Quick Answer

Start by sequencing operator decisions before growth spend: lock transaction ownership, prove replay-safe APIs and webhooks, and enforce payout eligibility through KYC/KYB/AML states. Then build density in one buyer-supplier wedge, measure transaction quality separately from topline growth, and expand only after reconciliation from ledger journals is consistently clean. Use ARR case studies for context, but run GMV execution on your own checkpoints, including payout batches, dispute handling, and documented exception ownership.

Why most two-sided B2B platforms stall before meaningful GMV#

Step 1. Reset the benchmark. A lot of marketplace advice explains two-sided mechanics well, but says much less about the sequence of decisions that actually gets you from zero to meaningful gross merchandise value. You can find plenty on supply and demand loops, pricing, and product-market fit. What is harder to find is a repeatable path that keeps transactions moving as volume rises.

That matters because milestone stories can distort planning. Sturgeon Capital's $100m ARR analysis is useful context for how startups grew across India, Indonesia, Brazil, and Mexico. But ARR is annualized revenue, not proof that your marketplace can generate and process GMV reliably at scale. Use ARR case studies for pattern recognition, not as a substitute for the operating choices a two-sided platform needs.

Step 2. Organize the work by decision owner. A go-to-market plan needs to be a concrete, time-bound blueprint, not a strategy document full of aspirations. If your team has a 12 to 24 month growth story but no 90 day operating plan, you are still in planning mode. Start with a simple owner map before you debate tactics:

- Product decides what transaction should happen first and what behavior counts as a successful match.

- Finance decides what counts as recognized platform revenue versus GMV and what exceptions are unacceptable.

- Operations decides where manual review is tolerable and where it will break the team.

- Engineering decides what must be observable before volume hides failures.

Use one practical checkpoint: if you cannot name one owner for each of those decisions, plus the pass or fail condition they are using, delay scale work. You do not have a growth problem yet. You have an accountability problem.

Step 3. Use ARR stories for context, not for substitution. ARR narratives still help in one way: they remind you that market pull usually develops gradually. Product-market fit is often the shift from push to pull, and almost never a clean, sudden moment. That matters because marketplace teams can mistake early hustle for durable liquidity.

The failure mode is familiar. A team sees encouraging booked revenue, raises spend, expands categories, and assumes the rest will catch up. Then transaction quality stalls because the operating foundation was never tested. In ARR businesses, a flatline in MRR can be a warning. In marketplaces, the equivalent is repeated effort without repeatable transaction behavior.

Step 4. Commit to checkpoints, red flags, and recovery moves up front. The rest of this article follows the decisions you need to make in order, with clear checkpoints after each one. Expect specific failure signals, such as owner gaps, growth plans without a 90 day operating layer, or evidence of push without real pull. Expect recovery moves too, so you can correct course before expensive rework spreads across product, finance, ops, and engineering.

If you want a deeper dive, read Two-Sided Marketplace Dynamics: How Platform Supply and Demand Affect Payout Strategy.

What to prepare before you scale anything#

Before you spend on growth, lock the basic launch controls first: clear decision owners, a minimum evidence pack, and observability that explains each money movement without guesswork.

| Control | What to confirm | Scale implication |

|---|---|---|

| Define ownership before launch | One accountable owner per milestone; name who owns pricing and liquidity decisions, KYC/KYB/AML policy gates, and payout-risk exceptions | If ownership is unclear, decisions that were fast at low volume usually slow down as volume rises |

| Assemble the minimum evidence pack | Target segment, initial supply-density plan, reconciliation requirements from ledger journals, and the escalation path for payout failures | Treat supply depth as a prerequisite before scaling demand |

| Confirm integration readiness under retry and failure | Requests can be retried safely, webhooks are consumed reliably, and payment or payout status changes are visible in an audit trail | If a failed payout cannot be detected, routed, and resolved clearly, you are not ready to scale |

| Set one go/no-go checkpoint | Trace request -> provider reference -> ledger journals -> export | If you cannot trace that path, delay scale and fix observability first |

- Define ownership before launch.

Your go-to-market plan should assign one accountable owner per milestone, not just revenue targets. Name who owns pricing and liquidity decisions, who owns KYC/KYB/AML policy gates, and who can approve payout-risk exceptions. If ownership is unclear, decisions that were fast at low volume usually slow down as volume rises.

- Assemble the minimum evidence pack.

Write down your target segment, initial supply-density plan, reconciliation requirements from ledger journals, and the escalation path for payout failures. Treat supply depth as a prerequisite before you scale demand.

- Confirm integration readiness under retry and failure.

Prove requests can be retried safely, webhooks are consumed reliably, and payment or payout status changes are visible in an audit trail. Replay the same request and verify that it does not trigger duplicate downstream actions. If a failed payout cannot be detected, routed, and resolved clearly, you are not ready to scale.

- Set one go/no-go checkpoint.

Make this rule explicit: if you cannot trace request -> provider reference -> ledger journals -> export, delay scale and fix observability first. This keeps finance trust intact and prevents growth from turning into a support problem.

Related: How to Calculate LTV for a Two-Sided Marketplace: Buyer LTV Seller LTV and Platform LTV.

Choose your transaction model before growth spends#

Decide who owns the transaction before you increase demand spend. Product-market fit usually emerges gradually, which makes it easy to delay this call while volume still feels manageable. Make it early anyway, because this choice sets your finance workflow, support path, and compliance operating model.

Step 1. Name the transaction owner in writing#

Create a one-page responsibility matrix before you approve more growth spend. Keep it explicit: who accepts buyer payments, who controls settlement timing, who handles disputes and exceptions, who records platform fees, and who owns tax or reporting artifacts where they apply.

Then run one sample order end to end. Confirm that the same ownership logic appears in contracts, payment records, ledger journals, support handling, and payout release decisions.

Step 2. Compare models explicitly before you scale#

Use a short decision table that finance, ops, engineering, and legal can all sign off on:

| Decision point | What to lock in writing before expansion |

|---|---|

| Payment acceptance | Who is the transaction owner in provider terms and customer-facing records |

| Settlement control | Who decides timing, holds, and exception release |

| Dispute handling | Who owns intake, evidence, and resolution path |

| Margin structure | How amounts are reported (gross/net) and posted in ledger journals |

| Tax/reporting artifacts | Who collects, validates, stores, and exports items such as VAT validation, W-8/W-9, and Form 1099 where enabled |

Set a hard internal rule: if you need tighter control over payment acceptance consistency and tax handling, prioritize a Merchant of Record path only after provider terms and counsel confirm the split. If flexibility is more valuable, keep more responsibility in-house and plan for the added operational burden.

Step 3. Map artifact ownership before acquisition spend#

Treat artifact handling as part of model design, not cleanup. If VAT validation, W-8/W-9, or Form 1099 workflows apply to your jurisdictions, assign ownership for collection, exceptions, storage, and export before you scale.

Use one no-go checkpoint: do not expand acquisition until transaction ownership, artifact ownership, and dispute ownership are documented and verified on a sample order.

For a step-by-step walkthrough, see MoR vs. PayFac vs. Marketplace Model for Platform Teams.

Build liquidity in one wedge before expanding geographies#

Build density in one narrow wedge first, then expand. In a B2B marketplace, repeat useful matches in the same buyer and supplier cohorts are a stronger signal than broad but shallow coverage.

Step 1. Pick a wedge that can repeat#

Choose one buyer use case, one supplier profile, and one transaction pattern, then watch it across multiple cycles. The goal is to see demand move from push to pull over time, because product-market fit is usually gradual rather than instant. If every order still needs heavy persuasion, keep narrowing before you expand.

Step 2. Fix match quality before you widen scope#

If outcomes are inconsistent, improve onboarding, eligibility checks, and matching inside the current wedge before you add regions or categories. On a two-sided platform, signup growth can hide weak execution. More listings do not help if buyers still fail to find reliable fulfillment.

Step 3. Separate liquidity signals from growth noise#

Track wedge-level transaction quality, successful matches, and repeat behavior separately from top-line growth metrics. GMV and ARR matter, but they do not tell you on their own whether the market is becoming easier to use. If you cannot isolate wedge performance clearly, fix instrumentation first.

Step 4. Expand geographies only after operations stay steady#

Geography expansion should follow operating trust, not lead it. Add a new region only when your current operating model stays stable under normal variance without a rising manual burden. If expansion erodes reliability, collapse back to the strongest wedge and rebuild density before pushing wider.

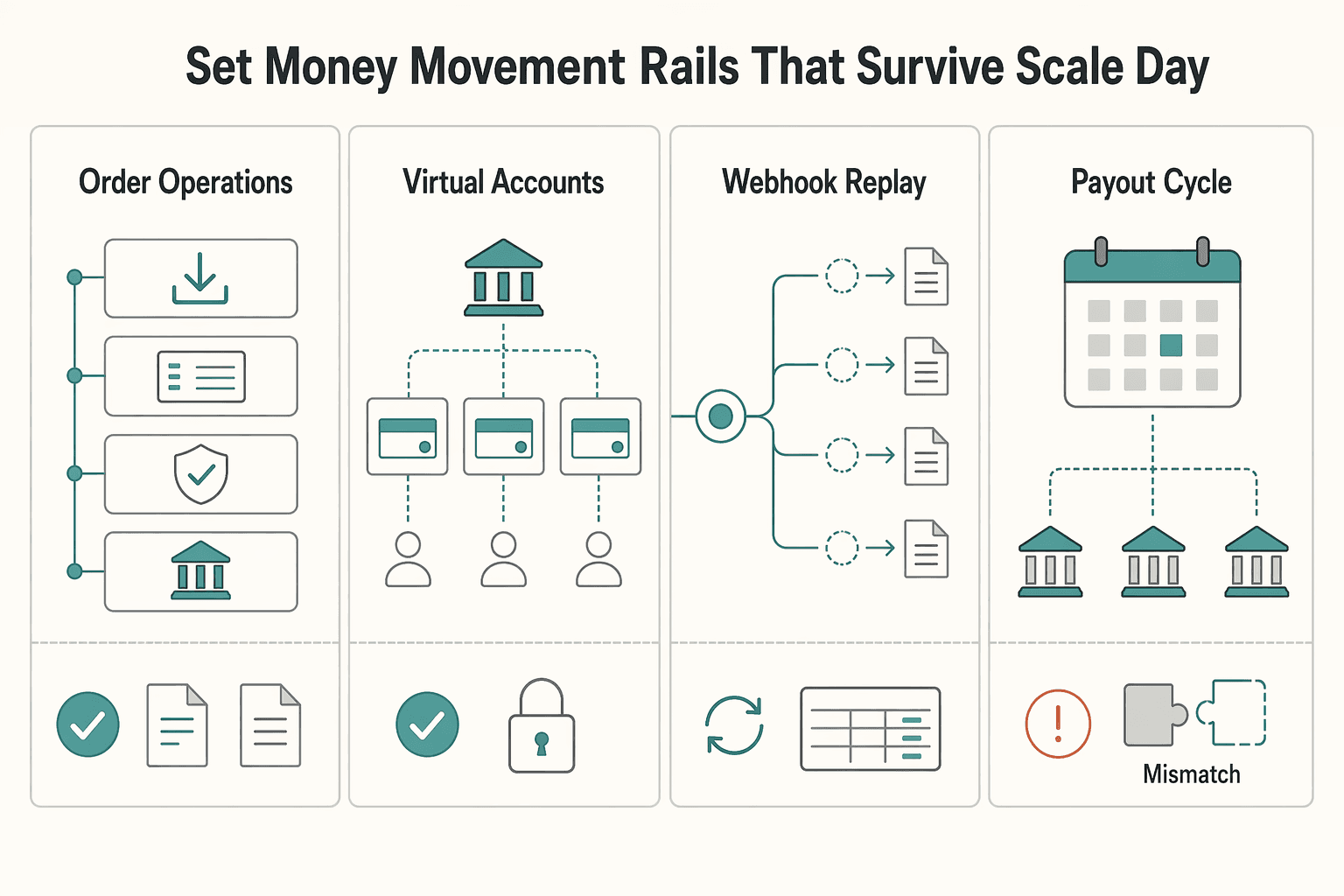

Set up money movement rails that survive scale day#

There is no single rail design validated by the evidence here, so use this as an operating checklist: your flow should be predictable, testable, and easy to reconcile before you push volume.

| Rail area | Requirement | Validation |

|---|---|---|

| Order of operations | Use one consistent sequence for collecting funds, posting ledger journals, running checks, and releasing payouts | Trace sample orders end to end to confirm each handoff is recorded the same way |

| Virtual Accounts | Use selectively for repeat bank-transfer flows where supported | Validate that incoming funds can be mapped to the right buyer and transaction context without a growing manual exception queue |

| API and webhook replays | Test idempotency controls across both API endpoints and webhook handlers | Replayed events should converge to one final business outcome, not conflicting states that require manual cleanup |

| Payout cycle close | Review cycle completeness, exception queue age, and reconciliation-ready evidence exports together | A high-level success view is not enough if unresolved exceptions or weak audit detail are still accumulating |

Step 1. Lock one order of operations and use it consistently. If you collect funds, post ledger journals, run checks, and release payouts in a different order across paths, reconciliation risk usually rises. Define one sequence in your system, then trace sample orders end to end to confirm that each handoff is recorded the same way.

Step 2. Use Virtual Accounts selectively for repeat bank-transfer flows. Where supported, Virtual Accounts can simplify repeat inbound transfers, but only if matching is clean. Validate that incoming funds can be mapped to the right buyer and transaction context without building a growing manual exception queue.

Step 3. Make retries safe if you rely on API and webhook replays. If you use idempotency controls, test them across both API endpoints and webhook handlers. Replayed events should converge to one final business outcome, not branch into conflicting states that require manual cleanup.

Step 4. Close each payout cycle with three explicit checks. Review cycle completeness, exception queue age, and reconciliation-ready evidence exports together. A high-level success view is not enough if unresolved exceptions or weak audit detail are still accumulating.

For related reading, see Content Marketing for B2B SaaS That Holds Up Under Real Work.

Put compliance and tax gates in the transaction path#

Your payout path should release funds only after required compliance and tax states are resolved under your policy, not as back-office cleanup after money moves.

Step 1. Gate payout eligibility with explicit compliance states. Tie payout eligibility to resolved account states, not order completion alone. If you use KYC, KYB, and AML controls, make payout release depend on those states being complete and traceable, with a clear decision source before a hold is lifted.

Step 2. Separate hard blocks from manual-review cases. Use non-bypassable hold states for clear failures or missing required items, and route ambiguous cases to manual review with named override authority, reason codes, and evidence. This keeps exceptions auditable and prevents ad hoc releases that are hard to justify later.

Step 3. Collect tax artifacts early and re-check at payout milestones. Capture tax documentation at onboarding, then re-check it before payout events where your workflow requires it. If your reporting setup includes W-8, W-9, VAT validation, Form 1099 workflows, or FBAR-related inputs, store those fields as part of the transaction path instead of rebuilding them later.

Step 4. Handle FBAR inputs with filing-grade precision, and pause expansion when exceptions outrun capacity. For FBAR (Report Foreign Bank and Financial Accounts) workflows, value each account separately and record the maximum account value as a reasonable approximation of the greatest value during the calendar year. Record amounts in U.S. dollars rounded up to the next whole dollar (for example, $15,265.25 becomes $15,266). Do not hardcode one deadline: the April 15, 2027 extension applies to certain individuals, while other individuals with an FBAR filing obligation remain due April 15, 2026. If review queues and document exceptions grow faster than your team can clear them, pause corridor expansion until controls and staffing catch up.

Instrument the metrics that predict durable GMV#

Durable GMV tracking starts with one rule: use only metrics you can trace to real system events, not blended growth charts.

Step 1. Build one scorecard from activity quality to money outcomes. Track liquidity health, payout success, dispute rate, and reconciliation lag from ledger journals in one place. Run this as a 90-day operating plan with a named owner, review cadence, and action threshold for each metric so accountability is explicit.

Step 2. Keep GMV and ARR separate in every planning view. GMV and ARR answer different questions, so report them separately with clear labels and definitions. If marketplace volume, transaction revenue, and subscription revenue are mixed into one unlabeled growth view, planning quality drops fast.

Step 3. Use external benchmarks as directional context, not operating truth. Use inputs like FJ Labs, Point Nine Capital, and Version One to pressure-test your assumptions, not to set targets for your platform. If benchmark narratives conflict with your dispute trends or reconciliation lag, prioritize your own operating data.

Step 4. Make event-level attribution non-negotiable. A metric should not drive pricing, corridor expansion, or headcount unless you can recreate it from an API call, webhook event, or ledger posting. Store the event source, metric owner, calculation logic, and decision use with each KPI. Require an end-to-end event trail before it enters weekly review.

Common failure modes and how to recover without a full rebuild#

Most stalls do not need a rebuild. They usually need tighter scope and clearer controls at the point where trust is breaking.

| Issue | Evidence | Recovery move |

|---|---|---|

| Activity spread too thin | Activity is spread too thin across categories or corridors | Pause expansion and refocus on the cohorts that already transact reliably |

| Off-platform movement | Repeat partners are moving off-platform | Improve payout reliability and strengthen reporting and operational tooling they depend on |

| Review load rising | Holds and manual reviews increase | Tighten and clarify KYC, KYB, and AML decision rules; automate clearly low-risk approvals where possible; standardize exception evidence |

| Finance trust gap | Balance variance is not clearly explained | Reconcile from ledger journals, validate payout batches, and publish a weekly exception-close report |

Step 1. Collapse fragmented liquidity. If activity is spread too thin across categories or corridors, pause expansion and refocus on the cohorts that already transact reliably. Rebuild density there first, then re-expand in a controlled way.

Step 2. Make bypassing the platform less attractive. If repeat partners are moving off-platform, improve payout reliability and strengthen reporting and operational tooling they depend on. The goal is simple: staying on-platform should be easier and more useful than side-channel workflows.

Step 3. Tighten compliance decisions, not just staffing. When holds and manual reviews increase, tighten and clarify KYC, KYB, and AML decision rules. Automate clearly low-risk approvals where possible, and standardize exception evidence so reviews are consistent.

Step 4. Rebuild finance trust from ledger journals. If balance variance is not clearly explained, reconcile from ledger journals, validate payout batches, and publish a weekly exception-close report. Keep each exception tied to an owner and current status so finance and ops are working from the same facts.

You might also find this useful: Platform-to-Platform Payments: How to Build B2B Settlement Between Two Marketplace Operators.

Want a quick next step? Try the free invoice generator.

Your next 90 days and the checklist to execute#

For the next 90 days, run an execution plan before a growth plan: align decisions, assign owners, and require auditable evidence before you add channels. Keep the plan concrete, time-bound, aligned to business strategy, and explicit about milestone ownership.

Step 1. Align the non-negotiables#

Start by locking one answer to three decisions: your transaction model, your first liquidity wedge, and the compliance posture for that wedge. If product, finance, ops, and engineering would answer differently, pause expansion until you resolve the conflict.

Ship a short decision memo with named owners, decision dates, open risks, and explicit approvals. The checkpoint is consistency across teams and clear accountability for overrides, exceptions, and escalation paths.

Step 2. Build the minimum operating backbone#

After the model is fixed, implement the minimum backbone you need to trust a transaction end to end: idempotent APIs, reliable webhook handling, traceable ledger journals, and auditable payout batches. Your verification standard should be practical: trace a real transaction from request through provider reference, ledger posting, and payout/export output.

Do not treat vendor demos or benchmark slides as proof. Some investor and market materials explicitly state third-party data was not independently verified and is subject to change, so your evidence should come from your own environment and owners.

Step 3. Gate expansion with operating checkpoints#

Expand only after your current wedge passes clear operating checks for payout reliability, compliance throughput, and reconciliation accuracy. Keep GMV and ARR reporting separated so metric ownership stays correct and remediation goes to the right team.

Use this checklist in your 90-day plan:

- Confirm MoR versus non-MoR responsibility split

- Confirm KYC/KYB/AML gating states and override ownership

- Confirm Virtual Accounts and payout rail availability by market or program

- Confirm W-8/W-9 and VAT validation capture points

- Confirm GMV versus ARR reporting separation and metric attribution

- Confirm incident recovery for failed payouts and unmatched ledger events

Frequently Asked Questions

What is a two-sided B2B marketplace strategy in practical terms?

It is the set of decisions that makes both sides get value at the same time: which buyer and seller cohort you start with, how you create repeat matches, and where your platform earns revenue through a take rate or subscription layer. In plain terms, you are not just selling software. You are making transactions happen reliably enough that both sides come back.

Which side should you scale first in a two-sided platform, and when should that change?

Start with the side that determines whether the other side gets an acceptable first experience, which is often supply. One operator-reported pattern says teams that solve supply density before scaling demand reach profitability faster, while teams that do the reverse can send buyers into thin coverage and lose them. Shift more effort to demand only when your core wedge has enough coverage and consistent conversion quality.

What metrics matter more than user growth when targeting durable GMV?

User counts can hide a weak market. You want indicators tied to transaction quality, especially supplier coverage in the core wedge, search-to-transaction conversion, repeat transactions, and buyer outcomes after first use. In one reported diagnostic example, heavy buyer acquisition spend ($180K/month) paired with weak supplier coverage (35%) and low search-to-transaction conversion (4%) signaled a liquidity problem, not proof of scale.

How is planning for $100M GMV different from planning for $100M ARR?

Treat them as different operating targets. ARR is annualized revenue, and the cited ARR source is explicitly about startups that reached $100M in annualized revenue. That does not, by itself, show marketplace transaction execution, so GMV planning should be evaluated with marketplace liquidity and transaction-quality evidence.

What usually breaks first as a marketplace scales across regions?

The cold start problem can reappear in each new market. A wedge that works in one region can lose density when buyers and sellers are spread too thin, so conversion can drop before growth headlines show the damage.

When does disintermediation become a material risk, and what can you do early?

Avoid hard rules on this point unless you have additional validated data for your specific marketplace.

What infrastructure must be in place before aggressive expansion?

You need enough transaction visibility to tell whether growth is improving or degrading marketplace health. At minimum, make sure you can measure supplier coverage and search-to-transaction conversion by core wedge before scaling demand.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- downloads.cs.stanford.edu/nlp/data/jiwei/data/vocab_wiki.txttrusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- sec.gov/Archives/edgar/data/1784535/0001213900200195...trusted

- elefanterevops.com/blog/go-to-market-planexternal

- fahrikarakas.medium.com/asked-claude-10-questions-about-2026-here-ar...external

- fasterthannormal.co/businesses/faireexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Supply and Demand Dynamics Should Set Your Marketplace Payout Strategy

In a two-sided marketplace, payout strategy is not back-office plumbing. It can shape whether sellers stay active, whether transactions complete reliably, and whether buyers can find supply that is ready to transact.

How to Calculate LTV in a Two-Sided Marketplace for Buyer, Seller, and Platform Decisions

In a two-sided marketplace, many teams look at buyer-side and seller-side value separately, then compare each view to the relevant Customer Acquisition Cost instead of forcing everything into one blended ratio. Treat Lifetime Value as an operating number, not a spreadsheet guess.

Platform-to-Platform Payments: How to Build B2B Settlement Between Two Marketplace Operators

If you need to stand up operator-to-operator settlement quickly, optimize for a controlled launch, not maximum speed on day one. This guide focuses on platform-to-platform B2B settlement for marketplace operators. It keeps the tradeoffs, control points, and recovery paths explicit for delayed, returned, or mismatched payments.