Quick Answer

Start by assigning payout actions to score bands, then enforce those actions at pre-release, release-time, and post-release checkpoints. Tie each band to a named owner in risk, compliance, finance, or ops, and log the decision path in your ledger or provider records. Build signals in layers: passive identity data, active checks, and behavior context, with MFA and KBA treated as supporting evidence. If you use anomaly detection such as Isolation Forest, manage threshold changes as controlled updates with an approver, reason, and outcome review.

What a Fraud Score for Contractor Payouts Should Cover#

Payout fraud scoring only helps when you treat it as an operating decision, not a model handoff. What matters is whether your team can turn a score into a clear payout action, with named owners, review limits, and evidence that still makes sense six months later.

That distinction matters because payment conditions change. Research on digital payment fraud shows that fixed anomaly score thresholds can deteriorate when traffic shifts or is actively manipulated. A score that looked sensible in testing can get noisy in production if payout mix, attacker behavior, or event quality changes.

This guide focuses on the parts many teams skip: payout-stage decision rules, escalation ownership, threshold governance, and audit-ready records.

Before you start#

- Define the payout decision before you tune the score.

Start with the action bands you actually need: release, step-up verification, temporary hold, or investigation. If you cannot point to the exact action tied to each band, plus who owns it, your score is still just analytics. A simple check: for any sample payout, your team should be able to answer what happens at pre-release, what happens at release time, and where that decision is logged.

- Assign ownership across risk, compliance, finance, and ops.

Payout fraud programs can break down when every team assumes someone else owns the exception. Risk may want to hold, compliance may want enhanced review, finance may need reconciliation certainty, and ops may be stuck executing the decision. If those handoffs are unclear, you get unnecessary holds on good contractors, inconsistent overrides, and growing manual queues.

- Treat threshold selection and evidence capture as first-class controls.

If you use anomaly detection, even practical approaches like Isolation Forest, do not treat the threshold as a one-time setup. The practical lesson from adaptive approaches such as TA-IFDC is that threshold choice can move with the data as score distributions evolve. You do not need that exact method to apply the operating rule. When thresholds move, the change should have a reason, an approver, a date, and a way to measure the effect.

Even if you already use vendor tooling or network-based fraud signals, that only answers part of the problem. You still need an internal record for each contested payout. It should show the event timeline, the signals used, the threshold in force, the operator action taken, and the payout reference written to your ledger or provider log. The goal is to keep payout decisions consistent and explainable as conditions change.

For examples of the behaviors your score should catch, see Top 10 Payment Fraud Patterns Hitting Freelancer and Platform Payouts.

What to prepare before you score a single payout#

Write policy boundaries, data-handling rules, and operating metrics before model work starts. Without that sequence, you can still rank risk, but you will struggle to defend payout decisions during disputes, compliance review, or later threshold changes.

Step 1. Define policy boundaries by market and program#

Create an internal decision table that states where KYC, KYB, and AML checks are required in your program, where checks are optional or risk-triggered, and who can approve exceptions. Keep this as an explicit operating rule by market, product line, or contractor program, with a named approver for each exception path.

Test it with three payouts from different markets. If your teams cannot consistently answer which checks apply, whether an exception is allowed, and who signs off, fix the policy boundary before tuning the score.

Step 2. Build the minimum document set before feature design#

Set the operating documents first, then design features. At minimum, keep:

- payout policy

- escalation matrix with named owners in risk, compliance, finance, and ops

- evidence retention policy

- tax artifact handling notes for W-8, W-9, and Form 1099 records

This prevents common failure modes in contested payouts: unclear release or hold decisions, missing approval trails, and fragmented case evidence across teams.

Step 3. Confirm data handling constraints before you decide what to log#

Fraud monitoring relies on continuous surveillance of user activity, device signals, and financial transactions, but that does not mean every raw field belongs in every workflow. Decide early which PII is masked in analyst views, which fields remain encrypted, and which risk events are allowed in logs that compliance or legal may review.

Capture only what you can retain and review safely. If your data layer is not secure, reliable, scalable, and integration-friendly, model quality alone will not make operations audit-ready.

Step 4. Lock your operating metrics before you touch thresholds#

Set the metrics that will evaluate threshold changes before you change cutoffs: fraud loss, false positives, review SLA, and payout delay. Those metrics make the tradeoff visible between fraud reduction and contractor payout experience.

Require each threshold change to include expected impact, then log actual outcomes after launch. That keeps tuning tied to operational results rather than analyst preference.

Map the contractor payout lifecycle and place score checkpoints#

Map checkpoints across the full payout lifecycle, not at one moment. Treat each checkpoint as a decision point with one owner, one action, and one durable record so initiation, execution, and follow-up can be reviewed separately.

A practical structure is to separate payment initiation or authentication from payment execution, then keep post-release monitoring distinct. That keeps controls aligned to the process actually in play.

Step 1. Split the lifecycle into three decision stages#

Use three stages: pre-release, release time, and post-release. This is usually enough to avoid mixed queues and unclear ownership.

| Stage | What you are checking | Primary actions | Minimum evidence to write |

|---|---|---|---|

| Pre-release | Payee status, account changes, velocity, policy gates | Allow, step-up verification, temporary hold | payout request ID, payee ID, triggered signals, decision and owner |

| Release time | Final send decision and provider handoff | Allow send, hold before send, escalate | internal ledger entry, provider request/reference ID, timestamp, actor |

| Post-release | Return events, disputes, anomalies, linked activity | Close, investigate, recover where possible, escalate | posting status, provider response, case ID, linked prior events |

If a score does not map to a specific next action, it is not operational yet.

Step 2. Make checkpoints rail-aware#

If you run FedNow, RTP, or Virtual Bank Accounts (VBAs), define checkpoint rules per rail in your own control map. Keep it concrete for each rail:

- the last internal point where a payout can still be held

- what provider event counts as release-time confirmation

- which post-release events auto-open investigation

Document this with payments ops, treasury, or your processor so teams do not handle the same retry differently. For rail context, see FedNow vs. RTP: What Real-Time Payment Rails Mean for Gig Platforms and Contractor Payouts.

Step 3. Define replay handling before duplicates happen#

If retries can occur, define how to classify replay versus new intent before launch. The goal is to keep one payout intent from becoming multiple risk events and duplicate reviews.

Use a consistent matching rule in policy, then test a timeout or retry scenario to confirm the second attempt attaches to the original case and ledger trail.

Step 4. Write the evidence path from request to posting#

At each stage, record where decision evidence, ledger evidence, and provider evidence are stored so cases can be traced end to end. Centralized access and reliable data matching matter here: investigators should be able to follow request, decision, provider reference, and posting outcome without stitching together disconnected tools.

For a step-by-step payout-ops comparison, see ACH vs Wire Transfer for Contractor Payouts When Platform Teams Should Use Each.

Build a signal stack that goes beyond passive identity data#

Use passive identity data as a starting filter, not the final decision for higher-risk payouts. For high-value, high-velocity, or recently changed payouts, require current evidence and recent behavior before release.

Step 1. Separate passive, active, and behavior signals#

Start with passive fields like email, phone, device identifier, and account history for early screening, but do not let them carry a high-risk decision alone. NIST SP 800-63-4 covers identity proofing and authentication as separate parts of digital identity guidance, which is a useful control boundary for payouts. In practice, treat profile consistency as one input, then require active and behavior signals before sensitive releases.

Step 2. Treat MFA and KBA as inputs, not guarantees#

Multi-Factor Authentication (MFA) and Knowledge-Based Authentication (KBA) can strengthen a decision, but they should not end the review by themselves. If other risk signals conflict, your policy should still allow a step-up check, temporary hold, or escalation. Record timestamp, challenge outcome, and session or actor context so the payout decision has usable evidence.

Step 3. Add network intelligence and normalize vendor output#

Where available, add Identity Authorization Network (IAN)-style or similar cross-account telemetry to detect linked patterns that single-account checks can miss. Keep vendor tools such as Stripe Radar mapped into a common internal risk schema so outputs stay comparable across sources. The goal is consistent decision logic, not tool-specific labels driving action.

Step 4. Set provenance and freshness standards before production#

Require each material signal to include source and event time, and define how long it remains valid for decisions. Without freshness rules, older features can be treated as current and quietly weaken controls. Include provenance and freshness fields in decision records so investigations can reconstruct why a payout was allowed, held, or escalated.

Choose a model stack your team can govern#

Use a layered stack your team can explain and operate under pressure: deterministic rules for hard policy blocks, anomaly detection for new patterns, and supervised scoring only where labels are reliable.

Step 1. Put hard policy rules in front of any model#

Make non-negotiable controls explicit rules, not model suggestions. If policy requires fresh verification after a recent payout-destination change, enforce that as a deterministic block so legal, compliance, and ops decisions stay stable even when behavior shifts.

For each blocked or held payout, confirm you can show which rule fired, the event timestamp, and the evidence record. If your decision service blends everything into one score, policy blocks can be overridden without clear accountability.

Step 2. Add anomaly detection where labels are thin or delayed#

Use anomaly detection to surface behavior your labeled fraud set does not capture yet. This matters because fraud events are rare, patterns evolve (concept drift), and confirmed outcomes often arrive late.

If you use methods like Isolation Forest, treat them as monitored detectors, not release authority by themselves. Log feature inputs, retain model version per case, and define fallback behavior before launch.

Step 3. Match model complexity to traffic volatility#

When traffic shifts by season, launch, or campaign, evaluate time-aware detection approaches so your baseline does not drift out of date. Add complexity only if investigators can review clear concept-level explanations rather than raw feature math.

That interpretability layer should translate model behavior into reviewable signals, such as unusual timing, destination-change clustering, or device novelty.

Step 4. Treat the data pipeline as part of the model, and pre-approve rollback#

Model quality depends on data quality. Feature latency, missing events, and backfills can distort risk decisions faster than algorithm choice can fix them.

If you run streaming features, for example through a DSMS-style real-time feature pipeline, record source event time, ingestion time, and verification timing for each material input. Define rollback triggers before launch so you can revert to rules-first review when data quality degrades.

How should you set thresholds without blocking good contractors#

Set thresholds as an operating control, not a one-time score cutoff. Define clear decision bands tied to actions and owners, then calibrate those bands by payout context so you can reduce fraud risk without turning normal payouts into unnecessary delays.

Step 1. Tie each decision band to an action, owner, and evidence record#

A score alone is not an operational decision. For each band, define what happens by default, who owns it, and what evidence must be logged before release or escalation.

| Decision band | Default action | Primary owner | Evidence checkpoint |

|---|---|---|---|

| Low risk | Auto-approve payout | Risk policy owner sets rules; release runs automatically | Log band, rule outcomes, model version, event timestamp |

| Medium risk | Step-up verification before release | Payments ops or trust ops | Log requested step-up and pass/fail result |

| High risk | Temporary hold and investigate | Fraud investigations, with compliance when required | Preserve event timeline, payout rail context, prior flags, operator actions |

This keeps decisions explainable under pressure and avoids inconsistent handling across ops queues.

Step 2. Use adaptive threshold logic when traffic behavior changes#

Fixed anomaly thresholds are simple, but they can degrade when traffic shifts or is actively manipulated. In fast-changing payout environments, adaptive thresholding is usually safer than a static cutoff left unchanged.

For IF-based anomaly layers, TA-IFDC-style calibration treats thresholding as adaptive rather than static post-processing. In practice, that means monitoring live score distributions and updating the decision boundary online so controls can adapt to drift while preserving precision during stable periods.

Step 3. Apply threshold policy by payout context, not one global cutoff#

A single cutoff across all payout flows is easy to run but often creates the wrong precision-recall tradeoff. Use separate threshold policies for materially different contexts, such as newly changed destinations, rail-specific behavior, or sudden velocity patterns.

This aligns with a multi-stage setup where deterministic rules and adaptive ML are coupled with dynamic threshold management to keep the precision-recall balance workable during real operational pressure.

Step 4. Review threshold performance on a fixed operating cadence#

Use a recurring review to evaluate fraud outcomes, false-positive burden, manual review load, and contractor payout delay together. If you monitor only one side of that tradeoff, threshold quality will drift.

Maintain a threshold change log with the affected segment, reason, approver, and post-change outcome so adjustments stay auditable and reversible.

Related: How to Set Up Direct Deposit for Contractor Payouts on Your Platform.

Define escalation ownership evidence packs and legal sign-off#

Thresholds only work when the next decision is explicit and documented. Define escalation ownership in writing, and default to a controlled hold when required evidence is incomplete.

Assign decision rights by role#

Set internal decision rights by role and document any allowed exceptions. In practice, that means your policy should name who can place or maintain a hold, who can require enhanced review, and who can approve policy exceptions. The critical control is consistency: every escalation should show the decision owner, escalation reason, evidence reviewed, and final outcome.

Use one standard investigation packet#

Use one standard packet so escalated payouts are reviewed on comparable records. At a minimum, include:

| Packet item | Included detail |

|---|---|

| Event timeline | From request to hold or release |

| Score components | Reason codes |

| KYC and AML status | From your internal checks |

| Prior flags | Related account history |

| Payout reference | Payout rail and provider reference |

| Operator actions | Timestamps and overrides |

If those records are missing, treat the case as incomplete and keep it on controlled hold until the packet is complete and sign-off is documented.

Add tax and identity artifacts only when relevant#

Include tax and identity artifacts only when they are relevant to the specific issue and access is authorized. Avoid attaching every W-8, W-9, FBAR, FEIE, or Form 1099 record by default.

For FEIE-related review, use IRS criteria carefully: the physical presence test is 330 full days during any 12 consecutive months, those days do not need to be consecutive, and failing to meet 330 full days fails the test regardless of reason. Also, excluded foreign earned income still must be reported on a U.S. tax return. Use those points to decide whether FEIE documentation belongs in the evidence pack, not as a standalone payout-release decision.

Run weekly controls and drift monitoring#

Run this review every week before you change thresholds. Drift in score bands or feature distributions can signal an input break, rollout side effect, or segment-mix change before it shows up as a clear incident.

Review score distributions before retuning thresholds#

Start with score-distribution movement, then decide whether thresholds need adjustment. Stripe's model-evaluation guidance explicitly includes score-distribution analysis, so this is the right first control check. If movement is abrupt, investigate the cause first instead of using cutoff changes to mask it.

Track model health and operating health together#

Keep model behavior and operations on the same weekly control page. Stripe's fraud guidance treats rules and manual reviews as part of performance improvement, and its ML operations framing emphasizes deploying models safely and frequently. If model outputs look stable but review operations are straining, treat that as a control issue, not a separate workflow problem.

Review by segment and revalidate after major change events#

Do not rely only on one blended view; compare meaningful internal segments so you can spot where global settings stop fitting local behavior. After major product, policy, or market changes, revalidate anomaly components before trusting prior settings. If alert patterns and review outcomes move sharply, pause threshold edits until you confirm whether behavior changed in the business or in the model stack.

Related reading: When Platforms Are Responsible for Contractor Tax Fraud or Money Laundering.

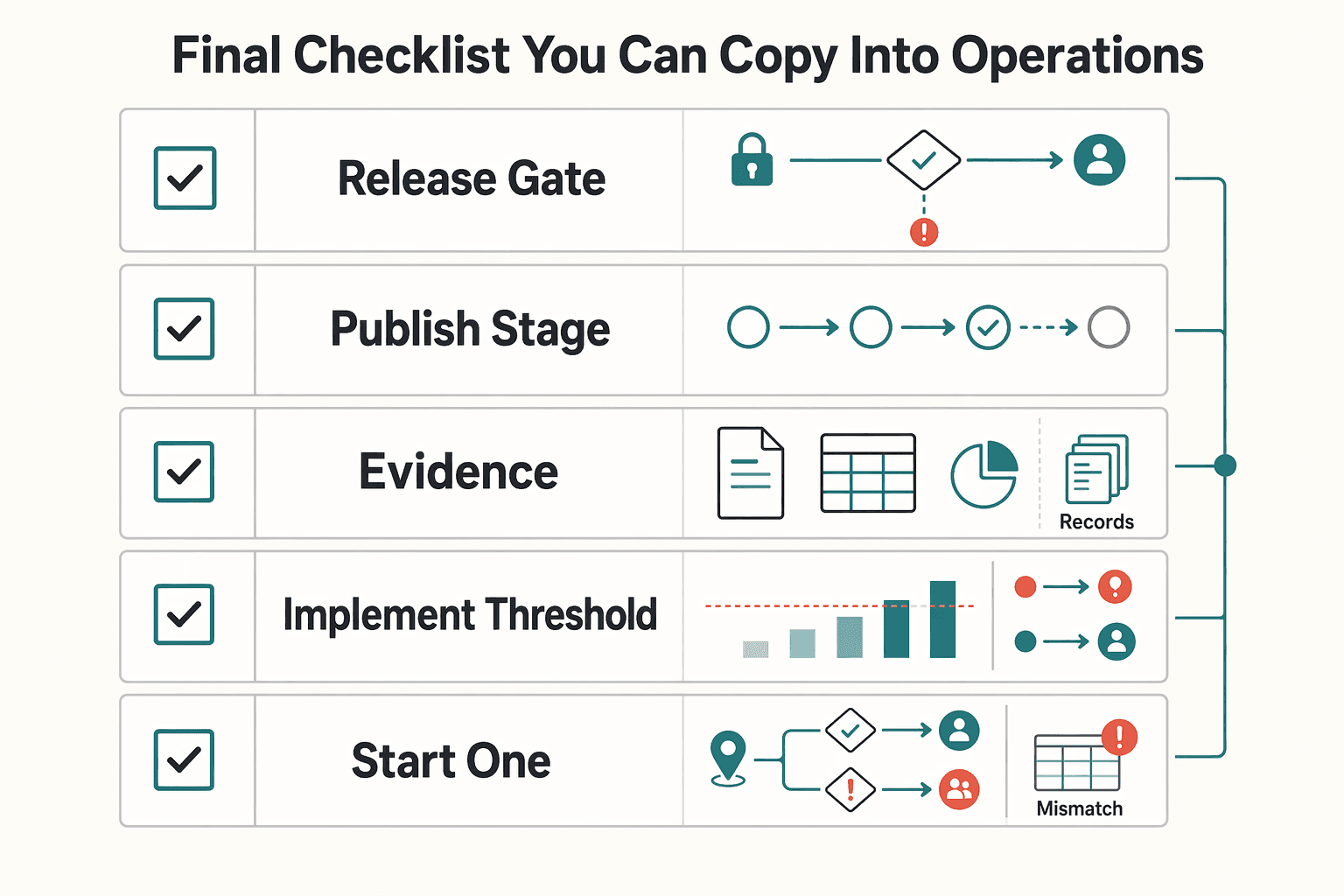

Final checklist you can copy into operations#

If you formalize one thing, formalize a written decision table with named owners. That is what makes a fraud score an auditable control instead of a stream of ad hoc exceptions.

- Confirm policy gates and ownership.

Document where KYC, KYB, and AML checks apply, who can approve exceptions, and when legal escalation is required. Keep escalation paths explicit by market or program so a held payout always maps to a clear gate, current due-diligence status, and an authorized decision-maker.

- Publish stage-based decisions for each payout flow.

Define pre-release, release-time, and post-release actions, and assign allowed outcomes at each stage (allow, step-up verification, hold, investigate). In high-volume manual workflows, this structure helps reduce mistakes, duplicate payments, and unauthorized transactions.

- Document signal inventory and model stack, including fallback and rollback.

List each signal, source, freshness expectation, and missing-data behavior. Then record decision logic order, fallback mode, and rollback triggers before launch. If vendor tooling feeds decisions, apply third-party due diligence before onboarding and throughout the relationship.

- Implement threshold governance with explicit review cadence and change log.

Set owners and a regular review rhythm, then log every threshold change with rationale, data window, approver, and backout condition. In periods of regulatory change, silent threshold edits are a control risk.

- Standardize investigation evidence packets and retention rules.

Use one packet format for serious cases (timeline, score inputs or components, control status, actions, and disposition). Set retention rules with legal or compliance rather than improvising case by case.

- Start with one market or program, validate outcomes, then expand.

Expand only after controls and staffing hold up under real volume. Use outcome quality, review load, exception volume, and evidence completeness as the expansion check.

Frequently Asked Questions

What is a fraud score for contractor payouts, and what is it not?

A fraud score is a risk input for a payout decision, not a verdict. In practice, it is one signal used to prioritize allow, step-up verification, hold, or investigation. It is not proof of fraud and should not be treated as a standalone compliance decision.

Which signals usually matter most for payout fraud decisions?

Behavioral analytics is a high-signal input because it analyzes user behavior in real time and can detect suspicious actions such as rapid navigation or inconsistent typing patterns. Vendor tooling such as Stripe Radar can also add signal by using network data to detect fraud.

When should we use fixed thresholds versus adaptive thresholds?

The source guidance here does not support a universal rule for fixed versus adaptive thresholds. What it does support is validating threshold changes with score-distribution review and precision-recall or ROC analysis, rather than reacting to one noisy period. It also supports combining model output with rules and manual reviews.

How do we set escalation thresholds without overblocking legitimate contractors?

Set escalation bands as operational decision points, then monitor false positives closely. Legitimate transactions incorrectly flagged as suspicious create alert fatigue, so reducing false positives should be a core part of threshold tuning.

What should compliance and finance review every week?

Keep model health and operating health in one shared review. At minimum, review score distributions, precision-recall or ROC behavior, false positives, and manual-review outcomes. Keep rules and manual-review feedback in the loop, since performance is framed as stronger when those controls are part of the system.

How do payout rails like FedNow, RTP, and VBAs change fraud controls?

The source guidance here does not support claiming that one of these rails is inherently riskier or prescribing rail-specific thresholds. If you need operational rail details, use separate rail documentation or a rail-specific guide such as FedNow vs. RTP: What Real-Time Payment Rails Mean for Gig Platforms and Contractor Payouts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- comptroller.war.gov/portals/45/documents/defbudget/fy2024/fy2024...trusted

- congress.gov/crs-product/R48850trusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AG_Level2_MasterV2....trusted

- dodcio.defense.gov/Portals/0/Documents/CMMC/AssessmentGuideL2.pdftrusted

- farmingdale.edu/courses/index.shtmltrusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- le.fbi.gov/cjis-division/cjis-security-policy-resource-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Bad Payouts Are Costing Your Supply in Two-Sided Platforms

Payout issues are not just an accounts payable cleanup task if you run a two-sided marketplace. They shape supply-side trust, repeat participation, and fill reliability. They can also blur the revenue and margin signals teams rely on.

FedNow vs RTP for Gig Platform Contractor Payouts

You are not choosing a payments theory memo. You are choosing the institution-backed rail path your bank and provider can actually run for contractor payouts now: FedNow, RTP, or one first and the other after validation.

Set Up Direct Deposit for Contractor Payouts Without Ops Debt

If you only pay a handful of 1099s, the product docs are often enough to get started. Once you own payouts for a contractor base, they are just the starting point. This guide is about getting direct deposit live without creating reconciliation headaches, support blind spots, or manual cleanup later.