Quick Answer

Yes. Positive Pay reduces check and ACH exposure when you treat it as an operating control, not just a bank feature. For checks, it depends on accurate issued-check data; for ACH, it depends on well-scoped Originator ID and transaction filters. The deciding factor is exception handling: each exception item needs a permissioned owner, a pay-or-return action, and a timestamp before cutoff. Without that governance layer, alerting alone will not produce a defensible result.

How Positive Pay helps prevent check fraud and unauthorized ACH debits#

Positive Pay works best when you treat it as a control process, not a feature you turn on in a bank portal. For platform teams, the real question is not "do we have it?" It is "can we show who reviewed each exception, who approved or rejected it, and whether that happened before cutoff?"

-

Two-rail coverage. Positive Pay applies to both check and ACH payment streams, and that split matters in day-to-day operations. Check Positive Pay addresses check risk. ACH Positive Pay adds a control layer that restricts which ACH transactions can post to your accounts. If your platform issues checks and also carries ACH debit exposure, covering only one rail can leave a gap.

-

Exception decisions are the real control. The value of Positive Pay shows up in exception handling, because flagged payments still need a business decision. In practice, potentially fraudulent payments are identified so businesses can approve or reject them, and pending exceptions are tied to cutoff notifications. What matters most is not alert volume but timing. If you cannot name the decision owner for every exception before the bank's deadline, you do not yet have a setup that is likely to hold up in production.

A good checkpoint is simple: pull one day of exceptions and verify that each item has an owner, a pay or return decision, and a timestamp another reviewer could follow later. One failure mode is an unowned queue. Once items sit unresolved near cutoff, teams start rushing decisions or chasing approvals in chat and email. That weakens both the control and the record.

- Governance matters as much as configuration. This article is written for compliance, legal, finance, and risk owners because Positive Pay decisions may become reviewable records, not just treasury operations. That framing matters. The ICBA's October 2025 guide presents Positive Pay through a checklist of operational considerations, and it also explicitly warns that such materials should not be taken as legal advice.

What matters here is defensibility. Your setup should leave an audit trail that shows what was flagged, who decided, when they decided, and what support they reviewed.

The goal is practical: reduce check fraud and unauthorized ACH debit exposure with controls that can stand up under review. In practice, that means clear ownership, enforceable decision timing, and records you can export without reconstructing events by hand. Just do not assume one bank program's rules, cutoffs, or approval expectations carry over to another.

For a step-by-step walkthrough, see How Platforms Stop Affiliate Fraud Before Commissions Are Paid.

How to choose a Positive Pay setup for your platform#

Choose for evidence, not feature count. If your team runs multi-entity payouts with recurring ACH debit exposure and check issuance risk, use a setup where a user with real account decision authority can decide each exception before cutoff. If you cannot prove who approved or returned each exception item, do not treat the setup as production-ready.

| Selection point | Key question | Grounded detail |

|---|---|---|

| Originator ID control depth | How precisely can the ACH program flag exceptions? | One documented model can flag by transaction type, dollar amount, and Originator ID |

| Exception queue usability | Can reviewers see core context and decide in one place? | One documented exception view includes account number, ACH company ID, company name, transaction type, effective date, and dollar amount |

| Approval SLA enforceability | What are the cutoff rules and missed-deadline outcomes? | One check workflow requires pay/return decisions by 4 p.m. local account time; one ACH workflow requires same-day effective-date exceptions by 10 p.m. CT on the next business day; at least one ACH program automatically returns undecided exceptions |

| Audit log export quality | What evidence will be available later? | Historical reporting on all exceptions and sample exports should be reviewed before launch |

| Market coverage | Do rules carry across markets, accounts, or partners? | Do not assume one cutoff pattern, approval flow, or policy gate applies across markets, accounts, or partners |

This section is not for teams that do not control bank-account decisions. In at least one bank program, only the primary administrator or a user with granted access can take exception actions; if you cannot assign and verify that authority, the rest of the setup is not reliable.

- Originator ID control depth

Start by checking how precisely the ACH program can flag exceptions. One documented model can flag by transaction type, dollar amount, and Originator ID, which gives tighter control than a simple broad allow list.

- Exception queue usability

Your queue should make a decision possible in one place. One documented exception view includes account number, ACH company ID, company name, transaction type, effective date, and dollar amount; if reviewers cannot see core context clearly, consistency drops near cutoff.

- Approval SLA enforceability

Treat cutoff handling as a hard requirement, not a policy note. Programs differ: one check workflow requires pay/return decisions by 4 p.m. local account time, and one ACH workflow requires same-day effective-date exceptions by 10 p.m. CT on the next business day. Also confirm the missed-deadline behavior; at least one ACH program automatically returns undecided exceptions.

- Audit log export quality

Score retained exception reporting before launch. Ask for historical reporting on all exceptions and review sample exports so you can confirm what evidence is actually available later.

- Market coverage

Validate terms bank program by bank program. Do not assume one cutoff pattern, approval flow, or policy gate applies across markets, accounts, or partners; document cutoff windows and coverage constraints up front.

Before choosing, request one sample day of exceptions, one sample export, and exact cutoff rules by rail. This usually surfaces the real risk early: an unowned decision queue when deadlines hit.

For a platform-specific look at check controls, see Positive Pay for Platforms: How Check Fraud Prevention Works in Digital Payment Systems.

Check Positive Pay and ACH Positive Pay compared for platform risk owners#

Check Positive Pay and ACH Positive Pay are complementary, not interchangeable: one validates check presentment against issued-check data, while the other constrains ACH debits using authorized-originator logic.

| Aspect | Check Positive Pay | ACH Positive Pay |

|---|---|---|

| Preventive scope | Compares presented checks to customer-submitted issued-check details; mismatches become exceptions | Compares ACH debits to customer-defined authorized activity; nonmatching items are flagged or trapped for review |

| Core artifact | Issued-check file / check issue data | Allow/deny filter logic, often including Originator ID (ACH company ID) |

| Main risk addressed | Check items that do not match issued records | Unauthorized ACH debits or debits outside configured authorization rules |

| Timing pressure | Issued-check data must be submitted in time to avoid avoidable exceptions | Filter design and exception decisions must be completed before cutoff |

| Example documented timing | One guide says issue checks at least 60 minutes before distribution, and visibility can take up to 60 minutes | One program alerts at approximately 5 a.m. CST, with a 2 p.m. CST final cutoff; undecided items default to Return |

1. Scope first: choose by rail exposure, not by feature list#

Use Check Positive Pay for check presentment risk and ACH Positive Pay for ACH debit authorization risk. A check-issued file does not control ACH debits, and Originator ID logic does not validate check presentment. If both rails are active, run both controls; single-rail deployment is usually only defensible when one rail is actually absent.

2. Inputs are the control surface#

For checks, the issued-check file is the control. If it is late, valid items can be pushed into exceptions due to your own timing. For ACH, the control is filter precision. Overbroad filters can let unwanted debits post, while overly restrictive filters can overload manual review.

3. Exception timing determines outcomes#

Both rails route nonmatching items to exception decisioning, and non-decision within the defined window can result in return processing. In ACH programs with short windows, this is especially operational: alerts alone are not enough if no entitled approver can act before cutoff.

Common failure modes:

- Stale issued-check data.

- Overbroad or poorly tuned ACH filters.

- Delayed exception decisions in the queue.

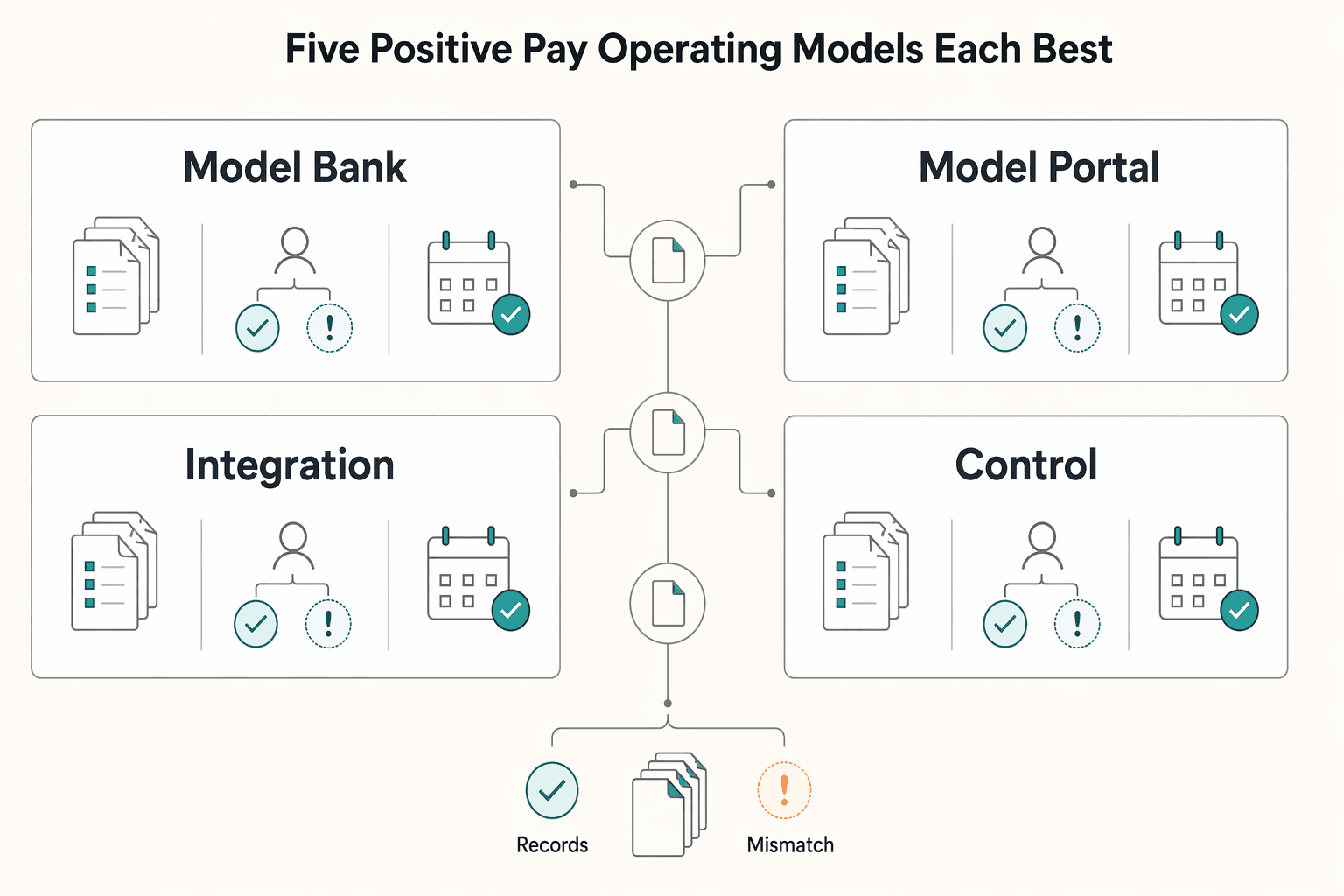

The five Positive Pay operating models and what each is best for#

Use the lightest model that still lets you prove three things on demand: what data was submitted, who made each pay/return decision, and whether each decision was made before cutoff.

| Model | Best for | Main tradeoff |

|---|---|---|

| Model 1: bank portal only | Low exception volume and daily review handled reliably in the bank portal | Manual dependency can consume hours per day and create cutoff risk if ownership is unclear |

| Model 2: portal plus internal checklist | Stronger governance before API integration | Process drift between internal trackers and portal reality, so routine reconciliation discipline is needed |

| Model 3: API-assisted decisioning | Scale that requires faster routing and stronger traceability across teams or markets | Exception windows can be time-boxed, for example 9 a.m. to 3 p.m. local processing time |

| Model 4: API plus rule-based fraud detection | High exception volume where triage matters as much as routing | Rule systems can generate false positives, and loose ACH pre-authorization settings can broaden exposure |

| Model 5: full control stack with velocity checks and policy gates | Stronger internal defensibility than queue handling and basic rules provide | Heavier change control for rules, thresholds, and approvals |

- Model 1: bank portal only

Use this when exception volume is low and daily review can be handled reliably in the bank portal. Portal-based Positive Pay is a complete operating model: users can manage items and work Positive Pay and ACH exceptions directly in digital banking. The tradeoff is manual dependency, which can consume hours per day and create cutoff risk if ownership is unclear.

- Model 2: portal plus internal checklist

Use this when you need stronger governance before API integration. The portal remains the system of record for decisions, while your checklist standardizes review, approval, and notes so audit-trail outputs remain useful. The main risk is process drift between internal trackers and portal reality, so you need a routine reconciliation discipline.

- Model 3: API-assisted decisioning

Use this when scale requires faster routing and stronger traceability across teams or markets. A Positive Pay API can match checks to issue data, submit exception decisions, and retrieve processed-exception history. In documented programs, exception windows can be time-boxed, for example 9 a.m. to 3 p.m. local processing time, so staffing and alerting should be designed to that clock.

- Model 4: API plus rule-based fraud detection

Use this when exception volume is high enough that triage matters as much as routing. Rules can prioritize which check or ACH items get first review, but payment-fraud rule systems are known to generate false positives. Rule defaults also matter: loose ACH pre-authorization settings can broaden exposure instead of reducing it.

- Model 5: full control stack with velocity checks and policy gates

Use this when you need stronger internal defensibility than queue handling and basic rules provide. Velocity checks add a specific control: monitoring how often transaction elements repeat within defined intervals. The gain is clearer, policy-backed handling of repeated suspicious patterns; the cost is heavier change control for rules, thresholds, and approvals.

For deeper context on rule design tradeoffs, see Fraud Detection for Payment Platforms: Machine Learning and Rule-Based Approaches.

Minimum control stack to launch without overbuilding#

If you're launching with limited time or headcount, prioritize decision quality over automation depth. A workable minimum stack is: complete bank-matching inputs, clear exception ownership, enforceable decision timing, and retained decision evidence.

| Control | What it includes | Why it matters |

|---|---|---|

| Approved inputs by rail | ACH approved Originator ID list plus any amount or spending limits; check issuance feed with check number, amount, Issue Date, Payee Name, and Issue Type | Incomplete or stale inputs increase exception noise and weaken every downstream control |

| Named ownership for every exception item | Who reviews each exception, who can make the pay/return decision, and who is the backup | A shared unowned queue is not launch-ready |

| One enforceable Approval SLA per rail | One decision SLA for checks and one for ACH based on the actual bank program, with fallback approvers for weekends and holidays | Cutoffs vary by bank, and some workflows auto-return unresolved items at cutoff, for example 12 pm Central Time in one documented program |

| Retained audit evidence plus baseline monitoring | Retain exception decision records and audit-trail reporting; export and store reports; track exception aging, return reasons, and repeat patterns | Bank-side history retention may not be enough; one documented system retains paid-item history for 90 days |

- Approved inputs by rail

For ACH, maintain an approved Originator ID list plus any amount or spending limits you intend to enforce. For checks, keep an issuance feed with the fields used for matching: check number, amount, Issue Date, Payee Name, and Issue Type. Incomplete or stale inputs increase exception noise and weaken every downstream control.

- Named ownership for every exception item

Assign who reviews each exception, who can make the pay/return decision, and who is the backup when that person is unavailable. Users are expected to decide exception items as pay or return before cutoff, so a shared unowned queue is not launch-ready.

- One enforceable Approval SLA per rail

Define one decision SLA for checks and one for ACH based on your actual bank program, with fallback approvers for weekends and holidays. Do not use a generic deadline: cutoffs vary by bank, and some workflows auto-return unresolved items at cutoff (for example, 12 pm Central Time in one documented program).

- Retained audit evidence plus baseline monitoring

Retain exception decision records and audit-trail reporting from launch. Do not assume bank-side history retention is enough for your needs (one documented system retains paid-item history for 90 days), so export and store reports on your side. Track exception aging, return reasons, and repeat patterns tied to ACH fraud or forged checks. If resources are tight, a consistent daily review beats partially configured tooling. For a related read, see AI Fraud Detection for Subscription Platforms Beyond Rules-Based Approaches.

Daily exception handling that stands up to audit review#

Daily exception handling should produce one outcome: each item is decisioned on time, with evidence and an audit trail you can retrieve later.

- Ingest alerts and classify the item before anyone decides

Start with pending-decision alerts, then reconcile those alerts to the actual exception queue so no item is missed. Classify each exception by rail, reason, and urgency before decisioning. Some programs send reminders 30 minutes before cutoff, while others send them one hour before cutoff, so confirm those alerts reach someone who can act.

- Apply the pay-or-return decision from item-level evidence

Each exception needs an explicit pay/return (or approve/return) decision based on the record, not on queue-clearing speed. For check exceptions, review the exception reason and check image before deciding. For ACH exceptions, review each transaction and decide whether to approve or return it. If your program applies a default action at cutoff, make sure the team knows that setting and its consequence for undecided items.

- Separate review and approval where your setup supports it

Avoid concentrating evidence review, decision submission, and record verification in one person when your platform can enforce separation. Dual-approval decisioning is available in some setups, including a secondary approver after the first approver submits. If you use dual approval, test primary and backup access regularly so approvals do not stall near cutoff.

- Close the queue with audit-ready records, then monitor exceptions

Queue closure should include a complete record: decision, support note, approver identity, and timestamp, plus the report trail used for review. Banks may expose this through decisioned-exception tracking and user activity audit reporting. Track unresolved items at cutoff, SLA overrides, and manual decisions with missing notes, then use repeated patterns to review policy, staffing, or upstream process design.

Escalation rules for suspicious activity across checks and ACH#

When suspicious activity repeats across related items, treat it as a pattern case, not routine queue work. Use a documented escalation matrix that contains risk quickly without turning every anomaly into a legal event.

- Trigger on linked patterns, not one-off exceptions

Move cases out of routine handling when you see repeated unauthorized ACH debits from the same Originator ID, clustered counterfeit check attempts, or abnormal bursts flagged by velocity checks. Escalation should key off repetition plus linkage (same counterparty, originator, account, check range, or short-window burst pattern), not just one loud item.

Require an evidence pack before escalation: ACH return reason, Originator ID, check image when applicable, timestamps, exception reason, and the velocity alert snapshot. If you are in Nacha Phase 1 scope, including participants with annual ACH origination volume in 2023 of 6 million or greater, risk-based ACH fraud-identification procedures are required.

- Use tiered escalation with explicit handoffs to compliance and legal

A practical matrix is operations triage, then compliance review, then legal or bank-partner involvement when internal suspected-fraud thresholds are crossed. Each handoff needs a named owner, deadline, and required evidence set.

Do not treat every unusual item as reportable: SAR expectations are tied to what the institution knows, suspects, or has reason to suspect. But once facts may meet that standard, timing matters. For teams with SAR responsibilities, the filing clock is 30 calendar days from initial detection, and delays to identify a suspect cannot extend reporting past 60 days from initial detection.

- Apply containment by rail, and keep controls scoped and reversible

For ACH, immediate containment can include blocking all ACH transactions, returning only ACH debits, or applying debit filtering; tighter Originator ID controls are often a first response. If an ACH debit is returned unauthorized or revoked, origination of that debit stream must stop.

For checks, temporary counterparty freezes or mandatory dual approval for high-risk items can buy investigation time. Scope the action to the suspect stream first, verify bank-side setting changes the same day, and define owner, start time, and exit criteria so containment does not unintentionally block legitimate activity.

Related: Velocity Checks for Payment Platforms: How to Cap Payout Frequency and Amount to Prevent Fraud.

Common failure modes and monthly control testing#

Monthly testing should answer two questions first: did the bank receive complete, matchable data, and was every exception decisioned with evidence before cutoff. Most breaks come from operational drift, not obvious fraud spikes.

- Data integrity drift

Verify issued-check feed completeness and mapping each month, because posted checks can only be exception-tested when issue data reaches the bank and fields match. For ACH, test Originator ID accuracy in filters and return-rate monitoring records. If data is late, incomplete, or mis-mapped, exception logic loses coverage before review starts.

- Process reliability gaps

Test your internal approval timing against actual cutoff behavior. In one operating guide, decisions are due by 12 pm Central Time and unresolved items are auto-returned, so track missed deadlines, aged exception-queue items, and decisions lacking pay/return evidence in the audit trail. Also review items still pending 30 minutes prior to cutoff and confirm alerts reached the assigned approver.

- Governance and evidence decay

Check that approver lists are current, overrides are documented, and return rationales are applied consistently enough to support ACH return-rate monitoring. Keep testing independent from day-to-day exception handling, and maintain segregation of duties for sensitive control tasks.

Close each cycle with one remediation owner and one verification checkpoint before the next month. Use concrete checks, such as confirming corrected issued-check data in the next transmission and confirming the next sample has no unresolved exceptions at cutoff with complete audit-trail history.

What to implement first in the next 30 days#

In the first 30 days, prioritize complete coverage and cutoff-ready operations over advanced detection.

- Deploy both rails first

If you run both checks and ACH debits, launch Check Positive Pay and ACH Positive Pay together. This closes the obvious gap of protecting one rail while leaving the other exposed. For setup, make sure check-issue file formatting and upload are working, and that ACH approval logic and allowed counterparties are configured from day one.

- Lock the three non-negotiables

Put a documented Approval SLA, a staffed exception queue, and an exportable audit log/report with decision history in place before adding anything else. Exception handling is cutoff-driven: one published pattern is notifying users about pending items 30 minutes prior to cutoff, but your actual deadline depends on your bank/program. If items miss cutoff or decisions are not traceable, the control is not reliable.

- Choose the lightest model that still proves ownership

Use the simplest workflow that enforces permissioned approvers and leaves a clear decision trail. User roles should control who can approve, and higher-risk items can use configurable approval levels or dual approval where supported. Lightweight is fine if you can still show who decided pay/return, what they decided, and when.

- Add velocity checks and deeper rules after the basics are stable

Expand to velocity checks and deeper rule-based fraud detection only after exception review is consistently on time and well logged. Adding more rules too early usually increases alert noise before governance is reliable.

For a broader view of layered fraud controls, see Transaction Monitoring for Platforms: How to Detect Fraud Without Blocking Legitimate Payments.

Frequently Asked Questions

What is Positive Pay, and what does it actually prevent?

Positive Pay is an electronic fraud-detection service used for both check and ACH transaction screening. It helps catch mismatched or unauthorized items by requiring a match or review against predefined criteria. The key point is scope: it is a layer of defense, not a guarantee of zero loss.

How is ACH Positive Pay different from Check Positive Pay in day-to-day operations?

Check Positive Pay compares presented check details, such as check number and dollar amount, against your issued-check records. ACH Positive Pay screens ACH items against preapproved vendors or other rules, and some banks let you flag by transaction type, dollar amount, and Originator ID. In practice, they rely on different control inputs: issued-check data for checks and approval lists or rules for ACH.

Who should approve an exception item, and how fast should decisions be made?

An exception item is a transaction blocked because it did not match predefined approval criteria, so approval should sit only with authorized users. Bank guidance describes this authority as a primary administrator or a user granted access through permission controls such as Access & Security Manager, not whoever happens to see the alert first. Decisions also have to be made before the bank cutoff. One published example is 3:30 p.m. ET, and if you miss it, the bank may apply a preset default action.

What must be preconfigured before launch, especially for `Originator ID` controls?

Before go-live, preconfigure the issued-check data, the approved ACH counterparty list, and the ACH review rules, including Originator ID where supported. If your bank supports it, configure transaction type and dollar amount filters alongside Originator ID rather than assuming one field is enough. Also confirm flagged items route to authorized approvers in time for cutoff-based decisions.

Does Positive Pay eliminate `check fraud` and `ACH fraud`, or only reduce exposure?

It reduces exposure. It does not eliminate fraud. The grounded way to describe it is as an effective layer of defense, which matters because weak permissions and missed deadlines can still let loss events through. If someone is selling it internally as complete protection, that is a red flag.

When should we escalate from normal exception handling to a formal `escalation matrix` path?

Escalation triggers are bank- and policy-specific, so define them in your own escalation matrix rather than assuming a universal rule. At minimum, escalate when an exception cannot be resolved by authorized approvers before cutoff, or when a missed decision would trigger an unwanted default pay or return action. Do not assume a fixed number of exceptions automatically requires external regulatory reporting.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/03trusted

- ecfr.gov/current/title-12/chapter-III/subchapter-B/pa...trusted

- fdic.gov/frequently-asked-questions-regarding-suspici...trusted

- federalreserve.gov/supervisionreg/srletters/SR2504a1.pdftrusted

- ithandbook.ffiec.gov/it-booklets/information-security/ii-informat...trusted

- americafirst.com/business/services/positive-pay.htmlexternal

- bankwithstifel.com/insights/how-positive-pay-protects-your-busi...external

- chase.com/content/dam/chase-ux/documents/commercial-ba...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Positive Pay Controls Check Fraud in Digital Payment Platforms

This list is for compliance, legal, finance, and risk owners who need to use Positive Pay without turning it into a bigger build than the risk justifies. The goal is practical: reduce check and electronic transaction fraud while keeping decisions and approvals auditable across products and bank relationships.

Fraud Detection on Payment Platforms with Rules and Machine Learning

For cross-border payout platforms, effective fraud detection is less about a single model or rule than about controls you can document, explain, and defend under audit or incident pressure.

Velocity Checks for Payment Platforms: How to Cap Payout Frequency and Amount to Prevent Fraud

**Payout velocity controls are not just fraud settings. They are policy decisions you will need to explain and reconstruct later.** If you cannot show why a payout was allowed, held, escalated, or declined, the rule is not ready for production.