Quick Answer

Start with a narrow Morocco pilot unless CIH Bank and CMI responsibilities are documented for contractor payouts. Use Bank Al-Maghrib as supervisory context rather than workflow proof, and treat IMF/World Bank material as background because it reflects 2015 missions with 2016 publication timing. Broader rollout is justified only when conversion handling, status ownership, exception paths, and reconciliation artifacts are all verifiable in writing.

What to Know Before Paying Contractors in Morocco#

Treat Morocco as an operational validation decision, not just a commercial opportunity. The real question is whether you can verify, with current primary evidence, that your contractor payout path works through the institutions you plan to use.

Anchor your starting point in what is actually evidenced. What is clearly evidenced here is dated, system-level context, not provider-specific support. A joint IMF-World Bank mission visited Rabat and Casablanca during April 16 to 30 and September 28 to 30, 2015. The World Bank assessment was published in February 2016, and the IMF stability assessment states it was completed on November 25, 2015.

Use that material as context, not as current proof of CIH Bank, CMI, or Bank Al-Maghrib support for your exact contractor payout design.

Separate system-level comfort from execution-level proof. FSAP material can help you assess financial-system stability, but it does not validate institution-level payout execution. The IMF is explicit that FSAP assesses the system as a whole, not individual institutions, and that operational, legal, and fraud risks are outside scope.

For rollout decisions, treat those reports as market context only. They are not substitute evidence for product eligibility, payout-rail behavior, FX documentation, or reconciliation mechanics.

Mark CIH, CMI, and Bank Al-Maghrib items as confirmed or unresolved. Keep a strict confirmed-versus-unresolved split from the start. From this evidence pack, Bank Al-Maghrib can be identified as Morocco's central bank. What remains unresolved are the institution-specific answers you need for contractor payouts that may involve CIH Bank or Centre Monétique Interbancaire. Track unresolved items explicitly:

- Whether CIH is currently willing and operationally able to support your contractor payout use case.

- Whether CMI is relevant to contractor payout execution, merchant acceptance, or both.

- What current FX approval, documentary, and reporting steps apply to your payout flow in Morocco.

If a claim is not backed by current written confirmation from a bank, regulator, or partner, keep it unresolved.

Decide what kind of answer you need by the end. Aim for one defensible internal decision: launch now with explicit constraints, run a controlled pilot to close evidence gaps, or pause until written confirmations arrive.

If leadership needs certainty on provider behavior, audit artifacts, and FX handling before go-to-market spend, the likely path is pilot or pause. If you can live with narrower corridors and more manual review early, a constrained launch may still be viable.

Related reading: How to Pay Contractors in Kenya with M-Pesa, PesaLink, and KRA Controls.

Start with what is confirmed and what is still unknown#

Use a strict split: confirm system-level context separately from live contractor-payout behavior for CIH, CMI, or Morocco FX workflows, and treat any unverified items as unresolved.

| Claim area | Verification status | How to handle it |

|---|---|---|

| System-level IMF-World Bank assessment material | Confirmed as background context from 2015 mission windows and February 2016 publication timing | Use as background only, not as proof of current CIH execution, CMI payout routing, or current FX handling |

| CIH FX TRADING and Article 10 claims | Confirm with the relevant authority | Keep unresolved until you have current primary documentation tied to your exact flow |

| CMI role in contractor payouts | Unresolved; CMI is still an open role question here, not a confirmed contractor-payout rail | Keep unresolved until the role is confirmed in writing |

| Morocco contractor-payment FX documentation, approval path, and reporting path | Confirm with the relevant authority | Avoid hard dependencies in rollout design until confirmed in writing |

Base confirmation on dated primary material. What is supported here is institutional background from the joint IMF-World Bank assessment cycle. That includes mission windows in April 16 to 30 and September 28 to 30, 2015, and publication timing in February 2016. The report includes oversight of Financial Market Infrastructures and says it should be read with the IMF Financial Sector Stability Assessment.

Treat those points as background only. Do not use 2015 to 2016 FSAP material as proof of current CIH execution, CMI payout routing, or current FX handling for contractor payments.

Keep CIH FX TRADING and Article 10 claims in the unresolved queue. Claims about CIH FX TRADING, Spot Exchange, Forward Exchange, online execution, and supervision details under Article 10 of Law No 76-03 are not confirmed for contractor-payout use. Keep them unresolved until you have current primary documentation tied to your exact flow. Before moving any of these items to confirmed, require dated written evidence you can attach to the decision record.

Keep CMI role and FX paperwork explicitly unresolved. CMI is still an open role question, not a confirmed contractor-payout rail. The exact Morocco contractor-payment FX documentation, approval path, and reporting path are also unresolved.

Until those process and ownership details are confirmed in writing, avoid hard dependencies in rollout design and treat launch as pilot-or-pause rather than fully committed execution.

Map the Morocco payment stack before you design product scope#

Map responsibilities before you scope product. If a function is not tied to a named operator, retrievable source text, and an internal owner, keep it out of phase one.

Separate oversight, execution, and processing in one table. Put a version of this in your decision record before product scoping:

| Stack layer | Named entity in scope | What is supported now | Evidence confidence by source type | Do not assume |

|---|---|---|---|---|

| Policy and oversight | Bank Al-Maghrib (candidate only) | Confirm supervision details for your contractor payout flow in writing | Retrievable official regulator text is required; scrape failures, generic lists, and archive navigation text are not usable evidence | Regulator language is not implementation guidance for your exact payout path |

| FX execution | CIH Bank / CIH FX TRADING (candidate only) | Confirm contractor-payout eligibility, execution method, and product scope in writing | Obtain official bank documentation or written bank confirmation before treating as operator evidence | A product name does not confirm contractor use for your case |

| Processing and routing | CMI or alternatives (candidate only) | Confirm whether CMI is in a contractor payout path | Named operator documentation is required; current inputs do not confirm routing ownership | Brand familiarity does not confirm payout routing ownership, exception handling, or status ownership |

Use evidence quality to decide what can move from candidate to confirmed. Only retrievable current official operator or regulator material should move a role to confirmed. The provided token text, generic vocabulary text, archive navigation text, and scrape failures do not prove live execution ownership for your flow.

Apply one checkpoint per claimed role. Keep it provisional unless you have a retrievable source, a capture date, and a named process owner.

Make non-claims explicit to prevent scope drift. Write down what you are not assuming at each layer. Treat Bank Al-Maghrib supervision detail, CIH FX TRADING contractor-payout scope, and CMI payout-role assumptions as unconfirmed until supported in writing.

Also mark source quality clearly. One listed PDF did not yield extractable body text, and other listed items are token text, a generic vocabulary list, or archive navigation content. Those inputs should not support phase-one architecture commitments.

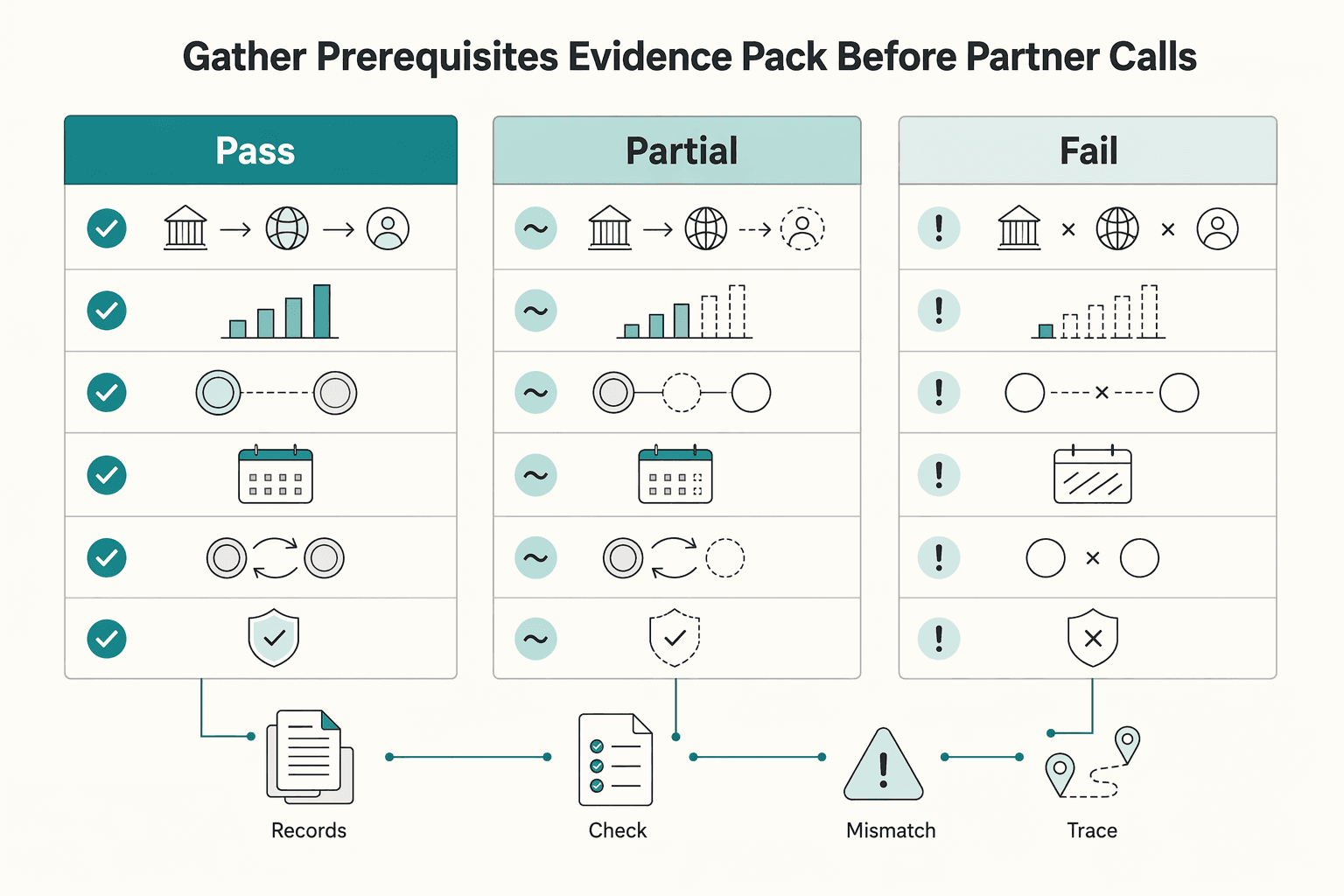

Gather prerequisites and the evidence pack before partner calls#

Do not use partner calls as loose discovery. Use them to turn interest into a testable decision record, with defined requirements, explicit unknowns, and a pass-partial-fail scorecard.

Define your operating profile before you ask about product fit. Start with the payout flow you need, then test partner fit against it. Capture monthly payout volume, average ticket size, funding and destination currencies, settlement windows, and whether treasury needs Spot Exchange only or may later need Forward Exchange or currency swap flexibility.

Keep two columns on your call sheet: needed by us and confirmed in Morocco. Contractor-payout FX handling remains unconfirmed for CIH Bank and CIH FX TRADING, so spot, forward, and swap items should stay validation questions until confirmed in writing.

Assemble an entity and compliance packet that documents operating intent. Bring a complete baseline packet even when local requirements are still unresolved. Include legal entity documents, ownership and signatory details, payout-purpose narrative, sample contractor payment scenarios, and internal approval and reconciliation controls.

Do not imply you already know the exact Morocco submission path. Morocco-specific FX documentation, approvals, and reporting for contractor payments remain unknown. Ask each provider to map your packet to its required evidence and mark missing items in writing.

If AML/CFT alignment stays verbal, treat it as non-evidence. The IMF Morocco FSSA and FSAP material is system-level context. It reflects mission visits in April and September 2015, discussion in November 2015, and completion on November 25, 2015. It names AML/CFT and oversight of systemic FMIs, but it does not provide current institution-specific onboarding approval for your flow.

Specify the control surfaces you need end to end. Define operational controls before integration planning starts. Require audit trail coverage, idempotent retries, provider reference IDs, and exception reporting across each payout state your ops team must handle.

Ask for sample artifacts during the call, such as a status payload, reference format, exception report, or settlement file layout. If a provider cannot show artifacts, treat the response as partial at best.

Prewrite pass, partial, and fail criteria before the calls start. Lock scoring rules before partner conversations so post-call optimism cannot rewrite evidence.

| Outcome | Minimum evidence standard |

|---|---|

| Pass | Written confirmation tied to a named product, operating process, or document owner |

| Partial | Verbal or broad capability statement without written scope or payout-state detail |

| Fail | Answer depends on generic regional practice, old background material alone, or an operator not clearly named in the flow |

Use the same standard for Morocco. FSAP and FSSA language is system-level background and does not assess individual institutions or cover all operational, legal, and fraud risks.

Keep Morocco-specific assumptions on a short leash. Only treat Morocco-specific claims as usable when they come from a named, retrievable, dated source. Keep everything else in an unknowns queue until written confirmation exists.

For this section, keep CIH contractor-payout eligibility, CIH FX TRADING support for this flow, CMI routing role, and current settlement and exception commitments explicitly unresolved until confirmed in writing.

For a step-by-step walkthrough, see How Platform Operators Pay Contractors in Colombia with PSE Nequi and DIAN Controls.

Choose the payout architecture that matches your risk tolerance#

Keep the architecture decision provisional until a named provider confirms your exact contractor payout flow in writing. With the current evidence pack, neither a bank-led model nor a platform-orchestrated multi-rail model is validated as an approved operating model.

Choose the default path from verified scope, not feature ambition. Start from what is confirmed in writing for your exact flow, then pick a path:

| Path | Potential upside | Primary risk | Do not proceed without |

|---|---|---|---|

| Bank-led (single-provider model) | Simpler ownership with fewer moving parts | Concentration risk if scope is unclear | Written confirmation of contractor-flow eligibility, payout-purpose handling, and exception ownership |

| Platform-orchestrated (multiple rails where supported) | More fallback options if one route fails | Ambiguity across operators and handoffs | A named operator per rail, written scope per rail, and documented conversion-to-payout exception handoff |

If confirmation is still verbal, keep the architecture marked provisional.

If launch speed matters, narrow the launch. When ambiguity is high, shrink the launch. Fewer corridors, stricter payout eligibility, and tighter scenario coverage keep unknowns contained and reduce the chance that unresolved requirements turn into live payout failures.

Treat access-gated or empty extracts as a coverage gap, not evidence. Sign-in UI text or placeholder annotations do not close Morocco-specific validation questions.

If FX predictability matters more than speed, prioritize confirmed conversion controls. If margin or planning depends on conversion timing, prioritize the structure that can confirm which conversion options and timing rules are in scope for your exact payout flow. Do not assume support exists for contractor payouts until it is explicitly confirmed in writing.

Require written answers to three points before sign-off:

- Is your contractor payout use case in scope?

- Which conversion options are in scope for that use case?

- Who owns exceptions when conversion and payout states diverge?

Set kill switches before go-live. Define a pause rule for each path so you can stop risky expansion without breaking stable payouts.

- Bank-led kill switch: pause new segments, corridors, or purposes when written scope confirmation is missing or withdrawn. Continue only the already approved cohort.

- Multi-rail kill switch: freeze new routing combinations when payout-state ownership is unclear across rails. Keep existing payouts on the last fully verified route.

With this evidence state, the practical choice is the architecture you can constrain, verify, and pause safely.

If you want a deeper dive, read How to Pay Contractors in Pakistan: RAAST Local Banks and FX Repatriation Rules.

When you finalize corridor scope and failure handling, map it to operational payout states and controls in Gruv Payouts.

Set clear FX execution rules for treasury and ops teams#

Once you have a provisional payout architecture, lock FX execution rules before go-live. Use Spot Exchange for near-term or still-moving payouts, and use Forward Exchange only when payout dates and amounts are predictable enough to justify a rate commitment.

Choose spot or forward from payout certainty. Base the decision on settlement definitions, not preference.

| Instrument | Settlement timing | Use it when |

|---|---|---|

Spot Exchange | within two business days | Payout timing is near-term or still variable |

Forward Exchange | more than two business days later | Payout date and expected amount are known, and margin is sensitive to rate moves |

A common failure mode is over-covering with forwards against forecasts that later slip, shrink, or get blocked. If forecast accuracy is weak, default to smaller spot windows until forecasting improves.

Reject stale quotes before they leak P&L. Accept only quotes that are still fresh under your internal policy, with quote timestamp, execution timestamp, and settlement date recorded in UTC or another equally unambiguous standard. That is operationally realistic because the evidence set includes an FX data/API example with UTC timestamps and real-time rates.

Do not imply a Morocco-mandated quote-expiry threshold here. Define your own maximum quote age by channel and batch type, then reject or re-quote once it is exceeded.

Restrict currency swap approvals to named exceptions. Treat currency swap as an exception path, not a default payout tool. A swap adds an initial exchange plus a reverse exchange later, which can increase timing and liquidity exposure. The evidence set also flags fast price movement and counterparty and liquidity risk for forwards and swaps.

Because the sources do not define an internal approver matrix, define one in your own policy. Name who can approve swaps, specify the exception conditions, and keep those decisions documented.

Log each conversion so finance can reconcile end to end. Record each conversion so finance can trace FX to payout without guesswork. At minimum, capture the source or venue reference. Also capture quote timestamp, execution timestamp, settlement date, currency pair, side, rate, internal payout or batch ID, and exception approver where relevant.

Month-end control test: starting from an internal payout ID, finance should be able to trace to exactly one conversion record and confirm amount, rate, and source reference.

Validate CIH and CMI with a structured partner questionnaire#

Do not treat partner scope as confirmed. For contractor payouts, treat both CIH Bank and Centre Monétique Interbancaire (CMI) as unconfirmed until each critical answer is backed by at least one extractable official document excerpt.

Ask CIH Bank to define CIH FX TRADING eligibility boundaries. Separate "can execute FX" from "can support this payout purpose." Ask CIH to confirm in writing whether CIH FX TRADING can be used for contractor payouts, and to state what is in scope and what is out of scope.

Do not accept a broad "we support FX" response as confirmation. Require the exact product or policy excerpt and document version date. If the answer is only verbal or comes from non-extractable material, mark it provisional.

Ask CMI to state where it sits in the flow. CMI has not been confirmed as a contractor payout rail, so require a direct role statement for your use case. Ask whether CMI is involved in payout execution, merchant acceptance only, status visibility, failure handling, or none of these.

Require a plain-language transaction-path description and ownership by stage. Also ask what artifacts or references your ops team can retrieve to trace a payout from initiation to final status.

| Question area | Who answers | Confirm only when |

|---|---|---|

| Contractor payout scope | CIH Bank | You have an extractable official document excerpt stating scope and boundaries |

| Payout role vs merchant acceptance | CMI | You have extractable formal material mapping CMI's role |

| Cutoffs, escalations, audit artifacts | Both | You have extractable formal material with owners and retrievable references |

Ask both parties for cutoffs, escalation paths, and artifacts. Request written definitions for cutoffs, escalation paths, and post-execution artifacts used for audit or dispute review. Store each answer with document title, version date, and responding team.

Be strict on evidence quality here. Generic word lists and sign-in or gating text cannot validate go-live assumptions.

Require a written responsibility statement for any Bank Al-Maghrib context they cite. Ask each party to state what it owns, what it does not own, and what remains your platform's responsibility, and mark any regulator-scope item as unconfirmed until you have extractable official material.

Avoid vague "regulator-approved" language. Require a written responsibility statement with named function ownership and escalation points.

For a comparison playbook, see How Platform Operators Pay Contractors in Indonesia With GoPay, OVO, DANA, or BI Fast.

Build compliance gates and governance before first live payout#

Before your first live contractor payout, make release dependent on coded controls, named owners, and an auditable evidence trail. If a required control, owner, or evidence record is missing, the payout should not move.

Assign control owners before you write release logic. Assign one owner per gate across compliance, payments ops, and engineering. Compliance defines required verification states, payments ops owns exception handling, and engineering enforces that payouts cannot release without required statuses.

Use a control matrix that maps each gate to one owner, one approval action, and one evidence source. In the provided evidence, the EU-Morocco agreement is described as signed in February 1996, in force in March 2000, and containing no binding commitments, so treat trade-agreement references as policy context, not payout-flow approval. The same excerpt says the Morocco-US agreement covers services, including financial services; that is still context, not an implementation checklist.

Enforce release gates in the product, not by inbox approval. Release decisions should come from machine-readable control states, not email or chat confirmations. This prevents payouts from moving on incomplete, outdated, or non-extractable evidence.

Record every approval with immutable audit metadata:

- payout intent ID and internal contractor or entity ID

- decision outcome, rule version, and timestamp

- approver role or service account

- evidence record ID, document title, version date, and file hash

- provider or bank reference when available

Minimize PII in logs while preserving investigation paths. Keep sensitive source documents in restricted storage, and log only what investigations and reconciliation need. Prefer masked fields and internal IDs over raw identity or banking data in event streams.

A practical test is whether finance and ops can trace a payout from approval to final status using internal IDs, masked fields, and structured references. If not, add structured references instead of adding raw PII.

Set a review cadence and remediation SLA before scaling. Define a recurring control review cadence as an internal governance choice, not as a Morocco-specific legal requirement in this evidence pack. Use named governance checkpoints such as global risk management and Pillar III (risks and capital adequacy) as review categories, then adapt them to your internal controls.

Set remediation ownership and timing now. Decide who can freeze payouts, who fixes broken gates, and how rule, code, and documentation updates are coordinated. The cited 2005 and 2015 materials are historical context, so treat current operational requirements as unconfirmed until validated from current primary sources.

Related: How to Pay Contractors in Vietnam: VietQR Napas and State Bank FX Rules for Platforms.

Integrate in a strict order so failures stay recoverable#

Integration order can matter more than speed here. Make one payout path replayable and reconcilable first, then add scale. In Morocco, key contractor-payout implementation details are still unverified in this evidence pack, so recoverability should outrank speed.

| Stage | Core requirement | Checkpoint |

|---|---|---|

| Quote and conversion handling | Capture quote and conversion controls before payout instruction creation | One payout ID maps cleanly to one accepted quote and one booked conversion decision without raw-log reconstruction |

| Payout instruction creation | Use one idempotency key per payout intent, not per API attempt | The same key cannot submit materially different instructions |

| Inbound event reconciliation | Ingest callbacks, file results, or status polls idempotently | Every external event either matches a known payout intent or provider reference, or lands in unmatched |

| Exception queue | Carry enough context to decide whether to wait, re-query, escalate, or return to compliance | Queue items include payout intent ID, provider reference if present, masked beneficiary details, amount, currency, conversion reference, latest external status text, internal checkpoint, item age, and owner |

| Batch automation | Automate only after a Morocco pilot corridor runs clean from quote to reconciliation | Expand only after a clean month-end close with no unexplained duplicates and no unresolved unmatched items |

The IMF Morocco Financial System Stability Assessment is dated 08 Feb 2016. It says the financial system has grown in size and complexity since 2007, and its scope includes policy oversight, bank resolution, and financial safety nets. Treat that as risk context, not product requirements. Use the sequence below as an internal control pattern, not as a Morocco-specific legal requirement. Avoid payout logic that only works when events arrive once and in order.

Implement quote and conversion handling first. Start with quote capture and conversion controls before payout instruction creation. Keep payout intent and FX decision separate so you can reject stale quotes, re-quote cleanly, and trace which conversion backed each payment.

Persist structured fields at this stage: internal payout intent ID, currency pair, quoted amount, quote timestamp, expiry timestamp, source reference, and approver, whether a user or service. Checkpoint: one payout ID should map cleanly to one accepted quote and one booked conversion decision without raw-log reconstruction.

Create payout instructions with business-level idempotency. After conversion is stable, wire payout creation to your rail with one idempotency key per payout intent, not per API attempt. Retries should replay the same instruction, not create a second money movement.

Bind that key to fixed amount, destination, and currency values so the same key cannot submit materially different instructions. Persist partner references immediately and map them to internal ledger submission events for later reconciliation.

Reconcile inbound events before scaling exception handling. Ingest callbacks, file results, or status polls idempotently and reconcile them against stored payout and conversion records. Design for duplicates and out-of-order events as normal behavior.

Use internal checkpoints such as credited, held, returned, and unmatched so your operations team can triage quickly. Every external event should either match a known payout intent or provider reference, or land in unmatched with enough metadata to investigate.

Build an exception queue with decision-ready evidence. Once reconciliation works, add the exception queue. Queue items should carry enough context to decide quickly whether to wait, re-query, escalate, or return to compliance.

Include internal payout intent ID, provider reference if present, masked beneficiary details, amount, currency, conversion reference, latest external status text, internal checkpoint, item age, and owner. Avoid queue records that only say "failed" or "pending review."

Automate batches only after a Morocco pilot cohort is clean. Automate batching last, after a Morocco pilot corridor runs clean from quote to reconciliation with replay-safe retries and consistent ledger mapping. Gate rollout by corridor, bank route, and contractor cohort.

If any route still depends on provisional partner answers, keep it blocked or pilot-only. Expand eligibility only after a clean month-end close with no unexplained duplicates, no unresolved unmatched items, and clear handling for held or returned outcomes.

Plan for common failure modes and recovery paths#

Treat these failures as predefined stop-and-recover events, not ad hoc operations calls. Morocco's FSAP-era evidence was published in February 2016 and based on 2015 mission work. It supports a risk-aware posture around oversight and crisis preparedness, but the provided excerpts do not define contractor-payout ownership or operating rules for your routes.

| Failure mode | Immediate response | Verification point |

|---|---|---|

| Ownership is unclear on a route | Freeze new traffic on that route and use only verified corridors | One accountable operator per stage, plus one escalation contact for failed, held, and returned outcomes |

| FX quote expires during batching | Stop and obtain a fresh quote before proceeding | One business payment reconciles to one accepted conversion decision at a time, with expired quotes retained as rejected attempts |

| Conversion and payout legs diverge | Move the item to investigation and confirm ledger truth first | Establish whether funds were converted, instructed, both, or neither before any resend or reversal |

| Holds accumulate | Treat hold buildup as an early risk signal with internal alerts, documented release criteria, and named risk ownership | Each released or returned hold includes case notes, screening outcome, approver, and release rationale |

Freeze routes when ownership is unclear. If a route cannot name, in writing, who owns payout initiation, status visibility, returns, and audit evidence, freeze new traffic on that route and use only verified corridors. Keep the route frozen until accountability and escalation ownership are explicit.

Verification point: one accountable operator per stage, plus one escalation contact for failed, held, and returned outcomes. Red flag: multiple parties can "see" a payment, but none will own final status or investigation artifacts.

Re-quote expired FX instead of forcing the batch through. If a quote expires during batching, stop and obtain a fresh quote before proceeding. Keep a clear internal decision trail linking the expired quote and the accepted quote to the same business payment.

Checkpoint: one business payment reconciles to one accepted conversion decision at a time, with expired quotes retained as rejected attempts. Red flag: a later rate is applied without a clear decision trail.

Correct reconciliation breaks from the ledger outward. When conversion and payout legs diverge, move the item to investigation and confirm ledger truth first. Establish whether funds were converted, instructed, both, or neither before any resend or reversal.

At minimum, use a consistent internal investigation template that captures payment identifier, amount, currency, available conversion reference(s), provider reference(s) if present, and latest external status text. Red flag: external portal actions happen before ledger state is verified.

Escalate hold accumulation before it becomes hidden backlog. Treat hold buildup as an early risk signal with internal alerts, documented release criteria, and named risk ownership. Supervisory context does not replace your internal release controls.

Verification point: each released or returned hold includes case notes, screening outcome, approver, and release rationale. If holds cluster by corridor or partner, pause new volume on that path until the cause is understood.

Conclusion#

Morocco is launch-ready only when each control is documented in writing, testable in your environment, and owned by a named team or partner.

- Confirm scope for

CIH Bank,CIH FX TRADING, and anyCMIdependency if those entities are part of your planned flow. Collect separate written confirmations for each party and use case. Each confirmation should state whether contractor payouts are in scope, excluded transaction types, and what status and exception artifacts are available. If anything remains verbal, pause GTM. - Document a regulatory responsibility map with

Bank Al-Maghrib(BAM) as context. Use regulator material as supervisory background, not as approval of your specific payout flow. Assign clear owners for screening, payout release, reconciliation, exceptions, and audit retrieval across partners and internal teams. - Set FX policy before scaling. Define in writing whether contractor payouts use FX at all, how quote-expiry is handled, and who can approve exceptions. Do not enable any FX path for contractor payouts without written partner confirmation for your exact use case.

- Make compliance controls hard release gates. Require audit-ready logs, masked PII handling, and reconciliation checkpoints before first live payout. A payout should never be released without a recorded approval path and enough evidence to reconstruct the event.

- Pass a narrow pilot before expansion. Start with one corridor and a limited contractor cohort in

Morocco. Expand only when statuses are interpretable, failures are recoverable, and month-end tie-out is clean across conversion, payout, and ledger records. - Keep evidence recency explicit in launch decisions. IMF and World Bank assessment context here comes from 2015 missions, with IMF information cutoff on November 25, 2015 and World Bank publication in February 2016, so treat it as system-level background rather than current institution-level operating guidance. FSAP findings do not cover operational, legal, or fraud risk.

Before committing GTM resources, confirm market-specific coverage, policy gates, and rollout constraints for your exact flow with Gruv.

Frequently Asked Questions

Can you pay contractors in Morocco directly through `CIH FX TRADING`, or is it only for specific commercial transaction types?

Treat direct contractor payout support as unproven until CIH Bank confirms in writing whether contractor payments are in scope, which transaction types are allowed, and what evidence is provided for holds, returns, and final status.

What does `Bank Al-Maghrib` regulate in this flow, and what remains the responsibility of `CIH Bank` or the payout platform?

Available documentation supports only system-level context, not institution-level operating rules for this route. The IMF Morocco FSAP covers system-level oversight, including the policy oversight framework and systemic FMIs, and it states FSAPs do not assess individual institutions and do not cover operational, legal, or fraud risks. For execution, require written ownership across payout initiation, screening, reconciliation, exceptions, and audit evidence.

Is `Centre Monétique Interbancaire` (`CMI`) a contractor payout rail, a merchant acceptance layer, or both?

The grounding here does not resolve that. Do not launch on assumptions that CMI is confirmed for contractor payouts, and do not rule it in from broad payment-stack descriptions alone. Ask for a flow map showing where CMI sits, what statuses it exposes, and who owns failed or returned outcomes if it is in the path.

When should a platform use `Spot Exchange` versus `Forward Exchange` for contractor payouts?

A Morocco-specific decision rule for Spot Exchange versus Forward Exchange in contractor payouts has not been established. Treat either option as unapproved for this route until your provider confirms the structure and responsibilities in writing for your exact use case.

What evidence should operators collect before committing GTM resources to Morocco payout launch?

Collect written scope confirmation from each partner, a responsibility map, escalation contacts, and sample status and return artifacts you can audit later. Use a simple checkpoint: each step must have one owner and one evidence artifact. If contractor-payment eligibility or exception handling stays verbal, pause GTM commitment.

How should teams verify claims when sources include official pages, broad `MENA region` guides, and older `International Monetary Fund` material?

Prioritize by decision value: direct written partner confirmations and current official institution material first, broad regional guides as background, and older IMF material as context. The IMF Morocco FSSA was completed on November 25, 2015, after missions in April and September 2015, so use it for system-level context rather than current institution-level payout operations.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- documents1.worldbank.org/curated/en/802191484661795353/pdf/Morocco-FS...trusted

- imf.org/external/pubs/ft/scr/2016/cr1637.pdftrusted

- openknowledge.worldbank.org/bitstreams/d7631b79-72d6-51b4-96c5-7fedac90c...trusted

- bkam.ma/en/Systems-and-means-of-payment/Articls/Syst...external

- bkam.ma/en/Systems-and-means-of-payment/Financial-ma...external

- cmi.co.maexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Pay Contractors in Pakistan with RAAST and Clear FX Ownership

Treat Pakistan as a two-part payout decision, not a single rail choice. The mistake that burns time is assuming local payout delivery, cross-border funding, and Foreign Exchange (FX) repatriation will all be cleared in the same product conversation. They often are not. If you blur them together too early, you can end up designing features before you know which party actually owns conversion, compliance, and exception handling.

Paying Contractors in Vietnam Under VietQR, NAPAS, and SBV FX Rules

Vietnam can be a conditional go for contractor payouts, not an automatic one. Fast domestic rails exist, but your decision should come down to whether your exact payout flow is workable and compliant.

How to Pay Contractors in Bangladesh: BEFTN bKash and Bangladesh Bank FX Rules

Use an operator lens because payout decisions can fail on data quality and control gaps. In the material available, some fields are explicitly unavailable (`..`), and some totals may not reconcile exactly because of rounding. Do not treat every table value as exact or complete. Set a few control checkpoints before you plan rollout: