Quick Answer

For payment platform compliance in the Netherlands, first decide whether your model falls within PSD2-relevant payment activity and whether DNB licensing questions need legal escalation. Then map who controls collection, holds, conversion, and payouts, set KYC, AML, monitoring, and reporting ownership, keep audit-ready evidence, and treat invoicing as a separate track before launch.

What Payment Platforms Need to Know About DNB and PSD2#

For payment platform compliance Netherlands, start with the perimeter question: does your model touch activity covered by PSD2, and do licensing questions tied to De Nederlandsche Bank (DNB) need escalation before you scale?

This matters when you run contractor, seller, or creator payouts, where product, treasury, and compliance decisions overlap. When the perimeter is unclear, teams can overbuild low-value process in one area and miss the real exposure elsewhere.

PSD2 is the anchor. DNB describes PSD2 as European legislation on consumer and business payments, introduced in the Netherlands in February 2019. If your model includes access to payment-account data, three first-pass checks matter:

- access is based on user consent

- the requesting firm holds a DNB licence or a licence issued in another EU Member State

- doubtful requests are checked against the DNB licence register

DNB also flags a practical failure mode: some access requests may be phishing attempts to obtain login or PIN credentials. If your team handles bank connectivity, embedded finance features, or third-party payment-data access, treat suspicious credential requests as a security and compliance event.

Purpose limitation matters just as much. DNB states that accessed payment data may only be used for the purpose for which access was granted, with compliance monitored by DNB and the Dutch Data Protection Authority. So data-access decisions are not only technical. You need a clear internal record of purpose and controls that keep downstream use inside that boundary.

This article is for compliance, legal, finance, and risk owners deciding what to build now and what to escalate. The goal is practical: identify potential DNB licensing questions, place PSD2-aligned controls where they matter, and be clear about where specialist legal confirmation is still required.

Define the regulatory perimeter before you design controls#

Get the scope right before you design controls. In the Netherlands, an early control decision is whether your flow is a regulated payment service at all. If you get that wrong, teams can either overbuild controls for out-of-scope activity or miss a licensing issue that should have been escalated early.

Keep the legal anchors distinct. The Wft is the principal Dutch financial-regulation base, DNB is a practical supervisory reference point for perimeter questions, and PSD2 is part of the framework DNB references for commercial-agent analysis. As a concrete checkpoint, DNB points to Wft Section 1:5a(2): services listed there do not qualify as payment services and therefore do not require a licence.

Treat exemptions as conditional, not automatic. DNB's commercial-agent exemption applies only if the agent acts for one side only (payer or payee) and the required conditions are met, including an agreement proving authorization by the payer or payee. If your contracts or operating model show you acting for both sides, DNB's position points back to payment-services-provider treatment. That agreement then becomes core perimeter evidence.

Keep three tracks separate#

Keep three tracks separate from day one and run them in parallel:

| Track | Primary focus | Article note |

|---|---|---|

| Licensing and supervision | PSD2/Wft perimeter analysis | DNB as the supervisory checkpoint |

| KYC and AML operations | Wwft obligations | Including the transposed 4th and 5th EU AML Directives |

| Invoicing and tax | Operationally important | Not a substitute for licensing analysis |

Document known unknowns explicitly. The current evidence does not confirm exact authorization thresholds or exemption cutoffs. The cited EBA consultation response also notes that some threshold-setting details are not defined and may produce fragmented supervisory practice. If your model depends on an exemption, record that dependency, the supporting contract evidence, and the trigger for mandatory legal review.

Map your payment flow to likely Dutch licensing exposure#

Map the flow before you debate controls. If your team may control money movement or timing, escalate early. Treat that control as an internal trigger for PSD2 legal analysis, not as a legal conclusion that a licence is required.

Use this as a screening map for counsel. Confirm exact PSD2 trigger mapping for collect, hold, convert, and payout with a qualified adviser.

| Flow step | What to document for review | Escalate legal review when (screening signals) |

|---|---|---|

| Collect | Who initiates collection, who can stop or retry it, and how the user-facing flow describes your role | There are signs your team may control start, stop, or retry decisions, or the product presents your platform as taking payment |

| Hold | Where funds sit in the process, who can delay release, and what policy controls exist | There are signs your team may place holds, delay release, batch settlement, or otherwise influence release timing |

| Convert | Who performs conversion, where timing decisions sit, and what users are told | There are signs your team may control whether or when conversion happens before payout |

| Payout | Who sets destination, schedule, retries, and release conditions | There are signs your team may change payout timing, destination, or release conditions |

Compare operating model choices before scale#

A direct regulated model and a partner-led model need different control setups. Use counsel to map where control, accountability, and evidence obligations sit in each model. Keep that comparison factual in your review pack, and do not assume one model is automatically faster or lighter.

If direct authorization is plausible, align early with DNB licence-note expectations for payment service providers. In those notes, ICT outsourcing and major ICT incident classification, follow-up, and reporting are routed to DORA as of 17 January 2025. The notes also reference Chapter V (Articles 28-30), Chapter III (Articles 17-20), and RTS/ITS templates and timelines for incident reporting.

Build a usable evidence pack#

Counsel should not have to reverse-engineer your model from scattered documents. Prepare a compact set of materials they can test quickly:

- Product and funds-flow diagrams showing actors, account touchpoints, and decision points

- Contract role allocation and customer-facing terms that describe responsibilities consistently

- Operational notes on manual interventions, for example holds, batching, retries, and exception handling

The key quality check is consistency. If diagrams, contracts, UI copy, and operations tell different stories, licensing analysis slows down and becomes less reliable.

Set ownership and escalation points before launch#

Set ownership before go-live. If escalation is ambiguous, KYC, AML, incident handling, and reporting quickly become side work, and gaps follow.

In the Netherlands, De Nederlandsche Bank (DNB) conducts integrity supervision of payment service providers, and its supervisory materials describe integrity risk as increasingly cross-sectoral. Treat that as a governance design input. Compliance should not own this alone. Name responsibilities across product, risk, legal, and finance so control changes can be reviewed consistently.

Build a RACI around decisions, not teams#

Your RACI should be built around decision rights, not department labels. It should define who decides, who reviews, and who is informed when live controls change.

| Work area | Primary owner (internal choice) | Consulted functions | Sign-off focus |

|---|---|---|---|

| Reporting and supervisory communications | Compliance or legal | Risk, finance | Whether an event needs internal or external escalation, what evidence is complete, and who submits |

| KYC and AML controls under Wwft assumptions | Compliance | Legal, risk, product | Whether control logic still matches legal assumptions, customer journey, and risk posture |

| Incident handling for payment operations | Risk or operations | Compliance, legal, product, finance | Customer impact, integrity impact, remediation, and whether regulator-facing review may be needed |

Assign one accountable owner per area, and consider a second review for material control changes. DNB's findings are grounded in 2024 examinations and evidence inputs, so your model should produce reviewable artifacts, not informal decisions.

Make escalation triggers explicit#

Write the triggers down before launch, or change drift will make the call for you. Internal triggers may include:

- new corridor or country pair

- new payout method

- declining transaction monitoring alert quality, for example unexplained false-positive spikes or scenario gaps

- material updates in DNB or other relevant supervisory guidance

For each trigger, use the same evidence pack: updated funds-flow diagram, impacted controls, customer-facing wording, monitoring-scenario changes, owner, approver, and effective date. Consistency is the control. Mismatched diagrams, product behavior, and review notes can become a failure mode.

Separate Wwft-driven changes from commercial tuning#

Not every change needs the same review path. Classify changes before production updates: either they affect Wwft assumptions and integrity controls, or they are commercial policy.

One workable model is to route changes affecting KYC logic, AML review logic, case handling, or monitoring scenarios through compliance and legal review before release. For commercial changes, product can lead, while risk and compliance confirm that the control chain did not move. Keep a guardrail on "simplification": faster approval paths help only if evidence quality and second-review discipline stay intact.

Related reading: KYC Best Practices for Reducing Money Laundering Risks: A Payment Platform Compliance Guide.

Build KYC and AML controls as ongoing operations#

Treat KYC and AML as live operations, not a one-time onboarding task. In the Netherlands, KYC verification is a legal requirement, grounded primarily in the Anti-Money Laundering and Anti-Terrorist Financing Act (Wwft), with related context from the Financial Supervision Act. The practical test is whether identity, risk, monitoring, and payout decisions stay connected after account approval.

Risk can change after onboarding. Profiles, payout setups, and transaction behavior can change, so your controls should adapt in production.

Define the minimum control chain#

Start with a complete chain, even if it is simple: identity capture, verification, risk tiering, periodic review, event-driven refresh, and case closure standards.

| Control stage | What should happen | What the product should do | What you should be able to evidence |

|---|---|---|---|

| Identity capture | Collect required customer data and documents for the account type | Keep the account restricted until required inputs are complete | What was submitted, when, by whom, and for which person or entity |

| Verification | Confirm identity details and record the result | Grant only permissions that match the verified state | Verification outcome, timestamp, reviewer or vendor result, and exceptions |

| Risk tiering | Assign an initial risk level | Apply review depth and payout permissions for that tier | Risk tier, rationale, and approval record |

| Ongoing review | Revisit the profile on your documented cadence by risk | Surface pending reviews before unrestricted payout continues | Review due date, notes, outcome, and control changes |

| Event-driven refresh | Re-check when profile or behavior materially changes | Pause or narrow payout access until refresh is resolved where appropriate | Trigger event, refresh request, decision notes, and release approval |

| Case closure | Close alerts and KYC/AML cases against documented internal standards | Release holds only when closure conditions are met | Case notes, linked evidence, timestamps, and final disposition |

The tradeoff is real. You need to reduce fraud risk while minimizing friction for legitimate customers. If you lower friction by letting transactions proceed while verification or review is unresolved, downstream AML follow-up can increase.

Make risk changes drive product changes#

A risk decision that does not change product behavior is not much of a control. If risk increases or the profile materially changes, re-verify what changed and tighten payout permissions until review is complete.

| Scenario | Required step 1 | Required step 2 |

|---|---|---|

| Key profile or payout details change | Trigger re-verification | Hold new payout instructions until review is complete |

| Transaction patterns no longer fit the original profile | Raise the risk tier | Route activity into enhanced review before releasing queued payouts |

| Monitoring produces a material alert that cannot be closed with complete evidence | Keep the hold in place | Escalate |

You do not need external numeric thresholds to run this well. You do need documented internal rules, named approvers, and a visible link between case outcomes and payout state.

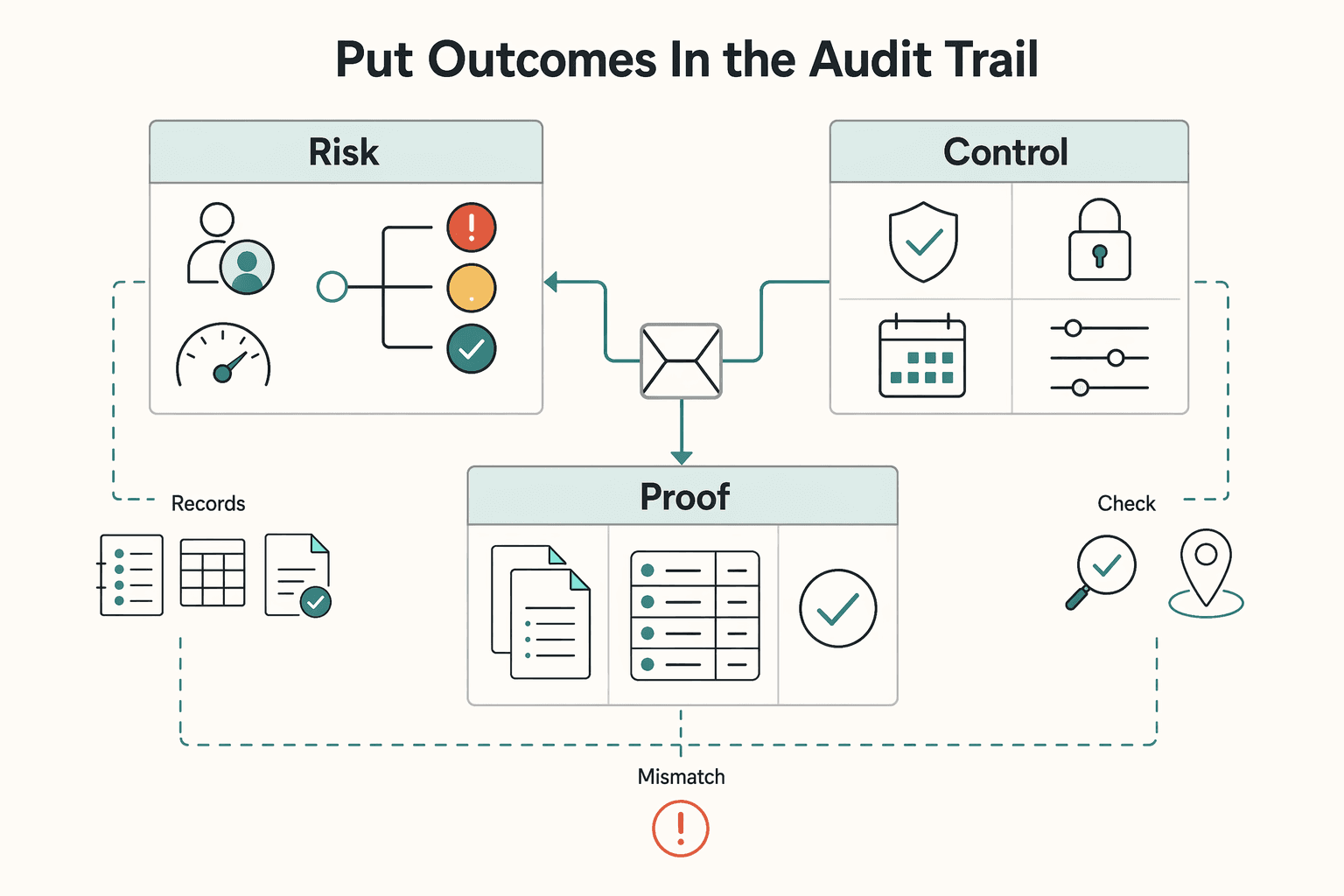

Put outcomes in the audit trail, not just analyst notes#

If the decision only lives in analyst notes, you do not have an audit trail. Your record should connect the trigger, evidence reviewed, risk assessment, account action, and release approval. If an account was restricted, the log should show when the restriction started, what caused it, and what cleared it.

Ops dashboards should make control state visible, including accounts pending verification, accounts under review after profile change, active payout holds, and unresolved material alerts. That visibility helps you detect when controls and product behavior drift apart.

Dutch market practice points in the same direction. TMNL was established by the five largest Dutch banks to identify unusual wires and payments across participating institutions, with a first phase focused on transfers involving corporates with Dutch accounts. That is not a direct requirement for non-bank platforms, but it is a clear signal that monitoring in this market is treated as an ongoing operational discipline.

Keep one operating rule: a KYC or AML outcome should change payout permissions, appear in operations views, and be reconstructable in audit history.

For a step-by-step walkthrough, see How to Build a Compliance Operations Team for a Scaling Payment Platform.

Design transaction monitoring and evidence packs auditors can follow#

Transaction monitoring is only as strong as the evidence behind each alert. If a reviewer cannot follow one alert from trigger to closure from the file alone, the control is not audit-ready for compliance or internal review.

Tie scenarios to how money moves on your platform#

Generic scenarios create noise. Use scenarios that match your payment model, and anchor them to the payment lifecycle: onboarding, initiation or authentication, and execution.

| Scenario | What should trigger review | Evidence to retain |

|---|---|---|

| Velocity spikes | Sudden increase in payout count or value versus the account's normal pattern | Triggered rule version, transaction list, prior baseline, analyst note |

| Destination changes | New bank account, new country, or changed beneficiary details shortly before payout | Change history, who made the change, linked verification results, hold or release decision |

| Unusual payout patterns | Timing, amount, or corridor does not fit the stated business profile | Account profile, recent activity, risk assessment, payout restriction decision |

| Linked-account behavior | Shared devices, identifiers, credentials, or payout endpoints across accounts that should be unrelated | Link analysis output, affected accounts, investigation notes, disposition timestamps |

If you support instant payouts, controls need to operate at execution speed. These payments can settle within 10 seconds and run 24/7. In that setup, fraud detection and sanctions screening should not rely on a slow manual queue.

Make every alert decision reconstructable#

Every alert file should stand on its own. Include a defensible risk assessment, a clear analyst note, and timestamped audit-trail entries. The file should show what triggered the alert, what evidence was reviewed, why the disposition was chosen, and what changed in payout permissions.

Keep a companion artifact that maps threats to controls and mitigations. It helps show that each scenario exists for a defined risk and is not just legacy noise.

Plan for monitoring failure, not only suspicious activity#

Good monitoring design also covers the day the monitoring stack fails. Define handling for failure modes such as third-party compromise, supply-chain issues, IT outages, and data interruptions.

When these happen, record the gap window, adjust reliance on affected controls, and backfill before treating monitoring as complete. Missing data reduces risk-model quality, so treat data availability as a control signal, not a reporting detail.

Add a recurring evidence checkpoint#

A recurring closed-alert sample is a simple way to test whether the control still works. Check that:

- event data, customer context, and triggered rule are attached or clearly linked

- the risk assessment aligns with the analyst note and payout action

- timestamps show trigger, review, disposition, and any release approval in sequence

If samples fail, fix the underlying scenario logic, analyst guidance, or data feed, not just the individual file.

Handle FX and payout risk without overblocking legitimate flows#

A practical way to reduce avoidable blocking is to separate FX conversion controls from payout-release controls. Treat conversion as an FX settlement-risk decision, then run AML, fraud, and release checks before funds leave.

That split matters because the risks are different. Payment versus payment (PvP) is designed to reduce FX settlement risk by making one currency transfer settle only if the other settles. Depending on design, it can also lower funding pressure through netting. At the same time, many deliverable FX trades still settle outside PvP, including cases where currencies are unsupported by existing arrangements or those arrangements are viewed as too expensive.

Separate conversion state from payout state#

Do not collapse conversion and payout into one status. Keep two distinct decisions in your audit trail: conversion decision first, payout-release decision second. If both are merged, control gaps are harder to spot and harder to explain.

In practice, keep separate fields for quote creation, quote expiry, conversion execution, payout approval, payout submission, and final settlement outcome. A conversion can be valid while payout release should still be held. A payout can also be ready for release while the original quote is no longer usable.

Reject stale quotes before execution#

Stale-quote rejection is a useful operational control. When a quote is no longer current, re-quote before execution. This can reduce conversion-state drift during delays from screening, retries, or manual review.

If that drift is not controlled, customer-facing terms, treasury execution, and ledger records can diverge, which can make disputes and audit review harder to resolve cleanly.

Choose strict or adaptive limits deliberately#

Controls should reflect evidence, not habit. Stricter limits can reduce loss exposure but may overblock legitimate low-risk flows. Adaptive limits can preserve speed but require stronger risk-assessment governance.

Consider stricter controls when history is thin, currencies are unsupported by available arrangements, settlement is non-PvP, or a provider path is new. Use adaptive limits only when you can clearly show why the user, corridor, or pattern justifies different treatment.

Make retries idempotent and reconstructable#

Retries need to be traceable back to one commercial intent. Keep them idempotent by using a stable payout identifier across retries, linking each retry to the original conversion and approval records, and logging why each resubmission or hold occurred.

That keeps disputes and reviews manageable because the file shows one original payout intent, one conversion decision, and a clear sequence of execution attempts.

Treat e-invoicing as a parallel compliance track, not a license substitute#

Keep invoicing and VAT work separate from payment-licensing work. In this section's sources, VAT evidence supports tax operations, but it does not establish PSD2 or DNB licensing scope.

Keep tax evidence separate from payment evidence#

A completed invoicing project should not be treated as proof that payment permissions are resolved. The grounding here supports VAT administration points such as OSS registration, filing cadence, and platform record-keeping, not payment-licensing conclusions.

If a taxable person opts into OSS, it is required to register in one Member State of identification and must declare all supplies covered by that scheme in the OSS return. OSS returns are additional and do not replace domestic VAT returns. Your control file should therefore assign VAT filing ownership and licensing-analysis ownership separately, by entity and flow.

Before launch, confirm a single matrix by entity and transaction pattern, such as domestic, intra-EU, and marketplace-facilitated flows. It should show whether OSS is used, which Member State of identification applies, and who still files domestic VAT returns.

Validate invoice standards and field sets explicitly#

Treat invoice standards and field sets as validation items, not assumptions. Confirm which fields are mandatory for your specific payment-platform scenarios with the relevant authority.

| Item to validate | What is covered | What you still need to confirm |

|---|---|---|

| EN 16931 | No requirement evidenced here | Whether it applies to your invoice type, buyer type, and jurisdiction |

| NLCIUS | No requirement evidenced here | Whether a Dutch public-sector or buyer-specific implementation rule applies |

| Peppol BIS 3.0 | No requirement evidenced here | Whether your counterparty or channel requires it |

| SI-UBL 2.0 | No requirement evidenced here | Whether it is relevant to any entity or trading pattern in scope |

| Dutch VAT invoice data, for example buyer references or payment terms | Specific mandatory field set not evidenced here | Which fields are required by invoice type, customer type, and country |

Operationally, keep a field-level data dictionary that maps owner, source record, validation rule, and fallback for missing data so tax, procurement, and product requirements do not diverge at go-live.

Split B2G and cross-border B2B decisions#

Do not treat B2G and cross-border B2B e-invoicing as one decision. Keep them as separate implementation tracks, and revalidate scope and timeline assumptions for each entity and transaction pattern before launch.

For unclear cross-border VAT treatment, consider a VAT Cross-border Rulings (CBR) request instead of inferring from invoice schema choices. The EU CBR page describes advance rulings for complex cross-border VAT transactions, requires alignment with national ruling conditions, and lists the Netherlands among participating countries.

Also flag OSS identification governance early. In certain Union-scheme identification cases, the choice can bind you for the current calendar year plus two following calendar years.

Related: Music Royalty Tax Compliance: How Platforms Handle 1099-MISC vs. 1099-NEC for Artist Payments.

Create a reporting calendar that finance and risk can actually run#

Use one shared reporting calendar across finance, risk, and compliance so deadlines, owners, and evidence do not fragment. For Netherlands operations, keep potential DNB items, potential Wwft operating checks, and internal governance checkpoints in the same tracker, with Netherlands-specific filing details marked as pending legal confirmation.

Cross-border reporting usually breaks down when teams track obligations in separate spreadsheets and tools. Different deadlines, submission windows, and formats then turn into unclear ownership and weak evidence trails. A single calendar helps reduce the risk of late filings, missing packs, and unresolved handoffs.

Put one owner against every reporting line#

Every reporting line needs a named owner. Each line should include an accountable owner, backup owner, reviewer, due date, status, and evidence link. If scope or filing details are still being confirmed, keep the line live as "pending legal confirmation," with a target date and named owner.

Keep DAC7 as its own line with an explicit scope decision. DAC7 can require platforms to collect, verify, and report seller information each year, but scope is not universal and some payment processing models may be excluded. It is not a substitute for DNB licensing or AML-related obligations.

Define the minimum monthly pack#

Keep the monthly pack compact and owned. As an internal operating baseline, track:

| Monthly pack item | What to capture | Owner check |

|---|---|---|

| Control exceptions | Failed or overridden controls, impact, remediation target date | Compliance/control owner |

| Unresolved AML cases | Aging, reason still open, next action, payout status | AML investigations lead |

| Payout holds | Count, value exposure, reason code, release blocker | Operations/risk owner |

| Reconciliation gaps | Break amount, affected ledger or wallet, root-cause status | Finance owner |

Do not mark items green without linked evidence. Do not accept verbal status in place of a dated audit trail, especially for payout decisions and KYC refresh actions. If an item is marked "monitor," require a next action and deadline in the record.

Test controls quarterly, not just when something breaks#

Monthly packs tell you what happened. Quarterly testing tells you whether the controls behind the pack are actually working. Where applicable, sample KYC refreshes, review transaction-monitoring outcomes, and check incident-closure evidence quality: who decided, when, based on what evidence, and whether closure is complete.

If your entity is in DORA scope, reserve calendar capacity for both reporting and testing. DORA has applied to EU financial entities since January 17, 2025, and includes incident reporting and digital operational resilience testing.

Add an escalation matrix before you need it#

Build the escalation matrix before the first issue hits. Typical triggers include filing dates at risk, incomplete evidence packs at review, control failures with customer or funds impact, incidents without documented root cause, and repeated reconciliation breaks or alert backlogs.

For each trigger, set the primary owner, backup approver, escalation forum, and whether external notification may be required. If evidence is missing at checkpoint, escalate that failure directly rather than waiting for the underlying case to resolve.

For the logging and controls side of platform compliance, see Internal Payment Audit Trail for Platform Compliance.

Common failure patterns in Netherlands expansions#

The biggest failures in Netherlands expansion are usually scope failures, not document failures.

-

Licensing gets treated as a one-time memo. Licensing requirements and ongoing requirements should be reviewed as separate decisions, not collapsed into a single launch check. If your current decision still relies on an old launch memo, treat it as stale.

-

Ongoing requirements are scoped too late. Teams may complete licensing work but treat post-authorization requirements as already covered. A safer approach is to run a distinct ongoing-requirements review for live operations.

-

Commercial readiness is mistaken for full payment readiness. Dutch payment behavior is local, and late discovery of expected local methods can hurt conversion. Teams also underestimate execution cost when method-by-method integrations consume engineering time for weeks.

-

Failure patterns are not reused across markets. Legal and regulatory weaknesses can repeat across jurisdictions, so reusable failure-pattern checks are usually stronger than rebuilding the review from scratch each time.

Pre-launch checklist for payment platform compliance Netherlands#

Do not launch until five items are closed: role-model review, legal escalation closure, end-to-end control testing, reporting ownership, and a separate invoicing track.

| Closeout item | What to confirm | Evidence or note |

|---|---|---|

| Role-model review | Collect, hold, convert, or payout design has been reviewed for licensing, registration, and PSD2 implications | Use current product diagrams and current contracts |

| Legal escalation closure | Open authorization questions are closed before go-live | Keep the exact question, current flow diagram, review date, owner, and the business assumption that fails if the answer changes |

| End-to-end control testing | KYC, AML, monitoring, and risk assessment work as one chain | Test one normal approval, one escalation, one monitoring alert, and one risk-change case that affects permissions |

| Reporting ownership | One owner per report or governance pack and a backup approver is named | Use one shared calendar recognized by finance, risk, and compliance |

| Separate invoicing track | Invoicing requirements are validated against the exact specification you plan to support | Test sample invoices for required tax-field completeness and keep a version date and owner |

Lock the role model before you test controls#

Test controls only after the funds-flow map and role model are locked. For the Netherlands, confirm your actual collect, hold, convert, or payout design has been reviewed for licensing, registration, and PSD2 implications using current product diagrams and current contracts. If the legal note predates a product, payout-method, or corridor change, treat it as stale.

Your sign-off basis should be one review pack showing the funds-flow map, contracting parties, control over fund-movement timing, and where customer-facing terms assign responsibility. If that pack is incomplete, escalation is still open, including any local authorization question.

Escalate open authorization questions before go-live#

Unresolved authorization questions are launch blockers, not backlog items. Cross-border due diligence is harder in unfamiliar jurisdictions, so leaving legal uncertainty open usually creates avoidable risk at go-live.

Treat the issue as open until counsel closes it. Keep evidence that includes the exact question, current flow diagram, review date, owner, and the business assumption that fails if the answer changes.

Test KYC, AML, monitoring, and risk assessment as one chain#

Configuration is not enough. Prove that controls work as one chain from onboarding through decisioning and case closure. Test scenarios, not screenshots: one normal approval, one escalation, one monitoring alert, and one risk-change case that affects permissions.

The record should stand on its own with input data, analyst note, timestamp, disposition, and resulting account state. Include relevant PSD2 checklist items in the same sign-off pack and test failure paths, not only happy paths.

Name reporting owners and backup approvers#

Reporting failures are usually ownership failures. Before launch, assign one owner per report or governance pack, set calendar dates, and name a backup approver.

Maintain one shared calendar recognized by finance, risk, and compliance. Keep regulatory reporting, recordkeeping, and document management tied to that calendar so approvals, evidence, and follow-ups stay together.

Keep invoicing checks separate from payment licensing#

If invoicing is in scope, validate invoicing requirements against the exact specification you plan to support, and test sample invoices for required tax-field completeness. Do not treat invoicing readiness as a substitute for payment-services analysis.

Revalidate standards assumptions periodically. Harmonised standards can change legal treatment when referenced in the Official Journal, and planning material is a living document, so the invoicing checklist should always carry a version date and owner.

If your funds-flow map and control owners are now clear, use the Gruv docs to align implementation details across product, risk, and engineering.

Conclusion#

The practical answer is sequence before scale. For payment platform compliance Netherlands, first narrow your likely Payment Service Directive and Dutch licensing exposure. Then make monitoring, risk, and reporting controls auditable from day one instead of trying to mature everything at once.

Keep the work in separate but connected tracks:

- Licensing and supervision scope

- Customer and transaction-risk controls

- E-invoicing implementation

That split reduces surprises because product changes can alter payment risk even when the visible work is happening elsewhere.

Use one operating standard across all tracks: every critical decision must be reconstructable. You should be able to show who approved a funds-flow design, when a risk rating changed, why a payout was held or released, and when escalation happened. The record should include timestamps, analyst notes, and resulting account or payout state.

Re-test evidence quality on a recurring basis, not only at launch. This matters because EU-level oversight still has monitoring and data-quality weaknesses.

If you add instant or near-real-time payment flows, tighten sanctions screening and fraud controls before broad rollout. Instant payments are expected within 10 seconds and 24/7, so faster release also means less time to detect abuse. In the cited EU timeline, banks must be able to receive instant payments from 9 January 2025 and send them by October 2025.

Keep e-invoicing concrete but separate from licensing analysis. If invoicing is in scope, validate EN 16931, NLCIUS, Peppol BIS 3.0, and SI-UBL 2.0 against the exact specification you plan to support, and make sure invoice evidence covers fields such as BTW numbers, buyer references, and payment terms. July 1, 2030 applies to cross-border B2B e-invoicing under ViDA, but published sources give conflicting Dutch B2G baseline years. Revalidate dates before locking plans.

If you use one closing rule, make it this: no critical control, approval, or exception should be unowned or unexplained.

When your launch checklist is complete and you need market/program confirmation before go-live, talk to Gruv.

Frequently Asked Questions

Is payment platform activity regulated in the Netherlands?

Yes, if your setup falls within PSD2-relevant payment activity. If your platform affects access to payment-account data or payment initiation, treat it as an early licensing and controls scoping issue.

Do marketplaces always need a Dutch payment license?

No. Do not assume every marketplace needs a Dutch payment licence, and do not assume every marketplace is exempt. As a practical check, confirm whether the provider is listed in the DNB licence register and whether it holds a Dutch licence or one from another EU Member State.

Who enforces KYC and AML duties for Dutch payment operations?

There is no single split that fits every model. For PSD2 data-use restrictions, DNB states that DNB and the Dutch Data Protection Authority monitor compliance. For broader KYC and AML ownership, document which entity is responsible in your structure before launch.

What are the minimum KYC and transaction monitoring controls to launch safely?

There is no universal minimum that replaces legal advice for every model. A practical launch standard is to test controls end to end and keep evidence of what was tested, who reviewed it, and the resulting account outcomes. The article's control chain includes identity capture, verification, risk tiering, ongoing review, event-driven refresh, and case closure.

How does PSD2 affect payout flows for contractor and creator platforms?

PSD2 matters when a non-bank accesses payment-account data or initiates payment actions. DNB states that this depends on customer consent and on the firm holding a DNB licence or a licence from another EU Member State. For payout flows, focus on who controls permissioning and payment actions in practice.

When is e-invoicing mandatory, and does it change payment licensing duties?

This article does not establish one universal e-invoicing mandate date for all platform models. Keep invoicing scope and timing as a separate track tied to your exact entity and transaction context. Do not treat invoicing readiness as a substitute for PSD2 licensing analysis.

What should be in a minimum Netherlands compliance checklist before go-live?

Use a closeout checklist that covers role-model review, legal escalation closure, end-to-end control testing, reporting ownership, and a separate invoicing track. Keep one evidence pack with current flow diagrams, contracts, test records, owners, and sign-off dates. Also verify provider licensing status, including the DNB licence register, and treat requests for login codes or PIN codes as a phishing red flag.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/cpmi/publ/d207.pdftrusted

- documents1.worldbank.org/curated/en/099011624132054588/pdf/P1787031cc...trusted

- eba.europa.eu/eba-response/92249trusted

- imf.org/external/pubs/ft/wp/2015/wp15200.pdftrusted

- lincolninst.edu/app/uploads/legacy-files/pubfiles/financing-...trusted

- sec.gov/Archives/edgar/data/1829311/0001683168250004...trusted

- stripe.com/resources/more/kyc-verification-in-the-nethe...trusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: