Quick Answer

Yes - use a tax home for domestic nomad planning by proving a principal business area and keeping assignment and travel records current. Keep that federal position separate from your state domicile file, and update both when facts change. If work in one location is expected to last more than 1 year, reassess deduction treatment right away; if no regular business base exists, itinerant status can put deductions at risk.

Tax Home vs. Domicile: The Critical Distinction for Nomadic Professionals#

You are dealing with two separate systems. One is a federal test for travel-expense deductions. The other is a state test for residency and tax exposure. If you treat them as the same, you can lose deductions and still end up with resident-state tax risk. Start by separating the questions: use tax home for federal travel deductions, and use domicile/residency for state income tax analysis.

| Concept | Main test | What it controls | Typical evidence | What goes wrong if misclassified |

|---|---|---|---|---|

| Tax home (federal) | Your main place of business or work area, with time spent at each location as a key factor | Whether you were traveling "away from home" for business and can deduct qualifying travel expenses | Work calendar, assignment dates, and travel records | IRS may treat costs as nondeductible at your tax home, and itinerant status can make away-from-home deductions hard to support |

| Domicile (state) | Your permanent home you intend to return to | Which state can claim broad taxing rights over your income | Records tied to home, time, family connections, business involvement, and other life ties | A former state can argue you never changed domicile and still treat you as a resident |

| State residency test (state-specific) | Separate statutory tests that can apply even if domiciled elsewhere | Whether a state still treats you as a resident for filing and tax | Day counts, permanent-place-of-abode facts, presence logs, housing records | Unexpected resident filing and tax exposure in a state you thought you had exited |

Use this decision order:

- If your goal is travel-expense deductibility, evaluate tax home first.

- If your goal is state tax exposure, evaluate domicile and state residency tests first.

- If both matter, document both in parallel from day one.

Practical federal checkpoint: can you show one principal business area, and can you show that any temporary assignment was not expected to exceed 1 year? If an assignment is expected to exceed 1 year, it is treated as indefinite for travel-expense purposes. If you do not have a regular main business location and do not maintain a regular place you live, you can be treated as itinerant.

Get a tax professional involved early if any of these apply

- You have strong ties in more than one state. - Your work pattern rotates often and no principal business area is clear. - You maintain a year-round dwelling in a state where statutory residency tests can apply. - Your day count is close to a state trigger, including New York's 184-days-or-more rule when combined with a permanent place of abode (where any part of a day counts). - A state such as California could argue your presence was not temporary or transitory.

Documentation is part of the strategy. For travel expenses, good records are essential. For domicile, no single document decides the issue on its own. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Phase 1: The Offensive Strategy - Establishing Your Base of Operations#

Start by building one consistent home-base record, then layer your travel-expense position on top of it. A workable setup is usually the state you can support cleanly with evidence, not just the one that appears cheapest.

In this phase, choose the one state you can actually maintain and keep your records from pointing in two directions.

Step 1. Compare realistic state options before you book the move#

The best option is usually the state you can document cleanly with the fewest exceptions. Shortlist a few states you would genuinely use, then compare setup friction and record quality, not just tax marketing.

| Decision factor | Why it matters | Candidate A | Candidate B | Candidate C |

|---|---|---|---|---|

| Domicile setup friction | Can you complete the setup steps and keep clean proof? | Verify current requirements and cost | Verify current requirements and cost | Verify current requirements and cost |

| Business admin load | How much ongoing admin might change based on where you base the business? | Verify current requirements and cost | Verify current requirements and cost | Verify current requirements and cost |

| Documentability for your domicile file | Can you produce consistent official records tied to one address? | Verify current requirements and cost | Verify current requirements and cost | Verify current requirements and cost |

| Practical logistics | Can you realistically maintain ties there over time? | Verify current requirements and cost | Verify current requirements and cost | Verify current requirements and cost |

Practical rule: if a state choice leaves you with scattered records, skip it.

Step 2. Complete onboarding in priority order and file proof as you go#

Consistency matters. Update core records first and save proof as each change happens. No single document should have to carry this alone; the strength comes from a consistent pattern across records.

Start with these records

| Action | Evidence to save in your domicile file |

|---|---|

| Set your primary address | Service agreement, lease, or first official mail showing that address |

| Update government ID records | Application/receipt and issued ID record |

| Update vehicle records (if applicable) | Registration/title paperwork and insurance update |

| Update voter registration (if applicable) | Registration confirmation |

| Update core account addresses | Confirmations from banking, insurance, tax, payroll/client, and active professional accounts |

Then follow with these updates

| Action | Evidence to save |

|---|---|

| Add practical local financial ties if they fit your facts | Opening confirmation and first statement |

| Update remaining legal/professional records still tied to the old state | Change confirmations |

| Move recurring life records only where real | Account/profile updates you actually use |

After both passes, your core records should tell the same address story.

Step 3. Align your business records with the move#

If your personal records move but your business records do not, you create avoidable inconsistencies.

| Business record | Keep aligned with move |

|---|---|

| Registry filings | Keep address and contact details consistent |

| Tax/business accounts | Keep address and contact details consistent |

| Banking | Keep address and contact details consistent |

| Payment processors | Keep address and contact details consistent |

| Insurance | Keep address and contact details consistent |

| Invoices | Keep address and contact details consistent |

| Contracts | Keep address and contact details consistent |

| Public business profiles | Keep address and contact details consistent |

Use this fork:

- If moving the entity is operationally clean, review that path with a CPA or business attorney. * If the current entity has meaningful history or obligations where formed, review whether to keep it there with professional guidance.

Whichever path you choose, keep business records synchronized with your move. At minimum, keep address and contact details consistent across registry filings, tax/business accounts, banking, payment processors, insurance, invoices, contracts, and public business profiles. If you are a sole proprietor, the same rule applies: your business paper trail should not contradict your personal move.

Escalate early for professional advice when S-corp structure, payroll, licensing, financing, or multi-state operations are in play.

Step 4. Catch common failure modes early#

Most problems start as small inconsistencies and become harder to explain later. Catch them while they are still easy to fix.

| Failure mode | Safe-default corrective action |

|---|---|

| Inconsistent addresses across ID, banking, and business records | Stop adding new records with old addresses; run one full address-update pass across core accounts; save each confirmation |

| Partial tie-severing from the old state | Close, cancel, or update old-state records you no longer need; document any ties you must keep and why |

| Business and personal records tell different stories | Reconcile both record sets in the same filing cycle; if mismatch must remain temporarily, get written CPA/attorney guidance |

Once this phase is done, shift from setup to maintenance: keep one consistent domicile file and one consistent tax-home narrative over time.

You might also find this useful: Tax Home vs. Abode: A Critical Distinction for the FEIE.

Phase 2: The Defensive Strategy - Building Your Audit-Proof File#

In this phase, maintain a consistent evidence trail that supports intent, timeline, and location across your personal, financial, and business records. Build it as you go, not at filing time, so your dates, addresses, and assignment facts stay clean.

Step 1. Capture a dated record trail as changes happen#

Real-time capture usually beats reconstruction. Keep answering these audit questions as the year unfolds: where were you based, where were you working, and when did each fact change? You carry the burden of proof, and travel deductions need extra substantiation, so save records as events happen and keep them organized.

Use one folder with subfolders for domicile, work assignments, travel logs, and old-state tie changes. Each time you update an address, start or end an engagement, book travel, or change a business record, save dated proof such as a statement, contract, portal confirmation, or email.

A simple test helps here: someone unfamiliar with your situation should be able to reconstruct your year from your file without guessing.

Step 2. Prioritize evidence that carries the most audit weight#

Not all records carry equal weight. Start with the records that connect identity, money, business activity, and physical presence.

| Evidence Type | Why It Matters in Audit | How to Store It | Refresh Cadence |

|---|---|---|---|

| Government ID and official address records | Shows whether your legal record trail is internally consistent | Save applications, issuance records, renewals, and change confirmations | At each change and renewal |

| Banking, insurance, payroll, and business account addresses | Shows where your financial and operating center is documented | Save address-change confirmations and first statement after each update | At each change; quarterly spot-check |

| Contracts, engagement letters, invoices, and assignment timelines | Supports your main work area and whether travel was tied to temporary work | Save signed contracts, amendments, invoice batches, and dated timeline notes | At assignment start, change, and end |

| Presence log plus corroborating travel records | Supports day-count and location positions in states that may question residency | Keep a real-time log and match it to flights, lodging, tolls, card records, and calendar entries | Log continuously; reconcile monthly |

| Old-state tie-change records | Supports abandonment of prior domicile and removes conflicting signals | Save closures, terminations, sales, and address updates tied to old-state accounts/assets | As each tie is ended |

If an assignment changes from temporary to expected beyond 1 year, document that change immediately. For federal travel-expense treatment, that expectation shift can make travel expenses nondeductible at that point.

Step 3. Sever old-state ties in priority order#

When you leave a state, clean up the signals that matter most first. Start with the records most likely to shape a residency argument, then work through the supporting ties.

| Priority tier | Tie or record | Article detail |

|---|---|---|

| High-weight first | Legal and address consistency | ID, voter, tax, payroll, insurance, and client/payment tax forms still tied to the former state |

| High-weight first | Financial center | banking, investment correspondence, recurring bills, and other core accounts using the old address |

| High-weight first | Dwelling exposure | any former-state residence suitable for year-round living, especially in states that apply permanent-place-of-abode tests |

| Supporting next | Memberships and similar lifestyle ties | memberships, subscriptions, medical/provider records, storage, and similar lifestyle ties |

| Supporting next | Community indicators | still make the prior state look like your fixed home base |

Work this list in order. If your personal records move but your business records do not, your file becomes inconsistent. Keep entity records, invoices, processor profiles, and business contact details aligned with your current story.

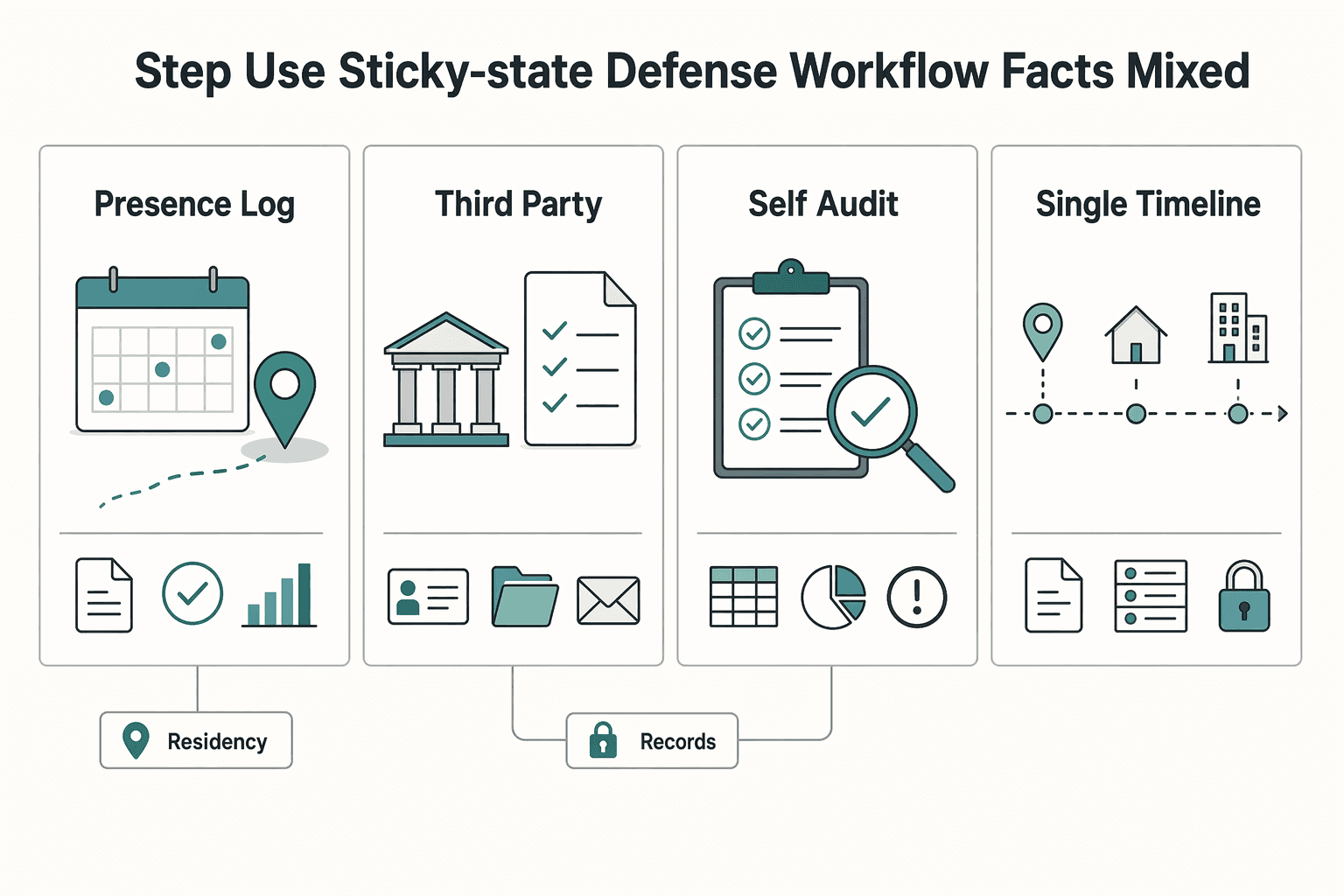

Step 4. Use a sticky-state defense workflow when facts are mixed#

If you keep meaningful ties to a state that closely reviews residency, tighten the process before the facts get muddy.

| Workflow element | What to do | Detail |

|---|---|---|

| Presence log | Keep a real-time state-by-state presence log | Thresholds vary by state; confirm the current rule before relying on a day count |

| Third-party support | Back that log with third-party records | so day counts and locations are verifiable |

| Self-audit | Run a quarterly self-audit | check for conflicts across ID, banking, business, and travel records |

| Single timeline | Maintain a single timeline | show when domicile-related ties ended and when new-state ties began |

Escalate to a CPA or tax attorney when any of these apply:

- For New York analysis, you maintain a former-state dwelling suitable for year-round use for more than eleven months * Your day count is approaching a state trigger (for example, New York's 184-days-or-more test, where any part of a day counts) * Your work assignment expectation changes beyond 1 year * Personal and business records still point to different states after a full cleanup cycle

By quarter-end, your file should support one coherent story without explanation gaps. For a step-by-step walkthrough, see The Tax Implications of a 'Stipend' for a Digital Nomad.

Turn your proof file into a repeatable system with the Tax Residency Tracker so your travel log and residency records stay audit-ready.

Phase 3: The Compliance System - Your Ongoing Operating Procedure#

This only works if you can keep it going month after month. Use one primary location log, backup third-party evidence, one monthly reconciliation, and one quarterly self-audit for tie and record conflicts.

Step 1. Maintain one primary location log#

Pick one source of truth for day tracking and stick to it. Splitting this across notes, inboxes, and memory creates gaps you may not be able to defend later.

Your log should show, by date, where you slept, where you worked, and whether each trip was tied to a temporary business need. Keep a rolling timeline for at least the last 12 months so you always have a dated record ready for an advisor or auditor.

Back up that log with dated third-party records: travel confirmations, lodging receipts, tolls, card charges, calendar entries, or similar evidence. You are not trying to save everything; you are trying to corroborate the timeline.

For each state you monitor, verify the current rules in your tracker. Do not rely on memory, old posts, or the 183-day rule alone. Residency is multi-factor, and day count by itself is a weak shield when home-base or tie signals still point to that state.

| Method | Audit defensibility | Effort | Failure risk | Best use |

|---|---|---|---|---|

| Automated tracker | Can be strong if you export and save data regularly | Low daily effort | App gaps, phone settings, dead battery, missing exports | Frequent movers who want passive capture |

| Manual calendar | Can be solid if updated daily and backed by third-party records | Medium | Missed days, backfilling from memory, vague entries | Lighter travel with strong discipline |

| Hybrid of both | Often the strongest practical option | Medium | Process drift if reconciliation stops | Convenience plus a readable, defensible record |

Month-end checkpoint: your primary log and backup evidence should match without guesswork.

Step 2. Keep your high-weight records aligned#

High-weight records need to match. Tax home and domicile are different concepts, but conflicting records can weaken both your travel-expense position and your state residency position.

Priority records to keep aligned:

- Federal and state tax filings

- Entity records and registered business address

- Contracts, engagement letters, invoices, and payment processor profiles

- Banking, insurance, payroll, and investment account addresses

- Voter registration and ID profile

No single record is universally determinative on its own, so focus on consistency across your records.

If you find a mismatch, fix high-weight records first, then lower-stakes records. Save the correction confirmation and the first statement or document that shows the updated address.

Step 3. Reconcile monthly and self-audit quarterly#

Monthly reconciliation keeps small issues from turning into filing problems. Match your primary log to backup evidence, fill missing records, and annotate any days that need explanation.

Run a quarterly self-audit workflow:

- Collect new proof and file it by category.

- Scan for lingering old-state ties, especially addresses, active accounts, and other home-base signals.

- Flag conflicts across personal, financial, and business records.

- Update one dated timeline showing when ties ended, when new ties began, and where you were physically located.

Step 4. Escalate when the facts stop being clean#

When the facts stop lining up, stop improvising and escalate. Bring in a CPA or tax attorney when records conflict, residency signals are ambiguous, or your timeline no longer supports one coherent story. Also escalate when your work pattern suggests you may not be traveling away from an established business base. That can increase itinerant-worker risk and put travel deductions at issue.

Keep the same cadence through filing season. If you are a US citizen or green card holder, you still file every year on worldwide income, so your logs, addresses, contracts, and timeline should already agree before you file. We covered this in detail in Digital Nomad Tax Residency in Thailand for 2026.

Conclusion: From Anxious Nomad to Confident CEO#

Use this as your end-of-article checklist: set a defensible base, keep proof current, and review compliance on a schedule.

- Offensive: Set your base. Define your federal tax home as the city or general area of your main place of business, and keep it separate from your state domicile, which is one state at a time. Ground it in business facts: where you spend the most working time and where work is centered. Watch assignment length, because work that runs more than 1 year is treated as indefinite for travel-expense rules. If your pattern is effectively "wherever you work," you may be treated as itinerant.

- Defensive: Maintain your proof file. Keep one dated record set that substantiates your expenses and supports notice responses. Keep residency-related records aligned over time so your file is coherent if a state reviews day counts or permanent-place-of-abode facts. Do not wait to rebuild records after a notice arrives.

- Ongoing compliance: Run periodic checks. Review estimated taxes during the year, not only at filing. If you expect to owe $1,000 or more as an individual, estimated payments are generally required; for corporations, the general threshold is $500. Recheck state exposure when travel patterns change, including New York's 184-day resident test element and California's temporary-or-transitory standard. If you receive a notice, respond by the due date and keep copies with your tax records.

Practical rule: prioritize documentation consistency over aggressive tax minimization tactics. If your facts are mixed-state or entity-complex, consult a qualified tax professional before relying on state or federal trigger thresholds.

Related: Moving From Hourly to Project-Based Rates. If your setup spans multiple states or complex income flows, contact Gruv to map a compliant, low-friction operating path.

Frequently Asked Questions

What is the fastest way to establish a new domicile for tax purposes?

There is no one-step shortcut. Update key records in a consistent sequence so your file tells one coherent story, then verify any state-specific step before you rely on it, because compliance obligations vary by state and by income type. If your record updates are split across states or your dates are unclear, talk to a CPA or tax attorney before you file.

How do I prove my domicile if I am a full-time US nomad?

Keep one dated file and keep it current with your travel log and core records. The goal is consistency: your records should support one state position without obvious conflicts. Talk to a pro if you still have major ties in another state or your records point to more than one state.

Can my mail-forwarding address serve as both my domicile and my tax home?

Treat your mail-forwarding address as admin support, not full proof. By itself, it is usually not enough to support either position. Back it with travel logs and consistent legal, financial, and business records, and verify your specific facts before filing.

Can a nomad from California legally stop paying California state taxes?

Document your timeline first, then confirm current California rules before you act. Keep a file with dated tie changes, address changes, and your filing position. Talk to a pro if your facts are mixed or your transition date is not clean.

Which no-tax state is best for a remote professional or business owner?

Choose for operational fit, not from a winner list. Compare states based on practical setup, ongoing admin burden, and how consistently you can document your position over time. Verify current state rules before relying on any move plan.

What happens if the IRS determines I am an itinerant worker?

Treat that as a signal to review any travel-expense position and tighten documentation now. Keep contracts, invoices, calendars, location logs, and expense support aligned so your facts are clear. For category detail, see A Guide to Deducting Business Travel Expenses. Talk to a pro if your work base changes repeatedly or your records were rebuilt after the fact.

Do I still need a tax home if I do not plan to deduct travel expenses?

Separate this decision: even if you skip travel deductions, you still need a defensible state-compliance position. If you are a U.S. citizen, you are still taxed on worldwide income. If you hold foreign financial accounts, verify whether your aggregate balance exceeded $10,000 at any point during the year, because that can trigger FBAR reporting to FinCEN and noncompliance can carry penalties, including potential civil and criminal exposure.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ftb.ca.gov/file/personal/residency-status/index.htmltrusted

- ftb.ca.gov/forms/2024/2024-1031-publication.pdftrusted

- irs.gov/taxtopics/tc511trusted

- irs.gov/businesses/small-businesses-self-employed/bu...trusted

- maine.gov/revenue/sites/maine.gov.revenue/files/inline...trusted

- nycourts.gov/reporter/files/bv/31AD3d.pdftrusted

- tax.ny.gov/pit/file/pit_definitions.htmtrusted

- tax.ny.gov/pubs_and_bulls/tg_bulletins/pit/permanent_pl...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Moving From Hourly to Project Rates Without Hurting Cashflow

The right pricing model matches uncertainty and cashflow risk. It should fit how clearly the work can be defined, approved, and defended, not just what you are used to selling. Hourly billing gives you room to work while requirements are still moving. Fixed project pricing gives the client stronger budget clarity once deliverables are stable enough to pin down.

A Guide to Deducting Business Travel Expenses

**For deducting business travel expenses, use a repeatable compliance system so you only claim costs you can prove.**