Quick Answer

The right marketplace payment setup depends on how much control you need over payout timing, refunds, disputes, and reconciliation, not just checkout speed. Early marketplaces often start with a direct PSP setup for faster launch, while scaling teams move toward an internal ledger, bank-transfer-first collection, hybrid migration, MoR, or ACH-heavy flows when finance control, verification gating, and clean reconciliation matter more.

Six Marketplace Payment Setups for Two-Sided Platforms: Checkout, Payout Control, and Reconciliation

How to Compare Marketplace Payment Setups#

In a two-sided marketplace, payments are bigger than checkout. You need a money flow your team can run, explain, and reconcile from onboarding through payout. Your platform connects buyers and sellers, enables payment, and coordinates what happens before and after the charge. As volume grows, the question shifts from "can the buyer pay?" to "can we control fund movement, enforce holds when needed, and explain every balance change clearly?"

- Checkout is only one layer

A standard marketplace payment flow includes seller onboarding, buyer checkout, and secure transaction handling. For marketplaces, the critical work often sits in split payments and delayed payouts, not the card form itself. Before comparing providers, map the full money path: who controls payout timing, how refunds route, and what happens when disputes arrive after funds move. If that picture is fuzzy, reconciliation gets harder after the fact.

- Compliance gates decide whether money can move

Seller onboarding is a prerequisite in many platform setups, and verification can be required before processing payments or payouts. These checks, commonly called KYC checks, vary by business model, transaction type, and country. The practical rule is simple: payout policy should follow verification status. Side-channel payouts may ease short-term pressure, but they can create downstream risk when funds move before required checks are complete.

- Reconciliation determines whether the model scales cleanly

You are responsible for reconciling payouts against transaction history. A workable process also covers refunds, disputes, fees, and withdrawals, not just successful charges. This article is for founders, product, engineering, finance, and ops owners who need decision-ready tradeoffs. The goal is to choose a setup that fits your stage now and still gives you a clean path as the network expands.

Choose the right setup before you pick a provider#

Choose your operating model before you compare provider feature lists. In a two-sided marketplace, the right setup is the one you can run through refunds, disputes, payout holds, and reconciliation, not just the one with the fastest checkout demo.

This matters most if you handle buyer payments, seller payouts, and post-charge exceptions. If your flow is closer to a single-merchant model with no seller balances or payout timing rules, parts of this may be more process than you need today.

- Control over fund flow

Decide who controls money movement after the charge. In Stripe Connect, charge type affects fund distribution and liability touchpoints for refunds and disputes. Separate charges and transfers gives you more control because charging and transferring are decoupled. If you need payout delays, policy-based fee logic, or holds until completion, use a setup where those controls are explicit and configurable. Validate it by tracing one order through charge, transfer, refund, dispute, and payout.

- Compliance burden for onboarding and verification

Verification is a gating function, not just form collection. Platform users may need to be verified before payments can be processed or funds paid out, and requirements can change over time. Hosted onboarding reduces integration effort and is often the fastest path. If you need more custom onboarding or verification handling, plan for more in-house ownership and ops support.

- Speed to launch

Launch speed is a fair early priority, and default provider flows can get you live faster. But marketplace complexity still shows up in delayed payouts and split payments, not in checkout UI alone. The tradeoff is usually reporting depth and exception handling. Accept that tradeoff on purpose, and make sure your finance flow will still reconcile cleanly as volume and edge cases increase.

- Expected effective take rate

Treat margin as an end-to-end operating outcome, not just a processing-fee question. Payout costs, refunds, disputes, and reconciliation effort all shape your real economics. In some indirect-charge flows, refunds, disputed amounts, and related fees are debited from the platform balance first. If margin defense and auditability matter, prioritize stronger reconciliation design and clear ledger visibility.

If your roadmap includes embedded financial services, multi-vendor expansion, or cross-border payouts, avoid architectures that hide payment and payout logic inside one opaque flow. Cross-border support can be corridor-limited. For example, the provider documents payments-balance cross-border transfers between the United States, Canada, United Kingdom, EEA, and Switzerland. Unsupported borders error out.

Pick the compromise on purpose: choose less control for near-term speed, or take on more control now to protect margin, improve auditability, and preserve expansion paths.

If you want a deeper dive, read The Complete Guide to Platform Payments: Everything a Marketplace Operator Needs to Know.

Compare six marketplace payment setups side by side#

Most teams can rule out bad fits quickly by deciding how much fund-flow control they need versus how fast they need to launch. If speed wins, a direct PSP setup or a phased hybrid can be a practical starting point. If payout timing control, exception handling, and reconciliation discipline are central, move earlier to ledger-owned or bank-transfer-first patterns.

Stripe documentation is detailed on charge types, disputes, and payout control. CS-Cart is useful for owner-vendor money-flow patterns. Antom is a settlement and infrastructure reference. Sharetribe is useful for market framing, including a six-provider comparison and selection factors such as country support, currencies, fees, and integration complexity.

| Option | Best for | Fund flow ownership (fee logic, refund routing, dispute evidence, payout timing) | Key pros | Key cons | Compliance load | Engineering lift | Failure modes | Do not choose when |

|---|---|---|---|---|---|---|---|---|

| Direct PSP setup | Early marketplaces that need checkout, onboarding, and seller payouts live fast | Platform configures PSP charge/account settings and payout controls (for example, destination charges or separate charges and transfers); ownership is constrained by charge type and provider rules | Fast launch, fewer moving parts | Less control as refunds/disputes scale; provider-shaped reporting | Low to medium | Low | Platform balance can be debited for fees/refunds/chargebacks in applicable flows; dispute handling varies by charge type and negative-balance responsibility | You need custom payout delays, complex fee logic, or ledger-grade reconciliation now |

| PSP plus internal ledger | Scaling platforms with finance/ops ownership | Platform owns posting, fee logic, refund routing in books, dispute evidence workflow, and payout timing; PSP remains rail/execution layer | Strong audit trail, clearer reconciliation ownership, better hold/reversal control | More build and operations ownership | Medium to high | High | Ledger-PSP drift, duplicate events, payouts before verification clears | You cannot staff reconciliation and payout-exception ownership |

| Virtual-account-first collection | Invoice-heavy or repeat-buyer bank-transfer flows | Platform maps inbound funds via virtual account numbers, then controls seller payout release after confirmed receipt | Better matching and deposit attribution | Asynchronous settlement; rail-specific exception paths; not universal across architectures | Medium | Medium to high | Unmatched deposits; crediting sellers before confirmed funds; growing manual queues | You need instant payment confirmation at checkout |

| MoR-led setup | Teams that want an external merchant boundary in parts of the flow | Merchant of record is legally responsible to customers; platform may give up part of direct control over fee/refund/dispute/payout design | Clearer transaction-accountability boundary | Reduced direct control; dependency on MoR scope/reporting | Medium | Low to medium | Opaque economics, limited policy control, harder migration later | Your margin model depends on custom seller-level fee and payout logic |

| Hybrid phased model | Teams that cannot replatform in one step | Starts PSP-led, then shifts ownership of ledger, payout rules, refund/dispute handling, and exception logic in phases | Launch now with a migration path | Temporary duplication and parity gaps between flows | Medium | Medium | Refund/dispute/fee behavior diverges across phases | You will not define migration gates and exit criteria up front |

| ACH payment processing heavy | US domestic flows with repeat buyers, invoice acceptance, or strong cost pressure | ACH Direct Debit is reusable and delayed-notification; payout release should follow acceptable funds confidence | Low-cost batched rail fit; reusable bank debit | Delayed notification, non-guaranteed outcomes, slower movement than cards | Medium to high | Medium | Seller paid before ACH failure/return; support load from delayed statuses | You need same-day certainty, instant fulfillment, or card-like dispute speed |

Use the table to shortlist. Then test the two or three plausible options against your actual payout and exception rules.

- Direct PSP setup: Best when launch speed matters most and you can live with provider-defined behavior in exceptions.

- PSP plus internal ledger: Best when finance control and reconciliation quality matter more than build simplicity.

- Virtual-account-first collection: Best when bank-transfer traceability is a core operational need.

- MoR-led setup: Best when you intentionally trade direct control for a different legal and operational merchant boundary.

- Hybrid phased model: Best when you need to ship now but still want a controlled path to deeper ownership.

- ACH-heavy model: Best when US bank-rail economics matter and your ops team can tolerate delayed outcomes, including acknowledgement up to 4 business days and standard ACH timing at minimum T+1, with payout timing commonly shown as 2-5 days.

Option 1 direct PSP split payments with provider-managed payouts#

This can be one of the fastest ways for an early two-sided marketplace to go live, as long as you accept provider-defined behavior for exceptions. You can get buyer payments, seller onboarding, and payouts running quickly, but you may have less control over exception handling as complexity grows.

Why teams start here#

A direct PSP setup can keep first-launch scope small. Stripe Connect is built to onboard, verify, and pay out recipients at scale, and its hosted onboarding is designed to collect business and identity details with minimal platform effort. It also positions prebuilt onboarding and UI paths as a low-effort way to get live quickly.

For split payments, a common pattern is separate charges and transfers: one buyer payment can be split across multiple connected accounts. Provider-managed automatic payout scheduling can also reduce day-one payout orchestration work.

What you gain and where pressure appears#

The immediate gain is speed and lower engineering lift. You are not building your own onboarding intake, verification collection, or first payout scheduler.

Pressure appears when refunds and disputes increase. In destination-charge and separate-charges-and-transfers flows, refunds, disputed amounts, and related fees are debited from the platform balance, and the platform remains liable for chargebacks and related costs. Recovering funds from connected accounts can require transfer reversals, so weak exception handling can create direct platform-loss risk.

Launch with explicit exit criteria#

Define your migration triggers before go-live, not after the model starts hurting. Typical triggers are:

- Refund and dispute workflows repeatedly require transfer reversals or create platform balance pressure.

- You need payout holds or timing controls that go beyond automatic payout schedules.

- Disintermediation becomes material: users meet on-platform, then transact without the platform's involvement and without paying platform fees.

Use this model to launch fast, but only with a clear plan for when you will move to deeper control.

Option 2 PSP plus internal ledger and payout orchestration#

This can be the next step once Option 1 starts breaking under exceptions. You keep buyer payment collection with the PSP, but move payout decisions and exception handling into your own ledger-driven rules.

Best fit#

This model can fit scaling marketplaces where finance needs clearer reconciliation evidence and engineering needs retry-safe payout control. It can create a cleaner split between payment flow and fund flow, stronger adjustment handling before payout, and tighter verification-based payout gating. The tradeoff is more engineering ownership, stricter operational discipline, and more verification checkpoints to maintain.

A concrete use case is keeping buyer authorization and capture in the PSP, posting internal ledger events, then releasing seller payouts only when your rules and verification checks pass.

How the model works#

The separate charges and transfers pattern shows the basic split: the charge on your platform account is decoupled from transfers, and funds can be sent to multiple connected accounts. In this model, your ledger tracks commercial state, such as platform fee, seller payable, refunds, disputes, and holds, while the PSP remains the rail that actually moves money.

Why teams accept the extra build#

The main benefit is control over timing and state, not automatic reconciliation. The provider is explicit that fees, refunds, and chargebacks debit the platform balance. It also makes clear that the platform remains liable for chargebacks and related costs in destination-charge and separate-charges-and-transfers flows. Posting those adjustments in your ledger before payout helps prevent paying out amounts you may need to recover later.

It also notes that recovery is often possible by reversing transfers. Treat that as a standard exception path to design for.

The checkpoint that matters most#

Payout gating on verification status is the key control here. The provider requires KYC for connected accounts, and when requirements.currently_due is not empty, capabilities can be restricted. Payout release should check current verification status at release time, not just during onboarding.

A practical sequence looks like this:

- PSP confirms buyer payment state.

- Your platform posts ledger events for order economics and any holds.

- Payout is queued only if onboarding and verification checks pass at that moment.

Where operational burden moves#

The burden shifts from provider defaults to your own reconciliation mapping. Its bank reconciliation reporting can help tie payouts to bank deposits and close processes, but you still need internal mapping from ledger state to PSP payouts and settlement.

You also need strict idempotency in payout-triggering writes and ledger-to-PSP handoffs. The provider supports idempotent requests so retries do not execute the same operation twice.

Provider differences matter more once you own this layer. Adyen requires split instructions across payment lifecycle calls, including refunds, and split-refund flows can assign refund liability. That flexibility can improve control, but it also increases the amount of lifecycle logic your team must operate consistently.

Option 3 virtual account collection and bank-transfer-first rails#

For invoice-heavy, repeat-buyer flows, this model can be a strong fit when you want better bank-transfer traceability and potential ACH cost advantages. A conservative operating rule is to release seller funds only after the transfer is confirmed, matched, and checked against return-risk rules.

Use this when buyers can push funds from their bank account instead of expecting instant card acceptance. A virtual bank account number, or VBAN, gives each customer or invoice context a dedicated transfer destination, which improves reconciliation while keeping your platform's real bank details hidden.

The main advantage is cleaner matching. In the provider's bank-transfer model, VBANs support automated inbound matching, and ACH is a supported U.S. rail for invoice-style collection. ACH can cost less than cards, with the tradeoff that settlement can take a few days.

The main risk is that exception handling becomes a front-line ops function. Bank transfer is an asynchronous push method, and unmatched inbound transfers can remain in customer balance until manually reconciled. Return and warranty timing is also context-dependent, including 60-day consumer error context and up to one year for certain non-consumer warranty claims.

A practical use case is to collect buyer funds through VBANs and process U.S. domestic receipts via ACH. Route seller payouts only after deposit status is confirmed and matched to the expected buyer or invoice. That sequencing fits split-and-delay payout needs and reduces the risk of paying out before transfer status is reliable.

Related reading: What is a Virtual IBAN and How Do Platforms Use It to Collect Payments Globally?.

Option 4 merchant of record for tax-heavy cross-border complexity#

Use a Merchant of Record, or MoR, when cross-border tax and compliance work is the main thing slowing expansion. The tradeoff is clear: you may reduce internal merchant and tax operations in some markets, but you hand part of transaction ownership to the MoR.

A MoR is the legal entity that sells to the end customer and carries core transaction liabilities. In practice, that scope can include payment operations, sales tax handling, PCI compliance, refunds, and chargebacks. It also changes the customer-facing accountability boundary, because the MoR name appears on the card statement.

1. Best fit when tax setup is the bottleneck#

Choose this path when demand is clear, but launch timelines keep slipping on jurisdiction-by-jurisdiction tax and compliance setup. In the EU, place-of-taxation rules determine which country's VAT rules apply, and those rules differ across countries.

A practical decision rule is this: if market entry is delayed more by tax registration and local compliance than by checkout or payout design, evaluate MoR seriously. Provider positioning around registration, collection, and remittance in over 100 jurisdictions shows why this model is attractive for cross-border expansion.

2. Main upside is clearer responsibility boundaries#

A key upside is cleaner ownership lines, not guaranteed better economics. When the MoR is the seller to the customer, tax, refunds, chargebacks, and statement-descriptor responsibility are more clearly assigned.

MoR is also positioned as an alternative to building a full in-house payments stack, especially for international sales where you are not locally set up. That can reduce internal operational surface area while you scale.

3. Main downside is dependency on provider scope#

Do not assume MoR covers everything in every market. Tax and compliance allocation is jurisdiction-specific. In UK guidance for some digital services, a third-party platform can account for VAT. In Canada's normal GST/HST regime, a non-resident supplier may still need to charge and collect tax even when sales run through a platform operator.

Before launch, confirm scope in writing:

| Area | What to verify |

|---|---|

| Tax handling | Covered jurisdictions and transaction types |

| Customer record | Whose name appears on statements and invoices |

| Exceptions | Ownership of refunds, chargebacks, and escalations |

| Integration compliance | Pre-production certification or approval requirements |

| Commercial model | How provider fees affect your platform fee and margin |

Some providers also enforce pre-launch compliance gates. If you deviate from required standards, risk and cost can shift back to your business.

4. Selective MoR by market requires careful design#

One possible pattern is hybrid deployment: use MoR in jurisdictions where tax complexity is blocking growth while retaining your existing setup elsewhere.

Treat this as controlled complexity, not plug-and-play. Define a market-by-market responsibility matrix before rollout so finance, ops, and support all work from the same merchant-of-record boundary.

Option 5 phased hybrid model for teams that cannot replatform at once#

If you cannot replatform in one move, use a phased hybrid model. Keep one provider for buyer payments and baseline seller payouts, then add control in a fixed order before you expand scope.

| Step | Focus | Grounded checkpoint |

|---|---|---|

| Start provider-first | Checkout, onboarding, initial payouts | Use one marketplace payment provider; connected accounts must meet verification requirements before they can accept payments and receive payouts; connected account type cannot be changed after creation |

| Shift to ledger-backed reconciliation | Fix reconciliation before new geographies | Treat rising disputes or slipping month-end close as a migration trigger; transaction-level reporting is not supported for funds in manual payouts; bank reconciliation is limited to direct US-based Stripe accounts on automated payouts |

| Make migration gates explicit | Block fund-flow changes until parity is defined | Set onboarding parity, refund parity, dispute-handling parity, and platform-fee calculation parity; watch for parallel monetization logic during migration |

- Start provider-first, but lock the boundary.

Use one marketplace payment provider for checkout, connected-account onboarding, and initial payouts. This is a practical starting point when you need KYC payout gates, because connected accounts must meet verification requirements before they can accept payments and receive payouts. Keep the setup intentional: connected account type cannot be changed after creation, so early defaults should not become permanent by accident.

- Shift to ledger-backed reconciliation before new geographies.

If disputes are rising or month-end close keeps slipping, pause expansion and fix reconciliation first. Provider-only reporting can become insufficient here: transaction-level reporting is not supported for funds in manual payouts, and bank reconciliation is limited to direct US-based Stripe accounts on automated payouts. If your team cannot reliably tie payouts, refunds, and dispute adjustments to bank deposits without manual stitching, treat that as a migration trigger.

- Make migration gates explicit before changing fund flow.

Set four release blockers: onboarding parity, refund parity, dispute-handling parity, and platform-fee calculation parity. Charge-type changes affect data availability, revenue reporting, and refund and chargeback handling. Dispute debits can shift by charge type, and with indirect charges the platform is responsible for negative balances while Stripe fees are collected from the platform. During migration, watch for parallel monetization logic so old and new fee rules do not conflict.

You might also find this useful: Accounts Payable vs. Accounts Receivable for Platforms and the Two-Sided Ledger.

Compliance gates that must happen before seller payout#

Treat seller payout as a release decision. If verification is pending, requirements are overdue, or risk screening flags the account, block payout and route it to exception ops instead of using manual side-channel payouts.

| Gate | What to check | Payout action |

|---|---|---|

| Onboarding identity checks | Required account information is collected and the required payout or charge capability is enabled | Block payout until capability is enabled with no blocking requirements |

| Verification status | Pending or past-due status, including outstanding requirements.currently_due; for Custom accounts, the due-date window is 14 days, and another 14 days later payments may also be paused if unresolved | Freeze payout release and route the exact missing items to exception handling |

| Risk and compliance screening | Current risk status at payout time, including local or global screening and unusual-activity flags | Hold funds until review clears |

| Market policy and reconciliation | Supported program and country coverage, plus payment, held-funds movement, payout event, and reconciliation records that tie together | Confirm through provider reporting and bookkeeping flows, not only an API success response |

Make the release sequence explicit and enforce it in order: buyer payment received, funds posted, policy checks passed, payout queued, payout executed, reconciliation confirmed. Payout schedule and fund availability are separate, so a daily payout setting does not mean every captured payment is ready to pay out.

- Onboarding identity checks

This is the first hard gate. Providers require account information before enabling charges and payouts, and PayPal requires seller onboarding before sellers can accept PayPal payments on your platform. Your operational checkpoint is not "form submitted." It is "required payout or charge capability enabled" with no blocking requirements.

- Verification status and outstanding requirements

Verification can change over time, so this gate is ongoing, not one-and-done. Adyen requires verification before payment processing and payouts, and notes that additional checks can disable payouts. Stripe also indicates outstanding requirements.currently_due can restrict capabilities. For Custom accounts, the due-date window is 14 days, and payouts can be paused. Another 14 days later, payments may also be paused if unresolved. If an account is pending or past due, freeze payout release and route it to exception handling with the exact missing items.

- Risk and compliance screening

Identity checks alone are not enough. PayPal states it performs local and global risk and compliance screening, and Adyen includes controls to flag unusual activity and stop suspicious payouts. Use current risk status at payout time, not only onboarding status. If flagged, hold funds until review clears.

- Market-specific policy controls and reconciliation confirmation

Program and country coverage vary by provider, and payout behavior is not globally uniform. Build those caveats into both product logic and ops procedures, and apply controls where supported and enabled. After payout executes, confirm reconciliation through provider reporting and bookkeeping flows, not just an API success response. If you cannot tie payment, held-funds movement, payout event, and reconciliation records together, the flow is not complete.

Where marketplace margin gets lost and how to defend effective take rate#

Do not manage marketplace margin from booked platform fees alone. Effective take rate can leak after checkout through payout choices, refunds, disputes, reconciliation gaps, and buyers or sellers moving off-platform.

1. Map leakage at the transaction level#

Track margin leakage per transaction, or losses will hide inside blended GMV, adjustments, and exception queues. Your working view should show platform fee earned, processing and network cost, payout cost, refund or dispute impact, and whether payment stayed on-platform from start to finish.

| Leakage point | How margin gets lost | Grounded signal to watch | Control that matters most |

|---|---|---|---|

| Processing fees | Fixed plus variable costs can compress low-ticket orders quickly. A Stripe domestic card example is 2.9% + 30¢ per successful transaction. | Net platform fee after processor cost by order cohort | Update your application fee or platform fee policy by ticket size, not one flat percentage |

| Payout costs | Faster payout can become a margin product you subsidize. In the US, a Stripe Instant Payout update moved pricing from 1% to 1.5% per payout starting June 1, 2024, while standard payout is 2 business days for free. | Share of seller volume using instant vs standard payout | Set payout timing rules and charge for accelerated access where your model supports it |

| Refund handling | A refund may not unwind upstream costs because banks and card networks can keep upfront transaction costs. | Refunded GMV vs nonrefundable processor cost | Keep platform-fee policy and seller reserve logic aligned with refund exposure |

| Dispute losses | A dispute reverses the payment and can add a dispute fee. Taking no action is treated as accepting the dispute. | Dispute rate, win rate, and evidence submission timeliness | Put dispute evidence on a strict SLA with clear ownership and escalation |

| Off-platform disintermediation | Users bypass your payment flow and transact off-platform, which directly removes revenue capture. | Drop in repeat on-platform payment rate after initial match or message | Tighten payment-policy enforcement and product incentives that keep repeat activity on-platform |

| Ops overhead | Manual payout handling shifts reconciliation burden to the platform team and can increase exception risk. | Manual payout count and unreconciled exception queue | Use settlement-batch reconciliation and reduce manual payout creation |

The real operator check is not a high-level dashboard. Finance should be able to tie settlement-batch payout reconciliation to transaction-level fee and cost reporting. If your close pack cannot connect order, platform fee, refund or dispute adjustment, payout batch, and bank settlement in one chain, your margin view is probably overstated.

2. Attach one control to each loss line#

Assign one named control to each leak. Processing fees and payout costs are pricing controls, meaning platform fee policy and payout timing policy. Refunds and disputes are execution controls, meaning evidence quality, deadlines, and ownership.

Payout speed should be an explicit pricing decision, not a default. If Instant Payouts can settle within 30 minutes but a standard schedule can be 2 business days with no payout fee, define when faster access is worth paying for. Define who pays for it, too.

Disputes need hard operating rules. A chargeback can reverse payment and debit the dispute amount plus a dispute fee, and taking no action is treated as acceptance. Set an evidence SLA, assign an owner, and treat late or incomplete submissions as expected loss in reporting and policy feedback loops.

3. Change controls by marketplace shape#

Marketplace shape changes where take rate leaks first. In high-frequency, low-ticket models, fixed card costs like the 30¢ in 2.9% + 30¢ matter more per order. Refund costs can add up quickly, and dispute handling can become labor-heavy relative to order value.

In lower-frequency, high-ticket models, single refunds or disputes hit harder in absolute dollars, and payout timing decisions carry more cash-risk weight. Cost mix can also differ when bank transfer fits the use case: ACH on Stripe is listed at 0.80%, capped at $5.00. If that applies to your flow, see ACH Payment Processing for Platforms: How to Move Money via the US Banking Network.

4. Separate accrued revenue from cash timing#

Keep revenue recognition separate from payout and cash timing. Under ASC 606-10-25-23, revenue is recognized when the customer obtains control of a good or service, and accrued revenue is recognized before billing or cash receipt.

For two-sided platforms, that means you can earn a platform fee while cash is still moving through settlement, refund windows, and payout timing. The practical defense is a close package that separates revenue booked, cash settled, and open liabilities or adjustments from refunds, disputes, and pending payouts.

For a step-by-step walkthrough, see Building a Two-Sided B2B Marketplace to Reach $100M GMV.

Before locking your architecture, run current vs target fee mix through the payment fee comparison calculator to stress-test effective take rate assumptions.

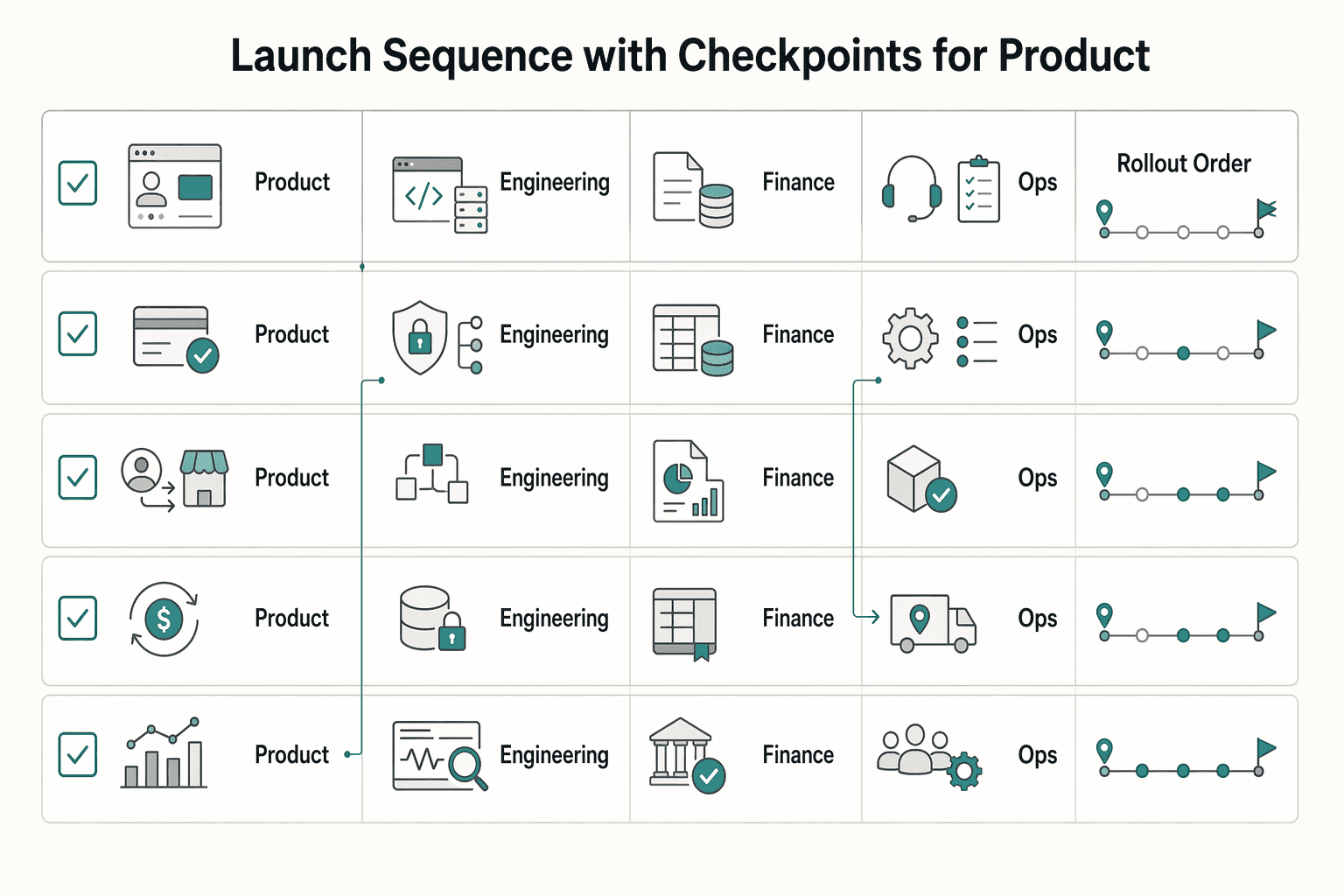

Launch sequence with checkpoints for product, engineering, finance, and ops#

Launch in gates, not in one "payments are live" moment. If you cannot show who gets debited for refunds, what record supports a seller payout, and how finance ties that payout to underlying transactions, you are still in build mode.

| Checkpoint | Main control | Grounded detail |

|---|---|---|

| Product | Lock payment and fund-flow design | Charge type determines how funds are split and can determine which account is debited for refunds and chargebacks |

| Engineering | Design for retries and async events | Use idempotency keys on POST requests; make webhook handling idempotent; persist needed events because processor Event objects are retrievable for 30 days |

| Finance | Prove reconciliation on real settlement data | Preserve transaction-to-payout linkage; where available, automatic payouts help maintain that association; payout.paid and payout.reconciliation_completed can drive automated reconciliation |

| Ops | Define exception queues before first live payout | Block payout if verification is pending or failed; returned payouts are typically seen within 2-3 business days; disputes should run from dispute-created webhooks with a named escalation owner |

| Rollout order | Release in stages | Use sandbox simulation, limited cohort rollout, controlled volume ramp, then market expansion |

Use the checkpoints below in order. They force agreement across product, engineering, finance, and ops before volume makes mistakes expensive.

- Product checkpoint

Lock payment flow and fund-flow design before UI launch. In marketplace setups, charge type determines how funds are split and can determine which account is debited for refunds and chargebacks, so your spec should clearly map buyer payment, seller payout, refund path, and dispute ownership.

Run one alignment test: can product, ops, and finance all answer "who loses cash first if this payment is refunded or disputed?" from the same diagram? If responsibility changes by configuration, document that explicitly.

- Engineering checkpoint

Build for retries and async events from day one. Use idempotency keys on POST requests so retries do not create duplicate objects or duplicate money movement, and make webhook handling idempotent with stored event IDs and duplicate-safe processing.

Keep audit-ready API request logs for buyer payment and seller payout flows. Because processor Event objects are retrievable for 30 days, persist the events you need for investigations instead of depending on short-window retrieval later.

- Finance checkpoint

Do not scale volume until reconciliation works on real settlement data. The key control is preserving transaction-to-payout linkage. Where available, automatic payouts help maintain that association, and events like payout.paid and payout.reconciliation_completed can drive automated reconciliation.

Set accrued revenue treatment before scale. Under ASC 606 and IFRS 15, the anchor is transfer of control, not cash timing. For a deeper revenue treatment walkthrough, see Accrued Revenue for Platforms: How to Recognize Revenue Before Buyers Pay in a Two-Sided Marketplace.

- Ops checkpoint

Define exception queues before the first live payout. Treat verification as a hard gate: if verification is pending or failed, block payout and route the case to exception handling. If issues are not resolved in time, capabilities can be disallowed, so keep a clear exception path.

Separate queues for returned payouts and disputes. Returned payouts are typically seen within 2-3 business days, and incorrect destination information is a common cause, so start triage there. For disputes, run an event-driven queue from dispute-created webhooks with a named escalation owner.

- Rollout order

Use this order: sandbox simulation, limited cohort rollout, controlled volume ramp, then market expansion. Sandbox testing is necessary, but a canary-style rollout is what limits blast radius. Release to a small slice first, confirm payment, payout, refund, and reconciliation behavior, then expand.

Related: Payments Infrastructure for Creator Platforms: A Complete Build vs. Buy Guide.

Conclusion#

- Operational fit beats feature depth.

The right choice is the setup your team can run cleanly now, not the provider with the longest feature checklist. A marketplace payment provider affects UX, revenue strategy, cost structure, and scalability, so start with practical filters: country coverage, compliance ownership, and reconciliation maturity.

Reconciliation is the real test. Automatic payouts keep transaction-to-payout linkage, which simplifies reporting. With instant payouts, your team is responsible for reconciling payouts against transaction history. If finance and ops cannot reliably tie bank movement to platform activity, operating risk rises fast.

- Choose one architecture intentionally, and define migration triggers now.

Provider-managed flows can work early, while some teams later move to more ledger-backed control when reconciliation, verification handling, and payout exceptions consume too much time. The goal is not a perfect end state on day one. It is a clear current model, clear change triggers, and clear ownership across product, engineering, finance, and ops.

Use concrete triggers: payout matching slows close cycles, compliance handling outgrows default provider flows, or expansion requires more country and currency control. Treat profitability signals, controls, and payout reliability as shared KPIs. Connect Onboarding can reduce basic KYC handling complexity, but it does not replace independent legal KYC obligations.

- Validate market and program coverage before you commit rollout dates.

Country support, currencies, fees, and integration complexity all belong in selection, and key limits are platform-specific. Connected-account country availability depends on your platform's business location, and cross-border payouts are qualification-based.

Verify gated capabilities early as well. Some features require explicit access requests, and some markets are still unsupported or in "register interest." Even where multi-currency settlement supports up to 18 currencies, confirm what is actually enabled for your platform country and connected-account countries before you promise timelines.

Frequently Asked Questions

What is the practical difference between payment flow and fund flow in a two-sided marketplace?

Payment flow is how the buyer is charged. Fund flow is how money is distributed between the platform and connected accounts, when funds become available, and when payouts happen. In separate charges and transfers, the platform charge is decoupled from later transfers.

How do refunds and disputes change seller payout timing and effective take rate?

Refunds and disputes reduce the payments balance, so they can shrink or delay what is available for seller payouts. Who is debited depends on charge type and liability setup. If a connected account goes negative after a refund or dispute, reserves can further constrain available balances.

When should a platform move from direct PSP payouts to a ledger-first model?

A platform should move when provider-managed flows start breaking under exceptions and tighter payout control is needed. Common triggers include repeated transfer reversals, platform balance pressure, and rising refund or dispute handling. There is no universal numeric cutoff.

What compliance checks should block payout even after buyer payment is received?

Pending or failed verification should block payout even if buyer payment succeeded. Required account information must be collected, required capabilities must be enabled, and outstanding requirements should be cleared. Current risk or compliance flags should also hold funds until review clears.

How do we reduce disintermediation without adding excessive friction?

Treat disintermediation as a revenue problem first. Make the on-platform path more trustworthy and easier to complete around checkout, payout predictability, and refund and dispute handling. If a control does not improve trust, compliance, or payout reliability, it is probably just friction.

Is ACH payment processing enough for marketplace scale, or do we need multiple rails?

ACH can be a strong domestic rail because it is low-cost and batch-oriented. It is not the right fit for every buyer or market. If you need broader conversion across customer locations and currencies, use multiple rails and tune the mix.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- docs.stripe.com/payments/bank-transferstrusted

- docs.stripe.com/connect/separate-charges-and-transferstrusted

- federalreserve.gov/paymentsystems/fedach_about.htmtrusted

- hbs.edu/faculty/Pages/item.aspxtrusted

- stripe.com/resources/more/two-sided-marketplace-strategytrusted

- taxation-customs.ec.europa.eu/taxation/vat/vat-directive/place-taxation_entrusted

- docs.adyen.com/platforms/verification-overviewexternal

- fasb.org/page/pccAccordionexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

ACH Payment Processing Platforms for U.S. Collections and Payouts

Start with the outcome, not the feature label. You may need a setup that collects money in and sends money out over the U.S. banking network, not just a generic bank-transfer option. In practice, that often means ACH debits for collections and ACH credits for payouts, with controls your product, engineering, and finance teams can run in production.

How Marketplace Operators Choose a Platform Payments Architecture That Lasts

# Marketplace Payments Architecture: MoR vs Split Flows, Real Margins, and Launch Controls

Accrued Revenue for Platforms Recognizing Revenue Before Buyers Pay

You can recognize revenue in a two-sided marketplace before buyer cash arrives, but only if you separate the earning event from billing and make the reclass path explicit. The practical job is to design the accounting so your finance, ops, and product teams can record revenue early without losing control of reconciliation. If you cannot explain that path clearly, your close team will feel it at month end.