Quick Answer

Deducting business travel expenses works best when you use a strict, repeatable system instead of guessing at filing time. Confirm that travel is business-related, away from your tax home, and ordinary and necessary, then document each line item as you go. Keep mixed personal costs out of your claim queue, and escalate edge cases early when assignment length, state exposure, or cross-border facts are unclear.

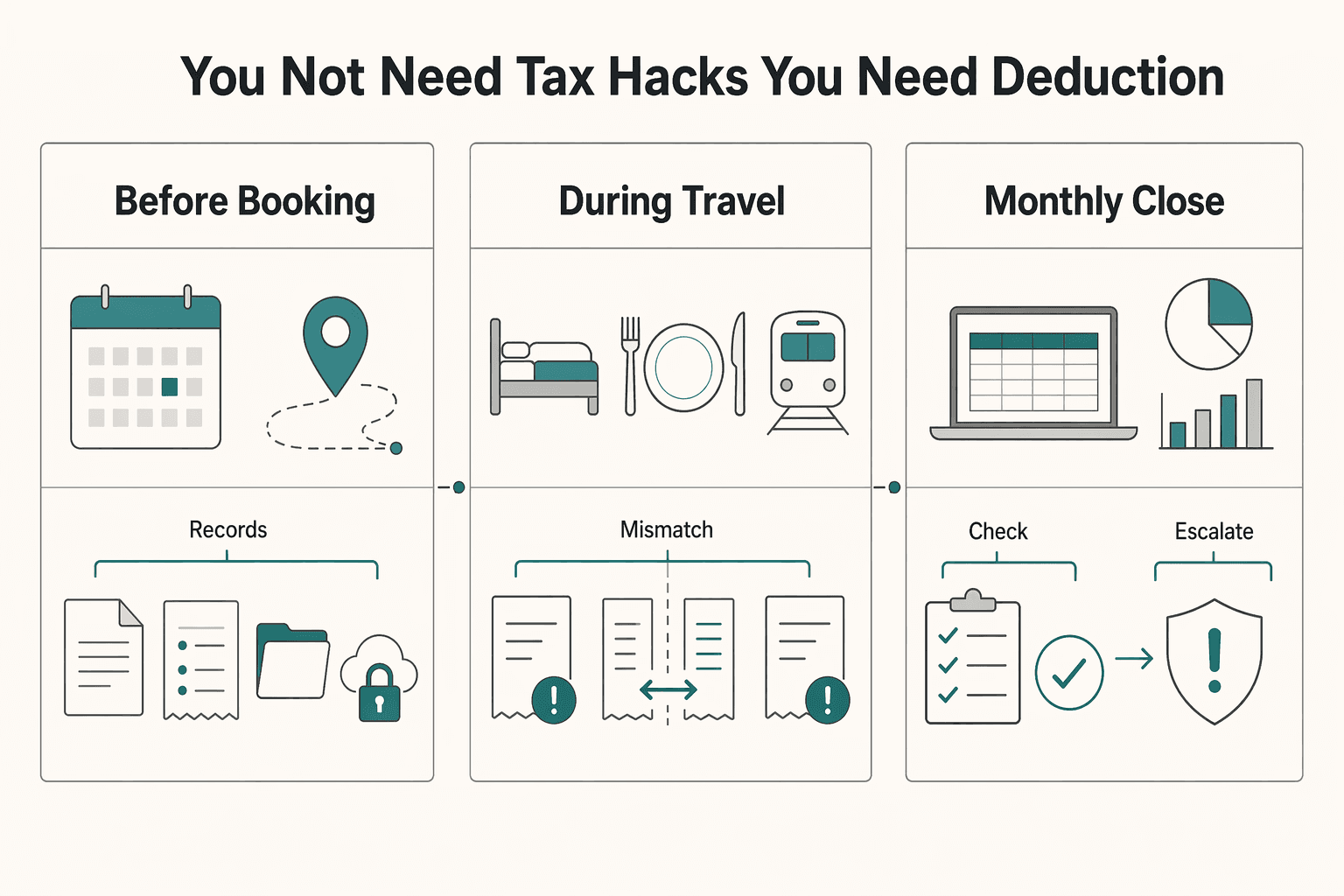

You do not need tax hacks you need a deduction system you can trust#

For deducting business travel expenses, use a repeatable compliance system so you only claim costs you can prove.

Frequent travel creates pressure, and confusing rules make fast decisions risky. The IRS notes that both frequent and occasional travelers can struggle with business travel deductions. When you guess on meals, lodging, or transportation, you create cleanup work now and stress later.

If you run a business of one, build a travel deduction process you can run consistently.

The goal is simple. Decide deductibility before booking, then run an audit-ready workflow from trip planning through filing. Use Publication 463 as your operating reference for what qualifies, how you report, and what records you keep. Date-check older IRS news guidance before relying on it.

If you run a solo business, map eligible travel costs to your Schedule C process instead of sorting receipts at year end. Treat costs as potentially deductible only when business takes you away from your tax home or main place of work.

| When you decide | Safe default action | Evidence you keep |

|---|---|---|

| Before booking | Mark any unclear expense as non-deductible | Business purpose note and planned itinerary |

| During travel | Log each charge to a category on the same day | Receipt, payment proof, and short business note |

| Monthly close | Reconcile claims against your policy | Clean category log and supporting documents |

A common scenario: you fly to meet a client, then extend the trip for personal time. A good system separates business and personal portions right away. It keeps only supportable business costs in your deduction queue. Every unclear line item stays non-deductible until the facts confirm treatment.

This guide is for freelancers and consultants who want lower-stress tax operations. Rules vary by jurisdiction, so the workflow includes escalation points by design.

- Escalate when your tax home or main place of work does not stay stable.

- Escalate when a trip crosses state or cross-border boundaries.

- Escalate when documentation gaps appear and you cannot reconstruct intent confidently.

If state exposure complicates your travel pattern, review Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?. Confirm treatment with a qualified tax professional.

What counts as deductible business travel and what does not#

Deductible business travel starts only after you establish three things: your tax home, away-from-home status, and that each cost is ordinary and necessary for work.

Before you claim meals, lodging, or transportation, set the boundary rules. If a cost fails any boundary test, mark it non-deductible under IRS rules and move on.

Publication 463 gives you the sequence: find your tax home first, then decide whether you traveled away from home for business. Your tax home is usually your regular main place of work, not automatically the place where your family lives. IRS Topic No. 511 makes this concrete with its Chicago and Milwaukee example.

| Test | What passes | What fails |

|---|---|---|

| Tax home | Your regular main place of work or post of duty | You assume family residence sets tax home |

| Away from home | Work keeps you away substantially longer than an ordinary workday and you need sleep or rest | Usually same-day local trips or commuting-style travel |

| Ordinary and necessary | Cost directly supports business purpose | Personal, lavish, or extravagant spending |

Use the Chicago and Milwaukee example as a practical default. If your regular work sits in Milwaukee, treat Milwaukee as your tax home. Do not deduct meals or lodging there. Do not deduct weekend transportation back to Chicago either, because that travel serves a personal purpose.

Run this checklist before every booking:

- Confirm your current main place of work.

- Confirm the trip requires enough time away that you need sleep or rest.

- Confirm each planned cost meets the ordinary and necessary standard.

- Split mixed-purpose plans early, then keep only supportable travel deductions.

- Classify unclear items as non-deductible until your records support a claim.

If you schedule client meetings in one city, then add personal days after the work ends, separate business days from personal days at planning time. Do not wait until filing time. That helps keep personal costs out of your travel deduction file.

Can you decide deductibility in 10 minutes before booking?#

Yes. You can make a pre-booking deductibility call by running a strict yes-or-no gate and treating unclear items as provisional or non-deductible until facts are confirmed.

Turn the boundary rules into a quick flow you run every time. The goal is not to fix it later. It is to book with a clear position on meals, lodging, and transportation.

Use this binary flow before you spend money:

| Decision gate | Fast question | Rule anchor | Action if unclear |

|---|---|---|---|

| Business purpose | Does this trip directly support client work or business operations? | Publication 463 and IRS Topic No. 511 business travel rules | Mark provisional and do not assume a deduction |

| Tax home check | Is this travel outside the city or general area of your main place of work? | IRS Topic No. 511 definition of tax home | Pause and verify your current tax home facts |

| Away from home check | Will work keep you away long enough that you need sleep or rest? | IRS Topic No. 511 away from home test | Treat as non-deductible until facts support overnight business status |

| Assignment status | Is this a temporary work assignment, not an indefinite work assignment? | Publication 463 and IRS Topic No. 511 one-year framework | Escalate if duration or extension risk is unclear |

| Category eligibility | Is each expense business-related and not personal, lavish, or extravagant? | IRS Topic No. 511 deductibility boundary | Remove the expense from your claim queue |

For assignment status, decide at the start of the engagement. If expected work goes beyond one year, treat it as indefinite. If facts change and a temporary assignment turns indefinite, update treatment immediately.

If a client trip might turn into rolling extensions, do not guess. Classify costs as provisional and escalate quickly to a CPA or enrolled agent.

Trigger escalation early when the trip creates California residency or sourcing complexity, especially when facts span multiple locations. California treats residency as a facts-and-circumstances question, and the FTB applies detailed residency audit procedures. In ambiguous cases, a CPA or enrolled agent can help you lock down a defensible position before filing.

Which travel costs usually qualify and which are common misclassifications?#

Most travel costs qualify only when they directly support business work away from your tax home, and denied claims usually trace back to personal use or weak allocation.

Once you run the pre-booking gate, classify each planned expense before you spend. This is where the rules turn into day-to-day bookkeeping.

Use IRS Tax Tip 2023-15 as a quick category map, then verify each item against current IRS guidance and solid records. Treat every line item as eligible only after it clears the ordinary and necessary test.

| Category | Usually deductible when business-linked | Common misclassification that gets denied |

|---|---|---|

| Airfare, train, bus, car between tax home and destination | Trip serves a clear business purpose | Personal getaway added to the same booking |

| Taxis and local transportation | Ride connects airport or station, hotel, and work location | Local personal rides logged as business transportation |

| Lodging | Overnight stay supports business travel | Extra nights for personal leisure |

| Meals | Non-entertainment business meals, generally subject to a 50% limit on unreimbursed cost | Claiming all meals without business context or current-year rule check |

| Baggage and shipping | Shipping samples or materials between regular and temporary work locations | Shipping personal items and treating them as business costs |

| Personal car use | Only the business-use portion | Claiming total vehicle cost without allocation |

| Convention travel | Attendance benefits your trade or business | Assuming any conference always qualifies, especially outside North America |

Meals need extra care. Consumer guidance such as TurboTax often references partial deductibility, but you still need to verify current IRS conditions before filing because rules can change by tax year. Treat that as a control, not a loose guideline.

Convention travel also needs intent proof. You can usually support the deduction when the event clearly benefits your work. Conventions outside North America trigger special handling, so escalate early if the facts look complex.

If you book a conference trip, add personal days, and upgrade activities for comfort, split costs immediately. Keep only business-linked amounts in your claim queue and mark the rest non-deductible.

Use this operator checklist every time:

- Tie each expense to a business purpose note.

- Keep receipts and category tags for meals, lodging, and transportation.

- Allocate mixed-use costs on day one, not at filing time.

- If facts stay unclear, classify the cost as non-deductible until documentation supports it.

What breaks deductions in mixed-purpose trips and long assignments?#

Mixed-purpose planning and assignment drift break valid claims fast, so you need to allocate costs early and reclassify the trip when facts change.

| Review area | Monthly action |

|---|---|

| Business purpose and tax home | Re-validate facts for each open assignment |

| Mixed-purpose costs | Re-allocate with receipts and business notes |

| Assignment length | Recheck against the temporary versus indefinite boundary |

| Cross-border reporting | Escalate questions early, since travel rules and account reporting rules differ |

Most deduction problems are not about categories. They come from timing and classification. Mixed-purpose trips and assignments that quietly extend are where otherwise valid travel costs get compromised.

Use this break test before you book, pay, or log airfare, meals, lodging, or transportation:

| Failure point | What usually goes wrong | Safe operator move |

|---|---|---|

| Mixed-purpose trip design | You blend business and personal days without a clear allocation plan | Split business and personal days up front, then claim only business-related travel expenses |

| Primarily personal trip | You add a small work task to a mostly personal trip and try to deduct the whole trip | Treat the full trip cost as personal and non-deductible |

| Assignment duration | A temporary work assignment quietly extends past one year | Reclassify as an indefinite work assignment and stop claiming travel deductions from that point |

| Tax-home drift | You rotate cities and stop validating your main place of work | Reconfirm your tax home before each trip and pause claims until facts are clear |

Picture a consultant rotating between client hubs while keeping one main place of work. Early engagements stay short, so travel can qualify. Then one client keeps extending the project. As soon as the expected duration crosses one year, you update classification, stop new travel claims, and escalate review instead of forcing old assumptions.

Keep residency-adjacent reporting separate from travel deductibility. FBAR (FinCEN Form 114) and Form 8938 follow a different rule set. Form 8938 does not replace FBAR, and FBAR is filed separately from the IRS return.

If aggregate foreign account totals exceed $10,000 at any time during the year, file FinCEN Form 114 on its own timeline (April 15 with automatic extension to October 15). Then review whether Form 8938 also applies.

Run this checklist every month:

- Re-validate business purpose and tax-home facts for each open assignment.

- Re-allocate mixed-purpose costs with receipts and business notes.

- Recheck assignment length against the temporary versus indefinite boundary.

- Escalate cross-border reporting questions early, since travel rules and account reporting rules differ.

- If state exposure grows while you travel, review Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

How do you keep audit-ready records without creating admin overload?#

Build your record system into the trip workflow, and your travel deductions become a controlled process instead of a year-end scramble.

| Expense type | Keep | Details |

|---|---|---|

| Transportation | Receipt or ticket record; payment proof | Date, route, and business purpose |

| Lodging | Hotel folio or paid bill; payment proof | Dates, location, and work reason for being away from your tax home |

| Meals | Receipt; payment proof | Date and place, and a brief business purpose note |

| Personal car business use | Trip sheet or mileage log | Purpose and date |

| Higher-cost non-transport items | Documentary evidence | Especially for non-transportation expenses of $75 or more |

If you want low admin, you need fewer decisions later. That means capturing the right evidence while the trip is happening, not trying to reconstruct intent months afterward.

Publication 463 and IRS substantiation standards set the baseline: prove each expense with clear records, capture time, place, and business purpose, and record details at or near the time of spending. Your supporting documents should show who you paid, how much you paid, proof of payment, and the date incurred. Electronic records are fine if they meet the same recordkeeping requirements as paper records.

| Workflow stage | What you capture | Why it protects the claim |

|---|---|---|

| Before trip | Engagement proof, planned itinerary, trip purpose note, policy gate for deductible vs provisional | You set scope early and stop unsupported claims before money leaves your account |

| During trip | Receipts, paid bills, payment proof, short business-purpose notes, categorization log for meals, lodging, and transportation | You preserve facts near-time, which strengthens your file if the IRS reviews it later |

| After trip | Reconciliation log, exception notes, final category decisions, archive pack | You can defend each line item without reconstructing intent months later |

Use a minimum evidence bundle for each category:

- Transportation: receipt or ticket record, payment proof, date, route, and business purpose.

- Lodging: hotel folio or paid bill, payment proof, dates, location, and work reason for being away from your tax home.

- Meals: receipt, payment proof, date and place, and a brief business purpose note.

- Personal car business use: trip sheet or mileage log plus purpose and date.

- Higher-cost non-transport items: keep documentary evidence, especially for non-transportation expenses of $75 or more.

If you return from a multi-stop client trip with mixed personal and business charges, do one thing right away: classify each line item, attach proof, and move unclear items to non-deductible until the facts support them.

Run a regular close routine. Apply policy gates, reconcile every travel line, and keep records traceable by default. If California exposure applies, keep retention discipline strong, because FTB review windows are usually four years from the return due date or filing date.

Related: The Freelancer Year-End Tax Prep Checklist.

What changes when you are cross-border and how do you confirm safely?#

When you operate across borders, treat business travel deductions as a layered decision that you verify in order, not a single yes or no call.

| Trigger | Related fact |

|---|---|

| Convention activity outside North America | Special rules apply |

| Multi-country itineraries | Mixed business and personal days |

| Away-from-home facts | Facts are unclear or the main place of work is changing |

| Assignment length | Over one year is treated as indefinite |

| California ties | Residency is uncertain |

Cross-border work raises the stakes because U.S. federal travel rules, state tax scope, and foreign-asset reporting can all apply at once. The safest way to handle it is to keep each lane separate and confirm them in order.

Use a confirmation ladder#

| Step | What to confirm | Safe action |

|---|---|---|

| 1 | Start with IRS Topic No. 511, then use Publication 463 for travel detail. Confirm away-from-home travel facts and temporary versus indefinite assignment logic (over one year is treated as indefinite). | Approve only expenses that meet federal travel standards. Mark unclear items non-deductible for now. |

| 2 | Check state overlay when facts touch California. FTB can tax residents on income from all sources, so state outcomes may differ from your federal framing. | Run a state review before filing. If needed, use Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?. |

| 3 | Separate travel deductions from Form 8938 and FBAR checks. FBAR goes to FinCEN, and filing Form 8938 does not replace FBAR duties. | Evaluate whether you need Form 8938, FBAR, or both. Track those decisions in a separate compliance checklist. |

| 4 | Identify conflicts or missing facts. | Escalate to a qualified CPA or enrolled agent before you claim. |

Do not guess when these triggers appear#

- Convention activity outside North America.

- Multi-country itineraries with mixed business and personal days.

- Unclear away-from-home facts or changing main place of work.

- An assignment that may run beyond one year.

- California ties that create residency uncertainty.

If you book client work in two countries and add personal time between meetings, classify each day and expense lane by lane. Stop at the first unresolved fact and escalate. That pause protects you more than a fast assumption.

If you want a deeper dive, read How to Handle Taxes for a Side Hustle.

Run this playbook every trip and escalate early when facts get messy#

A repeatable system beats ad hoc guesses and lowers filing stress every season.

The point of this playbook is consistency. Use IRS Topic No. 511 as your decision gate, then use Publication 463 to confirm category details and proof standards. Approve only costs that are ordinary and necessary, tied to being away from home, and documented with a clear business purpose.

| Trip phase | Decision rule | Record standard | Escalate when |

|---|---|---|---|

| Before booking | Confirm business purpose and trip structure under IRS rules | Keep itinerary, engagement context, and purpose note | Assignment may run more than one year |

| During travel | Classify each line item as business, personal, or provisional | Keep receipts, canceled checks, and supporting documents | Expense looks personal, lavish, or extravagant |

| Monthly close | Reconcile categories and finalize deductibility | Log each expense at or near the time with amount, time, place or description, and business purpose | Facts stay incomplete after reconciliation |

| Filing prep | Recheck edge cases and jurisdiction overlap | Keep one traceable file per trip with supporting documents | Convention activity sits outside North America or state treatment may differ |

If you take a multi-stop client trip and add personal days between meetings, split charges as they happen. Keep clear notes, and move any unclear item to non-deductible until facts support it. That habit prevents most cleanup pain.

Escalate early when facts get messy, especially when California enters the picture. California generally conforms to federal law with modification, and state treatment can differ from federal outcomes. If your travel and payment operations run globally, keep records traceable and reconciliation-ready by default, then confirm final tax treatment with a qualified advisor. If you need a state-focused follow-up, review Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Frequently Asked Questions

What qualifies as being away from home for business travel deductions?

You qualify as away from home when work keeps you away substantially longer than an ordinary workday and you need sleep or rest to meet the business demand. If a trip does not meet that standard, treat the related costs as non-deductible. Run this test before you approve spending.

What is a tax home and why does it matter for freelancers?

Your tax home is generally the city or area where your main place of business or work sits. It is not automatically your family residence. It matters because IRS travel tests start from your tax home, which drives whether transportation, lodging, and meals can qualify.

Can I deduct travel costs if my assignment is expected to last more than one year?

No. IRS Topic No. 511 treats an assignment expected to exceed one year as indefinite, and related travel expenses do not qualify for deduction. If duration looks unclear, default to holding the claim until facts support it.

Which business travel expenses are generally deductible under IRS rules?

When the trip meets business and away-from-home tests, common categories include transportation between your tax home and business destination, plus lodging and meals during the trip. Meals usually face a general 50% limit on unreimbursed business costs. Keep each expense tied to a clear business purpose, then confirm edge cases in Publication 463.

Are personal or lavish travel expenses ever deductible?

No. Personal costs do not become deductible just because they happen during a work trip. IRS rules also deny lavish or extravagant meals and lodging. When an item looks mixed or discretionary, treat it as personal until you can defend the business purpose.

Are convention travel expenses deductible and do different rules apply outside North America?

Convention travel can qualify when attendance benefits your trade or business. If the event is outside North America, special rules apply. Do not guess. Escalate early if facts feel borderline.

What records should I keep to substantiate business travel deductions?

Keep receipts, canceled checks, and related documents that support each deduction. For each line item, keep supporting documents and a clear business purpose, then tag it to meals, lodging, or transportation. Close each trip by classifying charges immediately and leaving unclear items non-deductible until you confirm them.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Handle Taxes for a Side Hustle

If you want less stress at filing time, use sequence instead of shortcuts. When one year includes payroll income, contractor income, and time in more than one country, the order of operations matters. This guide gives you a defensible path so you can make each decision once, document it, and avoid rebuilding the return later.

The Freelancer's Year-End Tax Prep Checklist (US Expat Edition)

Your year-end target is filing readiness. By December 31, you want a complete file for your U.S. federal return, not a last-minute chase for documents. For a globally mobile freelancer, the hard part is usually proving what happened, choosing the likely FEIE or FTC lane, and spotting the facts that need professional review.