Quick Answer

Yes, multi-currency payment links work well for fast launch if settlement design is defined first. Use them to localize checkout quickly, then block rollout until one corridor test reconciles checkout currency, captured amount, settlement currency, and bank payout amount. If those values do not align in testing, tighten quote validity handling, expiry rules, and duplicate-safe webhook processing before expanding.

Why offer local currency payment links#

Multi-currency payment links can speed up international collection, but the harder decision is operational: will your FX, settlement, and reconciliation setup produce the outcome finance and ops expect after payment?

At the collection layer, a payment link is a shareable hosted payment page you can create and send without building a full website checkout. That makes it a practical no-code or low-code way to test local-currency collection before investing in a heavier checkout build.

But customer currency choice and settlement outcome are not the same thing. A buyer in Germany might pay in euros while a buyer in Australia pays in Australian dollars, yet your setup may still convert incoming funds to a default home-currency payout depending on the provider and account configuration.

For each currency you plan to show at checkout, start with one question: what happens after authorization? Some setups can accrue balances and pay out in additional currencies. Others auto-convert incoming funds. Shopify documents the same pattern: you can sell in multiple currencies while still receiving payouts only in domestic currency. If you do not verify that early, conversions, fees, and reporting can surprise you after launch.

Then confirm settlement routing. Provider and account conditions can determine whether funds settle locally or move as a cross-border transfer. Adyen notes that if local payout is unsupported or you do not have a local bank account, settlement may occur via cross-border transfer. That changes treasury assumptions, payout timing, and support expectations.

Before you start#

Treat payment links as a collection shortcut, not a control shortcut. FX logic, accounting treatment, regulatory compliance, transaction costs, system integration, security, and customer experience still need clear ownership.

Run at least one end-to-end test transaction per target corridor and compare four fields side by side: checkout currency, captured amount, settlement currency, and bank payout amount. If those fields do not reconcile in test, production will not fix the mismatch.

Defaults matter too. Checkout.com payment links expire after 24 hours by default, which may be fine for short-lived invoices but risky for longer collection cycles.

The opportunity is large: global payments are projected to rise from $190 trillion in 2023 to $290 trillion by 2030. This guide stays practical: when to use links, how to design pricing and settlement, what to verify before go-live, and where hidden risk usually shows up.

For the back-office side, see How to Reconcile Multi-Currency Payouts Across Multiple PSPs in One Ledger.

What multi-currency payment links are and what they are not#

Multi-currency payment links are a fast collection layer, not a replacement for settlement design. A payment link is a shareable URL to a provider-hosted payment page where the payer may see or pay in a supported presentment currency, and the payment then flows into your existing settlement setup.

That distinction matters because many teams treat the checkout screen as proof of the financial outcome. It is not. The customer-facing amount is only one part of the payment chain. What you actually receive, when you receive it, and in which currency you receive it depend on provider support, account configuration, local payout coverage, and whether conversion is applied at charge, transfer, or payout.

What they are

- A no-code or low-code way to launch hosted collection quickly

- A customer-facing presentment choice that depends on provider and payment-method support

- A link-level handoff into your broader FX, settlement, and payout configuration

- A useful testing path when you want to validate localized collection before building a heavier checkout

What they are not

- Proof that funds will settle in the same currency the customer paid. If charge and settlement currencies differ, provider conversion can apply.

- The same thing as cross-border by default. Multi-currency is about processing in different currencies. Cross-border is about payer and recipient being in different countries.

- A full checkout rebuild. This is about link-based collection plus settlement handoff, not custom checkout architecture on Stripe or Checkout.com.

- A substitute for reconciliation, webhook handling, or tax decisions

Keep the scope tight and practical. Confirm supported presentment currencies by payment method, then validate corridor-level outcomes in testing: checkout currency, payment method, settlement currency, and payout result. Provider behavior differs at the link layer and by market, including reusability, one-time versus recurring scope, FX handling, fee logic, and payout coverage.

A useful way to frame the product decision is this: a payment link changes how quickly you can collect, but it does not remove the need to define what "successful collection" means internally. For most teams, that internal definition should include at least:

- the currency shown to the buyer

- the amount the buyer authorized

- the currency finance expects to receive

- the provider reference used to trace the payment later

- the exact event that moves an order from pending to paid

If those are undefined, you are not really launching multi-currency links. You are only launching a hosted page and hoping the back office sorts itself out later.

Decide if payment links are the right collection path#

Use payment links when speed matters most: fast launch, low engineering lift, and controlled localized-checkout testing. Move to embedded or more coded checkout when UX control, tax logic, or routing control matter more than launch speed.

Step 1. Start with the launch goal#

If you need to collect while your site or app checkout is still incomplete, hosted no-code or low-code links are usually the right first move.

They also work well for controlled tests in markets like Germany and Australia. Validate this in your own flow: run journeys from German and Australian English browser locales, confirm localization behavior, and record the presentment currency shown at checkout.

This is the right option when the question is, "Can we start collecting in local currency quickly?" It is a weaker option when the question is, "Can we control every part of checkout behavior, tax treatment, and routing from the first release?"

Step 2. Accept the hosted-page tradeoff#

Use links only if limited checkout customization is acceptable. Hosted link pages are intentionally constrained, which is usually fine for quick collection.

If you already need deeper ownership, move to a coded path instead of forcing payment links to do custom-checkout work. The tradeoff is simple: more control means more build and maintenance responsibility for core checkout logic.

A practical checkpoint is to list the things you cannot compromise on. If your team needs precise control over currency display rules, fallback behavior, order state timing, tax presentation, or payment-method routing, a hosted link may still work, but only if those controls can be handled around the link rather than inside it.

Step 3. Treat webhooks and reconciliation as the real gate#

Do not launch until webhook handling and reconciliation are ready. Creating the link is easy, but reliable fulfillment is the real gate.

Your server-side flow needs webhook-driven payment status handling, must be idempotent for duplicate events, and must support payout reconciliation back to underlying payment activity. If that is not in place, delay launch.

This is where many rushed launches fail. The link works, the customer pays, and then teams realize they do not have a stable way to decide whether the order is truly paid, whether a delayed confirmation arrived, or whether a refund changed the final financial outcome. The operational work is not optional just because the payment page is hosted.

Step 4. Make settlement visibility explicit from day one#

Make settlement visibility explicit from day one so you can scale later without finance rework. Track payment outcomes so presentment-versus-settlement behavior is explicit.

Customer-facing currency and bank-settlement currency can differ, and conversion can apply when they do. Your launch checkpoint is not just "customer paid." It is also "we can verify what currency actually settled and reconcile it."

A simple launch standard is useful here:

- product signs off on the customer-facing currency experience

- engineering signs off on webhook-driven status handling

- finance signs off on settlement visibility

- compliance or legal signs off on the baseline assumptions for card data and tax

If even one of those is still unresolved, payment links are usually being asked to cover for a bigger readiness gap. Related reading: How to Use Stripe Payment Links for Easy Invoicing.

Prepare prerequisites and ownership before you build#

Before you build, make ownership explicit across FX, settlement, tax, and webhook operations. If these decisions are unowned, launch and support risk goes up quickly.

Step 1. Name owners by decision surface#

Assign one named owner per decision surface: product for checkout and currency display, engineering for webhook handling and data scope, finance ops for settlement and refunds, and compliance or legal for PCI DSS posture and tax assumptions. You do not need a perfect RACI, but you do need one escalation point per topic.

| Owner | Focus area |

|---|---|

| Product | Checkout and currency display |

| Engineering | Webhook handling and data scope |

| Finance ops | Settlement and refunds |

| Compliance or legal | PCI DSS posture and tax assumptions |

This matters because multi-currency link projects often fail in the handoffs. Product assumes finance will define settlement behavior. Finance assumes engineering will store the right currency fields. Engineering assumes legal has confirmed the tax model. Clear named ownership reduces those assumptions.

Step 2. Build a minimum evidence pack before implementation#

Build a minimum evidence pack before implementation so provider constraints are documented, not assumed. For Stripe, capture the currencies you plan to support, note charge processing coverage of 135+ currencies, and record that FX can occur when presentment currency differs from settlement currency. For Rapyd, document that payout currency can differ from sender currency and that presentment may be converted into a settlement currency. For Tipalti, treat thresholds as variable and note that failed payments can be marked deferred with notifications to payer and payee.

| Provider | Document these points |

|---|---|

| Stripe | Currencies you plan to support; charge processing coverage of 135+ currencies; FX can occur when presentment currency differs from settlement currency |

| Rapyd | Payout currency can differ from sender currency; presentment may be converted into a settlement currency |

| Tipalti | Thresholds are variable; failed payments can be marked deferred with notifications to payer and payee |

Your pack should include:

- supported presentment currencies and available settlement currencies by provider

- refund rules and provider constraints you have actually verified

- webhook owner, event destinations, and provider-specific retry expectations

- link expiry behavior and whether the link is single-use, reusable, or bounded-use

- the exact fields finance will use later for reconciliation

The point of the evidence pack is not bureaucracy. It is to stop teams from discovering basic settlement behavior after launch.

Step 3. Confirm your control baseline before live traffic#

Confirm your control baseline before live traffic. PCI DSS applies to entities that store, process, or transmit cardholder or sensitive authentication data, and compliance validation expectations can be set by payment brands or your acquirer, not only by internal teams. Document what card data you touch, what you do not store, and how idempotency handles Stripe webhook retries for up to three days in live mode.

Even when the payment page is hosted, your system still has to be clear about what data enters your environment and which events trigger downstream actions. A hosted collection layer can reduce scope in some areas, but it does not remove the need to define how you verify events, update orders, and retain enough data for audit and support.

Step 4. Write EU launch assumptions down early#

Define EU launch assumptions in writing before rollout. VAT is a consumption tax on most goods and services, invoicing is compulsory for most B2B transactions, and cross-border B2C e-commerce VAT rules changed on 1 July 2021. If you are entering EU consumer markets, decide early whether OSS is part of your model. If it is not settled, keep initial payment-link rollout scoped to narrower corridors until tax treatment is clear.

The useful discipline here is to avoid letting a payment-link launch quietly become a tax-model launch. Payment links are good for fast collection. They are not a reason to postpone tax decisions until support tickets start arriving.

If you run a platform and need both collection and payout coverage, see Multi-Currency Payment Processing for Platforms: How to Accept and Disburse in 50+ Currencies.

Design currency presentation and pricing behavior#

Your pricing decision comes down to one question: who absorbs FX movement between checkout and settlement? Decide that per market before launch, then document display, fallback, and accounting rules so behavior stays predictable.

Step 1. Choose a pricing pattern corridor by corridor#

Do not force one global pricing rule across every corridor. Most teams compare three workable patterns:

| Pattern | What the customer sees | Main exposure | Usually fits when |

|---|---|---|---|

| Fixed local price | A static local-currency price | Higher exchange-risk exposure if rates move | You want stable local price perception |

| Base-currency price converted at pay time | A localized amount derived from a base currency | Amount can move based on conversion logic | You want lower pricing maintenance |

| Hybrid | Fixed pricing in selected markets, conversion elsewhere | Mixed exposure and higher operational complexity | You need stability in core markets and flexibility in long-tail corridors |

Static per-currency pricing can simplify customer expectations, but manually set currency prices carry greater exchange risk. Automatic local-currency conversion lowers integration effort, but then quote timing and validity become the control point.

If you need tighter FX control, use time-bounded conversion logic and reject stale quotes. Stripe supports rate locks for 5 minute, 1 hour, and 24 hour periods, with Extended Rate Quotes for 114 local currencies; a lock can expire if the rate moves by more than 3.5%. Define what happens next when a lock expires.

At minimum, record the base currency, presentment currency, conversion method, and maximum accepted quote age for each corridor.

Step 2. Set explicit customer-facing currency rules#

Set explicit customer-facing currency rules so checkout behavior is consistent. Local currency is the checkout currency shown to the customer and used at payment.

Define these three rules in plain language:

- Default display currency by market

- Fallback currency when the preferred currency is unavailable

- Rounding logic for converted amounts

If you use automatic conversion, decide whether conversion fee treatment is included in displayed prices and apply currency-specific rounding consistently. Keep link preview, checkout, confirmation, and internal order records aligned in the same presentment currency to prevent disputes.

The practical issue is not only accuracy. It is consistency. If the quote shown in an email, the amount shown on the hosted page, and the amount stored internally do not align, support cases multiply quickly.

Step 3. Design unsupported-currency behavior before launch#

Unsupported-currency behavior should be designed before production traffic arrives. Currency support varies by payment method and country, and restrictions can also be regional.

Use predictable failure paths:

- Block link creation for unsupported payment method, country, or currency combinations

- If availability changes later, either present a clear fallback currency or stop payment with a clear temporary-unavailable message

- Avoid silent currency switches after the payer has accepted a price

Also define refund handling for converted payments up front, because timing delays can create FX gains or losses. A silent switch from one currency to another is one of the fastest ways to create customer distrust and internal confusion. If a fallback is needed, make it explicit and document the exact conditions under which it is allowed.

Step 4. Connect pricing choices to accounting from day one#

Connect pricing choices to accounting from day one. Presentment and settlement currency can differ, and that is where payments FX appears. If you settle in multiple currencies, configure settlement accounts accordingly. For example, Stripe requires a separate supported bank account per settlement currency.

For transaction recognition, retain the data finance needs at transaction date, including transaction currency, functional currency, payout currency, exchange-rate basis, and any quote timestamp or lock duration used. Under IAS 21, initial recognition uses the spot rate at the transaction date.

A useful operator test is simple: finance should be able to trace one payment from customer-facing amount to fees, payout currency, and ledger entry without engineering reconstruction. If that trace depends on someone manually checking emails, dashboards, and export files together, the pricing design is not operationally ready yet.

If you are also reviewing regional price presentation, see How to Handle Multi-Currency Pricing for Your SaaS Product.

Build the link lifecycle and payment state machine#

Treat the lifecycle and event model as a financial control, not a UI detail. If you mark a link as paid from a browser redirect or assume a webhook arrives only once, you create duplicate fulfillment, bad balances, or ledger entries finance cannot explain.

Step 1. Define your internal state model first#

Define your internal state machine first, then map each provider into it. States like draft, active, expired, paid, and refunded work well as a normalization layer, but provider states differ: some expose paid, canceled, and expired, while others emphasize checks like "used" or "expired."

Keep link state separate from payment-attempt state. A link can stay active while an attempt is pending_confirmation, confirmed, or failed. That lets you handle delayed confirmations without promoting the whole link to paid too early.

Every inbound provider event and every internal action should map to one state transition with a stored reason code. This separation matters even more in multi-currency flows because customer checkout success and final settlement confidence may not happen at the same moment.

Step 2. Enforce expiry and replay protection before checkout starts#

Enforce replay protection and expiry before checkout starts. Use an opaque link token tied to a server-side record, store expiry, and enforce one-time or bounded-use rules based on your terms.

Provider defaults can help, but your policy still has to match your pricing and FX assumptions. For example, Adyen Pay by Link defaults to 24 hours expiry, allows up to 70 days from creation, and defaults to one successful payment. Checkout.com also checks whether a link is already used or expired before loading the payment page.

Store and enforce fields like expires_at, max_successful_payments, consumed_at, and pricing version so old links fail closed when terms no longer match. This is especially important when prices are based on time-bounded conversion logic. A link that remains technically usable after your pricing assumption has gone stale is an avoidable source of support and reconciliation problems.

Step 3. Make confirmation idempotent and concurrency-safe#

Make confirmation idempotent and concurrency-safe, and do not treat redirects as payment proof. Confirm from verified webhooks, because events can arrive asynchronously and may be delivered more than once.

Stripe explicitly notes duplicate event delivery and possible concurrent fulfillment calls for the same Checkout Session. In practice, protect against that with event deduplication and a concurrency lock on the object you update, such as a session, order, or provider payment reference.

Also verify webhook authenticity before trusting payloads. For Stripe, verify the Stripe-Signature header and construct the event with signature verification. For internal accounting design, a ledger-first posting model can preserve traceability across multi-currency payments, refunds, and adjustments. Cross-currency accounting can require entries in both invoice and payment currencies.

The core principle is simple: the browser is for customer experience, not for financial truth.

Step 4. Design for delayed confirmation and retry-safe reconciliation#

Design for delayed confirmation and retry-safe reconciliation from day one. Keep orders in a holding state such as pending_confirmation until verified confirmation arrives.

Stripe recommends webhook-driven handling for asynchronous confirmations and retries undelivered events for up to three days, so replay-safe processing is required across that full window. Anchor retries and investigations to provider references, not just amount and date. Adyen's 16-character PSP reference is one example of a stable reconciliation key.

Operator checkpoint: if checkout shows success but verified confirmation is missing in your expected window, queue reconciliation by provider reference instead of manually forcing paid.

That single rule prevents a surprising amount of damage. Manual status changes done to "help" a customer often create more work later when the payout, refund, or final settlement amount does not match the forced order state.

Handle FX quotes, settlement, compliance, and tax before launch#

Treat FX as a settlement control, not a display detail. If you do not separate quote type from settlement timing, finance can forecast one outcome and receive another. At the same time, do not treat settlement design as separate from compliance and tax. A fast launch only stays fast if those controls are defined before traffic arrives.

Step 1. Classify every quote before you use it#

Classify every rate as indicative or executable before you use it in pricing or payout logic. Indicative rates are not final and can differ from settlement outcomes.

Enforce provider-defined validity windows for executable rates. Stripe FX quotes support 5 minute, 1 hour, or 24 hour locks, while Goldman Sachs TxB rates are valid for 90 seconds during market hours. Keep the provider quote ID, currency pair, quoted amount, and valid_until, and reject attempts after expiry or invalidation.

Verification checkpoint: on each conversion attempt, confirm the quote is still valid for the exact currency pair and that your record marks it as indicative or executable.

The point is not to overcomplicate pricing. It is to stop teams from talking about a displayed amount and a settled amount as if they were guaranteed to be the same thing.

Step 2. Document corridor economics before launch#

Document corridor economics before launch so settlement behavior is predictable. Keep presentment currency, what the payer pays, separate from settlement currency, what you receive, because differences between them can trigger FX during settlement.

For each currency pair, document:

- payer currency and settlement currency

- where conversion occurs: charge, transfer, or payout

- who absorbs spread or variance if final settlement differs from estimate

- what fee disclosure appears to the payer, if any

- which fields finance uses for forecasting, such as quote ID, expected settlement amount, and provider reference

When FX variance is material, prefer an executable quote tied to the funding step where supported. Stripe Connect can apply an FX quote on transfer creation to confirm the connected account settlement amount.

This is where finance, ops, and product need the same vocabulary. Without it, teams use the word "amount" to describe three different things: the buyer-facing amount, the converted settlement expectation, and the final payout.

Step 3. Compare settlement behavior by provider and corridor#

Do not assume there is one universal finality point.

| Provider example | What to watch | Where conversion or amount confirmation occurs | When to treat amount as dependable |

|---|---|---|---|

| Stripe Connect | Payments FX can occur when presentment and settlement currencies differ | At payments or transfer layer; FX quote can be attached to transfer | After the valid quote is applied and final transfer amount is reported |

| Visa payouts | Quote IDs are pair-specific until expiry, but indicative quotes are not guaranteed at execution | At payout execution using quote ID | After payout execution, not at quote creation |

| Rapyd | Payout currency can differ from sender currency and presentment may be converted into a settlement currency | In the provider's payout and settlement path | After final payout details are available |

| Adyen | Local payout support and local bank account availability can change whether settlement is local or cross-border | In the provider payout configuration for the corridor | After settlement routing is confirmed for that setup |

The lesson is not that one provider is universally better. It is that you need to know which event or record your own team treats as the dependable amount for that corridor.

Step 4. Lock your compliance baseline before go-live#

Lock the compliance baseline before go-live, and write it down in implementation terms rather than provider marketing terms. PCI DSS applies to entities that store, process, or transmit cardholder or sensitive authentication data, and compliance validation expectations can be set by payment brands or your acquirer, not only by internal teams.

For a payment-link launch, write down:

- what cardholder data you touch

- what you do not store

- how webhook authenticity is verified

- how duplicate event delivery is handled

- how exceptions are escalated when a customer-facing success page appears before verified confirmation

This keeps the compliance conversation grounded in the actual implementation rather than in assumptions about what "hosted" means.

Step 5. Set tax boundaries before you scale the corridor list#

Set tax boundaries before you scale the corridor list. For EU launches, write down your VAT assumptions before rollout. VAT is a consumption tax on most goods and services, invoicing is compulsory for most B2B transactions, and cross-border B2C e-commerce VAT rules changed on 1 July 2021.

If you are entering EU consumer markets, decide early whether OSS is part of your model. If it is not settled, keep initial payment-link rollout scoped to narrower corridors until tax treatment is clear.

The practical takeaway is simple: do not let fast payment collection outrun your tax position. Narrower initial coverage is often the safer choice if VAT treatment, invoicing, or consumer-market scope is still unclear.

Set up reconciliation, month-end controls, and recovery playbooks#

A multi-currency link launch is only complete when finance can close the month without reconstructing what happened from screenshots and support tickets. Reconciliation and recovery planning are not back-office extras. They are what make the collection layer reliable.

Build the transaction trail you will actually need#

Start with the four-field comparison from testing and keep it in production data: checkout currency, captured amount, settlement currency, and bank payout amount.

Then retain the fields that explain why those values differ:

- provider payment reference

- link identifier

- payment-attempt status

- quote ID if one exists

- quote timestamp or lock duration if one exists

- transaction currency

- functional currency

- payout currency

- fee amounts and the currency of those fees

- refund status and refund currency if applicable

If you are using a ledger-first posting model, make the ledger entry traceable back to the provider reference and the internal order or invoice. Cross-currency accounting can require entries in both invoice and payment currencies, so the transaction record needs to keep those views separate instead of flattening them into one "amount" field.

Reconcile at the right level, not just at the payout total#

Payout-level matching is useful, but it is not enough by itself. Your system should support payout reconciliation back to underlying payment activity.

That means finance and ops should be able to answer:

- which payments are included in this payout

- what currency each customer saw

- whether any provider conversion occurred

- what fees were applied

- whether a refund or adjustment affected the final amount

- which exceptions still need review

Anchor this work to provider references, not just date and amount. Adyen's 16-character PSP reference is one example of the kind of stable key that helps. If a customer says they paid and the payout report looks short, the provider reference is usually the fastest path to an explanation.

Use a month-end checklist that reflects multi-currency reality#

A practical month-end close for payment links should confirm at least the following:

- all verified paid orders have a corresponding provider payment record

- all payouts are matched to underlying payment activity

- presentment currency and settlement currency differences are visible, not hidden

- refunds and adjustments are posted to the correct records

- expired links and unused links are not treated as collectible cash

- any pending confirmations are still in a holding state and not recognized as settled just because the browser showed success

- finance can trace sample payments from customer-facing amount to fees, payout currency, and ledger entry without engineering reconstruction

The value of the checklist is consistency. It forces teams to review the same risk areas every close instead of rediscovering them only when a discrepancy becomes material.

Common mistakes to catch early#

The most common mistakes here are operational, not technical.

| Mistake | Recovery action |

|---|---|

| Assuming checkout currency equals settlement currency | Compare the checkout currency, captured amount, settlement currency, and bank payout amount on test and live samples. If they diverge, document where conversion is happening and update finance expectations. |

| Launching before webhook handling is ready | Stop treating customer redirects as payment proof. Move fulfillment and ledger actions to verified webhook-driven confirmation. |

| Ignoring link expiry defaults | Review whether the provider default matches your collection cycle. Checkout.com defaults to 24 hours, and Adyen Pay by Link also defaults to 24 hours. If that is too short for your use case, change the policy before links are widely distributed. |

| Allowing silent currency switches | Either show a clear fallback currency or block payment when the preferred currency is unavailable. Do not change the accepted price after the payer has already committed to it. |

Manually forcing paid when confirmation is missing | Queue reconciliation by provider reference instead of overriding state. This keeps the order in a controlled holding state and avoids downstream accounting problems. |

| Failing to keep pricing version and quote timing | Store pricing version, quote details where used, and expiry data so old links fail closed when terms no longer match. |

Recovery playbooks worth defining before launch#

You do not need a huge incident manual, but you do need a few standard responses.

If checkout shows success but no verified confirmation arrives Keep the order in pending_confirmation, investigate by provider reference, and avoid manual fulfillment until the payment status is verified.

If a link is used after pricing assumptions changed Fail closed if your stored pricing version or expiry no longer matches the active terms. Reissue a new link rather than trying to reconcile stale pricing manually.

If payout amount differs from the estimate Check whether the quote was indicative or executable, whether it expired, and whether conversion occurred at charge, transfer, or payout.

If a refund creates an FX difference Make sure finance can identify the original transaction currency, the settlement currency, and the timing difference that created the gain or loss effect.

These playbooks do not eliminate exceptions, but they keep exceptions from turning into uncontrolled accounting decisions.

For a step-by-step walkthrough, see Using an HSBC Expat Multi-Currency Account Without Single-Point Payment Risk.

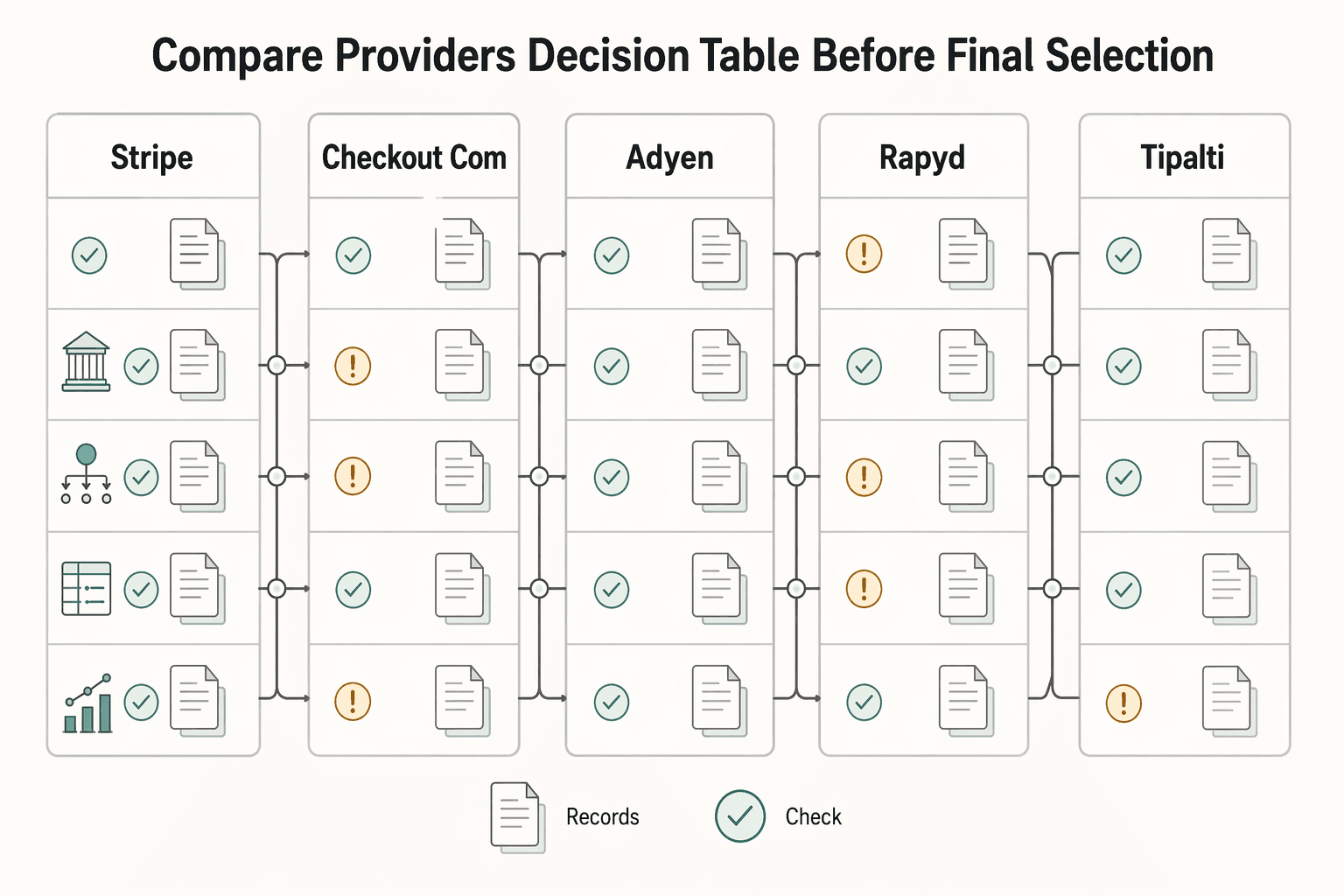

Compare providers with a decision table before final selection#

Do not pick a provider on link creation alone. The faster question is, "Can this provider generate a link?" The better question is, "Can this provider produce the settlement, payout, and reconciliation behavior we actually need?"

Start your comparison around five decision surfaces:

- presentment currency support

- settlement currency support

- link expiry and usage controls

- webhook and event handling expectations

- FX quote and payout behavior

Use a simple decision table to keep the evaluation honest.

| Provider example | What stands out for this use case | What to verify before selection | Best fit when |

|---|---|---|---|

| Stripe | Charge processing coverage of 135+ currencies; FX can occur when presentment and settlement currencies differ; rate locks of 5 minute, 1 hour, and 24 hour; Extended Rate Quotes for 114 local currencies; retries webhooks for up to three days | Supported presentment and settlement currencies for your corridors, separate supported bank account per settlement currency, duplicate event handling, and whether you need FX quotes at payment or transfer layer | You want broad currency coverage and are ready to handle webhook-driven state and explicit FX controls |

| Checkout.com | Payment links expire after 24 hours by default and the provider checks whether a link is already used or expired before loading the payment page | Whether the default expiry matches your collection cycle, how usage rules fit your workflow, and how settlement outcome maps to your finance process | You want fast hosted collection with strict lifecycle controls and are comfortable validating settlement behavior separately |

| Adyen | Pay by Link defaults to 24 hours expiry, allows up to 70 days from creation, and defaults to one successful payment; local payout support and local bank account availability can change whether settlement is local or cross-border | Corridor-level payout routing, local bank account requirements, expiry policy, and use of the 16-character PSP reference in your reconciliation flow | You need explicit control over link lifetime and strong payout-traceability discipline |

| Rapyd | Payout currency can differ from sender currency and presentment may be converted into a settlement currency | Exactly where conversion occurs, which payout currencies are available, and how payout outcomes are reported back into reconciliation | You need broad flexibility but want to document FX and payout behavior carefully before launch |

| Tipalti | Thresholds are variable and failed payments can be marked deferred with notifications to payer and payee | Which thresholds matter in your flow, how deferred payment states should map into your internal state model, and how those exceptions reach ops | You need an explicit exception-handling model and want to account for deferred outcomes in operations |

A few selection rules help:

- If settlement currency flexibility is the priority, compare payout behavior before link UX.

- If longer collection windows matter, compare expiry defaults and configurable limits early.

- If finance is sensitive to duplicate or delayed events, compare webhook retry behavior and your own idempotency readiness.

- If you expect large FX exposure, compare executable-quote support and the step at which the final amount becomes dependable.

You can also use Shopify as a reminder, even if it is not your link provider decision. The key lesson from Shopify's documentation is that selling in multiple currencies does not guarantee multi-currency payout. Keep that lesson in mind when any provider demo makes the front-end experience look simpler than the back-office reality.

Before final selection, run at least one end-to-end test per target corridor and review the same four fields every time: checkout currency, captured amount, settlement currency, and bank payout amount. If a provider cannot make those outcomes clear in testing, the operational cost will usually show up later in finance and support.

Before final sign-off, run your corridor-by-corridor requirements against webhook handling, reconciliation, and control checkpoints in the Gruv docs.

Conclusion#

Multi-currency payment links are useful because they let you launch collection quickly. They become risky when teams mistake that speed for simplicity.

The front-end decision is easy to see: what currency does the customer pay in? The operational decision is the one that matters later: what happens after authorization, where does FX occur, how do funds settle, and can finance reconcile the final payout without manual reconstruction?

If you keep the rollout disciplined, payment links are a strong way to test and scale international collection. The discipline is straightforward:

- verify settlement behavior per corridor

- choose a pricing pattern intentionally

- make webhook confirmation idempotent and authoritative

- document quote validity and payout behavior

- lock compliance and tax assumptions before wider rollout

- build reconciliation around stable provider references and visible currency fields

Treat payment links as a collection shortcut, not a control shortcut. If you do that, you can move quickly without surprising finance, ops, or your customers later. If you want a pre-launch review of your FX, settlement, and compliance operating model, talk to Gruv.

Frequently Asked Questions

Do multi-currency payment links mean I will receive funds in the same currency the customer paid?

No. A payment link can let the customer pay in a supported presentment currency, but that does not prove your payout will happen in that same currency. If charge and settlement currencies differ, provider conversion can apply. Verify the settlement and payout path for each corridor before launch.

Are multi-currency and cross-border the same thing?

No. Multi-currency is about processing in different currencies. Cross-border is about payer and recipient being in different countries. A flow can be one without being the other, and the operational implications are different.

When are payment links the right choice?

They are usually the right choice when speed matters most, engineering time is limited, and you want to test localized collection quickly. They are less suitable when you already know you need deep checkout customization, custom routing control, or more embedded tax logic from the start.

Can I rely on the checkout success page to mark an order as paid?

No. Do not treat redirects as payment proof. Confirm from verified webhooks, handle duplicate delivery safely, and keep orders in a holding state such as pending_confirmation until verified confirmation arrives.

What should I store for reconciliation in a multi-currency setup?

At minimum, keep checkout currency, captured amount, settlement currency, bank payout amount, provider reference, and the fields finance needs for transaction recognition, including transaction currency, functional currency, payout currency, exchange-rate basis, and any quote timestamp or lock duration used.

What happens if the currency quote becomes stale?

That depends on the quote type and validity window. Stripe supports locks for 5 minute, 1 hour, and 24 hour periods, and a lock can expire if the rate moves by more than 3.5%. Goldman Sachs TxB rates are valid for 90 seconds during market hours. Your process should reject stale or invalid quotes and define what happens next.

Do hosted payment links remove PCI DSS responsibilities?

No. PCI DSS applies to entities that store, process, or transmit cardholder or sensitive authentication data, and validation expectations can be set by payment brands or your acquirer. A hosted page can change your implementation scope, but you still need to document what data you touch, what you do not store, and how you verify and process payment events.

What should I verify for EU launches?

Write down your VAT assumptions before rollout. VAT is a consumption tax on most goods and services, invoicing is compulsory for most B2B transactions, and cross-border B2C e-commerce VAT rules changed on 1 July 2021. If you are entering EU consumer markets, decide early whether OSS is part of your model or keep the rollout narrower until tax treatment is clear.

How should refunds be handled in converted payments?

Define refund handling before launch, especially when presentment and settlement currencies can differ. Timing delays can create FX gains or losses, so finance needs the original transaction currency, settlement currency, and the related payment and refund records to explain the final outcome.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- docs.stripe.com/connect/currenciestrusted

- docs.stripe.com/currenciestrusted

- ecb.europa.eu/paym/target/target-professional-use-document...trusted

- imf.org/-/media/files/publications/analytical-notes/...trusted

- sec.gov/news/studies/sox-404_study.pdftrusted

- taxation-customs.ec.europa.eu/taxation/vat/vat-businesses_entrusted

- taxation-customs.ec.europa.eu/taxation/vat/fight-against-vat-fraud/tacklin...trusted

- blog.pcisecuritystandards.org/just-published-pci-dss-v4-0-1external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: