Quick Answer

Start by treating instant payout as a priced product, not a default entitlement. For embed financing options marketplace instant payout, set one plain-language SLA, model per-event and per-dollar margin after provider fees, and enable speed only for verified connected accounts that pass eligibility checks. Then keep a scheduled fallback path active and monitor failed and returned payouts through reconciliation exports. If contribution turns negative or exception volume spikes, pause expansion and tighten cohort rules before scaling.

Why instant payout should be treated like a margin product#

Step 1 Treat payout speed as a pricing decision#

You are not choosing a nice-to-have checkout feature. You are deciding how your marketplace gets paid, what risk it absorbs, and whether faster seller access to cash strengthens or weakens your take rate.

That matters because instant payout is not free acceleration. It is usually a payout option that sends funds to eligible bank accounts or debit cards within minutes, often appearing within 30 minutes, and it comes with a fee. Platforms can use that speed to open a new revenue stream and improve seller or worker retention, but the cost sits on every transaction that uses it. If you cannot say who pays that fee, what margin remains after it, and who owns the exceptions, you are not launching a feature. You are choosing a monetization and risk posture.

A simple checkpoint at this stage is to write down one sentence that finishes this phrase: "We offer faster payout because..." If the answer is only "users want it," the business case is still incomplete.

Step 2 Separate payments, payouts, and finance exposure#

Keep the boundary clean from day one. Embedded payments are the pay-in capabilities built directly into your product. Embedded payouts are the disbursement layer that sends funds out to sellers, creators, or contractors. Embedded finance is broader. Here, it starts to matter when payout timing introduces working-capital considerations or a real risk-position decision.

Be strict about those lines because teams often bundle all three into one roadmap item and lose sight of what actually makes money. The pay-in flow may earn one margin profile, the payout path may carry a different cost profile, and any earlier-access promise can change your risk exposure. Your product spec and finance memo should show those lines separately. If they do not, support commitments and profitability assumptions can drift quickly.

Step 3 Define the promise in margin terms#

The right promise is not "faster payouts at all costs." It is "faster payouts that improve growth without quietly compressing take rate." Take rate is the percentage of fees your platform captures from transactions. Instant speed only works when fee capture, retention impact, and operating cost make sense together.

Use market examples as a warning, not a benchmark. One provider cites instant-payout fees of 1% in most countries and 1.5% in the United States, Australia, and New Zealand. Those numbers are enough to show the issue. On thin-margin transactions, speed can consume a meaningful share of platform revenue before other operating costs are counted.

Before build, model one base case and one stress case that include current take rate, projected instant-payout adoption, and per-transaction fee assumptions. One failure mode is straightforward: the marketplace markets "instant" broadly, usage spikes, and the platform can end up subsidizing cash access while collecting too little in return. This guide is about avoiding that outcome.

Related: How Accommodation Rental Platforms Pay Hosts: Payout Architecture for Short-Term Rental Marketplaces.

Define the product boundary before you build#

Step 1 Separate the layers in the spec#

Define the boundary first: embedded payments is pay-in, embedded payouts is disbursement to external accounts for connected accounts, and embedded finance begins when you promise earlier access to funds or take on working-capital exposure.

Keep payout logic out of checkout scope. Put fund splitting, connected-account routing, and payout creation in the payout layer. Then map pay-in capture, ledger posting, transfer or split, and payout instruction as separate events.

Step 2 Define instant payout with a clock#

Treat "instant" as a timed promise, not a marketing label. Set a concrete settlement window for each payout path, and state which paths are instant versus on a standard payout schedule.

Use explicit exception states in the same definition: pending, standard scheduled, and failed. Call out payout.failed directly, and note that some failed payouts require updating the connected account's external account details before payouts can resume.

Step 3 Set one plain-language SLA per payout path#

Give each payout path one short SLA that product, ops, and support all use verbatim. For example: "Instant payout: eligible transactions are sent for payout immediately and typically settle within 30 minutes; if eligibility or destination account checks fail, funds move to the standard payout schedule."

Then check for consistency across UI copy, support macros, and incident notes. If the wording differs by channel, your payout promise is already drifting.

For a step-by-step walkthrough, see How to Embed Payments Into Your Gig Platform Without Rebuilding Your Stack.

Prepare the operating inputs your team will need#

Once the SLA language is fixed, this is an operating-readiness check: do not launch instant payouts until you can measure margin impact, trace money movement end to end, and hand finance a sign-off pack they can audit.

Step 1 Capture the baseline economics#

Start from production reality, not a launch forecast. Build one baseline view by payout type with take rate, direct payout cost, support burden, and failure/retry overhead.

Use your actual current payout cadence as the comparator. In some setups, connected accounts are paid on a daily rolling basis; in others, payouts are monthly, and terms like Net 45 or Net 60 push timing further out. If you benchmark against a vague "standard payout," you will usually overstate speed value and miss support cost.

Before launch, you should be able to answer for each payout type, from one consistent dataset: what you earn, what you pay, and what breaks most often.

Step 2 Document the live money flow artifacts#

Write down the exact artifacts and events already moving money today. At minimum, document connected accounts, split instructions (fund-splitting rules), the pay-in confirmation event, and payout status events after payout instruction creation.

Be strict about split instructions. Funds and fees must be booked to the correct balance accounts; if instructions are missing, the full transaction amount and fees can default to the marketplace liable account. That can create accounting drift and seller-balance confusion fast.

Make payout monitoring webhook-driven from day one. A practical test is to trace one transaction from pay-in capture to ledger posting, split booking, payout creation, and final payout status. Also assign explicit ownership for errored payouts, since scheduled payouts can stop until external account details are fixed.

Step 3 Assemble the finance sign-off pack#

Your sign-off pack should show that faster payout access does not weaken controls. Include payout-enablement policy gates, including KYC requirements, one reconciliation owner, one incident owner, and the audit exports finance will use post-launch.

In most cases, the key artifact is the payout reconciliation report, because it maps bank payouts to underlying payment batches and supports CSV export for review. That is usually the file finance uses to confirm you accelerated access to funds without blurring what was earned, held, or paid out.

Price instant payout so it funds itself#

Price instant payout as a speed product with a hard margin rule: if projected fee capture cannot cover higher real-time payout cost, failed-payout handling, and added support load, keep it limited to a narrower cohort first.

Step 1 Anchor pricing to the baseline you already run#

Use your current payout schedule as the baseline. In the cited Stripe US context, the standard schedule is 2 business days for free, while Instant Payouts moved from 1% to 1.5% per payout starting June 1, 2024. Square lists instant/same-day transfer speed at 1.95% of amount.

This is your first test: if your fee is below incremental cost, instant payout is a subsidy, not a self-funding product. Track contribution both per payout event and per dollar paid out so hidden margin leakage does not get masked by volume.

Step 2 Match the fee model to your payout shape#

Choose the model that follows your cost driver:

- Flat fee: simple, but can under-recover on larger payouts and feel expensive on smaller ones.

- Percentage fee: aligns to payout amount and public speed-pricing patterns (for example, 1.5% or 1.95%).

- Tiered fee: lower unit price at predefined volume levels; useful with stable cohort behavior, but adds threshold complexity.

- Blended fee: fixed plus variable; fits mixed event-driven and amount-driven cost.

| Payout path or pricing model | Direct cost | Expected failure mode | Support load | Net contribution to take rate |

|---|---|---|---|---|

| Standard schedule, 2 business days | Baseline can be free on Stripe's standard schedule | Delay complaints more than urgent payout failures | Baseline timing questions | Strong baseline for comparison because speed cost is minimal |

| Instant payout priced as a percentage | Variable cost tied to payout amount; public references include Stripe US 1.5% and Square 1.95% | Failed or rejected payouts appear in failed payout reporting | Retry and payout-status ticket load | Works when charged percent clears direct cost plus support burden |

| Instant payout priced as a flat fee | Fixed revenue per payout while underlying cost can still vary | Under-recovery on larger payouts; pushback on smaller payouts | More fee-fairness tickets | Best fit only when payout sizes are tightly clustered |

| Instant payout with blended or tiered pricing | Fixed + variable, or unit-price shifts by volume | Mis-billing, wrong tier assignment, threshold confusion | Higher billing-explanation load if statements are unclear | More stable when payout count and payout value vary |

Use payout reconciliation reporting, including Failed payouts, to validate whether your pricing assumptions hold in production.

Step 3 Stress-test payout size patterns and keep revenue lines separate#

For small, frequent payouts, margin is often more sensitive to event count than value. Retries, failed destination details, or support contacts can consume most contribution per event, so pilot on a limited cohort and monitor per-event margin directly.

For larger, less frequent payouts, sensitivity shifts toward amount-based pricing. Check method constraints early too: Square documents a $25 minimum balance after fees and a $10,000 maximum transfer size for instant transfers.

Keep reporting split between two revenue engines:

- Speed revenue: charges for faster access, with providers describing funds as typically settling within 30 minutes.

- Coverage revenue: expansion from broader reach, such as 195 countries, 135+ currencies, and 100+ payment methods.

If those are bundled into one line, you cannot tell whether margin improved from speed pricing or from wider destination coverage.

For more on the supply-side impact of payout speed, see How to Use Payout Speed as a Competitive Advantage to Attract Top Contractors.

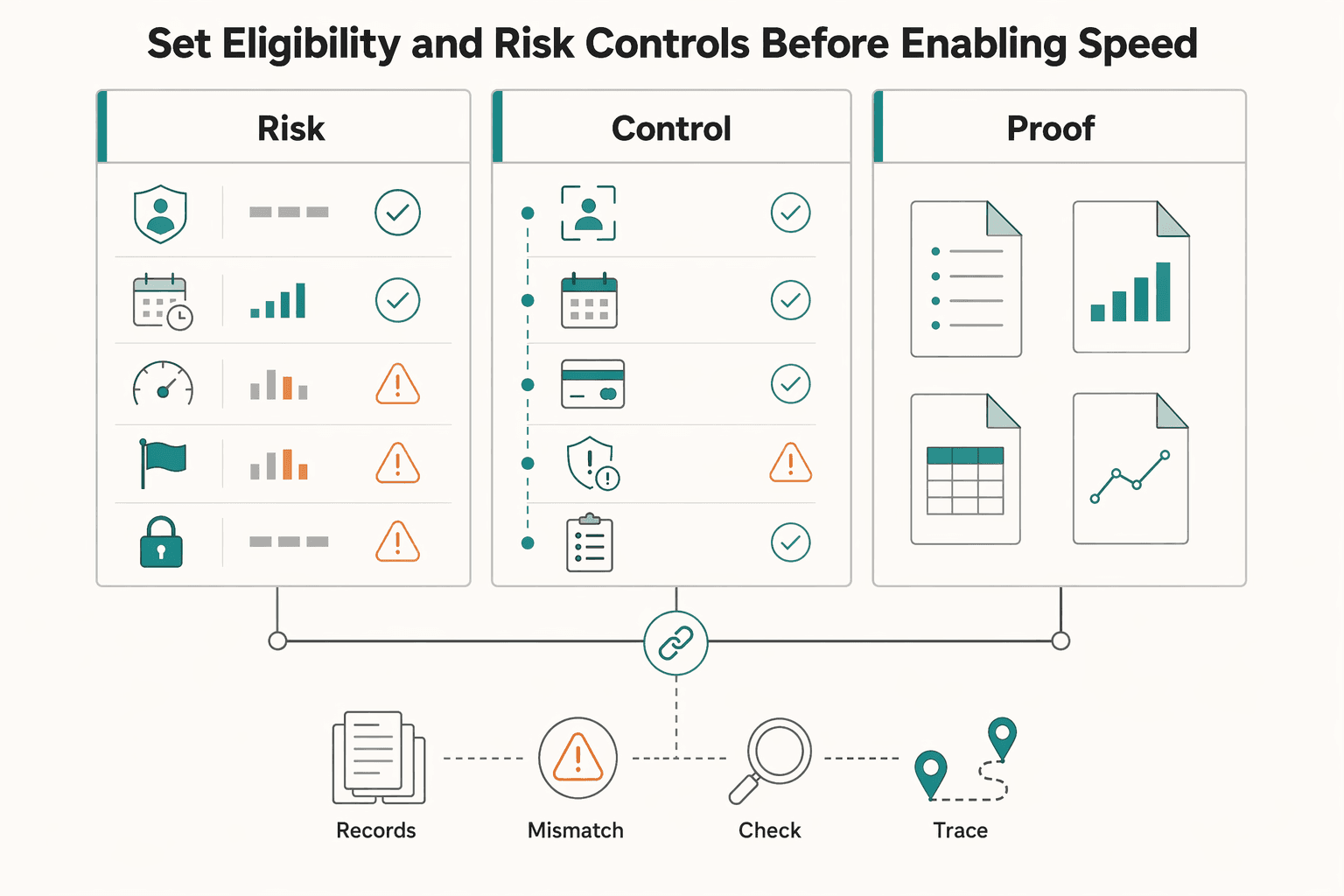

Set eligibility and risk controls before enabling speed#

Instant payout should be an earned option, with a predefined fallback to scheduled settlement when risk increases.

Step 1: Set eligibility in a strict order. Start with verified account data. Connected account requirements vary by location, business type, and requested capabilities, so confirm the account can receive funds before you consider performance signals. Then layer account tenure, transaction quality, dispute or refund flags, and current compliance status. If verification data is incomplete or a compliance check is unresolved, keep the account on scheduled payouts. Store which rules passed, failed, and whether the block is temporary.

Step 2: Tie eligibility to active risk controls. Qualification is not permanent. Use hold/release logic, including reserves when needed, because refunds, disputed amounts, and related fees can be debited from your platform balance. Add velocity controls over defined time windows to catch abnormal patterns. If your provider exposes account-level risk signals, route high-risk accounts to manual review instead of leaving instant payout on by default; for example, Stripe documents review logic like account_risk_level = 'highest' and labels "highest" at 90% probability and "elevated" at 50%.

Step 3: Define fallback rules before launch. Write explicit if X, do Y rules. If failures or reversals breach your internal tolerance, automatically remove instant access and move the account to the provider's predetermined payout schedule until review is complete. Be precise about the fallback window: scheduled settlement exists even when instant is available, and Adyen's default Sales day payout uses a two-day delay with a sales day from 00:00 to 23:59.

Step 4: Keep decisions auditable. For each eligibility change, log account ID, rule outcomes, risk inputs, timestamp, decision source, hold amount, if any, release condition, and assigned settlement window. That record lets support explain eligibility changes and lets finance reconcile cash-timing shifts without rebuilding events from raw logs.

For a broader payout strategy view, see Two-Sided Marketplace Dynamics: How Platform Supply and Demand Affect Payout Strategy.

Build the money flow so finance and ops can trust it#

Do not enable instant payout until one pay-in can be traced cleanly from capture to ledger to payout instruction.

Step 1 Map the sequence as separate money events. Keep collection and allocation as distinct steps, not one blended action. In a split-funds model, the platform charge is decoupled from transfers to connected accounts, and one captured payment can be allocated to multiple recipients. Make the sequence explicit: pay-in captured, ledger posted, funds allocated by fund-splitting rules, then payout instruction created.

For any transaction, finance should be able to see the provider payment reference, ledger entry ID, allocation result, and payout instruction ID in order.

Step 2 Make retries replay-safe at both layers. API retries should use idempotency keys, and webhook consumers should suppress duplicate events. Idempotency keys can be up to 255 characters and can be pruned after at least 24 hours.

That is only one layer. Webhook endpoints can receive the same event more than once, and undelivered events can be resent for up to three days. Store processed event IDs and block reprocessing so replayed deliveries do not create duplicate internal side effects.

Step 3 Build a reconciliation workflow people can use. Reconciliation should connect provider references, your ledger, and exported finance reports. Adyen's Settlement details report is designed for transaction-level reconciliation of settled and paid-out transactions.

Make the evidence visible and exportable. At minimum, each payout should link to the original pay-in reference, ledger posting timestamp, split allocation amounts, payout status, and the report line used for month-end review.

Step 4 Define exception ownership before launch. Write clear handoffs for unresolved or unmatched transactions. Product owns intended state and seller-facing behavior. Engineering owns event processing, idempotent execution, and repair paths for broken record links. Payments ops or finance ops owns daily review of unmatched, delayed, or reversed items and escalation when records do not reconcile.

Choose payout rails and routing by market reality#

Pick rails by corridor reality, not internal preference: use instant where it is supportable and priced intentionally, and keep a reliable non-instant fallback live in every market.

Step 1 Compare rails by speed, cost, and delivery behavior#

| Rail | Timing | Constraint |

|---|---|---|

| Credit cards (instant payout) | Any day/time; typically settle within 30 minutes | Each instant payout carries a provider fee |

| Pay by bank | Europe instant credit transfers: within 10 seconds; US Same Day ACH: settles three times daily | Same Day ACH has a $1 million per-payment cap |

| Interac e-Transfer (Canada) | Often near-instant; can take up to 30 minutes | Timing depends on the bank or credit union |

- Credit cards (instant payout): useful as an always-on premium path. Instant payouts can run any day/time and typically settle within 30 minutes, but each instant payout carries a provider fee, so this is usually a paid acceleration option rather than a universal default.

- Pay by bank: varies by region and rail. In Europe, instant credit transfers are designed to make funds available within 10 seconds; in the US, Same Day ACH settles three times daily with a $1 million per-payment cap.

- Interac e-Transfer (Canada): often near-instant for recipients using online banking in Canada, but transfers can take up to 30 minutes depending on the bank or credit union.

Step 2 Route by destination market and payout type#

Route using destination country, local currency, and payout type. For instant payouts, local-currency support is a hard constraint in each country.

| Market | Relevant route | Key constraint |

|---|---|---|

| Australia | Fast-payments infrastructure exists (NPP, launched February 2018) | Provider's supported route decides what you can offer |

| Canada | Interac is market-relevant | Timing is bank-dependent |

| Europe | Instant-bank capability exists | Coverage depends on provider and corridor |

| China | Cross-border payout flows can require declarant information | Regulatory fields can block payout flows before rail speed matters |

Step 3 Offer instant selectively and keep fallback rails active#

Not every corridor should carry the same speed promise. Some cross-border routes are not self-serve outside listed regions, and cross-border payouts can add explicit fees, for example, 0.25% in the cited provider guide. Where real-time routes are costly or inconsistent, keep instant as a selective option and default the broader base to a dependable local bank payout.

If your only route in a market is the fastest route, your payout product is fragile. Keep a non-instant bank path live for recovery, especially in corridors with extra compliance fields or uneven provider coverage.

Launch in controlled phases with hard verification checkpoints#

After routing is set, do not enable instant payout for everyone at once. Launch as a canary: a partial, time-limited rollout to a much smaller production subset, then expand only when the results support it.

Step 1 Start with a narrow, low-risk cohort#

Start with a small cohort so ops can verify payout behavior end to end, not just top-line completion. Track each payout state (processing, posted, failed, returned, canceled) and confirm each state reconciles to your ledger and support workflow.

Do not treat early completion rates as proof the launch is healthy. Some payouts are returned later, and returns are typically seen within 2-3 business days, so same-day success alone is not enough for expansion.

Step 2 Gate each expansion on diagnosis, not averages#

Before each cohort expansion, run a go/no-go check across:

- SLA adherence

- Failure and return reasons

- Manual-review load

- Net margin effect

Use exception diagnosis, not averages, to decide next steps. If you are expanding into a high-risk region or high-value segment, add pre-capture manual review for the payments feeding those payouts, because errors are harder to correct after instant funds are sent.

Step 3 Run a post-launch review against auditability and support load#

Treat "faster payouts" as necessary but not sufficient. Confirm payout speed improved without degrading auditability, overwhelming support, or creating a 24x7x365 operating load your team cannot handle.

If support volume rises, reconciliation quality slips, or review queues back up, pause expansion and fix the control point before widening rollout.

Related reading: Platform Take Rate Optimization: How to Set Marketplace Fees Without Losing Liquidity.

Make the decision with a copy-paste launch checklist#

Launch instant payout only after all six checks pass together; treat this as a go/no-go checklist, not a feature checklist.

- Document the product definition.

Use one plain-language SLA for instant payout and one for standard settlement. Define instant payout as an accelerated option to eligible destinations, available any day or time, with funds typically settling within 30 minutes, and define the baseline schedule as Daily, Weekly, Monthly, or Manual. Confirm support, product, and finance use the same wording for timing, eligibility, and fallback behavior.

- Check unit economics by payout method and cohort.

Run the math at payout-method level, not only blended marketplace margin. Include per-use instant payout fees plus retries, support load, and reconciliation effort for each cohort you plan to enable first. If contribution turns negative for a cohort, keep access narrow until pricing or cost structure is fixed.

- Enable controls before speed.

Make eligibility rules, hold/release logic, and exception ownership operational before launch. Verify bank-account identity data, since mismatches can lead to rejected payouts. Assign clear owners for approval, pause decisions, and returned-payout handling.

- Test operations with reconciliation evidence.

Finance should be able to match payouts to underlying transactions through a payout reconciliation report or equivalent export that preserves payout-to-transaction linkage. Validate returned-payout triage and require ops to review the explicit return reason in dashboard workflows.

- Agree rollout gates in writing.

Start with phased cohorts and predefine verification checkpoints and executive stop/go criteria. Track SLA performance, failure reasons, manual review load, and margin impact at each phase. For regional expansion, include provider-specific readiness checks because requirements can include local entity setup, compliance approval, and extra configuration.

- Set one launch date only after checks 1-5 pass.

Have product, finance, engineering, and payments ops sign off on the same checklist, then set the date. If any team is still relying on manual workarounds, delay launch.

Frequently Asked Questions

What is instant payout as a product in a marketplace context?

Instant payout is a faster-access option layered on top of your normal payout setup, letting connected accounts access available balance funds immediately after a successful charge. In supported cases, funds typically settle to the associated bank account within 30 minutes, and requests can be made 24/7, including weekends and holidays.

When should a marketplace offer instant payout instead of standard settlement?

Offer it when faster access has clear seller value and you can support the extra cost, exceptions, and support load. If your fee model does not absorb the provider’s per-use instant payout fee, keep it as an optional upgrade or limit it to a narrow cohort first. Standard settlement is still the better default when reliability, low ops overhead, or broad destination coverage matters more than speed.

How should we price instant payout without eroding take rate?

Treat it as a priced acceleration product, not a free feature. Providers can assess a fee on each instant payout, so your pricing has to cover direct payout cost plus operational overhead like support and reconciliation. If that math does not hold at the cohort level, do not widen access just to match a competitor’s UX.

Who should be eligible first for instant payout?

Start with connected accounts that use an eligible debit card or bank account and that your team can support operationally. That destination check matters because instant payouts are not available for every payout endpoint. Before enabling speed, confirm the seller’s destination type is supported and that your support team can trace payout status from instruction to posted or returned.

What causes instant payout failures most often in production?

Incorrect destination information is a common cause of returned payouts. A closed bank account is especially painful because the money can take up to 5 business days to return, which can delay reconciliation. The failure mode to watch is not just “failed” at send time, but delayed returns after an apparently clean request.

Can we offer instant payout consistently across global markets?

Not consistently enough to assume one global experience. Availability varies by country, bank or card support, and local rules, and instant payouts in each country must use the local currency. If you operate across markets, keep a fallback path to standard settlement rather than promising universal instant access. For more on seller payout variation by market, see How to Get Paid on Amazon Marketplace: Payout Options for International Sellers.

What records do finance teams need for auditability and reconciliation?

At minimum, finance needs payout-to-transaction matching and per-transaction cost visibility for reconciliation. The exact documents that matter most are a payout reconciliation report for matching bank payouts to included transactions and a transaction-level settlement details report for per-transaction costs and reconciliation. If you cannot export those records cleanly, your instant payout launch is not really finance-ready.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- docs.stripe.com/payouts/instant-payoutstrusted

- docs.stripe.com/reports/payout-reconciliationtrusted

- ecb.europa.eu/paym/retail/instant_payments/html/index.en.htmltrusted

- ecb.europa.eu/paym/retail/instant_payments/html/instant_pa...trusted

- stripe.com/resources/more/embedded-payments-for-growthtrusted

- stripe.com/pricingtrusted

- support.stripe.com/questions/what-are-instant-payouts-and-who-i...trusted

- support.stripe.com/topics/instant-payoutstrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How International Sellers Should Choose Amazon Marketplace Payout Paths

People often treat international Amazon seller payouts like a settings page. That's the wrong starting point. Your payout setup is an operating choice that shapes who controls FX, how quickly you can launch, and where issues show up after you go live.

How Supply and Demand Dynamics Should Set Your Marketplace Payout Strategy

In a two-sided marketplace, payout strategy is not back-office plumbing. It can shape whether sellers stay active, whether transactions complete reliably, and whether buyers can find supply that is ready to transact.

Host Payout Architecture for Short-Term Rental Platforms

Choose your payout architecture before you pick your next country. The usual break point is where host payments meet local payout-method coverage, identity checks, risk review, and finance close requirements.