Quick Answer

To deduct freelance startup costs safely, use a compliance-first system: classify each cost, confirm when your business actually began, apply startup deduction and amortization rules, and keep proof for every decision. The article’s framework emphasizes defensibility over shortcuts, including clear verification points, audit-ready documentation, and separate checks for state and cross-border filings before you submit.

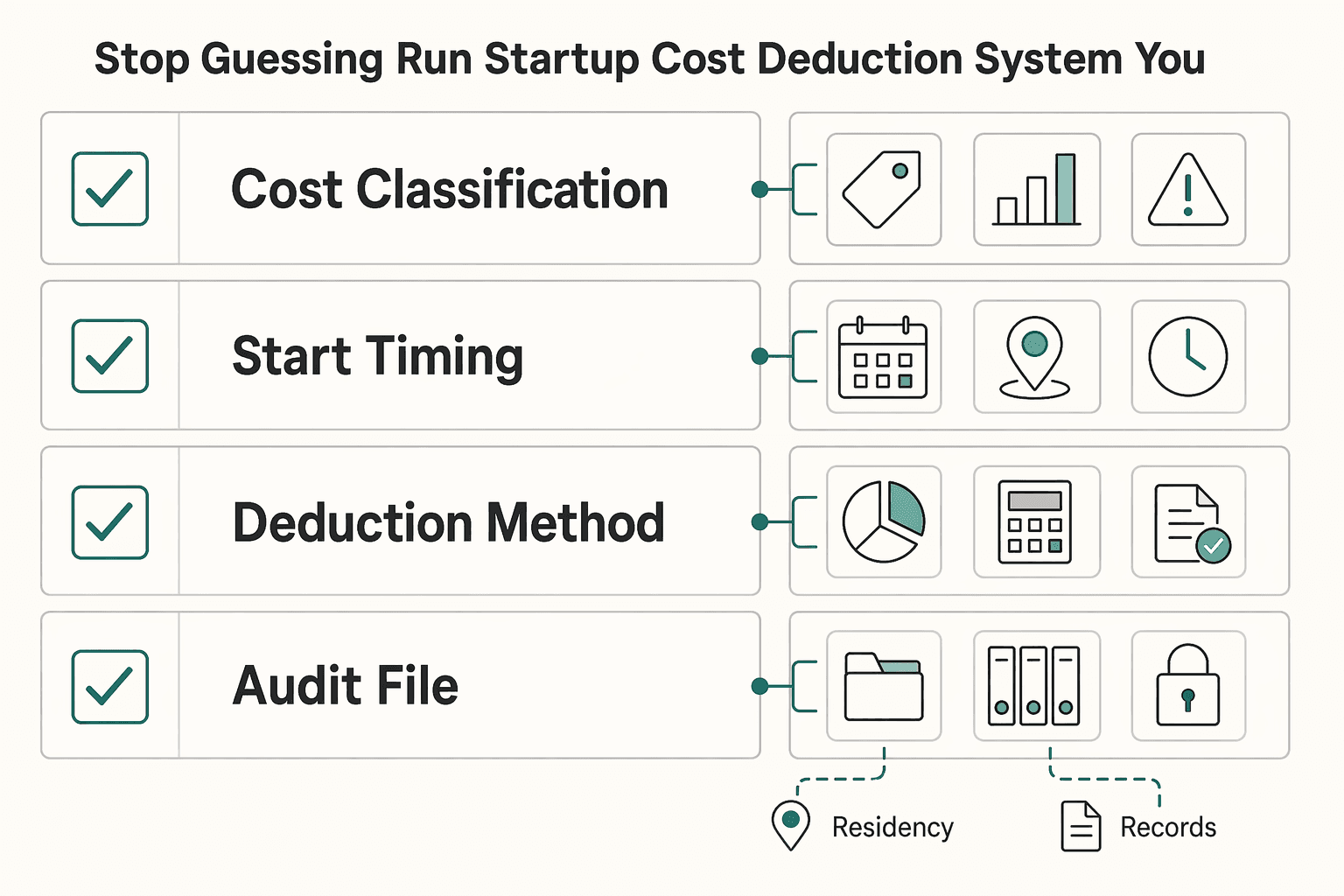

Stop guessing and run a startup cost deduction system you can defend#

If you want to claim startup costs safely, run a system that classifies each expense, confirms business start timing, applies startup deduction and amortization rules, and saves proof for every decision.

You are the CEO of a business-of-one. Treat taxes like operations. Define rules once, run them consistently, and keep an audit file that matches your decisions.

Most list-style advice creates risk for globally mobile operators because it blurs timing, classification, and jurisdiction. What holds up is an IRS-first workflow that lowers taxable income through valid business expenses. It also avoids rework when the IRS, a state agency, or a residency reviewer asks questions.

Before you start: Treat this guide as federal workflow design, then layer local rules. State and cross-border treatment can differ, including California and FTB residency or source-income checks.

| Decision area | Safe default | Why it lowers risk |

|---|---|---|

| Cost classification | Tag each item as startup or ongoing business expenses | Stops over-claiming and cleanup later |

| Start timing | Document when your active trade or business begins | Aligns Section 195 timing with your records |

| Deduction method | Apply available current startup deduction and amortize remaining eligible costs | Balances current tax benefit and defensibility |

| Audit file | Save receipt, date, business purpose, and rationale | Speeds responses to IRS or state inquiries |

- Step 1. Classify every cost line by line. Test each item against the ordinary and necessary standard before it enters your filing workflow. Verification point: every line includes a business purpose and a clear category.

- Step 2. Confirm when the business actually began. Section 195 ties deduction timing to when the active trade or business begins, not just when cash lands. Verification point: keep dated records that support when operations began.

- Step 3. Apply startup deduction and amortization on purpose. IRS guidance allows an election to deduct up to $5,000 of startup costs, that allowance is reduced when costs exceed $50,000, and remaining eligible amounts are recovered over a 180-month period through amortization. Verification point: write a short rationale tied to expected taxable income and freelance tax planning.

- Step 4. Build an audit-ready file now. Store support in one place so you can answer IRS, state, and residency questions fast. If you move jurisdictions midyear, federal startup-cost treatment and state sourcing treatment can differ.

If you have state mobility risk, review Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad? before you file.

What should you prepare before you touch your tax return?#

Build one complete prep file before you open your return so your startup-cost classifications stay defensible.

The core move is simple: build clean inputs first, then make classification calls. That order prevents late-week filing decisions you cannot explain later.

Before you start#

- Step 1. Consolidate one expense log. Put every item in a single ledger with invoice or receipt, date incurred, payee, amount paid, proof of payment, and business purpose. Add a short description of what you purchased or received. This lets you test each line consistently and tie it to business expenses.

| Field | Why it matters at filing time |

|---|---|

| Date, payee, amount, proof of payment | Supports deduction validity and timing |

| Description and business purpose | Shows business-expense character |

| Startup or ongoing tag | Prepares consistent classification decisions |

-

Step 2. Split startup-era costs from active-operating costs. Tag early items now, not during filing week. Use clear labels for review buckets such as opening advertising, trainee wages and instructors, and travel to secure prospective distributors, suppliers, or customers. Treat tags as checkpoints, not automatic deductions. For example, opening advertising can fit startup treatment, while deductible interest, taxes, and research or experimental costs follow separate treatment.

-

Step 3. Assemble filing anchors for tax and state checks. Prepare Schedule SE inputs, prior-year self-employment records, and current-year net earnings notes. Schedule SE is used to compute self-employment tax, and you generally must file it when line 4c is $400 or more.

In parallel, keep California notes for part-year and nonresident review. Treatment can depend on residency period and California-source income, so separate those records clearly.

- Step 4. Build your evidence folder structure now. Create folders by tax year, then by category (startup, ongoing, state, Schedule SE). Save every classification memo with the document it relies on.

Hypothetical example: if you worked abroad for part of the year and signed a client while physically in California, store the location and contract records together. That way, your IRS file and state file tell the same story.

Are your costs truly startup costs or just ongoing business expenses?#

Classify each cost by timing and purpose before filing so you protect your startup cost deduction and avoid treating normal operating spend as startup spend.

With records consolidated, run a strict classification pass. This is the gate that keeps your filing position clean and defensible.

Run the two bucket test#

- Step 1. Sort by timing first. Put costs incurred before you actually begin business operations into a startup review bucket. Put costs tied to current delivery and day-to-day operations into ongoing business expenses.

- Step 2. Test business purpose second. Keep only items that are ordinary and necessary for the business activity you run. If an item looks personal, mixed, or weakly connected, flag it for conservative treatment.

- Step 3. Apply edge rules line by line. Use one decision table so you do not inflate a startup cost deduction.

| Item type | Startup bucket signal | Ongoing expense signal |

|---|---|---|

| Advertising | Opening ads before operations begin | Recurring campaigns after launch |

| Travel | Pre-launch travel tied to starting the business | Travel during operations, with business and personal portions separated when use is mixed |

| Legal or accounting fees | Pre-opening setup work | Ordinary and necessary fees directly related to operating the business |

| Software | Pre-launch setup tied to business formation activities | Active subscriptions used to run client delivery |

| Workspace | Setup decisions before launch | Home office deduction during operations if you meet exclusive use rules |

- Step 4. Keep home office separate from startup-only logic. The home office deduction is not a startup-only category. If you choose the Simplified Home Office Deduction, use the fixed method of $5 per square foot, up to 300 square feet. Apply it only to qualifying business-use space.

Use a hard stop before you finalize#

Before you enter a line on your filing list, run this final gate:

- Confirm the bucket: startup or ongoing.

- Confirm the purpose: ordinary and necessary for business use.

- Confirm the treatment: current deduction or other treatment required by your startup-cost rules.

- Confirm the support: receipt, date, payee, and business rationale.

Hypothetical example: you pay for opening ads before launch and then continue monthly ads after launch. Classify the first set as startup review items and the later set as ongoing business expenses, then document both decisions in your file.

When can you start deducting startup costs if revenue has not arrived yet?#

You can set startup-cost timing before revenue arrives once your business begins operating, as long as you document the start date and apply it consistently.

This is your timing gate. Do not tie it to cash receipt if your services are already live and your business is already functioning.

Run a date proof protocol you can defend#

- Step 1. Set one start trigger date. Choose the date your business starts to function as a business in practice. Keep this as a single control date for your tax file.

- Step 2. Build a timing evidence packet. Save records that support the trigger event and your reporting positions, such as contracts, invoices, receipts, canceled checks, and related business records. Add a short memo explaining why this date marks active operations.

- Step 3. Classify costs around that date. Treat pre-start items as startup-cost review items, then decide startup-cost treatment, including amortization election where required. Treat post-start items as ongoing business expenses under general business-expense rules.

- Step 4. Reconcile timing to tax workflow inputs. Use the same trigger date when you build Schedule C support and self-employment tax support so your records do not conflict later.

| Timing question | Safe operator rule |

|---|---|

| No revenue yet, but services are live | Do not auto-delay classification. Use your documented start trigger. |

| Expense incurred before start trigger | Keep in a startup review bucket for startup-cost treatment or amortization decision. |

| Expense incurred after start trigger | Treat as an ongoing business expense under general business-expense rules. |

Schedule SE does not set your business start date. Your timing choices can still affect your self-employment tax workflow. If net self-employment earnings reach the filing threshold ($400 or more), Schedule SE becomes mandatory, so mismatched dates can create rework.

Hypothetical example: you launch your consulting offer, sign a client, and deliver work before payment clears. Use the launch and signed engagement evidence to support your start date, then classify costs using that same date so your tax file stays coherent.

Should you take the startup cost deduction now or use amortization?#

Take the startup cost deduction now when you need near-term relief and your classifications are clear, and use amortization when you want steadier deductions across future years.

With your start date locked, make a deliberate timing choice. This is where clean files either stay clean or turn into future cleanup.

Make the call with a defensible sequence#

Taxable income equals gross income minus allowed deductions, so this choice changes when deductions hit your return.

| Check | What to review | Key detail |

|---|---|---|

| Startup pool | Separate true startup items from ongoing business expenses | Then total startup expenditures |

| IRS limit | Apply IRS limits before choosing | $5,000 immediate amount is reduced when startup expenditures exceed $50,000 |

| Lower income now | Compare business trajectory, not just this return | If you expect lower taxable income now and stronger income later, spreading deductions through amortization may fit better |

| Current-year pressure | Compare business trajectory, not just this return | If current-year taxable income is your pressure point, the immediate startup cost deduction may fit better |

| Schedule SE impact | Align with self-employment tax workflow | Classification and timing choices can affect your Schedule SE base through net profit changes |

| Election deadline | Lock your election and escalation rule | Make the election by the return filing deadline for the year the business begins, including extensions |

| Escalation | Use a qualified tax professional when uncertainty is material | If classification uncertainty could materially change self-employment tax outcomes, escalate and document your rationale |

| Option | What you get now | What you commit to later | Best fit |

|---|---|---|---|

| Immediate startup cost deduction | You can elect up to $5,000 in the start year (subject to reduction rules) | You still amortize remaining eligible startup costs | You want more current-year deduction and your records support clean classification |

| Amortization focus | You take less upfront | You deduct remaining startup expenditures ratably over a 180-month period beginning when the active trade or business begins | You want smoother deduction timing and simpler year-to-year consistency |

- Step 1. Confirm your startup pool. Separate true startup items from ongoing business expenses, then total startup expenditures.

- Step 2. Apply IRS limits before choosing. The law reduces the $5,000 immediate amount when startup expenditures exceed $50,000, so run this check first.

- Step 3. Compare business trajectory, not just this return. If you expect lower taxable income now and stronger income later, spreading deductions through amortization may fit better. If current-year taxable income is your pressure point, the immediate startup cost deduction may fit better.

- Step 4. Align with self-employment tax workflow. Schedule SE figures self-employment tax due on net earnings, so classification and timing choices can affect your Schedule SE base through net profit changes.

- Step 5. Lock your election and escalation rule. Make the election by the return filing deadline for the year the business begins, including extensions. If classification uncertainty could materially change self-employment tax outcomes, escalate to a qualified tax professional and document your rationale.

Hypothetical: you open with uneven client demand and uncertain cost categories. Choose the more conservative treatment, document why, and protect audit simplicity first.

How do globally mobile freelancers avoid cross-border filing surprises?#

Map your residency, foreign accounts, and filing forms before you file. FBAR and Form 8938 are separate filing regimes, so treat them as separate checks and keep one evidence trail for federal and state review.

Once your startup-cost workflow is stable, add a cross-border control layer. The goal is one coherent evidence trail, even when federal filing, state residency, and foreign reporting are all in play.

Run a pre-filing cross-border screen#

- Step 1. Map where you lived and worked. List each jurisdiction where you performed services and where your financial accounts sit. Mark any California ties, because California can tax all income while you are a resident and can tax California-source income while you are a nonresident.

- Step 2. Test FBAR exposure first. If your foreign financial accounts exceed an aggregate value of $10,000 at any time during the year, prepare FBAR reporting. File FBAR as FinCEN Form 114, not with your IRS tax return.

- Step 3. Test Form 8938 separately. Do not assume FBAR filing covers FATCA reporting. Form 8938 has its own thresholds and scope. One key difference is that some non-account foreign assets can appear on Form 8938 but not on FBAR.

- Step 4. Calendar deadlines immediately. Set your FBAR timeline for the standard April 15 due date and the automatic extension to October 15, then align this with your return timeline.

| Requirement | FBAR | Form 8938 |

|---|---|---|

| Filing channel | FinCEN Form 114 | Filed with tax return |

| Core trigger | Foreign account aggregate exceeds $10,000 at any time | Threshold based on filing status and residency |

| Scope example | Foreign accounts | Includes some specified foreign assets not reportable on FBAR |

Keep one audit-ready file#

Store cross-border records in the same folder system you use for startup costs, amortization, and business expenses. Use a simple control rule: one decision memo per filing position, plus the document that supports it.

Hypothetical example: you work across countries while keeping a foreign brokerage account. Save account statements, residency notes, and classification memos together. This makes it easier to answer IRS or FTB follow-up quickly.

Related: The Freelancer Year-End Tax Prep Checklist.

Which mistakes create tax rework and how do you recover quickly?#

Reduce tax rework by reclassifying costs by timing, separating startup cost deduction from ongoing business expenses, rebuilding weak records, and escalating cross-border issues before filing.

Mistakes here are rarely about one receipt. They usually come from mixing buckets, skipping timing proof, and trying to patch it after the return is already built.

Run this four-step recovery playbook#

| Problem | Recovery action | Verification |

|---|---|---|

| Timing not separated | Mark each line item as pre-operation or operating, then confirm the business-start month before applying startup cost deduction and amortization rules | Each cost has a timing tag, a business purpose note, and a clear bucket |

| Startup and current expenses mixed | Build a corrected ledger with separate columns for startup costs and ongoing business expenses | You can explain each classification in one sentence |

| Gray-area support is weak | Collect contracts, invoices, receipts, and notes that show amount and business purpose; use conservative treatment if records stay weak | Your support file stays ready for IRS inspection |

| State or global issues unresolved | Review California residency and sourcing exposure under FTB guidance, then test FBAR and Form 8938 separately | Assign one checklist owner and one escalation rule for high-impact ambiguity |

- Step 1. Reclassify early spending by timing first. Mark each line item as pre-operation or operating. Treat pre-operation startup items as capital in nature, then apply startup cost deduction and amortization rules only after you confirm the business-start month. Keep the

ordinary and necessarytest attached to every item. Verification point: each cost has a timing tag, a business purpose note, and a clear bucket. - Step 2. Split startup items from current business expenses. Build a corrected ledger with separate columns for startup costs and ongoing business expenses. Do not mix the two, because one sloppy category creates cleanup later. Hypothetical example: you pay setup costs and deliver client work in the same period, so you still log setup and operating costs in different buckets even when one card statement shows both. Verification point: you can explain each classification in one sentence.

- Step 3. Rebuild support for gray-area items. For opening advertising, legal fees, and other gray-area setup costs, collect contracts, invoices, receipts, and notes that show amount and business purpose. Opening advertising can fit startup treatment, while research and experimental costs follow separate treatment. If records stay weak, use conservative treatment and flag the item for advisor review. Verification point: your support file stays ready for IRS inspection.

- Step 4. Resolve state and global overlays before filing. Review California residency and sourcing exposure under FTB guidance, then test FBAR and Form 8938 separately because one does not replace the other. Update your workflow so federal return tasks and FinCEN filing tasks stay distinct controls. Verification point: you assign one checklist owner and one escalation rule for high-impact ambiguity.

If California residency questions remain open, read Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?. Check it before you finalize your filing package.

If you want a deeper dive, read How to Handle Taxes for a Side Hustle.

Use this copy and paste checklist to file with confidence#

Use this checklist to turn startup-cost decisions into a filing package you can defend, not rework next quarter.

| Checklist item | Action | Verification point |

|---|---|---|

| Business-start timing | Mark the tax year your active trade or business began and save records that show when you moved from setup into active business operations | Your file has one clear start date and supporting documents |

| Cost bucket | Separate pre-operation startup costs from current operating business expenses, then test each deductible item as ordinary and necessary | Every expense line has a category, business purpose, and support document |

| Method choice | Evaluate whether an immediate deduction election fits your taxable income plan or whether amortization is the better fit | A one-page memo states your method and why |

| Overlap checks | Confirm whether Schedule SE applies if your line 4c amount is $400 or more, then run foreign-account checks separately | You assigned owners and deadlines for return filing, FinCEN filing, and any Form 8938 work |

| Escalation | If California sourcing or FTB residency treatment remains unclear, escalate to a qualified tax professional and document the question, assumptions, and final decision path | Your escalation log is complete, and you remain accountable for return accuracy |

This is the final operator pass. Treat it like a release checklist: actions, verification points, and no loose ends.

- Step 1. Confirm your business-start timing. Mark the tax year your active trade or business began, because startup cost deduction and amortization begin from that point. Save records that show when you moved from setup into active business operations. Verification point: your file has one clear start date and supporting documents.

- Step 2. Classify every cost into the correct bucket. Separate pre-operation startup costs from current operating business expenses, then test each deductible item as ordinary and necessary. Do not mix setup spending with ongoing delivery costs in one ledger line. Verification point: every expense line has a category, business purpose, and support document.

- Step 3. Choose deduction or amortization with a written rule. For eligible startup costs, evaluate whether an immediate deduction election fits your taxable income plan or whether amortization is the better fit. The common framework is up to $5,000 potentially deductible, reduced when total startup costs exceed $50,000, with remaining eligible amounts recovered over 180 months. Verification point: a one-page memo states your method and why.

- Step 4. Run overlap checks before final numbers. Confirm whether Schedule SE applies if your line 4c amount is $400 or more, because self-employment taxes can shift your final liability. Then run foreign-account checks separately: FBAR can trigger when aggregate foreign accounts exceed $10,000, and Form 8938 uses its own thresholds and filing mechanics, so filing one does not replace the other. Verification point: you assigned owners and deadlines for return filing, FinCEN filing, and any Form 8938 work.

- Step 5. Escalate ambiguity and lock controls. If California sourcing or FTB residency treatment remains unclear, escalate to a qualified tax professional and document the question, assumptions, and final decision path. Rules vary by scenario, so if you split time across countries and states, flag unresolved sourcing before filing instead of patching after a notice. Verification point: your escalation log is complete, and you remain accountable for return accuracy.

Frequently Asked Questions

Can freelancers deduct startup costs?

Yes, if your active trade or business has begun and the costs qualify under IRS startup rules. Keep it clean by separating pre-operation items from ongoing business expenses. Document business purpose and start timing for each line so your freelance tax file stays defensible.

How much startup cost deduction can I usually take in year one?

The IRS lets you elect up to $5,000 of certain startup costs in year one. That limit shrinks when total startup costs exceed $50,000. You recover remaining eligible costs through amortization.

When does startup cost deduction eligibility begin if I have no revenue yet?

Eligibility starts when you begin an active trade or business, not only when cash arrives. No-revenue status alone does not prove eligibility and does not block it. Prove your start timing with records that show when you began operations.

What expenses count as startup costs versus regular business expenses?

Startup costs are expenses you incur before operations begin. Regular business expenses are current operating costs after launch, and they still must meet the ordinary and necessary standard. Use two ledger buckets so you do not mix startup cost deduction items with day-to-day deductions.

Should I choose immediate deduction or amortization for startup costs?

Take the immediate deduction when you qualify and the position stays clear and supportable. Use amortization for remaining eligible costs over 180 months starting in the month your business begins. When facts look borderline, choose the safer treatment and document why.

What records should I keep to satisfy IRS review?

Keep supporting documents, receipts, contracts, and payment records that show the amount paid and that the amount was for a business expense. Keep a short classification memo that explains why each item belongs in startup costs or operating expenses. Retain books and records as long as their contents may become material to tax administration.

How do FBAR, FATCA, or Form 8938 concerns affect globally mobile freelancers?

Run foreign reporting as a separate control track from your startup-cost workflow. FBAR (FinCEN Form 114) can apply when aggregate foreign accounts exceed $10,000 at any point in the year. It has an April 15 due date and an automatic extension to October 15. You file Form 8938 with your tax return under FATCA rules, and it does not replace FBAR. Form 8938 thresholds vary by filing status and residency, so confirm the right threshold set before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Handle Taxes for a Side Hustle

If you want less stress at filing time, use sequence instead of shortcuts. When one year includes payroll income, contractor income, and time in more than one country, the order of operations matters. This guide gives you a defensible path so you can make each decision once, document it, and avoid rebuilding the return later.

The Freelancer's Year-End Tax Prep Checklist (US Expat Edition)

Your year-end target is filing readiness. By December 31, you want a complete file for your U.S. federal return, not a last-minute chase for documents. For a globally mobile freelancer, the hard part is usually proving what happened, choosing the likely FEIE or FTC lane, and spotting the facts that need professional review.