Quick Answer

Build the policy from operations first: create one table for onboarding, payment collection, payout, and support, then attach owner, market signal, and execution evidence to each statement you plan to publish. Keep unresolved GDPR or CCPA/CPRA trigger rows marked `counsel required`, and do not ship those claims yet. Release only after the notice text, user-facing request paths, and backend status handling all match documented behavior.

What a Platform Privacy Policy Needs to Cover#

Some teams keep GDPR and California's CCPA/CPRA payment-data disclosures in one policy framework, but that alone does not guarantee compliance; the policy still has to match how your teams actually process data and handle rights in practice. Treat the policy as an operating document, not a legal summary.

That matters because the two regimes differ in scope and mechanics. GDPR can apply to organizations outside the EU when they target or collect data related to people in the EU. CCPA/CPRA applies to residents of that state and their personal data. The requirements also differ materially, including a commonly described opt-in model under GDPR and opt-out treatment for certain sales or sharing contexts under CCPA/CPRA.

Before you start, have these inputs ready before you draft or revise:

- a current map of payment-related data flows by product and market

- your live privacy policy text and notices used in payment journeys

- your current rights-request process, including ownership and closure steps

Use one checkpoint for every planned policy statement about collection, use, access, deletion, or opt-out. Confirm who executes it and what record shows it happened.

This guide is for compliance, legal, finance, and risk owners who need operational clarity. The sequence is practical. Define where GDPR and CCPA/CPRA may apply, align disclosures and rights handling, assign decision owners, verify implementation before publish, and escalate unclear points to specialist counsel instead of guessing.

That discipline matters. Poor multi-region privacy execution can lead to fines, trust damage, and operational disruption. Under GDPR, administrative fines can reach up to EUR20 million or 4% of annual global turnover. Enforcement can also include orders to stop processing or to delete or restrict data. Under CCPA/CPRA, required privacy-policy disclosures and rights-request handling have to work in operations, not just on the page.

We covered the website-policy side of this in detail in How to Create a GDPR-Compliant Privacy Policy for Your Website.

Gather inputs before drafting policy language#

Start with evidence, not wording. Without a clear picture of how your payment flows, tax registrations, and support operations actually run, policy text will drift away from operational reality.

| Evidence item | Key detail |

|---|---|

| Live policy text and notice variants | Used in checkout, payout, and support |

| Entity and market mapping | For each flow |

| OSS registration details | Member State of identification |

| OSS return operations | Which supplies are reported under the selected scheme |

Build a flow inventory by product and market. Map payment journeys separately for EU residents and residents of each relevant Member State. Use real flows, not generic labels: onboarding, payment collection, payout, refund, chargeback, and support. For each flow, record the product, market, legal entity, data captured, where it is stored, and which vendors or internal teams handle it.

Also flag where your platform may be treated as a marketplace for VAT purposes. Include cases where it is a deemed supplier and where record-keeping still applies. EU cross-border B2C e-commerce VAT rules changed on 1 July 2021 and affect marketplaces and platforms across the supply chain, so do not stop the inventory at the UI layer.

Collect the records your draft will rely on. Pull the current public policy text, in-product notices, and internal records already used in payment journeys. The goal is operational proof. Every planned policy statement should have an owner, an execution path, and a record.

A practical evidence pack usually includes the items below. If a statement has no underlying record, flag the gap before drafting.

- live policy text and notice variants used in checkout, payout, and support

- entity and market mapping for each flow

- OSS registration details for the Member State of identification

- OSS return operations showing which supplies are reported under the selected scheme

Confirm cross-border constraints before you write. Before you write policy language, check whether current VAT choices already constrain routing or ownership. If you use OSS, a taxable person registers in one Member State of identification and must declare all supplies under that scheme through OSS returns. Filing cadence is quarterly for Union and non-Union schemes, and monthly for the import scheme.

For complex cross-border transactions, confirm whether a VAT cross-border ruling (CBR) request is appropriate in the participating EU country where the taxable person is VAT-registered. In some Union-scheme cases, changing the Member State of identification is restricted and can create a lock-in through the current calendar year plus the next two calendar years.

Those choices can shape how you document cross-border flows. If operational constraints are unclear, escalate instead of drafting from assumptions. For related operating context, see A Guide to Data Localization Laws for Global Freelancers.

Step 1 map jurisdictions and legal triggers#

Do not start with one global rule. Build a jurisdiction matrix that separates verified market evidence from unproven privacy-law triggers.

Build the matrix from verified market evidence. Use one row per flow and user type. At minimum, include flow name, user type, operating entity, market signal, source record, and status (in scope, out of scope, counsel required).

Start by separating proven EU commercial footprint from privacy applicability. EU VAT signals such as OSS use, Member State of identification, deemed supplier analysis, marketplace record-keeping duties, the 1 July 2021 rule change, and the EUR 10 000 threshold show EU market touchpoints. They do not establish GDPR scope by themselves.

| Matrix row | Evidence you can verify now | What you can mark confidently | What must stay open |

|---|---|---|---|

| EU cross-border payment or payout flow | OSS registration, Member State of identification, deemed supplier analysis, marketplace record-keeping duty | EU market touchpoint exists | GDPR trigger analysis needs a separate legal source or counsel note |

| State payment, refund, or support flow | Internal market mapping, contract/entity mapping, prior counsel memo if one exists | Operational touchpoint may exist | Confirm CCPA/CPRA applicability with legal counsel |

| Mixed or unclear flow | Conflicting location data, unresolved entity owner, unclear routing/storage | Unknown | Mark counsel required before drafting policy text |

When you use EU public materials, confirm they are on the europa.eu domain. For VAT Cross-border Ruling requests, note the participating EU country where the taxable person is VAT-registered.

Split in-scope people by user type and flow. Broad labels like "users" are too loose for this step. Split rows by role in your product: payer, payee, seller, contractor, creator, and support requester where applicable.

For each row, record the exact market signal you used, for example billing country, payout country, account profile, or contracting entity. Do not treat one location field as universal across all flows.

Use the matrix as a drafting gate, not a legal conclusion. GDPR extraterritoriality criteria and CCPA/CPRA thresholds require legal review. Use the matrix as a drafting gate only.

If a flow is already confirmed by counsel or an existing memo as in GDPR scope, keep a separate GDPR review track before you draft policy language. If a flow is confirmed as in CCPA/CPRA scope, keep a separate CCPA/CPRA review track. Keep privacy-law controls out of generic global text unless they are backed by a separate legal source or counsel note. For mixed flows, keep both tracks visible in the same row.

Mark unknowns as counsel required. If you cannot point to a trigger memo, statute analysis, or documented jurisdiction decision, do not draft policy language for that row. Mark it counsel required.

A common failure mode is filling legal-trigger gaps with polished prose. Keep an evidence pack per row with source record, owner, review date, and unresolved question. Then escalate rows that still need specialist review.

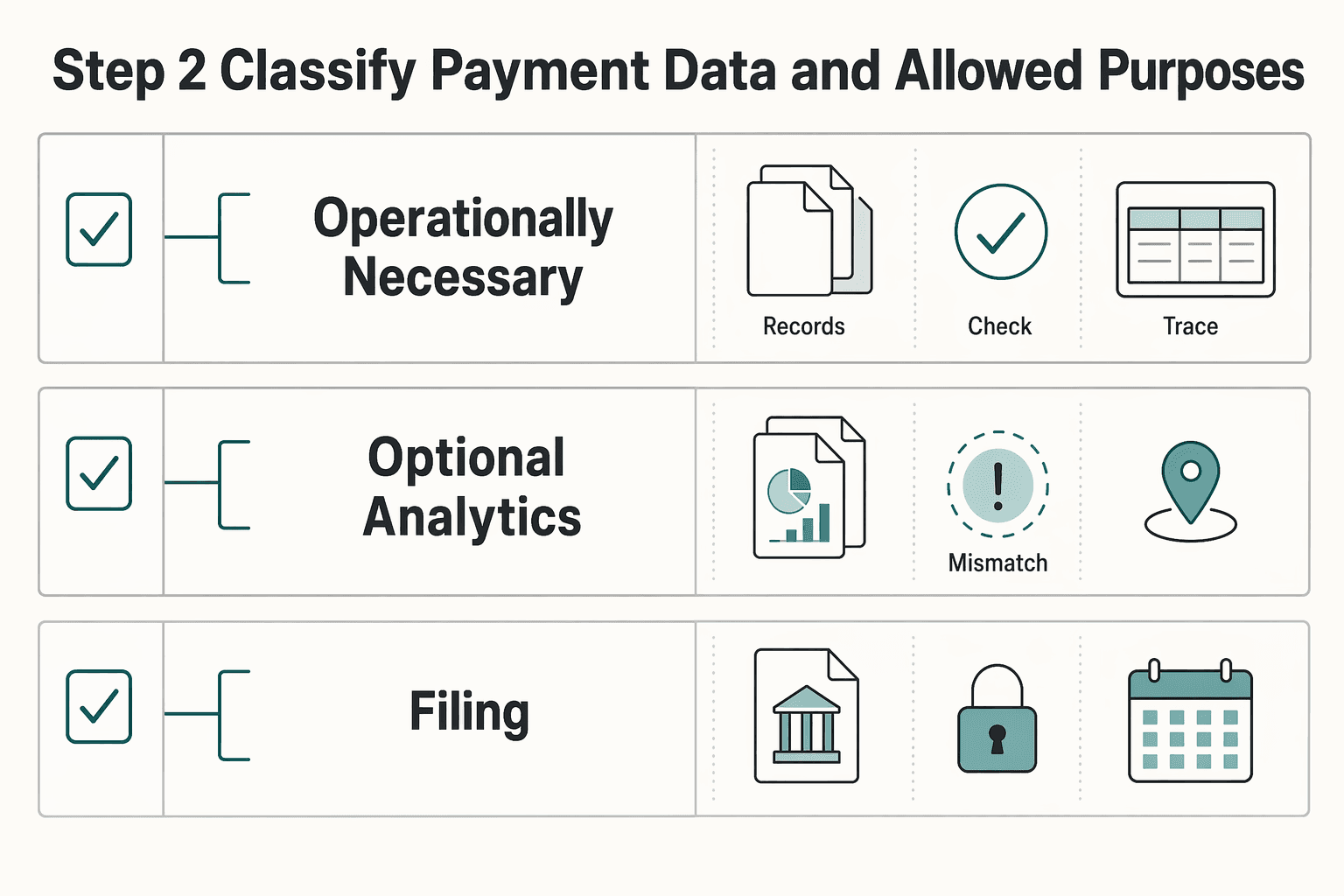

Step 2 classify payment data and allowed purposes#

Once scope is confirmed, classify payment-related personal data by processing purpose before you draft notice text. Use a hard gate: if you cannot state the purpose, record it, and document the legal basis for GDPR rows, do not ship the field or event.

Group by use, not by storage location. Start with why the data is processed, not where it sits. Purpose limitation means personal data should be tied to a particular, explicitly stated purpose, and that purpose should be recorded. Keep the same internal purpose groups for CCPA/CPRA rows so disclosures reflect actual use, not a catch-all label.

| Purpose group | What belongs here | What you must record | Policy match check |

|---|---|---|---|

| Operationally necessary processing | Data used to complete payment transactions and related support | Specific purpose statement, affected user type, jurisdiction row, documented legal basis for GDPR rows | Public policy text should describe this use, and system behavior should stay within it |

| Optional analytics on payment journeys | Events or fields used to measure drop-off, diagnose behavior, or improve conversion | Separate purpose record from core processing, owner, review date | If notice says optional, the product should be able to stop it without breaking core payment execution |

| Marketing or profiling based on payment behavior | Reuse of payment-related data for campaigns, segmentation, or promotional messaging | Separate purpose record, approval note, consent assessment where relevant | If purpose changed from operations to marketing, reassess consent and disclosures before reuse |

Broad "payments" buckets are convenient internally, but they are also where policy language and real processing can drift apart.

Separate necessary processing from optional use. Keep operationally necessary processing separate from optional analytics or marketing. If they share one purpose line, consent decisions are harder to justify and user explanations get muddy.

For GDPR rows, attach legal basis to each purpose record. For CCPA/CPRA rows, map the disclosure description to that same record. Use one classification structure with jurisdiction-specific outputs. If purpose changes, obtain new consent when your approach depends on consent. Do not treat that as an informal ticket note.

Add a no purpose, no processing gate. Make "no purpose, no processing" a release gate for new payment-flow fields, events, or vendor routes. Require this evidence pack before launch:

- field or event name

- stated purpose

- affected flow and user type

- legal basis record for GDPR rows

- exact policy or notice line describing the use

Then verify behavior in product, not just in documents. Every new field or event must trace to a declared purpose in your inventory. If it cannot, stop release.

A common failure mode is policy text that stops at transaction processing while product behavior also routes payment-journey data into analytics or marketing. That mismatch can increase compliance risk and weaken disclosure quality. For a step-by-step walkthrough, see How to Set Up a Multi-Entity Payment Structure for Global Platform Operations.

Step 3 decide consent opt-out and legal basis by flow#

Do not finalize consent, opt-out, or legal-basis decisions from the current evidence alone. The materials here support VAT OSS and CBR mechanics. They do not support GDPR legal-basis assignment, CCPA/CPRA opt-out mechanics, or mixed-jurisdiction privacy conflict rules.

Build the flow table now for onboarding, payment collection, payout, and support, and mark these privacy fields as unverified until jurisdiction-specific privacy sources confirm them. Keep unresolved privacy fields as pending decisions before release.

| Flow | GDPR legal basis | Explicit consent path | CCPA/CPRA opt-out path | Release status |

|---|---|---|---|---|

| Onboarding | Unverified | Unverified | Unverified | Pending verification |

| Payment collection | Unverified | Unverified | Unverified | Pending verification |

| Payout | Unverified | Unverified | Unverified | Pending verification |

| Support | Unverified | Unverified | Unverified | Pending verification |

Once those fields are verified, keep policy language, UI notices, and backend behavior aligned to the same per-flow decisions.

Step 4 operationalize data subject rights from intake to closure#

At this point, the priority shifts from drafting to execution. Build the operating path now, and keep legal interpretation unverified until privacy counsel confirms jurisdiction-specific rules. The goal is simple: every request is owned, traceable, and reviewable from intake through closure.

1. Build the rights matrix before execution rules. Create one matrix for counsel-defined request categories, and keep legal labels unverified until counsel confirms them.

Capture operating fields, not legal conclusions: request label, intake channels, systems touched, owner, legal-rule status, evidence location, and escalation path.

| Request type | Intake owner | Systems touched | Legal rule status | Evidence logged before closure | Escalation path |

|---|---|---|---|---|---|

| Counsel-defined category A | Privacy or support ops | Internal systems and relevant vendors in scope | Unverified | Intake record, handling notes, execution timestamp, closure notice | Legal review queue when interpretation is unresolved |

| Counsel-defined category B | Privacy or support ops | Internal systems and relevant vendors in scope | Unverified | Intake record, handling notes, execution timestamp, closure notice | Legal review queue when interpretation is unresolved |

| Counsel-defined category C | Privacy or support ops | Internal systems and relevant vendors in scope | Unverified | Intake record, handling notes, execution timestamp, closure notice | Legal review queue when interpretation is unresolved |

2. Add a triage gate for requests that need legal interpretation. Do not auto-close requests when legal interpretation is unresolved. Route them to legal review before operational action.

Use a fixed triage flow:

- Log at intake.

- Map the request to a counsel-defined category.

- Freeze automated closure when legal interpretation is unresolved.

- Record the legal instruction in the case file before execution.

- Resume execution after instruction is documented.

3. Standardize the evidence pack for every request. Define one internal evidence pack and keep it consistent across tools and owners so case handling stays traceable and reviewable.

Keep the distinction clear. OSS materials support record-keeping discipline and audit readiness, including recurring return checkpoints and documented participation-state changes (for example, voluntary leave or exclusion). They do not define GDPR or CCPA rights-handling rules. Use them as an operational model for traceability, not as a substitute for privacy-law requirements.

4. Add closure checkpoints across all relevant systems. Do not close a request on operator assertion alone. Close only when traceable proof exists across each internal system and each relevant vendor involved in the case.

Use this checkpoint list before closure:

- request is mapped to a counsel-defined matrix row

- legal-instruction status is documented

- decision rationale is explicit in the case file

- each touched system has an execution record or a documented no-action note

- closure notice matches the executed actions

If legal interpretation remains unresolved, keep the case open, preserve collected evidence, and avoid improvised case-by-case decisions.

Step 5 set retention deletion and localization guardrails#

This is where many policies get vague. Set explicit, operational rules for retention, deletion, and localization so the section does more than promise data is kept "as needed." Use one controlled schedule by data category, purpose, and legal-basis status. Then tie each rule to a real execution path.

| Case outcome | What to record |

|---|---|

| Deleted from relevant live systems | Record that outcome in the case file |

| Anonymized or de-identified | Record that it is the approved path; if anonymization is used, document why, what was transformed, and what downstream copies still exist |

| Retained under a documented exception | Record the reason and approver |

Tie retention to purpose and legal basis. Use the same category labels already disclosed in your notice. If you list Payment Information, keep that exact label in the retention schedule and map it across all covered surfaces, including websites, mobile applications, and physical or kiosk-based collection points.

For each category, document: purpose, legal-basis status, retention trigger, deletion or anonymization path, and exception or escalation notes. If purpose or legal-basis status is unresolved, avoid broad retention promises for that category.

Define deletion and anonymization triggers. Use observable triggers, not vague language. For example: a documented lifecycle trigger plus confirmation that no retention reason remains, except where an approved legal or operational hold applies.

For rights requests where applicable (including Right to Delete and Right to Erasure), record one of three outcomes in the case file:

- deleted from relevant live systems

- anonymized or de-identified where that is the approved path

- retained under a documented exception with reason and approver

If anonymization is used, document why, what was transformed, and what downstream copies still exist.

Document transfer and localization constraints. State clearly where transfer or storage handling is jurisdiction-conditional. Use the same conditional logic you already apply for regional rights handling, such as when EU, UK, or Swiss law applies.

Keep each rule specific to the flow: market, vendor, constraint, and exception owner. For a deeper operating checklist, use Cross-Border Payment Compliance: GDPR CCPA and Data Localization Requirements.

Review and version the schedule on a recurring checkpoint. Review this schedule whenever payment-data processing changes, including product, market, or vendor changes. Confirm that categories, purposes, triggers, and transfer notes still match real operations.

Track an explicit Effective Date for both the notice and the retention schedule version. Dates such as "effective as of March 31, 2024" and "Effective Date: December 18, 2025" make it clear which policy version was active at the time of a request or review.

Step 6 assign owners approvals and escalation points#

Do not implement OSS or CBR process changes without clear ownership, explicit approvals, and a written escalation path. For each material change, set one accountable owner, one approver, and an evidence pack tied to the effective date.

| Escalation trigger | What to check |

|---|---|

| Unclear OSS special scheme | Which scheme applies: non-Union, Union, or import |

| Missing OSS filing coverage | Whether all supplies in the chosen OSS scheme are included in the OSS return |

| CBR alignment issue | Whether the request can be aligned with national VAT ruling conditions in the filing country |

| Member State of identification change | Whether a lock-in may apply for the current calendar year plus the next two calendar years |

| Deregistration or exclusion risk | Whether a participant is preparing to deregister or has been notified of possible exclusion from a scheme |

Name one accountable owner for each decision type. Assign owners by decision type, not by title. For example: one owner for OSS opt-in decisions (the schemes are optional), one for Member State of identification decisions, one for return filing operations, and one for record-keeping and audit readiness. For CBR requests involving multiple companies, name one filing entity to submit on behalf of the others.

Keep accountability single-threaded: one person carries the change through review, gathers evidence, and closes comments, even when multiple teams are involved. For each change, you should be able to identify one owner, one approver, the effective date, and the supporting evidence.

Define escalation triggers before conflicts happen. Write escalation triggers in advance so conflicts do not get handled ad hoc. Trigger escalation when evidence is conflicting, scope is unclear, or the same operational failure repeats.

Escalate when any of these occur:

- it is unclear which OSS special scheme applies (non-Union, Union, or import)

- the filing team cannot show that all supplies in the chosen OSS scheme are included in the OSS return

- a CBR request cannot be aligned with national VAT ruling conditions in the filing country

- a request to change the Member State of identification when a lock-in may apply (calendar year plus two following years)

- a participant is preparing to deregister or has been notified of possible exclusion from a scheme

Set a fixed reporting cadence for open issues. Use a fixed reporting rhythm for open OSS and CBR issues, unresolved scope questions, and pending approvals. Choose a cadence your team can sustain, and keep it consistent.

When possible, align reporting checkpoints with scheme operations: quarterly for non-Union and Union returns, and monthly for import returns. The goal is early visibility and checkpoint discipline, not reactive cleanup.

Add a release gate for process updates. Treat OSS/CBR process publication as a gated release, not a drafting milestone. Publish only after the designated approver confirms execution evidence.

Require evidence, not verbal confirmation. At minimum, include scheme choice, Member State of identification, filing cadence, record-keeping and audit checkpoints, and any CBR ownership or filing conditions, plus the exact effective date for the published version. Before final sign-off, align policy gates, payout controls, and audit-trace expectations with your operating model.

Step 7 publish policy notices and verify implementation#

By this stage, publication should be the last step, not the first visible one. Publish only when each notice claim matches a control your team can show in production. If a statement cannot be tied to a working intake path, process, or record, remove it or delay release.

Map each notice section to an operating control. Map the policy text line by line to evidence from Step 6, with extra scrutiny on rights handling and required notices. For CCPA/CPRA language, verify both sides are real: the notice content and the request-handling process behind it.

Do not claim outcomes you cannot execute. In particular, do not describe deletion as unconditional when exceptions apply.

Test the public request channels before release. Test request channels the way a user would use them, including every path you publish, for example web form and email. Confirm each path is live and reaches the team and workflow that handle privacy requests.

Run sample requests for the rights you state in the notice, including Right to Know and Right to Opt-Out. If you claim non-discrimination for exercising rights, confirm that behavior in practice.

Run a post-publish contradiction check. After publishing, compare live behavior to notice language in impacted jurisdictions. Treat any mismatch between public text and actual handling as a release defect.

Keep a short verification record with the published version date, tested channels, sample request records, jurisdiction tested, and any open exceptions.

Common mistakes that create regulatory surprises and how to recover#

Many regulatory surprises come from one gap: the policy sounds global, but operations are local, partial, or undocumented. Once you reach this stage, remove any claim you cannot tie to a jurisdiction-specific rule, a live process, and a record you can produce.

Remove generic law summaries that are not tied to a real payment journey. A generic GDPR-versus-CCPA summary is not operational policy text. Rewrite the section by payment journey, such as onboarding, collection, payout, support, and tax, and keep only statements mapped to a control owner, system action, and retained evidence.

Use extra caution with terms like legal basis, purpose limitation, Right to Opt-Out, Right to Delete, and Right to Erasure. The grounding for this section does not establish those detailed requirements, so route them to jurisdiction-specific legal review instead of presenting them as settled operating facts.

A practical checkpoint can be one evidence pack per journey: user path, owner, notice text, and one production record. If you cannot assemble that quickly, the text is probably ahead of operations.

Split jurisdiction logic before you promise one global rule. Avoid treating EU and California users as one operational audience. Even with one public notice, your internal decision logic should be split by regime and tested separately.

Use the same discipline for EU indirect tax handling. Since 1 July 2021, EU VAT rules for cross-border B2C e-commerce changed, and eligible sellers, including marketplaces and platforms, can register in one Member State for OSS declaration and payment. OSS is optional, but if you opt in, you must declare all supplies that fall under the chosen scheme via the OSS return.

The recovery pattern is straightforward: split the logic, then retest each branch. Confirm which flows are in scope, confirm your Member State of identification, and confirm records match the reporting path you actually use.

Pause deletion-style claims until you have auditable closure proof. Do not promise deletion or erasure outcomes you cannot prove end to end. The grounding here does not establish detailed Right to Delete or Right to Erasure requirements, so keep claims narrow until evidence is in place.

Use auditable closure proof, not narrative status updates. For payment operations, that can include a case record, systems checked, execution timestamp, exceptions, and retained proof of completion or lawful limitation. If policy language promises broad completion but records are only inbox threads, treat that as a release defect.

Escalate market-specific transfer or localization ambiguity instead of guessing. If localization or transfer obligations are unclear, escalate instead of drafting a generic global sentence. The provided sources do not establish privacy-law localization duties for payment personal data, so do not state them as confirmed requirements here.

You can still document market-specific handling decisions already grounded in cross-border VAT operations:

| Decision point | What to verify | Failure mode |

|---|---|---|

| OSS registration | Registration in one single Member State as Member State of identification | Wrong assumptions about reporting jurisdiction |

| OSS filing scope | Inclusion of all supplies that fall under the chosen OSS scheme | Underreporting after opting in |

| Complex cross-border VAT treatment | Whether to submit a VAT Cross-border Rulings request in the participating EU country of VAT registration | Ad hoc treatment of ambiguous transactions |

If you use OSS, also verify filing cadence: quarterly for Union and non-Union schemes, monthly for import. Record-keeping and audits are part of OSS operations, and exclusion by a Member State is an explicit failure mode. For unresolved market questions, escalate to counsel or tax specialists.

Copy and paste launch checklist for your next policy update#

Use this as the final publish gate. If a policy statement cannot be tied to a live control, evidence, and owner, mark it counsel required or remove it. EU VAT process checkpoints are well-documented; privacy-law specifics should be treated as counsel required unless validated separately.

| Step | Confirm | Evidence to attach before publish | Red flag |

|---|---|---|---|

| Step 1 | Keep scope logic explicit for your EU VAT setup (including One Stop Shop (OSS) scheme and Member State of identification). Leave unresolved privacy-jurisdiction scope questions explicit as counsel required. | Scope matrix by product flow and audience, plus an owner for each open issue. If you mention EU VAT handling, include your OSS scheme and Member State of identification. | One global sentence that implies universal coverage, or treating EUR 10 000 as a privacy threshold. |

| Step 2 | For each policy statement you name, confirm you can show the live control, usage, and owner behind it. If legal-basis language appears, mark it counsel required unless separately validated. | Processing inventory entry, internal basis note (if used), and matching product flow or field list. | The policy names a purpose that product, support, or finance cannot prove in the live flow. |

| Step 3 | If you state user notice or choice controls, confirm those controls are implemented where stated. Test both user path and backend status change. | Screenshot of notice or choice point, test result, and sample audit record showing status written correctly. | Public text promises a control, but UI, storage, or downstream propagation is missing. |

| Step 4 | For every user-rights workflow you name, confirm operational handling exists, or mark it counsel required until validated. | One completed test case with intake record, identity-validation outcome, decision rationale, execution timestamp, and closure notice. | A listed workflow has no demonstrable intake, verification, execution, or documentation path. |

| Step 5 | Confirm retention, deletion, and any storage or transfer constraints you already operate are documented and executable. | Retention schedule, deletion trigger, exception path, and market-specific storage or routing note. If EU tax statements appear, confirm OSS cadence is quarterly (Union/non-Union) or monthly (import), and that OSS returns are additional to domestic VAT returns. | "Kept as needed" language without an executable schedule, or privacy text that drifts into tax claims not matched by filing practice. |

| Step 6 | Assign approvals, escalation triggers, and reporting owners before publish. Keep release approval evidence-based, not editorial-only. | Named approvers across legal, compliance, finance, and risk, plus publish decision record and open-issue list. | Legal signs off on wording, but operations cannot sign off on execution proof. |

Cross-border EU VAT process detail is well-documented; privacy-law detail requires separate validation. If your notice references OSS, verify the exact scheme, your Member State of identification, and whether that choice can bind you for the current calendar year plus two following years. If your platform could be a deemed supplier for VAT purposes, have tax validate wording before publication.

For unusual cross-border VAT treatment, do not infer in privacy text. Escalate to tax on whether a VAT Cross-border Rulings (CBR) request is appropriate, and follow national VAT ruling conditions in the filing country. Treat that as a VAT escalation path, not a privacy review substitute.

Final gate: every checked line must point to proof. If proof is missing, remove the statement or hold release. For California-specific implementation details, see CCPA for Platform Operators: How to Handle Contractor Financial Data Under California Law.

If you still have mixed-jurisdiction edge cases before publishing, contact Gruv to validate rollout assumptions and escalation paths.

Frequently Asked Questions

What is the practical difference between GDPR and CCPA/CPRA for a payment platform privacy policy?

Keep separate EU and state operating logic, then have counsel confirm privacy-law differences before you describe them publicly. Also keep VAT and privacy analysis separate, because OSS is a VAT declaration-and-payment path, not a privacy-law substitute.

What minimum sections must one policy include for EU residents and California residents?

These sources do not provide a verified minimum section list for EU or state privacy notices. Use your internal draft structure as a working checklist, then validate each section against your live process and records before publication. For EU payment operations, confirm that any VAT language is consistent with your OSS setup, Member State of identification, and actual record-keeping.

When do CCPA and CPRA obligations likely apply to a platform business operating in California?

Treat state applicability as a legal-review question, especially for multi-entity or cross-border operating models. Keep it separate from EU VAT scope, because OSS registration in one Member State addresses VAT declaration and payment, not state privacy applicability.

How should one policy handle both explicit consent requirements and Right to Opt-Out requirements?

Keep public language limited to controls you have actually implemented, and escalate unresolved cross-jurisdiction conflicts to counsel before release. Verify that notice text, UI choice points, and backend status handling match the promise, and treat unknowns as release blockers.

Which data subject rights should teams operationalize first if resources are limited?

The provided material does not rank data subject rights or define a supported priority order under GDPR, CCPA, or CPRA. Prioritize requests you already describe publicly and can close with system-level proof. Keep auditable records for intake, identity validation, decision rationale, execution timing, and closure.

What are the biggest unknowns in public explainers that require legal review before publication?

The biggest unknowns are the same ones these sources do not support: GDPR versus CCPA/CPRA differences, required policy sections, state applicability tests, consent-versus-opt-out conflict handling, and rights prioritization. Another risk is privacy text that drifts into VAT claims without matching operations. If you reference OSS, verify scheme choice (non-Union, Union, or import), Member State of identification, supply coverage in OSS returns, and filing cadence (quarterly for Union and non-Union, monthly for import). For complex cross-border VAT treatment, evaluate whether a VAT Cross-border Rulings request is needed under national VAT-ruling conditions, and account for possible Member State exclusion from OSS.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/crs-product/R45631trusted

- cppa.ca.gov/regulations/pdf/ccpa_updates_all_written_com...trusted

- cppa.ca.gov/meetings/materials/20230203_item4_fsor_appen...trusted

- eit.europa.eu/sites/default/files/eit-digital-data-soverei...trusted

- lawreview.gmu.edu/print__issues/the-antitrust-and-privacy-inte...trusted

- oag.ca.gov/privacy/ccpatrusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Cross-Border Payment Compliance: GDPR CCPA and Data Localization Requirements

Cross-border payment compliance is two linked jobs, not one checklist: privacy-transfer compliance and payment-control compliance. In the same payout flow, you may need to manage cross-border personal data transfer obligations under GDPR and separate privacy obligations under CCPA. You may also need to run KYC and AML controls that can affect onboarding, payment release, holds, and escalation.

Create a Privacy Policy for SaaS That Matches Real Operations

For the founder of a Business-of-One, the privacy policy often feels like a legal chore, something to check off with a generic template and forget. That is the wrong way to treat it. In SaaS, your policy is one of the first public proofs of how you actually handle customer data.

Data Localization Laws for Global Freelancers Before You Sign

You can work within **data localization laws** without stalling a cross-border deal, but only if you scope data location before price and timelines are set. For freelancers, the goal is simple: make assumptions explicit, tie them to contract language, and update them when facts change.