Quick Answer

Use a three-gate decision in this order: confirm the buyer’s MAS route, including SIN 54151ECOM when relevant, prove control evidence for CIP and AML plus tax records such as W-9 and W-8 BEN, then test one live integration path. In government buying, feature depth is secondary until those checks pass. Expand only after a constrained pilot shows traceable failures, reconciled outputs, and clear exception ownership.

What Changes When Billing Must Meet Public-Sector Requirements#

For government and public-sector subscription billing, a practical starting point is three verifiable gates in this order: procurement path, compliance evidence operability, and fit with the agency environment you already have to live in.

Public-sector buying has constraints a standard SaaS comparison can miss. GSA says MAS provides access to over 25 million commercial products and services, and its eCommerce and subscription services path explicitly includes federal, state, local, and tribal agencies. But procurement access is only the first gate. Agencies must maintain an agency-wide information security program under FISMA, and FedRAMP continuous monitoring requires recurring evidence monthly, annually, every three years, and as needed.

- Procurement feasibility

Confirm the buyer can acquire the specific offer through a route they already use, such as the General Services Administration Multiple Award Schedule, including SIN 54151ECOM for eCommerce and subscription services. GSA's page, updated Mar 10, 2026, explicitly lists federal, state, local, and tribal agencies, and Cooperative Purchasing can extend some IT buying to eligible state and local governments. If the acquisition path is unclear, feature depth will not move the deal forward. GSA MAS buying guidance also states that for buyers covered by required-use rules, if a commercial product or service meets the need and is available on a governmentwide contract like MAS, they must use it.

- Compliance operability

Treat this as an evidence-production test, not a promise test. In federal cloud contexts, FedRAMP continuous monitoring requires deliverables and supporting evidence on a defined cadence: monthly, annually, every three years, and on an as-needed basis. Validate ownership for evidence generation, review, and retention early. Surface payment-policy interpretation early as well. GSA has clarified that, under specific conditions, an upfront payment is not considered an advance payment.

- Integration reality

Validate the billing model against the agency's current technical estate, not a clean demo environment. GAO reports that for FY 2024, 26 agencies planned about $95 billion in IT spending, with $74 billion for operations and maintenance and $21 billion for development, modernization, and enhancement. GAO also found that, across 11 critical systems it reviewed, 8 used outdated languages, 4 had unsupported hardware or software, and 7 were operating with known cybersecurity vulnerabilities.

Use this list as a filter. If an option is strong on product but weak on MAS route, evidence production, or legacy fit, you may be looking at delay risk rather than a smaller feature gap.

How this list was scored and who should use it#

Use this list when you need a go/no-go decision on a public-sector segment before you commit GTM or engineering resources. It is for offers aimed at Federal agencies, State agencies, Local agencies, or Tribal agencies where the main risk is choosing something that cannot be bought, evidenced, or operated.

- Who this filter is for

Use this frame when the decision is market-entry risk, not feature depth. If your question is whether an offering can be sold and supported without creating procurement or audit debt, this is the right filter.

- How each option was judged

Every option is scored on three gates, in order. Route to buy: Can the buyer acquire it through a path they already use, such as GSA Multiple Award Schedule and, where relevant, SIN 54151ECOM for eCommerce and subscription services? Federal, state, local, and tribal agencies are listed as eligible users for that SIN, but some state, local, territorial, and tribal access may be conditional, so validate eligibility program by program. Compliance controls: Can you produce auditable evidence for identity, entity, and AML controls, including KYC/KYB-like expectations? The checkpoint is operating evidence: written, risk-based identity verification under CIP, beneficial-owner identification and verification for legal entities where required, and ongoing AML internal controls. Implementation burden: How much integration and ongoing operational ownership your team must absorb to run those controls in production.

- What counts as a no-go

If your team cannot produce auditable records for tax and identity flows, treat that as a no-go. Here, that includes evidence for W-9 TIN collection, W-8 BEN documentation where foreign status applies, and 1099-NEC reporting inputs when required. This list is a risk filter, not a product catalog.

For a step-by-step walkthrough, see How to Integrate Your Subscription Billing Platform with Your CRM and Support Tools.

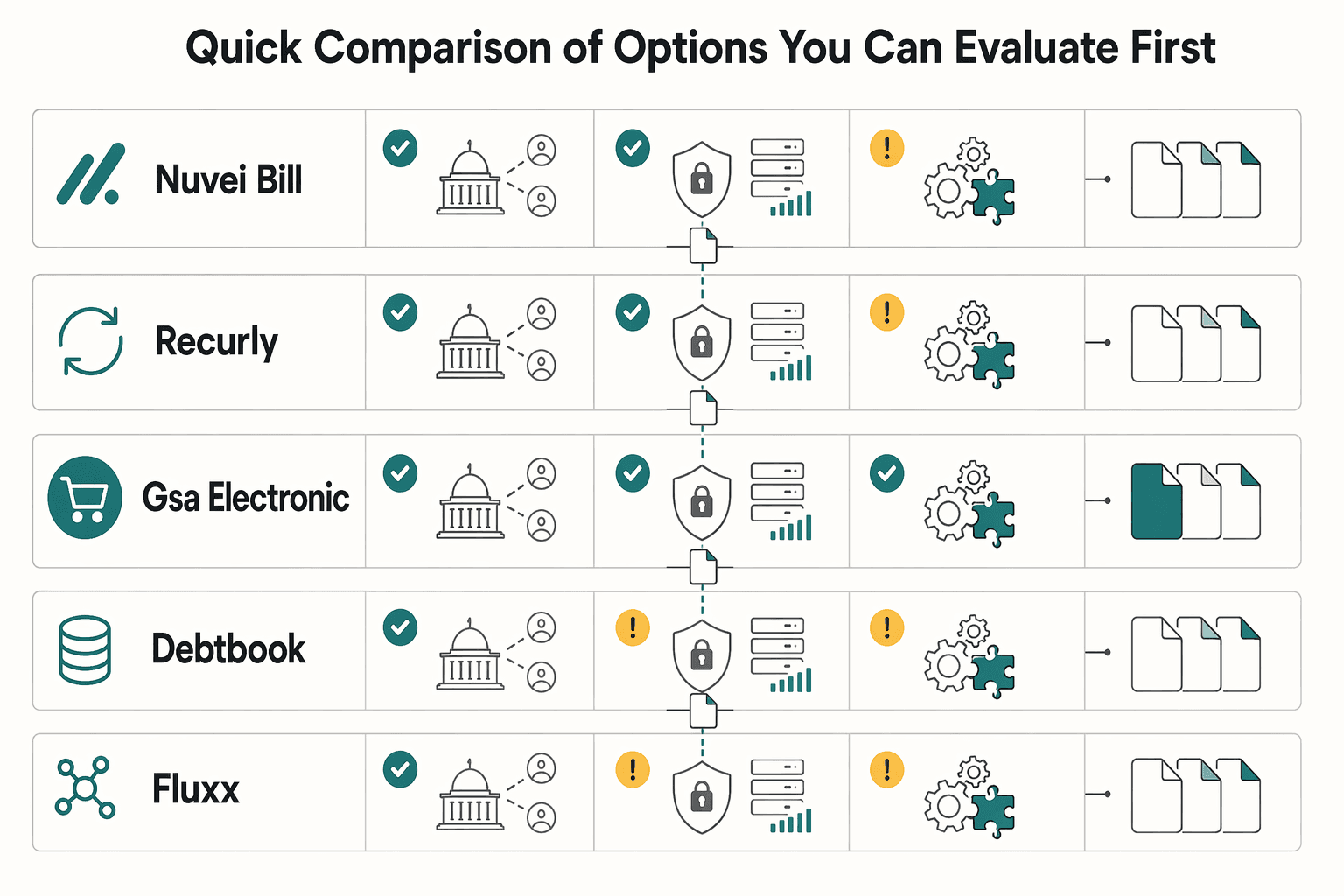

Quick comparison of options you can evaluate first#

Shortlist only the options that pass all three gates in your target segment: buyer access path, control evidence, and implementation burden. In the current evidence, GSA Electronic Commerce and Subscription Services is the clearest verified procurement signal. The vendor options show useful fit signals, but they still need contract and compliance validation.

| Option | Buyer access path | Fit for Federal vs State agencies | Compliance depth from available evidence | Case management surface | Rollout risk | Confidence |

|---|---|---|---|---|---|---|

| Nuvei Bill Pay | No GSA/MAS path confirmed here | Federal: unverified procurement fit. State: plausible agency-payment fit; Nuvei self-reports 30+ states, 3,000+ agencies and municipalities, and 8M+ agency payments/year | Self-reported scale is visible, but no control documentation here proving KYC, KYB, AML, or tax-document ownership | Clearest signal in this set: Nuvei publicly claims deep integration with existing case management software | Medium: self-reported delivery signal is strong, but procurement and control ownership may still block rollout | Mixed: integration and footprint are public claims; control coverage is still unknown |

| Recurly | No specific public-sector procurement route verified in this evidence | Federal: unknown. State: unknown. Verified as a recurring billing platform category, not a confirmed government buying path | General subscription lifecycle capability only in this set | No case-management integration evidence in this set | High if product fit is evaluated before acquisition path and control ownership | Low to medium: category fit is verified; government route and compliance depth are unknown |

| GSA Electronic Commerce and Subscription Services | Verified MAS procurement lane | Federal: strong procurement relevance. State: possible, but state/local access is program-scoped rather than universal | Procurement path only; does not itself prove KYC, KYB, AML, tax, or operational sufficiency | None by itself; this is a buying route, not an integration layer | Low for procurement discovery, high if treated as implementation proof | High for buyer access, limited for everything else |

| DebtBook | No GSA/MAS path confirmed here | Federal: not evidenced. State: stronger fit from public positioning for state/local government finance operations; DebtBook self-reports 2,100 customers nationwide | Finance/accounting positioning is visible, but no payment-control evidence here | No case-management integration evidence in this set | Medium to high: may support finance governance, but this evidence does not show billing or identity-control ownership | Mixed: government finance fit is clearer than procurement and payment-control depth |

| Fluxx | No GSA/MAS path confirmed here | Federal: publicly targeted. State: publicly targeted, alongside local and tribal segments | Fluxx publicly claims built-in compliance features across the grant lifecycle, but this is not payment-level KYC, KYB, or AML evidence | No payment or case-management integration proof in this set | Medium to high: useful for grants oversight, but this evidence does not show payment-infrastructure ownership | Medium for segment fit, low for payment-specific compliance and buying-route proof |

If your main risk is whether agencies can buy your offer, start with the MAS lane and confirm agency-specific eligibility before you proceed. If your main risk is implementation inside existing agency workflows, Nuvei has the strongest integration signal in the current evidence. You still need a named buying path and clear ownership of identity/entity checks and tax evidence where required.

Treat Recurly, DebtBook, and Fluxx as focused tools until they clear the same three gates for your segment. A practical checkpoint is simple: require a concrete acquisition route plus explicit ownership of auditable records for KYC and KYB decisions, AML monitoring, and tax-document or reporting inputs where required. Otherwise, keep the option in "unknown."

Nuvei Bill Pay for agency payment collection and citizen payment experience#

Nuvei Bill Pay stands out here when your immediate goal is to improve how residents pay utilities, courts, permits, and similar agency charges while keeping core systems in place. The caveat is the same throughout this list: this evidence shows delivery fit, but it does not by itself prove your procurement route or compliance-control ownership.

Where Nuvei looks strongest#

Nuvei publicly positions this offer for local, municipal, and state agencies and software providers, with government payment functions that include utilities, courts, property tax, permits, licensing, and parking. It also markets multi-channel acceptance and payment UX features, including POS, IVR phone, AutoPay, eBilling, Text to Pay, Pay by Email, alerts, and notifications.

Nuvei also self-reports operating scale: 8M+ agency payments per year, 3,000+ agencies and municipalities served, 30+ states served, and 2.5B+ processed annually. Treat these as vendor-reported fit signals, not independent audit proof.

Why the integration angle matters#

The integration story is one reason Nuvei is plausible for agency modernization projects that must keep existing back-office tools in place. Nuvei claims 300+ integration partners and transition support, which points to a model designed to fit around existing systems rather than force replacement.

Independent market context points in the same direction. A November 13, 2025 public-sector payments report on Passport highlighted integration with existing municipal systems to speed access to funds and reduce operational complexity. That does not validate Nuvei directly, but it supports the same implementation pattern.

What to verify before you commit#

Do not approve on feature surface alone. Require evidence on these points:

- A named integration path to your current agency software, including data write-back, failure handling, and exception workflows.

- Reporting outputs for payment status, reversals, refunds, and daily reconciliation.

- Channel-level operating detail for AutoPay, IVR, and text or email payment links, including authentication and failed-payment tracing.

- A control map for KYC and AML obligations in your model, including who collects, stores, and can produce required records.

BSA/AML is the U.S. regime for anti-money-laundering and counter-terrorist-financing controls, and CIP is part of an AML compliance program. If your flow depends on customer identification evidence, you need explicit ownership boundaries.

The main risk to keep in view#

The main risk is buying into a better citizen payment experience, then stalling in procurement or compliance review. In the current evidence, Nuvei is not shown as purchasable through GSA MAS or another specific federal vehicle. Transaction-level KYC and AML ownership is also not fully documented. For federal targets, resolve those gaps first. For local utility or court modernization, proceed only with a named integration plan and a defensible evidence pack.

Recurly for subscription lifecycle management in public and nonprofit contexts#

Recurly is worth evaluating when the gap is subscription lifecycle control, not procurement certainty. If you already have payment rails and need stronger handling from sign-up through cancellation or upgrade, it can make sense. Do procurement and legal checks before you start integration work.

Recurly's government and nonprofit positioning is explicit, and it claims lifecycle coverage across recurring billing, payments orchestration, revenue recognition, reporting, and analytics. It also states multiple integration methods, including APIs, JavaScript, webhooks, hosted account-management and payment pages, and API-based two-way communication with ERP, CRM, and data-warehouse systems.

Where Recurly looks strongest#

The clearest use case is a platform that already knows how funds move but needs better control over plans, renewals, upgrades, cancellations, and recurring invoicing. Recurly also frames public and nonprofit usage in similar terms, including annual billing for access to reports or databases.

Configuration flexibility is another practical strength. Recurly documentation says its billing models support 140+ currencies, which can matter for nonprofits or mixed public-private programs.

The procurement checkpoint that matters most#

The main limit in this dataset is straightforward: it does not show Recurly itself holds a GSA award. GSA does show that this category is buyable through MAS under SIN 54151ECOM for federal, state, local, and tribal agencies, but that does not confirm this specific vendor is on that vehicle.

For federal opportunities, confirm the acquisition path before you lock architecture. FAR 8.405 requires schedule ordering procedures when placing schedule orders or BPAs, and GSA MAS guidance says required-use contracts must be used when available. If you cannot name the path, whether direct, partner, or another approved vehicle, pause build-out.

What to verify before you commit#

You need an evidence pack, not a feature walkthrough. Confirm:

- Acquisition path by buyer type, including whether SIN 54151ECOM, another vehicle, or a partner route is required.

- Security and compliance artifacts you can review. Recurly indicates document access through a trust-center request form.

- Control ownership boundaries. Recurly cites PCI DSS, SOC 2, HIPAA, and GDPR, but verify separately whether it offers native KYC, KYB, or AML workflows for government-specific payment compliance.

- Integration proof for your stack, including webhook behavior, two-way ERP and CRM sync, cancellation state handling, failed-payment tracing, and reconciliation outputs.

A common failure mode is treating subscription maturity as full public-sector readiness. Recurly can be a strong subscription layer, but the requiring agency still provides applicable regulatory and statutory requirements during schedule ordering under FAR 8.404. Use Recurly when lifecycle depth is the gap, and move only after the acquisition route and compliance ownership are explicitly documented.

If you want a deeper dive, read How to Build a Subscription Billing Engine for Your B2B Platform: Architecture and Trade-Offs.

GSA MAS route for procurement feasibility before technical build#

Start with the General Services Administration (GSA) route when procurement feasibility is the biggest risk, not product capability. If you do not know whether the agency can buy from you, resolve that before scoping integrations.

| Check | What to confirm | Grounded detail |

|---|---|---|

| Buyer authorization | The target buyer is an authorized ordering activity for your route | Access may be direct MAS, Cooperative Purchasing, Disaster Purchasing, or another path |

| Contract alignment | The planned procurement path aligns to the relevant MAS contract route | Electronic Commerce and Subscription Services under SIN 54151ECOM is the lane named in the article |

| Post-award roles | What stays with your team versus the agency after award | GSA guidance says the agency manages the orders it places under MAS contracts |

One strong signal is Multiple Award Schedule (MAS), especially Electronic Commerce and Subscription Services under SIN 54151ECOM. GSA says federal, state, local, and tribal agencies can simplify procurement for eCommerce and subscription services through MAS (page last updated Mar 10, 2026). For federal buyers, FAR Subpart 8.4 describes MAS as a simplified process for obtaining commercial supplies and services. GSA also reported $51.5 billion in FY 2024 MAS sales, indicating this channel operates at significant scale.

Use that as a buy-path check, not an implementation verdict. MAS can indicate a purchasing route, but it does not confirm KYC, KYB, AML, tax-document, security, or integration readiness. It also does not mean every state, local, territorial, or tribal entity can buy the same way. GSA notes some non-federal access is conditional and may run through Cooperative Purchasing or Disaster Purchasing programs.

Before committing engineering time, verify three items in writing:

- Whether your target buyer is an authorized ordering activity for your route, and whether access is direct MAS, Cooperative Purchasing, Disaster Purchasing, or another path.

- Whether your planned procurement path aligns to the relevant MAS contract route and SIN 54151ECOM.

- What responsibilities remain with your team versus the agency after award, since GSA guidance states the agency manages the orders it places under MAS contracts.

The failure mode is treating procurement visibility as implementation readiness. If you cannot name the buyer type, ordering path, and exact contract route, pause architecture work.

DebtBook for budgeting and subscription cost governance in government finance teams#

DebtBook fits best when the question is finance governance, not checkout, collections, or tax operations. For State agencies and Local agencies trying to control subscription sprawl before adding another vendor, the available evidence points first to budgeting and contract visibility.

DebtBook positions itself as treasury and accounting software for government and nonprofit teams, and it explicitly markets to state and local government organizations. Its published capabilities emphasize centralizing contract portfolios, tracking spend, and managing post-signature agreements, with visibility into obligations, vendor relationships, and renewal trends.

A clear use-case signal here is SBITA tracking under GASB Statement No. 96, not payment processing. GASB defines SBITAs as contracts conveying the right to use another party's IT software. Washington State's Office of Financial Management says the state uses DebtBook for lease and SBITA tracking tied to GASB 87 and 96 compliance, implemented in fiscal year 2024.

If you evaluate DebtBook, confirm one workflow in a live demo: can your team follow one software agreement from contract record to SBITA classification, spend tracking, and renewal date across one connected workflow? DebtBook states native integration between its Contract Management and Lease/Subscription Management applications, so validate that exact record flow.

Do not treat this as proof of billing or downstream compliance coverage. The available material does not confirm deep case-management integration, payment controls, or built-in 1099 preparation or filing. Keep those ownership boundaries explicit, especially with IRS Publication 1099 changes effective for tax year 2026 / processing year 2027.

Fluxx for compliance program management around grants and regulated operations#

Fluxx can be a stronger fit when your core need is grants compliance inside program operations, not payment-rail controls. It is most credible here as Government compliance software for award workflow and oversight.

Fluxx describes a secure, cloud-based government platform spanning the full grant lifecycle: intake, review, award, monitoring, and reporting. It also positions the product for federal, state, local, and tribal governments, with automated workflows, built-in compliance features, and reporting. That can make it a practical option when your requirements are tied to 2 CFR Part 200 program obligations rather than recurring billing mechanics.

Its clearest documented advantage is workflow-level compliance. Fluxx says processes can run from Notices of Funding Opportunities and pre-award applications through post-award payments and requirements. It also cites SAM.gov integration and controls like SSO, MFA, role-based access control, and attribute-based access control. For public-sector teams, that is a stronger oversight signal than a billing-engine signal.

If you evaluate Fluxx, validate one end-to-end path in a demo: application intake, review, award decision, monitoring milestone, SAM.gov validation, and reporting output. Then confirm who can view, edit, and approve each step, and how Fluxx's FedRAMP-compliant cloud hosting claim maps to your agency review.

Do not treat "post-award payments" as proof of transaction-level KYC, KYB, or AML controls. The available evidence does not confirm those functions, so use Fluxx alongside payment infrastructure when those controls are required.

Choose by risk lane not by feature list#

The cleanest way to decide is to separate the risk lanes and treat each one as a gate. Do not let a polished demo or better UX hide the real blocker.

| Lane | Exact anchor to test | What a pass looks like | If it fails |

|---|---|---|---|

| Procurement | GSA Multiple Award Schedule, especially SIN 54151ECOM for Electronic Commerce and Subscription Services | You can name the buying path for your target agency type and confirm the buyer is eligible to use it | Stop and resolve the route to buy before more product work |

| Compliance | CIP, beneficial ownership identification, risk-based AML program, tax forms such as W-9 and W-8BEN | You can show who collects, verifies, stores, and exports each control artifact | Redesign scope and control ownership |

| Delivery | Real integration path with an existing case-management workflow and one constrained payment journey | You can map the data handoff, exception handling, and reporting output for one live use case | Shrink rollout to one use case |

1. Procurement lane first#

If procurement does not clear, stop. A buyer can like your product and still be unable to purchase it through the route you assumed.

Use the GSA Multiple Award Schedule and, for this category, SIN 54151ECOM as concrete checks. MAS includes federal, state, local, and tribal governments, plus other eligible buyers, and SIN 54151ECOM lists federal, state, local, and tribal agencies as eligible users. But non-federal access can depend on program-specific authorities, including Cooperative Purchasing or Disaster Purchasing.

Ask procurement to name the exact contract vehicle, the applicable SIN, and the agency authority to use it. If that stays unclear, treat it as a fail. A strong payment UX does not fix an unclear procurement path.

2. Compliance lane needs named controls and named owners#

A purchasable route is not a defensible control posture. If nobody can show ownership for identity checks, beneficial-owner verification for legal entities, AML review, and tax-document handling, you have a gap.

CIP requires minimum customer information before account opening, including items such as name and address, and date of birth for individuals. Legal-entity due diligence requires beneficial-owner identification and verification at account opening. AML expectations are risk-based.

For review, ask for evidence artifacts, not policy statements: what data is collected, when it is verified, where exceptions go, and how records are exported. Include tax handling in the same packet. W-9 is used for TIN collection, W-8BEN for foreign beneficial-owner withholding status, and the 1099 e-file threshold is 10 returns effective for filings on or after January 1, 2024. If the flow is unclear, redesign scope before launch.

3. Delivery lane is where you narrow scope#

If delivery is weak, reduce scope to one use case and one integration path. That aligns with FAR modular contracting, which is intended to reduce program risk.

Do not accept "it integrates with case management software" as proof. Validate one concrete flow: what record moves, when it moves, and what happens on failure. Test failed payments, duplicate identities, and reconciliation output. Since the current evidence does not verify deep integrations for named options, require field-level mapping and a sample exception report before expanding.

Weight the matrix like a buyer would#

Use a weighted matrix that puts procurement and compliance blockers above convenience features. FAR requires evaluation factors and their relative importance to be clearly stated, and those factors must support meaningful comparison. FAR 15.101-1 allows tradeoffs, but higher-priced selections must be justified and documented.

A practical rule is simple: if an option is strong on UX or reporting polish but weak on buyer eligibility, CIP evidence, beneficial-owner handling, or tax-document ownership, it should not survive the shortlist.

Use this point in your evaluation to map procurement, compliance, and delivery gates into an implementation checklist in the Gruv docs.

Validate in 90 days before scaling engineering and GTM#

Use a 90-day window as an internal validation cycle, not a launch promise. If route to buy, one live delivery path, and auditable control evidence are not verified in that window, pause expansion before engineering and GTM assumptions harden.

| Window | Focus | Evidence |

|---|---|---|

| Days 1-30 | Lock buyer segment and confirm route to buy | Name the contract vehicle, applicable SIN, and buyer authority; distinguish Federal agencies from state, local, and tribal agencies |

| Days 31-60 | Run one constrained pilot | Test one payment journey, one integration path, and one reporting output; keep field mapping, a sample exception report, and logs for failed payments, duplicate identities, timeouts, and record mismatches |

| Days 61-90 | Replace policy claims with operating evidence | Verify identity and AML controls, designated ownership, internal controls, independent testing, personnel training, and exportable Form W-9, Form W-8 BEN, and Form 1099-NEC outputs with an audit trail |

Days 1-30#

First, lock the buyer segment: Federal agencies or state, local, and tribal agencies. That choice can change procurement eligibility.

For eCommerce and subscription buying, the Multiple Award Schedule and SIN 54151ECOM are practical checkpoints, and eligible users are listed as federal, state, local, and tribal agencies. But non-federal access can depend on authorities such as Cooperative Purchasing or Disaster Purchasing, so treat "public sector" as too broad for planning.

Your checkpoint is documentary: name the contract vehicle, the applicable SIN, and the buyer authority for that agency type. Keep a short evidence pack with those items. If this is unclear, the pilot baseline is weak.

Days 31-60#

Run a constrained pilot: one payment journey, one integration path, one reporting output. This aligns with FAR modular contracting's risk-reduction logic through successive interoperable increments.

Use one concrete flow into a downstream system (for example, case management software) and test it end to end: what record moves, which fields move, when handoff happens, and what happens on failure. If integration is claimed, require field mapping and a sample exception report.

Log failures explicitly, for example failed payments, duplicate identities, timeouts, and record mismatches. If failures cannot be traced from source to destination, do not treat the implementation as scale-ready.

Days 61-90#

Treat this phase as a control-evidence test for finance and legal review. Replace policy claims with operating evidence.

For identity and AML-related controls, where Customer Identification Program standards are the benchmark for you or your regulated partners, verify what data is collected, when identity is verified, how exceptions are handled, and who owns day-to-day review. For AML operations, confirm evidence of internal controls, independent testing, designated day-to-day ownership, and personnel training.

Validate tax-document and reporting operations with the same rigor. Form W-9 supports TIN collection, Form W-8 BEN supports foreign beneficial-owner withholding documentation, and Form 1099-NEC may be relevant for nonemployee compensation reporting. Because IRS information-return penalties can apply to late or incorrect filing, verify that outputs are generated, reviewed, and exportable with an audit trail.

No-go triggers#

Stop scaling if any of these remain unresolved:

- Procurement eligibility is assumed, not verified, for the actual buyer type

- Control ownership is unclear for identity, AML review, or tax-document and reporting operations

- Finance or legal cannot obtain auditable records from pilot operations without manual reconstruction

Scale only when procurement path, control evidence, and integration and failure handling all hold under live conditions. For a related example, see Gift Subscriptions and Prepaid Plans for Platform Billing Without Cleanup Chaos.

Red flags that should pause a public-sector subscription launch#

If these gaps are still open, pause the launch. In this market, you need a provable buying path, a mapped control model, and auditable operating evidence for the exact agency type you plan to serve.

| Red flag | Why it pauses | Required proof |

|---|---|---|

| Acquisition path is unnamed | The team cannot name the schedule path, relevant SIN, and buyer eligibility authority | Document agency type, contract vehicle, and purchase authority in one short note |

| Controls are described as covered but not mapped | CIP, beneficial-owner checks, AML, and tax support are not tied to operating steps and owners | Show what data is collected, when verification happens, who handles exceptions, and where W-9 and W-8BEN records are stored |

| References are driving vendor choice | References are not auditable operating evidence while integration details remain undefined | Require a field map, a sample exception report, and one traced transaction from source to destination |

| One public-sector motion is assumed | Federal and local buying conditions are treated as interchangeable even though state and local MAS access is program-based | Rework CAC, timeline, and implementation package by agency type |

| Full build is funded before pilot criteria exist | A pilot without clear objectives and a formal data strategy is not a validation step | Define success, required data, no-go triggers, auditable logs, exportable records, and 1099-NEC readiness for the January 31 deadline |

- You cannot name the acquisition path for the target buyer.

If you can describe features but cannot name the route to buy, you are not launch-ready. Federal buying follows FAR-wide rules, and FAR 8.4 provides a simplified path through Federal Supply Schedules. If your team says "GSA" or "MAS" but cannot name the schedule path, relevant SIN, and buyer eligibility authority, treat that as unresolved risk. At minimum, document agency type, contract vehicle, and purchase authority in one short note. If that note does not exist, pause.

- Your compliance answer is "covered," but no one can map controls end to end.

Pause when claims about customer identification, beneficial-owner checks, AML, and tax support cannot be tied to operating steps and ownership. Covered banks must implement a written CIP, AML programs require internal controls and independent testing, and legal-entity due diligence includes beneficial-owner information. If your team uses "KYB," map it to the underlying legal-entity and beneficial-owner checks, then show the flow: what data is collected, when verification happens, who handles exceptions, and where W-9 and W-8BEN records are stored. If no owner can walk that flow start to finish, stop.

- Vendor choice is driven by references while integration details remain undefined.

References can shortlist vendors, but they are not auditable operating evidence. Require a field map, a sample exception report, and one traced transaction from source to destination, including timeout, duplicate-identity, and record-mismatch handling. If finance or legal would still need manual reconstruction, readiness is not there. If the integration cannot survive a field-level walkthrough, pause.

- Pricing assumes one public-sector motion across different buying conditions.

Pause if federal and local motions are modeled as interchangeable. State and local MAS access is program-based, and Cooperative Purchasing is limited to certain categories and SINs. That can change effort, timeline, and implementation overhead by agency type even for the same product. If your model still uses one CAC, one timeline, and one implementation package for both, rework it before launch.

- You are funding full build before pilot pass or fail criteria are explicit.

A pilot without measurable objectives and a defined data-gathering method is not a validation step. Federal IT guidance supports prototyping before implementation, and pilot evaluation practice emphasizes clear objectives plus a formal data strategy. Define success, required data, and no-go triggers before scaling build spend. Include operational outputs, not demos only: auditable logs, exportable records, and reporting readiness. If the pilot cannot produce reviewable tax outputs where required, including 1099-NEC readiness for the January 31 deadline, delay launch.

Related: FTC Click-to-Cancel Rule: What Subscription Platforms Must Build Before the Deadline.

Conclusion#

The order matters: can agencies buy it, can compliance defend it, can operations run it. Treat those as hard gates, because passing one does not prove the others.

- Procurement gate

Confirm a real route to buy before integration work. GSA places eCommerce and subscription services under MAS, with SIN 54151ECOM as the lane to check, and eligibility for state, local, territorial, and tribal buyers may depend on programs such as Cooperative Purchasing or Disaster Purchasing. If your team cannot name buyer type, MAS route, and program clearly, procurement is not validated.

- Compliance gate

Treat control evidence as separate from procurement eligibility. In the relevant bank/MSB contexts, that means ongoing Customer Due Diligence for banks, beneficial-owner procedures where applicable for covered financial institutions, and an effective AML program for MSBs, plus tax-document handling tied to Form W-9 and Form W-8 BEN-E when relevant. Reporting operations should also show, where 1099-NEC rules apply, how nonemployee compensation of $600 or more is identified, how the general January 31 filing timing is supported, and whether the 10 or more returns e-filing threshold is handled.

- Operations gate

Run a constrained pilot designed to collect decision-grade evidence. Validate one payment journey, one downstream integration, one reconciliation path, exception handling, and ownership of unresolved issues. If all three gates clear with defensible evidence, expand in stages. If any gate fails, pause and re-scope before costs compound.

Choose the option that survives all three gates with evidence, not the one with the longest feature list. If your pilot is close to go/no-go, align market coverage, compliance gating, and rollout scope with your team in a focused planning call.

Frequently Asked Questions

What are the table-stakes capabilities for subscription billing in government and public-sector platforms?

You need three basics: a usable buying path, defensible control evidence, and an integration finance can reconcile cleanly. On procurement, name the MAS path, the relevant SIN where applicable, and whether your buyer is federal or only conditionally eligible through programs such as Cooperative Purchasing. On controls, require identity checks, tax-profile capture, and exportable records tied to Form W-9, W-8 documentation, and downstream 1099 reporting workflows.

How is procurement risk different from payments compliance risk when choosing a platform?

Procurement risk asks whether the agency can buy your product, and through which route. GSA positions eCommerce and subscription services under MAS, with ordering for eligible agencies through eBuy and GSA Advantage, but non-federal access is conditional in GSA program language. Payments compliance risk is separate. It is whether you can prove written CIP procedures, risk-based identity verification, AML internal controls, independent testing, and beneficial-owner procedures where applicable.

When should a team prioritize a GSA and MAS path before product integration work?

Prioritize it first when your motion depends on federal buyers or your team cannot name the exact acquisition route yet. FAR Subpart 8.4 provides a simplified federal process, but only when the buyer can use the schedule path in scope. If your team is still saying “GSA” without a defined MAS lane and buyer eligibility, integration work is early.

What evidence should we require to validate KYC, KYB, AML, and tax-document controls?

Require an evidence pack, not a capability slide. At minimum, ask for mapped CIP logic, identity-verification checkpoints, exception handling, AML internal controls, independent testing evidence, and written beneficial-owner procedures for legal-entity customers. On tax documentation, require sample W-9 and W-8 capture flows, storage and retrieval evidence, and reporting extracts that support 1099-NEC and 1099-MISC production.

How do we compare Nuvei Bill Pay, Recurly, DebtBook, and Fluxx when source detail is uneven?

Use three buckets: verified procurement evidence, verified control evidence, and vendor claim only. Nuvei markets configurable government payments and publishes volume metrics, while Recurly, DebtBook, and Fluxx market recurring-billing, GASB 96 subscription management, or grants-lifecycle compliance capabilities. Treat all of those as vendor claims unless you can separately verify procurement eligibility and control operation.

What is a practical first 90-day sequence to test feasibility before full rollout?

Use it as a feasibility test sequence, not a guarantee. In days 1-30, lock buyer type and confirm route-to-buy assumptions against MAS and agency eligibility, including whether state or local access applies to your case. In days 31-60, run one constrained payment journey and one source-to-destination integration. Then in days 61-90 produce an audit-ready evidence pack: identity checks, beneficial-owner handling where relevant, W-9 records, W-8 records where requested, and reporting outputs finance can use directly.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/subpart-8.4trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- gsa.gov/technology/it-contract-vehicles-and-purchasi...trusted

- gsa.gov/buy-through-us/purchasing-programs/multiple-...trusted

- irs.gov/payments/information-return-penaltiestrusted

- irs.gov/forms-pubs/about-form-w-9trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Build a Subscription Billing Engine for Your B2B Platform

If you are designing a B2B subscription billing engine, get the close and reconciliation model right before you chase product flexibility. A durable sequence is to define recurring billing scope (plans, billing periods, usage, and trials), then map settlement and payout reconciliation to transaction-level settlement outputs, and finally tie that discipline into month-end close controls. The real test is simple: finance should be able to trace invoices, payments, and payouts from source events through settlement records into reconciled close outputs without ad hoc spreadsheet rescue.

FTC Click-to-Cancel Rule Status: 6 Controls Subscription Platforms Should Prioritize

This article gives you a decision-ready baseline for what to build, test, and document now, based on what is clear in FTC and Federal Register records and what is still unsettled.

How to Migrate Your Subscription Billing to a New Platform Without Losing Revenue

If you need to **migrate subscription billing platform without losing revenue**, treat it as a revenue operations change, not a simple software swap. Billing migrations sit close to renewals, revenue reporting, and payment credentials, so mistakes rarely stay technical. They can show up as duplicate records, inaccurate revenue reporting, failed renewals, or customer-facing downtime.