Quick Answer

Start with a written scope, then run a single evidence-based process: issue one Request for Proposal (RFP), score vendors with weighted criteria, and apply hard fail rules before commercial negotiation. For a vendor selection process platforms evaluate third-party relationships, the article recommends early checks for KYC, KYB, AML, operational traceability, and exception handling rather than demo-led ranking. Final approval comes only after staged due diligence, implementation verification, and documented ownership for ongoing monitoring.

What to evaluate before signing#

Step 1: Treat vendor choice as a risk decision, not a feature contest. A solid vendor selection process matches your requirements to vendor capabilities and pricing through a clear set of procurement steps. That sounds basic, but it matters because poor vendor choices have real business consequences. Feature lists rarely tell you how a provider will perform under real operational and risk constraints. If your team starts by comparing dashboards, coverage maps, or headline fees, you can end up shortlisting vendors that look strong in demos but fail once legal, finance, or operations gets involved.

For many teams, that gap shows up fast. A vendor is not just another software tool. It affects day-to-day operations, visibility, and how risk is handled when something breaks. The practical rule is simple. If a vendor cannot be evaluated against written requirements, it is too early to compare vendors.

Step 2: Align the people who will live with the decision. Procurement often owns vendor selection, but the decision is rarely procurement-only. Founders, product, engineering, finance, and ops all see different failure modes, so you need those perspectives before vendor outreach, not after it. A defined process reduces risk because it aligns internal teams on requirements, budget, and evaluation criteria before you engage the market.

A useful checkpoint is whether your team can answer three questions in writing without calling a vendor: what problem are we solving, what constraints matter most, and who decides on tradeoffs? If those answers are still vague, demos will create more confusion than clarity. One common failure mode is a product-led shortlist that later stalls because key reviewers were never part of the initial screen.

Step 3: Aim for a decision you can defend, not just a vendor you like. The outcome of this guide is not a pile of notes from sales calls. It is a decision-ready sequence built around weighted criteria, due diligence, and clear decision checkpoints. Weighting matters because it forces decisions to reflect impact instead of drifting into price-only comparisons. Due diligence matters because shortlisted suppliers still need to be checked for financial stability, risk, and compliance before final selection.

That gives you something more useful than a ranked list. You should leave the process with an evidence pack you can explain to internal stakeholders and leadership. It should include documented requirements, weighted scoring, reasons for rejection, and proof that the final choice survived more than a product demo. If you cannot show why a vendor was chosen and what would have disqualified them, the process is not decision-ready yet.

Set the scope before you evaluate vendors#

Step 1#

Set scope before outreach: tools support the process, but they do not replace due diligence. source-to-pay software and vendor selection software can standardize intake, approvals, and scoring, while risk review still has to cover money movement, compliance exposure, and operational failure paths. If your provider touches merchant processing activity, keep that evaluation separate from card-issuing capabilities that are not part of your buying decision.

Use a one-page scope check: what you are buying, what it must do, and what is out of scope. If a feature is outside that scope, do not score it as a bonus.

Step 2#

Define included capabilities up front and use the same labels across RFP, scorecard, and legal review. For many platform decisions, that means explicitly marking Merchant of Record (MoR), Virtual Accounts, Payouts, and tax/compliance workflows as in scope now, later, or excluded.

Keep comparisons objective by scoring every shortlisted vendor against the same included capabilities only. Do not add "nice-to-have" items during demos.

Step 3#

Lock the risk boundary in writing before detailed commercial comparison. Document which flows may require KYC, KYB, or AML review, which jurisdictions matter, and whether expectations such as NYDFS are relevant to your launch path. If legal or compliance cannot confirm that boundary, pause evaluation until they can.

End with explicit exclusions: flows, geographies, and features you are not evaluating. That prevents the process from drifting into a feature contest.

If you want a deeper dive, read Third-Party Risk Management for Payment Platforms: How to Vet and Monitor Your Payment Vendors.

Prepare the evaluation packet before outreach#

Freeze one evaluation packet before the first intro call so every vendor is scored against the same assumptions and evidence.

| Packet item | Include or request | Checkpoint |

|---|---|---|

| RFP | Use-case volumes, target geographies, settlement expectations, and key exception paths | Every response should map to the same scenarios |

| Risk evidence | Vendor risk management controls, incident handling, audit trails, and third-party cyber risk posture | Review how incidents are identified, escalated, communicated, and closed |

| Legal, compliance, and tax artifacts | Policy summaries, KYC/KYB approach, AML gating logic, and VAT validation support where relevant | Ask what data the vendor captures, what outputs it can generate or export, and what remains manual |

| Scoring ownership | Engineering owns integration and auditability; finance and ops own settlement, exception handling, and tax-document output; compliance owns risk controls and gating logic | Decision ownership is clear for each scored area |

Step 1#

Send one Request for Proposal (RFP) version to every vendor. Include your use-case volumes, target geographies, settlement expectations, and key exception paths (like returns, held funds, delayed payouts, manual investigations, and status mismatches between provider and internal records).

Define scenarios clearly enough that vendors must answer your real operating model, not a demo narrative. The checkpoint is consistency: every response should map to the same scenarios, with no custom add-ons changing scope mid-comparison.

Step 2#

Require evidence, not assurances. Ask for artifacts covering vendor risk management controls, incident handling, audit trails, and third-party cyber risk posture.

Focus on how the provider operates when something fails. You should be able to review how incidents are identified, escalated, communicated, and closed, and what audit evidence exists for disputed transaction or payout states.

Step 3#

Define legal, compliance, and tax artifacts before demos begin. Request policy summaries and a clear description of KYC/KYB approach, AML gating logic, and VAT validation support where relevant.

Bring finance and tax into packet design early. If your workflows may involve W-8, W-9, Form 1099, FEIE, or FBAR, ask what data the vendor captures, what outputs they can generate or export, and what remains manual for your team.

For Foreign Earned Income Exclusion (FEIE), avoid vague "supports FEIE" claims. Ask whether the product can preserve facts your team may need later, because FEIE eligibility depends on conditions such as having a tax home in a foreign country and, under the physical presence test, being abroad for 330 full days in a 12-month period. Those 330 days do not need to be consecutive, and excluded foreign earned income still must be reported on a U.S. tax return.

Step 4#

Assign scoring owners before demos start. Engineering should own integration and auditability, finance and ops should own settlement and exception handling plus tax-document output, and compliance should own risk controls and gating logic.

The checkpoint is clear decision ownership for each scored area. If ownership is unclear, gaps usually surface late during contract review.

You might also find this useful: Merchant of Record for Platforms and the Ownership Decisions That Matter.

Build a weighted scorecard with hard go or no-go rules#

Build the scorecard before demos, and use it to filter out unacceptable risk, not just rank vendors. Weighted scoring gives you a defensible way to tier options, but only after you define what is an automatic no-go.

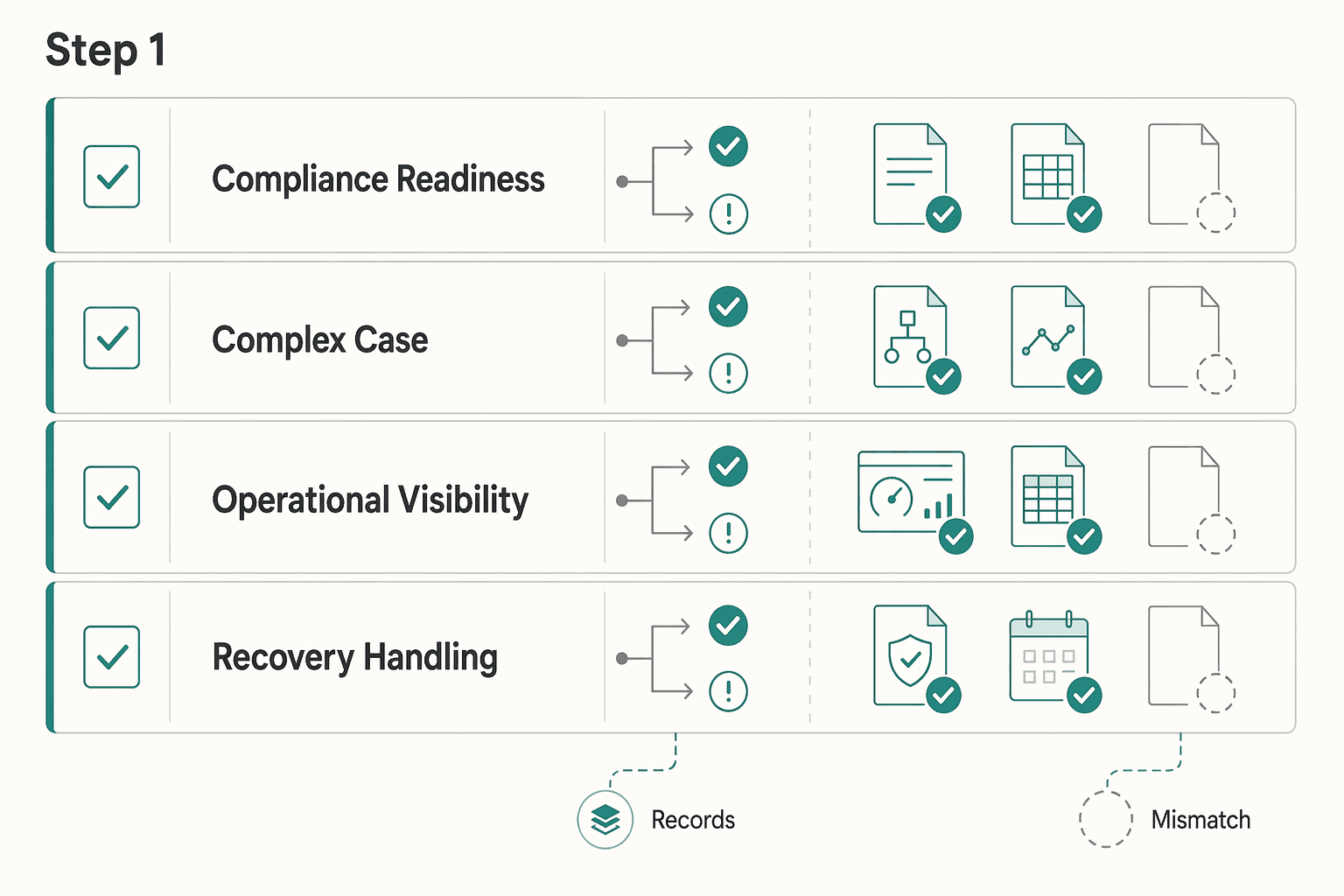

Step 1#

Set weighted dimensions around launch risk, then score every vendor from the same evidence pack.

| Dimension | What you are scoring | Sample weight | Minimum evidence to score |

|---|---|---|---|

| Compliance readiness | Control clarity, approval/block logic, exception handling | 35% | Written controls, real decision paths, escalation owners |

| Integration complexity | API/event model fit, implementation burden, reliability behavior | 25% | Technical docs, sample payloads, clear state transitions |

| Operational visibility | Status traceability, exports, reconciliation support, auditability | 20% | Ops views, export examples, matchable reference fields |

| Recovery handling | Disputes, returns, held-funds investigations, remediation flow | 20% | Exception-path process docs, ownership, closure evidence |

Use the weights as a starting point and adjust to your launch constraints. If a vendor can only be scored from demo narration, leave the score blank until artifacts are provided.

Step 2#

Define hard fail rules before totaling points. A weighted score should help you choose among acceptable vendors, not justify a weak control posture.

Use no-go rules like these:

- Fail vendors that cannot show credible third-party risk management across the lifecycle, including onboarding, due diligence, monitoring, and remediation.

- Fail vendors that cannot provide enough operational transparency for your team to reconstruct transaction and payout states when issues occur.

- Fail vendors that cannot walk through dispute, return, or held-funds recovery with clear ownership and inspectable evidence.

- Fail vendors that rely on one-time review posture when your model requires continuous oversight.

This matters because third-party risk can include cyber threats, data breaches, regulatory violations, and financial instability.

Step 3#

Set pass thresholds for launch-critical capabilities, then write tradeoff rules in advance. If a vendor has broader coverage but weaker controls, require approved compensating controls with named owners or reject the option.

End with a clear decision bucket for each provider: pass, pass with compensating controls, or fail. If evidence is missing, record it as a dated follow-up item instead of scoring by assumption.

Run due diligence in a fixed order that exposes risk early#

Use a fixed stage-gate sequence to surface high-impact risk before your team spends cycles on commercials: risk and compliance first, architecture second, operations third, finance fourth, then negotiation. This is an operating choice, not a regulatory mandate, and it helps you rule out weak options earlier.

| Stage | Focus | Evidence |

|---|---|---|

| Risk and compliance | KYC, KYB, AML, incident handling, and TPRM evidence | Check due diligence/onboarding, risk assessment, remediation, continuous monitoring, and offboarding |

| Architecture | Behavior under failure and retry conditions | Review sample payloads, state-transition documentation, error-handling notes, and one replay walkthrough |

| Operations | Held funds, returns, payout failures, and investigations for unmatched deposits | Confirm who owns each case type, what data your team can access directly, and how closure is documented |

| Finance | Exports and audit evidence for reconciliation; tax-document handling if in scope | Check stable identifiers, status fields, timestamps, traceability into your internal ledger, and handling for W-8, W-9, and Form 1099 data |

| Negotiation | Move forward only after written checkpoint sign-off | If evidence is incomplete, log the gap with an owner and date and stop there |

Step 1. Start with risk and compliance evidence. Begin with KYC, KYB, AML, incident handling, and broader Third-Party Risk Management (TPRM) evidence. Use the five-phase lifecycle as your check: due diligence/onboarding, risk assessment, remediation, continuous monitoring, and offboarding. If a provider can only show onboarding and cannot show credible monitoring, mitigation, or exit handling, treat that as an early warning.

Ask for written policy summaries, escalation paths, and named exception owners. Then check consistency across the Request for Proposal (RFP), demo, and follow-up documents before moving forward.

Step 2. Validate architecture before commercial terms. Confirm technical behavior under failure and retry conditions before pricing discussions pull focus. For your implementation, verify idempotent behavior across retries, webhooks, provider references, and ledger reconciliation paths. If the same event can create duplicate postings or mismatched states, that is a launch risk.

Ask for sample payloads, state-transition documentation, error-handling notes, and one replay walkthrough. Require evidence that repeated delivery does not create duplicate payout or status outcomes.

Step 3. Test real exception handling with operations. Run awkward scenarios, not just the happy path: held funds, returns, payout failures, and investigations for unmatched deposits. The goal is to confirm ownership, evidence quality, and closure discipline before go-live.

Ask who owns each case type, what data your team can access directly, and how closure is documented. If the vendor can only describe support escalation in general terms, pause progression.

Step 4. Confirm finance evidence, then require sign-off before negotiation. Before contract redlines, confirm exports and audit evidence are usable for reconciliation. For Payouts, check stable identifiers, status fields, timestamps, and traceability into your internal ledger. If tax-document handling is in scope, review how W-8, W-9, and Form 1099 data is collected, updated, exported, and retained.

Require written checkpoint sign-off at each stage before moving to the next. If evidence is incomplete, log the gap with an owner and date and stop there.

Compare integration and operating model fit, not just feature breadth#

Choose the operating model your team can govern under the legal authorities that apply to you, not the vendor with the longest feature list.

Step 1#

Start by mapping responsibility before comparing bundled and modular designs. If you are evaluating a bundled MoR path versus a setup using Virtual Accounts and Payouts, document who owns each obligation when money moves, exceptions occur, and evidence is requested.

Where FTA third-party contracting rules apply, treat this as a hard gate. Circular 4220.1G is applicable as of January 17, 2025, and it makes recipient compliance responsibility explicit; when circular text conflicts with statute or regulation, statute or regulation controls. Build a written responsibility matrix in the Request for Proposal (RFP) or draft contract and mark each area as vendor-owned, customer-owned, or shared.

Step 2#

Compare integration fit using operating evidence, not API marketing. Ask for concrete artifacts your teams can review, then score clarity and traceability across implementation and operations.

Use one practical checkpoint: can your team trace a single event consistently from provider status to internal records and finance outputs without guesswork. If that trace is unclear, treat it as unresolved operating risk regardless of feature breadth.

Step 3#

Make the operating-model decision explicit in your memo and tie it to ownership and governing authority. State the burden you are accepting, the evidence reviewed, and which rule set controlled the decision.

This keeps selection disciplined: even when a vendor performs part of the workflow, your organization remains responsible for compliance with applicable legal authorities.

Decide what to automate now and what to keep manual#

After you choose the operating model, split work into two lanes: automate repeatable evidence handling, and keep uncertainty-based decisions with human reviewers.

Step 1#

Automate repetitive collection and tracking first. Start with document intake, control attestations, renewal reminders, and a baseline third-party risk management score based on objective fields. Vendor management software and vendor management systems can help by centralizing vendor performance, payments, and compliance tracking, and some tools support automated risk assessment and compliance monitoring.

A practical first pass:

- required document intake with owner assignment and due dates

- attestation collection with clear current or expired status

- contract and control renewal reminders

- baseline scoring from simple fields such as document completeness, policy freshness, and declared service scope

Success is not that reminders were sent. Success is that missing or expired evidence is flagged, routed to an owner, and does not appear complete in review.

Step 2#

Keep judgment-heavy reviews manual when facts are messy or the compliance path is unclear. Use a simple rule: automate for consistency, escalate for uncertainty.

Automated checks can identify missing policy summaries or upcoming renewals, but they should not close ambiguous risk and compliance decisions on their own. One vendor-evaluation guide explicitly warns teams not to skip vendor risk and compliance, and manual assessments without consistent policy handling and real-time visibility can increase exposure.

For manual review, require a clear evidence pack: raw submission, tool-flagged exceptions, relevant incident context, and a short written disposition.

Step 3#

Define re-evaluation triggers before launch so reviews reopen when risk changes, not only on calendar dates. Typical triggers include incidents, product expansion, service-scope changes, and shifts in third-party cyber risk posture.

Your operating checkpoint is simple: can you show what triggers reassessment, who owns follow-up, and what evidence must be refreshed? If not, automation may collect records without catching meaningful risk changes. Related reading: Subscription Billing Platforms for Plans, Add-Ons, Coupons, and Dunning.

Fix common vendor selection mistakes before they become incidents#

These mistakes are predictable, and they usually start before contract signature. Treat selection as evidence review plus ongoing ownership, not a demo contest.

Step 1#

Do not treat a polished demo as proof of readiness. Use your vendor selection matrix to require evidence for normal operations and exception handling before approval.

Your checkpoint is simple: can your team trace how a real exception is handled and resolved in practice? A common failure mode is a tool that looks complete in a walkthrough but breaks when edge-case workflows appear.

Step 2#

Do not rely on procurement records as your risk gate. source-to-pay software can organize purchasing data, but it should not replace dedicated due diligence and vendor risk management review.

This is where third-party risk management carries real weight. If a vendor will access your systems or handle your data, use a rigorous TPRM review rather than ratings alone, since ratings-only tools can miss the workflow depth needed to remediate issues.

Step 3#

Do not ignore remediation and exception workflows. Ask how risk findings are triaged, assigned, and tracked to closure, not just how they are scored.

The red flag is hand-waving. If the answer stops at "we monitor continuously," ask what internal assessments are automated, what external signals are monitored, and how follow-up actions are documented.

Step 4#

Assign post-launch ownership before go-live. Continuous monitoring is part of vendor selection, not a later add-on.

Name cross-functional owners and set a recurring third-party control review cadence with a defined follow-up path for issues found. If nobody owns post-contract monitoring, problems surface late and escalation starts after the incident.

For a step-by-step walkthrough, see Best Merch Platforms for Creators Who Want Control and Compliance.

Make the decision and launch with a copy paste checklist#

Use one signed checklist to convert evaluation into a launch decision. If any item is unresolved, pause contract signature or launch. A dashboard is not the whole solution, so every approval should tie to documents, sample outputs, or test evidence.

| Launch check | Confirm | Verification |

|---|---|---|

| Scope and exclusions | Plain-language boundary for MoR, Virtual Accounts, and Payouts from the final proposal and contract | Internal summary, commercial terms, and solution description all match |

| Control ownership | Coverage and ownership for KYC, KYB, AML, VAT validation, and tax-document handling | Do not accept generic supported claims without a policy summary, process detail, sample output, or clear handoff |

| Weighted scorecard | Named owners across engineering, finance/ops, and compliance; record tradeoffs | If you choose a lower-scoring option, require written sign-off and a dated compensating action |

| Implementation path | Webhook tests, idempotent retries, and ledger reconciliation using realistic failure cases | Treat missing event-to-ledger traceability as a no-go |

| Post-launch monitoring | Owners and dates for vendor risk management, incident review, and periodic reassessment | Calendar, escalation path, and evidence repository are all in place |

-

Document scope and exclusions. Write one plain-language boundary for

MoR,Virtual Accounts, andPayoutsfrom your final proposal and contract. Make explicit what the provider does not own and who does. Verification point: internal summary, commercial terms, and solution description all match. -

Validate control ownership for regulated and tax-sensitive flows. Confirm required coverage and ownership for

KYC,KYB,AML,VAT validation, and tax-document handling. Do not accept generic "supported" claims without a policy summary, process detail, sample output, or clear handoff. Failure mode: no clear owner for blocked users, exceptions, or tax-form intake. -

Finalize the weighted scorecard and record tradeoffs. Close scoring with named owners across engineering, finance/ops, and compliance. Weigh vendor responses against the critical problems you need to solve, not demo polish. If you choose a lower-scoring option, require written sign-off and a dated compensating action.

-

Prove the implementation path before launch approval. Run checkpoint tests for

webhooks, idempotent retries, andledgerreconciliation using realistic failure cases. Confirm duplicate delivery does not double-post and finance can trace provider events to internal records. Treat missing event-to-ledger traceability as a no-go. -

Approve post-launch monitoring before go-live. Assign owners and dates for

vendor risk management, incident review, and periodic reassessment. Include both routine reviews and trigger-based reassessment after incidents or meaningful scope changes. Verification point: calendar, escalation path, and evidence repository are all in place.

Related: Vendor Risk Assessment for Platforms: How to Score and Monitor Third-Party Payment Risk. Related: eCommerce Reseller Payouts: How Marketplace Platforms Pay Third-Party Sellers Compliantly. Want a quick next step for "vendor selection process platforms evaluate third-party"? Try the free invoice generator.

Frequently Asked Questions

What is the difference between source-to-pay tooling and vendor selection due diligence?

source-to-pay software helps manage purchasing workflows, approvals, and vendor records. Vendor selection due diligence is the broader evaluation work used to decide fit against your requirements, budget, weighted criteria, and risk expectations, then monitor performance after contract.

What should platform teams evaluate first in a third-party provider?

Start by defining requirements, budget, and evaluation criteria before deep vendor engagement. In many teams, this includes risk and compliance expectations early so disqualifiers surface before detailed proposal comparison and commercial negotiation.

When should we automate vendor assessments versus keep them manual?

Automate repeatable intake tasks such as document collection, baseline scoring, and renewal tracking. Keep manual review for ambiguous or high-impact cases and for final judgment calls. Automation should support the process, not replace third-party risk and compliance accountability.

How do we standardize assessments across compliance, security, and operational risk categories?

Use one vendor selection matrix with weighted criteria, named owners, and a shared evidence pack. That gives you objective side-by-side comparison while still leaving room for qualitative factors like communication quality and responsiveness during review. Standardization breaks when each team asks different questions in different formats, so lock the template before outreach.

What are the most useful go or no-go decision rules for payment and payout vendors?

Make your go/no-go rules concrete and tied to your weighted criteria. Typical no-go triggers include failure to meet critical requirements, weak risk/compliance evidence, or unclear service commitments in contract terms. Treat unresolved critical gaps as launch blockers, not post-signature cleanup.

How often should we re-evaluate a vendor after onboarding?

Re-evaluation should be continuous, not just an annual formality. Keep a recurring review cadence and trigger reassessment when incidents occur or the service scope and risk profile changes. The verification point is simple: you should have clear owners, a schedule, and a written follow-up path for issues found.

Which documents should finance, engineering, and compliance each require before approval?

Use a shared evidence checklist aligned to your selection criteria. Finance typically confirms commercial terms and reporting expectations, engineering validates integration and service-fit details, and compliance verifies control, risk, and monitoring evidence needed for approval and ongoing oversight.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- occ.treas.gov/publications-and-resources/publications/comp...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC10072045trusted

- transit.dot.gov/sites/fta.dot.gov/files/2025-01/Third-Party-...trusted

- artofprocurement.com/blog/key-supplier-selection-criteria-every-p...external

- atlassystems.com/blog/vendor-selection-processexternal

- atlassystems.com/blog/vendor-management-toolsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Vendor Risk Assessment for Platforms: How to Score and Monitor Third-Party Payment Risk

Use this guide to build a practical, defensible approach to scoring and monitoring payment-adjacent vendor risk, with clear escalation points and named ownership. It is for compliance, legal, finance, and risk teams that need decisions and evidence that will hold up under scrutiny.

Third-Party Risk Management for Payment Platforms: How to Vet and Monitor Your Payment Vendors

Payment-vendor risk is easier to control when ownership, evidence, and escalation are explicit from the start.

How Marketplace Platforms Pay Third-Party Sellers Compliantly

Generic marketplace payout advice usually skips the part that breaks in production. Paying many sellers is not just moving money out. It is deciding who gets paid, when they become eligible, what happens when a buyer disputes a payment, and how finance proves every release later. If you are working on **ecommerce reseller payouts marketplace platforms pay third-party sellers**, this guide is for the marketplace operator, not for solo freelancer banking tips.