Quick Answer

A go-live payout compliance checklist should define the release gates that must clear before money moves, name who can hold, release, or escalate exceptions, and specify the evidence your team must retain. Before launch, validate beneficiary bank data, confirm provider licences and permits, test sanctions, AML, tax, and recordkeeping workflows, and prove every payout decision can be reconstructed from system records.

What to Confirm Before Global Payout Go-Live#

Use your global payout compliance checklist as a go-live decision tool, not just a list of control themes. Cross-border payouts pass through multiple systems, currencies, intermediaries, and rules. Before launch, your checklist should make three things explicit: what must be verified before money moves, who approves exceptions, and what evidence you will retain if a payout is delayed, rejected, or questioned.

The failure modes are practical. Wrong IBAN, account number, or SWIFT/BIC details are a leading cause of international payment failure, and even small typos can trigger delays or rejects. In one example, a payment was returned after five days because of a single IBAN digit error, with $50 in intermediary fees. Treat that as a reminder of how small data errors create real operational and financial friction.

Banks and payment providers also run KYC and AML checks as part of compliance review. Your launch standard should turn those requirements, along with internal finance and operations needs, into clear release decisions your team can execute consistently. At minimum, your pre-launch review should answer:

- What are the non-negotiable checks before the first payout is released?

- Who owns each decision when payee data is missing, inconsistent, or escalated?

- What evidence will you retain to prove the check ran and the payout outcome matched the decision?

Use the checklist to assess current capability and identify day-zero gaps. Two practical checkpoints are beneficiary data validation and provider due diligence. Verify that bank-detail checks are reliable, and confirm your provider has the necessary licences and permits for cross-border payments with acceptable security and compliance standards.

The goal is proportionate, defensible controls for the markets, payee types, and payout rails you are enabling first, then more depth where actual transaction and exception patterns justify it. If you are launching contractor, seller, or creator payouts, coverage can vary by market and program, so use local legal and tax counsel for country-specific obligations.

For the ongoing review cadence after launch, see Build a Global Contractor Payment Compliance Calendar for Monthly, Quarterly, and Annual Obligations.

Set the go-live standard before you buy more tooling#

Set your release standard before you add tools. If your team cannot state what must be true before money moves, tooling will only automate unclear decisions. Start by defining six control domains in one go-live control statement:

- Written AML program

- Suspicious activity reporting

- Record retention

- Transmittal-of-funds recordkeeping

- FBAR threshold and valuation checks

- Governance and escalation ownership

For a U.S. baseline, anchor that statement to concrete FinCEN control lanes: a written AML program (31 CFR § 1022.210), suspicious activity reporting, and record retention (31 CFR § 1010.430), including transmittal-of-funds records (§ 1010.410(e)). Treat these as owner-and-evidence requirements, not abstract themes.

Use a hard internal launch gate. No live payout should be released unless your documented control checks are complete and your filing and recordkeeping paths are operational. Position this as house policy, not as a FinCEN-mandated payout-release rule.

Before first live traffic, document escalation for:

- Who receives potential suspicious activity cases for SAR review

- Who owns FinCEN-related reporting decisions

- Who can place and maintain payout holds during review

Before you move into market design, prove the control statement works in practice with two operator checks:

- Confirm your evidence pack can produce the current AML policy version, alert disposition, approver, and timestamp on demand.

- Test missing-required-field failure handling, since filings or submissions can be rejected when required elements are missing.

If foreign account reporting is in scope, add an FBAR checkpoint: when maximum single-account or aggregate value exceeds $10,000, trigger filing review, and value each account separately.

The output here should be a concise control statement with named owners, escalation paths, and evidence checkpoints for launch and exceptions.

If you need to translate these release gates into an operational workflow with audit trails and retries, review the Gruv docs.

Lock scope by market and payout rail before control design#

Lock scope before you design controls: name the first-wave markets, map each to a real payout rail, and set an explicit operating model for each path.

Freeze first-wave markets#

Inventory launch markets as named entries by country or jurisdiction, not a single regional bucket. Assign one status per market: in scope now, defer, or blocked pending counsel.

Use a readiness gate before marking anything in scope now. If you cannot show sufficient staff, time, financial, and legal resources, keep that market out of the first release.

If you need a country-by-country planning frame, use Cross-Border Compliance Checklist for Platform Payouts: Licenses Registrations and Reporting by Country.

Map payout paths by rail#

For each market, map the production rail you expect to use, for example SWIFT, correspondent banking, local rails, or wallet-based settlement rails. Do not treat a single provider integration as a single control surface. One integration can expose multiple rails, but rail-level operations and evidence still need to be defined.

Rail choice has operating tradeoffs. For example, local acquiring is typically associated with higher acceptance and lower cost than cross-border routes, so route choice should be explicit, not assumed. If your team still needs a quick reference for bank and routing identifiers across rails, see Bank Code vs. Routing Number vs. Sort Code: A Global Platform Payout Reference Guide.

| Rail or path | Decide now | Minimum evidence checkpoint |

|---|---|---|

| SWIFT | Which corridors use it first and through which provider or bank path | Route decision, approver, payout confirmation, and reconciliation record |

| Correspondent banking | Where intermediary-bank paths are expected | Planned path and confirmation artifacts explaining payment movement |

| Local rails | Which markets use local instead of cross-border routes | Market-to-rail decision, provider used, and reconciliation proof |

| Wallet rails | Where wallet-based settlement is used by market and payee type | Stricter destination-change control, approval trail, and payout confirmation |

Choose the operating model before detailed controls#

Document where operations are direct versus handled indirectly through a third party. Do not leave this implicit. For each market and rail path, name who owns execution, approvals, and evidence retention. If ownership is unclear, mark the market blocked pending counsel.

The final artifact is one market-by-rail matrix with status (in scope now / defer / blocked pending counsel), rail, operating model, and owner.

Assign control ownership and escalation authority#

Once your market-by-rail matrix is fixed, assign named decision owners for your internal workflow. If your process includes hold, release, permanent block, or payout-escalation actions, name who can take each action so the controls are usable in real operations.

Put one accountable owner on each control domain#

A simple RACI can work, but map it to people, not only teams. For each control, document one accountable owner, one execution owner, and a clear handoff when work moves from routine handling to judgment.

| Control area | Accountable owner | Execution owner | Verification checkpoint |

|---|---|---|---|

| KYC and KYB | Named Compliance owner | Ops, with Engineering support for intake and status | Internal identity-check status is documented before release decisions |

| Sanctions screening and PEP review (if in scope) | Named Compliance approver | Ops or screening queue for initial routing | Hold, release, or block outcome records person, timestamp, and reason |

| AML alerts and potential SAR review | Named AML investigations owner | Compliance or Risk analyst | Escalation path for suspicious activity review is documented |

| Tax forms | Named Finance or Tax Ops owner | Ops or onboarding team | Tax-form workflow ownership and release dependency are documented |

| Audit exports and filing data | Engineering owner for extraction plus business sign-off owner | Engineering with Compliance or Finance | Test export is reproducible and includes required filing fields |

Queues can route work, but decision authority should still be explicit. Shared inboxes can support intake, but final decision ownership should be documented in your workflow.

Separate action authority from case handling#

If your workflow uses temporary hold, release-after-review, and permanent-block actions, define named approvers for each. These actions can sit with different teams, but each should have named primary and backup coverage.

Engineering can implement controls, Ops can process cases, and Legal can advise. Your approval matrix should still show who has final release authority when a case becomes judgment-based.

Define the FinCEN escalation path before first use#

FinCEN identifies suspicious activity reporting as a specific MSB compliance area and lists a written AML program as an MSB requirement. Build the escalation path now, including who reviews and who makes the final filing decision for potential SAR events.

If you operate through a foreign-located MSB structure, confirm the U.S.-resident agent for service of legal process is designated and included in your escalation tree.

Test evidence and filing failure points#

Ownership is only real if evidence can be produced under pressure. Run a simulated case in each critical lane and verify that you can produce the alert source, reviewer, decision, and payout action.

For FinCEN-related filing data, test for hard-fail gaps before go-live. FinCEN XML guidance documents rejection risk when required elements are missing.

Where your structure creates an FBAR obligation, assign a filing owner and backup. FBAR filing applies when a single account or aggregate maximum value exceeds $10,000. The standard annual due date is April 15 with an automatic extension to October 15, and FinCEN may issue event-specific extensions. If you find errors after filing, an amended FBAR is required, and the prior report BSA Identifier must be retrievable.

The final output for this section is a live approval matrix with named people and backups, plus an on-call escalation tree usable during a real payout incident.

Build onboarding controls with risk tiers, not one-size-fits-all checks#

Use tiered onboarding as an internal operating policy, then make first-release rules explicit in a decision tree your team can apply consistently.

Use payee type, jurisdiction, payout volume pattern, and rail type as internal policy inputs. The sources used here do not treat them as regulatory factors. From there, define a small set of tiers and the required evidence for each tier before first payout release.

For entities, ownership and control checks can be set as an internal release gate, but the sources used here do not define specific KYB onboarding requirements or payout-hold rules.

Define enhanced review triggers before go-live so judgment calls are not improvised in live traffic. Keep those triggers documented as internal policy, since the sources used here do not specify corridor-, rail-, or profile-based trigger rules.

If your structure can create FBAR obligations, capture the filing-critical data at onboarding so Finance is not reconstructing records later.

| FBAR checkpoint to capture early | Why it matters later |

|---|---|

| Who has financial interest or signature authority over foreign accounts | A U.S. person in that position must file an FBAR (FinCEN Form 114) when thresholds are met |

| Account-level records and statement trail | Maximum account value is based on the greatest value during the calendar year; periodic statements may be used if they fairly reflect that maximum |

| Currency and year-end conversion basis | Non-USD accounts are converted using the Treasury Financial Management Service rate for the last day of the calendar year |

| Threshold logic in reporting workflow | FBAR is required when a single-account maximum or aggregate maximum exceeds $10,000 |

| Edge-case handling fields | For fewer than 25 accounts, item 15a ("amount unknown") may apply in specific cases; if a computed maximum is negative, enter 0 |

| Filing lifecycle traceability | Annual due date is April 15 with an automatic extension to October 15; amended filings require a new full FBAR with the Amend box checked |

| Required XML field completeness, if filing automation is used | Missing required elements can cause rejection |

The final output for this section is an onboarding decision tree with named tiers, required documents by tier, enhanced-review triggers, and a clearly labeled internal entity rule for incomplete ownership or control data.

Implement sanctions and AML controls that can actually stop bad payouts#

Onboarding tiers only matter if live controls can still stop release, so make sanctions and AML checks a real payout gate.

Screen the full payout context before release#

Run sanctions screening before the first payout, then rescreen active payees using a risk-based approach. Do not screen names alone: include relevant people, entities, and jurisdictions, and check both country-based and list-based sanctions.

Use current KYC/KYB/CDD and live payout data at the time of approval. If key payee details changed since the last clear result, rescreen before funds move.

Monitor for explainable AML risk signals#

Start with a small rule set your team can operate consistently, then tune it as you learn:

- Unexpected velocity spikes versus expected payout activity

- Jurisdiction anomalies against expected patterns

- Material shifts in transaction amount or behavior profile

Route alerts into clear case states, for example new, under review, cleared, hold, or blocked. Keep alert quality high early. False-positive flooding is a known AML failure mode and can hide real risk.

Put stop rules in writing#

Write the release rules down so teams do not improvise in live queues:

- Unresolved sanctions hit: pause payout release until the match is resolved under internal policy

- Unresolved suspicious behavior: place a controlled hold and escalate for AML review under internal policy

- Release only after documented clearance with approver accountability

Document what was reviewed, what matched or did not match, the disposition reason, and who approved the outcome.

Keep Travel Rule data transferable where applicable#

Travel Rule requirements are jurisdiction-specific. Where comparable data-transfer obligations apply in your payment chain, keep payment and screening records in structured formats tied to the payee and payment. Avoid free-text-only evidence trails so records stay portable and auditable across providers.

Define the output artifact#

Use an alert triage log that captures core fields such as case ID, payee ID, trigger type, disposition reason, approver, and timestamp. If a peer cannot reconstruct why a payout was blocked or released from the log alone, tighten the control design before go-live.

For a step-by-step walkthrough, see Crypto Payout Compliance for Blockchain Disbursements in 2026.

Treat tax onboarding as a release gate, not a back-office cleanup task#

A clear onboarding result is still not enough if tax data is unresolved. Put tax onboarding on the same release path as your other payout controls so you catch bad data before money moves and before remediation multiplies.

Capture tax form data and reconcile it to the payee record#

Before first payout, decide which tax data your policy expects for that payee and record structured data, not just an uploaded file.

Reconcile tax data to the approved payee profile fields that commonly break reporting later: legal name, address, and tax identification number (TIN). If tax data conflicts with the payee profile details, move the payout to review instead of letting the queue guess.

Use a clear rule for missing, incomplete, or inconsistent tax data. Manual cleanup while payouts continue is exactly how inconsistencies and missed tasks accumulate.

Put 1099 readiness into normal operations, not January triage#

Define internal handoffs before launch, including who owns exceptions and who owns reporting readiness checks.

Build readiness around data completeness, not year-end urgency. Where 1099 reporting applies, completed tax verification and eligibility drive whether forms are delivered electronically or postmarked by January 31st. Waiting until January to discover TIN or name mismatches puts you straight into remediation mode.

Add one recurring reconciliation checkpoint: export payout data to CSV and confirm payments tied to each client or payee are fully accounted for. This simple control can catch payout-ledger and reporting-population drift early.

Route tax-data changes through review#

Do not let tax status live only in email threads or spreadsheet notes while payouts keep flowing. When legal name, address, or TIN changes, or when tax data no longer matches the approved profile, send the account back to review under a defined process.

Keep correction handling explicit. For 1099 field corrections, such as TIN, legal name, or address, route requests through the platform flow to payer-side review and tie payout decisions to that case.

Define the tax status ledger#

The output artifact for this section is a tax status ledger that keeps payout operations, reporting, and remediation tied to one decision record. Include at least:

- payee ID, payee type, and jurisdiction

- tax form type on file

- legal name, address, and TIN match status

- tax review status and hold reason

- payout status and last approved release timestamp

- 1099 readiness flag, reporting year, and reconciliation status

- correction case owner and resolution timestamp

Specify the audit evidence pack your team must produce on demand#

Your evidence pack should let a reviewer reconstruct any payout decision without relying on inboxes, chat threads, or memory. This is where policy turns into operation-level evidence that Internal Audit, Compliance, and external auditors can actually test.

1. Make each payout decision reconstructable#

For any payout ID, your record should connect the full decision chain: what was reviewed, who decided, and the final release, hold, or reject action.

Use a simple test: can the record answer, in one place, what was reviewed, who decided, and what happened next? If those answers are split across multiple tools with no clear link, you have fragments, not an audit-ready documentation trail.

2. Keep a tamper-evident event trail for material state changes#

Do not rely on final status alone. Keep a tamper-evident audit log for material state changes tied to payout controls. That includes holds, releases, rejects, escalations, overrides, and profile changes that trigger re-review.

For each event, preserve enough context to show when it happened, who acted, what changed, and why. This is what proves a control operated on a real case, not just on paper.

3. Define export and handling standards before requests arrive#

Set a standard export package in advance: what is included, who can assemble it, and how retrieval works. Keep it consistent enough for internal and external review while maintaining clear handling boundaries for restricted materials.

Make those boundaries explicit in your process: what is excluded from routine exports, who can access restricted records, and when Compliance or Legal approval is required. Because laws, regulations, and standards change, review and update this evidence standard on a 12-month cadence.

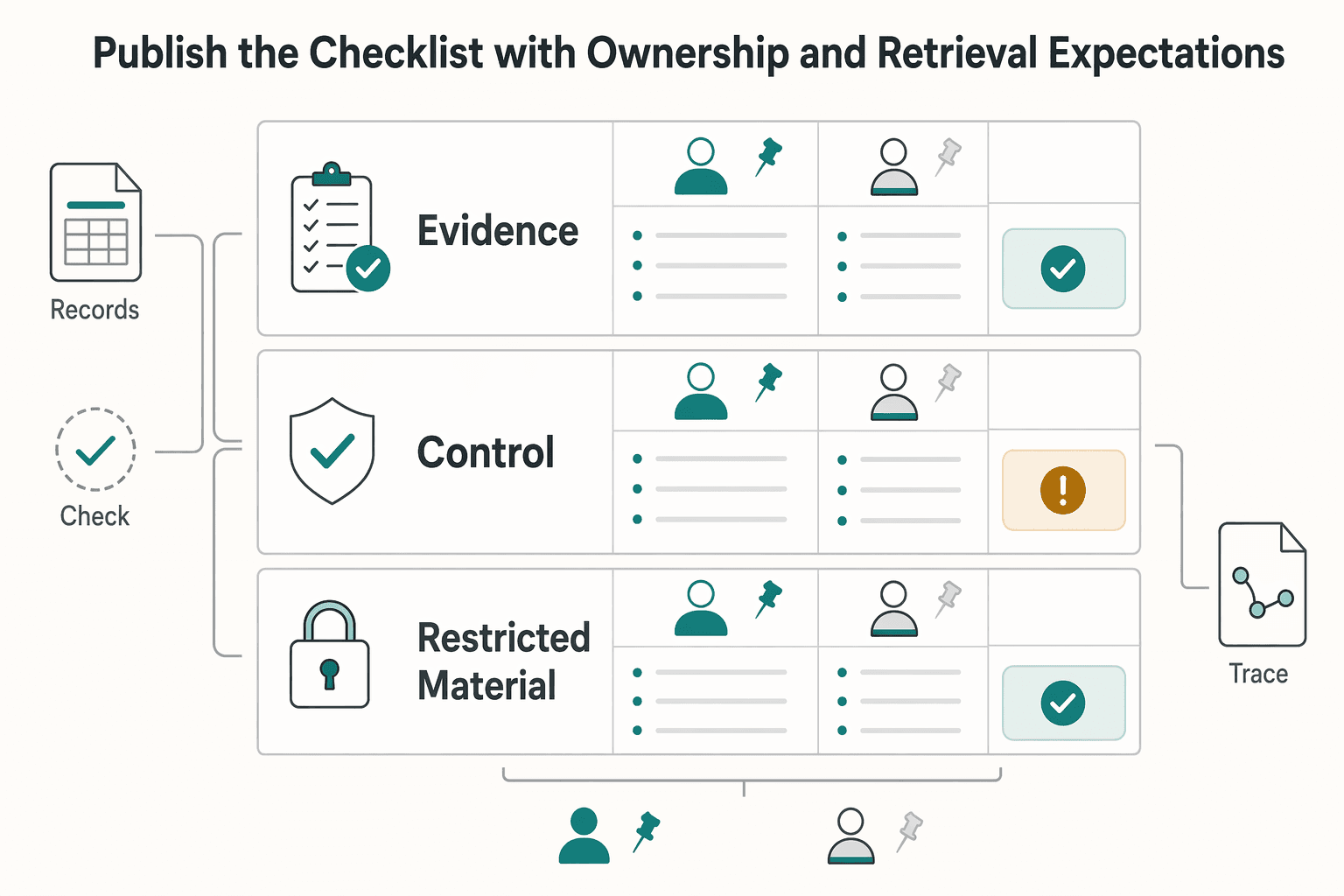

4. Publish the checklist with ownership and retrieval expectations#

Use a master checklist as the operating artifact. Assign a primary owner and backup owner for every item so retrieval does not depend on one person.

| Evidence item | What it must prove | Owner and backup | System of record | Retrieval expectation |

|---|---|---|---|---|

| Payout decision record | End-to-end traceability from review through release, hold, or reject | Compliance Ops owner + backup | Payout ledger or case system | Documented process |

| Control review history | Screening or risk-review result, disposition, approver, and timestamps | Controls owner + backup | Review and case tools | Documented process |

| Supporting documentation status | Required-document status, exception handling, review decision, and decision link | Operations owner + backup | Record store and profile system | Documented process |

| Restricted-material export rule | What is excluded from routine exports and who must approve access | Compliance lead + Legal backup | Access-controlled repository | Documented process |

For a detailed reference on payout rail details by market, see Bank Code vs. Routing Number vs. Sort Code: A Global Platform Payout Reference Guide.

Decide what must exist at day zero and what can wait until day ninety#

At go-live, prioritize controls that can block a non-compliant payout and any FinCEN or BSA duties that apply to your operating model. Defer optimization work to a dated backlog with clear ownership.

What cannot wait#

Your day-zero baseline should include enforceable payout-release gates from your control framework and named escalation owners. Manual handling is only acceptable if it can actually stop release and leaves a clear decision record.

For U.S.-applicable MSB exposure, treat these as launch prerequisites:

- a written AML program

- suspicious activity reporting ownership and process

- recordkeeping and retention operations

- FBAR handling that can detect when a single-account or aggregate maximum value exceeds

$10,000 - an FBAR amendment process, using a new FBAR marked as an amendment

- submission-quality checks so required filing elements are not missed

| Control area | Day-zero requirement | Pre-launch verification |

|---|---|---|

| Release gating | Blocking controls can hold payout release until review is resolved | Test one pass case and one hold case end to end |

| FinCEN or BSA core operations | AML program, SAR ownership flow, and record-retention method are operational | Confirm owners, approval path, and retained event history |

| FBAR operations | If FBAR filing is in scope, threshold detection, maximum-value method, and correction path are defined | Confirm $10,000 trigger logic, value evidence, and amendment workflow |

| Filing readiness | Filing data includes required elements and clear error handling | Validate submission payload quality before production use |

If FBAR filing is in scope, make sure the team can explain how maximum account value is calculated. They should also be able to show how exchange-rate source evidence is captured when no Treasury rate is available, and how annual filing timing is tracked (April 15th due date, automatic extension to October 15th).

What can wait until day ninety#

Day ninety is for optional depth, not missing obligations. Use it for deeper scenario analytics, corridor-specific tuning, and automation of repeat alert classes only after your manual disposition pattern is stable.

Do not push basic completion controls to day ninety. If errors are discovered, the amendment flow must already work. If required filing elements are missing, submissions can be rejected, so data-quality checks belong in the launch baseline.

The guardrail for deferrals#

Do not defer controls your legal mapping identifies as required in markets where you are already live. Defer tuning, not release-critical or filing-critical obligations.

For each deferred item in your phased backlog, record:

- the control being deferred

- the risk created by the delay

- the interim control used now

- the owner and target date

- the evidence used to prove the interim control operated

Run pre-launch sanity checks on real payout scenarios#

Approve go-live only after end-to-end payout simulations match your written decision rules and can be explained from logs, not configuration screenshots or policy text alone.

Mirror your documented release, hold, and escalation paths. The exact scenario set, gate logic, and artifact list are internal policy choices, so define them explicitly before launch.

Before you sign off, verify that each simulation can be reconstructed from system records within the audit window your team defines, including:

- what triggered the decision path

- what control or reviewer made the decision

- what final payout state was reached

If a scenario cannot be reconstructed clearly, treat it as a potential no-go until the gap is resolved. If you need a practical workflow reference for those tests, review the Gruv docs.

Monitor the first month as a controlled risk window#

Treat the first month after go-live as a controlled risk window, not steady state, so you can catch drift before assessment windows reduce response time.

Watch the controls that fail quietly#

Track a short control-health set and review trends, not just counts:

- KPI movement in your monitoring program

- remediation aging

- evidence completeness

- upcoming scan or assessment checkpoints (including quarterly scans where applicable)

Use these as early indicators of work that is stalling or being pushed downstream. Each review cycle, sample real transactions and compare actual treatment to your disclosed policy and written decision rules. If a held or delayed transaction is later released, the reason should be reconstructable from system records and approval history.

Use regular reviews to change what is not working#

Run recurring cross-functional reviews across Compliance, Ops, Finance, Legal, and Engineering to adjust controls based on observed outcomes, not status reporting. Use review outputs to guide changes, then update escalation playbooks before small gaps accumulate.

Use clear decision logic. If KPI trends worsen while aging work is increasing, fix triage capacity, matching logic, or case routing before loosening release gates. If reviews surface higher-risk activity in a segment treated as low risk, raise that tier before optimizing speed.

Keep a jurisdiction watch with source discipline#

Maintain a regulatory-change watch list for in-scope markets. Verify legal references against official publications before acting. FederalRegister.gov is useful for monitoring, but it states that legal research should be verified against an official edition of the Federal Register.

Close month one with a compliance operating report for leadership and audit stakeholders. Include document types, named owners, key metrics, notable incidents, policy changes made, and open watch items so you have a dated, accountable evidence record. For recurring filings and operating deadlines, keep a companion Global Contractor Payment Compliance Calendar for Monthly, Quarterly, and Annual Obligations.

Conclusion#

A credible go-live checklist is not a topic list. It is a set of release gates, named decisions, and retrievable evidence that can stand up under scrutiny. Before money moves, your team should be able to answer yes to three questions:

- Do release gates block payouts when required data is incomplete? This includes identity and ownership checks, sanctions checks, and other required prerequisites for release.

- Is there a clear decision owner for hold, release, block, and suspicious-activity escalation decisions? If ownership is unclear, suspicious-activity alerts may remain unresolved.

- Can you retrieve an evidence pack for a sample payout from system records? Onboarding data, sanctions checks, risk assessments, and transaction logs should already be archived in audit-ready form.

If any answer is no, treat it as a launch blocker. If you cannot show who approved a payout, why they approved it, and what records supported that decision, you increase compliance risk, including fines, frozen funds, and reputational damage.

Use a retrieval test as an operator checkpoint. Pick a real or simulated payout and confirm you can produce the onboarding result, sanctions check result, current risk assessment, monitoring status, approver, and release action without relying on chat history or memory.

Also include payment-data quality in release controls. Even minor typos can delay or reject international payouts, and incorrect beneficiary identifiers such as IBAN, account number, or SWIFT/BIC are a major operational failure mode. One cited example shows a payment returned after five days with a $50 intermediary fee.

From there, expand with a risk-based approach rather than one uniform review path. Start with controls that prevent high-impact failures, then add depth by jurisdiction and risk profile as operations mature, including SAR handling where required and FATF Travel Rule data handling where applicable.

If your team is validating day-0 controls across multiple payout rails, talk with Gruv to confirm market and program coverage before go-live.

Frequently Asked Questions

What is a global payout compliance checklist before go-live?

It is a pre-launch control set that defines what must clear before money moves, who can approve exceptions, and what evidence you keep. Its purpose is to catch release-critical failures before payout release and turn compliance requirements into clear operating decisions.

What checks are mandatory before the first cross-border payout is released?

There is no single universal checklist for every cross-border payout program. Before first release, confirm the release-critical prerequisites for your model, including reliable beneficiary data validation and provider due diligence. If payouts involve workers or salaries, verify local engagement, payroll registration, tax IDs, and employer social security setup where required.

Who should own payout compliance decisions across Compliance, Legal, Finance, Ops, and Engineering?

The article does not prescribe one required ownership model or fixed RACI split. It recommends named people, not only teams, for each release-critical control, with separate approval authority for hold, release, and permanent-block actions plus clear cross-functional escalation and backup coverage.

What evidence should we retain to satisfy audit and regulator requests?

Retain records tied to payout compliance decisions so a reviewer can reconstruct what was reviewed, who decided, and the final payout action. That can include engagement-model analysis, jurisdiction setup checks where relevant, provider licence or permit due diligence, control review history, and supporting-document status. Set retention periods with jurisdiction-specific legal advice.

How do we avoid overbuilding controls while still meeting AML, sanctions, and tax obligations?

Start with controls tied to legal prerequisites and payout-release gates, then add depth where risk, transaction patterns, and local law justify it. The article also recommends starting with a small AML rule set your team can operate consistently, then tuning it as you learn instead of building one global pattern for every market and rail.

When should a payout be held, escalated, or permanently blocked?

The article does not give universal thresholds for hold, escalate, or block decisions. Use documented internal criteria tied to whether required prerequisites and jurisdiction checks are complete before funds move. Unresolved sanctions hits and suspicious behavior should pause or hold payout release for review, and unclear cases should escalate instead of being forced through.

Can one global policy cover every country we pay into?

No. A global policy can set baseline principles, but local rules still apply by jurisdiction. Use a global baseline plus country-specific requirements for worker engagement and payroll or tax setup, and review each new market accordingly.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bidopportunities.iowa.gov/Home/GetBidOpportunityDocument/e4fa7584-e808...trusted

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- congress.gov/crs_external_products/R/PDF/R48531/R48531.8.pdftrusted

- egrove.olemiss.edu/cgi/viewcontent.cgitrusted

- fac.gov/assets/compliance/2024-Compliance-Supplement...trusted

- federalregister.gov/documents/2026/03/27/2026-05959/regulatory-c...trusted

- federalreserve.gov/supervisionreg/guide-regulation-cc-complianc...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: