Quick Answer

Define three buckets first: client pass-through, agency overhead, and freelancer business cost. Reimburse only costs tied to client scope, receipt evidence, and approval proof, then move them through review, invoice mapping, and payout release. Keep markup contract-led and disclosed, because pass-through is easier to defend in invoice disputes. Use duplicate-safe event handling with one idempotency key per retry path, and send approved records to QuickBooks with exceptions tracked separately.

Build a Clear Process for Client Expenses#

For an agency platform, it helps to make three decisions before freelancer expenses reach payout: what gets reimbursed, what stays agency overhead, and what should never be paid out. If you treat freelancer expenses as only a pricing question, you miss operational choices that can protect margin. A lot of freelance advice focuses on rates and pricing. Product teams usually need a tighter answer.

That distinction matters because freelancers naturally incur real business costs. Some are legitimate business expenses in the tax sense, and good bookkeeping still matters for recording, tracking, and categorizing them. For an agency platform, though, the harder problem is deciding which costs belong to the client engagement, which belong to the agency, and which stay with the freelancer as part of running their own business.

This is where client-cost reimbursement can get messy. Teams may start with a simple idea like "let contractors upload receipts," then realize they still do not have a shared rule for client pass-through, a clear evidence standard, or a reliable way to reconcile approvals against invoices and payouts. Finance can see leakage, ops may handle exceptions by hand, and engineering may patch edge cases after the process is already live.

A better starting point is disciplined categorization and controls. Categorizing expenses improves visibility into where money is going and supports accurate tax reporting. In a product setting, it also means you design the records and status changes before you design the form. If a cost cannot be traced to a client scope, supporting evidence, and a decision path, it is not ready for reimbursement no matter how reasonable it looks on first review.

This guide takes that operational view. You will work from a reimbursement flow built around clear records, status tracking, and policy gates so finance, ops, and engineering are all looking at the same state changes. The goal is not abstract best practice. It is a flow you can verify. A submitted cost should have an owner, a category, an approval result, a billing outcome, and a payout decision you can trace later without rebuilding the story from inbox threads and spreadsheet notes.

By the end, you should have concrete decision rules for the three places teams often lose control first: margin protection, payout timing, and reconciliation. If you are building or tightening this process now, the useful question is not "can we reimburse this?" Ask instead, "what record, evidence, and approval logic must exist before this can move safely from submission to client billing to contractor payout?"

Define what is reimbursable and what is not#

Define reimbursement policy before you build intake or approval screens: every cost should land in one of three buckets, client pass-through, agency overhead, or freelancer business cost.

For the freelancer-cost bucket, keep taxes on the freelancer side unless your contract explicitly says otherwise. The IRS defines self-employment tax as Social Security and Medicare taxes for people who work for themselves, and Schedule SE (Form 1040) is used to calculate that tax.

Use a policy matrix so reviewers apply the same standard every time.

| Bucket | Typical example | Minimum evidence to review internally |

|---|---|---|

| Client pass-through | Travel or software bought specifically for client work | Receipt, linked client scope line, contract clause or written pre-approval, VAT treatment flag where applicable |

| Agency overhead | Internal admin tools, team ops spend | Receipt plus internal cost owner, no client rebill path |

| Freelancer business cost | Self-employment tax, retirement contribution | Categorize as non-reimbursable, no client rebill path |

Set one hard default and enforce it everywhere: if a submitted cost cannot be tied to a client scope line and a complete evidence pack, classify it as non-reimbursable agency spend until proven otherwise.

Keep the approval checkpoint blunt: if a reviewer cannot see the scope reference, receipt, approval proof, and tax-handling note in one place, do not approve. Approving first and chasing documents later usually creates disputes and margin leakage.

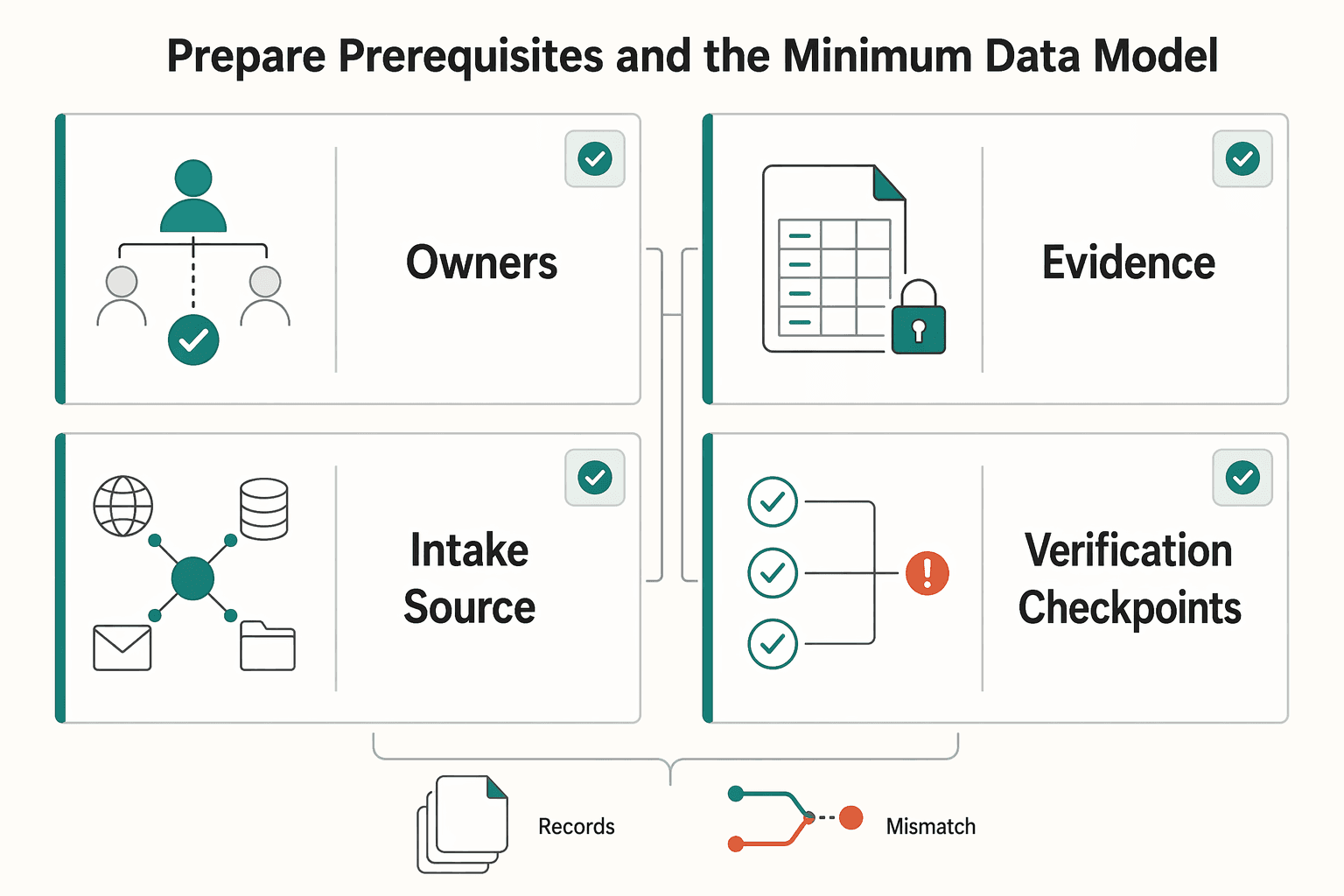

Prepare prerequisites and the minimum data model#

Before you open intake, make four decisions in writing: who owns decisions, what fields every expense record must include, which intake source is authoritative when records conflict, and which checks must pass before payout. That keeps expense management in its core lane: documented, approved, and reimbursed under policy rather than handled ad hoc.

| Decision | What to define | Detail |

|---|---|---|

| Owners | Who owns decisions | Name clear owners for workflow-state changes, policy thresholds, exception handling, and integration reliability. |

| Minimum record shape | What fields every expense record must include | Reviewers should be able to confirm who submitted the cost, what work it belongs to, what evidence was provided, what decision was made, and where the accounting record lives. |

| Intake source | Which intake source is authoritative when records conflict | Direct app forms, API intake, and imports from Airtable or QuickBooks can all work, but only if you define which system is authoritative for key fields and post-approval edits. |

| Verification checkpoints | Which checks must pass before payout | Set pass/fail checks for policy fit, duplicate detection, compliance, invoice mapping, and payout release. |

Assign owners by decision type. Name clear owners for workflow-state changes, policy thresholds, exception handling, and integration reliability. If ownership is shared without a final decider, approvals, exception queues, and payment records drift out of sync.

Lock a minimum record shape before building forms or imports. Keep the schema small but complete enough to trace each expense from submission to accounting entry. Reviewers should be able to confirm who submitted the cost, what work it belongs to, what evidence was provided, what decision was made, and where the accounting record lives.

Choose intake surfaces now, then define conflict resolution. Direct app forms, API intake, and imports from Airtable or QuickBooks can all work, but only if you define which system is authoritative for key fields and post-approval edits. Write that rule before the first mismatch.

Predefine verification checkpoints before payout. Set pass/fail checks for policy fit, duplicate detection, compliance, invoice mapping, and payout release. This reduces late-stage rework where teams unwind approvals and reconcile conflicting records after payment is already in motion.

This pairs with How to Deduct Startup Costs for Your Freelance Business.

Choose pass-through at cost or markup by scenario#

Default to pass-through at cost when you want the easiest model to defend during invoice review. Use markup only when the contract explicitly allows it and the extra charge is disclosed clearly.

Compare the two charging models before you encode billing rules#

This choice is operational: what can your team explain quickly with receipts, approvals, and invoice lines? Clear pricing communication tends to reduce friction, while hidden markup language in fine print tends to create it later.

| Model | Client transparency | Dispute risk | Margin upside | Accounting complexity |

|---|---|---|---|---|

| Pure pass-through | High. Billed amount matches expense evidence. | Lower when receipt and approval records map directly to invoice lines. | None on the expense line itself. | Lower. Reimbursement and chargeable amounts are the same. |

| Markup on expense | Lower unless markup is explicit in contract and invoice. | Higher if the client expects reimbursement at cost only. | Possible, if a handling spread is contract-backed and disclosed. | Higher. You must track vendor cost, billed amount, and retained margin separately. |

Use a simple rollout test: can a reviewer reconcile receipt, approved amount, and invoice line without interpretation? If not, markup will usually add friction rather than solve it.

Apply scenario rules from the contract, not from habit#

If a client asks for line-by-line support on reimbursed costs, start with pass-through. The goal is direct reconciliation between the receipted amount, approval record, and client invoice line.

If contract language allows admin or handling fees, markup can be viable, but only with explicit disclosure. Reimbursement policies vary by client, so store this rule at the client or project level instead of relying on a generic agency default.

Also treat this as a policy guardrail: blended service pricing does not automatically authorize markup on reimbursable items. If procurement language blocks bundled markups on pass-through costs, route coordination effort into overhead or your core service pricing instead.

Model the margin math before rollout#

Before launch, make sure each expense record carries these three values:

- Reimbursement amount: what you pay out or owe for the expense

- Chargeable amount: what you bill the client

- Retained margin: chargeable amount minus reimbursement amount minus any non-billable ops effort you attribute to that transaction

A quick logic check: if a third-party item costs $30, pure pass-through keeps reimbursement and chargeable amounts at $30, so expense-line margin is $0 before ops effort. With disclosed markup, the chargeable amount is higher than $30, but true retained margin is what remains after sourcing, verification, correction, and documentation work.

Related: How to Automate Pass-Through Expense Tracking from Clients in QuickBooks.

Build the expense lifecycle from submission to payout#

Treat this as a documented, multi-step workflow before you automate it. Start by defining reimbursable expenses, standardizing how expenses are submitted, automating approvals and reviews, and linking each item to the relevant contract or project so billing and reimbursement decisions stay defensible.

Standardize submission and force the contract link#

A consistent submission path is the foundation. If expenses arrive through different channels, normalize them into one intake process so reviewers are evaluating the same structure every time.

Just as important, tie each expense to the right contract or project from the start. Without that linkage, you have a cost record, but not a clear reimbursable decision.

Separate review from later financial handling#

Keep review outcomes explicit and keep their meaning narrow. Approval should mean the expense passed policy and contract review, not that every downstream financial step is already complete.

This separation reduces cleanup later. When review and downstream handling are treated as different stages, teams can resolve exceptions without rewriting earlier decisions.

Record transitions so decisions are traceable#

As the item moves from submission through review and reimbursement handling, record each transition clearly. A traceable history makes it easier to reconcile records, explain decisions, and resolve disputes without relying on memory or side-channel notes.

The practical standard is simple: at any point, a reviewer should be able to see what was submitted, how it was reviewed, and how that decision connected to contract-backed reimbursement handling.

Add compliance and tax gates without freezing operations#

Keep intake moving by holding reimbursement release, not expense submission, when compliance or tax documentation is incomplete.

| Item | When checked | Note |

|---|---|---|

| KYC/KYB/AML | Before release | Use a decision table with only two outcomes: blocks payout or flags for manual review; keep overrides limited to payout exceptions. |

| W-8 | Checked at payout release | Treat as a profile dependency where your program supports U.S. tax reporting, not as a receipt-level review judgment. |

| W-9 | Checked at payout release | Treat as a profile dependency where your program supports U.S. tax reporting, not as a receipt-level review judgment. |

| Form 1099 | Checked at payout release | Treat as a profile dependency where your program supports U.S. tax reporting, not as a receipt-level review judgment. |

| FEIE | Reporting support workflow | If you track FEIE, capture date windows and foreign tax home evidence; one qualification path uses 330 full days during any period of 12 consecutive months. |

| FBAR | Reporting support workflow | Keep the label accurate as Report Foreign Bank and Financial Accounts. |

Split blocking checks from review flags#

Define one decision table for KYC, KYB, and AML with only two outcomes: blocks payout or flags for manual review. Keep overrides limited to payout exceptions, and define the approving role in policy.

Store every override on the expense or payout record (actor, timestamp, reason, linked case). Avoid handling overrides in Slack or email so release decisions stay auditable.

Separate tax profile completeness from tax advice#

Where your program supports U.S. tax reporting, treat W-8, W-9, and Form 1099 as profile dependencies checked at payout release, not as receipt-level review judgments.

Keep FEIE and FBAR in reporting support workflows. For FEIE, the IRS states that qualifying individuals still file a U.S. return reporting the income, eligibility includes a foreign tax home, and one qualification path uses 330 full days during any period of 12 consecutive months (not required to be consecutive). If you track FEIE, capture date windows and foreign tax home evidence as reporting inputs.

Do not hardcode a single FEIE cap year; IRS maximums are adjusted annually for inflation (for tax year 2026, the published maximum is $132,900 per person). For FBAR, keep the label accurate as Report Foreign Bank and Financial Accounts.

Expose requirement timing in the product#

Prevent over-blocking by labeling each requirement as required now or required before payout, and attach the program/jurisdiction context to each rule.

Before release, the payout checkpoint should confirm: payout-eligible KYC/KYB/AML status, required tax profile completeness for that program, logged override rationale (if any), and no open compliance review.

Related reading: Mental Models for Freelance Strategists to Make Better Client and Pricing Decisions.

Connect product events to accounting and client billing systems#

Make each approved expense traceable before it reaches accounting systems, so finance does not have to reconstruct events from manual exports. That keeps workflows scannable and reduces the budget/compliance risk that comes from receipt and data-handling errors.

Define the handoff contract#

Keep a small, explicit record contract across product, billing, and reimbursement, including expense ID, approval decision, client invoice line ID, and payout reference. Store it on the record itself so a reviewer can quickly trace what was approved, how it was billed, and how it was reimbursed.

Send a minimal accounting package and track exceptions clearly#

If QuickBooks is your accounting destination, send a minimal package from the expense workflow: approved expense data, billing treatment, and the linked identifiers needed for follow-up. Keep exception handling in a clearly labeled ops queue (for example, Airtable) and reference the canonical expense ID so issue resolution does not become a second source of truth.

Reconcile routinely and document off-system edits#

Use routine reconciliation to compare invoice totals, reimbursement totals, and unresolved exceptions so finance keeps current visibility instead of working across silos. Set ledger-journal tie-out formulas and compensating-journal procedures in your own accounting policy and require a recorded reason for any off-system adjustment.

For a step-by-step walkthrough, see Freelance Client Retention: Weekly Systems for Repeat Work and Long-Term Relationships.

Handle the failure modes competitors ignore#

After your accounting handoff is in place, prevent bad states from leaking into billing or payout by routing failures into explicit exception states instead of editing records in place.

| Failure mode | Action | Record detail |

|---|---|---|

| Missing receipt | Move the item to an evidence-review state and pause export until evidence is complete. | Keep who flagged it, when, and whether a missing-receipt declaration or replacement file was provided. |

| Duplicate intake or retries | Log processed event IDs and ignore repeats; reuse the same idempotency key across retries. | The same idempotency key should be reused across retries within the 255-character limit. |

| Partial approvals | Preserve approved and denied line-item outcomes in the audit trail. | Do not rewrite the original decision into a single final total. |

| Payout failure or hold | Reopen reimbursement resolution and track payout status independently from billing status. | A payout.failed event is a payout-state problem, not automatically a billing-state reversal. |

| Expired FX quote | Request a new quote and log the decision path. | An expired quote can return a 400 response; keep both quote IDs, timestamps, and approver context. |

- Move missing-receipt cases back to evidence review.

If an approved expense loses its receipt or the file is unreadable, move it to an evidence-review state (for example, pending_evidence) in your model and pause export until evidence is complete. Receipts are part of the proof layer, so approval is not enough when evidence is missing. Keep auditable metadata for who flagged it, when, and whether a missing-receipt declaration or replacement file was provided.

- Deduplicate event intake and make retries replay-safe.

Treat duplicate risk at both the expense layer and the event layer, then protect write actions with idempotency. Duplicate transactions can cause overpayment, and webhook endpoints can receive the same event more than once, so log processed event IDs and ignore repeats. For create or payout actions, reuse the same idempotency key across retries (within the 255-character limit) so retries are recognized as the same request.

- Store partial approvals as snapshots, not overwrites.

When reports are partially approved or rejected, preserve both approved and denied line-item outcomes in the audit trail. Do not rewrite the original decision into a single final total, or you lose reason codes, denied amounts, and reviewer context.

- Handle payout failures without collapsing billing state.

When payouts fail or are held, reopen reimbursement resolution, assign ops follow-up, and track payout status independently from billing status. A payout.failed event is a payout-state problem, not automatically a billing-state reversal. In flows where a failed payout disables the external account, keep that follow-up visible until account details are corrected.

- Reject expired FX quotes and requote with traceability.

Do not disburse on an expired FX quote; request a new quote and log the decision path. Attaching an expired quote can return a 400 response, so keep both quote IDs, timestamps, and approver context in the record. If disbursements may sit before execution, choose quote windows deliberately (such as 1-hour or 24-hour) and still log rate changes.

If you want a deeper dive, read How to Handle Billable Expenses in QuickBooks.

Conclusion#

The setup that holds up is not smarter pricing advice. It is clear policy boundaries, disciplined bookkeeping, and a payout path that can survive disputes and tax review without anyone rebuilding the story from email and chat. If you want this process to stay clean, make every reimbursement decision traceable from scope to evidence to billing to payout.

- Define policy boundaries first.

Write a simple matrix for reimbursable client expense, agency overhead, and non-reimbursable freelancer business cost, then attach the evidence each one needs. Your checkpoint is practical: a reviewer should be able to link every approved cost to a client scope line, a receipt or invoice, and a business purpose without asking the original submitter. If that link is missing, treat it as overhead and do not rebill it.

- Map every status change to a durable record.

Your lifecycle can be simple, but it needs to be explicit: submitted, reviewed, approved or denied, invoiced, funds confirmed, reimbursed. If you use asynchronous updates, add duplicate-safe controls on any action that can trigger reimbursement, and map each state change to a durable system of record so reconciliation is deterministic later. The test is straightforward: one approved item should still produce one payout outcome even if retries fire or notifications arrive twice.

- Place compliance and tax gates where they block the least work.

Hold payout release when required checks or documents are missing, but do not freeze expense intake and review unless your program rules require it. For U.S. payees, Form W-9 is used to request the correct name and taxpayer identification number, and the IRS says the completed W-9 should be kept in your files for four years. When nonemployee payments reach the reportable threshold amount, Form 1099-NEC is the form you need to plan for. For compliance checks, keep the rule simple in product terms: show what is required now versus what is required before payout.

- Connect client rebilling and bookkeeping outputs early.

Push approved rebill lines and reconciliation outputs into your primary accounting system, and use a separate tracker only for exceptions if you already rely on one. The red flag is when finance starts correcting numbers outside the main record and nobody can tell which figure is authoritative. Your monthly tie-out should show that invoice totals, reimbursement totals, and unresolved exceptions all reconcile back to your source-of-truth records.

- Review the signals that expose hidden cost.

Check margin leakage, dispute volume, duplicate attempts, and payout return rate every month, with an owner for every spike. Also watch your realized average rate, defined as total dollars received divided by total hours worked, because hidden management costs can raise the total cost of using external resources even when spend looks controlled. In one AgencyAgile case-study summary, scope and work were underestimated by 25-35% on average, so do not assume a clean reimbursement queue means the economics are healthy.

Frequently Asked Questions

What counts as a reimbursable client expense versus agency overhead?

As a practical rule, treat costs tied to specific client work as client expenses and treat general operating costs as overhead. Keep records clear and categorized, and keep business and personal spending separate to avoid accounting and tax issues.

Should freelance agencies mark up client expenses or pass them through at cost?

The grounding here does not set a universal markup rule. Use your contract terms, and make invoice treatment explicit so the client can clearly see how expenses are handled.

What are the minimum fields required to track and rebill client costs reliably?

The key requirement is disciplined tracking and categorization so spending visibility and tax reporting stay clear.

How do you prevent duplicate reimbursements when webhooks retry?

Keep your expense records consistent and review reimbursement outcomes so the same cost is not processed twice.

Which records are mandatory for audits, disputes, and finance sign-off?

Exact requirements vary by country and accounting process. At minimum, maintain organized, categorized records and a clear business-versus-personal split.

How do FX timing and payout holds change when reimbursement should be released?

For cross-border purchases, FX payments can affect your final cost. Understanding and managing FX timing helps with cost control and profitability, so review the economics before finalizing reimbursement decisions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- cooperativecomputing.com/blog/outsourcing-vs-inhouse-digital-marketin...external

- emburse.com/resources/guide-to-tracking-expenses-for-sma...external

- financialmodelslab.com/blogs/startup-costs/freelance-data-analysis-...external

- oysterhr.com/library/best-expense-management-software-for...external

- paulmaplesden.com/freelance-guides/freelance-business-expensesexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Handle Billable Expenses in QuickBooks

**Treat QuickBooks billable expenses as a reimbursement system, not just a bookkeeping feature, so you recover client project costs through invoices instead of absorbing them.**

How to Automate Pass-Through Expense Tracking from Clients in QuickBooks

If you want better control of client-related costs in QuickBooks, focus on one outcome: costs are tracked clearly, reviewed, and billed intentionally so margin does not leak. This is not generic bookkeeping. It is a reimbursement control process with manual checkpoints before anything reaches an invoice.

Using Airtable as a CRM for a Solo Marketing Consultant

**[Airtable](https://www.airtable.com/) can work for consultants when you run it as one connected system, not one bloated table.** If your client work is spread across email, notes, spreadsheets, and memory, it gets harder to prioritize outreach and keep conversations moving.