Quick Answer

Build one country-by-vertical decision table before launch, then validate money movement before scaling. Separate PRM/CRM relationship signals from payment-system truth, and require evidence such as status screenshots, named exception owners, and reconciliation checks. Keep can-launch and can-scale distinct, and pause expansion when partner-facing statuses diverge from webhook or bank events.

Why Payment Execution Matters to Partners#

Expansion decisions tend to hold up better when you evaluate top-line demand alongside three execution realities: your Partner Experience Platform, your Payment Experience (PX), and the quality of the data behind both. If you optimize only for demand, you can enter markets that look promising on paper but still lose partner trust once operations begin.

Partner experience is operational, not cosmetic. It shows up in your ability to build and keep long-term partner relationships, and payment execution is often where that relationship gets tested first. When onboarding drags, disbursement status is unclear, or payment methods do not match local business behavior, confidence can drop quickly.

Founders and operators still have to choose countries, verticals, and rollout order before they have full certainty. That is why market-specific payment constraints need real weight in planning. Cross-border payments are still shaped by the same pressure points emphasized in the G20 roadmap era: speed, transparency, access, and cost. Weakness in any one of those can damage trust early.

A common failure pattern is that demand signals look strong, signups rise, and teams assume the market is ready. Then live payment flows can expose settlement delays, manual exception handling, or unclear money states. Support load can rise, channel teams patch gaps by hand, and reported launch success can drift away from partner reality.

Payment-flow design changes commercial outcomes too, not just interface feel. Stripe reported that dynamically surfacing at least one additional relevant payment method was associated with an average 12% revenue increase and 7.4% conversion-rate increase. Method mix can materially improve or suppress performance in the same market.

Data quality is the control layer for all of this. Whether you use a CDP or a simpler stack, the goal is the same: make operating decisions from clean, reconciled records. Before a go or no-go call, verify that partner-facing statuses match internal payment events and that onboarding and disbursement metrics are trustworthy. IBM reports that 43% of chief operations officers cite data quality issues as their top data priority. That fits the expansion reality that weak data can make good markets look bad and bad markets look good.

This article follows a decision sequence:

- Assess market constraints first.

- Choose payment-flow design to fit those constraints.

- Measure partner impact in real operations.

- Validate conclusions against reliable data.

- Make the go or no-go decision.

Related: Airline Delay Compensation Payments: How Aviation Platforms Disburse Refunds at Scale.

Define the terms before you compare markets#

Market comparisons only hold up if you separate partner management, payment execution, and the data layer before you score any country. Otherwise, strong relationship tooling can hide weak money movement, and clean-looking dashboards can hide unreliable status data.

| Term | What it is | Details |

|---|---|---|

| Partner Experience Platform | Partner lifecycle layer | Onboarding, training, deal registration, co-marketing, and incentives |

| Payment Experience (PX) | How partners experience each money step | Checkout and payment onboarding through Payouts; onboarding can include document upload and verification |

| PRM and CRM | Systems for partner relationships, sales context, and unified profile/history views | Not by themselves the authoritative source for money-state execution |

| Data layer | Real-Time CDP and Adobe Experience Platform-style enrichment | Connects first-party profiles with partner-provided attributes across sources |

- Partner Experience Platform: the partner lifecycle layer, including activities such as onboarding, training, deal registration, co-marketing, and incentives.

- Payment Experience (PX): how partners experience each money step, from Checkout and payment onboarding through Payouts. In practice, payment onboarding can include document upload and verification.

- PRM and CRM: systems for partner relationships, sales context, and unified profile/history views. They are not, by themselves, the authoritative source for money-state execution.

- Data layer: Real-Time CDP and Adobe Experience Platform-style enrichment can connect first-party profiles with partner-provided attributes across sources.

Use one rule for the rest of this article: if a claim cannot be tied to observable partner behavior and payment outcomes, treat it as opinion.

For a step-by-step walkthrough, see Which Contractor Payment Experience NPS Metrics Actually Predict Retention.

Where partner trust breaks first in cross-border expansion#

Trust often breaks at the first point where a partner cannot move forward or cannot tell what is happening with their money. Once you separate lifecycle UX from money execution, three common failure points tend to show up early: onboarding in the Partner Portal, visibility during settlement, and exception handling when payouts fail.

| Failure point | What breaks trust | What to verify |

|---|---|---|

| Slow onboarding in the Partner Portal | Repeated document requests and partners are not ready to receive funds | Track first-pass activation success for disbursements and document resubmission rates |

| Unclear status during settlement | Partners cannot tell where a delay sits | Reconcile partner-facing status with internal payment events and processor or bank events |

| Weak exception handling when payouts fail | The recovery path is not explicit or practical | Tell partners what failed, whether the external account involved is disabled, what is needed to remediate, and who owns the next step |

Extu, Medallia, and Cisco PXP all reinforce the value of partner experience and simplification. That framing is useful, but it is not enough on its own for market entry. You still need to verify the failure path: what breaks, who can see it, and how quickly it can be resolved.

Slow onboarding in the Partner Portal#

The first trust test is not whether a portal exists. It is whether partners can move from invite to approval without repeated document requests and become ready to receive funds.

Salesforce describes partner portals as a way to share pertinent CRM data with partner resellers. In cross-border onboarding, Stripe notes why this can break: fast onboarding is attractive, but hard for marketplaces because compliance requirements vary by geography. For launch readiness, track first-pass activation success for disbursements and document resubmission rates, not just whether the portal was completed.

If one market shows frequent resubmissions, narrow the initial segment so your team handles a smaller set of entity, bank, and verification patterns first.

Unclear status during settlement#

Settlement-status opacity can break trust quickly because partners cannot tell where a delay sits.

BIS notes that even with faster rails, cross-border speed still varies significantly across end-to-end routes. AWS's January 6th, 2026 collections-visibility launch shows the operational impact. Sellers on monthly disbursement had previously waited up to 30 days to understand collection status, and AWS links better visibility to fewer unnecessary payment-status follow-ups.

Your check here is straightforward: reconcile partner-facing status with internal payment events and processor or bank events. If those views diverge, partners can stop trusting the status they see.

Weak exception handling when payouts fail#

When payouts fail, trust depends on the recovery path being explicit and practical. Stripe defines a concrete failure event (payout.failed) and notes that a failed payout can disable the external account involved until corrected.

Your exception handling should tell partners what failed, whether the destination account is disabled, what is needed to remediate, and who owns the next step.

Retention risk also shows up in market signals. PayPal warns that delayed payouts, limited payout options, and cumbersome processes can increase attrition. Visa reports 68% of surveyed sellers missed or delayed a payment obligation due to delayed marketplace payouts in the last year. For expansion planning, treat unclear recovery paths as a launch risk.

Score countries and verticals with one operator decision table#

Use one decision table for every market choice, and require evidence across payment steps, disbursement behavior, compliance gates, and staffing impact before you commit GTM resources. This keeps strong demand narratives from outrunning operating reality.

A strong partner platform or portal can still mask payment risk. Score by country plus vertical or use case, not by broad region, because conditions differ across wholesale, retail, and remittance-like flows. The Financial Stability Board reports that global policy progress has not yet produced equivalent end-user outcomes, so pilot success in one corridor is not enough to assume scale readiness.

Build rows around actual money movement#

Build rows around the exact launch motion, not geography alone. For example, "Germany reseller disbursements in euro" and "U.S. contractor disbursements" should be separate rows because rail behavior, document gates, and exception patterns differ.

| Country + vertical | Required payment steps | Expected disbursement behavior | Compliance + Document management gates | Evidence before launch | Can launch | Can scale |

|---|---|---|---|---|---|---|

| Euro area B2B reseller program | Partner onboarding, bank account capture, payout-status view, support contact path | Instant Payments Regulation obligations apply to euro credit transfers. Receiving deadlines apply from 9 January 2025 and sending from 9 October 2025 in euro-area member states. Instant-transfer charges cannot exceed non-instant charges. | Compliance and document requirements vary by provider and market. Track document resubmissions by entity type. | Status acknowledgements where available, sample partner-facing status screens, documented investigation path, and SLA language that avoids universal real-time promises. | Yes, if rails are stable and the initial entity pattern is narrow. | Yes, only after consistent status visibility and low manual chasing across multiple cycles. |

| United States contractor or affiliate disbursements | Account opening, identity verification, payout preference, payout-status tracking, exception intake | FedNow is designed for 24x7x365 processing and settlement is final. If ACH is used, monitor return quality and avoid reversal assumptions on final-settlement rails. | CIP requires risk-based identity verification before account opening, including minimum customer information. | Proof of CIP completeness, rail-specific exception targets, near-real-time status acknowledgements where supported, and ACH unauthorized return-rate monitoring under 0.5% over the preceding 60 days or two calendar months. | Yes, if identity collection is complete and reliability is proven on the selected rail. | Yes, only after final-settlement exception handling and ACH return quality remain stable as volume grows. |

| UK marketplace or referral partner program | Onboarding, transaction detail display, payout notices, complaint and investigation channel | Do not assume instant-style visibility. Partner communications need transaction references, dates, amounts, charges, and exchange-rate detail where relevant. | Requirements vary by market and entity, but complaint handling needs clear ownership and staffing. | Sample partner communications, status-detail screens, and complaint-response language aligned to the common expectation of a response within 15 business days in most cases. | Yes, if transaction-level visibility is already present in partner communications. | Yes, only after complaint volume, manual lookups, and investigation times stay within team capacity. |

Decision rules that keep pilots honest#

A pilot should prove controlled readiness. It should not get mistaken for evidence that the market is ready to scale.

- If local disbursement reliability is uncertain, consider delaying GTM launch until reliability evidence improves.

- If onboarding friction is high but rail behavior is stable, launch with a narrower segment (for example, fewer entity types, bank patterns, or one corridor).

- If both onboarding and recovery are weak, mark the market as no-go for now.

- Separate

can launchfromcan scaleso controlled pilot readiness is not confused with durable economics.

This split matters because cross-border outcomes remain uneven. The FSB reports only slight KPI improvement globally, flags sticky costs, and sets most quantitative targets to end-2027.

What to verify before trusting the score#

Before you trust any score, require one non-negotiable checkpoint: partner-facing payment status must reconcile with internal payment events and rail or bank acknowledgements. Where near-real-time rails are used, verify that status messages such as pacs.002 are received, stored, and shown clearly to partners.

A common breakdown is fragmented ownership. PRM and CRM records look healthy while the money trail is unclear. For each row, keep an evidence pack with document requirements, a status-tracking screenshot, a named exception owner, an exception turnaround target, and partner-facing SLA language. That is how you separate "can launch" from "can scale."

Related reading: Affiliate Marketing Management for Platform Operators Running a Partner Network.

If payout reliability is a gating variable in your table, review how compliance-gated status tracking and batch operations work in Gruv Payouts.

Choose payment flow designs that match partner expectations#

Choose the flow your partners will judge most often, not the one that only looks smooth at first launch. If the core job is paying in once, optimize Checkout. If the core job is getting paid repeatedly, prioritize clear status on outgoing funds.

| Flow pattern | Best fit | Main upside | Main tradeoff | Pre-launch checks |

|---|---|---|---|---|

| Card-led Checkout | Programs where fast first payment matters most and card use is expected | Cards are commonly used online and in person. In Stripe's experiment, adding relevant methods beyond cards improved average conversion and revenue, with the largest gains from local methods, wallets, and bank debits. | Faster front-end conversion can shift problems downstream if disbursement handling, verification, or status visibility is weak. | Confirm method support by country, currency, and product; test partner-facing payment and disbursement status updates end to end. |

| Bank-transfer-first onboarding | Cost-sensitive B2B programs or markets where bank rails are standard | Direct bank debits can reduce transaction-fee cost versus cards, and local non-card methods can matter in some markets. | More up-front information and verification can slow activation, and non-instant transfers may only show estimated arrival timing. | Validate verification and document requirements before transacting; confirm how estimated arrival timing is shown to partners. |

| Hybrid collection plus disbursements | Marketplaces, referral programs, contractor ecosystems, and other collect-and-disburse models | Balances front-end conversion with stronger operational control when collection and disbursement states are visible in one journey. | More moving parts: onboarding requirements, eligibility, event handling, and reconciliation must stay aligned. | Verify availability by country or program, implement webhook infrastructure, and test partner-facing status messages before go-live. |

Capabilities and timing vary by market, provider, supported currency, and compliance configuration. A flow that works in one program can fail in another. A method may be available for collection but not for sending funds, or additional verification may be required before payments can be processed.

Read the tradeoffs where ops feels them first#

The right flow is the one your operations team can support without hiding problems from partners.

Card-led flows can win early because they reduce front-door friction. Use that as directional evidence, not a universal promise. The real question is whether higher checkout completion also holds up in disbursement operations, exceptions, and reconciliation.

Bank-transfer-first flows trade speed for control. Incremental onboarding can activate accounts faster, but missed later requirements can create disbursement or processing issues. Stricter up-front onboarding adds friction, but reduces that risk.

Hybrid flows can be a practical choice for platforms. If partners can see a completed collection but cannot see fund-status changes, they may still experience the payment flow as broken.

A practical if then rule#

If your vertical depends on frequent small disbursements, prioritize status transparency over front-end Checkout polish. In those models, unclear money movement is often a bigger operational risk than minor checkout polish gaps.

Before you commit, keep a short evidence pack for each program. Include payment-method and disbursement support by country and currency, verification requirements, a tested webhook path, and partner-facing status screenshots. Treat this as a hard gate, because some country feature sets allow collection but do not allow sending funds.

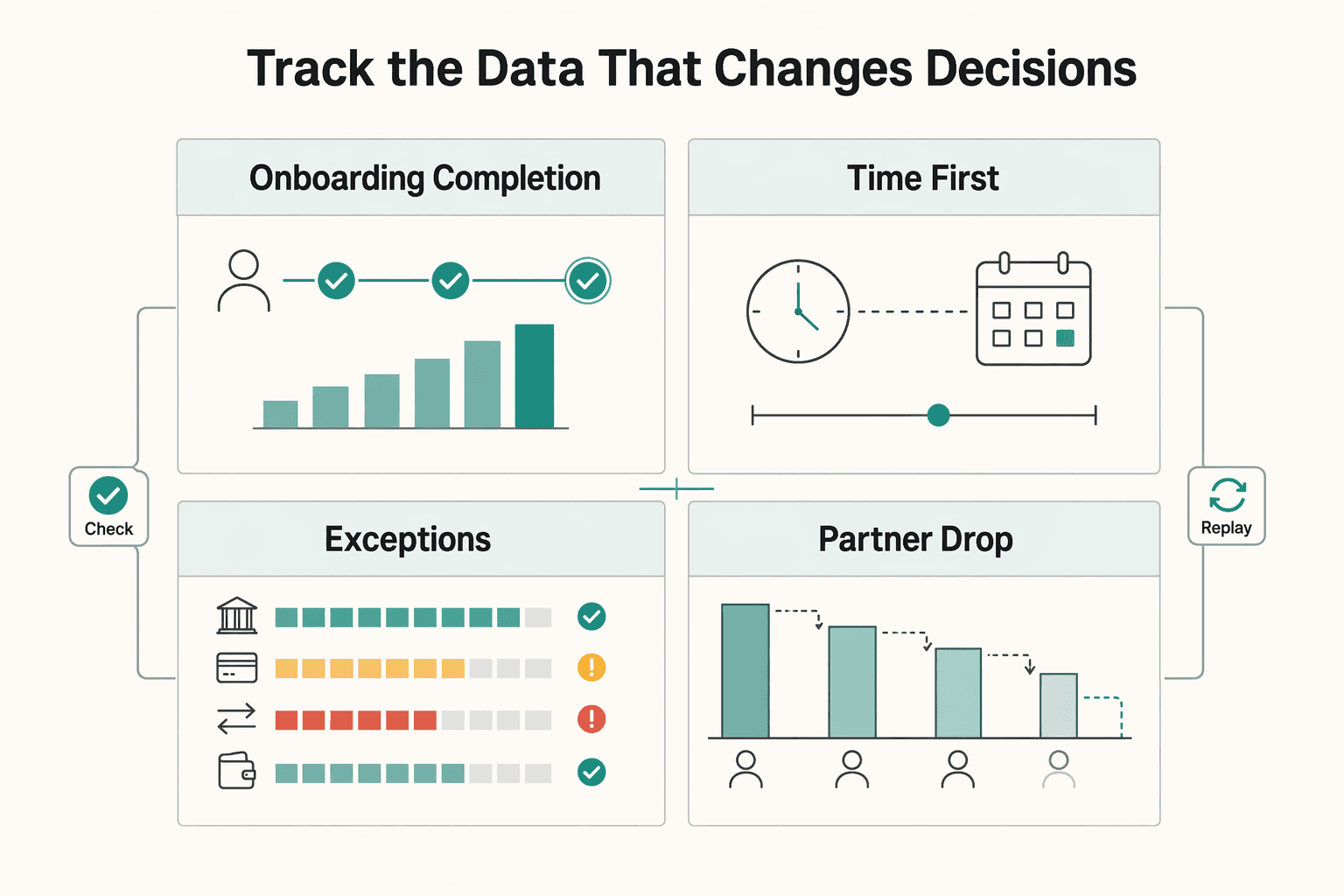

Track the data that changes decisions, not vanity dashboards#

Track only the signals that change a product fix, an ops intervention, or a rollout call. Once you have chosen a payment flow, the core question is simple: do partners complete onboarding and get paid without avoidable failure or delay?

Use a minimum signal set: onboarding completion, time to first successful disbursement, exception rate by payment rail, and partner drop-off by step. Together, these show where activation slows, where money movement breaks, and whether issues are broad or cohort-specific. For step-level loss, GA4 Funnel exploration helps you see where users fall out. For checkout flows, GA4 Checkout journey reporting depends on events like begin_checkout, add_payment_info, and purchase, so event quality directly shapes what the funnel appears to show.

| Metric | What to verify before trusting it | Decision use |

|---|---|---|

| Onboarding completion | Confirm accounts actually completed required onboarding requirements, not just the final UI step | Prioritize instrumentation and friction fixes, then decide which segment to invite next. |

| Time to first successful disbursement | Reconcile webhook events with payout status states and reconciliation output | Monitor and escalate disbursement issues, and set realistic partner expectations. |

| Exception rate by payment rail | Distinguish failed vs pending vs returned states, and tag rail or method consistently | Improve failure handling and partner-facing status messaging. |

| Partner drop-off by step | Rebuild the funnel and confirm each step fires once and in order | Fix event quality and step design, then narrow targeting when issues cluster by cohort. |

Segment with profile data you can actually defend#

Segmentation only helps if you can defend the inputs. Use a Real-Time CDP when rollout decisions need more than aggregate metrics. Adobe documentation supports supplementing first-party profiles with trusted partner-provided attributes and notes these partner insights can be used for segmentation even when they are not used for personalization.

In practice, combine observed operational signals, such as completed onboarding requirements, first successful disbursement, or repeated payout failures, with partner attributes you already collect. This helps you avoid blunt rollout decisions when issues are concentrated in a specific cohort.

Reconcile partner facing status with money state#

Do not use these metrics for GTM decisions until partner-facing status matches your internal event trail. Stripe recommends a webhook endpoint for Connect events, including payout failures. When a payout fails, external account status is set to errored and scheduled payouts stop. If a portal still shows "processing," your metrics can mislead you.

Use payout reconciliation as a second check. Stripe's payout reconciliation reporting is based on daily activity from 12:00 am to 11:59 pm, with transaction-level drill-down from payout summaries. Also separate delayed from failed states. Returned transfers are typically visible within 2-3 business days, while trace status can remain pending for up to 10 days after arrival_date in some cases.

If you want a deeper dive, read How the Payments Experience Improves Your Partner Network: A Platform Operator's Playbook.

Sequence the first 90 days of rollout to reduce rework#

A clean rollout sequence matters more than a fast one. Start with the minimum viable money path, harden disbursement operations next, and expand scope only after tracking and reconciliation stay reliable in production. That order can reduce rework when growth would otherwise outpace onboarding, money-out handling, or exception control.

| Phase | Focus | Checkpoint |

|---|---|---|

| Phase 1 | Core Partner Portal path | Account creation, onboarding completion, clear next steps, and a defined completion path immediately after account creation |

| Phase 2 | Disbursement operations | Treat webhook events as the real-time status source, and confirm failed items in reconciliation reporting match items in the exception queue |

| Phase 3 | Channel expansion | Expand only after real-time tracking is stable and reconciliation quality is proven in the operating cycle |

Phase 1#

Launch only the core Partner Portal path: account creation, onboarding completion, and clear next steps. The key control is a defined completion path immediately after account creation, because the account must have a way to complete onboarding requirements.

Choose onboarding mode deliberately. Up-front onboarding collects eventually due requirements earlier and can reduce payout or processing issues from missed deadlines. Incremental onboarding only collects currently due requirements, but can leave a partner appearing live while still blocked on missing requirements. If you use incremental onboarding, show unresolved requirements in the portal and route partners back to completion without support intervention.

Make fallback explicit. If an onboarding link is expired, already visited, or invalid, it should route through a refresh URL and return the partner to the flow cleanly.

Phase 2#

Once the first cohort is live, harden disbursement operations before you add channel scope. Treat webhook events as the real-time status source for asynchronous money-state updates.

Your exception handling should separate states at minimum: processing, posted, failed, returned, and canceled. Those states need different partner messaging and different operations responses.

Keep retries and document completeness in scope. Retry tools can improve collection outcomes in some flows, but returned payouts are a separate issue and are commonly tied to incorrect destination information. Since returns are often visible within 2-3 business days, verify your team can detect and resolve them before the next cycle.

Use one concrete checkpoint: failed items in reconciliation reporting should match items in your exception queue. If they drift, portal status, webhook handling, or finance reporting is out of sync.

Phase 3#

Expand channel scope only after two conditions are true: real-time tracking is stable, and reconciliation quality is proven in your operating cycle. Stable tracking means webhook-driven status changes reliably reach your application and match partner-facing status.

Reconciliation quality means finance can tie transactions to disbursement batches, or to transaction-level settlement details where supported. If you use Adyen settlement reconciliation, confirm payout frequency is configured before relying on that output.

Before broader availability, run an ORR-style readiness check across onboarding recovery, webhook delivery, status handling, exception triage, and reporting output together.

One gating rule#

Set one internal gate and document it: if exception volume exceeds team capacity in consecutive review cycles, pause market expansion and fix root causes first. This is an operator rule, not an industry or regulatory standard.

Typical root causes include missing onboarding requirements, destination-data errors behind returned payouts, and status mismatches between the portal and actual money state. If a rail has threshold risk, include it in the gate. For ACH, monitor early because Nacha sets an unauthorized return rate threshold of 0.5% over the preceding 60 days or two calendar months.

Spot red flags before you spend more GTM budget#

Do not increase GTM spend when your operating evidence is incomplete or contradictory. At this stage, weak activation can reflect payment operations, verification handling, or status-visibility gaps, not just demand quality.

Once an initial cohort is live, do not treat top-of-funnel interest as a scaling signal by itself. In channel partner programs, a partner that does not begin actively selling within the first 90 days is a risk signal. Test whether the blocker is commercial fit or payment execution before you buy more leads.

The red flags worth treating as real#

Watch these signals together, not in isolation:

- rising manual interventions in payment operations

- unresolved verification or document backlog

- partner complaints that payment or money-out states are unclear

- inconsistent outcomes for similar partner cases

Manual intervention is not automatically bad, but it becomes a scaling risk when it grows with volume. The grounding data shows 98% of organizations still rely on manual payment work somewhere, and one-third lose a full day per week to those tasks. If your team is handling more cases manually each cycle, manual support load can outpace your team's capacity.

Document backlog is a direct capability risk. In Adyen's verification model, unresolved issues can lead to payment capabilities being disallowed. If your portal shows "onboarded" while compliance or payments still shows unresolved requirements, treat that as a money-movement risk, not just an activation issue.

The misleading signal most teams overvalue#

Strong lead flow with weak activation can be a vanity-metric pattern. Healthy PRM or CRM volume does not prove the payment path is stable.

Use a cohort-level check instead: onboarding completion, time to first successful disbursement, and share of partners needing manual intervention before first success. If applications rise while first successful disbursement stalls, investigate execution before rewriting positioning. Payment execution is not always the cause, but it should be a primary hypothesis.

Also confirm that partner-facing status matches provider truth sources, such as webhook events or status reports. If support says "sent" but provider events or status reports show a different state, that contradiction is a scale blocker.

Use a hard stop, not a hopeful interpretation#

Set one explicit rule: pause spend increases when the operating picture is incomplete or conflicting. You do not need a universal exception-rate threshold. You need evidence that new volume will behave like current volume.

Use a stop condition when:

- finance cannot reconcile failed or returned transfers to the same items in your exception queue

- document issues age without a clear owner or resolution path

- complaints about invisible payment states cannot be validated against event logs or status reports

- similar partners receive different disbursement outcomes without a documented reason

Use this as a decision test, not a slogan. If your partner platform records, payment records, and reporting disagree on who is activated, who can be paid, and what state money is in, more spend can mask the problem in the short term and deepen it later. The grounding data also notes that operational payment failures can become expensive quickly, with more than 60% resulting in at least $1 million in total losses.

When evidence conflicts, fund diagnosis first. Resume spend only after status visibility, document readiness, and disbursement outcomes align for the same cohort in the same reporting period.

Assign ownership across teams so issues do not bounce#

Partner-impacting issues can bounce when ownership and handoffs are unclear, even if the initial failure is in a single system. Define roles explicitly, but treat them as an operating model that may vary by entity, market, and compliance setup.

A practical split can look like this:

- Product can own partner-facing UX, status language, instrumentation, and defects where the portal state is wrong or missing.

- Payments ops can own payment execution, provider-side investigation, and exception handling when transactions are routed to exception queues.

- Finance can own reconciliation: matching transaction records to accounting records so outcomes can be explained.

- Compliance can own policy and capability gates tied to requirements and oversight.

Use a clear handoff rule: keep relationship context in PRM and CRM, and keep money-state truth in payment records and the ledger. CRM and PRM are relationship systems. They are not the source of truth for transaction state, balances, or settlement. If a relationship system shows a partner as live but money records do not support that state, treat it as a mismatch to investigate.

Run a shared recurring review for unresolved partner-impacting defects with channel, product, ops, finance, and data owners, with clear communication and escalation paths, using the same evidence pack. If reviews rely on screenshots or anecdotal notes instead of event and reconciliation evidence, issues are more likely to keep bouncing.

Build the go or no-go evidence pack for leadership#

Make this pack a decision memo. Leadership should be able to approve, limit, or pause rollout based on evidence, not narrative updates.

Start with a concise summary (often one page) that states:

- the market or program rationale

- the payment design choice at key payment touchpoints

- the expected first-phase partner impact (as a forecast, not proof)

- the key operational risks and their implications

- the specific action requested

Then attach the artifacts that support that summary:

- the score table, with each metric checked against its underlying report definition

- status-tracking evidence for disbursements across successful and failed outcomes (for example: processing, posted, failed, returned, canceled, and visible return reasons)

- the exception definitions used by the operating teams, aligned to provider-specific status models

- reconciliation checks that tie disbursement batches to bank-statement matching and show what each batch included (payment, refund, chargeback)

End with one clear recommendation sentence and explicit caveats where coverage varies by market, industry, or program. If timing can vary, say so directly, including provider-specific ranges such as Stripe initial payouts around 7-14 days after a first successful payment and returned payouts often 2-3 business days but sometimes longer by recipient country.

Conclusion#

Better partner outcomes are more likely when payment execution and decision-grade data are operationally sound, not when branding language is polished. A polished portal is unlikely to compensate for missing local payment methods, unclear payout states, or weak reconciliation.

The evidence here is operational, not rhetorical. Worldpay reports a correlation between payment-experience satisfaction and retention-related outcomes, but that is not causal proof. A practical signal is whether partners can pay and get paid through familiar rails, track money states, and resolve exceptions quickly.

Make the next step small and testable:

- Run one candidate market through your score table.

- Test one payment design (card-led, bank-transfer-first, or hybrid).

- Review execution evidence before expanding country scope or partner segments.

Keep verification concrete. Confirm that partner-facing statuses match your internal payment and settlement records, and verify that you can reconcile transactions in each disbursement batch with a payout reconciliation report. If you use a Real-Time CDP, use it to enrich context, not to hide money-state gaps.

Do not treat market availability as operational readiness. Capabilities vary by provider, country, and account configuration. Coverage changes over time, some agreement types are available only in select countries, some account setups limit payment functionality, and recipient-account transfers can add 24 hours. Adyen also requires payment-method configuration before processing starts.

Separate "can launch" from "can scale." You may launch with controlled manual handling, but scale only when local payment method fit, exception handling, and reconciliation quality are evidenced. If you want a final pre-expansion check, talk to Gruv to confirm market or program coverage and implementation constraints before committing broader resources.

Before committing expansion budget, align your market plan with Gruv to confirm what is enabled for your program in each country: Talk to Gruv.

Frequently Asked Questions

What is the difference between a Partner Experience Platform and Payment Experience (PX)?

A Partner Experience Platform covers relationship workflows, including channel sales collaboration and partner portal activity in PRM and CRM contexts. In this context, Payment Experience is the execution layer: local payment method fit, timing for getting paid, money-state visibility, and failure handling. Use PRM and CRM to understand relationship context, but use payment-system evidence to confirm whether money movement is working.

How does payment execution quality affect partner retention in channel partner programs?

Payment execution issues often appear when partners do not see familiar payment options, cannot track payout status, or face unclear failures. CompTIA reports that 50% of channel firms dropped a vendor due to poor partner experience practices, and 35% said they only work with vendors offering seamless partner experience. Not every retention issue is a payment issue, but weak payment execution can contribute to partner strain.

Which metrics should a data platform track before expanding to a new country?

Track decline-rate trends, failure-type mix, and status distribution for outgoing funds before launch decisions. Classify failures into practical types (for example, issuer declines, blocked payments, and invalid API calls) and monitor states such as processing, posted, failed, returned, and canceled. Validate that partner-facing statuses match payment event data, including webhook-tracked activity, so expansion decisions are based on reliable execution signals.

What should founders validate first when partner expectations conflict with local payment constraints?

Validate local payment method fit first, because payment localization starts with local expectations and constraints, and missing familiar options can increase abandonment. Then validate timing for getting paid and status visibility, including how returns are communicated. Returned payouts are typically completed in 2-3 business days but can take longer depending on the recipient country. For EU euro transfers, treat instant-payment requirements as EU-specific regulatory conditions, not a global default.

When should a team delay GTM expansion even if demand signals look strong?

Delay when payment execution evidence is incomplete or inconsistent, especially around declines, failure classification, and visibility into money-out states. Cross-border payments still face structural frictions in cost, speed, access, and transparency, so demand alone is not enough to justify rollout. If you cannot clearly explain payment outcomes operationally, pause and fix execution before scaling acquisition.

How can PRM and CRM data be used without confusing relationship health with payment health?

Use PRM and CRM data for relationship health: engagement, collaboration, account context, and support history. Use payment-system data for payment health: declines, failures, and money-state outcomes. Then combine both views in a unified profile layer for diagnosis, while keeping relationship signals and money-state signals analytically distinct.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/cpmi/cross_border.htmtrusted

- bis.org/cpmi/publ/swift_gpi.pdftrusted

- consumerfinance.gov/compliance/supervision-examinations/complian...trusted

- csrc.nist.gov/pubs/sp/800/30/r1/finaltrusted

- dhs.gov/sites/default/files/2022-03/Action%20Memo%20...trusted

- docs.stripe.com/global-payouts/manage-payoutstrusted

- ecb.europa.eu/paym/retail/instant_payments/html/instant_pa...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: