logs and support tooling#

If you are serious about reducing exposure, start with logs and support tooling. Default to logging proof metadata, not personal artifacts. A known failure mode is collecting onboarding documents and then storing them indefinitely with weak governance.

Log the proof ID, claim type, proof-check version, and decision outcome. Avoid logging document fields, uploaded images, or free-text notes that restate them. In support flows, link to governed records instead of embedding copies. That reduces the chance of creating a data honeypot.

Validate this operationally. Sample recent logs, alerts, and exception tickets, then confirm that they do not contain raw identity artifacts.

Document regional assumptions without over-claiming what proofs do#

Keep the legal position narrow and defensible. Proofs can help validate required conditions while minimizing data exposure. They do not replace identity verification or AML policy gates.

For data-protection alignment (including GDPR/CCPA where relevant), document what each artifact proves, what remains outside the proof path, and when manual review applies. For EU-facing designs, include how your model fits privacy goals alongside MiCA and AMLR review context without claiming specific legal thresholds from the proof itself.

Define retention classes for proof artifacts, logs, and exceptions#

Do not apply one blanket retention rule. Records retention is part of verification operations, but universal retention durations are not established here, so define classes, owners, and deletion triggers through your policy process.

| Record type | Keep | Exclude | Audit checkpoint |

|---|---|---|---|

| Proof artifact | Proof ID or hash, claim name, proof-check version, timestamp | Raw identity fields, document images | Auditor can tie proof to request and policy result |

| Decision log | Request ID, decision outcome, policy version, service actor | Full KYC payload, copied source documents | Team can reconstruct allow or deny without reopening sensitive records |

| Exception ticket | Reason code, reviewer, escalation path, link to governed source | Embedded screenshots, pasted IDs, free-text personal data | Manual review is explainable without creating a second data store |

If a ticket or log needs raw personal data to be usable, treat that as a design defect and fix it before scale. Keep these retention classes aligned with your broader payment data privacy policy.

For a step-by-step walkthrough, see How to Build a Compliance Operations Team for a Scaling Payment Platform.

Engineer for reliability under real payment load#

Privacy is only half the job. In payment verification, reliability matters just as much. Current evidence suggests that hybrid off-chain and on-chain designs are practical, but testing maturity is still limited, so failure handling should be explicit from day one.

Treat the verifier as a dependency that can fail#

Design proof checking as a fault-prone dependency, not as a local call that always succeeds. In hybrid flows with a trusted off-chain KYC provider, a prover, and a proof-checking service, define what happens when the result is late, unavailable, or ambiguous.

Keep the policy outcome deterministic. If verification is required and does not complete, route to a clear state such as pending review, retry queued, or denied with a reason code. Do not silently bypass the gate.

Separate transport security from proof privacy#

ZKPs let you verify a claim without exposing the underlying data, but they do not by themselves define how transport or orchestration is secured. Keep your existing transport and operational controls in place alongside the proof flow.

Operationally, make sure proof request IDs, payment or payout references, and proof outcomes stay bound end to end so teams can explain one decision path per request.

Require idempotency on verification and money movement#

Design for idempotent handling in both verification requests and the payout or authorization action that depends on them. Current evidence does not define standard key formats or universal replay-safety guarantees, so specify and test this behavior in your own system.

This matters even more when you combine off-chain checks with an on-chain proof-checking component. One example is the January 2025 MVP pattern using Groth16, Circom, and snarkjs with a single smart contract on Sepolia.

Track metrics operators can act on#

Do not stop at cryptographic validity. Track reliability metrics operators can actually use.

The January 2025 MVP tracked proof generation time and gas costs. Use that as a baseline signal, then add business-impact monitoring in your own environment. Given limited qualitative user testing and uneven industry experimentation, validate those thresholds before scale. We covered this in detail in How to Build a Deterministic Ledger for a Payment Platform.

Roll out in phases and keep a clean rollback path#

Roll out ZKP verification in controlled phases, and only expand scope when you can roll back quickly without changing money-movement logic.

Narrow the first corridor#

Start with one narrow claim and one limited flow so you can observe behavior clearly before broad rollout. Keep the first release intentionally simple: one prover path, one checking path, one policy outcome, and one owner group.

Keep the scope tight for scale risk too. A July 2023 paper on the privacy-enhanced blockchain platform ZGridBC warns that at very large populations, for example around two million, blockchain may not process all transactions. That result comes from an electricity-tracking context, not a payment benchmark. It is still a useful warning to validate throughput and queue behavior before widening coverage.

Run shadow mode and force mismatch triage#

Before enforcement, run ZKP verification alongside your current control and compare outcomes per request. Store enough detail to reconstruct one end-to-end decision trail: current decision, proof result, reference IDs, proof version, and mismatch reason.

Do not expand rollout while mismatches are unexplained. Keep shadow mode active until your team can consistently explain why the paths disagree and resolve those gaps.

Promote only after explicit checkpoints#

Treat enforcement as an internal gated decision. Set explicit checkpoints for technical reliability and retained decision evidence before broad enforcement.

Document those checkpoints with traceable artifacts: sample decision traces, mismatch tickets, and dated owner signoffs. If you already use payment tokens in this corridor, keep identifiers stable during the pilot so reconciliation variance stays isolated to the proof path.

Rehearse rollback before you need it#

Define rollback triggers in production symptoms, such as verification error spikes, payout backlog growth, or evidence gaps. Assign owners and make the enforcement-off switch and in-flight state transitions explicit.

Practice rollback as an operational drill. Confirm that traffic returns to the prior control path, idempotency protects against duplicate payout actions, and pending items do not get stranded. If both payout operations and explainability degrade, roll back first and investigate second.

For a related finance-ops view, see Lean Finance and the Modern CFO: How Payment Platform Leaders Evolve from Cost Center to Strategic Driver.

Common mistakes that create platform debt and how to recover#

Platform debt often starts when the proof gets the wrong role. Reset early if your ZKP path starts acting like a compliance override, a hype-driven choice between zk-SNARKs and zk-STARKs, or a replacement for baseline payment controls.

Keep KYC and AML as the authority#

ZKPs should reduce disclosure, not replace policy gates. Keep KYC and AML decisions authoritative, and map each proof to a named gate owner and decision point in your policy flow.

A practical checkpoint is traceability. For any onboarding or payout decision, you should be able to reconstruct the policy decision and the proof result. You should also be able to trace the trusted off-chain KYC-provider reference when one is used before proof generation. Watch for a failure mode where the prover or proof-checking service approves a narrow claim while the broader compliance decision is still unresolved.

Re-run the proof-system choice against real constraints#

If your zk-SNARKs or zk-STARKs choice came from network momentum, run it again against production constraints. In regulated payment environments, privacy, performance, and operational cost can pull in different directions, and prototype-era crypto choices can harden into long-term architectural debt.

Weight your decision table around verification latency, trust assumptions, implementation complexity, and operator overhead. Attach evidence, not preference: security review notes, integration effort, and explicit defer conditions. If the current choice does not survive that review, change it before proof-check behavior hardens in APIs, events, or contracts.

Layer ZKPs with baseline controls instead of replacing them#

Keep ZKPs as one control in a layered design, not as a substitute for controls like 3D Secure and data encryption. Leave baseline controls active at their current enforcement points and test incident paths where proof verification degrades or fails.

Run one concrete failure drill for your architecture. If you use an off-chain and on-chain split, or a single proof-checking contract as in the January 2025 proof of concept with one Sepolia contract, test proof-check unavailability and confirm fallback behavior. Treat this type of implementation as proof-of-concept rather than full production validation, especially when user testing is limited. You should retain decision evidence and have a named owner who can disable proof enforcement without weakening the rest of the payment path. You might also find this useful: How to Hire a CFO for Your Payment Platform.

Copy and paste launch checklist#

Use this as a release gate: if any item is incomplete, do not enforce proof-based verification in production.

| Release gate | Required elements |

|---|---|

| Define the claim map | true-case test; false-case test; 'must not disclose' field list; owner for proof creation, proof checking, and the final policy decision |

| Document proof choice and rollback | selected proof system; performance-versus-trust tradeoff; who approved it; rollback trigger tied to observed production symptoms; issuer support for the credential flow |

| Approve a minimal evidence model with compliance | claim ID; proof result; policy decision; timestamps; case owner; external verification reference when used |

| Test replay, failure handling, and operator ownership | replay the same verification request; consistent decision path; failover drills; documented fallback behavior; manual-review ownership; track your own latency budget; identity assertions below 150ms in the cited zk-creds implementation |

| Validate audit-trail reconstruction | request received; proof checked; policy decision made; action allowed or blocked; references rather than raw sensitive fields |

- Define the claim map. Write each claim so the Prover can assert it and the receiving system can validate it without raw records. For each claim, include a true-case test, a false-case test, a "must not disclose" field list, and the owner for proof creation, proof checking, and the final policy decision.

- Document proof choice and rollback. Record why this scope uses the selected proof system, the performance-versus-trust tradeoff you accepted, and who approved it. Add a rollback trigger tied to observed production symptoms, for example proof-check instability, latency regression, or missing decision evidence, and confirm issuer support for the credential flow.

- Approve a minimal evidence model with compliance. Get written sign-off for the retained evidence model through legal/compliance review for the jurisdictions and programs you operate in. Keep evidence narrow: claim ID, proof result, policy decision, timestamps, case owner, and external verification reference when used.

- Test replay, failure handling, and operator ownership. In staging, replay the same verification request and confirm a consistent decision path. Run failover drills that break proof-check dependencies and confirm documented fallback behavior and manual-review ownership. Track your own latency budget. The cited zk-creds implementation reports identity assertions below 150ms.

- Validate audit-trail reconstruction. Reconstruct one completed request end to end: request received, proof checked, policy decision made, action allowed or blocked. The trail should use references rather than raw sensitive fields, including a transparency-log or equivalent credential pointer when your design uses one.

When your checklist is stable, map each checkpoint to concrete API and webhook tasks in the Gruv docs.

The practical next move for platform teams#

A low-risk first move is narrow and testable. Choose one verification claim that currently causes repeated data exposure, and prove that claim with less disclosure while keeping your existing policy gates intact. If policy ownership or compliance scope is still unclear, pause expansion.

Choose one claim that already hurts operations#

Start with a claim your team already checks often, not a broad goal like "privacy-first onboarding." Pick a narrow identity or eligibility assertion near existing controls. The Prover should submit a proof, and the checking service should return pass or fail without moving the full underlying record.

Anchor the pilot to checkpoints you already run, such as identity verification, beneficial ownership checks, or ongoing transaction monitoring. The pilot should reduce repeated raw-data sharing inside an approved path, not create a parallel compliance path. Checkpoint: write the claim in one sentence, then write a matching "do not disclose" sentence.

Define one measurable privacy objective#

Set one objective tied to exposure reduction, not a generic privacy goal. For example, define where sensitive onboarding artifacts should stop moving beyond the part of your identity-verification infrastructure that actually needs them.

This matters because broad collection and weak governance can create a data honeypot. A documented failure mode is copying familiar KYC handling patterns without equivalent governance for document collection, due diligence, and records retention. That can reduce perceived regulatory risk while increasing operational risk. Checkpoint: review one current payload, one log, and one support view, and confirm which sensitive fields must disappear in the pilot.

Keep policy gates and failure handling explicit#

Do not treat proofs as replacements for required controls. Keep existing KYC and AML policy gates authoritative, and use proofs to reduce unnecessary disclosure around those gates.

Make failure behavior explicit. Decide who owns timeouts, who can retry safely, and what operator-visible audit trail remains. If teams cannot explain decisions without reopening raw identity artifacts, the design is not ready. Checkpoint: run one tabletop failure case and document ownership, retry behavior, and dispute evidence.

Pause expansion until boundaries are proven#

A pilot win is enough. Do not expand proof surfaces until coverage, governance, and operator burden are clear. Under regulatory pressure, teams can default to collection-first infrastructure decisions. Avoid repeating that pattern by scaling before the boundaries are proven.

Use a short evidence pack before any expansion: claim definition, prohibited fields, gate owner, failure path, and one audit-log example. Then decide whether to keep scope narrow, expand, or roll back.

If you want a second pass on rollout scope, policy gates, and payout controls before build, talk with Gruv.

Frequently Asked Questions

What is a ZKP in payment verification, in plain terms?

A Zero-Knowledge Proof lets a prover show that a claim is true without revealing the underlying data. In payment verification, the receiving system gets the check outcome, often a yes or no result, instead of the full record. One example in this material is proving someone is over 18 without revealing the birthdate.

How is ZKP verification different from traditional raw-data checks?

Traditional raw-data checks can move sensitive data across more systems and parties. Proof-based verification is meant to confirm the claim while withholding personal attributes. The practical difference is data minimization: verify what matters without turning each check into a raw-data transfer.

When should a platform choose zk-SNARKs instead of zk-STARKs?

This material does not support a blanket rule for choosing zk-SNARKs over zk-STARKs. The choice should be based on the specific claim, proof size, verification speed, trust assumptions, and implementation complexity in your environment. If you cannot justify the proof family for the actual production scope, defer.

Can ZKPs help with regulatory verification under GDPR, CCPA, or MiCA-related controls?

ZKPs can help reduce unnecessary data sharing, which aligns with data-minimization goals. But this material does not support claiming that proofs alone satisfy GDPR, CCPA, or MiCA-related obligations. Use them as one control in a broader compliance design.

Where should ZKP checks sit in onboarding, authorization, and payout flows?

There is no single correct placement across onboarding, authorization, and payout flows in this material. Put checks where they reduce repeated raw-data sharing and where the downstream service only needs an accept-or-reject result. Do not treat them as a replacement for KYC or AML policy gates.

What are the biggest production risks when shipping ZKPs in a payment platform?

One major risk is reducing disclosure in the proof flow while reintroducing exposure through logs, payloads, alerts, or support tickets. Another is underestimating proving cost, deployment complexity, and reliability demands under real payment load. Teams also need explicit failure handling, idempotent retries, and rollback paths.

Do ZKPs replace KYC and AML checks?

No. This material does not support the claim that ZKPs replace KYC or AML controls. Keep those decisions authoritative and use proofs for narrow checks that reduce unnecessary disclosure.

Ethan covers payment processing, merchant accounts, and dispute-proof workflows that protect revenue without creating compliance risk.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- cs.purdue.edu/homes/clg/files/zk-creds.pdftrusted

- en.wikipedia.org/wiki/Zero-knowledge_prooftrusted

- imf.org/-/media/files/publications/ftn063/2025/engli...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC10764853trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC10366433trusted

- pnnl.gov/main/publications/external/technical_reports...trusted

- www2.eecs.berkeley.edu/Pubs/TechRpts/2025/EECS-2025-20.pdftrusted

- arxiv.org/html/2502.18535v2external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade:

Spain Digital Nomad Visa Guide: Requirements, Application & 2026 Updates

Stop collecting more PDFs. The lower-risk move is to lock your route, keep one control sheet, validate each evidence lane in order, and finish with a strict consistency check. If you cannot explain your file on one page, the pack is still too loose.