Quick Answer

Form 945 is the annual return for federal income tax withheld from nonpayroll payments, including backup withholding. Platform teams should confirm the payment flow is nonpayroll, identify the payer responsible for withholding, reconcile the annual withheld amount to source records and related Form 1099 or Form W-2G support, and file by January 31 only after totals and payment setup are validated.

What Form 945 covers for platform operators#

Treat Form 945 as an ownership and reconciliation process, not a last-minute filing task. Your team needs to know when it is in scope, who owns the filing decision, what must reconcile before submission, and when to escalate before mistakes turn into penalties, interest, or rework.

Form 945 is the annual return for federal income tax withheld from nonpayroll payments. Backup withholding is payer-side withholding in certain cases, and the rate in the source material is 24% of the gross payment amount. In practice, scope errors tend to show up in both withheld cash and reporting, especially as the January 31 filing deadline approaches.

Before you start#

This guide is for compliance, finance, legal, risk, and payments operations owners handling payer setup, withholding decisions, annual filing, or exceptions. Keep one boundary explicit in your close process: Form 941 is for payroll taxes, and Form 945 is for nonpayroll withholding.

Operating checkpoints#

- Confirm scope first. Verify whether you are handling nonpayroll payments with backup withholding. If the facts indicate Forms 1042/1042-S obligations, do not force that flow into a 945 process.

- Lock ownership early. The payer is responsible for backup withholding compliance. If your structure makes payer responsibility unclear, document the assumption and escalate edge cases before filing season.

- Set a hard reconciliation standard. Do not approve filing unless withheld amounts trace back to source payments and tie to related information returns where applicable. Your minimum document pack is payer identity data, including name, address, and EIN, plus withholding totals and reconciliation support to related 1099 or W-2G reporting.

Later sections cover Form 945, Form 945-A, Form 945-X, and IRS electronic payment channels in more detail. For now, treat unreconciled totals or unclear ownership as hard stops, and confirm e-file readiness early given the lowered threshold of 10 aggregated information returns for filings required on or after January 1, 2024.

Start with scope and filing responsibility#

Scope is the first hard gate. Before anyone opens a return, decide whether the payment flow is nonpayroll and whether the issue is backup withholding. If yes, treat Form 945 as the likely lane and confirm ownership before filing. As a practical control, if the facts point to payroll withholding, route that work to Form 941 instead.

Step 1#

Confirm nonpayroll + backup withholding first. A common miss is applying payroll logic to a nonpayroll withholding case. Require a payroll-versus-nonpayroll tag for each withheld population before year-end close, then test sample payments back to source records. If the payment belongs in Form 1099 reporting and backup withholding, keep it out of the 941 lane.

Step 2#

Assign responsibility based on your actual role in the payment flow. If your entity appears to be the withholding party for that nonpayroll flow, treat Form 945 as potentially in scope and escalate disputed role questions to tax counsel before sign-off. Keep your internal memo explicit on the payer entity, who controls payment, who withholds, and why backup withholding under Internal Revenue Code section 3406 is the lens you are applying.

State your assumptions plainly: principal versus intermediary role, whether funds move through your accounts, and which source documents support the call. IRS information return instructions note that section references are to the Internal Revenue Code unless otherwise noted, so cite the Code section you are relying on.

Step 3#

Route cross-border facts out early instead of forcing them into a domestic backup-withholding queue. Publication 515 treats Forms 1042 and 1042-S reporting obligations as a separate area from Form 1099 reporting and backup withholding. Use that as a routing trigger. If onboarding data, residence address, or tax status suggests a non-U.S. path, pause the 945 assumption and review 1042/1042-S handling first. For digital-asset broker edge cases, Notice 2025-3 provides limited penalty relief tied to specific years and conditions, including TIN Matching checkpoints in certain 2028 scenarios.

Related reading: IRS B-Notice Procedures for Platform Contractor TIN Mismatches.

Gather the minimum data and documents before you touch IRS Form 945#

Do not start drafting until you can answer three questions quickly: what was withheld, which payer it belongs to, and what support proves the number. The IRS excerpts here do not make each internal control step mandatory, so use this as a practical pre-filing checklist.

| Artifact | Use | Detail |

|---|---|---|

| Annual backup-withholding totals | Build the withholding population | Pull totals for each nonpayroll stream that can fall under section 3406 and tie each total to a payer entity plus a support population |

| Payer identity data | Show which payer the withholding belongs to | name, address, and EIN |

| Filing credentials | Confirm filing setup before filing week | EFINs, ETINs, and passwords |

| Reconciliation support | Defend the return total | trace workpaper totals back to underlying withholding records and the annual support population |

| IRS TIN Matching response | Retain payee identity validation evidence when used | showing the name and TIN match |

| Notice 2025-3 support | Keep narrow digital-asset evidence where relevant | good-faith support and, where relevant, records on whether withheld digital assets were immediately liquidated for cash |

Step 1 Pull the annual withholding population from reporting families#

Build the withholding population from the same IRS instruction set that covers Forms 1099 and W-2G and includes a dedicated backup withholding section. Pull annual backup-withholding totals for each nonpayroll stream that can fall under section 3406, and tie each total to a payer entity plus a support population, not just a ledger code.

Reuse your information-return inventory where possible. With the aggregated e-file threshold at 10 returns, effective for returns required on or after January 1, 2024, that inventory can help you catch smaller nonpayroll streams that still produced withheld tax.

Step 2 Confirm payer records and filing credentials before filing week#

Lock down payer identity records and filing credentials before the return is ready. If you file through an authorized IRS e-file provider, Publication 4163 identifies the core credential artifacts: EFINs, ETINs, and passwords.

Treat access testing as an early control, not a filing-day task. If your team also uses IRIS for information returns, treat that as a separate workflow and confirm this annual withholding return setup independently.

Step 3 Reconcile source events to the finance total you will defend#

Use a reconciliation method you can defend quickly. Even though the excerpts here do not prescribe a specific method, you should be ready to trace return workpaper totals back to underlying withholding records and the annual support population.

Check for timing mismatches before filing week. Late adjustments, reversals, or manual journals can leave logs and ledger totals individually plausible but still out of alignment.

Step 4 Build one pre-filing evidence packet for internal control#

Create a single packet with reconciliation outputs plus payer and credential records you already maintain. Keep this framed as an internal control file, not as a claim that the IRS requires these exact artifacts for this section.

If you relied on payee identity validation, retain the IRS TIN Matching response showing the name and TIN match. In the narrow digital-asset context discussed in Notice 2025-3, keep any related good-faith support and, where relevant, records on whether withheld digital assets were immediately liquidated for cash.

For a step-by-step walkthrough, see IRS Form 1042-S for Platforms: How to Report US-Source Income Paid to Foreign Contractors.

Map your payment flows to the right IRS form family#

Form selection should be an explicit control, not a memory test at close. Use one routing matrix with named owners and escalation rules so payroll-linked, cross-border, and foreign-asset questions are separated before filing decisions are made.

A useful anchor here is Publication 515. It separates "Forms 1042 and 1042-S Reporting Obligations" from "Form 1099 reporting and backup withholding." Treat those as distinct reporting families in your process, and document where additional authority is needed for final form routing.

Step 1 Classify by tax role and withholding trigger first#

Start with two questions: what triggered the tax event, and what tax role your entity played. If a flow appears in your Form 1099 and backup-withholding population, keep it in your nonpayroll withholding review lane for this guide. If the facts indicate nonresident withholding, escalate to your 1042/1042-S owners for review instead of resolving it inside the domestic backup-withholding queue.

If payroll already owns the payment flow, keep payroll ownership explicit in the file. The excerpts here do not establish detailed Form 941 boundary rules, so documented owner sign-off is the control.

Step 2 Use a compact decision matrix so close teams stop guessing#

| Payment flow or signal | Start lane | Why | Verify |

|---|---|---|---|

| Nonpayroll payment in Form 1099 + backup-withholding population | Nonpayroll withholding review lane | Publication 515 has a distinct "Form 1099 reporting and backup withholding" section; detailed Form 945 boundary rules are not established in the provided excerpts | Tie withheld amount to payer entity, support population, and document final form determination support |

| Cross-border or nonresident withholding pattern | 1042/1042-S review lane | Publication 515 separately addresses "Forms 1042 and 1042-S Reporting Obligations"; detailed routing rules are not established in the provided excerpts | Collect residency and withholding-classification support before close |

| Payment flow already owned by payroll tax operations | Payroll or employment tax review lane | Detailed Form 941 routing is not established in the provided excerpts | Keep written payroll-owner confirmation with workpapers |

| Settlement or payout feed used for Form 1099-K operations | Source-data review only | Use feed data to identify candidate populations, not as a standalone final form decision | Confirm whether feed reflects gross payments only or actual withholding events |

| Foreign asset or offshore account question | Separate Form 8938 or FBAR review | These are separate filing obligations | Open a separate case and keep it out of the withholding return packet |

Step 3 Route cross-border and foreign-asset issues to separate review early#

For nonresident withholding signals, hand off early to the 1042/1042-S lane for dedicated review. If your team needs detailed handling, use IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

Keep foreign-asset reporting and other international disclosure questions separate from the Form 945 workstream. If a payment flow raises offshore-account, treaty, or foreign-information-reporting questions, open a dedicated review lane rather than mixing those issues into the backup withholding close packet.

Step 4 Write exclusions into the matrix so scope does not drift#

Write exclusions directly into the matrix and reviewer notes. A nonpayroll withholding workstream should not absorb every international or account-related issue.

Write exclusions directly into the matrix and keep them narrow. The goal is not to solve every international tax question inside the Form 945 file. Document the handoff, name the owner, and keep the withholding packet focused on backup withholding triggers, deposit operations, and filing support.

If you want a deeper dive, read Non-Resident Withholding on Contractor Payments: Platform Guide to the 30% Rule and Treaty Reductions.

Set deposit operations before year-end close#

Set payment execution controls before close, but treat deposit rails and timing rules as unverified until treasury, tax, and current IRS instructions confirm them in writing.

Prerequisite: confirm the payer entity, funding account, and in-scope backup-withholding liabilities before payment setup. If those inputs are still moving, close-week payment work becomes guesswork.

Step 1 Validate your planned payment channel#

If your team plans to use a specific payment channel, for example EFTPS, test it before the final close window. Confirm access, roles, bank authority, and that the exact filing entity can schedule and release payments.

Keep fallback assumptions explicit. Current IRS Form 945 materials identify EFTPS, IRS Direct Pay, and an IRS business tax account as standard electronic payment options. Treat any other rail or treasury workaround as an exception that needs current-instruction validation before you rely on it in close.

Step 2 Set internal cutoffs and exception handling#

The provided IRS excerpts do not establish Form 945 deposit cutoffs or same-day rules, so set internal deadlines and approval paths in advance. Name who prepares, approves, and releases payments, plus who is authorized if primary approvers are unavailable.

Document a short same-day escalation path for late liabilities, access failures, or bank changes. If payment cannot be completed through a tested channel by your internal cutoff, escalate immediately to compliance and treasury leadership.

Step 3 Align on what IRS guidance supports#

Use supported guidance as your control anchor. The 2025 General Instructions for Certain Information Returns include dedicated Backup Withholding and Penalties sections. That supports treating this as a penalty-sensitive control area, but it does not by itself establish a specific Form 945 deposit rail.

Apply the same standard to Executive Order 14247. The excerpts for this guide do not establish a requirement from that order for this process. If it is cited as authority, require counsel-backed analysis and keep it separate from operating instructions.

Step 4 Create a payment-proof checkpoint that survives review#

For internal control, make traceability mandatory for each scheduled deposit. Keep one record that ties the payment event to the liability it was intended to satisfy, including:

| Field | Keep with payment proof |

|---|---|

| Payer entity and EIN | Tie the payment event to the liability it was intended to satisfy |

| Internal liability date or tax period | Keep the liability reference |

| Deposit amount | Record the amount |

| Payment channel | Record the channel used |

| Release date and time | Keep timing of the release |

| Approver | Record who approved the payment |

| Confirmation number or bank trace reference | Keep the confirmation or trace |

| Source liability report or ledger reference | Link payment proof back to the exact liability |

Your review test should work both ways: liability to payment proof, and payment proof back to the exact liability. If that link fails, reconciliation risk rises and misapplied payments can appear as missed deposits until resolved manually.

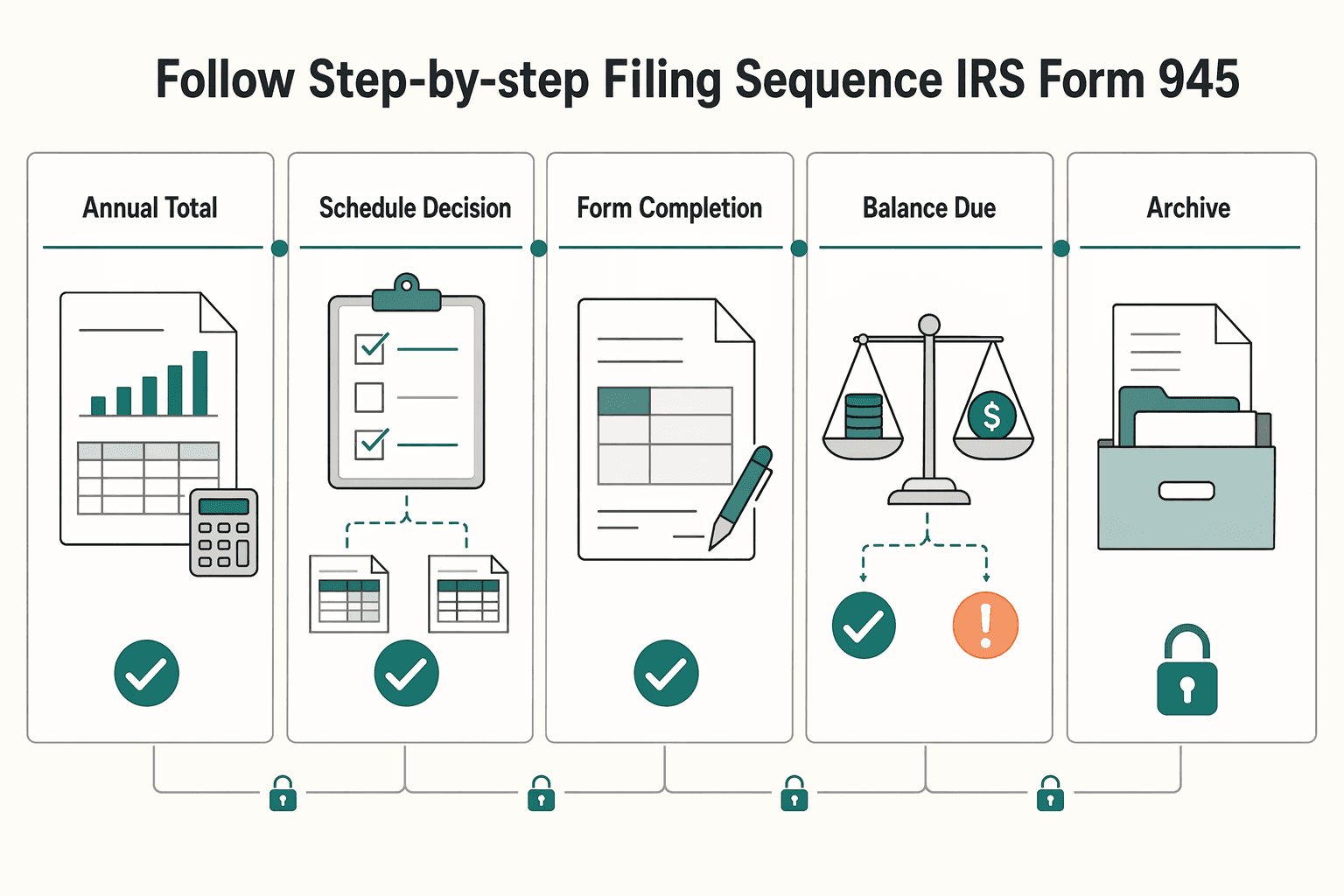

Follow a step-by-step filing sequence in IRS Form 945#

Keep the filing sequence rigid. Do not submit until your annual withholding total and support files reconcile.

| Stage | Action | Check |

|---|---|---|

| Annual total | Freeze one full-year withheld federal income tax total with payer name, address, EIN, and source support | If the annual amount does not trace from source records to the Form 945 workpaper, stop and correct it before drafting the return |

| Schedule decision | Make an explicit schedule decision and document it in the filing packet | If your process involves Form 945-A or monthly liability entries on Form 945, confirm current criteria in IRS instructions and capture tax-owner confirmation |

| Form completion | Complete Form 945 only after totals and schedule logic are already validated | If the withholding amount does not reconcile to Form 1099 and Form W-2G support files, do not file |

| Balance due | Lock the payment method before release and confirm it against current IRS instructions and internal policy | If a voucher-and-check option is proposed, require confirmation against current Form 945-V instructions before using it |

| Archive | Store the filed return, submission receipt or acceptance acknowledgment, payment proof, reconciliation workpapers, and reviewer approvals in one audit archive | The archive should let a reviewer confirm what was filed and what support existed at filing time |

Form 945 is the annual return for withheld federal income tax on nonpayroll payments. The control risk is in the handoffs, so lock each handoff before moving to the next step.

Step 1 Finalize the annual withholding total first#

Freeze the filing population and lock one full-year withheld federal income tax total. Build a base packet with payer name, address, EIN, and the annual withheld amount tied to source records.

Use a fixed extraction date and clear ownership for the compiled figure. If the annual amount does not trace from source records to the Form 945 workpaper, stop and correct it before drafting the return.

Step 2 Validate the liability schedule path before completing the form#

Make an explicit schedule decision before form completion and document it in the filing packet. Do not let preparers infer this from prior-year habit.

If your process involves Form 945-A or monthly liability entries on Form 945, confirm the current criteria in IRS instructions and capture tax-owner confirmation.

Step 3 Complete Form 945 only after support files reconcile#

Complete Form 945 only after totals and schedule logic are already validated. Treat the form as output, not as your reconciliation workspace.

Set a hard stop before submission: if the withholding amount does not reconcile to Form 1099 and Form W-2G support files, do not file. Also verify that you are filing Form 945, not Form 941, and that payer identity fields and EIN match supporting records.

Step 4 Decide the payment method before submission if a balance is due#

If a balance is due, lock the payment method before release and confirm the method against current IRS instructions and internal policy.

If a voucher-and-check option is proposed, require confirmation against current Form 945-V instructions before using it. If payment ownership or method is unresolved, escalate before filing.

Step 5 Archive post-filing proof in one place#

After submission, store the filed return, submission receipt or acceptance acknowledgment, payment proof, reconciliation workpapers, and reviewer approvals in one audit archive.

Your archive should let a reviewer confirm what was filed and what support existed at filing time without reassembling evidence. Treat this archive as part of filing completion, since late or inaccurate filing can lead to penalties and interest.

Before final sign-off, align your internal control checklist with implementation patterns in the Gruv docs.

Assign owners and escalation triggers across Compliance Finance Legal and Ops#

Once the return packet reconciles, ownership is the next control question. Assign one accountable owner for the filing position, a separate owner for deposit execution, and a correction owner if a later issue needs a correction workflow.

Step 1 Assign one accountable owner to each artifact#

Treat this as an internal policy choice, not an IRS-prescribed org chart. Each work item should have one person answerable for sign-off.

| Work item | Primary owner | Key reviewers or contributors | Verification before sign-off |

|---|---|---|---|

| Annual return package and filing packet | Compliance or Tax | Finance for totals, Legal for edge-case classification | Withheld amounts tie to source support, and the chosen form family is documented |

| Deposit execution and payment records | Finance or Treasury Ops | Compliance confirms approved amount and due status | A named executor and backup are assigned before filing release, and payment proof is retained |

| Correction assessment and correction file | Compliance or Tax | Legal if scope or classification changed, Finance if cash impact changed | Error memo states what changed, why, and what supporting records were updated |

| Related information returns and recipient statements | Reporting Ops | Compliance or Tax | If backup withholding applied, the appropriate Form 1099 or Form W-2G and recipient statement are accounted for |

A practical check is whether each owner can produce their evidence without cross-team reconstruction.

Step 2 Define escalation triggers before filing week#

Set escalation gates at form-family boundaries before drafting. Publication 515 presents Forms 1042/1042-S obligations separately from Form 1099 reporting and backup withholding, so mixed flows need an explicit routing decision.

Escalate when any of these are true:

- No one can clearly state which entity is the payer or withholding-role holder for the payment flow.

- The same payout population includes both domestic backup-withholding cases and nonresident-withholding cases.

- Ops routed payments to a Form 1099 lane, but legal or tax believes Form 1042-S treatment may apply.

- A reporting-channel dependency changes, especially for nonresident reporting, where IRIS is available beginning January 1, 2026 and FIRE is set to retire for tax year 2026, affecting filing season 2027.

Keep two checkpoints explicit: if backup withholding was taken, the appropriate Form 1099 or Form W-2G is required, and the recipient statement path must be owned; and for information returns required to be filed on or after January 1, 2024, the e-file threshold is 10 in the aggregate.

Step 3 Use counsel escalation when classification is disputed#

If legal classification is disputed, treat that as an internal escalation trigger and consider pausing final sign-off assumptions until tax counsel confirms the treatment. This is a policy control meant to prevent inconsistent routing across teams.

A common failure mode is split filing logic: one team routes a payout to Form 1099 backup-withholding reporting while another routes a similar payout to 1042-S treatment. Require a short written decision memo that names the payment type, entity role, chosen form family, and approvers, then file only after that memo is in the archive.

Related: 1099-K Reporting Threshold Changes: What Platform Operators Need to Know After the IRS Delay.

Build an evidence pack that survives audit questions#

Your evidence pack should let a reviewer answer, from one filing-year folder alone, what was filed, which relief conditions were met, and what changed.

Step 1 Store one filing-year packet and freeze the tie-out#

Build one packet that shows how the backup-withholding reporting outcome was produced and reviewed. Include the records used in the calculation, the final information return and associated payee statement versions, and the sign-off record.

A second reviewer should be able to start from the underlying records and reach the same annual amount without relying on hidden logic from the preparer. Keep the calculation version that fed the filed records, not only later cleaned-up versions.

Step 2 Tie filing evidence to scope and threshold rules#

Keep filing-channel evidence and aggregate count support with this packet. For information returns required to be filed on or after January 1, 2024, the e-file threshold is 10 in the aggregate.

If you are relying on transitional relief for certain brokers under Notice 2025-3, retain evidence of the good-faith effort to file the appropriate information return and furnish the associated payee statement accurately.

Step 3 Preserve relief-path artifacts and reviewer reasoning#

If anything changes after filing, archive the correction record as carefully as the original filing. Keep an issue memo describing what changed, affected amounts, issue date, and reviewer notes showing who approved the correction path.

Do not rely on chat notes alone. The file should show before amount, after amount, and the reason for change.

For digital-asset edge cases only, keep the specific evidence required by the relief path you are using. If relying on Notice 2025-3 conditions for certain broker reporting, retain the IRS TIN Matching Program submission and IRS response showing a payee name and TIN match. If relying on value-decline backup-withholding relief, retain proof that the withheld digital assets were immediately liquidated for cash. Document the applicable relief window in the packet, for example filings in 2028 for 2027 sales, and conditions that apply only before January 1, 2029 or on or before December 31, 2028, as relevant.

Fix errors fast with Form 945-X and transcript checks#

When you find a material error, move it into a formal correction record immediately so the filing, change, and payment trail stays intact.

Step 1 Open a correction file as soon as the error is confirmed#

Create one correction packet for the filing year and preserve the original numbers before workpapers change. A reviewer should be able to see, in one place, the filed amount, corrected amount, variance, and affected records.

Include the original IRS Form 945 workpaper, any correction-form draft, the issue memo, and the impacted payees, transactions, or liability periods. The provided excerpts do not confirm specific Form 945-X filing mechanics, so verify those separately against current IRS form instructions. If the issue involves Notice 2025-3 transitional relief for digital-asset sales, keep the exact support for that position, such as an IRS TIN Matching Program response confirming a payee name and TIN match, or records showing immediate liquidation for cash when that condition is required.

Step 2 Preserve electronic filing evidence when your channel uses MeF#

If your authorized provider files through Modernized e-File (MeF), keep the validation and submission evidence aligned with IRS Publication 4163 checkpoints, including "3.2 Validating Your Return" and "2.7 Submitting a Timely-Filed Electronic Tax Return."

Do not keep only a final PDF. Retain the validation results, acknowledgments, and any reject, correction, or acceptance trail that exists.

Step 3 Use transcript checks as an external verification control#

The provided excerpts do not establish a required IRS Business Tax Account transcript re-check cadence after a correction. If transcript review is part of your controls, use it as an additional confirmation step, not a replacement for your ledger and workpapers.

Step 4 Document root cause before closing the issue#

Finish with a short postmortem that records root cause, date found, impacted records, control gap, and fix owner. If recurrence risk exists at the deposit, form-prep, or review stage, name it so the next cycle changes the control, not just the number.

Avoid the mistakes that create penalties and rework#

Routing and control failures can create avoidable rework. Keep this practical: classify correctly, verify your numbers before filing, and escalate mixed or unclear cases instead of forcing them through one path.

Step 1 Add a form-selection checkpoint before close#

Start with classification, not habit. In the cited IRS guidance, if required SSN or EIN information was not obtained before payment, backup withholding applies, 24 percent is withheld, and that withholding is reported on Form 945.

Use Form W-9 as the upstream control point. The same guidance says to request Form W-9 before work begins, so your close checkpoint should confirm whether TIN certification was collected before payment and whether the record was routed to the correct reporting track.

When populations are mixed, keep boundaries explicit. Publication 515 separates Forms 1042 and 1042-S Reporting Obligations from Form 1099 reporting and backup withholding, so unclear cases should be escalated rather than forced into a single form path.

Step 2 Require a documented tie-out before approval#

Before filing, make sure your support is reproducible. Your approval packet should let a reviewer trace the proposed Form 945 amount back to source records, identify exceptions, and see who owns each open item.

This is a control choice, not a formatting exercise. A simple, documented tie-out is enough if it clearly shows what was included, what was excluded, and why.

Step 3 Keep filing-lane readiness separate from classification quality#

Do not treat filing-channel readiness as proof that backup-withholding classification is correct. They are separate controls and should be reviewed separately.

For your Form 1099 lane, IRS general instructions say the e-file threshold is 10 aggregated information returns for filings required on or after January 1, 2024, and IRIS is available for 2022 and later tax years. Those facts matter for information-return operations, but they do not replace correct backup-withholding routing and Form 945 support.

Step 4 Keep controls targeted and escalate edge cases#

Apply backup-withholding controls where the trigger is clear: missing required TIN data before payment. Keep that review logic targeted so the exceptions that need action are easier to spot.

If a case appears to belong in a different withholding or reporting framework, escalate it to the appropriate track instead of stretching Form 945 logic to fit.

Close the year with a copy and paste control checklist#

Use a literal close checklist, not a memory test. For year-end Form 945 work, the highest-value control is proving scope, tie-out, and evidence before submission.

- Confirm scope against your approved tax memo.

Validate that the population going into Form 945 matches the population your legal or tax review assigned to this filing path and backup withholding treatment. The 2025 general instructions include an "N. Backup Withholding" section, so your workpapers should point to that topic and show why included payments fit. If treatment is still disputed, stop and escalate instead of forcing an ops decision.

- Document boundaries with related filing streams, including Form 1099-K context.

Treat this as a documentation control, not a judgment call at filing time. Add a one-page boundary memo stating which populations were excluded from the Form 945 total and why, based on your approved tax position. For Form 1099-K, keep the threshold context in view: more than $2,500 in 2025, and more than $600 in calendar year 2026 and after.

- Reconcile annual withholding totals and keep the math traceable.

Tie the draft annual withholding total to your ledger, then to the supporting Form 1099 and Form W-2G data used by reporting. A high-level total match is not enough. You should be able to trace sampled amounts from transaction record to ledger bucket to recipient reporting file. A clean ledger tie-out without 1099 or W-2G support can still leave an audit gap.

- Archive payment evidence you actually have, with mapping to liabilities.

If your team used a payment channel for remittance, do not rely on a bank statement alone. Save the confirmation page, confirmation number, date, amount, and internal approval record, then map each item back to the liability record in your workpapers. IRS exam guidance expects workpapers to support conclusions, and missing payment artifacts increase review risk.

- Require cross-functional sign-off before filing.

Compliance should sign the filing position, finance should sign reconciled totals and payment evidence, and legal should sign any boundary issue that is not obvious. Treat unresolved comments as blockers. The general instructions include a penalties section, and IRS notice guidance emphasizes timeliness, so late cleanup is a real operational risk.

- Submit, then archive filing proof in one place.

Use current Form 945 instructions to confirm the allowed submission method and what qualifies as filing proof for your case. Do not treat IRIS as proof that Form 945 itself was filed. IRIS is an e-file portal for information returns. If your team plans to pull IRS account records, verify access and record availability first, then archive what was actually available.

- If an error appears, correct quickly and log root cause.

Prepare a corrected filing using current IRS correction instructions, and confirm the available filing channel before promising timing. Keep the original filing, corrected figures, and a short root-cause note in one evidence pack. That note is what helps prevent the same failure from repeating next close.

If your Form 945 process depends on controlled disbursements and traceable payment evidence, evaluate Gruv Payouts.

Frequently Asked Questions

What is IRS Form 945 used for, and when does Backup Withholding belong on it?

Form 945 is the annual return for federal income tax withheld from nonpayroll payments. backup withholding belongs in the Form 945 lane when the payment flow is nonpayroll and falls within Form 1099 reporting and backup withholding rather than payroll or 1042 or 1042-S reporting. Confirm the current Form 945 instructions before making the final filing decision.

Does a platform operator file IRS Form 945, or only the direct payer entity?

The filing responsibility turns on which entity is the payer or withholding-role holder in the payment flow. If contracts, funds flow, or tax role are unclear, do not treat it as an ops assumption. Pause and get tax counsel or internal legal sign-off before filing.

How is IRS Form 945 different from Form 941 in day-to-day operations?

Form 941 is for payroll taxes, while Form 945 is for nonpayroll withholding. In day-to-day operations, teams should tag each withheld population as payroll or nonpayroll before year-end close. Keep nonpayroll backup-withholding cases out of the 941 lane.

When is Form 945-A needed, and when are monthly liability entries enough?

This guide does not establish the trigger. If your process involves Form 945-A or monthly liability entries on Form 945, confirm the current criteria in the IRS instructions and capture tax-owner confirmation before submission.

How should deposits be made for IRS Form 945 liabilities using EFTPS, IRS Direct Pay, or FTCS?

Federal tax deposits must be made by electronic funds transfer. Current Form 945 materials list EFTPS, IRS Direct Pay, or an IRS business tax account as the standard channels, so test the exact channel your entity will use before filing week. If your treasury team wants a different rail or a third-party arrangement, treat it as an exception that needs current-instruction validation and written owner approval.

What is the right way to correct a previously filed return with Form 945-X?

Open a formal correction file as soon as the error is confirmed and preserve the originally filed numbers before workpapers change. Keep the original Form 945 workpaper, the correction draft, the issue memo, and a clear before-and-after variance record in one packet. Verify Form 945-X mechanics, timing, and filing channel against current IRS instructions rather than relying on another form by analogy.

What changed recently in Form 945 operations, including electronic payments, direct deposit refunds, and transcript access?

This guide does not confirm Form 945-specific changes in electronic payments, direct deposit refunds, or transcript access. The supported nearby update is for information returns: the e-file threshold is 10 aggregated returns for filings required on or after January 1, 2024, and IRIS is available for 2022 and later tax years. Use that as a boundary check, not proof that Form 945 operations changed the same way.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: