Quick Answer

Use wise jars for tax savings by allocating funds when each invoice settles, not by applying one fixed percentage to everything. Move collected VAT out first, then calculate income-tax reserves from net revenue and place them in jars labeled by liability and payment currency. This keeps spendable cash clearer and reduces last-minute FX surprises. If U.S. reporting applies, keep per-account maximum-value records so your preparer can evaluate FBAR exposure and prepare FinCEN Form 114 with defensible support.

The Danger in "Set Aside 30%": A Tax Strategy for Global Professionals#

If you work across borders, a fixed "set aside 30%" rule can be too blunt to manage tax risk well. Before you move money, define four variables: your taxable base, your timing, your settlement or reporting currency, and your jurisdiction mix.

Start with the base. Thirty percent of what amount? If you collect VAT, separate that from earnings first. VAT is designed as a consumer-borne tax, and HMRC states that if output VAT is higher than input VAT, you pay the difference to HMRC. Start your reserve decision from the amount that is actually yours, not from a mixed balance.

Next is timing. In the U.S., taxes are pay-as-you-go, and many sole proprietors generally need estimated payments when they expect to owe at least $1,000 at filing. If you wait for a month-end sweep, you can miss that rhythm even when your year-end totals look close. A practical default is to allocate when each invoice is paid, using the treatment you know at that point.

Currency is where a simple percentage often breaks down. The IRS requires foreign-currency tax items to be translated into U.S. dollars, and HMRC requires foreign-currency VAT transactions to be converted into sterling. If your income, reporting, and remittance currencies differ, one pooled reserve can hide shortfalls until payment day.

| Decision point | Fixed-percentage rule | Invoice-driven allocation |

|---|---|---|

| Decision quality | Generic estimate with an unclear base | Uses the actual paid invoice amount and known treatment |

| FX exposure | Easy to hold the wrong currency too long | Reserve can match reporting or settlement currency |

| Cashflow clarity | Tax money and spendable cash stay mixed | Spendable cash is clearer after each allocation |

| Compliance readiness | Bulk, late calculations weaken records | Per-invoice records are easier to reconcile |

Then map your jurisdiction exposure. Residency-based exposure can mean your residence country taxes worldwide income. For example, UK residents are normally taxed on UK and foreign income, while UK non-residents are generally taxed only on UK income. Citizenship-based filing exposure is different: the IRS states U.S. citizens and resident aliens are taxed on worldwide income, and it also recognizes overlap cases where foreign and U.S. tax can apply to the same income. Tax-year frames can also differ across jurisdictions, and a flat percentage gives you limited control.

The shift is simple: move from passive saving to active tax-liability management. Wise supports multiple currency balances, and Wise Jars are designed to keep money separate from your main balance for future use, including funds you do not want spent by card or Direct Debit. From there, you build separate buckets for distinct obligations instead of relying on one generic percentage.

You might also find this useful: A Guide to R&D Tax Credits for Tech Startups.

Part 1: Your Foundation - Building a Multi-Jar "Digital Treasury"#

If you keep all tax reserves in one place, it becomes harder to separate two decisions: what an obligation is for, and which currency you expect to pay in. A practical starting point is to split reserves into clearly labeled jars by purpose, with an optional buffer jar for expected variance.

If you use separate jars for tax reserves, treat each jar as a purpose bucket rather than a general savings goal. Many teams keep expected remittance funds, collected tax amounts, and optional buffer funds in distinct jars. Clear labels and boundaries help keep those categories from blending into operating cash, personal spending, or profit.

| Setup | Profit clarity | FX risk control | Payment readiness | Traceability |

|---|---|---|---|---|

| Single tax jar | One balance may hide what is actually spendable. | Currency intent can blur over time. | You still need to sort funds before payment. | Harder to map balances to obligations. |

| Multi-jar treasury | Reserved funds are visibly separated. | Each jar can be linked to a currency plan. | Each obligation already has a home. | Balances are easier to reconcile to records. |

The key control is boundary discipline, not the exact jar count. Label each jar by obligation and intended payment currency, define what can enter it, and define what never belongs in it. Set one explicit conversion rule per jar to reduce last-minute currency decisions. Use this setup checklist:

- Create jars by obligation first, then add intended payment currency in the label.

- Write one short rule per jar: what goes in, what stays out, and when you review it.

- Reconcile on a fixed cadence and after unusual invoice or refund events.

- Keep notes with each move so allocations are easy to review later.

Once that structure is in place, the next step is execution: allocate each paid invoice into the right jar when the money arrives. Related: Hiring Your First Subcontractor: Legal and Financial Steps.

Part 2: Your System - The "Invoice-Driven" Funding Method#

Run this routine every time an invoice is paid, not at month-end. That keeps collected indirect tax, income-tax reserves, and true spendable profit from getting mixed together.

Wise Jars let you keep money separate from your main balance, and once money arrives you can convert it, hold it, or send it. Wise guidance does not describe automatic per-invoice tax allocation, so you need a repeatable per-invoice method.

Run the same three steps on every paid invoice#

Start from the invoice record: what was billed, what tax was charged, and which currency each liability will be paid in. A common mistake is treating all incoming cash as revenue. If indirect tax was collected, that portion is not spendable.

| Step | What to do | Key detail |

|---|---|---|

| 1. Isolate indirect tax | Move any VAT, GST, or sales tax collected to the indirect-tax jar immediately | If VAT applies, verify the invoice record meets local rules; for UK VAT invoices, VAT should be shown separately, including rate and amount |

| 2. Calculate income-tax reserve | Calculate reserve on net revenue, not gross | Net revenue = Gross payment - indirect tax collected; Income-tax reserve = Net revenue x your verified blended rate |

| 3. Fund jars by payment currency | Decide whether to hold the received currency or the currency you will actually pay in | Convert now into the destination-currency jar or use a clearly named pre-conversion buffer jar with a written conversion rule |

- Isolate indirect tax first.

First question: did this invoice include VAT, GST, or sales tax collected from the customer? If yes, move that exact amount to your indirect-tax jar immediately. If VAT applies, verify the invoice record meets your local rules. For UK VAT invoices, VAT should be shown separately, including rate and amount. If the tax line is unclear, do not estimate. Correct the invoice record first.

- Calculate income-tax reserve from what remains.

After indirect tax is removed, calculate reserve on net revenue, not gross:

Net revenue = Gross payment - indirect tax collected

Income-tax reserve = Net revenue x your verified blended rate

If you have multiple income-tax obligations, split this reserve across the relevant jars using your verified allocation rules.

- Fund jars in the payment currency of each liability.

For each obligation, decide whether to hold the received currency or the currency you will actually pay in. If the payment currency differs, either convert now into the destination-currency jar or place funds in a clearly named pre-conversion buffer jar with a written conversion rule.

Decision points people usually miss#

One point people often miss is settlement currency. A jar labeled only by tax type or country is incomplete if the liability is paid in another currency.

Scheduled transfers are useful for recurring execution, but they are not a substitute for invoice allocation. The FX rate is not guaranteed when scheduled, and Wise does not auto-pull from other currencies to cover shortfalls. For fixed-amount scheduled transfers, Wise recommends holding extra balance to absorb rate movement.

Auto Conversion is useful when you know your target currency and only want to convert at your target rate or better. If a payment deadline is close, do not rely on that target being hit in time.

Monthly sweep versus invoice-driven allocation#

The tradeoff is simple: a monthly sweep can be easier to run, but it gives you weaker control when tax treatment or currency differs by invoice.

| Method | Cashflow visibility | FX control | Tax-fund segregation | Error risk |

|---|---|---|---|---|

| Monthly percentage sweep | Spendable cash can look overstated until sweep day. | Currency decisions get delayed. | Tax funds can sit mixed with operating cash. | One month-end error affects many invoices. |

| Invoice-driven allocation | Reserved vs spendable is clear after each payment. | Currency choice is made per liability. | Funds are separated by liability type right away. | Issues are usually isolated to one invoice. |

If you pay US federal estimated tax, this cadence can align with pay-as-you-go timing. Estimated tax payments are generally due April 15, June 15, September 15, and January 15 of the following year.

Finish each invoice cycle#

An invoice cycle is done only when all of these are true:

- Indirect tax was checked, and any collected amount was moved to the correct indirect-tax jar.

- Income-tax reserve was calculated from net revenue using your current verified rates.

- Reserves were moved to jars labeled by liability type and intended payment currency.

- Any required conversion was completed, or parked in a named buffer jar with a clear conversion trigger.

- Remaining main-balance funds are confirmed as spendable profit from that invoice.

For a step-by-step walkthrough, see The Most Overlooked Tax Deductions for Freelancers.

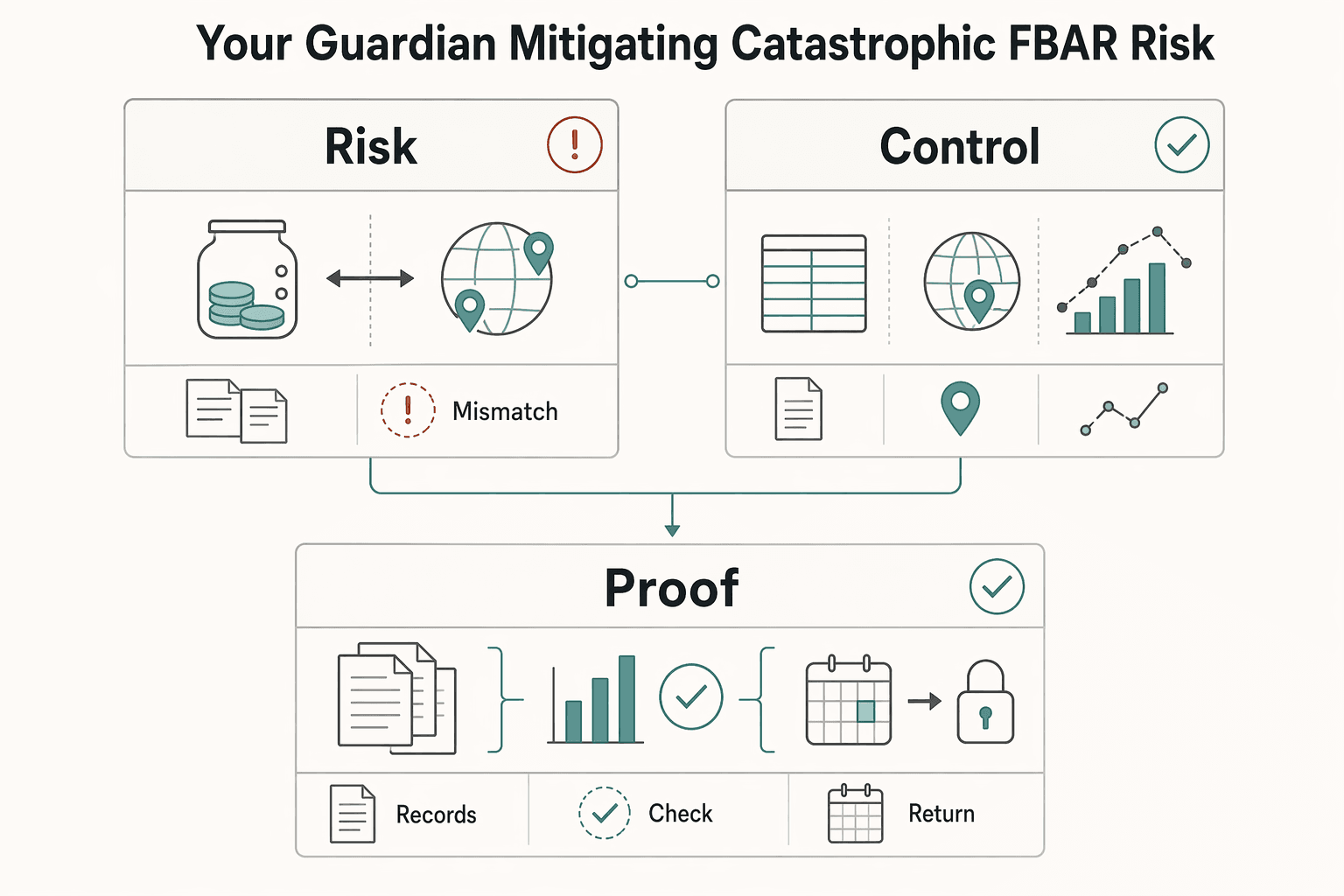

Part 3: Your Guardian - Mitigating Catastrophic FBAR Risk#

Your invoice-driven process can support FBAR risk control by documenting what you held, where you held it, and each account's highest value during the year.

If you use Wise Jars for tax reserves, do not assume labels determine FBAR treatment. For FBAR, you and your preparer need defensible records for each account's maximum value, then an aggregate check against the filing threshold for the reporting year.

What you need to track#

Track this year-round, per account:

- each foreign account your preparer is evaluating for FBAR

- the maximum value of each account in that account's own currency during the calendar year

- the evidence supporting that maximum value

If you have multiple accounts, value each one separately before aggregation. If your platform shows multiple balances, currencies, cards, or jars in one interface, track at the most granular level you can and have your preparer confirm filing treatment.

Why segregation still helps#

Segregation does not change the filing rule. It does change whether you can reconstruct maximums and hand over clean records before filing.

| Workflow | Audit trail quality | Account-aggregation visibility | Handoff readiness for your tax preparer |

|---|---|---|---|

| No segregation workflow | Mixed inflows and reserves can make balance spikes harder to explain. | Annual highs may need to be rebuilt late from statements. | Your preparer may need to untangle mixed activity and infer peaks. |

| Invoice-driven multi-jar workflow | Transfers can tie to invoice, reserve, and FX decisions. | You can identify which account hit a high, in which currency, and when. | You can provide exports, reconciled balances, and a usable high-balance log. |

Maintain a live high-balance log#

Do not wait for filing season. Periodic statements are usable only if they fairly reflect the year's maximum value. Include these fields in your log:

| Log field | Record |

|---|---|

| Institution account name and internal label | institution account name and your internal label |

| Account currency | account currency |

| Highest observed balance | highest observed balance in that currency |

| Date and time of high | date and time, if available, of that high |

| Evidence reference | statement, export, or screenshot file |

| USD conversion used for filing | USD conversion used for filing, including rate source when Treasury's rate is unavailable |

| Final reported amount in USD | final reported amount in USD, rounded up to the next whole dollar |

Also keep transfer-level records: date, source account, destination account, amount, currency, FX details, and purpose or invoice link. If a computed value for item 15 is negative, report 0 for maximum account value. Use "amount unknown" (item 15a) only in the limited case where you have fewer than 25 accounts and cannot determine whether aggregate maximum values exceeded the filing threshold.

Compliance handoff before filing#

Before your advisor prepares or reviews FinCEN Form 114, confirm you have:

| Handoff item | Requirement |

|---|---|

| Statements and transaction exports | statements and transaction exports for each evaluated foreign account |

| High-balance log | a reconciled full-year high-balance log with separate per-account values |

| USD conversion and rounding documentation | USD conversion and rounding documentation, including non-Treasury rate sources where used |

| Support for major spikes | support for major spikes, including internal transfers and FX conversions |

| Account map | an account map linking platform balances, jars, or sub-accounts to exported records |

| Advisor review | advisor review queued before the applicable deadline, with current FinCEN notices checked and required e-filing elements verified |

What matters is having records strong enough to validate exposure against the filing threshold for the reporting year and avoid preventable filing errors.

We covered this in detail in Using Wise for Large Transfers Without Cashflow Surprises.

Before you lock your month-end checklist, run your account setup through the FBAR calculator to catch reporting gaps early.

Conclusion: You are the CFO of Your Business-of-One#

Your job is to keep this process boring and repeatable: protect cashflow, separate tax reserves before they get spent, and keep records that are ready for filing. A practical end state looks like this:

- Separate reserves by obligation and filing currency. If you handle more than one obligation or filing currency, keep those balances distinct enough that the purpose of each reserve is obvious.

- Move allocations when client payments settle, or on one fixed sweep schedule. Use one trigger consistently so allocations do not drift into operating cash.

- Keep a filing-ready record set. For each transfer, keep the invoice, your calculation note, transfer confirmation, and related account record together. If account reporting may be triggered, verify the current reporting threshold before filing.

Many avoidable problems start with vague labels, mixed balances, or transfers without support. Those gaps can create cashflow pressure, weaker audit trails, and compliance surprises. For filing checkpoints, keep the filing name and identifier together in your records.

Week to week, keep it simple: review reserve balances, reconcile transfers against settled invoices, and verify upcoming obligations early. That is how this jar setup helps in practice: clearer spendable cash, a cleaner handoff to your preparer, and fewer surprises at filing.

If you want a deeper dive, read Separating Business and Personal Finances: An Important Step for LLCs.

If you want to extend this jar method into a full get-paid workflow, use the Gruv tools library to choose your next implementation checklist.

Frequently Asked Questions

How much should you set aside for taxes?

Do not default to a fixed percentage unless your advisor has confirmed it fits your actual obligations. Set a working rate per liability, label jars by liability and filing currency, and move funds when each invoice payment settles, or at your scheduled sweep. Keep the invoice, your calculation note, and the transfer record together so the reserve amount is auditable.

Does money in jars count toward FBAR?

Do not assume a jar label determines FBAR treatment. Have your preparer confirm which balances are foreign financial accounts based on where the account is located and which entity holds it, then test the combined value against the $10,000 aggregate threshold. If required, file FinCEN Form 114 through BSA E-Filing and retain required account records for 5 years from the FBAR due date (April 15, with an automatic extension to October 15).

Should you use one tax jar or several?

Use one jar only when your setup is simple. Use liability-specific jars when you have multiple authorities, VAT, or multiple filing currencies. Wise supports multiple jars and also supports multi-currency jars, so choose the structure that keeps your filing trail clear. | Setup | Best fit | Label example | Main tradeoff | |---|---|---|---| | Single jar | One authority, one filing currency | Tax Reserve USD | Easier setup, weaker liability-level visibility | | One multi-currency jar | One container across currencies | Tax Reserve Multi | Fewer containers, but tracking can blur across liabilities | | Liability-specific jars | Multiple authorities/VAT/cross-border | Income Tax USD, Residency Tax EUR, VAT EUR | More setup, stronger audit handoff |

Can you use jars for VAT?

Yes, and treat VAT as collected tax rather than spendable cash. Under EU rules, an invoice is required for most B2B supplies and should show VAT charged, so move that VAT amount into a dedicated jar when payment arrives. Keep the invoice, VAT summary, and transfer proof aligned so your return and payment trail matches.

When should you move money into the jar?

Move it as soon as the payment lands, or use a fixed weekly checkpoint if volume is high. Consistency matters more than perfect timing, so use the same trigger each cycle and attach the invoice reference to each transfer. This works because jar money stays separate from your main balance and is not available for card spending or Direct Debits.

Is interest earned in jars taxable?

If interest is credited and you can withdraw it without penalty, it is generally taxable in the US when it becomes available. Wise's US guidance says customers earning more than $10.00 USD in interest receive a Consolidated Form 1099, and says the 2025 form is available by January 31st, 2026. Save that form and reconcile it to your account records so interest income is fully captured at filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- congress.gov/79/crecb/1946/07/17/GPO-CRECB-1946-pt7-12.pdftrusted

- congress.gov/119/bills/hr5371/BILLS-119hr5371eas.pdftrusted

- dlcp.dc.gov/sites/default/files/dc/sites/DLCP/publicatio...trusted

- epa.gov/system/files/documents/2026-02/2024-4th-quar...trusted

- fincen.gov/system/files/2025-12/FBAR-FBAR-Filing-Requir...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

- govinfo.gov/content/pkg/FR-1966-01-27/pdf/FR-1966-01-27.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.