Quick Answer

Treat the tax deduction tracker categorize expenses workflow as a control gate, not a posting shortcut. Auto-route only stable recurring items with readable support, then force manual queues for mixed-use, travel, mileage, home office, and startup-timing decisions. Under the IRS ordinary-and-necessary standard, a clean export is insufficient without receipts or bills, business purpose, and reviewer accountability. When treatment differs by market or allocation support is weak, pause processing and escalate before filing.

What a defensible tax deduction tracker needs#

Use a tax deduction tracker categorize expenses workflow as a proof control, not just a faster way to code transactions. The goal is to make each tax write-off defensible with clear evidence, a documented business purpose, and the right jurisdiction rule.

| Jurisdiction | Deduction rule |

|---|---|

| U.S. | Business expenses are tested under the "ordinary and necessary" standard. |

| Canada | Current expenses must be reasonable and incurred to earn income. |

| UK | Trading deductions are limited to costs incurred "wholly and exclusively" for the trade. |

| Australia | Expenses must be directly related to earning assessable income, and mixed business/private costs must be apportioned to the business-use share. |

This matters most if you run compliance or finance across countries. You carry the burden of proof for return positions, and a categorized export on its own is not enough. The IRS says taxpayers must prove return entries and deductions, substantiate required expense elements, and generally keep documentary evidence such as receipts, canceled checks, or bills. Your recordkeeping system can be simple or advanced, but it must clearly show income and expenses and be backed by documents.

Treat automation as labor savings, not deductibility logic. Receipt capture, bank feeds, card imports, and accounting integrations can reduce manual work, but they do not by themselves complete a claim. If an item lacks documentary support or a clear business basis, treat it as a control failure and hold it for review.

Jurisdiction rules do not travel cleanly. If treatment differs by country, mixed-use allocation is unclear, or your team cannot document the basis for a claim, escalate before filing and get local professional advice. This guide focuses on the operating choices you control: categorization rules, review gates, evidence standards, and escalation paths. Related: A Guide to Deducting Business Travel Expenses.

Define the terms and the operating model early#

Start by treating this as a recordkeeping control first and a coding tool second. Your tracking and categorization workflow should clearly show income and expenses (and related deductions and credits), with supporting documents retained where substantiation requires them.

- Tax deduction tracker: Your recordkeeping system for tax reporting and substantiation.

- Deductible category: A category used only when an expense can meet the IRS ordinary-and-necessary standard.

- Exception queue: Transactions held because key support is missing or unclear.

- Escalation trigger: A rule that stops routine processing and routes an item for specialist review.

Use a practical operating sequence, even though the IRS does not require one exact order:

- Receipt scanning and capture

- Bank account import and business credit card import

- Categorization

- Review

- Filing support assembly

This order keeps imports and evidence aligned. In practice, the business checking account is often the main source for book entries, but imported data should not clear review until records support the transaction and the business purpose is clear.

Do not assume an expense report by itself is enough audit evidence. It is a summary. Substantiation generally depends on supporting documents such as receipts, paid bills, invoices, and canceled checks, and sometimes multiple records are needed to support all elements. Evidence expectations are stricter in areas like travel, gifts, and auto expenses, and documentation standards are often tighter for many expenses at or above $75 under 26 CFR substantiation rules.

The control objective is simple: maximize legitimate deductions while reducing false-positive claims. If evidence is incomplete, hold the item for review.

Decide system boundaries and ownership before you configure tools#

Set ownership before you configure tools. Your system should make routine categorization efficient, but tax treatment calls need named accountability. If ownership is vague, convenience usually wins over substantiation. The filer still carries the risk because taxpayers remain responsible for what is on the return, even when a preparer is involved.

Use named owners, not team aliases. Assign one owner for category policy, one for review operations, and one for final filing sign-off. A shared inbox can collect intake, but each exception and approval should map to a specific person. You should be able to show who set the rule, who reviewed the item, and who approved it.

Draw a clear boundary between what your tools handle and what goes to a tax preparer or tax specialist. Keep standard capture, bank import matching, and settled rules in tooling. Escalate calls that depend on legal interpretation, timing, or jurisdiction. If an item may turn into an IRS dispute, route it to a credentialed EA, CPA, or attorney.

| Area | Tooling boundary | Review boundary |

|---|---|---|

| Home office deduction | Do not auto-approve mixed-use space. | Where exclusive-use rules apply, mixed personal/business use can block deduction treatment. |

| Business travel expense deduction | Keep routine categorization in-system. | Require manual review when business purpose is weak, personal days are mixed in, or an assignment may run past one year; keep time, place, and business-purpose records with the item. |

| Startup cost deduction | Keep standard coding in-system. | Escalate pre-opening spend and timing questions; immediate deduction is capped at $5,000, reduced when start-up expenditures exceed $50,000, with the remainder generally amortized over a 180-month period starting when the active trade or business begins. |

Set one escalation rule from day one: if treatment changes by country, treaty position, or state conformity, stop auto-processing and route the item for specialist review before filing.

Build a category policy matrix your team can actually run#

A workable policy matrix should combine evidence requirements and routing rules in one place. That lets reviewers decide quickly and consistently. The IRS does not require a single bookkeeping method, but your system must clearly show income and expenses and be supported by records, so category labels alone are not enough.

Keep the matrix tool-agnostic. Whether intake starts from receipt scanning, bank feeds, or card imports, each category should require a source document, a transaction summary in your books, a review path, and an escalation trigger. An Expense report is a summary layer, not a substitute for receipts, invoices, paid bills, or canceled checks.

| Category name | Required evidence | Auto-allowed or manual-only | Escalation trigger | Deductibility status |

|---|---|---|---|---|

| Ordinary operating expense | Legible receipt scan or invoice, matched transaction summary, complete Expense report with business purpose and payee | Auto-allowed only after repeated reviews show consistent evidence quality | Unreadable scan, missing payee, duplicate-looking charge, or category mismatch | Likely deductible |

| Business travel | Documentary evidence plus complete Expense report with business purpose, dates, destination, and approver | Manual-only unless narrowly defined and low risk | Mixed personal days, vague business purpose, or incomplete travel details | Needs more documentation |

| Mileage tracking | Records that substantiate business-use miles, with linked transaction summary when reimbursements apply | Manual-only | Personal and business miles mixed, missing mileage records, or rate treatment unclear | Needs more documentation |

| Mixed-use spend | Receipt or bill, allocation note showing business-use portion, support for the split basis, complete Expense report | Manual-only | Unclear allocation method, unsupported split, or full-amount claim on mixed-use item | Hold for specialist review |

| New or unmapped category | Source document, draft category rationale, complete Expense report, reviewer note | Manual-only by default | Jurisdiction-specific treatment question or repeated reviewer disagreement | Needs more documentation |

Two rows should stay high-control by default. For Mileage tracking, travel and auto categories need stricter substantiation, and when use is mixed, only the business-use portion is deductible. If you use the standard mileage method, reference the 2025 business rate of 70 cents per mile and keep records that support which miles were business miles.

For mixed-use spend, block full-amount claims unless business-use allocation is documented clearly. A receipt alone is not enough. The allocation logic should be clear enough that a reviewer can explain it plainly.

Make capture quality explicit in policy. Receipt scanning should be readable enough to confirm merchant or vendor, date, and amount, and the image should remain linked to the transaction summary. For electronic records, keep integrity controls so records remain accurate and reliable over time.

Apply the same standard to the Expense report. Mark it incomplete if business purpose, category rationale, or approver is missing. For travel and auto items, route incomplete entries to Needs more documentation automatically.

Use one internal three-state field on every decision:

- Likely deductible

- Needs more documentation

- Hold for specialist review

This is an operating control, not an IRS taxonomy. It separates missing-document issues from items that need specialist judgment.

Default new categories to manual review. Move to auto-allowed only after real transactions show stable evidence quality in your own reviews. There is no IRS-approved false-positive threshold, and the taxpayer keeps the burden of proof.

If mileage is one of your highest-error categories, validate your allocation assumptions before policy sign-off with the mileage deduction calculator.

Design capture and ingestion controls that reduce downstream cleanup#

Once the policy matrix is set, fix intake before you worry about smarter categorization. Most cleanup starts upstream with weak capture, partial imports, and duplicate records.

Set a minimum bar for what counts as captured#

Only send an item to auto-categorization when a reviewer can verify the core fields consistently. Supporting documents should identify the payee, amount paid, proof of payment, date incurred, and a description. Use a minimum capture standard:

- supporting documentation is readable enough to confirm payee, date, amount, and proof of payment

- merchant name is normalized to one approved form

- transaction currency is stored consistently, with translated USD amounts shown separately when your books are in U.S. dollars

- supporting documentation stays linked to the transaction summary and any later reimbursement record

Electronic records are valid, but they carry the same baseline requirements as paper records. Your storage system should preserve integrity, accuracy, reliability, security, retrieval, and readable reproduction over time.

Stage imports before any category job runs#

Run categorization only after imports are complete and reviewed. A practical sequence is to import bank and card transactions, stage them in a review queue, run duplicate and matching checks, and then allow category suggestions.

If both Bank account import and Business credit card import are active, finish the feed update window before categorization. If your provider refreshes on a roughly 24-hour cycle, set review cutoffs after that cycle to avoid partial-data exceptions.

Block duplicate spend before it hits the ledger#

Duplicate posting can become a tax control issue, not just bookkeeping hygiene. Common failure modes include manual statement imports plus bank-feed imports, or receipt-to-card merge failures.

Before posting, check for near matches on amount, date, merchant, and currency. Keep thresholds as internal control settings, not legal standards. Tool rules like a seven-day receipt-to-card window or a 5 percent FX tolerance are product logic. When matching is unclear, route the item to exception review.

Reimbursements need a second link check. Tie each reimbursement to the underlying expense and confirm substantiation, because reimbursement treatment can fail when expenses are not substantiated or excess amounts are retained.

Force visible exceptions for unmapped imports#

When an imported transaction cannot map cleanly to an approved category, stop auto-posting and require an explicit exception state. The label can vary, but it should be sortable and aging-friendly, for example unmapped merchant, mixed-currency review, duplicate suspect, reimbursement pending, or insufficient supporting-document quality.

Do not let vague merchant data, missing currency-translation support, or unreadable supporting documents flow into generic expense buckets. Hold the record in queue until the evidence is complete and the transaction can be explained clearly.

Set automatic and manual categorization rules with explicit guardrails#

After intake quality is stable, keep auto-categorization narrow, evidence-first, and easy to reverse. If documentation is missing or the match is not clearly explainable, route to manual review even when automation suggests a category.

Pick rule types by signal reliability, not convenience#

Merchant rules are often a conservative default. Amount-pattern and keyword rules can help, but they need tighter guardrails because they can catch unrelated spend.

| Rule type | Good fit | Auto-post only when | Block from auto-posting when |

|---|---|---|---|

| Merchant rule | Stable recurring vendors with one usual business purpose | Merchant name is normalized, the vendor consistently maps to one approved category, and the linked receipt or bill supports the treatment | Merchant aliases are inconsistent, the same vendor can produce mixed-use spend, or documentation is missing |

| Amount-pattern rule | Repeating charges with a distinctive amount | The amount reliably maps to one recurring expense and does not overlap with reimbursements, transfers, or multiple categories | The same amount appears across categories or matching context is unclear |

| Keyword rule | Specific, stable text in description or bank text | The keyword is narrow and paired with complete evidence | The text is generic, appears in multiple contexts, or the item lacks readable supporting documentation |

Use merchant logic as the primary rule, then add amount or keyword conditions as support rather than as catch-alls. Rule builders can be flexible, but that flexibility also increases the chance of brittle matches.

Hard gates should override any suggestion#

Deduction treatment depends on substantiation, so categorization cannot be the final authority on a tax write-off. If evidence is incomplete or unclear, stop auto-posting and require manual approval. Use a hard stop when any of these are true:

- supporting documentation is missing or unreadable

- core transaction details are incomplete

- business purpose is unclear

- the item may include personal or mixed-use spend

- suggested category conflicts with the supporting document

This gate should apply even when a suggestion looks strong. As one Head of Compliance put it, "I think human involvement has to be mandatory."

More automation increases throughput and mistake scale#

Automation can improve speed and consistency, but weak controls can scale errors just as quickly. Start with simple, consistent recurring transactions, keep daily review active, and expand conservatively as evidence quality stays stable.

Broad keyword rules can catch unrelated transactions, and seemingly clean merchant rules can fail when a vendor's charges span deductible and nondeductible uses. Prioritize explainability before speed, because records still need to support filed deductions.

Restrict rule changes and keep rollback routine#

Limit rule creation and edits to admin-level owners, with tax or compliance approval on rule intent. Keep a simple change log with the rule name, priority, old logic, new logic, requester, approver, effective date, and reason.

Priority order matters because higher-priority settings can override lower-priority outcomes. For rollback, keep versioned rule sets, restore the prior version when misclassification appears, and re-review transactions affected during the change window.

Related reading: Using Wise 'Jars' to Automatically Set Aside Tax Money for Multiple Jurisdictions.

Handle mixed-use and high-risk categories without guesswork#

Mixed-use and timing-sensitive items should default to manual review. Do not claim them unless the allocation logic is written and defensible. If you cannot document the method clearly, hold the item for specialist review.

| Category | Key rule | Documentation |

|---|---|---|

| Home office deduction | A specific area must meet exclusive use and regular use; if that area is also used for personal living, the claim is generally not supportable for that portion of the home. | The specific area claimed, why it meets exclusive and regular use, which expenses are direct vs. indirect, and how the business-use percentage was calculated |

| Business travel expense deduction | The expense must be ordinary and necessary, tied to travel away from home for business, and supported by records; personal travel costs are not deductible. | Records that show who traveled, when, and why the trip was business-related |

| Startup cost deduction | The rules apply in the taxable year the active trade or business begins; up to $5,000 may be immediately deductible, reduced when startup expenditures exceed $50,000, and the remainder is deducted ratably over 180 months. | Invoice and payment support, plus a dated note explaining why the item is a startup expenditure rather than an operating expense |

These categories often break down for predictable reasons: business purpose is unclear, records are too vague to support treatment, or the allocation percentage cannot be explained later. In those cases, keep the hard stop.

Home office needs more than a home address#

For the U.S. Home office deduction, start with eligibility: a specific area must meet exclusive use and regular use. If that area is also used for personal living, the claim is generally not supportable for that portion of the home.

Then classify expenses correctly under the regular method. Direct business expenses can be deducted in full, while indirect home expenses must be allocated by business-use percentage. Require a short record that shows:

- the specific area claimed for business use

- why it meets exclusive and regular use

- which expenses are direct vs. indirect

- how the business-use percentage was calculated

If the file only shows a flat percentage without item-level support, do not claim it.

Travel must be tied to business, not just movement#

For the U.S. Business travel expense deduction, the expense must be ordinary and necessary, tied to travel away from home for business, and supported by records. Personal travel costs are not deductible.

Use a simple checkpoint: can you match each charge to a clear business purpose and supporting records? Generic merchant descriptions or summary card lines should stay in review until the records show who traveled, when, and why the trip was business-related.

Block auto-approval when you see:

- no stated business purpose

- mixed personal and business itinerary

- family or companion costs combined with business bookings

- allocation based on memory instead of records

If business and personal portions cannot be separated from the available records, do not convert uncertainty into a tax write-off.

Startup spending is a timing problem as much as a category problem#

For U.S. Startup cost deduction treatment under IRC §195, timing is part of the test: the rules apply in the taxable year the active trade or business begins. Up to $5,000 may be immediately deductible, reduced when startup expenditures exceed $50,000, and the remainder is deducted ratably over 180 months.

Review two points together: what the cost was, and when the active trade or business began. Keep invoice and payment support, plus a dated note explaining why the item is a startup expenditure rather than an operating expense. Do not treat all early spending as immediately deductible in full.

For related guidance, see Using a Tax Home to Deduct Travel Expenses as a U.S. Domestic Nomad.

Build an audit evidence pack before filing season pressure hits#

Build the evidence file when you categorize each expense, not at filing time. If a claim cannot be tied to documentary evidence and a clear business explanation, it is not filing-ready, even if it appears in an Expense report.

For each deduction, keep one bundle with five items: source receipt or bill, business purpose note, category rationale, reviewer approval (when your process requires review), and the final Expense report link. The first three support the return position. Reviewer approval and report linkage are internal control records that show who accepted the treatment and where it landed. Supporting documents remain the foundation for both your books and your tax return.

Write the business purpose note so it can verify amount, time, place, and business purpose in one read. For travel, entertainment, gifts, and auto expenses that need additional substantiation, a stored receipt alone is often not enough. If a merchant line is vague, require a note that makes the business context clear.

Separate filing records from operating records#

Keep a clean split between what feeds tax filing software and what stays in internal logs.

| Record type | What belongs here | Typical destination |

|---|---|---|

| Filing records | Receipt, invoice, bill, business purpose note, category rationale, final amount claimed | Tax filing software or return support folder |

| Operational records | Queue status, exception tags, reviewer assignment, follow-up requests, duplicate check results | Internal audit log or tax deduction tracker |

| Sensitive approval history | Reviewer comments, approval timestamps, override history, access logs | Restricted internal records |

This keeps the filing package focused on return support while preserving internal review history with tighter access.

Retention and access need explicit rules#

Set retention by the period of limitations, not by a blanket "seven years" rule. A common baseline is 3 years. It can extend to 6 years when omitted income exceeds 25% of gross income shown on the return, and there is no limit for a fraudulent return or no valid return. Electronic records must meet the same standards as paper records.

Set access controls up front for sensitive tax records, including reviewer comments and approval history. In covered FTC Safeguards Rule contexts, access should be limited to authorized users who need the data. Customer information should also be securely disposed of no later than two years after last use, subject to rule exceptions.

Use a hard completeness test#

Use a binary release gate: no deduction is ready if any required artifact is missing.

- source document is present and legible

- business purpose note can verify amount, time, place, and purpose

- category rationale matches policy

- reviewer approval is recorded when review is required

- final linkage to the Expense report and filing support is complete

Partial files can fail substantiation even when some documents are present. If your process cannot pass this completeness test, keep the item pending rather than treating it as deductible.

For a step-by-step walkthrough, see What is the difference between a 'tax deduction' and a 'tax credit'?.

Run month-end verification and escalation checkpoints#

At month-end, do not sign off until each deduction candidate is tied to captured transactions, resolved exceptions, and a documented decision.

A consistent close checklist makes that workable. Tax rules do not require one universal checklist format, but they do require supportable records, and control guidance expects follow-up and timely remediation of gaps.

Use one checklist and make each item testable#

Run the same four checks every close period:

| Close check | What to confirm |

|---|---|

| Uncategorized transaction count | Owner and status for each open item |

| Exception aging | Stuck items are visible before they become filing risk |

| Reimbursement reconciliation | Reimbursements have a business connection, are substantiated, and any excess amounts are returned |

| Mileage tracking completion | Mileage tracking completion (or other adequate records) for any vehicle-related deduction position |

Record counts and dispositions together. A defensible control record shows what stayed open, who owned it, and whether it was held from deduction pending support.

Reconcile imports before final approval#

Before final review, reconcile captured transactions to Bank account import and Business credit card import totals. Reconciliation is a control activity, and differences should be followed up, investigated, resolved, and documented.

Check each feed for period coverage, transaction count, and total posted amount. Separate timing differences from true breaks, and hold sign-off until every variance has an explanation.

Set and enforce escalation cutoffs#

Unresolved high-risk items should not roll forward indefinitely. There is no one universal legal escalation deadline for every organization, so set a close cutoff (or close plus a short review window) in your policy and route unresolved items to compliance, a tax specialist, or counsel by that date.

Use explicit escalation triggers, such as missing support, unclear business purpose, or incomplete mileage substantiation. For each escalated item, keep the owner, escalation date, decision, and whether it was excluded from the current deduction set.

Feed recurring failures back into policy#

Recurring issues are a policy signal, not just cleanup work. If the same mismatch or documentation gap appears each month, update the policy matrix, tighten evidence requirements, or move that category to manual review until error rates improve.

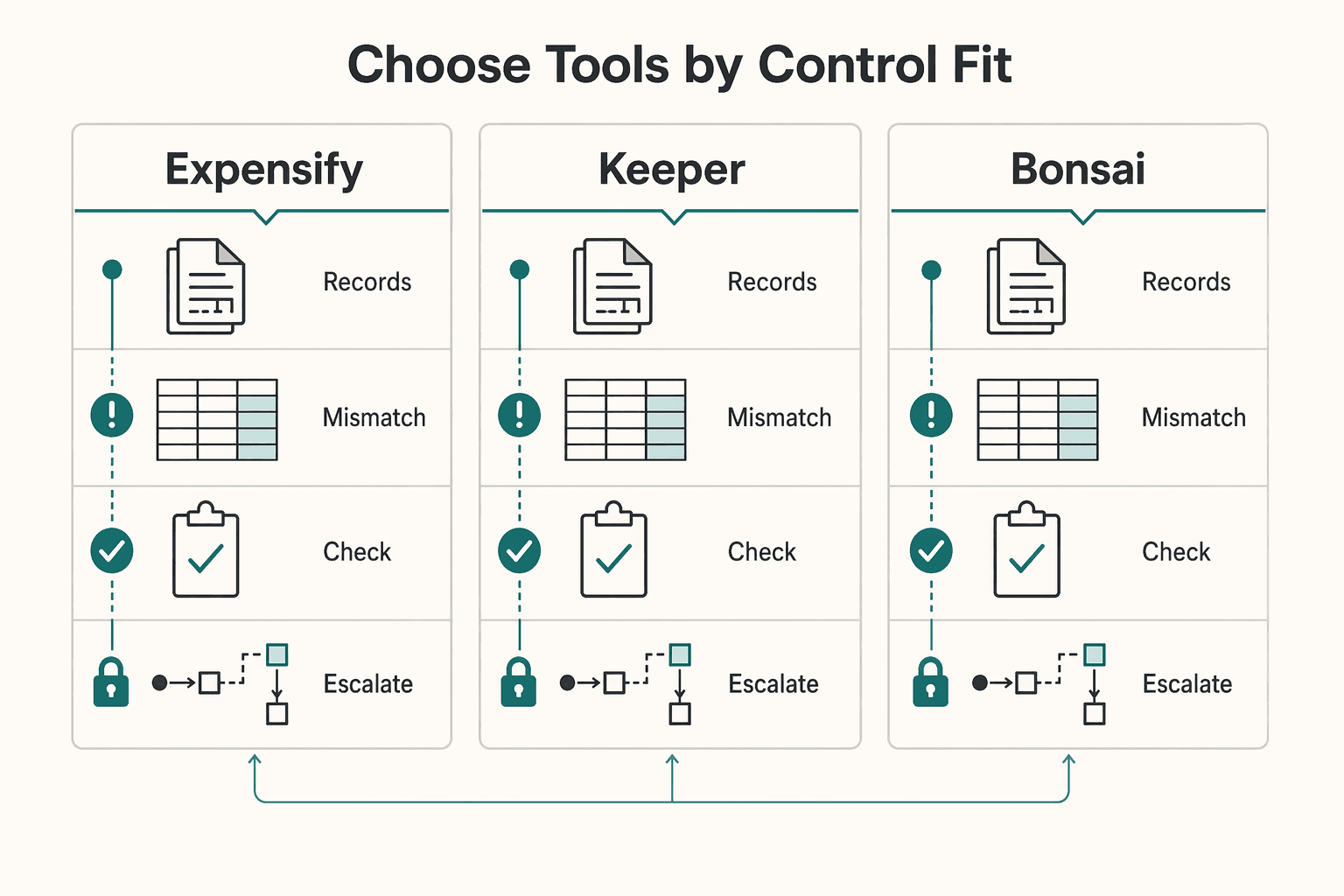

Choose tools by control fit, not by marketing claims#

Choose the tool that enforces your approval flow and keeps evidence intact across handoffs when you test it. If you cannot verify that, it is not a fit for compliance-led operations, regardless of demos, rankings, or app-store momentum.

| Tool | Grounded strength | What you still need to verify |

|---|---|---|

| Expensify | Supports single-approver and multi-level approval chains, including a second approval for reports over a set amount, and can lock the approval path unless a Workspace Admin overrides it. | When data moves through integrations or into your tax filing workflow, do receipt images, business-purpose notes, approver names, and approval dates stay linked to each transaction? |

| Keeper | Markets an AI-plus-human accountant model and says every return is reviewed and signed by a tax pro. | Does that review layer preserve your internal approval history, exception notes, and category rationale, or only produce a filed-return outcome? |

| Bonsai | Describes bank/card auto-import, classification/tracking, and sync with QuickBooks Online and Xero. | Can you require manual review for high-risk categories, and do synced records carry attachments and review comments rather than only coded totals? |

Use Forbes Advisor and Nav as discovery inputs, not as selection criteria. Both publish top-app recommendations and both disclose partner compensation.

Treat Apple App Store ratings as usability signals, not compliance signals. Apple frames ratings and reviews as customer experience feedback. Summary ratings are territory-specific, can be reset on a new version, and are refreshed at least weekly when enough reviews exist. A 4.8 for Keeper or 4.6 for Expensify may indicate user satisfaction, but not audit-defensible controls.

Run a hands-on control test before selection: submit one expense through approval, sync or export it onward, and inspect the destination record. If the handoff drops receipt files, reviewer identity, override history, or evidence links, you have identified the real risk.

Apply the model in cross-border payment operations with Gruv#

Use Gruv as your record spine for cross-border payments so categorization, approval, and payout evidence stay traceable end to end. Gruv states it keeps an audit trail for operational workflows, supports exportable evidence packs, and links transactions to contracts, invoices, and payment proofs in a searchable, export-ready ledger.

That traceability matters because deduction support depends on proof. The IRS standard is direct: you must be able to prove certain elements of expenses to deduct them, and electronic records must be complete, accurate, and accessible. If categorization sits in one system, approvals in another, and payout proof in a third, you can create avoidable evidence gaps before filing.

Use Gruv as the end-to-end evidence link#

The core control is traceability, not a clean-looking expense report. For each claimed business expense, verify that you can follow the chain from supporting document through approval to payment record.

Use a live sample transaction and confirm the destination record still includes:

- Business-purpose context

- Approval status

- Linked invoice or contract

- Payment proof

If any link breaks, your team may be forced into manual reconstruction during close.

Align deduction review with market and program gates#

Do not apply one approval rule across all markets. Gruv states that coverage, methods, and timelines vary by market and are subject to compliance and policy checks, and that tax and compliance features vary by jurisdiction and customer configuration.

Set your review rule accordingly: when support requirements or treatment depend on country, program, or customer setup, route the item for specialist review before it moves into tax filing workflows. This matters more as cross-border regulatory requirements continue to increase.

A common failure mode is treating coverage as static. Instead, attach explicit market or program qualifiers to the review step so exceptions are visible before filing.

Reconciliation exports can reduce close surprises when used early#

Gruv states it supports reconciliation-friendly exports and integration modes including APIs, webhooks, and file exports. Use those outputs before close, not only after exceptions surface.

If your accounting integration receives totals while detailed proofs remain in Gruv, run a recurring match process that ties booked amounts back to exportable evidence packs. Start with high-volume categories that already have standardized supporting documents and clear exception handling, then expand only after exception rates are stable.

Keep the retention rule in view: records must be kept as long as needed to prove income or deductions. In practice, retention should cover receipts and invoices, plus approval and payout evidence that supports why each entry was accepted.

Conclusion#

Use a tax deduction tracker categorize expenses workflow as a recordkeeping aid, not as proof by itself. Better outcomes come from clear policy, complete evidence, and escalation when treatment depends on jurisdiction or specialist judgment.

The core standard is substantiation. You should be able to tie each claim to underlying records and explain why it was treated that way. Record format is flexible, but record clarity is not. Your process should show income and expenses clearly, reconcile what moved through accounts, and catch weak claims before filing.

If you want the shortest useful next step, do three things in order:

- Build the category matrix.

Define category status, required evidence, auto-post versus manual review, and escalation triggers, including jurisdiction-specific handling.

- Run a verification cadence.

Use a recurring check that fits your business (for example, daily, weekly, or monthly) to reconcile expenses to bank and card activity, clear uncategorized items, resolve exceptions, and confirm source records are attached.

- Validate escalation paths by market.

Confirm who owns edge-case decisions, what cutoff applies for unresolved items, and what documentation specialists require before sign-off.

Before treating anything as filing-ready, verify traceability from the summary line to the source document, category rationale, and supporting records. Retention rules also vary. IRS baselines can be 3 years, at least four years for employment tax records, and up to 6 or 7 years in specific cases. ATO guidance uses a 5-year baseline with longer periods for some records, and UK guidance requires accurate records that identify business transactions.

The takeaway is simple: policy, evidence, and escalation discipline drive defensible deductions, not app features alone. If you need policy-gated approvals, payout traceability, and audit-ready records where supported, talk to Gruv to confirm coverage for your program.

Frequently Asked Questions

How does a tax deduction tracker categorize expenses automatically without increasing audit risk?

Use automation only for repeat expenses with a stable pattern and complete documentation already attached. If merchant detail is vague or records are missing, route the item to manual review. Do not treat "IRS-compliant report" marketing language as proof that the output is accepted on its own.

What should be auto-categorized and what should always stay in manual review?

Auto-categorize recurring, low-judgment expenses with consistent merchants and predictable documentation. Keep mixed-use and higher-substantiation categories in manual review, including home office, travel, vehicle expenses, and mileage-related items. Also keep manual review where jurisdiction differences can change treatment.

What records are required to defend a deduction during an audit?

You generally need documentary evidence such as receipts, canceled checks, bills, and similar source records. A summary report alone is not enough if it cannot be tied to those records. For travel, gifts, and auto expenses, keep stronger substantiation and business-purpose support with the underlying documents. Retain records as long as needed to prove deductions. Common IRS anchors include 3 years for general assessment, at least 4 years for employment tax records, and 7 years for certain bad-debt or worthless-securities refund claims.

How should teams handle expenses that are partly business and partly personal?

Split mixed-use expenses between business and personal use instead of posting the full amount as business. Personal, living, or family expenses are generally not deductible. If the allocation method is not well documented, hold the claim for specialist review.

What month-end checklist best confirms deductions are complete before filing?

There is no single mandated checklist for every jurisdiction, so use a consistent close routine. Reconcile expense captures to bank and card activity, clear uncategorized items, verify each claimed item has source records and a business-purpose note, and confirm mixed-use items are allocated between business and personal use. If using the IRS standard mileage method, confirm business miles before applying the 2025 rate of 70 cents ($0.70) per mile.

When should finance escalate an expense decision to tax or legal specialists?

Escalate when treatment depends on jurisdiction or judgment you cannot support with records. Typical triggers include mixed-use allocations, travel that appears partly personal, unclear merchant descriptions, and missing substantiation. The IRS Interactive Tax Assistant can help with basic tax-law questions before escalation. Using an external preparer also does not transfer taxpayer responsibility for return information.

What is the minimum policy set for cross-market expense categorization?

Start with five written rules: required evidence by category, categories allowed for auto-posting, categories that are manual-only, escalation triggers for jurisdiction differences, and retention requirements. Add market qualifiers so teams do not apply one country's treatment to another. Keep one explicit boundary: personal expenses are generally non-deductible, and mixed business/private costs are claimable only for the business portion.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- apps.irs.gov/app/IPAR/resources/help/ordnec.htmltrusted

- ato.gov.au/businesses-and-organisations/income-deductio...trusted

- business.gov.au/finance/tax/tax-deductionstrusted

- irs.gov/taxtopics/tc305trusted

- irs.gov/newsroom/tips-for-choosing-a-tax-professionaltrusted

- sao.wa.gov/bars-annual-filing/bars-gaap-manual/accounti...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Home Office Deduction for Real Estate Agents: Qualify, Choose a Method, and Keep Records

If you file Schedule C, the key question is not whether this deduction looks aggressive. It is whether you can prove you qualify, choose the right method for that tax year, and support the claim with clean records.

A Guide to Deducting Business Travel Expenses

**For deducting business travel expenses, use a repeatable compliance system so you only claim costs you can prove.**

How to Deduct Startup Costs for Your Freelance Business

**If you want to claim startup costs safely, run a system that classifies each expense, confirms business start timing, applies startup deduction and amortization rules, and saves proof for every decision.**